Sensitivity of the Eisenberg–Noe clearing vector to individual interbank liabilities.111The views expressed in this work are those of the authors and do not necessarily reflect the views of Norges Bank. This material is based upon work supported by the National Science Foundation under Grant No. 1321794.

Abstract

We quantify the sensitivity of the Eisenberg–Noe clearing vector to estimation errors in the bilateral liabilities of a financial system. The interbank liabilities matrix is a crucial input to the computation of the clearing vector. However, in practice central bankers and regulators must often estimate this matrix because complete information on bilateral liabilities is rarely available. As a result, the clearing vector may suffer from estimation errors in the liabilities matrix. We quantify the clearing vector’s sensitivity to such estimation errors and show that its directional derivatives are, like the clearing vector itself, solutions of fixed point equations. We describe estimation errors utilizing a basis for the space of matrices representing permissible perturbations and derive analytical solutions to the maximal deviations of the Eisenberg–Noe clearing vector. This allows us to compute upper bounds for the worst case perturbations of the clearing vector. Moreover, we quantify the probability of observing clearing vector deviations of a certain magnitude, for uniformly or normally distributed errors in the relative liability matrix.

Applying our methodology to a dataset of European banks, we find that perturbations to the relative liabilities can result in economically sizeable differences that could lead to an underestimation of the risk of contagion.

Our results are a first step towards allowing regulators to quantify errors in their simulations.

Keywords: Systemic risk, model risk, Eisenberg–Noe clearing vector, sensitivity analysis, interbank networks, contagion.

1 Introduction

Some important streams of the literature on contagion in networks has focused on interbank contagion, building on the network model of Eisenberg and Noe (2001). Central banks and regulators have applied the model to study default cascades in their jurisdictions’ banking systems. (Anand et al. (2014), Hałaj and Kok (2015), Boss et al. (2004), Elsinger et al. (2013), Upper (2011), Gai et al. (2011)). Hüser (2015) provides a comprehensive and detailed review of the interbank contagion literature. Hurd (2016) presents a unified mathematical framework for modeling these contagion channels. Recently, the Bank of England has extended this model to analyse solvency contagion in the UK financial system (Bardoscia et al. (2017)). Multiple, extensions of this model have been developed to include effects such as

- •

- •

- •

- •

Moreover, a number of papers analyze the implications of network topology on systemic risk in greater detail. Amini et al. (2016a) derive rigorous asymptotic results for the magnitude of the default cascade in terms of network characteristics and find that institutions that have large connectivity and a high number of “contagious links” contribute most to contagion. Detering et al. (2016) show that if the degree distribution of the network does not have a second moment, local shocks can propagate through the entire network. This is relevant as realistic financial networks typically display a core-periphery structure with inhomogeneous degree distribution (Cont et al. (2013)). Chong and Klüppelberg (2018) characterise the joint default distribution of a financial system for all possible network structures and show how Bayesian network theory can be applied to detect contagious channels.

Regulators have identified the inclusion of such contagion mechanisms in stress tests as a key priority (Basel Committee on Banking Supervision (2015), Anderson (2016)). Furthermore, recent research illustrates that accounting for feedback effects and contagion can change the pass/fail result in stress tests for individual institutions (Cont and Schaanning (2017)).

A key ingredient required to estimate contagion in these models is the so-called liabilities matrix , where is the nominal liability of bank to bank .

Often, the exact bilateral exposures are not known and thus need to be estimated (Hałaj and Kok (2013), Anand et al. (2015), Elsinger et al. (2013), Hałaj and

Kok (2015)).

Despite considerable efforts after the crisis to improve data collection, data gaps have not been closed yet.

Beyond logistical issues like the standardization of reporting formats and the creation of unique and universal institution identifiers, further hurdles remain, such as legal restrictions that limit regulators’ access only to data pertinent to their respective jurisdictions.

Therefore, the estimation of specific bilateral exposures remains an important issue (Langfield et al. (2014), Anand et al. (2015, 2017), Financial Stability Board and International Monetary

Fund (2015)).

The early literature often used entropy maximizing techniques to “fill in the blanks” in the liabilities matrix given the total assets and liabilities of banks (viz. the row and column sums of ).

However, a growing empirical literature has shown that real-world interbank networks look quite different from the homogeneous networks that are obtained with such techniques (Bech and

Atalay (2010), Mistrulli (2011), Cont et al. (2013), Soramäki et al. (2007)).

A recent Bayesian method to estimate the bilateral liabilities, given the total liabilities and potential other prior information, is proposed in Gandy and Veraart (2016) and applied to reconstruct CDS markets in Gandy and

Veraart (2017).

In particular, Mistrulli (2011), Gandy and Veraart (2016) show how wide estimates of systemic risk may fluctuate when estimating contagion on real-world and heterogeneous networks versus uniform networks.

This highlights the pivotal role that the matrix of bilateral exposures plays in quantifying the extent of contagion when computing default cascades.

Beyond the above-mentioned legal hurdles that restrict regulator’s access to data outside their jurisdiction, another important example of uncertainty in the interbank exposures arises due to time gaps between data collection and the run of the stress test: For some regulatory stress tests (e.g. Dodd-Frank stress tests) data is collected annually, which can both give rise to window-dressing behaviour by banks, as well as exposures naturally changing over time. In this case the existence or non-existence of an exposure between two banks will be known, and the uncertainty mainly surrounds its magnitude.

Capponi et al. (2016) studies the effects of the network topology on systemic risk through the use of majorization-based tools.

To the best of our knowledge, Liu and Staum (2010) is so far the only paper that performs a sensitivity analysis of the Eisenberg–Noe model.

Their analysis

focuses on

the sensitivity of the clearing vector with respect to the initial net worth of each bank.

The main contribution of this paper is to perform a detailed sensitivity analysis of the clearing vector with respect to the interbank liabilities in the standard Eisenberg–Noe framework.

To this end, we define directional derivatives of order of the clearing vector with respect to “perturbation matrices,” which quantify the estimation errors in the relative liability matrix.

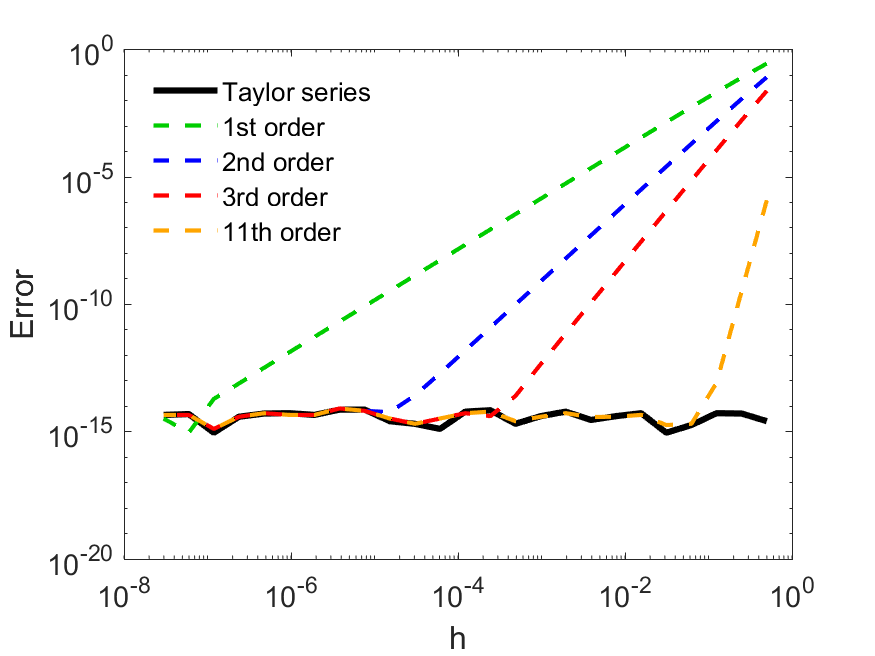

This allows us to derive an exact Taylor series for the clearing vector.

Moreover, we introduce a set of “basis matrices,” which specify a notion of fundamental directions for the directional derivative. We demonstrate that the directional derivative of the clearing vector can be written as a linear combination of these basis matrices.

We proceed to use this result to study two optimisation problems that quantify the maximal deviation of the clearing vector from its “true” value, and obtain explicit solutions for both problems.

These analytical results additionally provide an upper bound to the (first-order) worst case perturbation error. We extend these results by computing the probability of observing deviations of a given magnitude when the estimation errors are either uniformly or normally distributed.

Finally, we illustrate our results both in a small four-bank network and using a dataset of European banks.

Our results suggest that, though the set of defaulting banks may remain stable across different bilateral interbank networks (calibrated to the same data set), the deviation of the clearing vector from perturbations in the relative liabilities can be large.

While our stylized setting ignores other extensions of the Eisenberg–Noe framework (such as bankruptcy costs or fire sales for instance), it provides a first step towards quantifying the sensitivity of the clearing vector to the liabilities matrix, which has not been addressed in the literature before.

In this paper, we occasionally consider external liabilities along with the interbank liabilities. We aggregate all external liabilities into a single external “societal firm.” This additional “bank” is a stand-in for the entirety of the economy that is not included in the financial network. This is discussed in more details in, e.g., Glasserman and

Young (2015). In particular, as utilized in Feinstein et al. (2017), the impact on the wealth of the societal firm can be used as an aggregate measure for the health of the financial network as a whole. We will make use of the societal firm in a similar way in order to study the effects of estimation errors in the interbank liabilities on external stakeholders.

We have limited the literature review mainly to papers that are close to the Eisenberg–Noe methodology. Needless to say, since the financial crisis a vast number of papers have been written on measuring systemic risk, using different approaches such as Agent-Based Modeling (Bookstaber et al. (2014)), Econometry (Brownlees and Engle (2016)), Mean-Field Games (Carmona et al. (2015)) or Economic analysis (Brunnermeier and

Cheridito (2014), Hellwig (2009)).

Axiomatic measures of systemic risk and set-theory approaches have been developed in (Chen et al. (2013), Kromer et al. (2016), Biagini et al. (2015), Feinstein et al. (2017)).

Bisias et al. (2012), Fouque and

Langsam (2013) and Duffie (2010) provide broad overviews of this vast literature.

The organization of the paper is as follows. In Section 2 we present the Eisenberg–Noe framework and

provide initial continuity results of that model. We then study directional derivatives and the Taylor series of the Eisenberg–Noe clearing payments with respect to the relative liabilities matrix. These results allow us to consider the sensitivity of the clearing payments. In Section 3 we use the directional derivatives in order to determine the perturbations to the relative liabilities matrix that present the “worst” errors in terms of misspecification of the clearing payments and impact to society. These results are extended to also consider the probability of the various estimation errors. In Section 4 we implement our sensitivity analysis on data calibrated to a network of European banks. Section 5 concludes with a summary and a discussion of the limitations of our approach. Technical proofs are mostly relegated to the appendix which also provides details on the orthogonal basis of perturbation matrices.

2 Sensitivity analysis of Eisenberg–Noe clearing vector

We consider a financial system consisting of banks, . For , is the nominal liability of bank to bank .222External liabilities can be considered as well through the introduction of an “external” bank . This is discussed in more detail in Section 3.2. Equivalently, is the exposure of bank to bank . is called the liabilities matrix of the financial network, and we assume that no bank has an exposure to itself, i.e., for all . The total liability of bank is given by . The relative liability of bank to bank is denoted , where when . We allow to be arbitrary when and only require .333Note that the arbitrary choice of in the case has no impact on the outcome of the Eisenberg–Noe model since the transpose of the relative liability matrix is multiplied by the incoming payment vector , whose entry is 0 when (cf. (2)). We denote the relative liability matrix . Any relative liability matrix must belong to the set of admissible matrices , defined as the set of all right stochastic matrices with entries in and all diagonal entries 0:

| (1) |

Finally, denote the external assets of bank from outside the banking system by . A bank balance sheet then takes the simplified form of Table 1, and a financial system is given by the triplet .

| Assets | Representation | Liabilities | Representation |

|---|---|---|---|

| Interbank | Interbank | ||

| External | External | ||

| Capital |

A bank is solvent when the sum of its net external assets and performing interbank assets exceeds its total liabilities. In this case, the bank honours all of its obligations. However, if the value of its obligations is greater than the bank’s net assets plus performing interbank assets, then the bank will default and repay its obligations pro-rata. 444This corresponds to the assumption that all interbank and external claims can be aggregated to a single figure per bank and that all creditors of a defaulting bank are paid pari passu. These rules yield a clearing vector as the solution of the fixed point problem

| (2) |

Let be the fixed point function with parameters . As proved in (Eisenberg and Noe 2001, Theorem 2), the clearing vector is unique if a system of banks is regular. Regularity is defined as follows: A surplus set is a set of banks in which no bank in the set has any obligations to a bank outside of the set and the sum over all banks’ external net asset values in the set is positive, i.e., and . Next, consider the financial system as a directed graph in which there is a directed link from bank to bank if . Denote the risk orbit of bank as . This means that the risk orbit of bank is the set of all banks which may be affected by the default of bank . A system is regular if every risk orbit is a surplus set. Uniqueness of the clearing vector has important consequences in terms of the continuity of the function , which in turn is important for our sensitivity analysis. For this reason we will proceed under the assumption that our financial system is regular.

Proposition 2.1.

Consider a regular financial system in which and are fixed. The function , defined via (2), is continuous with respect to .

We finish these preliminary notes by considering a simple example of the Eisenberg–Noe clearing payments under a system of banks. We will return to this example throughout as a simple illustrative case study.

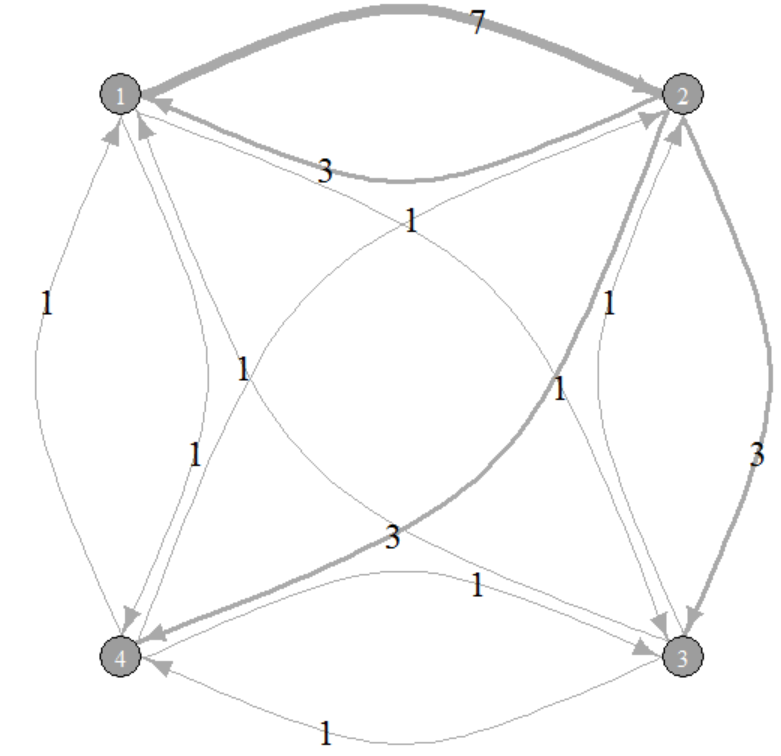

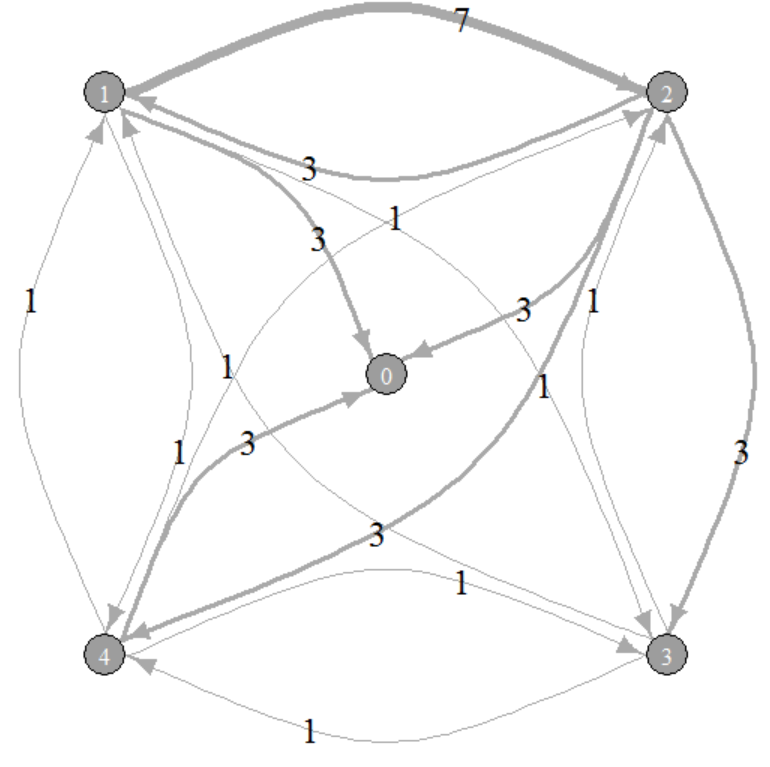

Example 2.2.

Consider the following example of a network consisting of four banks in which the bank’s nominal interbank liabilities are given by

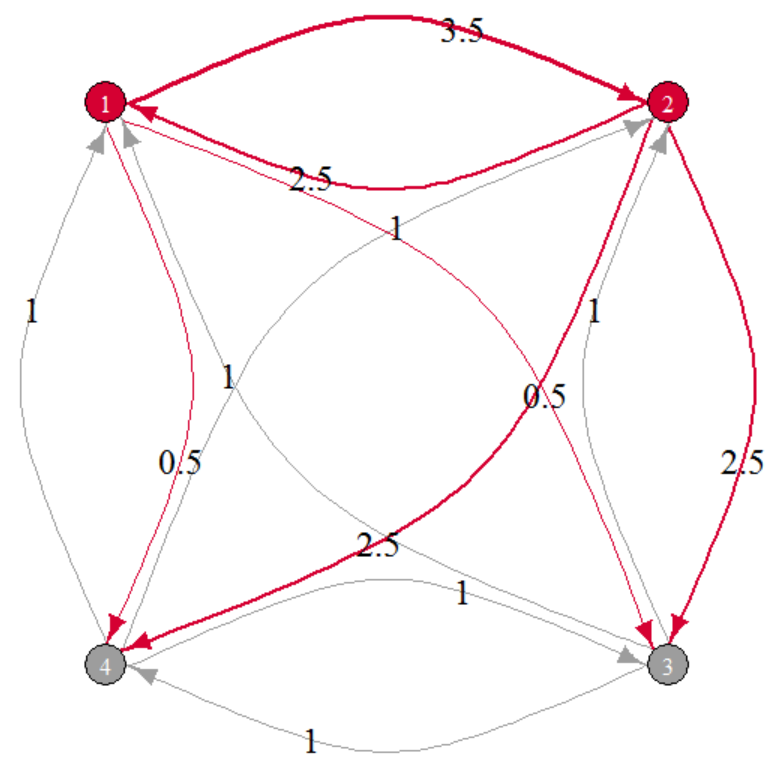

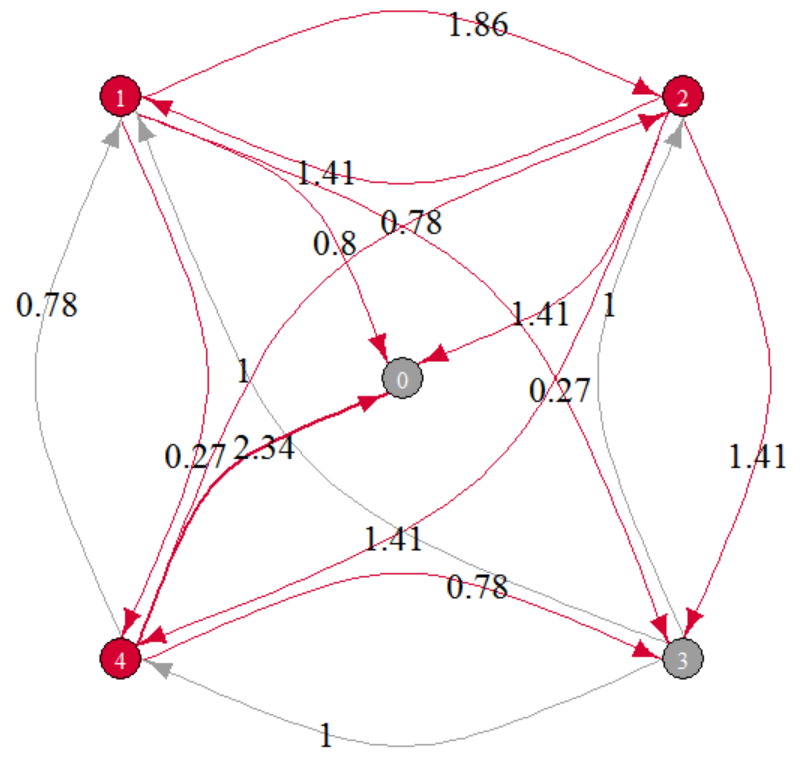

as shown in Figure 1(a). Assume the banks’ external assets are given by the vector . With 0 net worth and positive liabilities, Bank 1 defaults initially. The Eisenberg–Noe clearing vector (2) can be easily computed to be , showing that Bank 2 also defaults through contagion. The realized interbank payments are shown in Figure 1(b). Banks who are in default are colored red and payments that are repaid less than whole are also colored red. The edge widths are proportional to the payment size.

2.1 Quantifying estimation errors from the (relative) liabilities matrices

We assume that some estimation error is attached to the entries of the relative liability matrix, leading to a deviation of the clearing vector from the “true” clearing vector . Denote the true relative liabilities matrix by and let denote the liabilities matrix that includes some estimation error, for a perturbation matrix and size . First we consider the class of perturbation matrices, , under which we assume that the existence or non-existence of a link between two banks is known to the regulator and hence, the error is limited to a misspecification of the size of that link. In practice, this type of uncertainty arises when data is collected at a low frequency, which can lead to exposure evolving naturally, as well as banks trying to improve their balance sheet composition ahead of regulatory reporting dates.555 Evidence for such behaviour at the end of a quarter can, for instance, be seen in the balance sheet reduction of European Banks and the corresponding spikes this creates in the utilization of the Federal Reserve’s Reverse Repo facility, see: http://libertystreeteconomics.newyorkfed.org/2017/08/regulatory-incentives-and-quarter-end-dynamics-in-the-repo-market.html.

Remark 2.9, Corollary 3.2 and Corollary 3.17 will utilize the results in this section to provide bounds for the perturbation error in general without predetermining existence or non-existence of links.

Definition 2.3.

For a fixed , define the set of relative liability perturbation matrices by

The summation conditions ensure that the total liabilities and total assets, respectively, of each bank are left unchanged by the perturbation. Of course it is not possible to have for any . Throughout this work we consider perturbation magnitudes in a bounded interval, , where

for any to assure . We exclude from this calculation of any bank where since this has no impact on the results. It is natural to consider directional derivatives on a unit-ball, whence we focus on the bounded set of perturbations

where is the Frobenius norm, i.e., .

Remark 2.4.

A more general case can be considered in which one allows for errors that create links where there were none or remove connections where there was one. This set is defined as follows: For a fixed ,

We will consider in particular the bounded set of perturbations

Such perturbations thus allow a “rewiring” of the network. In general, allowing edges to be added or deleted increases the potential error in the clearing vector. However, the infinitesimal nature of the sensitivity analysis necessarily restricts the rewiring to the creation of new links; any strictly positive liability cannot be deleted through an infinitesimal perturbation. We discuss this issue in more detail in Corollary 3.2, where we apply our methodology to the complete network, as well as in Figure 11(a), which shows a distribution of payouts to society under a rewiring of the interbank network.

2.2 Directional derivatives of the Eisenberg–Noe clearing vector

Next, we analyse the error when using the clearing vector of a perturbed liability matrix, , instead of the clearing vector of the original liability matrix, , for small perturbations , with .

Definition 2.5.

Let . In the case that the following limit exists, we define the directional derivative of the clearing vector in the direction of a perturbation matrix as

The first order Taylor expansion of about gives

The following theorem provides an explicit formula for the directional derivative of the clearing vector for a fixed financial network.

Theorem 2.6.

Let be a regular financial system. The directional derivative of the clearing vector in the direction of a perturbation matrix exists almost everywhere and is given by

| (3) |

where is the diagonal matrix defined as where

Here, (3) holds outside of the measure-zero set in which some bank is exactly at the brink of default.

The term also appears in Chen et al. (2016), which the authors call the “network multiplier.” This multiplier appears in the dual formulation of the linear program characterising the Eisenberg–Noe clearing vector, where the authors introduce it to study the sensitivities of the clearing vector with respect to the capital (of defaulting banks) and the total liabilities (of non-defaulting banks). The computation of the directional derivative above can be viewed as a generalisation of this result to arbitrary perturbations. The interpretation remains the same in our case: The “network multiplier” describes how an estimation error propagates through the network.

2.3 A Taylor series for the Eisenberg–Noe clearing payments

In the same manner, we can define higher order directional derivatives.

Definition 2.7.

For , we define the order directional derivative of the clearing vector with respect to a perturbation matrix as

| (4) |

when the limit exists, and

Remarkably, as Theorem 2.8 shows, all higher order derivatives also have an explicit formula, which allows us to obtain an exact Taylor series for the clearing vector. We impose an additional assumption on allowable perturbations so that the matrix (as defined in Theorem 2.6) as a function of is fixed with respect to , i.e., we require sufficiently small so that the same subset of banks is in default when the liability matrix is as when the liability matrix is . Let

| (7) | ||||

| (10) | ||||

| (11) |

We necessarily have because we exclude the measure-zero set in which a bank is exactly at the brink of default.

Theorem 2.8.

Let be a regular financial system. Then for , and for all :

| (12) | ||||

where . Moreover, for , the Taylor series

| (13) |

converges and has the following representation

| (14) |

outside of the measure-zero set .

Comparing the directional derivative (3) to the full Taylor series (13) allows us to make the interpretation of the “network multiplier” more precise: The network multiplier captures the first order effect of the error propagation in the final “round” of the fictitious default algorithm. The order effect of the error propagation is captured by the network multiplier raised to the power. Finally, the Taylor series of the fixed-point is the infinite series of these order network multipliers; as this is of a similar form it can be interpreted as the multiplier of the network multiplier.

Remark 2.9.

We can extend the Taylor series expansion results to the more general space of perturbation matrices rather than . Over such a domain the Taylor series (14) is only guaranteed to converge for

as negative perturbations are not feasible.

3 Perturbation errors

In this section we study in detail estimation errors in an Eisenberg–Noe framework, relying on the directional derivatives discussed in the previous section. Specifically we calculate both maximal errors as well as the error distribution assuming a specific distribution of the mis-estimation of the interbank liabilities, notably uniform and Gaussian. We do this first in the original Eisenberg–Noe model, considering the Euclidean norm of the clearing vector as objective. Then we turn to an enhanced model that includes an additional node representing society and study the effect of estimation errors on the payout to society.

3.1 Deviations of the clearing vector

We concentrate first on the -deviation of the actual clearing vector from the estimated one.

3.1.1 Largest shift of the clearing vector

We return to the first order directional derivative to quantify the largest shift of the clearing vector for estimation errors in the relative liability matrix given by perturbations in . Let and assume that for a given . Then, the worst case estimation error under is given as

In order to remove the dependence on and the magnitude of , we consider instead the bounded set of directions and infintesimal perturbations,

In this section, we call the estimation error and the maximal deviation in the clearing vector under . Because appears via a linear term in (3), this allows us to use a basis of perturbation matrices in an elegant way to quantify the deviation of the Eisenberg–Noe clearing vector under the space of perturbations .

Throughout the following results we will take advantage of an orthonormal basis of the space . More details of this space are given in Appendix A.2.

Proposition 3.1.

Let be a regular financial system. The worst case first order estimation error under is given by

| (15) |

for any choice of basis where denotes the spectral norm of a matrix. Furthermore, the largest shift of the clearing vector is achieved by

where are the components of the (normalised) eigenvector corresponding to the maximum eigenvalue of .

Proof.

Note first that any perturbation matrix can be written as a linear combination of basic perturbation matrices, i.e., . Thus,

Immediately this implies, denoting the largest eigenvalue of a matrix by ,

Finally, the independence of the solution from the choice of basis is a direct result of Proposition A.3. ∎

Hence, if the true liability matrix were perturbed in the direction of , this would generate the largest first order estimation error in the clearing vector. By error, we mean the Euclidean distance between the “true” clearing vector in the standard Eisenberg–Noe framework, and the clearing vector under the perturbed liabilities matrix. This is in general not equivalent to the direction that would change the default set most rapidly. Moreover, if regulatory expert judgement allowed to estimate reasonable absolute perturbations, our infinitesimal methodology could be used iteratively in a greedy approach until such an absolute estimation error was reached.

We can use this result on the maximum deviations of the clearing vector under in order to provide bounds of the worst case perturbation error without predetermining the existence or non-existence of links.

Corollary 3.2.

Let be a regular financial system. The worst case first order estimation error under all perturbations is bounded by

| (16) |

for any choice of orthonormal bases as above and of any completely connected network . In the case that itself is a completely connected network then this upper bound is attained.

Proof.

Remark 3.3.

Our empirical analysis suggests that this bound is quite sharp (see Figure 11(b)).

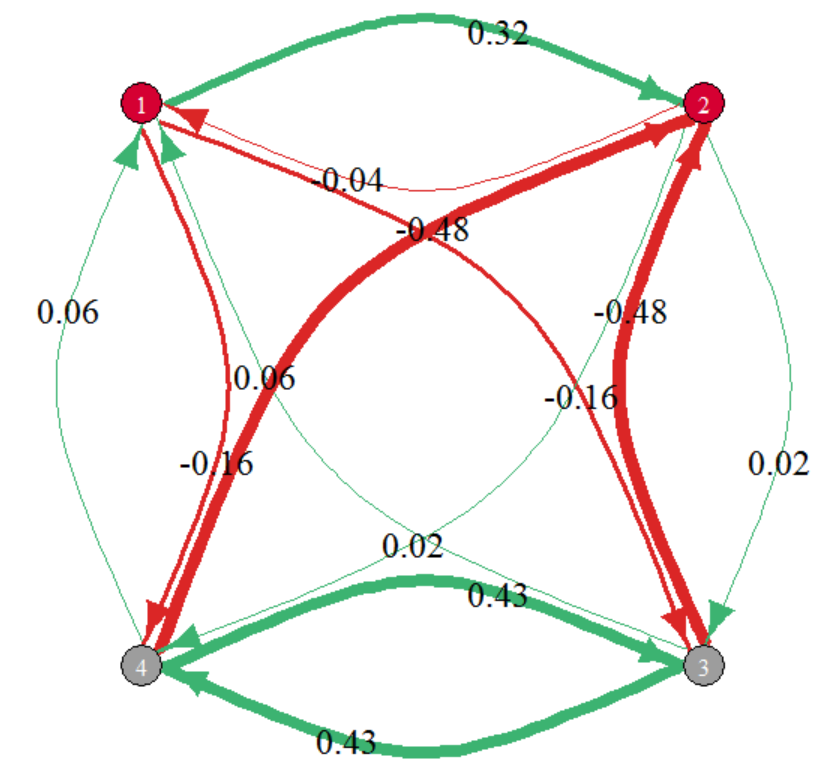

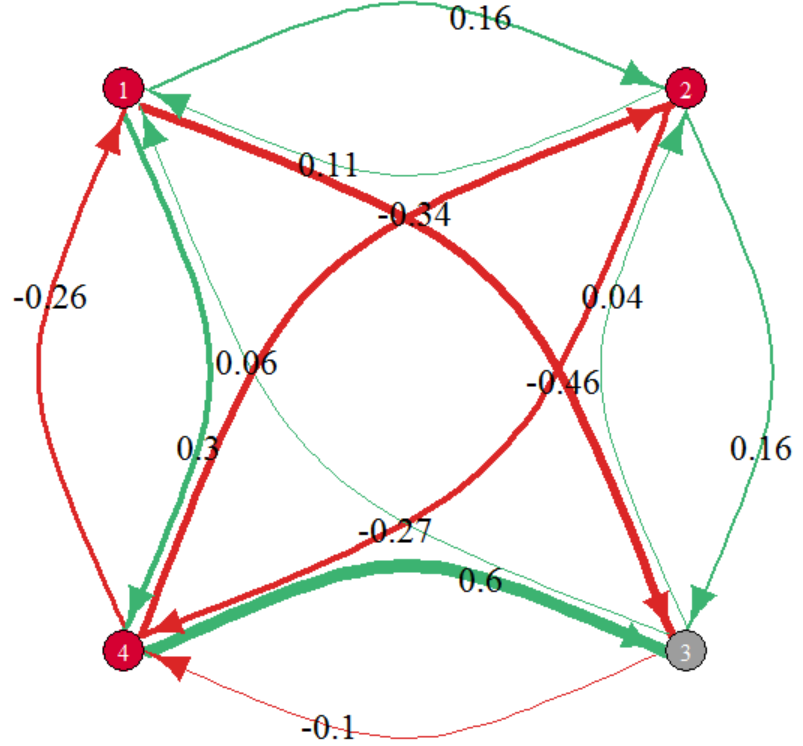

Example 3.4.

We return to Example 2.2 and consider the same toy network consisting of four banks in which each bank’s nominal liabilities are shown in Figure 1(a). The largest shift of the clearing vector (15) under , as described in Proposition 3.1, is given by the matrix

As this network is complete, this is furthermore a solution to both optimization problems (15) and (16) for the worst case perturbation. Additionally, the upper bound in Corollary 3.2 is attained. This perturbation is depicted in Figure 3. As before, banks who are in default are colored red. The edges are labeled with the perturbation of the respective link between banks that achieves this greatest estimation error. The edge linking one node to another is red if the greatest estimation error under the set of perturbations occurs when we have overestimated the value of this link and green if we have underestimated it. Note that due to the symmetry of the optimal estimation error problem, is also optimal and thus the interpretation of red and green links in Figure 3 can be reversed. Indeed, when studying the deviation of the clearing vector, the solutions and are equivalent. When analysing the shortfall of payments to society in Section 3.2, this will be no longer the case. Edge widths are proportional to the absolute value of the entries in . Though our Taylor expansion results (Theorem 2.8) are provided for only, the strict inequality is only necessary if denotes the perturbation size at which a new bank defaults, not when a connection is removed. So when , we obtain

which has the clearing vector

One can immediately verify that has indeed the same total interbank assets and liabilities for each bank, but they are distributed in a different manner. Hence, in this example, there can be a deviation of up to 15% in the relative norm of the clearing vector for a network that is still consistent with the total assets and total liabilities.

Remark 3.5.

It may be desirable to normalize the first order estimation errors by, e.g., the clearing payments or total nominal liabilities, rather than considering the absolute error. In a general form, let denote a normalization matrix (e.g., or ). Then we can extend the results of Proposition 3.1 and Corollary 3.2 by

for any completely connected network . Similarly the distribution results presented below can be generalized by considering in place of .

3.1.2 Clearing vector deviation for uniformly distributed estimation errors

In this section, we will extend the above analysis to the case when estimation errors are uniformly distributed. This is done by considering the linear coefficients for the basis of perturbation matrices to be chosen uniformly on the -dimensional Euclidean unit ball. Then is a perturbation matrix.

Proposition 3.6.

Let be a regular financial system. The distribution of the estimation error when the perturbations are uniformly distributed in the -unit ball is given by

where is the diagonal matrix with elements given by the eigenvalues of for any choice of orthonormal basis , vol denotes the volume operator, and is the gamma function.

Proof.

Let be uniform on the -dimensional unit ball. Then is a perturbation matrix. One obtains

The matrix is diagonalizable because it is real and symmetric. Therefore we can write

where is a diagonal matrix of the eigenvalues and is orthonormal. Combining the above equations, we have

Then since is uniform on the unit ball and , is also uniform on the unit ball and thus we have

As in Proposition 3.1, the independence of the distribution from the choice of basis is a direct result of Proposition A.3. ∎

Remark 3.7.

In the case where or then can explicitly be given by and respectively where is the collection of eigenvalues of . In the case that , the probability can be given via the volume formula provided in Proposition 3.6 as nested integrals,

where and is a reordering of the eigenvalues such that .

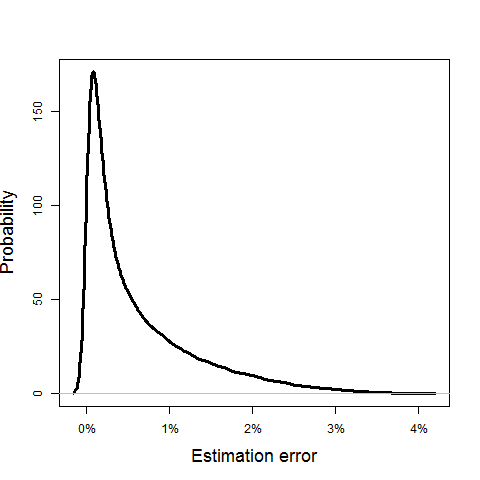

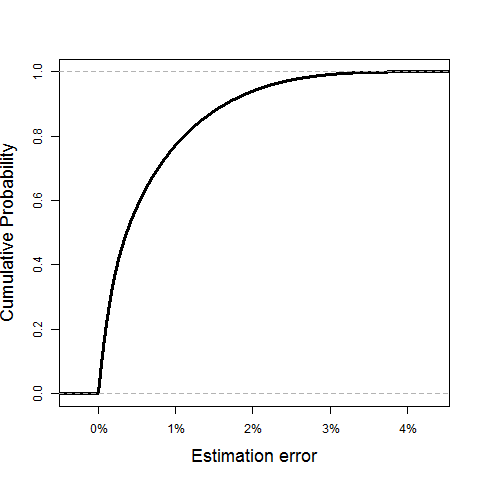

Example 3.8.

We return again to Example 2.2 to consider perturbations sampled from the uniform distribution. Figure 4 shows the density and CDF estimation for the relative estimation error, , corresponding to our stylized four-bank network. The probabilities are estimated from 100,000 simulated uniform perturbations.

3.1.3 Clearing vector deviation for normally distributed estimation errors

We extend our analysis from the previous subsection by considering normally distributed perturbations. To do so, we consider the linear coefficients for the basis of perturbation matrices to be chosen distributed according to the standard -dimensional multivariate standard Gaussian distribution. Then is a perturbation matrix . Though our prior results on the deviations of the clearing payments have been within the unit ball , under a Gaussian distribution the magnitude of the perturbation matrices are no longer bounded by 1 and thus the estimation errors can surpass the worst case errors determined in Proposition 3.1 and Corollary 3.2.

Proposition 3.9.

Let be a regular financial system. The distribution of estimation errors where the perturbations are distributed with respect to the standard normal is given by the moment generating function

where is the diagonal matrix with elements given by the eigenvalues of for any orthonormal basis .

Proof.

Let be a -dimensional standard normal Gaussian random variable. Then is a perturbation matrix. As in Proposition 3.6, we can write

where is the diagonal matrix of eigenvalues of and is orthonormal. Since and , we have . Therefore,

Then and so each component and the ’s are independent. Therefore

The distribution of is , and thus the sum has the moment generating function

where are the eigenvalues of . As in Proposition 3.1, the independence of the distribution from the choice of basis is a direct result of Proposition A.3. ∎

Remark 3.10.

Example 3.11.

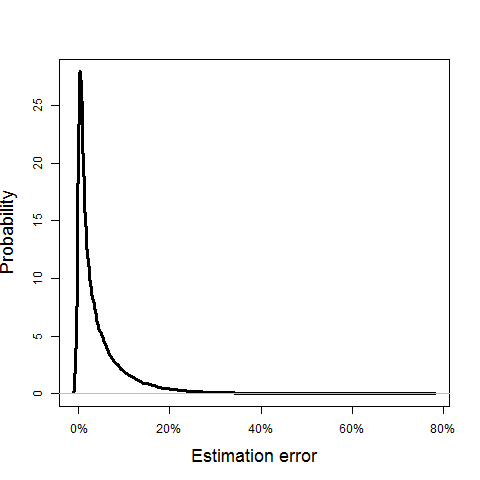

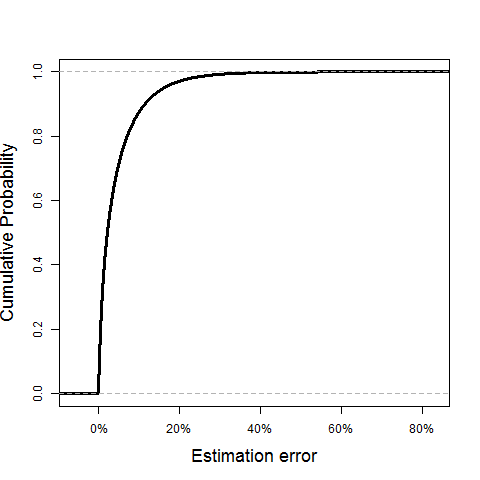

We return again to Example 2.2 to consider perturbations sampled from the standard normal distribution. Figure 5 shows the density and CDF estimation for the relative estimation error, , corresponding to our stylized four-bank network. The probabilities are estimated from 100,000 simulated Gaussian perturbations.

3.2 Impact to the payout to society

In this section, we assume that in addition to their interbank liabilities, banks also have a liability to society. Here, society is used as totum pro parte, encompassing all non-financial counterparties, corporate, individual or governmental. Hence, the set of institutions becomes . Without loss of generality, we assume that all banks owe money to at least one counterparty within the system. Otherwise, a bank who owes no money can be absorbed by the society node as it plays the same role within the model structure. The question of interest is then how the payout to society may be mis-estimated (and in particular overestimated) given estimation errors in the relative liabilities matrix. This setting has been studied in, e.g., Glasserman and Young (2016) with the introduction of outside liabilities. We adopt their framework to analyze this question.

The interbank liability matrix of the previous section is expanded to given by

where is the society liability vector. We require that at least one bank has an obligation to society, i.e., for some . The total liability of bank is now given by . As stated above, we also require that each bank owes to at least one counterparty within the system (possibly society), i.e., for all . The relative liability matrix is transformed accordingly, i.e., and . An admissible relative liability matrix thus belongs to the set of all right stochastic matrices with entries in , all diagonal entries 0, and at least one :

An admissible interbank relative liability matrix thus belongs to the set

which has the same properties as the original interbank relative liability matrix defined in (1), except that row sums are smaller or equal to , with at least one strictly smaller than .

The following result is implicitly used in the subsequent sections. This provides us with the ability to, e.g., consider the directional derivative with respect to the payments made by the financial firms without considering the societal node (which is equal to by assumption).

Proposition 3.12.

If is a regular network then is invertible.

Proof.

This follows immediately from

where and is the vector of default indicators (of length to include the societal node). In particular, since (as shown in the proof of Theorem 2.6), we can conclude that . ∎

Example 3.13.

We include now a society node into our example from Section 2. The nominal interbank liabilities and liabilities from each bank to society are shown in Figure 6(a). Note that at least one bank has an obligation to society and the society does not owe to any bank. As above, the banks’ external assets are given by the vector . The clearing payments, or the amount of its obligations that each bank is able to repay, is given in Figure 6(b). Banks who are in default are colored red, as are the liabilities that are not repaid in full.

3.2.1 Largest reduction in the payout to society

Next, we use the directional derivative in order to quantify how estimation errors, under in the interbank relative liability matrix, could lead to an overestimation of the payout to society. As it turns out, this problem also has an elegant solution using the basis of perturbation matrices discussed in Appendix A.2. We assume that is a regular financial system and additionally that both the relative liabilities to society and the total liabilities are exactly known.

Definition 3.14.

Let be a regular financial system. The payout to society is defined as the quantity where is the clearing vector of the firms.

Herein we consider the relative liabilities matrix to be an estimation of the true relative liabilities. We thus consider the perturbations of the estimated clearing vectors to determine the maximum amount that the payout to society may be overestimated. To study the optimisation problem of minimizing the payout to society, we assume that at least one bank, but not all banks, default. The following proposition shows that this assumption excludes only trivial cases.

Proposition 3.15.

Let be a regular system with the interbank relative liability matrix and . If all banks default, or if no bank defaults, then the payout to society remains unchanged for an arbitrary admissible perturbation .

Proof.

Let be an arbitrary perturbation matrix. We show that in both cases .

-

1.

Assume that no bank defaults. Then , and the result holds as .

-

2.

Assume all banks default. Then . Hence, . Note that , because by definition . Using this and the definitions of and , it follows .

∎

Let and assume that for a given . Then, the minimum payout to society is

In order to remove the dependence on and the magnitude of , we subtract the constant term and consider instead

As in Section 3.1.1, using the basis of perturbation matrices of (see Appendix A.2), we can compute the shortfall to society due to perturbations in the relative liability matrix in .

Proposition 3.16.

Let be a regular financial system. The largest shortfall in payments to society due to estimation errors in the liability matrix in is given by

Furthermore, the largest shortfall to society is achieved by

Additionally, both the largest shortfall and the perturbation matrix that attains that shortfall are independent of the chosen basis .

Proof.

Since the problem

has a linear objective, it is equivalent to

By the necessary Karush–Kuhn–Tucker conditions, we know that any solution to this problem must satisfy

for some . The first condition implies . Plugging this into the second implies that . With two possible solutions we plug these back into the original objective to find that the minimum is attained at for an optimal value of:

Therefore, the solution is

By Proposition A.4, this result is independent of the choice of basis matrices. ∎

Corollary 3.17.

Let be a regular financial system. The worst case shortfall to society is bounded by

where is any orthonormal basis of perturbation matrices of any completely connected network . In the case that itself is a completely connected network then this upper bound is attained.

Proof.

Example 3.18.

We continue the discussion from Example 3.13: The perturbation resulting in the greatest shortfall for the society’s payout, as described in Proposition 3.16, is given by the matrix

This perturbation is depicted in Figure 7. Each edge is labeled with the perturbation of the respective link between banks that achieves this greatest reduction in payout to society. As before, banks who are in default are colored red. The edge linking one node to another is red if the greatest reduction in payout occurs when we have overestimated the value of this link and green if, in the worst case under , we have underestimated the value of this link. Edge widths are proportional to the absolute value of the entries in . In contrast to Example 3.4, note that is not a solution anymore. As this network is complete, this also equals the worst case shortfall of , which is nearly 32% of the entire estimated payment to society.

3.2.2 Shortfall to society for uniformly distributed estimation errors

In this section we compute the reduction in the payout to society when the perturbations are uniformly distributed. To do so, we consider the linear coefficients for the basis of perturbation matrices to be chosen uniformly from the -dimensional Euclidean unit ball. Then is a perturbation matrix.

Proposition 3.19.

Let be a regular financial system. The distribution of changes in payments to society where the perturbations are uniformly distributed on the unit ball is given by

for and 0 for and 1 for . In the above equation, is the standard hypergeometric function. Furthermore, this distribution holds for any choice of basis matrices .

Proof.

Let be a uniform random variable on the unit ball in centered at the origin. Then is a perturbation matrix. Note that by linearity of the directional derivative, we have

where Since is uniform on the unit ball,

| (17) | ||||

| (18) | ||||

where is the regularized incomplete beta function (see, e.g., (DLMF , Chapter 8.17)) and is the standard hypergeometric function (see, e.g., (DLMF , Chapter 15)). Equation (17) follows from considering the probability by taking the ratio of the volume of the fraction of the unit ball satisfying the probability event to the full volume of the unit ball. Equation (18) follows by symmetry of the unit ball and since has unit norm. The penultimate result follows directly from the volume of the spherical cap (see, e.g., (Li 2011, Equation (2))). The final result follows from properties of the regularized incomplete beta function (see, e.g., (DLMF , Chapter 8.17)), i.e.,

with , and noting that the case for positive and negative can be written under the same equation using the standard hypergeometric function. The independence of this result to the choice of orthonormal basis follows as in Proposition 3.16 as the distribution only depends on the basis through the norm . ∎

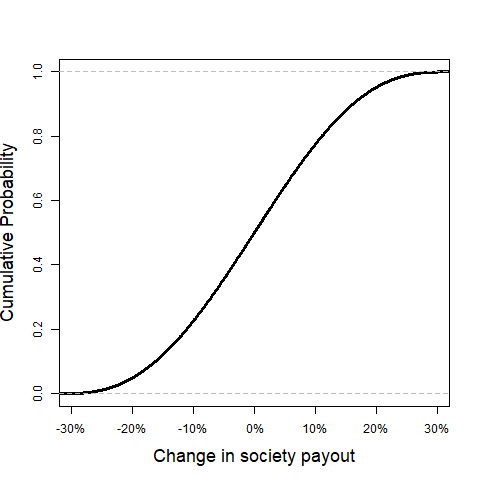

Example 3.20.

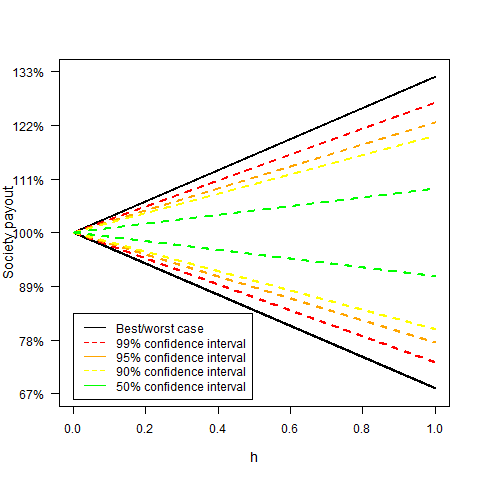

We return to Example 3.13 and consider perturbations sampled from the uniform distribution. The left and right panels of Figure 8 show the density and the CDF respectively for the relative reduction in society payout under uniformly distributed errors in our stylized four-bank network. Figure 9(a) shows both the largest reduction and increase in the payout to society as well as various confidence intervals for the change in the payout as a function of the perturbation size, . As and depend on the choice of perturbation matrix , we present the confidence intervals on an extrapolated interval for .

3.2.3 Shortfall to society for normally distributed estimation errors

We will now consider the same problem as above under the assumptions that the errors follow a standard normal distribution. As in Section 3.1.3, we note that the magnitude of the perturbations is no longer bounded by 1 in this setting.

Proposition 3.21.

Let be a regular financial system. The distribution of changes to payments to society where the perturbations follow a multivariate standard normal distribution is given by

Furthermore, this distribution holds for any choice of basis matrices .

Proof.

Let be a -dimensional standard normal Gaussian random variable. The result follows immediately by linearity and affine transformations of the multivariate Gaussian distribution. The independence of this result to the choice of orthonormal basis follows as in Proposition 3.16 as the distribution only depends on the basis through the norm . ∎

Example 3.22.

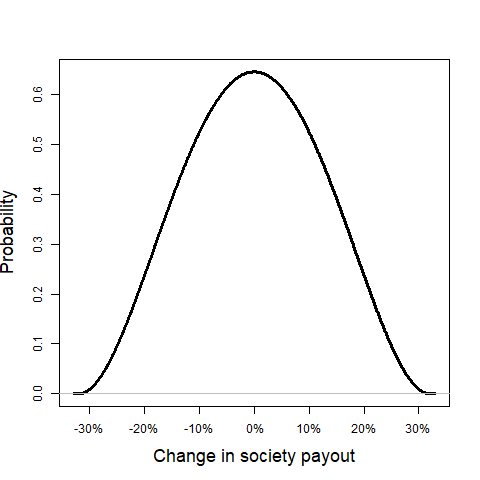

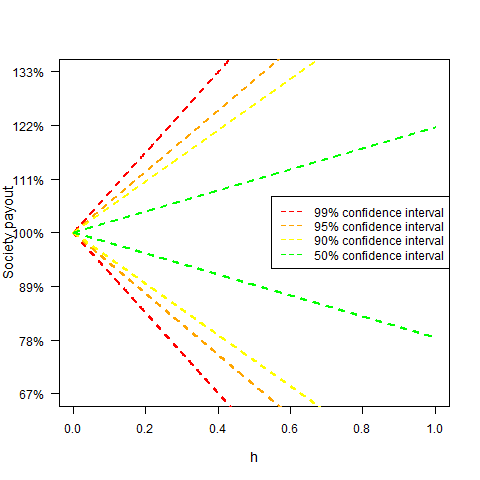

We return once more to Example 3.13 to consider perturbations sampled from the standard normal distribution. Figure 9(b) shows various confidence intervals for the relative change in payout to society under normally distributed errors under , as a function of the perturbation size, . As and depend on the choice of perturbation matrix we present the confidence intervals on an extrapolated interval for .

4 Empirical application: assessing the robustness of systemic risk analyses

In this section, we study the robustness of conclusions that can be drawn from systemic risk studies that use the Eisenberg–Noe algorithm to model direct contagion. We use the same dataset from 2011 of European banks from the European Banking Authority that has been used in previous studies relying on the Eisenberg–Noe framework (Gandy and Veraart (2016), Chen et al. (2016)). As in these papers, given the heuristic approach to the dataset, our exercise should be considered to be an illustration of our results and methodology, rather than a realistic full-fledged empirical analysis.

With respect to the model’s data requirements, the EBA dataset only provides information on the total assets , the capital and a proxy for interbank exposures, . To populate the remaining key variables of the Eisenberg–Noe model, we therefore first assume, as in Chen et al. (2016), that for each bank the interbank liabilities are equal to the interbank assets. Furthermore, we assume that all non-interbank assets are external assets, and the non-interbank liabilities are liabilities to a society sink-node. Hence,

Consequently, the Eisenberg–Noe model variables are

Note that each bank’s net worth hence exactly corresponds to the book value of equity, or the banks’ capitals: .

The final key ingredient to the model is the (relative) liabilities matrix. This is usually highly confidential data, and is not provided in the EBA data set. In Gandy and Veraart (2016), Gandy and Veraart propose an elegant Bayesian sampling methodology to generate individual interbank liabilities, given information on the total interbank liabilities and total interbank assets of each bank. The authors have developed an -package called “systemicrisk” that implements a Gibbs sampler to generate samples from this conditional distribution. As our analysis requires an initial liability matrix, we use the European Banking Authority (EBA) data as input to their code in order to generate such a liability matrix. As suggested by (Gandy and Veraart 2016, Section 5.3), we perturb the interbank liabilities slightly (such that they are not exactly equal to the interbank assets, while keeping the total sums equal) to fulfill the condition that be connected along rows and columns. We then run their algorithm, with parameters , to create one realisation of a 87 87 network of banks from the data. (We needed to exclude banks DE029, LU45 and SI058 because the mapping of the data to the model as described above created violations of the conditions for the algorithm and resulted in an error message.)

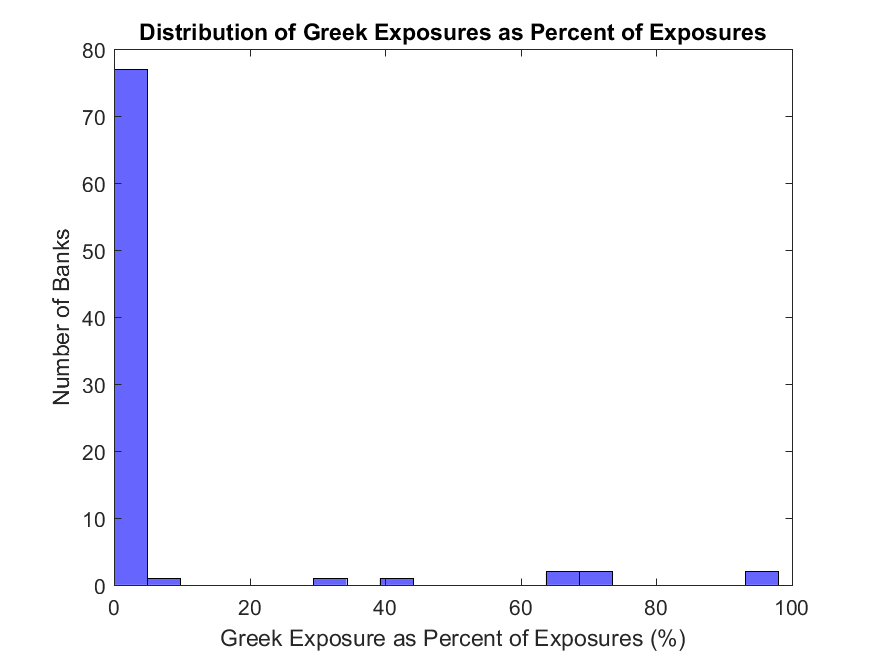

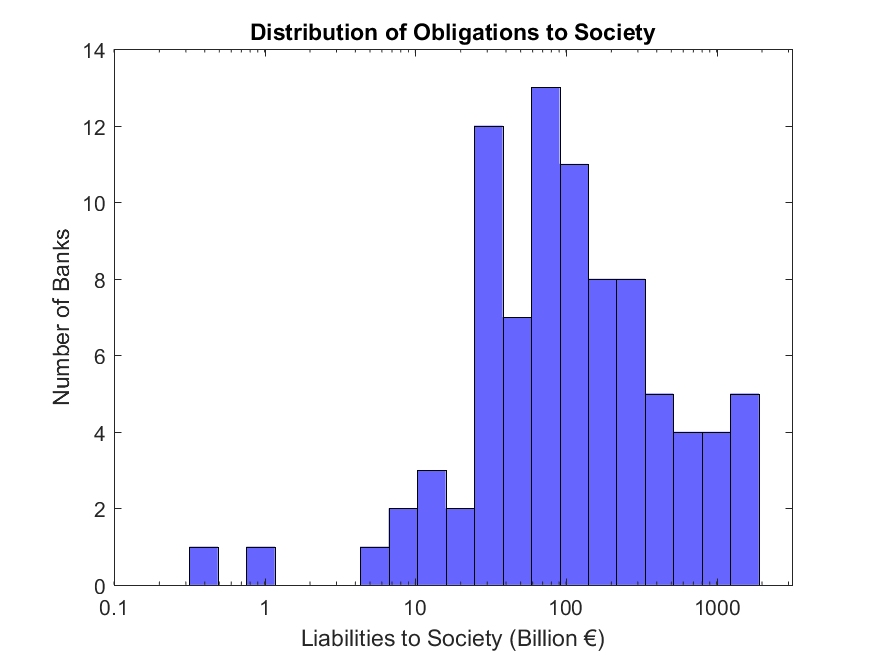

For simplicity and to consider an extreme event that would trigger a systemic crisis in the European banking system, we analyze what might have happened if Greece had defaulted on its debt and exited the Eurozone. We study this shock by decreasing the external assets of each bank by its individual Greek exposures, i.e. setting Greek bond values to zero. The histogram of Greek exposures (as a percentage of total exposures), displayed in Figure 10(a), shows a large heterogeneity of exposures, with the majority of banks having no (or negligible) exposures to Greece, but a small number of Greek banks having substantial exposures to Greece (between 64% - 96% of total assets). In our sensitivity analysis we resample the underlying liabilities matrix from the Gandy & Veraart algorithm Gandy and Veraart (2016) 1000 times.

In each of our 1000 simulated networks considered there were 9 specific institutions that default on their debts in the Eisenberg–Noe framework; in only 3 simulated networks (0.3% of all simulations) there were between 1 and 3 additional banks that fail. As such, the traditional analysis of sensitivity of the Eisenberg–Noe framework would conclude that this contagion model is robust to errors in the relative liabilities matrix. This is consistent with the work of, e.g., Glasserman and Young (2015).

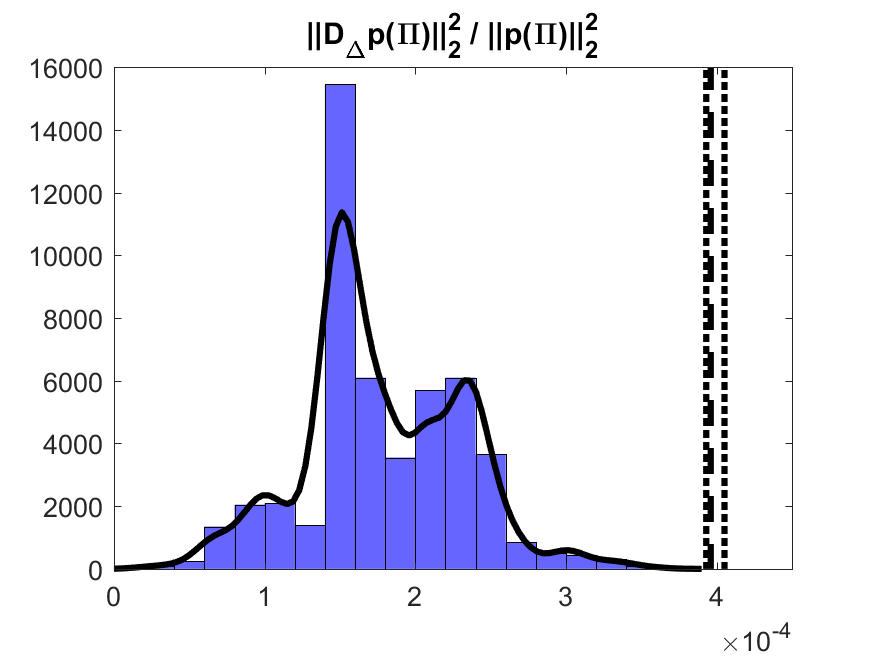

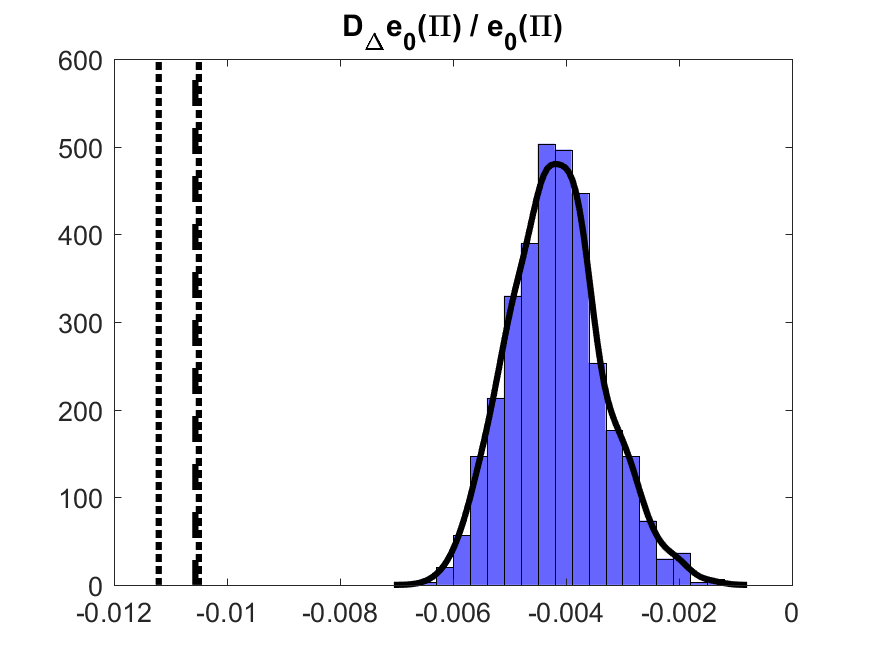

However, we now consider the maximal deviation in both the estimation errors and the payments to society in each of our 1000 simulated networks under . The societal obligations are the same in all 1000 simulated networks, and their histogram, depicted in Figure 10(b), reveals as for the Greek exposures, considerable heterogeneity. Figure 11(a) depicts the empirical density of the maximal deviation estimation errors for . Figure 11(b) depicts the empirical density of maximal fractional shortfalls to society . We also depict the upper bound of the worst case perturbation errors for each of the 1000 simulated networks.

Notably in Figure 11(a) we see that the shape of the network, calibrated to the same EBA data set, can vastly change the impact that the worst case estimation error has under perturbations in . In this plot of the empirical densities, we see the range of normalized worst case first order estimation errors range from 0 to nearly . That is a 0 to 2% normed deviation of the clearing payments (while the value of itself has only minor variations: a total range of under 27 million EUR compared to its norm of near 5 trillion EUR for the different simulated networks ). The upper bound on these perturbation errors (for the norm rather than norm squared) is approximately 2%, and as can be seen in Figure 11(a), the range of obtained upper bounds is very small. This indicates that such a bound is rather insensitive to the initial relative liability matrix . Therefore any such computed upper bound is of value to a regulator, even if the initial estimate of the relative liabilities is incorrect.

When we consider instead Figure 11(b) we see that the density is more bell shaped, again with a large variation from the least change (roughly ) to the most change (roughly ) in the normalized impact to society; this proves as with Figure 11(a) that the underlying network can provide large differences in the apparent stability of a simulation to validation. While these values may appear small, the arises from normalising the deviation of the clearing vector with the value of the societal node but still amounts to a variation on the order of 23.2 - 162.4 billion EUR. Thus this sensitivity is as if entire banks’ assets vanished from the wealth of society. The upper bound of these perturbation errors is approximately twice as high as the obtained maximal deviations computed under . Notably, the median upper bound of the worst case error is nearly equal to the minimum possible value, though with a skinny tail reaching off to greater errors.

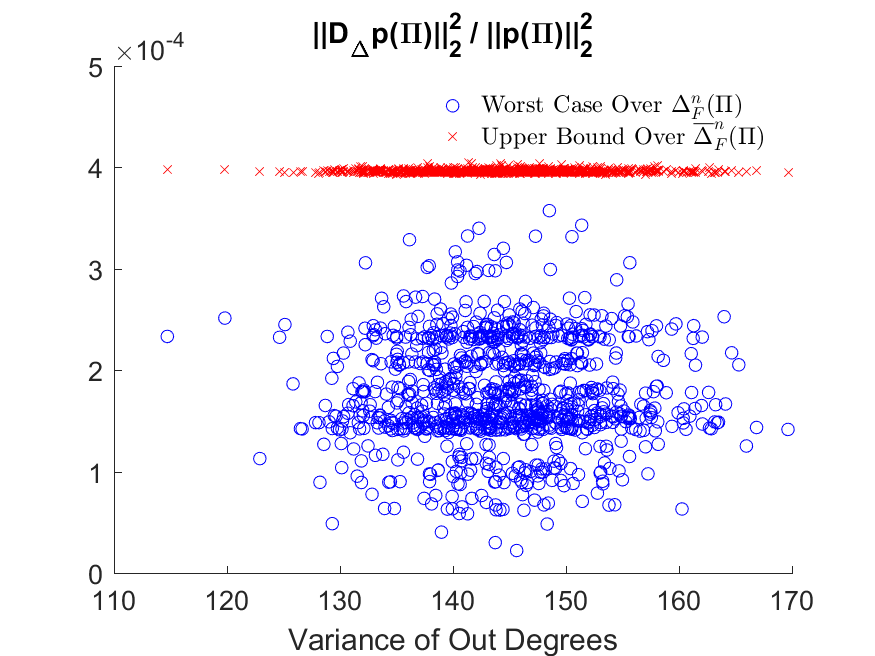

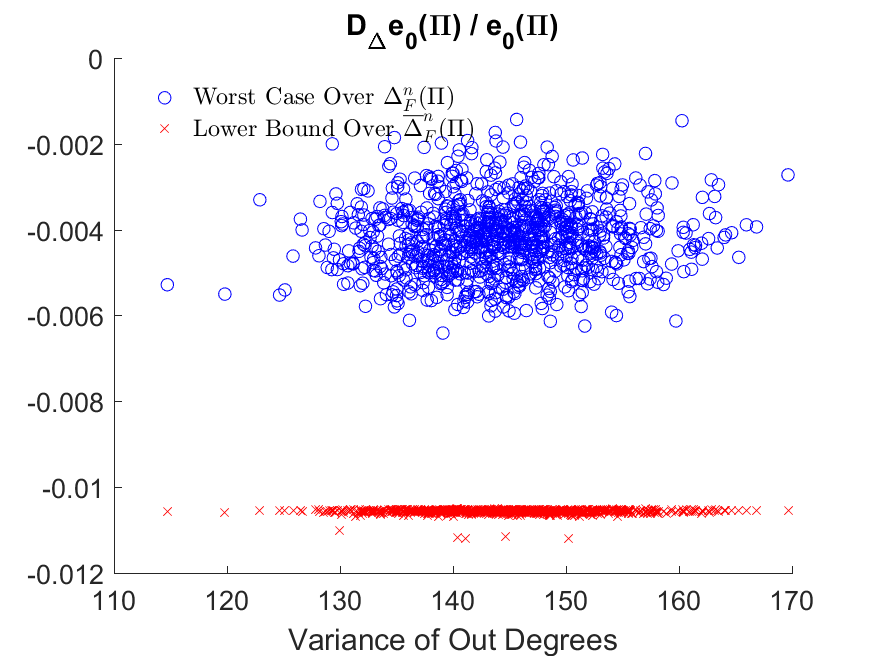

Finally, Figures 11(c) and 11(d) analyze the impact of network heterogeneity on the perturbation of the clearing vector. To this end, we quantify “network heterogeneity” as the variance of the degree distribution of out-edges. It varies between 110 to 170 in the 1000 simulated networks, thus displaying a reasonable level of heterogeneity. Figure 11(c) shows the worst case relative error over (blue circles) and (red crosses) respectively. Similarly, Figure 11(d) shows a scatter plot of the relative error of the payment to society against the variance of the degree distribution in the network. Neither figure seems to suggest a clear relation between the relative errors and the network heterogeneity. Note that Figures 11(a) and 11(b) are obtained by projecting all points onto the -axis in Figures 11(c) and 11(d).

5 Conclusion

In this paper we analyse the sensitivity of clearing payments in the standard Eisenberg–Noe framework to misspecification or estimation errors in the relative liabilities matrix. We accomplish this by determining the directional derivative of the clearing payments with respect to the relative liabilities matrix. We extend this result to consider the full Taylor expansion of the fixed points to determine the clearing payments as a closed-form perturbation of an initial solution.

We further study worst case and probabilistic interpretations of our perturbation analysis. In this simple setting, our results provide an upper bound on the largest shift for the clearing vector as well as a lower bound for the shortfall to society. In a numerical case study of the European banking system, we demonstrate that, even when the set of defaulting firms remains constant, the clearing payments and wealth of society can be greatly impacted. This is true even in the case that the existence and non-existence of links is pre-specified. When the existence and non-existence of links is unknown, then the upper bound of the errors can be utilized which generally provides errors that are significantly less sensitive to the initial estimate of the relative liabilities and roughly twice as large as the errors under pre-specification of links.

Our sensitivity analysis is based on the standard Eisenberg–Noe model. As such, it omits a number of other important extensions that have been developed in the literature (such as bankruptcy costs, fire sales, or the impact of the network topology). For a full quantification of risk and uncertainty, future research will therefore need to develop a model that combines – and weighs – all of these relevant channels of contagion. Nevertheless, our results provide a first step towards quantifying the impact of estimation errors in the interbank liability matrix and thereby improving tools for systemic risk analysis.

6 Acknowledgements

The collaboration leading to this article was initiated at the AMS Mathematics Research Community 2015 in Financial Mathematics, supported by the National Science Foundation, Division of Mathematical Sciences, under Grant No. 1321794. Eric Schaanning’s PhD studies were kindly funded by the Fonds National de la Recherche Luxembourg under its AFR PhD grant scheme.

References

- Amini et al. (2016a) Amini H, Cont R, Minca A (2016a) Resilience to contagion in financial networks. Mathematical finance 26(2):329–365.

- Amini et al. (2016b) Amini H, Filipović D, Minca A (2016b) Systemic risk with central counterparty clearing. Swiss Finance Institute Research Paper No. 13-34, Swiss Finance Institute, URL https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2275376.

- Amini et al. (2016c) Amini H, Filipović D, Minca A (2016c) Uniqueness of equilibrium in a payment system with liquidation costs. Operations Research Letters 44(1):1–5, URL https://doi.org/10.1016/j.orl.2015.10.005.

- Anand et al. (2014) Anand K, Bédard-Pagé G, Traclet V (2014) Stress testing the Canadian banking system: A system-wide approach. Bank of Canada Financial Stability Review URL http://www.bankofcanada.ca/wp-content/uploads/2014/06/fsr-june2014-anand.pdf.

- Anand et al. (2015) Anand K, Craig B, von Peter G (2015) Filling in the blanks: network structure and interbank contagion. Quantitative Finance 15(4):625–636, URL https://doi.org/10.1080/14697688.2014.968195.

- Anand et al. (2017) Anand K, van Lelyveld I, Ádám Banai, Friedrich S, Garratt R, Hałaj G, Fique J, Hansen I, Jaramillo SM, Lee H, Molina-Borboa JL, Nobili S, Rajan S, Salakhova D, Silva TC, Silvestri L, de Souza SRS (2017) The missing links: A global study on uncovering financial network structures from partial data. Journal of Financial Stability ISSN 1572-3089, URL http://dx.doi.org/10.1016/j.jfs.2017.05.012.

- Anderson (2016) Anderson RW (2016) Stress testing and macroprudential regulation: A transatlantic assessment. Systemic Risk Center, Financial Markets Group & CEPR Press URL http://voxeu.org/sites/default/files/Stress_testing_eBook.pdf.

- Banerjee et al. (2018) Banerjee T, Bernstein A, Feinstein Z (2018) Dynamic clearing and contagion in financial networks. Working Paper URL https://arxiv.org/abs/1801.02091.

- Bardoscia et al. (2017) Bardoscia M, Barucca P, Brinley Codd A, Hill J (2017) The decline of solvency contagion risk. Bank of England Staff Working Paper 662, URL http://www.bankofengland.co.uk/research/Documents/workingpapers/2017/swp662.pdf.

- Basel Committee on Banking Supervision (2015) Basel Committee on Banking Supervision (2015) Making supervisory stress tests more macroprudential: Considering liquidity and solvency interactions and systemic risk. BIS Working Paper 29, URL http://www.bis.org/bcbs/publ/wp29.pdf.

- Bech and Atalay (2010) Bech ML, Atalay E (2010) The topology of the federal funds market. Physica A: Statistical Mechanics and its Applications 389(22):5223 – 5246, URL https://doi.org/10.1016/j.physa.2010.05.058.

- Biagini et al. (2015) Biagini F, Fouque JP, Frittelli M, Meyer-Brandis T (2015) A unified approach to systemic risk measures via acceptance sets. Mathematical Finance .

- Bisias et al. (2012) Bisias D, Flood M, Lo AW, Valavanis S (2012) A survey of systemic risk analytics. Annual Review of Financial Economics 4(1):255–296, URL https://doi.org/10.1146/annurev-financial-110311-101754.

- Bookstaber et al. (2014) Bookstaber R, Paddrik M, Tivnan B (2014) An agent-based model for financial vulnerability. Office for Financial Research Working Paper URL https://www.financialresearch.gov/working-papers/files/OFRwp2014-05_BookstaberPaddrikTivnan_Agent-basedModelforFinancialVulnerability_revised.pdf.

- Boss et al. (2004) Boss M, Elsinger H, Summer M, Thurner S (2004) Network topology of the interbank market. Quantitative Finance 4(6):677–684, URL https://doi.org/10.1080/14697680400020325.

- Brownlees and Engle (2016) Brownlees C, Engle RF (2016) Srisk: A conditional capital shortfall measure of systemic risk. Review of Financial Studies URL https://doi.org/10.1093/rfs/hhw060.

- Brunnermeier and Cheridito (2014) Brunnermeier M, Cheridito P (2014) Measuring and allocating systemic risk .

- Capponi and Chen (2015) Capponi A, Chen PC (2015) Systemic risk mitigation in financial networks. Journal of Economic Dynamics & Control 58:152–166, URL https://doi.org/10.1016/j.jedc.2015.06.008.

- Capponi et al. (2016) Capponi A, Chen PC, Yao DD (2016) Liability concentration and systemic losses in financial networks. Operations Research 64(5):1121–1134, URL https://doi.org/10.1287/opre.2015.1402.

- Carmona et al. (2015) Carmona R, Fouque JP, Sun LH (2015) Mean field games and systemic risk. Communications in Mathematical Sciences (4):911 – 933, URL http://www.pstat.ucsb.edu/faculty/fouque/PubliFM/Carmona-Fouque-Sun-George70-revised-1-28-14.pdf.

- Chen et al. (2013) Chen C, Iyengar G, Moallemi CC (2013) An axiomatic approach to systemic risk. Management Science 59(6):1373–1388, URL https://doi.org/10.1287/mnsc.1120.1631.

- Chen et al. (2016) Chen N, Liu X, Yao DD (2016) An optimization view of financial systemic risk modeling: Network effect and market liquidity effect. Operations Research 64(5):1089–1108, URL https://doi.org/10.1287/opre.2016.1497.

- Chong and Klüppelberg (2018) Chong C, Klüppelberg C (2018) Contagion in financial systems: A Bayesian network approach. SIAM Journal on Financial Mathematics 9(1):28–53.

- Cifuentes et al. (2005) Cifuentes R, Ferrucci G, Shin HS (2005) Liquidity risk and contagion. Journal of the European Economic Association 3(2-3):556–566, URL https://doi.org/10.1162/jeea.2005.3.2-3.556.

- Cont et al. (2013) Cont R, Moussa A, Santos EB (2013) Network structure and systemic risk in banking systems. Handbook on Systemic Risk, 327 – 368 (Cambridge University Press), URL https://doi.org/10.1017/CBO9781139151184.018.

- Cont and Schaanning (2017) Cont R, Schaanning E (2017) Fire sales, indirect contragion and systemic stress testing. Norges Bank Working Paper 02/2017, URL https://ssrn.com/abstract=2541114.

- Detering et al. (2016) Detering N, Meyer-Brandis T, Panagiotou K, Ritter D (2016) Managing default contagion in inhomogeneous financial networks. arXiv preprint arXiv:1610.09542 .

- Di Gangi et al. (2015) Di Gangi D, Lillo F, Pirino D (2015) Assessing systemic risk due to fire sales spillover through maximum entropy network reconstruction. Working Paper URL http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2639178.

- (29) DLMF (2017) NIST Digital Library of Mathematical Functions. http://dlmf.nist.gov/, Release 1.0.15 of 2017-06-01, URL http://dlmf.nist.gov/, f. W. J. Olver, A. B. Olde Daalhuis, D. W. Lozier, B. I. Schneider, R. F. Boisvert, C. W. Clark, B. R. Miller and B. V. Saunders, eds.

- Duffie (2010) Duffie D (2010) How Big Banks Fail and What to Do About It? (Princeton University Press).

- Eisenberg and Noe (2001) Eisenberg L, Noe TH (2001) Systemic risk in financial systems. Management Science 47(2):236–249, URL https://doi.org/10.1287/mnsc.47.2.236.9835.

- Elliott et al. (2014) Elliott M, Golub B, Jackson MO (2014) Financial networks and contagion. American Economic Review 104(10):3115–53, URL https://doi.org/10.1257/aer.104.10.3115.

- Elsinger (2009) Elsinger H (2009) Financial networks, cross holdings, and limited liability. Österreichische Nationalbank (Austrian Central Bank) Working Paper 156, URL https://www.oenb.at/dam/jcr:b2f1721c-7af9-4646-9568-d93faec67bac/wp156_tcm16-138413.pdf.

- Elsinger et al. (2013) Elsinger H, Lehar A, Summer M (2013) Network models and systemic risk assessment. Handbook on Systemic Risk, 287 – 305, URL https://doi.org/10.1017/CBO9781139151184.016.

- Feinstein (2017a) Feinstein Z (2017a) Financial contagion and asset liquidation strategies. Operations Research Letters 45(2):109–114, URL https://doi.org/10.1016/j.orl.2017.01.004.

- Feinstein (2017b) Feinstein Z (2017b) Obligations with physical delivery in a multi-layered financial network. Working Paper URL https://arxiv.org/abs/1702.07936.

- Feinstein and El-Masri (2017) Feinstein Z, El-Masri F (2017) The effects of leverage requirements and fire sales on financial contagion via asset liquidation strategies in financial networks. Statistics & Risk Modeling URL http://dx.doi.org/10.1515/strm-2015-0030.

- Feinstein et al. (2017) Feinstein Z, Rudloff B, Weber S (2017) Measures of systemic risk. SIAM Journal on Financial Mathematics to appear, URL https://arxiv.org/pdf/1502.07961v5.pdf.

- Financial Stability Board and International Monetary Fund (2015) Financial Stability Board, International Monetary Fund (2015) The financial crisis and information gaps - sixth progress report on the implementation of the G-20 data gaps initiative URL http://www.imf.org/external/np/g20/pdf/2015/6thprogressrep.pdf.

- Fouque and Langsam (2013) Fouque JP, Langsam JA, eds. (2013) Handbook on Systemic Risk (Cambridge University Press), ISBN 9781139151184, URL https://doi.org/10.1017/CBO9781139151184, cambridge Books Online.

- Gai et al. (2011) Gai P, Haldane A, Kapadia S (2011) Complexity, concentration and contagion. Journal of Monetary Economics 58(5):453–470, URL https://doi.org/10.1016/j.jmoneco.2011.05.005.

- Gai and Kapadia (2010) Gai P, Kapadia S (2010) Contagion in financial networks. Bank of England Working Papers 383, Bank of England, URL https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1577043.

- Gandy and Veraart (2016) Gandy A, Veraart LAM (2016) A Bayesian methodology for systemic risk assessment in financial networks. Management Science URL https://doi.org/10.1287/mnsc.2016.2546.

- Gandy and Veraart (2017) Gandy A, Veraart LAM (2017) Adjustable network reconstruction with applications to CDS exposures. Working Paper URL https://ssrn.com/abstract=2895754.

- Gentle (2007) Gentle JE (2007) Matrix Algebra (Springer-Verlag New York), ISBN 978-0-387-70872-0.

- Glasserman and Young (2016) Glasserman P, Young H (2016) Contagion in financial networks. Journal of Economic Literature to appear, URL http://dx.doi.org/10.1257/jel.20151228.

- Glasserman and Young (2015) Glasserman P, Young HP (2015) How likely is contagion in financial networks? Journal of Banking and Finance 50:383–399, URL https://doi.org/10.1016/j.jbankfin.2014.02.006.

- Hałaj and Kok (2013) Hałaj G, Kok C (2013) Assessing interbank contagion using simulated networks. Computational Management Science 10(2-3):157–186, URL https://doi.org/10.1007/s10287-013-0168-4.

- Hałaj and Kok (2015) Hałaj G, Kok C (2015) Modelling the emergence of the interbank networks. Quantitative Finance 15(4):653–671, URL http://dx.doi.org/10.1080/14697688.2014.968357.

- Hellwig (2009) Hellwig MF (2009) Systemic Risk in the Financial Sector: An Analysis of the Subprime-Mortgage Financial Crisis. De Economist 157(2):129–207, URL https://doi.org/10.1007/s10645-009-9110-0.

- Hurd (2016) Hurd TR (2016) Contagion! Systemic Risk in Financial Networks (Springer).

- Hüser (2015) Hüser AC (2015) Too interconnected to fail: A survey of the interbank networks literature. Journal of Network Theory in Finance 1(3):1–50, URL https://doi.org/10.21314/JNTF.2015.001.

- Kromer et al. (2016) Kromer E, Overbeck L, Zilch K (2016) Systemic risk measures on general measurable spaces. Mathematical Methods of Operations Research 84(2):323–357.

- Kusnetsov and Veraart (2016) Kusnetsov M, Veraart LAM (2016) Interbank clearing in financial networks with multiple maturities. Working Paper URL https://ssrn.com/abstract=2854733.

- Langfield et al. (2014) Langfield S, Liu Z, Ota T (2014) Mapping the UK interbank system. Journal of Banking and Finance 45:288–303, URL http://dx.doi.org/10.1016/j.jbankfin.2014.03.031.

- Li (2011) Li S (2011) Concise formulas for the area and volume of a hyperspherical cap. Asian Journal of Mathematics and Statistics 4(1):66–70, URL http://dx.doi.org/10.3923/ajms.2011.66.70.

- Liu and Staum (2010) Liu M, Staum J (2010) Sensitivity analysis of the Eisenberg and Noe model of contagion. Operations Research Letters 38(5):489–491, URL https://doi.org/10.1016/j.orl.2010.07.007.

- Mathai (1982) Mathai AM (1982) Storage capacity of a dam with gamma type inputs. Annals of the Institute of Statistical Mathematics 34(1):591–597, URL https://doi.org/10.1007/BF02481056.

- Meyer (2000) Meyer CD (2000) Matrix Analysis and Applied Linear Algebra (SIAM), ISBN 978-0-898714-54-8.

- Mistrulli (2011) Mistrulli PE (2011) Assessing financial contagion in the interbank market: Maximum entropy versus observed interbank lending patterns. Journal of Banking and Finance 35(5):1114 – 1127, URL https://doi.org/10.1016/j.jbankfin.2010.09.018.

- Nier et al. (2007) Nier E, Yang J, Yorulmazer T, Alentorn A (2007) Network models and financial stability. Journal of Economic Dynamics and Control 31(6):2033–2060, URL https://doi.org/10.1016/j.jedc.2007.01.014.

- Ren et al. (2014) Ren X, Yuan GX, Jiang L (2014) The framework of systemic risk related to contagion, recovery rate and capital requirement in an interbank network. Journal of Financial Engineering 1(1):1450004, URL https://doi.org/10.1142/S2345768614500044.

- Rogers and Veraart (2013) Rogers LCG, Veraart LAM (2013) Failure and rescue in an interbank network. Management Science 59(4):882–898, URL https://doi.org/10.1287/mnsc.1120.1569.

- Soramäki et al. (2007) Soramäki K, Bech ML, Arnold J, Glass RJ, Beyeler WE (2007) The topology of interbank payment flows. Physica A: Statistical Mechanics and its Applications 379(1):317–333, URL https://doi.org/10.1016/j.physa.2006.11.093.

- Upper (2011) Upper C (2011) Simulation methods to assess the danger of contagion in interbank markets. Journal of Financial Stability 7(3):111–125, URL https://doi.org/10.1016/j.jfs.2010.12.001.

- Weber and Weske (2017) Weber S, Weske K (2017) The joint impact of bankruptcy costs, fire sales and cross-holdings on systemic risk in financial networks. Probability, Uncertainty and Quantitative Risk 2(1):9, URL https://doi.org/10.1186/s41546-017-0020-9.

Appendix A Appendix

A.1 Proofs

Proof of Proposition 2.1

Proof.

This proof follows the logic of (Feinstein et al. 2017, Lemma 5.2) and (Ren et al. 2014, Theorem 4). Fix the net assets and total obligation . Let be the function defined by , where

The function is jointly continuous with respect to the payment vector and the relative liabilities for . Because the system is regular and thus has a unique fixed point, it follows from (Feinstein et al. 2017, Proposition A.2) that the graph

is closed. Define the projection as . By (Feinstein et al. 2017, Proposition A.3), is a closed mapping in the product topology. Then, in order to show that is continuous, take closed. Then

The graph of is closed and is closed by definition. Hence is closed and the function is continuous with respect to . ∎

Proof of Theorem 2.6

We note that our proof does not assume a priori that the clearing vector is differentiable; we comment on this simpler case below.

Proof.

We assume that the net external assets lie in the set

Denote and . By continuity of with respect to (Proposition 2.1) we have for all , as and thus , and . To prove the existence of , we will show that the following two limits,

are equal for each component. Consider the upper limit

for some function .

Similarly, we get

Hence, both and are fixed points of the same mapping . Assuming that this fixed point problem has a unique solution it follows

for all . Therefore, under this assumption, is well defined and it is the solution to the fixed point equation

Next, we proceed to show that is invertible, which establishes uniqueness of the fixed point and the directional derivative (3) to conclude the proof.

First, assume that is irreducible, i.e., the graph with adjacency matrix has directed paths in both directions between any two vertices . Then by the Perron–Frobenius Theorem (see, e.g., (Gentle 2007, Section 8.7.2)), has an eigenvector corresponding to eigenvalue , where is the spectral radius of a matrix. As eigenvectors are only unique up to a multiplicative constant, we may assume . Under the assumption of a regular system, at least one bank must be solvent, i.e., there exists some such that . This implies that there exists a column such that the column sum of is strictly less than 1. In fact, any insolvent institution with obligations to bank will have column sum of strictly less than 1. If all banks are solvent, is the zero matrix and the result is trivial. Thus there is some matrix , so that each column sum of is 1, i.e.

Note that the column sums of are at most 1 since each row sum of is 1. Therefore the spectral radius of must be less than or equal to . Moreover, we must have . Otherwise, , which along with the scaling of the eigenvector so that implies

as by the definition of eigenvalues. Therefore, we can conclude that, in the case is irreducible, .

Now suppose that is reducible, i.e., is similar to a block upper triangular matrix , with irreducible diagonal blocks , for some . Under the assumption of a regular system, each has at least one column whose sum is strictly less than 1. As in the preceding case, this implies that for each and therefore

Since the maximal eigenvalue of is strictly less than 1, 0 cannot be an eigenvalue of . This suffices to show that is invertible. ∎

Remark A.1.

If one assumes that is differentiable with respect to the relative liabilities , the result of Theorem 2.6 can be obtained directly from implicit differentiation of the representation

Proof of Theorem 2.8

Proof.

We prove the result by induction. Theorem 2.6 shows the result for . We now assume that equation (12) holds for and we proceed to show that it holds for . As in Theorem 2.6, we show the existence of (4) by computing the two limits:

The first order Taylor approximation for matrix inverses gives by the differentiation rules for the matrix inverse (cf. (Gentle 2007, p. 152)) for and small enough: . Applying this fact with and , we have

Additionally, we note that the order derivative, similarly to all lower order derivatives, is continuous with respect to the relative liabilities matrix since (by assumption of the induction) , where and are both continuous with respect to (see Proposition 2.1 and the continuity of the matrix inverse). Consider now the upper limit

Similarly, we obtain . The existence of the limit and the result (12) follow for all .

With the above results on all order directional derivatives, we now consider the full Taylor expansion. First, by the definition of given in (11), is fixed for . By the definition of the clearing payments (given in (2)) and defaulting firms (defined in Theorem 2.6), along with the fact that is invertible (as shown in the proof of Theorem 2.6 since remains a regular system by ), we have

| (19) | ||||

Similarly we find that

| (20) |

By combining (19) and (20), we immediately find

Additionally, we can show that

directly by

Therefore, for any , we find

i.e., (14).

Now let us consider the perturbations of size within the neighbourhood

We will employ the following property of matrix inverses (see (Meyer 2000, p. 126)): If so that exists and , then

We take and . Since by the assumption that , we have

using a property of the spectral radius (see (Meyer 2000, p. 617)). Thus, by combining this result with (19), we have

The penultimate equality above follows directly from (20). The last equality follows directly from the definition of the order directional derivatives proven above. Thus we have shown the full Taylor expansion is exact on .

Finally, since we have already shown that (14) is exact for any and

is singular for at least one of the elements by construction, it must follow that . That is, .

∎

A.2 An orthonormal basis for perturbation matrices

We construct here an orthonormal basis for the matrices in . To fix ideas, consider the case , where the general form of a matrix for a fully connected network can be written as

from which it is clear that there are degrees of freedom. It is easy to see that in general one has degrees of freedom. In the case , two such basis elements and are given by

In general we note that is a closed, convex polyhedral set; we will take advantage of this fact in order to generate a general method for constructing basis matrices for , as follows:

-

1.

Define

to be a vectorised version of .

-

2.

Construct a matrix so that . Note that the total degrees of freedom for (and therefore also for ) is given by the rank of the matrix . We include enough rows in the matrix in order to ensure that the row sums and (weighted) column sums are 0 and that components of are equal to zero based on .

-

3.

An orthonormal basis of can be found by generating the orthonormal basis of the null space of .

-

4.

Finally our basis matrices can be generated by reshaping the basis of the null space of by setting for any and .

Definition A.2.

The set

is an orthonormal basis of perturbation matrices for the relative liability matrix . Additionally, the vector

is a vector of basis directional derivatives for the relative liability matrix .

We define two matrices to be orthogonal when their vectorised forms are orthogonal in , and note that, by construction, any matrix in the basis of perturbation matrices has unit Frobenius norm.

Proposition A.3.

Let . Then the set of eigenvalues of is the same for any choice of orthonormal basis of perturbation matrices . Additionally, if is the eigenvector corresponding to eigenvalue and basis , then is independent of the choice of basis.

Proof.

Let be the vectorised version of and let be a different orthonormal basis. By linearity of the directional derivative (see Theorem 2.6) we can immediately state that for some matrix . Let be an eigenvalue and eigenvector pair for the operator and let such that . We will show that is an eigenvalue and eigenvector pair for and thus the proof is complete:

The last equality follows from the fact that is the unique projection matrix onto . ∎

Proposition A.4.

Let . Then is independent of the choice of orthonormal basis of perturbation matrices and for any fixed vector .