Vector-Valued Multivariate Conditional Value-at-Risk

Abstract

In this study, we propose a new definition of multivariate conditional value-at-risk (MCVaR) as a set of vectors for discrete probability spaces. We explore the properties of the vector-valued MCVaR (VMCVaR) and show the advantages of VMCVaR over the existing definitions given for continuous random variables when adapted to the discrete case.

1 Introduction

Conditional value-at-risk (CVaR) is a widely used tool, especially in financial optimization, for assessing the risk associated with a certain decision. The value of CVaR at an uncertainty level is the expected outcome given that it is unfavorable compared to at least 100% of the possible realizations. The threshold value corresponds to the -quantile, which is also known as the value-at-risk (VaR). VaR is a suitable risk measure for the cases where the aim is to avoid unfavorable outcomes with high probability. However, it does not measure the magnitude of the unfavorable outcomes. To address this, CVaR has been introduced to quantify the expected value of the undesired outcomes as well as computing the VaR as a by-product [16].

CVaR is first introduced as a risk measure for univariate random variables. Due to its desirable properties such as coherence and law invariance, CVaR is widely incorporated into optimization problems to minimize or limit the risk of the corresponding decisions (see e.g., [16], [17], [7]). However, in many real life problems, decision makers are interested in measuring the risk arising from multiple factors rather than a single outcome. One way of extending the univariate definitions of VaR and CVaR to the multivariate case is to use a scalarization vector for turning the random outcome vector into a scalar. However, the relative importance of criteria is usually ambiguous. The weights of criteria with respect to each other are not always quantifiable as a unique vector, as they may be subject to conflicting opinions of a group of decision makers. To address this, recent work considers a robust approach, where the set of possible scalarization vectors is assumed to be known and often assumed to be polyhedral or convex, and a worst-case scalarization vector in this set is used to scalarize the multivariate random vector [11, 10, 8, 12, 13]. These papers not only define the concept of polyhedral multivariate CVaR for finite discrete distributions, but also give optimization models and solution methods when the multivariate random outcome vector is a function of the decisions. For computability of these risk measures, the solution methods rely on sampling from the true distribution. In this context, it is natural to consider finite discrete distributions, described with a finite number of scenarios. In this paper, instead of a scalarized real-valued representation of the multivariate CVaR, we introduce a vector-valued risk measure without the need for the specification of an ambiguity set describing the possible weights.

The first challenge in defining a multivariate CVaR is the determination of the -quantile (multivariate VaR). While the -quantile corresponds to a single real value in the univariate setting, -quantile of a random vector may point to several vectors in the multivariate context. There are several studies addressing this issue. Prékopa [14] proposes a multivariate definition of VaR as a set of vectors, called -Level Efficient Points (LEPs), rather than a single value for arbitrary multivariate distributions. Cousin and Di Bernardino [3] propose an alternative approach for the continuous distribution case that computes a single vector as the expectation of the boundary surface of the multivariate quantile function. Torres et al. [18], on the other hand, introduce a direction parameter and compute the multivariate VaR vector in that direction. Di Bernardino et al. [6] and Adrian and Brunnermeier [1] also provide single, vector-valued definitions of multivariate VaR by conditioning on the information on certain criteria. As in the univariate case, these multivariate VaR definitions are only concerned with the probability of having favorable outcomes, and not the magnitude of the unfavorable outcomes.

The second challenge in defining a multivariate CVaR is related with the ambiguity in the characterization of undesirable outcomes in the multivariate case. Lee and Prékopa [9] provide a single and real-valued definition of multivariate CVaR that classifies a vector as undesirable if it is not better than or equivalent to any LEP as defined in [14]. Cousin and Di Bernardino [4] propose a single, vector-valued CVaR definition such that realizations worse than at least one LEP with respect to every criteria are assumed to be undesirable. The details of these studies providing a definition for multivariate will be discussed in Section 3.

This study is dedicated to defining a vector-valued multivariate CVaR that specifically targets discrete random variables without characterizing a set that describes the relative importance of criteria in advance. Throughout the paper, smaller values of random variables as well as smaller values of risk measures are assumed to be preferable. We propose a new definition for multivariate CVaR and explore its properties in Section 2. In Section 3, we review the existing definitions, and demonstrate their shortcomings in the case of finite discrete distributions. We show that our new definition overcomes these problems, which leads to a unified context for multivariate CVaR.

2 Multivariate CVaR

We use the multivariate VaR definition in [14] as the -quantile function for our multivariate CVaR definition. Prékopa [14] defines multivariate VaR using LEPs for the discrete distribution case.

Definition 2.1 (Prékopa [14])

Let be a random vector and its c.d.f. The vector is a LEP (or a -efficient point) of the distribution of , if and there is no such that .

In the multivariate context, there may be several vectors (LEPs) satisfying the above conditions. Hence corresponds to the set of such vectors. Dentcheva et al. [5] show that the set is finite in the case that has a finite discrete distribution. The problem of finding elements of can be seen as the following multi-objective optimization problem:

| (1a) | ||||

| (1b) | ||||

The elements in correspond to the Pareto efficient points of problem (1) with joint chance constraints. There is no polynomial-time algorithm to solve (1) unless P=NP. Prékopa [15] reviews several algorithms to enumerate the exponential set . As mentioned earlier, concerns the -quantile of the multivariate risk only. To measure the magnitude of the risk associated with the % worst outcomes of multiple risk factors, a multivariate analogue of CVaR is needed.

Next, we propose a new definition for multivariate CVaR as a set of vectors, each associated with a LEP in . In our definition, outcomes exceeding a LEP in at least one criterion are considered as undesirable with respect to that LEP.

Definition 2.2 (Vector-Valued Multivariate Conditional Value-at-Risk)

Assume that is a random vector with a set of LEPs at confidence level . The vector-valued multivariate CVaR of at level , denoted as is defined as,

| (2) |

where

and for all .

The operator in Definition 2.2 ensures that an element of is non-dominated by another element in this set, i.e., the elements of form an efficient frontier. (In the context that smaller values are preferable, a vector is non-dominated by a vector if for some . In addition, dominates if for all .) Note that if is a univariate random variable with a finite discrete distribution, then there is a unique element for , hence the Min operator is not needed. To see why this operator is needed in the multivariate case, we provide an example next.

Example 2.1

Let be a bivariate random vector with support such that each realization is equally likely. At confidence level , . Using this information, we compute , and . Clearly, , hence we let .

The definition of VMCVaR is analogous to the univariate definition of CVaR for a univariate random variable given by

Suppose that follows a finite discrete distribution. In other words, there is a finite number of scenarios, , where represents the realization of under scenario with probability . Then an equivalent representation of univariate CVaR is given by a linear program (LP)

| (3) |

It is well known that at an optimal solution to this LP, . Now we consider an analogous representation of . Let be the realization of under scenario with probability for . Then,

| (4a) | ||||

| s.t. | (4b) | |||

or equivalently

| (5a) | ||||

| s.t. | (5b) | |||

| (5c) | ||||

| (5d) | ||||

| (5e) | ||||

| (5f) | ||||

Here is in the set , if under scenario we have and is a large enough number so that constraint (5e) is trivially satisfied if . The complexity of the multivariate CVaR definition is evident from comparing the formulations for the univariate and multivariate case; the former is an LP (3), whereas the latter is a multiobjective mixed-integer program (5) or a chance-constrained program (4). However, the main difficulty lies at identifying the MVaR values. Once these are identified, say using the methods reviewed in [15], calculating for each is polynomial in the number of scenarios, .

In the next proposition, we provide a more intuitive definition of for the case that .

Proposition 2.1

For a random variable and such that , the following equality holds,

| (6) |

where denotes a component-wise relation such that for at least one , and represents a vector whose component is equal to .

Proof.

For a criterion , the component of is equal to,

∎

This is also analogous to the univariate definition of CVaR since for a univariate random variable such that ,

| (7) |

The proposed multivariate risk measure should satisfy some desired properties to be a useful tool for evaluating the risk of random vectors. Artzner et al. [2] axiomatize the desired properties of univariate risk measures under the coherence concept. A coherent univariate risk measure is normalized, positively homogeneous, translation equivariant, monotone and subadditive. The risk measure of interest in this study, , is a mapping from a -dimensional random vector to a set of -dimensional vectors. Hence, we aim to prove an analogous form of these properties for set-valued multivariate risk measures. Note that for two random vectors, and , of the same finite probability space, means that for each scenario and criterion .

Proposition 2.2

For a -dimensional random vector , satisfies the following properties,

-

(i)

Normalized:

-

(ii)

Positively homogeneous: for .

-

(iii)

Translation equivariant: for .

-

(iv)

Monotone:

Proof.

It can be easily seen that is normalized. We will prove the remaining properties using the fact that for all , for some .

-

(ii)

From [9], we know if , then for . Hence,

-

(iii)

Lee and Prékopa [9] show that for when . Using this,

-

(iv)

By the monotonicity property of MVaR given in [9], implies that for all there exists such that and there is no such that for some . Consider the set of undesirable scenarios for , denoted by partitioned into two subsets: , and . Using this definition,

(8) (9) (10) (11) where equality (8) follows from the definition of sets ; inequality (9) follows from the fact that for , ; inequality (10) follows from the facts that for (here is taken as ); and inequality (10) follows from the fact that and .

∎

Note that Lee and Prékopa [9] show that the properties in Proposition 2.2 hold for their definition of MCVaR (we will give this definition in detail in Section 3). While we use the same definition of MVaR as [9], our definition of MCVaR is different, hence the need to prove these properties for our definition. Lee and Prékopa [9] also show that a multivariate analogue of the subadditivity property, which is included in the coherence definition of univariate risk measures, is not satisfied by their MCVaR definition. We consider this property next.

Remark 2.1

Risk measure does not satisfy the following analogue of the subadditivity property:

Proof.

Consider the following counterexample. Let and be bivariate random vectors with supports

such that each realization is equally likely. At confidence level , , and . Using this information, we compute , and . It can be seen that , hence subadditivity property is violated. ∎

In addition to coherence, from definition (3), it is clear that in the univariate case, CVaR is a conservative approximation of VaR, as for a univariate random variable . Analogously, it is expected that the multivariate CVaR value should not dominate its corresponding LEP, i.e., we should not have for any for a random vector . By definition (2), clearly satisfies this property. In the next section, we show that this may not be the case for some existing definitions of multivariate CVaR.

3 Comparison to Existing Definitions

In this section, we briefly review other multivariate CVaR definitions from the literature and compare them with the proposed definition of MCVaR.

Prékopa [15] utilizes the definition of MVaR given in Definition 2.1 as a basis for their multivariate CVaR definition. Using the definition of , they assume an outcome to be desirable if

| (12) |

and undesirable if

where is the complement of set . These definitions imply that an event is undesirable if it is not better than or equivalent to any element in . Here, we assume that set includes the zero vector along the same lines with the univariate definition of . Assume that the set of desirable outcomes, defined in the right-hand-side of (12), is denoted as . The set represents the closure of its complement, which is the set of undesirable outcomes.

Definition 3.1 (Prékopa [15])

The Multivariate Conditional Value-at-Risk of the random vector at confidence level , denoted by , is defined as

where is a -variate function such that exists.

In particular, the function in [15] is defined as where and . This scalarization function is consistent with the weighted sum approach commonly applied in multicriteria optimization, where is interpreted as the relative weight of criterion . Using the expansion on conditional probability, we know that

and consequently we obtain,

Assuming that the probability of is negligible, this equation can be used to estimate the value of . This assumption is quite natural in case of continuous distributions. For discrete probability distributions, it provides an approximation.

A shortcoming of this definition is that fails to determine the risk associated with an outcome vector at any level in some discrete cases, which we describe next.

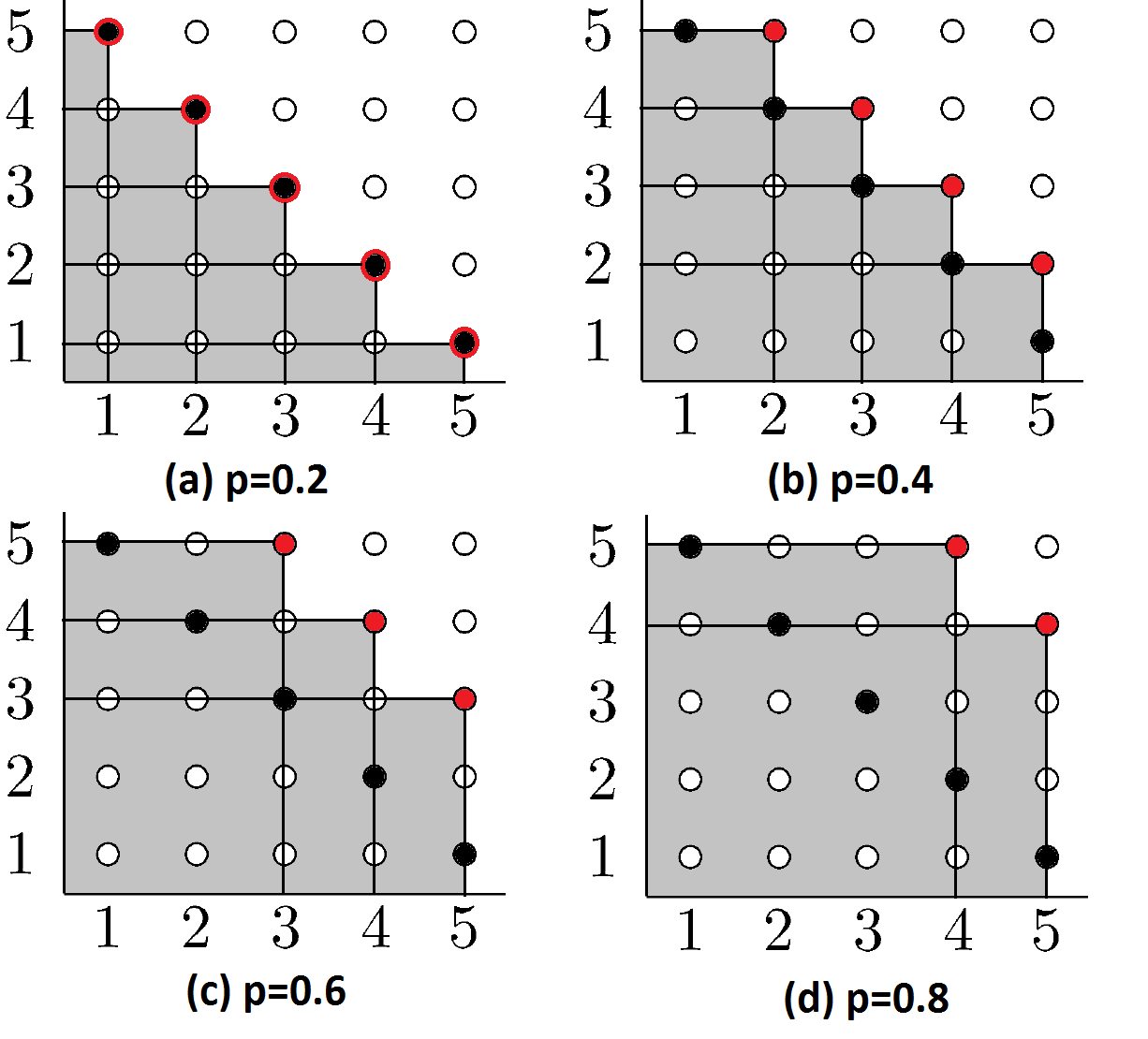

Example 3.1

Consider bivariate random variable with support

All realizations are assumed to have equal probability, 0.2. For different values of , the set of desirable outcomes is depicted in Figure 1 as the gray shaded areas. The black and red points represent the realizations and LEPs of , respectively. As it can be seen, all possible realizations of are desirable for each possible value . Consequently, is undefined at any level .

Another problem is the possibility of obtaining an value that is preferable to for some . Consider the following example.

Example 3.2

Let be a bivariate random variable with support

such that and all the other realizations are equally likely. At confidence level , we obtain . For LEP (4,4), the realizations (1,5) and (5,1) are undesirable. The value corresponding to this LEP is , which is smaller than , for any increasing function including the linear function proposed in [15].

To the best of our knowledge, the only vector-valued alternative to the of Prékopa [15] for defining multivariate CVaR is proposed by Cousin and Di Bernardino [4] under the name lower-orthant conditional tail expectation (CTE).

Definition 3.2 (Cousin and Di Bernardino [4])

For a given random vector with distribution function at level , the lower-orthant conditional tail expectation is defined as

| (13) |

This definition includes only the outcomes dominated by or equal to a LEP in the computation of multivariate CVaR, whereas the of Prékopa [15] considers the outcomes worse than all LEPs in at least one criterion. A possible issue with this definition is that it may potentially lead to a conservative set of undesirable outcomes and consequently cases in which the risk measure is undefined. For instance, the set of undesirable outcomes in Example 3.1 based on this definition is empty for all confidence levels. Our proposed definition remedies this issue, because the values exceeding the -quantile in not all but some of the criteria are also considered as undesirable in the VMCVaR definition.

Next we compare these risk measures with the proposed definition of MCVaR for the simple case of a random variable with a single LEP. Assume that we are given a random vector such that is the only LEP of at uncertainty level , i.e. . By doing so, we ensure that all multivariate CVaR definitions correspond to a single vector and hence they can be compared. Furthermore, we consider the vector-valued adaptation of , denoted by , where we replace the scalarization function in Definition 3.1 with the vector . In particular, we define

| (14) |

as the expected vector value of undesirable outcomes as defined in [15]. As explained previously, this may result in a multivariate CVaR value that dominates . The following results would also hold for the case that all measures are scalarized using the same vector.

We represent definition (13) equivalently as,

Note that in the following discussion, when the set has a single element in it, we refer to that element as , as well.

Proposition 3.1

For a given random vector such that , , and for all , where are possible realizations of with probabilities , the following relations hold,

when and are well-defined for .

Proof.

Note that the conditions of the proposition ensure that the risk measures are comparable. We consider the case that all risk measures are well-defined for (recall that and may not be defined in some cases). Since defined in (14) takes the expectation of while takes the expectation of (see Proposition 2.1) and the condition in given in Proposition 2.1 is more restrictive, we have . To show that , we represent equivalently as,

The first terms in both definitions are the same except for the conditions, conditions on the realizations with , while conditions on the realizations with ). Hence the claim follows.

∎

In summary, we propose a new definition of a vector-valued multivariate CVaR that is consistent with its univariate counterpart. We compare this definition with alternative vector-valued definitions, and show its advantages. However, we recognize the computational difficulties involved with obtaining this vector, especially when used in an optimization setting. In this case, we believe that the scalarization approaches in [11, 10, 8, 12, 13] provide a practical and reasonable estimation of the multivariate risk.

Acknowledgment

Simge Küçükyavuz and Merve Meraklı are supported, in part, by National Science Foundation Grants 1732364 and 1733001.

References

- Adrian and Brunnermeier [2016] T. Adrian and M. K. Brunnermeier. . The American Economic Review, 106(7):1705–1741, 2016.

- Artzner et al. [1999] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent measures of risk. Mathematical finance, 9(3):203–228, 1999.

- Cousin and Di Bernardino [2013] A. Cousin and E. Di Bernardino. On multivariate extensions of value-at-risk. Journal of Multivariate Analysis, 119:32–46, 2013.

- Cousin and Di Bernardino [2014] A. Cousin and E. Di Bernardino. On multivariate extensions of conditional-tail-expectation. Insurance: Mathematics and Economics, 55:272–282, 2014.

- Dentcheva et al. [2000] D. Dentcheva, A. Prékopa, and A. Ruszczynski. Concavity and efficient points of discrete distributions in probabilistic programming. Mathematical Programming, 89(1):55–77, 2000.

- Di Bernardino et al. [2015] E. Di Bernardino, J. Fernández-Ponce, F. Palacios-Rodríguez, and M. Rodríguez-Griñolo. On multivariate extensions of the conditional value-at-risk measure. Insurance: Mathematics and Economics, 61:1–16, 2015.

- Fábián and Veszprémi [2007] C. I. Fábián and A. Veszprémi. Algorithms for handling -constraints in dynamic stochastic programming models with applications to finance. 2007.

- Küçükyavuz and Noyan [2016] S. Küçükyavuz and N. Noyan. Cut generation for optimization problems with multivariate risk constraints. Mathematical Programming, 159(1-2):165–199, 2016.

- Lee and Prékopa [2013] J. Lee and A. Prékopa. Properties and calculation of multivariate risk measures: and . Annals of Operations Research, 211(1):225–254, 2013.

- Liu et al. [2017] X. Liu, S. Küçükyavuz, and N. Noyan. Robust multicriteria risk-averse stochastic programming models. Annals of Operations Research, pages 1–36, 2017. https://doi.org/10.1007/s10479-017-2526-z.

- Noyan and Rudolf [2013] N. Noyan and G. Rudolf. Optimization with multivariate conditional value-at-risk constraints. Operations Research, 61(4):990–1013, 2013.

- Noyan and Rudolf [2016] N. Noyan and G. Rudolf. Optimization with stochastic preferences based on a general class of scalarization functions. Optimization Online, http://www.optimization-online.org/DB_FILE/2016/09/5636.pdf, 2016.

- Noyan et al. [2017] N. Noyan, M. Merakli, and S. Küçükyavuz. Two-stage stochastic programming under multivariate risk constraints with an application to humanitarian relief network design. Optimization Online http://www.optimization-online.org/DB_FILE/2017/01/5804.pdf, 2017.

- Prékopa [1990] A. Prékopa. Dual method for the solution of a one-stage stochastic programming problem with random RHS obeying a discrete probability distribution. Zeitschrift für Operations Research, 34(6):441–461, 1990.

- Prékopa [2012] A. Prékopa. Multivariate value at risk and related topics. Annals of Operations Research, 193(1):49–69, 2012.

- Rockafellar and Uryasev [2000] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- Rockafellar and Uryasev [2002] R. T. Rockafellar and S. Uryasev. Conditional value-at-risk for general loss distributions. Journal of banking & finance, 26(7):1443–1471, 2002.

- Torres et al. [2015] R. Torres, R. E. Lillo, and H. Laniado. A directional multivariate value at risk. Insurance: Mathematics and Economics, 65:111–123, 2015.