A Stable Coin with Pro-rated Rebasement and Price Manipulation Protection

Abstract

An existing pseudo-commodity and a smart contracts framework allow the creation of a purely automatic and self-sufficient price-stable cryptocurrency, without human intervention. This new currency, we denominated Toroid111 v0.106 UNPUBLISHED WORK: All rights reserved. This work is not to be published in any way without permission from the author. or TRD, can be used more extensively for commerce than pseudo commodity cryptocurrencies due to its lower volatility. Also, is suitable for investment, as the tokens in each account multiply, return interest, when the market grows. Like the controlled fiat money of a central bank plus the benefits of an inflation-adjusted perpetuity bond. It eliminates the need of debt as the basic mechanism of the economy, although allows banking and further lending on top of it. Collateral in base coin, for example BTC or ETH, can be added to bootstrap your own Toroid investment or withdrawed after a very small investment period. So, the Toroids are not created from nothing nor have a limited monetary base. The minimum investment period can be very small, for example one day, and you keep the interest but you can return the Toroids and refund your collateral. That is a one-side only peg to a deflationary crypto-commodity. The stability is guaranteed by endogenous measurements of number of transactions and wallet pro-rated rebasement of balance to reduce volatility of price. Each account has its own rebasement due to the account creation timestamp. Rebasement control mechanism is progressive during initial bootstrap period because price manipulation protection is more severe when the capital involved is smaller. Rebasement has a quick positive start to incentivize early adopters that see only big growth in their TRD account during bootstrap period. Finally, the new rebasement control makes it economically infeasible for an attacker targeting the coin with manipulated transaction volume if we set the minimum rebasement greater than profits from massive currency manipulation. This protection increases its robustness and effectiveness over time because a coin with bigger capitalization is more difficult to manipulate.

1 Introduction

There is some discussion that we need new cryptocurrencies that can keep the pace of the economy, that can grow with the economy. Possible best alternatives are not based on debt. But still need to be dynamic, as pseudo commodities like Bitcoin have an almost static supply after some time.

With Ether, the money supply grows faster than BTC, but still slow enough to have a growth rate that tends towards (on the order of ). Assuming the economy grows faster than a linear rate (which historically has always been the case), Ether is also a "deflationary currency". [7]

Current fiat currencies based on debt are facing a huge crisis of trust due to growth stagnation in the developed countries and citizens and entrepreneurs demanding more freedom to generate their own financial assets. Also, many players are demanding a reduction in the financial friction such as fees, so everyone can invest on small and big scale. Most important, if big players don’t get so unproportioned returns on investment compared to smaller players that can’t afford expensive sophisticated funds and management services, the later can enter the game.

Ultimately, excessive debt resembles a Ponzi scheme. Nations, businesses, and individuals need to borrow ever-increasing amounts to repay existing borrowings and maintain economic growth. In the half-century leading up to 2008, the amount of debt needed to create US$1 of GDP in the US increased from US$1-2 to US$4-5. This rapid rise is insustainable, given an aging population, slower growth, and low inflation. [6]

Similarly to blood cells that are generated in abundance from bone marrow stem cells, and similarly to gold or silver-backed paper currencies, we are proposing that the current robust cryptographic pseudo-commodities [1] and the smart contract platform are used as a basis for pseudo-fiat currencies that will be bootstrapped by depositing basic coins (will be using ETH in example and first token) to generate a sub-currency that has enough features to have a more stable price, to have an non-limited monetary supply and to provide economical unfeasibility of currency manipulation.

To obtain all the features of currency which are scarcity, fungibility, divisibility, durability, and transferability, and to obtain the three main uses of currency which are as a medium of exchange, as a unit of account and as a store of value, we need our currency to be more stable than Bitcoin or gold. Who can pay for a coffee in Bitcoin if the coffee shop owner knows the price can change 10% in minutes? Currencies which includes features to stabilize its price are sometimes called stable coins [5] or if they use an elastic monetary base are called Hayek Money [4]. Other technical definition can categorize our stable coin as a smart beta bond [3], an intelligent bond with a market exposure lower than 1, that indicates an investment with lower volatility than the market.

Some stable coins have been designed to support collateral deposits to generate bonds in a way to bootstrap the new currency [2]. In our proposed design, we also use collateral to bootstrap the new currency but the funds remain frozen only a small period and you have the liberty to withdraw it but you keep the variable interest rate you recieved (and can be negative). Also, the stable coin we proposed is no two-way pegged to an external basket of existing currencies. Is only one way pegged, price can only be smaller, than the basic pseudo-commodity that fuels the smart contracts consensus framework. We also need some mechanism to deflect currency manipulation attacks or at least to make them economically unfeasible.

2 Features

2.1 General features

The Toroid cryptocurrency fund can be implemented easily on a cryptocurrency platform with smart contracts such as RootStock or Ethereum. It will have a one-way peg to the underlying deflationary token of the platform, such as BTC (in the RSK platform) or ETH (in the Ethereum platform). This results on the price of the TRD being smaller than the underlying pseudo-commodity but its monetary base being elastic. We will call base coin to the underlying BTC or ETH that fuels the smart contract platform and serves as collateral for bootstrapping ICOs (Initial Coin Offerings) and investment on the new more stable currency. Also, we will call stable coin or TRD to the new sub-currency defined by the smart contract.

We have an automatic rebasement in place, that is, the amount of TRDs in circulation is controlled by the smart contract that represents the fund and all the accounts or wallets. The rebasement is pro-rated across all wallets. An account with twice as TRD compared to another account will get twice of the rebasement adjustment measured in TRD coins. After the initial bootstrap period where is only positive, the rebasement can be positive or negative. A recurrent time-period, such as 1 day, 1 hour or 5 minutes is fixed as the TRD monetary base adjustment. For example, if we choose a 1-day period and 12AM GMT as the time of the rebasement and the smart contract decided that the current daily rebasement is 0.1% positive then all account have their balance increased on 0.1% to compensate endogenous metrics that have been measured on the previous period.

2.2 One-way peg to underlying deflationary token

This means that the price of the TRD will always be lower than a fixed amount of base cryptocurrency (we choose Ethereum platform and ETH base token for the sake of example). The one-way peg is implemented as following:

-

1.

to open a wallet with 1 TRD you need to deposit a fixed collateral, for example 1 decibitcoin (1/10 of ETH or 1 dETH );

-

2.

you can buy any amount of extra TRDs by depositing more collateral with the same rate of 1 dETH;

-

3.

the collateral is held as collateral in the smart contract and associated with your wallet until you close you decide, if you want, to return the original TRD amount;

-

4.

to close your account and get back the complete collateral you need to have at least in your account the amount of TRDs proportional to the amount of collateral.

The result of this design is that you can buy 1 TRD with 1 dETH or less, but never the price of 1 TRD will exceed 1 dETH, the fixed amount of collateral in the configuration. During the bootstrap of the Toroids there are incentives to deposit collateral and get the TRD interest added. At some point, during the Toroids will be less expensive on an exchange and you also get the return of the investment of you buy them on an exchange. Ideally, during bootstrap and after that during the first moments of the Toroids TRD owners will have little incentives to sell their TRD so new users will directly invest collateral to get their Toroids. If at some point the arbitrageurs will start funding the Toroid Fund to get cheap TRD and the price of the TRD will drop. If investors will analyze the estimated interest of ETH deposits returned in TRD to decide if they want to fund with ETH or buy TRD directly in the open market. If the TRD in circulation are few, then users that want to refund their ETH will need to buy TRD so the price of TRD will increase until when arbitrageurs will start funding and increasing the TRD supply.

2.3 Elastic currency supply with security limits

On an initial stage the currency price won’t be stable but will grow its supply to incentivize the early adopters. This period lasts time , for example 3 months. Also, the rebasement is by-design limited by the cost of an attack, so every attack is economically infeasible. We can model this by saying that rebasement ratio consists of three components:

TRD supply is rebased accross all wallets, according to

Volume is considered only as the number of transactions during the last period. We do not consider trading volume in TRDs because with only few big transactions any Sybil attack can be performed by many users or one user with many wallets. Supply is the total supply of TRDs in the system. Time step variable help us estimated time from bootstrap and analyze the previous steps during computations.

The initial ratio starts for example in 1.10 and slowly converges to 1.0 as the incentives for early adopters should fade after the other rebasement components becomes the main component. Example:

In this case and , so after 90 days the initial incentives per daily period reduces to only 1% from the 10% per day at the beginning. This initial rebasement ratio is not a function of last period’s volume of transactions.

As of , this section of the rebasement places a limit on the variation based on the cost of the transaction, to make the currency manipulation economically unfeasible for an attacker that wants to generate a massive number of fake transactions. As gas, based on the Ethereum platform, we mean the cost measured in native deflationary token (ETH) of executing different smart contracts. If we have during the last period wallet transactions, considering all the wallets in the system, and during the previous period there were no transaction at all222Remember that this is not transaccion volume, but the number of transactions. Other factors can also be used.. This is the worst-case scenario. We assume in this discussion that the price is gas is 20 gwei and the cost of basic transaction in the Ethereum platform is 20000 gas. And we consider that each transaction, a transference of TRDs from one wallet to another, costs a fixed amount of gas, measured in fractions of underlying base token (in our example is ETH). Then one basic wallet transference, costs 0.0004 ETH. If all activity during the period was only a Sybil attack then the cost of the attack is:

We used the knowledge that 1 TRD is one-way pegged to 1 deciETH. If we have , an attack of 10 thousand spurious transactions, then the cost for the attacker is . So, if we limit the profit from a malicious Sybil rebasement to 40 TRD, in this case, then we make the attack economically infeasible. Then if total supply of TRDs:

Then is the ratio allowed to limit Sybil attacks including an increase in the number of transactions. Similarly, if the number of transactions have been suddenly reduced in one period. We are assuming that currency supply rebasement is very quickly absorbed but market demand reflected linearly on price changes. Is a very simple model but other more sophisticated can be implemented in future versions. An ideal TRD transaction, hostile or ordinary, will never contribute more than its gas transaction cost to the total rebasement measured in ETH.

The main type of attacks to the stabilized cryptocurrency we want to prevent are pump and dump. Happen when simulated or exaggerated interest on the new coin is showed in the market to inflate its price and then the inventory of coin is liquidated by the attacker at an unusually higher price. Because of this type attack also the price of the coin plummets to very low levels.

3 Simulated results

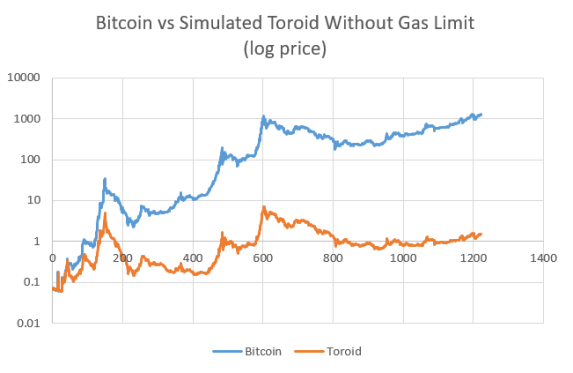

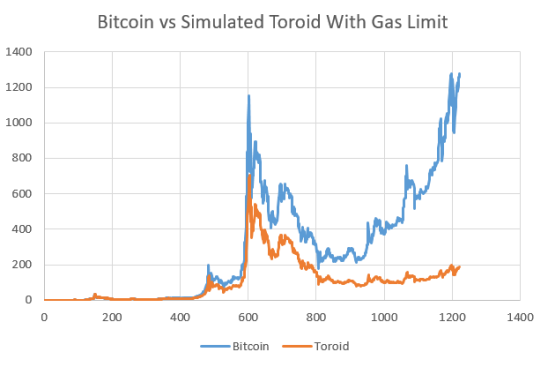

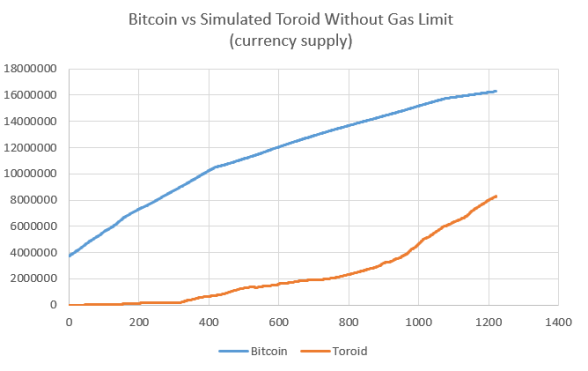

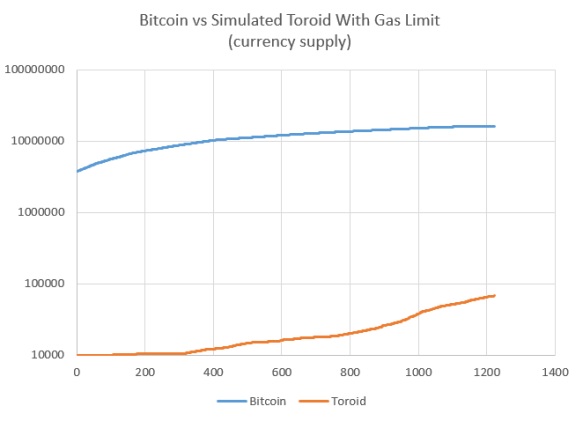

We simulated the behaviour of Toroid price compared to Bitcoin assuming the market absorbs the rebasement and adjust completely the coin to a new price. We can see in Figures 1 and 2 the price evolution over time of a simulated version or Toroid token. We see that the gas limit protection comes with a drawback, that is, a less powerful control over the price. Something similar is shown in Figures 3 and 4 where the token supply is shown, and including the gas limit makes the supply of the simulated Toroid grow slowly but still exponentially compared to base Bitcoin.

4 Conclusions

We proposed a system of stabilized cryptocurrencies based on a Smart contract platform that allow us to use the currency fueling the Smart contracts as collateral for the generation of the new coin interest. This system is not an artificial Ponzi scheme because the interest generated, based on endogenous metrics, can also be negative, the holding period can be is very small, and the stabilization of the new currency is adding value to the new currency and improving its conditions to be used as means of exchange for goods and services.

References

- [1] Bitcoin - open source p2p money. https://bitcoin.org/en/.

- [2] Makerdao. https://makerdao.com/.

- [3] Smart beta etfs. http://smart-beta.info/ETFs/.

- [4] Ferdinando M. Ametrano. Hayek money: The cryptocurrency price stability solution. SSRN, (August 13), 2016.

- [5] Vitalik Buterin. The search for a stable cryptocurrency. https://blog.ethereum.org/2014/11/11/search-stable-cryptocurrency/, 2014.

- [6] S. Das. The Age of Stagnation: Why Perpetual Growth is Unattainable and the Global Economy is in Peril. Prometheus Books, 2016.

- [7] madavidj. Comment on: Why 30 million ? why so inflationary ? https://forum.ethereum.org/discussion/107/why-30-million-why-so-inflationary, 2014.