Semiparametric Efficiency in Convexity Constrained Single Index Model

Abstract

We consider estimation and inference in a single index regression model with an unknown convex link function. We introduce a convex and Lipschitz constrained least squares estimator (CLSE) for both the parametric and the nonparametric components given independent and identically distributed observations. We prove the consistency and find the rates of convergence of the CLSE when the errors are assumed to have only moments and are allowed to depend on the covariates. When , we establish -rate of convergence and asymptotic normality of the estimator of the parametric component. Moreover, the CLSE is proved to be semiparametrically efficient if the errors happen to be homoscedastic. We develop and implement a numerically stable and computationally fast algorithm to compute our proposed estimator in the R package simest. We illustrate our methodology through extensive simulations and data analysis. Finally, our proof of efficiency is geometric and provides a general framework that can be used to prove efficiency of estimators in a wide variety of semiparametric models even when they do not satisfy the efficient score equation directly.

Abstract

Section S.1 proposes an alternating minimization algorithm to compute the estimators proposed in the paper. Section S.2 provides some insights into the proof of Theorem 4.1. Section S.3 shows that the asymptotic variance in Theorem 4.1 is the Moore-Penrose inverse of the efficient information matrix. Section S.4 provides further simulation studies. Section S.5 provides additional discussion on our identifiability assumptions. Section S.6 finds the minimax lower bound for the model (1.1) under (A1)–(A3) and shows that the CLSE is minimax rate optimal when Section S.8 provides new maximal inequalities that allow for unbounded errors. These maximal inequalities are used in Section S.9 to allow for heavy-tailed and heteroscedastic errors. These results are also of independent interest. Sections S.7–S.12 contain the proofs omitted from the main text. Section S.9 proves the results in Section 3. Section S.10 completes the proof of the approximate zero property in (4.16). Sections S.11 and S.12 complete the proofs of the steps in Section S.2. Section S.13 provides a comment regarding the computation of the function estimate in the CLSE when there are ties.

Keywords: bundled parameter; errors with finite moments; geometric proof of semiparametric efficiency; Lipschitz constrained least squares; shape restricted function estimation

1 Introduction

Suppose we have i.i.d. observations from the following single index regression model:

| (1.1) |

where () is the predictor, is the response variable, and satisfies and almost everywhere (a.e.) , the distribution of . We assume that the real-valued link function and are the unknown parameters of interest.

Single index models are ubiquitous in regression because they provide convenient dimension reduction and interpretability. The single index model circumvents the curse of dimensionality encountered in estimating the fully nonparametric regression function by assuming that the link function depends on only through a one dimensional projection, i.e., ; see e.g., [65]. Moreover, the coefficient vector provides interpretability [51] and the one-dimensional nonparametric link function offers some flexibility in modeling. The above model has received a lot of attention in statistics in the last few decades; see e.g., [65, 50, 37, 31, 34, 13, 12, 44] and the references therein. The above papers propose estimators for the single index model under the assumption that is smooth (i.e., two or three times differentiable).

However, quite often in the context of a real application, qualitative assumptions on may be available. For example, in microeconomics, production and utility functions are often assumed to be concave and nondecreasing; concavity indicates decreasing marginal returns/utility [78, 57, 51]. In finance, the relationship between call option prices and strike price are often known to be convex and decreasing [1]; in stochastic control, value functions are often assumed to be convex [40]. The following two real-data examples further illustrate that convexity/concavity constraints arise naturally in many applications.

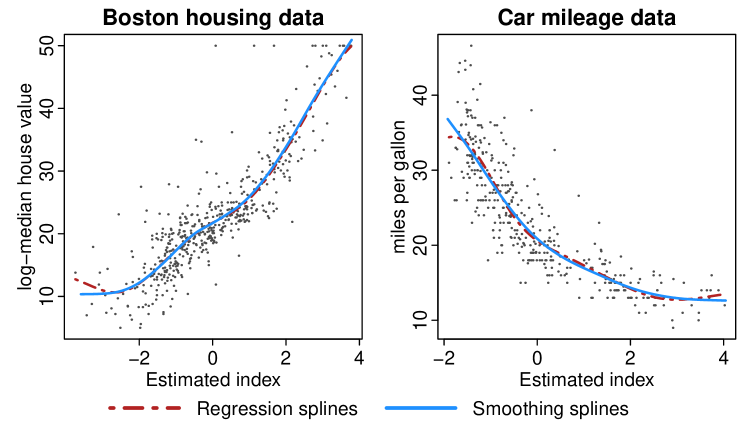

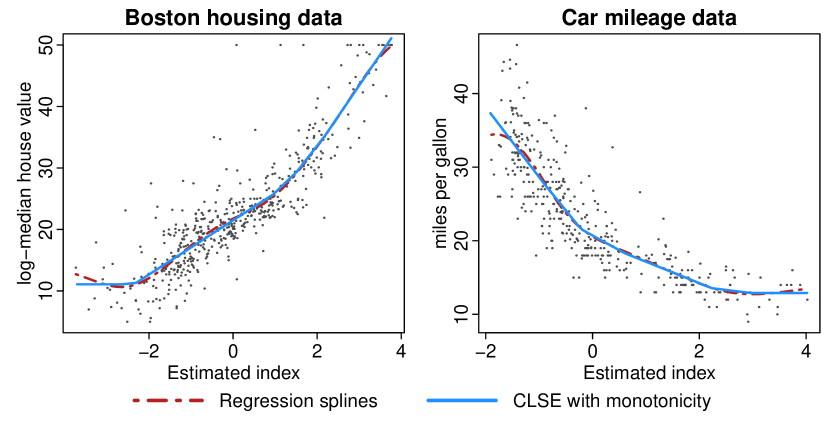

Example 1.1 (Boston housing data).

Harrison and Rubinfeld [32] studied the effect of different covariates on real estate price in the greater Boston area. The response variable was the log-median value of homes in each of the census tracts in the Boston standard metropolitan area. A single index model is appropriate for this dataset; see e.g., [26, 81, 82, 85]. The above papers considered the following covariates in their analysis: average number of rooms per dwelling, full-value property-tax rate per USD, pupil-teacher ratio by town school district, and proportion of population that is of “lower (economic) status” in percentage points. In the left panel of Figure 1, we provide the scatter plot of , where is the estimate of obtained in [81]. We also plot estimates of obtained from [44] and [81]. The plot suggests a convex and nondecreasing relationship between the log-median home prices and the index, but the fitted link functions satisfy these shape constraints only approximately.

Example 1.2 (Car mileage data).

Donoho and Ramos [16] consider a dataset containing mileages of different cars. The data contains mileages of cars as well as the following covariates: displacement, weight, acceleration, and horsepower. Cheng et al. [11] and [44] have fit a partial linear model and a single index model, respectively. In the right panel of Figure 1, we plot the estimators proposed in [44] and [81]. Both of these works consider estimation in the single index model under only smoothness assumptions. The “law of diminishing returns” suggests should be convex and nonincreasing. However, as observed in Figure 1, the estimators based only on smoothness assumptions satisfy this shape constraint only approximately.

In both of the examples, the smoothing based estimators do not incorporate the known shape of the nonparametric function. Thus the estimators are not guaranteed to be convex (or monotone) in finite samples. Moreover, the choice of the tuning parameter in smoothness based estimators is tricky as different values for the tuning parameter lead to very different shapes. This unpredictable behavior makes the smoothness based estimators of less interpretable, and motivates the study of a convexity constrained single index model. We discuss these two datasets and our analysis in more detail in Sections 6.1 and 6.2.

In this paper, we propose constrained least squares estimators for and that is guaranteed to satisfy the inherent convexity constraint in the link function everywhere. The proposed methodology is appealing for two main reasons: (1) the estimator is interpretable and takes advantage of naturally occurring qualitative constraints; and (2) unlike smoothness based estimators, the proposed estimator is highly robust to the choice of the tuning parameter without sacrificing efficiency.

In the following, we conduct a systematic study of the computation, consistency, and rates of convergence of the estimators, under mild assumptions on the covariate and error distributions. We further prove that the estimator for the finite-dimensional parameter is asymptotically normal. Moreover, this estimator is shown to be semiparametrically efficient if the errors happen to be homoscedastic, i.e., when a.e. for some constant . It should be noted that in the examples above the link function is also known to be monotone. To keep things simple, we focus on only convexity constrained single index model. However, all our results continue to hold under the additional monotonicity assumption, i.e., our conclusions hold for convex/concave and nondecreasing/nonincreasing . More generally, our results continue to hold under any additional shape constraints; see Remarks 3.11, 4.4, and S.1.1 and Section 6 in the paper for more details.

One of the main contributions of this paper is our novel geometric proof of the semiparametric efficiency of the constrained least squares estimator. Note that proving semiparametric efficiency of constrained (and/or penalized) least squares estimators often requires a delicate use of the structure of the estimator of the nonparametric component (say ) to construct least favorable paths; see e.g. [61], [76, Chapter 9.3], and [35] (also see Example 4.5). In contrast, our approach is based on the following simple observation. For a traditional smoothness based estimator , the path will belong to the (function) parameter space for any smooth “perturbation” (for small enough ). However this is no longer true when the underlying parameter space is constrained. But, observe that the projection of onto the constrained function space certainly yields a “valid” path. Our proof technique is based on differentiability properties of the path , where denotes the -projection onto the (constrained) function space. This general principle is applicable to other shape constrained semiparametric models, because differentiability of the projection operator is well-studied in the context of constrained optimization algorithms; see Section 1.1 below for a more detailed discussion. Also see Example 4.5, where we discuss the applicability of our technique in (re)proving the semiparametric efficiency of the nonparametric maximum likelihood estimator in the Cox proportional hazard model under current status censoring [35]. To be more specific, we study the following Lipschitz constrained convex least squares estimator (CLSE):

| (1.2) |

where

| (1.3) |

and denotes the class of all -Lipschitz real-valued convex functions on and

| (1.4) |

Here denotes the usual Euclidean norm, and is the Euclidean unit sphere in . The norm-1 and the positivity constraints are necessary for identifiability of the model111 Without any sign or scale constraint on no will be identifiable. To see this, fix any and define and , then ; see [7], [12], and [21] for identifiability of the model (1.1). Also see Section 2.2 for further discussion..

The Lipschitz constraint in (1.2) is not restrictive as all convex functions are Lipschitz in the interior of their domains. Furthermore in shape-constrained single index models, the Lipschitz constraint is known to lead to computational advantages [39, 38, 53, 22, 58]. Additionally on the theoretical side, the Lipschitzness assumption allows us to control the behavior of the estimator near the boundary of its domain. This control is crucial for establishing semiparametric efficiency. To the best of our knowledge, this is the first work proving semiparametric efficiency for an estimator in a bundled parameter problem (where the parametric and nonparametric components are intertwined; see [36]) where the nonparametric estimate is shape constrained and non-smooth. Note that the convexity constraint in (1.2) leads to a convex piecewise affine estimator for the link function ; see Section 3 for a detailed discussion.

Our theoretical and methodological study can be split in two broad categories. In Section 3, we find the rate of convergence of the CLSE as defined in (1.2), whereas in Section 4 we establish the asymptotic normality and semiparametric efficiency of . Suppose that is -Lipschitz, i.e., . If the tuning parameter is chosen such that , then under mild distributional assumptions on and , we show that and are minimax rate optimal for estimating and , respectively; see Theorems 3.2 and 3.6. We also allow for the tuning parameter to depend on the data and show that the rate of convergence of is uniform in , up to a multiplicative factor; see Theorem 3.3. This result justifies the usage of a data-dependent choice of , such as cross-validation. Additionally, in Theorem 3.8, we find the rate of convergence of In Section 4, we establish that if , then is -consistent and is asymptotically normal with mean and finite variance; see Theorem 4.1. The asymptotic normality of can be readily used to construct confidence intervals for . Further, we show that if the errors happen to be homoscedastic, then is semiparametrically efficient.

Our contributions on the computational side are two fold. In Section S.1 of the supplementary file, we propose an alternating descent algorithm for estimation in the single index model (1.1). Our descent algorithm works as follows: when is fixed, the update is obtained by solving a quadratic program with linear constraints, and when is fixed, we update by taking a small step on the Stiefel manifold with a guarantee of descent. We implement the proposed algorithm in the R package simest. Through extensive simulations (see Section 5 and Section S.4 of the supplementary file) we show that the finite sample performance of our estimators is robust to the choice of the tuning parameter . Thus we think the practitioner can choose to be very large without sacrificing any finite sample performance. Even though the minimization problem is non-convex, we illustrate that the proposed algorithm (when used with multiple random starting points) performs well in a variety of simulation scenarios when compared to existing methods.

1.1 Semiparametric efficiency and shape constraints

Although estimation in single index models under smoothness assumptions is well-studied (see e.g., [65, 50, 37, 31, 34, 13, 81, 12] and the references therein), estimation and efficiency in shape-restricted single index models have not received much attention. The earliest reference on this topic we could find was the work of Murphy et al. [61], where the authors considered a penalized likelihood approach in the current status regression model (which is similar to the single index model) with a monotone link function. Chen and Samworth [10] consider maximum likelihood estimation in a generalized additive index model (a more general model than (1.1)) and only prove consistency of the proposed estimators. In Balabdaoui et al. [3], the authors study model (1.1) under monotonicity constraint and prove -consistency of the LSE of ; however they do not obtain the limiting distribution of the estimator of Balabdaoui et al. [4] propose a tuning parameter-free -consistent (but not semiparametrically efficient) estimator for the index parameter in the monotone single index model.

In this paper, we show that is semiparametrically efficient under homoscedastic errors. Our proof of the semiparametric efficiency is novel and can be applied to other semiparametric models when the estimator does not readily satisfy the efficient score equation. In fact, we provide a new and general technique for establishing semiparametric efficiency of an estimator when the nuisance tangent set is not the space of all square integrable functions. The basic idea is as follows. Suppose represents the semiparametrically efficient influence function, meaning that the “best” estimator of satisfies the following asymptotic linear expansion:

| (1.5) |

for every . A crucial step in establishing that satisfies (1.5) is to show for any ,

i.e., is an approximate zero of the efficient score equation [76, Theorem 6.20]. Because minimizes over , the traditional way to prove the approximate zero property is to use the fact that for all perturbation “directions” and find an such that the derivative of at is ; see e.g., [63]. In fact, using this method one can often show that the estimator satisfies the efficient score equation exactly. If is a valid path (i.e., for all in some neighborhood of zero) for an arbitrary but “smooth” then it is relatively straightforward to establish the approximate zero property [63].222 As is restricted to have norm , does not belong to the parametric space for and . However, this can be easily remedied by considering another path that is differentiable and has the same “direction”; we define such a path in (4.3). However, this approach does not work when the nonparametric function is constrained. This is because under constraints, might not be a valid path for arbitrary but smooth . The novelty of our proposed approach lies in observing that in contrast to , is always a valid path for every smooth ; here is the -projection of onto . Thus if is differentiable, then for any perturbation . Then establishing that is an approximate zero boils down to finding an such that

Differentiability of projection operators is well-studied; e.g., see [14, 20, 59, 68, 69] for sufficient conditions for a general projection operator to be differentiable. The generality and the usefulness of our technique can be understood from the fact that no specific structure of or is used in the previous discussion; we elaborate on this in Section 4.2. On the other hand, existing methods (see e.g., [61]) require delicate (and not generalizable) use of the structure of the nonparametric estimator to create valid paths around the nonparametric function; see e.g., [61] for semiparametric efficiency in current status regression, and [76, Chapter 9.3] and [35] for efficiency in the Cox proportional hazard model with current status data; see Example 4.5.

1.2 Organization of the exposition

Our exposition is organized as follows: in Section 2, we introduce some notation and formally define the CLSE. In Section 3, we state our assumptions, prove consistency, and give rates of convergence for the CLSE. In Section 4, we detail our new method to prove semiparametric efficiency of the CLSE. We use this to prove -consistency, asymptotic normality, and efficiency (when the errors happen to be homoscedastic) of the CLSE of . We discuss an algorithm to compute the proposed estimator in Section S.1. In Section 5, we provide an extensive simulation study and compare the finite sample performance of the proposed estimator with existing methods in the literature. In Section 6, we analyze the Boston housing data [32] and the car mileage data [16] introduced in Examples 1.1 and 1.2 in more details. In both of the cases, we show that the natural shape constraint leads to stable and interpretable estimates. Section 7 provides a brief summary of the paper and discusses some open problems.

Section numbers in the supplementary file are prefixed with “S.”. Section S.2 of the supplementary file provides some insights into the proof of Theorem 4.1, one of our main results. Section S.4 provides further simulation studies. Section S.5 provides additional discussion on the identifiability of the parameters. Sections S.7–S.12 contain the proofs of our results. Section S.10 completes our novel proof of semiparametric efficiency sketched in Section 4.2.

2 Notation and Estimation

2.1 Preliminaries

In what follows, we assume that we have i.i.d. data from (1.1). We start with some notation. Let denote the support of and define

| (2.1) |

where denotes the convex hull of the set . Let denote the class of real-valued convex functions on that are uniformly Lipschitz with Lipschitz bound For any , let denote the nondecreasing right derivative of the real-valued convex function . Because is a uniformly Lipschitz function with Lipschitz constant , without loss of generality, we can assume that , for all We use to denote the probability of an event and for the expectation of a random quantity. For any , let denote the distribution of . For , define Let denote the joint distribution of and let denote the joint distribution of when where is defined in (1.1). In particular, denotes the joint distribution of when and satisfies (1.1). For any set () and any function , we define and for The notation is used to express that for some constant . For any function , let denote each of the components of , i.e., and . We define and For any function and , we define for all We use the following (standard) empirical process theory notation. For any function , and , we define

Note that can be a random variable when or or both are random. Moreover, for any function , we define and

2.2 Identifiability

We now discuss the identifiability of and . Letting observe that minimizes In fact we can show in Section S.5.1, that

| (2.2) |

This implies that is always identifiable and further, one can hope to consistently estimate by minimizing the sample version of ; see (1.2).

Note that the identification of does not guarantee that both and are separately identifiable. Hence, in what follows, when dealing with the properties of separated parameters, we will directly assume:

-

(A0)

The parameters and are separately identifiable, i.e., for some implies that and .

Ichimura [37] has found general sufficient conditions on the distribution of under which (A0) holds; these sufficient conditions allow for some components of to be discrete, also see Horowitz [33, Pages 12–17] and Li and Racine [51, Proposition 8.1]. When has a density with respect to Lebesgue measure, Lin and Kulasekera [54, Theorem 1] find a simple sufficient condition for (A0). We discuss and compare these two sufficient conditions in Section S.5.2 of the supplementary file.

3 Convex and Lipschitz constrained LSE

Recall that CLSE is defined as the minimizer of over . Because depends only on the values of the function at , it is immediately clear that the minimizer is unique only at . Since is restricted to be convex, we interpolate the function linearly between ’s and extrapolate the function linearly outside the data points.333Linear interpolation/extrapolation does not violate the convexity or the -Lipschitz property Thus is piecewise affine. In Section S.7 of the supplementary file, we prove the existence of the minimizer in (1.2). The optimization problem (1.2) might not have a unique minimizer and the results that follow hold true for any global minimizer.

Remark 3.1.

For every fixed , has a unique minimizer. The minimization over the class of uniformly Lipschitz functions is a quadratic program with linear constraints and can be computed easily; see Section S.1.1.

3.1 Asymptotic analysis of the regression function estimate

In this section, we study the asymptotic behavior of . We will now list the assumptions under which we study the rates of convergence of the CLSE for the regression function.

-

(A1)

The unknown convex link function is bounded by some constant on and is uniformly Lipschitz with Lipschitz constant .

-

(A2)

The support of , , is a subset of and for some finite .

-

(A3)

The error in model (1.1) has finite th moment, i.e., where . Moreover, a.e. and for all

The above assumptions deserve comments. (A2) implies that the support of the covariates is bounded. In assumption (A3), we allow to be heteroscedastic and can depend on . Our assumption on is more general than those considered in the shape constrained literature, most works assume that all moments of are finite and “well-behaved”, see e.g., [4], [34], and [84].

Theorem 3.2 (proved in Section S.9.1) below provides an upper bound on the rate of convergence of to under the norm. The following result is a finite sample result and shows the explicit dependence of the rate of convergence on and .

Theorem 3.2.

Assume (A1)–(A3). Let be a fixed sequence such that for all and let

| (3.1) |

Then for every and , there exists a constant depending only on and , and constant depending only on , and such that

where the supremum is taken over all and all joint distributions of and parameters for which assumptions (A1)–(A3) are satisfied with constants and . In particular if , and as , then

Note that (3.1) allows for the dimension to grow with and to change with . For example if for some fixed , then we have that if . In the rest of the paper, we assume that is fixed. In Proposition S.6.1 in Section S.6, we find the minimax lower bound for the single index model (1.1), and show that is minimax rate optimal when .

The next result shows that the rates in Theorem 3.2 are in fact uniform (up to a factor) in . This uniform-in- result is important for the study of the estimator with a data-driven choice of such as cross-validation or Lepski’s method [49]. Theorem 3.2 alone cannot provide such a rate guarantee because it requires to be non-stochastic.

Theorem 3.3.

Under the assumptions of Theorem 3.2, the CLSE satisfies

| (3.2) |

Remark 3.4 (Diverging ).

The dependence on in Theorems 3.2 and 3.3 suggest that the estimator may not be consistent if diverges too quickly with the sample size. The simulation in Section 5.3 suggests that the estimation error has negligible dependence on and that the dependence on in Theorems 3.2 and 3.3 might be sub-optimal. We believe this discrepancy is due to the lack of available technical tools to prove uniform boundedness of the estimator in terms of . At present, we are only able to prove that with high probability, for all ; see Lemma S.9.1. If one can prove for all , with high probability, for a constant independent of , then our proofs can be modified to remove the dependence on in Theorems 3.2 and 3.3.

3.2 Asymptotic analysis of and

In this section we establish the consistency and find rates of convergence of and separately. In Theorem 3.2 we proved that converges in the norm but that does not guarantee that converges to in the norm. A typical approach for proving consistency of is to prove that is precompact in the norm ( is defined in (2.1)); see e.g., [3, 61]. The Arzelà-Ascoli theorem establishes that the necessary and sufficient condition for compactness (with respect to the uniform norm) of an arbitrary class of continuous functions on a bounded domain is that the function class be uniformly bounded and equicontinuous. However, if is allowed to grow to infinity, then it is not clear whether the sequence of functions is equicontinuous. Thus to study the asymptotic properties of and we assume that , is a fixed constant. For the rest of paper, we will use and to denote (or ) and (or ), respectively. The next theorem (proved in Section S.9.4) establishes consistency of and separately. Recall that denotes the nondecreasing right derivative of the convex function .

Theorem 3.5.

Fix an orthonormal basis of such that Define . We will use the following two additional assumptions to establish upper bounds on the rate of convergence of and

-

(A4)

is a positive definite matrix.

-

(A5)

The density of with respect to the Lebesgue measure is bounded above by .

Assumption (A4), is used to find the rate of convergence for and separately and is widely used in all works studying root- consistent estimation of in the single index model, see e.g., [65, 37, 44, 4]; also see Remark 3.7. (A5) is mild, and is satisfied if has a continuous covariate such that: (1) has a bounded density; and (2) . Compare assumption (A5) with [37, 12, 4, 81, 80] where it is assumed that has a density bounded away from zero for all in a neighborhood of . Assumption (A5) is used to find rates of convergence of the derivative of the estimators of . In Theorem 3.6, we only use the fact that is absolutely continuous with respect to Lebesgue measure. The following result (proved in Section S.9.5) establishes upper bounds on the rate of convergence of and respectively.

Remark 3.7.

A simple modification of the proof of Proposition S.6.1 will prove that is also minimax rate optimal. Under additional smoothness assumptions on , in the following theorem (proved in Section S.9.7) we show that , the right derivative of converges to in both the and the supremum norms.

Theorem 3.8.

Remark 3.9.

As in (3.3), (3.4) can also be proved under -Hölder continuity of , but in this case the rate of convergence depends on explicitly. Assumption (B2) allows for the density of to be zero at some points in its support; see Section 4 for a detailed discussion. Further if the density of is bounded away from zero, then can be taken to be .

Remark 3.10.

Remark 3.11 (Additional shape constraints on the link function).

It might often be the case that in addition to convexity, the practitioner is interested in imposing additional shape constraints (such as monotonicity, unimodality, or -monotonicity [29]) on . For example, in the datasets considered in Examples 1.1 and 1.2, the link function is plausibly both convex and monotone; see [10] for further motivation on additional shape constraints. The conclusions (and proofs) of Theorems 3.2 and 3.3–3.8 also hold for the CLSE under additional constraints on the link function. An intuitive explanation is that the parameter space is only reduced by imposing additional constraints on the link function and this can only give better rates (if not the same). In case of an additional monotonicity constraint on , one can modify the proof of Proposition S.6.1 to show that the rate obtained in Theorem 3.2 is in fact minimax optimal for the the CLSE (under further monotonicity constraint).

4 Semiparametric inference for the CLSE

The main result in this section shows that is -consistent and asymptotically normal; see Theorem 4.1. Moreover, is shown to be semiparametrically efficient for if the errors happen to be homoscedastic. The asymptotic analysis of is involved as is a piecewise affine function and hence not differentiable everywhere.

Before deriving the limit law of , we introduce some notations and assumptions. Let denote the joint density (with respect to some dominating measure on ) of . Let and denote the corresponding conditional probability density of given and the marginal density of , respectively. In the following we list additional assumptions used in Theorem 4.1. Recall and from (2.1) and let denote the Lebesgue measure.

-

(B1)

and is -Hölder continuous on for some . Furthermore, is strongly convex on , i.e., there exists a such that is convex.

-

(B2)

There exists and such that for all intervals .

For every , define .

-

(B3)

The function is -Hölder continuous and for a constant ,

(4.1) -

(B4)

The density is differentiable with respect to for all .

Assumptions (B1)–(B4) deserve comments. (B1) is much weaker than the standard assumptions used in semiparametric inference in single index models [61, Theorem 3.2]. Assumption (B2) is an improvement compared to the assumptions in the existing literature. Assumption (B2) pertains to the distribution of and is inspired by [21, assumption (D)]. In contrast, most existing works require the density of to be bounded away from zero (i.e., ); see e.g., [37, Assumption 5.3(II)], [12, Assumption (d)], [4, Lemma F.3], [81, Assumption A2], [80, Assumption (A2)]. Our assumption is significantly weaker because it allows the density of to be zero at some points in its support. For example, when , the density of might not be bounded away from zero [21, Figure 1], but (B2) holds with Assumption (B3) can be favorably compared to those in [61, Theorem 3.2], [25, Assumption (A5)], [4, Assumption (A5)], and [70, Assumption G2 (ii)]. We use the smoothness assumption (B3) when establishing semiparametric efficiency of . The Lipschitzness assumption (4.1) can be verified by using the techniques of [2], when is -Hölder continuous for all in a neighborhood of and the Hölder constants are uniformly bounded in .

In general, establishing semiparametric efficiency of an estimator proceeds in two steps. Let and denote the estimators of a parametric component and a nuisance component in a general semiparametric model. In a broad sense, the proof of semiparametric efficiency of involves two main steps: (i) finding the efficient score of the model at the truth (call it ); and (ii) proving that satisfies ; see [76, pages 436-437] for a detailed discussion. In the Sections 4.1 and 4.2, we discuss steps (i) and (ii) in our context, respectively.

4.1 Efficient score

In this subsection we calculate the efficient score for the model:

| (4.2) |

where and satisfy assumptions (B1)–(B4). First observe that the parameter space is a closed subset of and the interior of in is the empty set. Thus to compute the score for model (4.2), we construct a path on the sphere. We use to parametrize the paths for model (4.2) on when . For each , and , define the following path , with “direction” , through (which lies on the unit sphere)

| (4.3) |

where for every , is such that for every , and is orthogonal to . Furthermore, we need to satisfy some smoothness properties; see Lemma 1 of [44] for such a construction. Note that, if , then for any in a neighborhood of zero, there exists an such that . Thus, if , then lies on the “boundary” of and the existing semiparametric theory breaks down. Therefore, for the rest of the paper, we assume that is strictly positive.

The log-likelihood of model (4.2) is For any , consider the path defined as . Note that by the definition of , is a valid path in through ; i.e., and for every in some neighborhood of . Thus the score for the parametric submodel is

| (4.4) |

where

| (4.5) |

The next step in computing the efficient score for model (4.2) at is to compute the nuisance tangent space of the model (here the nuisance parameters are , and ). To do this define a parametric submodel for the unknown nonparametric components:

| (4.6) | ||||

where , is a bounded function such that and , is a bounded function such that and , with

| (4.7) | ||||

Note that when satisfies (B1) then reduces to Thus Theorem 4.1 of [63] (also see Ma and Zhu [55, Proposition 1]) shows that when the parametric score is and the nuisance tangent space corresponding to is , then the efficient score for model (4.2) is

| (4.8) |

Note that the efficient score depends on and only through . However if the errors happen to be homoscedastic (i.e., ) then the efficient score is , where

| (4.9) |

As is unknown we restrict ourselves to efficient estimation under homoscedastic error; see Remark 4.3 for a brief discussion.

4.2 Efficiency of the CLSE

The -consistency, asymptotic normality, and efficiency (when the errors are homoscedastic) of will be established if we could show that

| (4.10) |

and the class of functions indexed by in a “neighborhood” of satisfies some technical conditions; see e.g., van der Vaart [76, Chapter 6.5]. As discussed in Section 1.1, because minimizes over , the traditional way to prove (4.10) is to use the fact that for any such that is a valid path (i.e., ). One then finds such that the derivative of at is approximately ; such an is called the (approximate) least favorable submodel; see van der Vaart [76, Section 9.2]. In Section 4.1, we saw that if is strongly convex then . However is piecewise affine and we can only show that . Thus is valid path only if ; see [61] for another example where . In such cases it is hard to find the least favorable submodel as often the step to compute the least favorable model involves computing projection onto ; see e.g., [62]. Thus when is not (or a very simple subspace of ), the standard linear path arguments fail to find the least favorable submodel. To overcome this, [61] use a very complicated and non-linear path; see Section 6.2 of [61]; also see [44].

Our proposed technique crucially relies on the observation that is a valid path for every . Thus if is differentiable, then establishing that is an approximate zero boils down to finding an such that

| (4.11) |

for every In Section S.10, we show is differentiable if , where

| (4.12) |

and are the set of kinks of . For a piecewise affine function, a kink is a point where the slope changes. Furthermore, in Theorem S.10.1, we find an that satisfies (4.11). The advantage of the technique proposed here is that the construction of approximate least favorable submodel is analytic and does not rely on the ability of the user to “guess” the least favorable submodel; see e.g., [76, Section 9.2-9.3] and [61]. The above discussion and [76, Theorem 6.20] lead to our main result (Theorem 4.1) of this section. Recall and defined in (4.4) and (4.9), respectively.

Theorem 4.1.

Remark 4.2.

If is twice continuously differentiable then . Hence, is equivalent to assuming . Note that allows for covariate distributions for which the density of can go to zero. In Theorem 4.1, to keep notations in the proof simple, we assume that . However, by using Remark 3.10, this condition can be weakened to . In Section S.3, we show that the limiting variances in Theorem 4.1 are unique and do not depend on the particular choice of .

Sketch of the proof.

The proof follows along the lines of Theorem 6.20 of [76]. The main novelty in the proof is a new mechanism to verify that the estimator satisfies the score equation (4.10). However to simplify the algebra involved,444All the proofs will go through with instead of . However, usage of will require more remainder terms to be controlled and thus will lead to more tedious proofs. we will work with

| (4.15) |

a slight modification of . The only difference between and is the last term (. In Section S.2 of the supplementary file we show that

| (4.16) |

implies

| (4.17) |

The conclusion of the proof follows by observing that . We will now give a brief sketch of the proof of (4.16). Define for every , , , and ,

Observe that is the minimizer of and is a valid path in through . Thus is the minimizer of for every and . Hence if is differentiable then

| (4.18) |

Furthermore, if functions (for some ) are such that is differentiable for all , then

for any . Note that the proof of (4.16) will be complete, if we can show that for every , there exist a and functions such that is differentiable and

| (4.19) |

This means that it is enough to consider the approximation of by the linear closure of . Instead of fully characterizing the linear closure set, we find a large enough subset that suffices for our purpose using the following steps.

- 1.

-

2.

For every such , in Lemma S.10.3, we show that

Thus to prove (4.19), it is enough to show that

where is defined in (4.15). In more general constraint spaces, one might need to use the generality of but in our case, it suffices to work with ; see Theorem S.10.1. ∎

Remark 4.3 (Efficiency under heteroscedasticity).

Remark 4.4 (Efficiency under additional shape constraints).

As discussed in Remark 3.11, it might be the case that the practitioner is interested in imposing additional shape constraints such as monotonicity, unimodality, or -monotonicity (in addition to convexity). If satisfies these constraints in a strict sense (i.e., is strictly monotone or -monotone) then the discussion in Section 4.1 implies that the efficient score (at the truth) is still (4.8) even under the additional shape constraints. This is true, because even under these additional shape constraints on link functions, as does not lie on the “boundary” of the parameter space. In fact, under these additional constraints, the proof of Theorem 4.1 can be used with minor modifications to show that CLSE of satisfies (4.13).

To further illustrate the usefulness of our new approach we discuss the proof of semiparametric efficiency in the Cox proportional hazards model under current status censoring [35, 76].

Example 4.5 (Cox proportional hazards model with current status data).

Suppose that we observe a random sample of size from the distribution of , where , such that the survival time and the observation time are independent given , and that follows a Cox proportional hazards model with parameter and cumulative hazard function ; e.g., see [35, Section 2] for a more detailed discussion of this model. Huang [35] shows that , the nonparametric maximum likelihood estimator (NPMLE) of , is a right-continuous step function with possible discontinuities only at (the observed censoring/inspection times). Huang [35] also proves that (the NPMLE for ) is an efficient estimator for . However just as in the single index model, the proof of efficiency is complicated due to the fact that will not necessarily be a valid hazard function for every smooth .555 is not guaranteed to be monotone as is a nondecreasing piecewise constant function and not strictly increasing. To establish (4.10) for the above model, Huang [35, pages 563-564] “guesses” an approximately least favorable path (also see [76, pages 439-441]). However, using the arguments above we can easily see that is differentiable if is a piecewise constant function with possible discontinuities only at the points of discontinuities of . Then using the property that one can establish a result similar to (4.11). A similar strategy can be used to establish efficiency in the current status regression model in Murphy et al. [61].

4.3 Construction of confidence sets and validating the asymptotics

Theorem 4.1 shows that when the errors happen to be homoscedastic the CLSE of is -consistent and asymptotically normal with covariance matrix:

| (4.20) |

where is defined in (4.9). This result can be used to construct confidence sets for However since is unknown, we propose using the following plug-in estimator of :

| (4.21) |

where . Note that Theorems 3.6 and 3.8 imply consistency of .

For example one can construct the following confidence interval for :

| (4.22) |

where denotes the upper th-quantile of the standard normal distribution. The truncation guarantees that confidence interval is a subset of the parameter set.

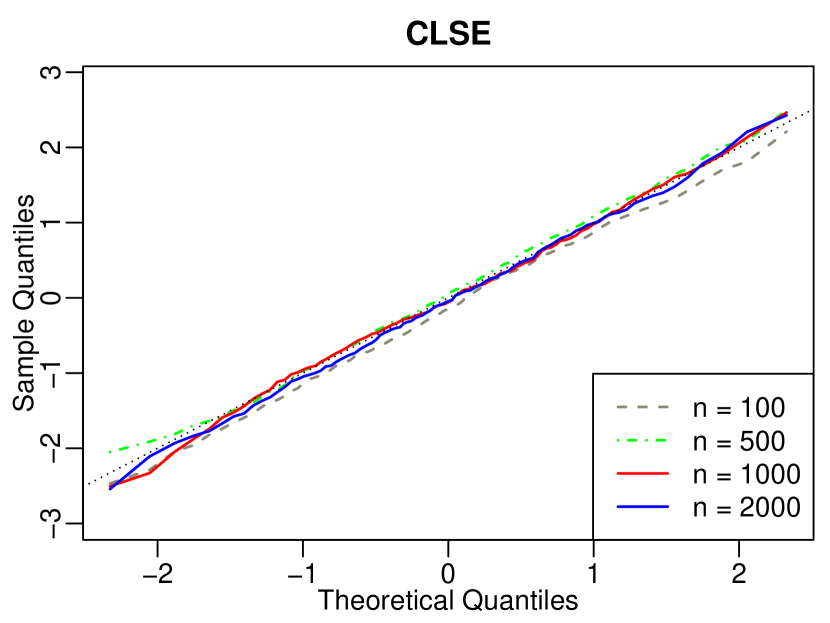

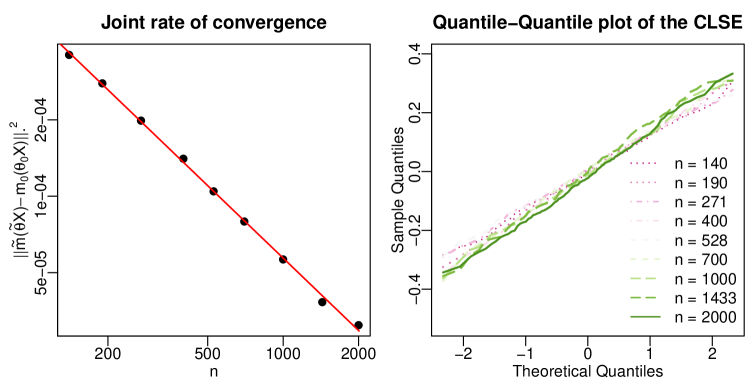

We now give an illustrative simulation example. We generate i.i.d. observations from the model: where and for increasing from to For the above model, is .666To compute the limiting variance in (4.20), we used a Monte Carlo approximation of with sample size and true . The limiting covariance matrix , where is the identity matrix and is the matrix of all ones. In the left panel of Figure 2, we present the Q-Q plot of based on 800 replications; on the -axis we have the quantiles of the standard normal distribution. The Q-Q plot validates the asymptotic normality and shows that the sample variance of the CLSE converges to the limiting variance found in Theorem 4.1. In the right panel of Figure 2, we present empirical coverages (from replications) of confidence intervals based on the CLSE constructed via (4.22).

| CLSE | ||

|---|---|---|

| Coverage | Avg Length | |

| 50 | 0.92 | 0.30 |

| 100 | 0.91 | 0.18 |

| 200 | 0.92 | 0.13 |

| 500 | 0.94 | 0.08 |

| 1000 | 0.93 | 0.06 |

5 Simulation study

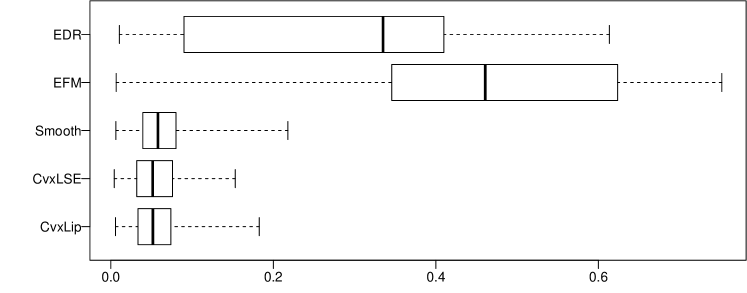

In Section S.1 of the supplementary file, we develop an alternating minimization algorithm to compute the CLSE (1.2). In this section we illustrate the finite sample performance of the CLSE using the implementation in the R package simest. . We also compare its performance with other existing estimators, namely, the EFM estimator (the estimating function method; see [12]), the EDR estimator (effective dimension reduction; see Hristache et al. [34]), and the estimator proposed in [44] with the tuning parameter chosen by generalized cross-validation ([44]; we denote this estimator by Smooth). We use CvxLip to denote the CLSE.

5.1 Another convex constrained estimator

Alongside these existing estimators, we also numerically study another natural estimator under the convexity shape constraint — the convex LSE — denoted by CvxLSE below. This estimator is obtained by minimizing the sum of squared errors subject to only the convexity constraint. Formally, the CvxLSE is

| (5.1) |

The computation of CvxLSE is discussed in Remark S.1.2 and is implemented in the R package simest. . However, theoretical analysis of this estimator is difficult because of various reasons; see Section S.14 of the supplementary file for a brief discussion. In our simulation studies we observe that the performance of CvxLSE is very similar to that of CvxLip.

In what follows, we will use to denote a generic estimator that will help us describe the quantities in the plots; e.g., we use to denote the in-sample root mean squared estimation error of , for all the estimators considered. From the simulation study it is easy to conclude that the proposed estimators have superior finite sample performance in most sampling scenarios considered.

5.2 Increasing dimension

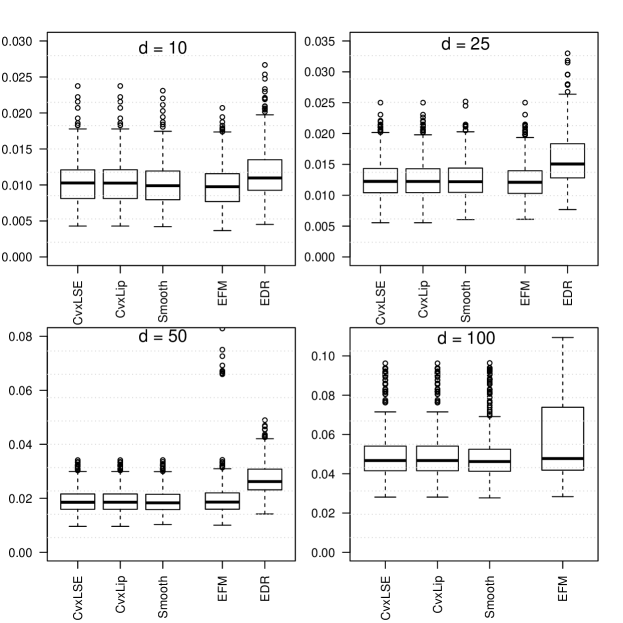

To illustrate the behavior/performance of the estimators as grows, we consider the following single index model where denotes the Student’s -distribution with degrees of freedom. In each replication we observe i.i.d. observations from the model. It is easy to see that the performance of all the estimators worsen as the dimension increases from to and EDR has the worst overall performance; see Figure 3. However when , the convex constrained estimators have significantly better performance. This simulation scenario is similar to the one considered in Example 3 of Section 3.2 in [12].

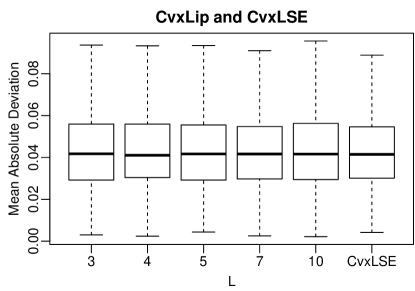

5.3 Choice of

In this subsection, we consider a simple simulation experiment to demonstrate that the finite sample performance of the CLSE is robust to the choice of tuning parameter. We generate an i.i.d. sample (of size ) from the following model:

| (5.2) |

Observe that, we have and as To understand the effect of on the performance of the CLSE, we show the box plot of as varies from to in Figure 4. Figure 4 also includes the CvxLSE which corresponds to . The plot clearly show that the performance of CvxLip is not significantly affected by the particular choice of the tuning parameter. The observed robustness in the behavior of the estimators can be attributed to the stability endowed by the convexity constraint.

6 Real data analysis

6.1 Boston housing data

We briefly recall the discussion in Example 1.1. The Boston housing dataset was collected by [32] to study the effect of different covariates on the real estate price in the greater Boston area. The dependent variable is the log-median value of homes in each of the census tracts in the Boston standard metropolitan area. Harrison and Rubinfeld [32] observed covariates and fit a linear model after taking transformation for covariates and power transformations for three other covariates; also see [82] for a discussion of this dataset.

Breiman and Friedman [6] did further analysis to deal with multi-collinearity of the covariates and selected four variables using a penalized stepwise method. The chosen covariates were: average number of rooms per dwelling (RM), full-value property-tax rate per USD (TAX), pupil-teacher ratio by town school district (PT), and proportion of population that is of “lower (economic) status” in percentage points (LS). Following [81] and [85], we take logarithms of LS and TAX to reduce sparse areas in the dataset. Furthermore, we have scaled and centered each of the covariates to have mean and variance Wang and Yang [81] fit a nonparametric additive regression model to the selected variables and obtained an (the coefficient of determination) of . Wang et al. [82] fit a single index model to this data using the set of covariates suggested in [8]. In [26], the authors create uniform confidence band for the link function and reject the null hypothesis that the link function is linear. Both in [26] and [82], the fitted link function is approximately nondecreasing and convex; see Figure 2 of [82] and Figure 5 of [26]. This motivates us to fit a nondecreasing and convex single index model to the Boston housing dataset. In particular, we consider the following estimator:

| (6.1) |

where is the set of real-valued nondecreasing functions on . Following the discussions in Remarks 3.11 and 4.4, we observe that the results in this paper also hold for . The computation of the CLSE under the additional monotonicity constraint is discussed in Remark S.1.1 and implemented in the accompanying R package.

We summarize our results in Table 1. We call , the MonotoneCLSE. In Figure 5, we plot the scatter plot of overlaid with the plot of and the regression splines based estimator of [81]. For MonotoneCLSE and CvxLip, we chose (an arbitrary but large number). We also observe that the for the monotonicity and convexity constrained (MonotoneCLSE) and just convexity constrained single index models (CvxLip and CvxLSE), when using all the available covariates, is approximately . To further understand the predictive properties of the estimators under different smoothness and shape constraints, in Table 1 we report the -fold cross-validation error averaged over 100 random partitions. The large cross-validation error for the CvxLSE is due to over-fitting of at the boundary of its support; see Figure S.1 for an illustration of this boundary effect.

6.2 Car mileage data

First, we briefly recall the discussion in Example 1.2. We consider the car mileage dataset of Donoho and Ramos [16] for a second application for the convex single index model. We model the mileage () of cars using the covariates (): displacement (Ds), weight (W), acceleration (A), and horsepower (H). Cheng et al. [11] fit a partial linear model to this this dataset, while [44] fit a single index model (without any shape constraint). The “law of diminishing returns” suggests should be convex and nonincreasing. However, the estimators based only on smoothness assumptions satisfy these shape constraints only approximately. In the right panel of Figure 5, we fit a convex and nonincreasing single index model.

We have scaled and centered each of covariates to have mean and variance for our analysis, just as in Section 6.1. We performed a test of significance for using the plug-in variance estimate in Section 4.3. The covariates A, Ds, and H were found to be significant and each of them had -value less than . In the right panel of Figure 5, we have the scatter plot of overlaid with the plot of and regression splines based estimator obtained in [81]; here is defined as in (6.1) but now denotes the class of real-valued nonincreasing functions on . Table 1 lists different estimators for and their respective and cross-validation errors.

Method Boston Data Car mileage data \bigstrut RM PT CV-error Ds W A H CV-error LM777LM denotes the linear regression model. 2.34 0.73 20.75 0.71 18.61 Smooth 0.44 0.77 17.80 0.42 0.18 0.11 0.88 0.76 15.29 MonotoneCLSE 0.49 0.80 17.93 0.44 0.17 0.13 0.87 0.76 15.34 CvxLip 0.48 0.80 17.93 0.44 0.18 0.12 0.87 0.76 15.22 CvxLSE 0.43 0.80 21.44 0.39 0.14 0.12 0.90 0.77 16.38 EFM 0.48 — — 0.44 0.18 0.13 0.87 — — EDR 0.44 — — 0.33 0.11 0.15 0.93 — —

7 Discussion

In this paper we have proposed and studied a Lipschitz constrained LSE in the convex single index model. Our estimator of the regression function is minimax rate optimal (Proposition S.6.1) and the estimator of the index parameter is semiparametrically efficient when the errors happen to be homoscedastic (Theorem 4.1). This work represents the first in the literature of semiparametric efficiency of the LSE when the nonparametric function estimator is non-smooth and parameters are bundled. Our proof of semiparametric efficiency is geometric and provides a general framework that can be used to prove efficiency of estimators in a wide variety of semiparametric models even when the estimators do not satisfy the efficient score equation directly; see sketch of proof of Theorem 4.1 and Example 4.5 in Section 4.2.

Theorem 3.2 proves the worst case rate of convergence for the CLSE. It is well-known in convex regression that if the true regression function is piecewise linear, then the LSE converges at a much faster (near parametric) rate [29]. This behavior is called the adaptation property of the LSE. It is natural to wonder if such a property also holds for . In Section S.4.3 of the supplementary file, we investigate the behavior of and (as sample size increases) when is piecewise linear. The simulation suggests that converges at a near parametric rate when is piecewise linear. However a formal proof of this is beyond the scope of this paper as it requires different techniques. Furthermore, the asymptotic behavior of in this setting is an open problem.

References

- Aït-Sahalia and Duarte [2003] Aït-Sahalia, Y. and J. Duarte (2003). Nonparametric option pricing under shape restrictions. J. Econometrics 116(1-2), 9–47.

- Alonso and Brambila-Paz [1998] Alonso, A. and F. Brambila-Paz (1998). Lp-continuity of conditional expectations. Journal of mathematical analysis and applications 221(1), 161–176.

- Balabdaoui et al. [2019] Balabdaoui, F., C. Durot, and H. Jankowski (2019). Least squares estimation in the monotone single index model. Bernoulli 25(4B), 3276–3310.

- Balabdaoui et al. [2019] Balabdaoui, F., P. Groeneboom, and K. Hendrickx (2019). Score estimation in the monotone single-index model. Scandinavian Journal of Statistics 46(2), 517–544.

- Bogachev [2007] Bogachev, V. I. (2007). Measure theory. Vol. I, II. Springer-Verlag, Berlin.

- Breiman and Friedman [1985] Breiman, L. and J. H. Friedman (1985). Estimating optimal transformations for multiple regression and correlation. 80(391), 580–598.

- Carroll et al. [1997] Carroll, R. J., J. Fan, I. Gijbels, and M. P. Wand (1997). Generalized partially linear single-index models. Journal of the American Statistical Association 92(438), 477–489.

- Chen and Li [1998] Chen, C.-H. and K.-C. Li (1998). Can SIR be as popular as multiple linear regression? Statist. Sinica 8(2), 289–316.

- Chen and Plemmons [2010] Chen, D. and R. J. Plemmons (2010). Nonnegativity constraints in numerical analysis. In The birth of numerical analysis, pp. 109–139. World Sci. Publ., Hackensack, NJ.

- Chen and Samworth [2016] Chen, Y. and R. J. Samworth (2016). Generalized additive and index models with shape constraints. J. R. Stat. Soc. Ser. B. Stat. Methodol. 78(4), 729–754.

- Cheng et al. [2012] Cheng, G., Y. Zhao, and B. Li (2012). Empirical likelihood inferences for the semiparametric additive isotonic regression. J. Multivariate Anal. 112, 172–182.

- Cui et al. [2011] Cui, X., W. K. Härdle, and L. Zhu (2011). The EFM approach for single-index models. Ann. Statist. 39(3), 1658–1688.

- Delecroix et al. [2006] Delecroix, M., M. Hristache, and V. Patilea (2006). On semiparametric m-estimation in single-index regression. Journal of Statistical Planning and Inference 136(3), 730–769.

- Dharanipragada and Arun [1996] Dharanipragada, S. and K. Arun (1996). A quadratically convergent algorithm for convex-set constrained signal recovery. IEEE transactions on signal processing 44(2), 248–266.

- Dirksen [2015] Dirksen, S. (2015). Tail bounds via generic chaining. Electron. J. Probab. 20, no. 53, 1–29.

- Donoho and Ramos [1983] Donoho, D. and E. Ramos (1983). Cars dataset–1983 asa data exposition dataset. http://lib.stat.cmu.edu/datasets/cars.data.

- Dümbgen et al. [2004] Dümbgen, L., S. Freitag, and G. Jongbloed (2004). Consistency of concave regression with an application to current-status data. Math. Methods Statist. 13(1), 69–81.

- Dümbgen et al. [2013] Dümbgen, L., R. J. Samworth, and D. Schuhmacher (2013). Stochastic search for semiparametric linear regression models. In From Probability to Statistics and Back: High-Dimensional Models and Processes–A Festschrift in Honor of Jon A. Wellner, pp. 78–90. Institute of Mathematical Statistics.

- Durrett [2010] Durrett, R. (2010). Probability: theory and examples (Fourth ed.). Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge.

- Fitzpatrick and Phelps [1982] Fitzpatrick, S. and R. R. Phelps (1982). Differentiability of the metric projection in hilbert space. Transactions of the American Mathematical Society 270(2), 483–501.

- Gaïffas and Lecué [2007] Gaïffas, S. and G. Lecué (2007). Optimal rates and adaptation in the single-index model using aggregation. Electron. J. Stat. 1, 538–573.

- Ganti et al. [2015] Ganti, R., N. Rao, R. M. Willett, and R. Nowak (2015). Learning single index models in high dimensions. arXiv preprint arXiv:1506.08910.

- Giné et al. [2000] Giné, E., R. Latał a, and J. Zinn (2000). Exponential and moment inequalities for -statistics. In High dimensional probability, II (Seattle, WA, 1999), Volume 47 of Progr. Probab., pp. 13–38. Birkhäuser Boston, Boston, MA.

- Giné and Nickl [2016] Giné, E. and R. Nickl (2016). Mathematical foundations of infinite-dimensional statistical models. Cambridge Series in Statistical and Probabilistic Mathematics, [40]. Cambridge University Press, New York.

- Groeneboom and Hendrickx [2018] Groeneboom, P. and K. Hendrickx (2018). Current status linear regression. The Annals of Statistics 46(4), 1415–1444.

- Gu and Yang [2015] Gu, L. and L. Yang (2015). Oracally efficient estimation for single-index link function with simultaneous confidence band. Electronic Journal of Statistics 9(1), 1540–1561.

- Guntuboyina and Sen [2013] Guntuboyina, A. and B. Sen (2013). Covering numbers for convex functions. Information Theory, IEEE Transactions on 59(4), 1957–1965.

- Guntuboyina and Sen [2015] Guntuboyina, A. and B. Sen (2015). Global risk bounds and adaptation in univariate convex regression. Probab. Theory Related Fields 163(1-2), 379–411.

- Guntuboyina and Sen [2018] Guntuboyina, A. and B. Sen (2018). Nonparametric shape-restricted regression. Statist. Sci. 33(4), 568–594.

- Han and Wellner [2018] Han, Q. and J. A. Wellner (2018). Robustness of shape-restricted regression estimators: an envelope perspective. ArXiv e-prints arxiv:1805.02542.

- Härdle et al. [1993] Härdle, W., P. Hall, and H. Ichimura (1993). Optimal smoothing in single-index models. Ann. Statist. 21(1), 157–178.

- Harrison and Rubinfeld [1978] Harrison, D. and D. L. Rubinfeld (1978). Hedonic housing prices and the demand for clean air. Journal of environmental economics and management 5(1), 81–102.

- Horowitz [1998] Horowitz, J. L. (1998). Semiparametric methods in econometrics, Volume 131 of Lecture Notes in Statistics. Springer-Verlag, New York.

- Hristache et al. [2001] Hristache, M., A. Juditsky, and V. Spokoiny (2001). Direct estimation of the index coefficient in a single-index model. Ann. Statist. 29(3), 595–623.

- Huang [1996] Huang, J. (1996). Efficient estimation for the proportional hazards model with interval censoring. Ann. Statist. 24(2), 540–568.

- Huang and Wellner [1997] Huang, J. and J. A. Wellner (1997). Interval censored survival data: a review of recent progress. In Proceedings of the First Seattle Symposium in Biostatistics, pp. 123–169.

- Ichimura [1993] Ichimura, H. (1993). Semiparametric least squares (SLS) and weighted SLS estimation of single-index models. J. Econometrics 58(1-2), 71–120.

- Kakade et al. [2011] Kakade, S. M., V. Kanade, O. Shamir, and A. Kalai (2011). Efficient learning of generalized linear and single index models with isotonic regression. In Advances in Neural Information Processing Systems, pp. 927–935.

- Kalai and Sastry [2009] Kalai, A. T. and R. Sastry (2009). The isotron algorithm: High-dimensional isotonic regression. In COLT.

- Keshavarz et al. [2011] Keshavarz, A., Y. Wang, and S. Boyd (2011). Imputing a convex objective function. In 2011 IEEE International Symposium on Intelligent Control, pp. 613–619. IEEE.

- Klaassen [1987] Klaassen, C. A. J. (1987). Consistent estimation of the influence function of locally asymptotically linear estimators. Ann. Statist. 15(4), 1548–1562.

- Kosorok [2008] Kosorok, M. R. (2008). Introduction to empirical processes and semiparametric inference. Springer Series in Statistics. Springer, New York.

- Kuchibhotla and Chakrabortty [2018] Kuchibhotla, A. K. and A. Chakrabortty (2018). Moving beyond sub-gaussianity in high-dimensional statistics: Applications in covariance estimation and linear regression. arXiv preprint arXiv:1804.02605.

- Kuchibhotla and Patra [2016a] Kuchibhotla, A. K. and R. K. Patra (2016a). Efficient estimation in single index models through smoothing splines. arXiv preprint arXiv:1612.00068.

- Kuchibhotla and Patra [2016b] Kuchibhotla, A. K. and R. K. Patra (2016b). simest: Single Index Model Estimation with Constraints on Link Function. R package version 0.4.

- Kuchibhotla and Patra [2019] Kuchibhotla, A. K. and R. K. Patra (2019). On least squares estimation under heteroscedastic and heavy-tailed errors.

- Lawson and Hanson [1974] Lawson, C. L. and R. J. Hanson (1974). Solving least squares problems. Prentice-Hall, Inc., Englewood Cliffs, N.J. Prentice-Hall Series in Automatic Computation.

- Ledoux and Talagrand [2011] Ledoux, M. and M. Talagrand (2011). Probability in Banach spaces. Classics in Mathematics. Springer-Verlag, Berlin. Isoperimetry and processes, Reprint of the 1991 edition.

- Lepski and Spokoiny [1997] Lepski, O. V. and V. G. Spokoiny (1997). Optimal pointwise adaptive methods in nonparametric estimation. The Annals of Statistics, 2512–2546.

- Li and Duan [1989] Li, K.-C. and N. Duan (1989). Regression analysis under link violation. Ann. Statist. 17(3), 1009–1052.

- Li and Racine [2007] Li, Q. and J. S. Racine (2007). Nonparametric econometrics. Princeton University Press, Princeton, NJ. Theory and practice.

- Li and Patilea [2017] Li, W. and V. Patilea (2017). A new minimum contrast approach for inference in single-index models. Journal of Multivariate Analysis 158, 47–59.

- Lim [2014] Lim, E. (2014). On convergence rates of convex regression in multiple dimensions. INFORMS Journal on Computing 26(3), 616–628.

- Lin and Kulasekera [2007] Lin, W. and K. B. Kulasekera (2007). Identifiability of single-index models and additive-index models. Biometrika 94(2), 496–501.

- Ma and Zhu [2013] Ma, Y. and L. Zhu (2013). Doubly robust and efficient estimators for heteroscedastic partially linear single-index models allowing high dimensional covariates. J. R. Stat. Soc. Ser. B. Stat. Methodol. 75(2), 305–322.

- Massart [1990] Massart, P. (1990). The tight constant in the dvoretzky-kiefer-wolfowitz inequality. The annals of Probability, 1269–1283.

- Matzkin [1991] Matzkin, R. L. (1991). Semiparametric estimation of monotone and concave utility functions for polychotomous choice models. Econometrica 59(5), 1315–1327.

- Mazumder et al. [2019] Mazumder, R., A. Choudhury, G. Iyengar, and B. Sen (2019). A computational framework for multivariate convex regression and its variants. Journal of the American Statistical Association 114(525), 318–331.

- McCormick and Tapia [1972] McCormick, G. and R. Tapia (1972). The gradient projection method under mild differentiability conditions. SIAM Journal on Control 10(1), 93–98.

- Murphy and van der Vaart [2000] Murphy, S. A. and A. W. van der Vaart (2000). On profile likelihood. J. Amer. Statist. Assoc. 95(450), 449–485.

- Murphy et al. [1999] Murphy, S. A., A. W. van der Vaart, and J. A. Wellner (1999). Current status regression. Math. Methods Statist. 8(3), 407–425.

- Newey [1990] Newey, W. K. (1990). Semiparametric efficiency bounds. Journal of applied econometrics 5(2), 99–135.

- Newey and Stoker [1993] Newey, W. K. and T. M. Stoker (1993). Efficiency of weighted average derivative estimators and index models. Econometrica 61(5), 1199–1223.

- Pollard [1990] Pollard, D. (1990). Empirical processes: theory and applications. NSF-CBMS Regional Conference Series in Probability and Statistics, 2. Institute of Mathematical Statistics, Hayward, CA; American Statistical Association, Alexandria, VA.

- Powell et al. [1989] Powell, J. L., J. H. Stock, and T. M. Stoker (1989). Semiparametric estimation of index coefficients. Econometrica 57(6), 1403–1430.

- Samworth and Yuan [2012] Samworth, R. J. and M. Yuan (2012). Independent component analysis via nonparametric maximum likelihood estimation. Ann. Statist. 40(6), 2973–3002.

- Seijo and Sen [2011] Seijo, E. and B. Sen (2011). Nonparametric least squares estimation of a multivariate convex regression function. Ann. Statist. 39(3), 1633–1657.

- Shapiro [1994] Shapiro, A. (1994). Existence and differentiability of metric projections in hilbert spaces. SIAM Journal on Optimization 4(1), 130–141.

- Sokolowski and Zolesio [1992] Sokolowski, J. and J.-P. Zolesio (1992). Shape sensitivity analysis of variational inequalities. In Introduction to Shape Optimization, pp. 163–239. Springer.

- Song [2014] Song, K. (2014). Semiparametric models with single-index nuisance parameters. Journal of Econometrics 178, 471–483.

- Talagrand [2014] Talagrand, M. (2014). Upper and lower bounds for stochastic processes, Volume 60 of Ergebnisse der Mathematik und ihrer Grenzgebiete. 3. Folge. A Series of Modern Surveys in Mathematics [Results in Mathematics and Related Areas. 3rd Series. A Series of Modern Surveys in Mathematics]. Springer, Heidelberg. Modern methods and classical problems.

- Tsiatis [2006] Tsiatis, A. A. (2006). Semiparametric theory and missing data. Springer Series in Statistics. Springer, New York.

- Tsybakov [2009] Tsybakov, A. B. (2009). Introduction to nonparametric estimation. Springer Series in Statistics. Springer, New York. Revised and extended from the 2004 French original, Translated by Vladimir Zaiats.

- van de Geer and Lederer [2013] van de Geer, S. and J. Lederer (2013). The Bernstein-Orlicz norm and deviation inequalities. Probab. Theory Related Fields 157(1-2), 225–250.

- Van de Geer [2000] Van de Geer, S. A. (2000). Applications of empirical process theory, Volume 6 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge: Cambridge University Press.

- van der Vaart [2002] van der Vaart, A. (2002). Semiparametric statistics. In Lectures on probability theory and statistics (Saint-Flour, 1999), Volume 1781 of Lecture Notes in Math., pp. 331–457.

- van der Vaart and Wellner [1996] van der Vaart, A. W. and J. A. Wellner (1996). Weak convergence and empirical processes. Springer Series in Statistics. Springer-Verlag, New York. With applications to statistics.

- Varian [1984] Varian, H. R. (1984). The nonparametric approach to production analysis. Econometrica 52(3), 579–597.

- Wainwright [2019] Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, Volume 48. Cambridge University Press.

- Wang and Wang [2015] Wang, G. and L. Wang (2015). Spline estimation and variable selection for single-index prediction models with diverging number of index parameters. Journal of Statistical Planning and Inference 162, 1–19.

- Wang and Yang [2009] Wang, J. and L. Yang (2009). Efficient and fast spline-backfitted kernel smoothing of additive models. Ann. Inst. Statist. Math. 61(3), 663–690.

- Wang et al. [2010] Wang, J.-L., L. Xue, L. Zhu, and Y. S. Chong (2010). Estimation for a partial-linear single-index model. Ann. Statist. 38(1), 246–274.

- Wen and Yin [2013] Wen, Z. and W. Yin (2013). A feasible method for optimization with orthogonality constraints. Math. Program. 142(1-2, Ser. A), 397–434.

- Xia et al. [2002] Xia, Y., H. Tong, W. Li, and L.-X. Zhu (2002). An adaptive estimation of dimension reduction space. J. R. Stat. Soc. Ser. B. Stat. Methodol. 64(3), 363–410.

- Yu et al. [2011] Yu, K., E. Mammen, and B. U. Park (2011). Semi-parametric regression: efficiency gains from modeling the nonparametric part. Bernoulli 17(2), 736–748.

- Yuan [2011] Yuan, M. (2011). On the identifiability of additive index models. Statistica Sinica, 1901–1911.

section1em2.5em \cftsetindentssubsection1.5em3em

Supplement to “Semiparametric Efficiency in Convexity Constrained Single Index Model”

section.S.1 subsection.S.1.1 subsection.S.1.2 section.S.2 section.S.3 section.S.4 subsection.S.4.1 subsection.S.4.2 subsection.S.4.3 section.S.5 subsection.S.5.1 subsection.S.5.2 section.S.6 section.S.7 section.S.8 subsection.S.8.1 section.S.9 subsection.S.9.1 subsection.S.9.2 subsection.S.9.3 subsection.S.9.4 subsection.S.9.5 subsection.S.9.6 subsection.S.9.7 section.S.10 subsection.S.10.1 subsection.S.10.2 section.S.11 subsection.S.11.1 subsection.S.11.2 section.S.12 subsection.S.12.1 subsection.S.12.2 section.S.13 section.S.14

S.1 Alternating minimization algorithm

In this section we describe an algorithm for computing the estimator defined in (1.2). As mentioned in Remark 3.1, the minimization of the desired loss function for a fixed is a convex optimization problem; see Section S.1.1 below for more details. With the above observation in mind, we propose the following general alternating minimization algorithm to compute the proposed estimator. The algorithms discussed here are implemented in our R package simest [45].

We first introduce some notation. Let denote a nonnegative criterion function, e.g., . And suppose, we are interested in finding the minimizer of over , e.g., in our case is . For every , let us define

| (E.1) |

Here, we have assumed that for every , has a unique minimizer in and exists. The general alternating scheme is described in Algorithm 1.

Note that, our assumptions on does not imply that is a convex function. In fact in our case the “profiled” criterion function is not convex. Thus the algorithm discussed above is not guaranteed to converge to a global minimizer. However, the algorithm guarantees that the criterion value is nonincreasing over iterations, i.e., for all To lessen the chance of getting stuck at a local minima, we use multiple random starts for in Algorithm 1. Further, following the idea of [18], we use other existing -consistent estimators of as warm starts; see Section 5 for examples of such estimators. In the following section, we discuss an algorithm to compute , when and .

S.1.1 Strategy for estimating the link function

In this subsection, we describe an algorithm to compute as defined in (E.1). We use the following notation. Fix an arbitrary . Let represent the vector with sorted entries so that . Without loss of generality, let represent the vector of responses corresponding to the sorted .

When , we consider the problem of minimizing over . Note that the loss depends only on the values of the function at the ’s and the minimizer is only unique at the data points. Hence, in the following we identify and interpolate/extrapolate the function linearly between and outside the data points; see footnote 3. Consider the general problem of minimizing

for some positive definite matrix . In most cases is the identity matrix; see Section S.13 of the supplementary file for other possible scenarios. Here denotes the square root of the matrix which can be obtained by Cholesky factorization.

The Lipschitz constraint along with convexity (i.e., ) reduces to imposing the following linear constraints:

| (E.2) |

In particular, the minimization problem at hand can be represented as

| (E.3) |

for and written so as to represent (E.2). It is clear that the entries of involve . If the minimum difference is close to zero, then the minimization problem (E.3) is ill-conditioned and can lead to numerical inaccuracies. For this reason, in the implementation we have added a pre-binning step in our implementation; see Section S.13 of the supplementary for details.

Remark S.1.1 (Additional monotonicity assumption).

Note that if is additionally monotonically nondecreasing, then

where is the zero vector of dimension , with and all other entries of are zero. Thus, the problem of estimating convex Lipschitz function that is additionally monotonically nondecreasing can also be reduced to problem (E.3) with another matrix and vector .

In the following we reduce the optimization problem (E.3) to a nonnegative least squares problem, which can then be solved efficiently using the nnls package in R. Define , so that . Using this, we have if and only if Thus, (E.3) is equivalent to

| (E.4) |

where and An equivalent formulation is

| (E.5) |

Here represents coordinate-wise inequality. A proof of this equivalence can be found in Lawson and Hanson [47, page 165]; see [9] for an algorithm to solve (E.5).

If denotes the solution of (E.5) then the solution of (E.4) is given as follows. Define . Then , the minimizer of (E.4), is given by 999Note that (E.4) is a Least Distance Programming (LDP) problem and Lawson and Hanson [47, page 167] prove that cannot be zero in an LDP with a feasible constraint set.. Hence the solution to (E.3) is given by .

Remark S.1.2.

Recall, the CvxLSE defined in (5.1). The CvxLSE can be computed via Algorithm 1 with . To compute in Step 1 of Algorithm 1, we can use strategy developed in Section S.1.1 with (E.2) replaced by the following set of linear constraints:

| (E.6) |

Similar to the CLSE, this reduces the computation of (for a given ) to solving a quadratic program with linear inequalities; see Section S.1.1. The algorithm for computing developed below works for both CvxLip and CvxLSE.

S.1.2 Algorithm for computing

In this subsection we describe an algorithm to find the minimizer of over . Recall that is defined to be the “positive” half of the unit sphere, a dimensional manifold in . Treating this problem as minimization over a manifold, one can apply a gradient descent algorithm by moving along a geodesic; see e.g., Samworth and Yuan [66, Section 3.3]. But it is computationally expensive to move along a geodesic and so we follow the approach of [83] wherein we move along a retraction with the guarantee of descent. To explain the approach of [83], let us denote the objective function by , i.e., in our case . Let be an initial guess for and define

where denotes the gradient operator. Next we choose the path where

for , and find a choice of such that is as much smaller than as possible; see step 2 of Algorithm 1. It is easy to verify that

see Lemma 3 of [83]. This implies that is a nonincreasing function in a neighborhood of . Recall that for every , (the first coordinate of ) is nonnegative. For to lie in , has to satisfy the following inequality

| (E.7) |

where and represent the first coordinates of the vectors and , respectively. This implies that a valid choice of must lie between the zeros of the quadratic expression on the left hand side of (E.7), given by

Note that this interval always contains zero. Now we can perform a simple line search for , where is in the above mentioned interval, to find . We implement this step in the R package simest.

S.2 Main components in the proof of Theorem 4.1

-

Step 1

In Theorem S.11.1 we show that is approximately unbiased in the sense of [76], i.e.,

(E.1) Similar conditions have appeared before in proofs of asymptotic normality of maximum likelihood estimators (e.g., see [35]) and the construction of efficient one-step estimators (see [41]). The above condition essentially ensures that is a good “approximation” to ; see Section 3 of [60] for further discussion.

- Step 2

-

Step 3

To complete the proof, it is now enough to show that

(E.4) A proof of (E.4) can be found in the proof of Theorem 6.20 in [76]; also see Kuchibhotla and Patra [44, Section 10.4]. Lemma S.12.3 in Section S.12.2 of the supplementary file proves that satisfy the required conditions of Theorem 6.20 in [76].

Observe that (E.3) and (E.4) imply

| (E.5) | ||||

The proof of the theorem will be complete, if we can show that

the proof of which can be found in Step 4 of Theorem 5 in [44].

S.3 Uniqueness of the limiting variances in Theorem 4.1

Observe that the variance of the limiting distribution (for both the heteroscedastic and homoscedastic error models) is singular. This can be attributed to the fact that is a Stiefel manifold of dimension and has an empty interior in

In Lemma S.3.1 below, we show that the limiting variances are unique, i.e., they do not depend on the particular choice of . In fact matches the lower bound obtained in [63] for the single index model under only smoothness constraints.

Lemma S.3.1.

Suppose the assumptions of Theorem 4.1 hold, then the matrix is the unique Moore-Penrose inverse of

| (E.1) |

Proof.

Recall that

| (E.2) |

For the rest of the proof, define

| (E.3) |

In the following, we show that is the Moore-Penrose inverse of By definition, it is equivalent to show that

| (E.4) |

Proof of : We will now show that , an equivalent condition is that is idempotent and . Observe that is idempotent because,

| (E.5) |

Note that Thus . However,

Thus Thus to prove it enough to show that . We will prove that the nullspace of is the same as that of . Since implies that , it follows that

We will now prove the reverse inclusion by contradiction. Suppose there exists a vector such that and Set . Then we have that . Thus by Lemma 1 of [44], we have that for some constant . (If , then , a contradiction). This implies that there exists such that or in particular , since . This, however, is a contradiction since is symmetric and

| (E.6) | ||||

Proof of : It is easy to see that

| (E.7) |

Proof of :

| (E.8) |

as is a symmetric matrix. Recall that and the columns of are orthogonal to . Thus let us define , by adding as an additional column to , i.e., . Recall that by definition of , and (E.6), we have that . Multiplying by on the left and on the right we have,

| (E.9) | ||||

Multiplying by on the left and on the right we have,

| (E.10) | ||||

here the second equality is true, since Thus, . Since is a nonsingular matrix, we have that Proof of follows similarly. ∎

S.4 Additional simulation studies

S.4.1 A simple model

In this section we give a simple illustrative (finite sample) example. We observe i.i.d. observations from the following homoscedastic model:

| (E.1) |

In Figure S.1, we have a scatter plot of overlaid with prediction curves for the proposed estimators obtained from one sample from (E.1). Table 2 displays all the corresponding estimates of obtained from the same data set. To compute the function estimates for EFM and EDR approaches we used cross-validated smoothing splines to estimate the link function using their estimates of .

| Method | Theta Error | Func Error | Est Error | |||||

|---|---|---|---|---|---|---|---|---|

| Truth | 0.45 | 0.45 | 0.45 | 0.45 | 0.45 | — | — | — |

| Smooth | 0.38 | 0.49 | 0.41 | 0.50 | 0.45 | 0.21 | 0.10 | 0.10 |

| CvxLip | 0.35 | 0.50 | 0.43 | 0.48 | 0.46 | 0.21 | 0.13 | 0.15 |

| CvxLSE | 0.36 | 0.50 | 0.43 | 0.45 | 0.48 | 0.20 | 0.18 | 0.15 |

| EFM | 0.35 | 0.49 | 0.41 | 0.49 | 0.47 | 0.24 | 0.10 | 0.11 |