On a robust risk measurement approach for capital determination errors minimization

Abstract

We propose a robust risk measurement approach that minimizes the expectation of overestimation plus underestimation costs. We consider uncertainty by taking the supremum over a collection of probability measures, relating our approach to dual sets in the representation of coherent risk measures.

We provide results that guarantee the existence of a solution and explore the properties of minimizer and minimum as risk and deviation measures, respectively. An empirical illustration is carried out to demonstrate the use of our approach in capital determination.

Keywords: Uncertainty modeling; risk measures; deviation measures; capital determination.

1 Introduction

The interest in risk measures with interpretation as capital determination from a theoretical point of view has been raised in mathematical finance and insurance since the seminal paper of Artzner et al. (1999). From there, an entire stream of literature has proposed and discussed distinct features, including axiom sets, dual representations, mathematical and statistical properties. We suggest Föllmer and Weber (2015) and Föllmer and Schied (2016) for a recent review of this theory. See Emmer et al. (2015) for a discussion and comparison of properties of popular risk measures, which include variance, Value at Risk (VaR), Expected Shortfall (ES), and Expectile Value at Risk (EVaR).

Despite the investigations carried out in this regard, there is still no consensus about a definitive set of properties or the best risk measure for practical matters. In this context, there is scope for proposing new risk measurement approaches, such as Righi and Ceretta (2016), Furman et al. (2017), Righi (2019a), Bellini et al. (2019) and Pichler and Schlotter (2020). A possible interesting risk measurement process could seek to minimize capital determination errors to reduce the costs linked to it. From the regulatory point of view, risk underestimation, and consequently capital determination underestimation, is the main concern. In this case, capital charges are desirable to avoid costs from unexpected and uncovered losses. However, from the perspective of institutions, it is also desirable to reduce the regret costs arising from risk overestimation because the latter reduces profitability.

Based on this perspective, we propose a risk measurement procedure that represents the capital determination for a financial position that minimizes the expected value of the sum between costs from risk overestimation (regret for lesser profits) and underestimation (uncovered losses). We measure these two costs in our framework by positive random variables , for gains, and , for losses. These costs may refer, for instance, to financial rates traded in the market or even as a function of variables of interest. Typically, such costs can be interpreted as the cost of opportunity measured by the rate of a similar investment or even risk free rate of the exceeding capital, in the case of , and the cost of raising money, by borrowing from bank or other debt sources, in the case of underestimation to cover an unexpected loss, in the case of . More specifically, our goal is to minimize for the expectation of . The term represents a situation where the realized outcome of is better than the capital requirement and the surplus could be invested at cost . Similarly, relates to a situation where the capital reserve is not enough to cover the loss, where the difference must be raised at cost .

Thus, in this paper we have four contributions to both academic literature and the financial industry:

-

(i)

The type of loss function we consider has not been considered for such purpose. In this sense, Laeven and Goovaerts (2004) and Goovaerts et al. (2005) explore a loss function more similar to . Dhaene et al. (2003), Goovaerts et al. (2005), and Goovaerts et al. (2010) present, even briefly, a loss function similar to . It is worth to mention also the works of Zaks et al. (2006), Dhaene et al. (2012), Xu and Hu (2012), and Xu and Mao (2013), among other research on this topic. Such studies also focus on minimizing the mentioned costs in order to obtain the optimal amount of capital. The term is the cost of putting aside the initial capital instead of investing it in a financial instrument with returns payoff , which is not a random variable in these studies. This is distinct to regret or overestimation costs as in our framework since has not its realization known a priori. In our case, we penalize regret costs only the exceeding value over capital determination. Thus, our focus is more on risk measurement errors. If the determined capital (risk measure) is precisely the monetary value that we need to cover the loss, then there is no reason for penalization. On the other hand, most of these works focus on determining the optimal composition for aggregated capital of a financial firm from its business units. We emphasize that such approaches are originally proposed to determine economic capital for insurance analysis.

-

(ii)

We provide results that guarantee a solution for the optimization problem linked to our risk measure, develop properties that it fulfills, and characterize the resulting minimum cost as a deviation measure in the sense of Rockafellar et al. (2006). In this sense, our approach considers a risk measure that has random variables, the costs and , as parameters. With very few exceptions, such as the maximal correlation risk measure in Rüschendorf (2006), parameters for risk measures are real numbers. This is the case of VaR and ES, for instance, where the quantile significance level is the parameter. In fact, when and , our risk measure coincides with VaR, and its related minimum is a scaled ES deviation from the expectation. This kind of generalization leads to technical difficulties we handle, such as dependence between the financial position and costs and . The paper of Rockafellar and Uryasev (2013) relates to risk and deviation measures linked by a common optimization problem but does not consider random variables as parameters. Bellini et al. (2014) study generalized quantiles as risk measures by minimizing asymmetric loss functions but also do not consider random variables as parameters.

-

(iii)

Our approach is robust in the sense we consider a supremum of probability measures over our optimization problem. This is a worst case approach, where the functionals are not sensitive to the choice of some specific probability measure that represents a particular belief about the world. In this sense, we are in concordance to the stream of Shapiro (2017), Righi (2019b), Bellini et al. (2018), and Guo and Xu (2019). Nonetheless, none of them consider the same features we address in our study, such as random variables as parameters and the minimum as a deviation. Moreover, we relate our approach with the dual representation of coherent risk measures, since we are based on a supremum of expectations over probabilities. For model risk purposes, Cont (2006) uses this dual representation scheme for robust expectations regarding pricing contingent claims.

-

(iv)

We provide an illustration considering real financial data with the purpose of showing the practical usefulness of our approach. In this sense, we perform an adaptation of the dual representation of usual discrete probability spaces. We then consider capital requirements determined by our risk measures against usual risk measures applied for this purpose. Results allow us to conclude that capital determination based on typical tail risk measures that the Basel and Solvency accords recommend and by risk measures that also focus on minimizing capital costs that are too punitive, lead to more costs concerning risk measures obtained from our approach.

Regarding structure, the remainder of this paper divides in the following contents: in Section 2 we expose definitions and results regarding the existence of solutions to the optimization problems in our proposed approach; in Section 3 we prove results regarding the properties of our risk and deviation measures in relation to financial positions and costs for capital determination errors; in Section 4 we exhibit an empirical illustration of our approach for capital determination; in Section 5 we summarize and conclude the paper.

2 Proposed approach

The content is based on the following notations. Consider the real valued random result of any asset ( is a gain, is a loss) that is defined on a probability space . All equalities and inequalities are considered almost surely in . We define , , and as the indicator function for an event .

We let denote the set composed of probability measures defined on that are absolutely continuous with respect to , with Radon-Nikodym derivative and a non-empty set. Moreover, , and are, respectively, the expected value, the distribution function and the (left) quantile of under . We drop the subscript when it is regarding .

Let be the vector space of (equivalent classes of) bounded random variables. We write . We have that and are its cones of non-negative and positive elements, respectively. We denote by convergence in the essential supremum norm, while means -a.s. convergence.

We recurrently use the following facts for any without further mention:

-

•

.

-

•

and , .

-

•

if is continuous, then also is .

-

•

if or regarding , then the same is true concerning for any and .

We now define our risk measurement approach as the supremum of minimization problems regarding costs from capital determination errors.

Definition 1.

Let . Then:

-

(i)

Our risk measure is a functional defined as:

(1) -

(ii)

Our deviation measure is a functional defined as:

(2)

The negative sign for is to keep the pattern for losses. Moreover, in Propositions 4 and 5 we prove that our both functionals are in fact finite and, thus, well-defined. It would also be interesting to extend our results to general loss functions , with and beyond the identity function as in Bellini et al. (2014). We do not pursue this goal because we want to keep the intuitive meaning of our specific loss function.

Remark 1.

A recently highlighted statistical property is Elicitability, which enables the comparison of competing models in risk forecasting. See Ziegel (2016) and the references therein for more details. A functional is elicitable if it is the argmin for expectation of some score function and satisfies certain properties. For instance, mean and -quantile are elicitable under scores and , respectively. However our functionals are not fitted in this class because costs and are random variables that are not necessarily functions of the position . A possibility could be to consider a score function defined as with holding certain properties. However, we do not pursue such framework since our focus is precisely into considering and as general random variables that are not strictly dependent to .

Remark 2.

It is straightforward that for any and any . It would be possible to develop our theory by considering the domain of both and as the vector space of -integrable random variables since this is a larger space. In such case, we would have to restrict ourselves to probability measures with -a.s. bounded Radon-Nikodym derivatives, i.e., . Such technicality is in order to guarantee integrability since for any under these conditions we have from Hölder inequality that

which is finite. Most results we expose are easily adaptable to such framework.

We now expose a formal result that guarantees our minimization problems have a solution. Note that for , and for . Thus, the minimization problem would not be altered when we take optimization over the compact interval instead of the whole real line because we consider random variables in .

Proposition 1.

Under notation of Definition 1, let . Then for each :

-

(i)

is a closed interval.

-

(ii)

if and only if satisfies the first order condition given by

-

(iii)

if is continuous in , then is a singleton if and only if is strictly increasing in .

Proof.

Fix . Then:

-

(i)

Let be defined as . Clearly, is finite, due to Remark 2, convex and, hence a continuous function. Note that is proper and level bounded. Thus, is finite and the set is non-empty and compact. Moreover, since is convex, is an interval.

-

(ii)

We have to solve the first order condition for in order to obtain the argument that minimizes the expression. Note that is convex. Then is a minimizer if and only if

Thus, we have from Dominated convergence that both

and

By taking and , we get the claim.

-

(iii)

Note that when is continuous in we have . Then, the first order condition of (ii) is equivalent to , which can be rewritten as . For the if part, assume that there exist and , i.e., is not a singleton. Since is strictly increasing in , we get that and, thus, . Now, from we have . Therefore,

Thus, does not fulfill the first order condition, a contradiction. The reasoning is analogous for . Hence, is a singleton, as desired. For the only if part, let and be continuous in but constant in some half ball with radius around , i.e., is not strictly increasing in . Then, for any , we have that . Thus, it is direct that

Therefore, also fulfills the first order condition and is not a singleton.

∎

Remark 3.

Equivalent forms for the first order condition of item (ii) are available, such as . We have in fact used it in the proof of item (iii) and will keep using it without further mention. Moreover, continuity of is not a necessary condition for the argmin set to be a singleton. For instance, Take and with for some . Then is the unique minimizer despite that is not continuous at .

We now derive a solution in terms of quantile functions under the assumption that position is independent of both costs and regarding any probability measure in . Note that this result rules out convexity from since VaR is not a convex risk measure.

Proposition 2.

Under the notation in Definition 1, let be independent of both and regarding any probability measure in and . Then:

-

(i)

(3) -

(ii)

(4)

Proof.

-

(i)

We have that the first order condition in Proposition 1 becomes for each

which is valid since . Thus, for , is a - quantile of . We then get that the minimum value that satisfies such condition is

Applying the supremum over leads to the desired result.

-

(ii)

By letting we see that the minimum becomes, for each :

The equivalence between expectation and integral in the last step is due to the optimization formula for Expected Shortfall (also known as Conditional Value at Risk or Average Value at Risk), see Proposition 4.51 of Föllmer and Schied (2016) for instance. By applying the supremum over we get the desired claim.

∎

Remark 4.

When and , we obtain as solution the -quantile (VaR). We recommend Bellini et al. (2014) for details. When is continuous at for any , we get

which is directly linked to the tail mean (ES) deviation by representing the distance between regular and tail expectations. Moreover, when we may end up to be in a situation where and are constants. Nonetheless, for the general situation where can be any strict subset of (a particular example is a singleton ) we are not necessarily limited to and constants. For instance, let be such that and for any . Also, let and for some . Then, regarding any , is independent of both and , while and are not constants.

Regarding the ambiguity set, one can choose in an ad hoc sense according to some a priori established risk aversion parameter. Another possibility is to consider those probability measures that represent beliefs absolutely continuous inside some distance from a nominal measure , as in Shapiro (2017). It is straightforward to note that implies both and .

We now expose a particular choice for linked to dual representations of coherent risk measures (sub-linear expectations as in Sun and Ji (2017)). These kind of functionals possess the properties of Monotonicity, Translation Invariance, Positive Homogeneity and Convexity. We now present a formal result that guarantees the dual representation of coherent risk measures in .

Theorem 1 (Artzner et al. (1999), Delbaen (2002)).

A functional is a lower semi-continuous in sense for bounded sequences coherent risk measure if and only if it can be represented as

where is a closed and convex non-empty set, called dual set of . If is finite, then the same is true without lower semi-continuity in sense.

Example 1.

Possible, but not limited, choices of are:

-

•

Expected Loss (EL): This risk measure is defined as . It is the most parsimonious one, indicating the expected value (mean) of a loss. Its dual set is a singleton , i.e., only consider the basic belief.

-

•

Mean plus Semi-Deviation (MSD): This risk measure is defined as . The advantages of this risk measure are its simplicity and financial meaning. represents its dual set.

-

•

Expected Shortfall (ES): This risk measure is defined as . It represents the expected value of a loss, given it is beyond the - quantile of interest. Its dual set is . ES is the most utilized coherent risk measure, being the basis of many representation theorems in this field.

-

•

Expectile Value at Risk (EVaR): This measure links to the concept of an expectile, given by . Its dual set is . EVaR is the only coherent risk measure, beyond EL, that possesses the property of elicitability.

-

•

Maximum loss (ML): This is an extreme risk measure that has dual set , i.e., all the considered beliefs. We define it as . Such a risk measure leads to the more protective situations since for any coherent risk measure .

Formulations (1) and (2) can be considered in situations with , where is a coherent risk measure. We define both and in order to ease notation. The next Proposition presents an alternative formulation for .

Proposition 3.

Let , where is a lower semi-continuous in sense for bounded sequences coherent risk measure. Then:

| (5) |

Proof.

The result follows from the Sion’s minimax theorem, see Sion (1958), because the map has the needed continuity and quasi-convex properties, is convex, and the optimization over can be done in a compact interval since . As we are considering negative results as losses, we need to correct the sign inside . ∎

3 Main properties

We now explore the main properties of our risk and deviation measures. We begin with those in relation to the position , which is the praxis in risk and deviation measures literature.

Proposition 4.

Let be as in (1). Then it has the following properties:

-

(i)

Monotonicity: if , then .

-

(ii)

Translation Invariance: .

-

(iii)

Positive Homogeneity: .

-

(iv)

Lipschitz continuity.

-

(v)

Lower semi-continuity regarding sense if are independent of any for any . If in addition is a singleton, then it is continuous in sense.

-

(vi)

Acceptance set: , where

with

Proof.

-

(i)

Fix and let be as and . We have, from the definition of indicator functions, that and are non-decreasing in the first argument and non-increasing in the second. Now, let with . Then for any . Furthermore, notice that if and , then . Thus

Then, we get from the first order condition of Proposition 1 that

Note that such expressions are well defined because, from Proposition 1, the argmin set is a closed interval. We then must have since . By multiplying both sides by and taking the supremum over we get the claim.

-

(ii)

Directly obtained from the definition in (1) by a change of variables.

-

(iii)

Analogous to (ii). Note that .

-

(iv)

Monotonicity plus Translation Invariance implies Lipschitz continuity regarding norm, see Corollary 2 of Delbaen (2012), for instance. In particular, 1 is a valid Lipschitz constant. Thus, we then have for any that Hence, is finite and well defined.

- (v)

-

(vi)

From the properties of , we have that it can be recovered by , see Proposition 4.6 of Föllmer and Schied (2016), for instance. We then have that

∎

Monotonicity requires that if one position generates worse results than another, then its risk will be greater. Translation Invariance ensures that if one adds a certain gain to a position, then its risk will decrease by the same amount. Positive Homogeneity indicates that risk proportionally increases with position size. In this case, is a closed cone that contains and has no intersection with . In the context of Proposition 2, we have that

This set is surplus invariant in the sense of Koch-Medina et al. (2017), i.e., and implies in . To see this, note that

Thus .

Remark 5.

Regarding lower semi-continuity, it could be obtained if the argmin sets were singleton for any . For this convergence of argmin sets see Theorem 7.33 in Rockafellar and Wets (2009), for instance. We also have that the maximum of argmin sets is monotone in . The reasoning is similar to that in (i) but considering as and .

Proposition 5.

Let be as in (2). Then it has the following properties:

-

(i)

Translation Insensitivity: .

-

(ii)

Positive Homogeneity: .

-

(iii)

Non-negativity: For all , for constant , and for non-constant .

-

(iv)

Convexity: .

-

(v)

Lipschitz continuity.

-

(vi)

Lower semi-continuity regarding sense for bounded sequences. If in addition is a singleton, then it is continuous in sense for bounded sequences.

-

(vii)

Range Dominance:

-

•

if , then .

-

•

if , then .

-

•

if , then .

-

•

-

(viii)

Dual representation: , where is the closed convex hull of

Proof.

-

(i)

Directly obtained by a change of the minimization variable.

-

(ii)

Analogous to (i).

-

(iii)

Since , we have that . If is not a constant, with abuse of notation, we have that with . We then get that at least one between or is strictly positive. Hence, .

-

(iv)

Consider any pair and any . We then obtain for each that

By taking the supremum over on both sides of the resulting inequality and from linearity of the real line one gets . Together with Positive Homogeneity (item (ii)) it implies that is a convex functional.

-

(v)

For Lipschitz continuity, note that is bounded since for any we have

Furthermore, from both Convexity and Positive Homogeneity, we have that is sub-linear, i.e., . Thus,

By reversing the roles of and we get

Since are fixed, we get the claim.

-

(vi)

For any and any by Dominated convergence we have that bounded implies, for any bounded sequence such that , in

Let be a sequence where each member is from the argmin set for under . Since is bounded, also is bounded for any . By the Bolzano-Weierstrass Theorem, we have, by taking a subsequence if needed, that is well defined and finite. We then get that

When we have in addition that

Hence .

-

(vii)

For we have for any that

For the reasoning is analogous with rather than . When both the upper bound is a direct consequence.

-

(viii)

Let . From the properties of , Theorem 1 of Rockafellar et al. (2006) and The Main Theorem of Pflug (2006), for instance, we have the following dual representation:

where

The fact that supremum is not altered by considering the closed convex hull is due to convexity and lower semi-continuity of and can be verified in Proposition 4.14 of Righi (2019b).

∎

Translation Insensitivity indicates the deviation in relation to the expected value does not change if we add a constant value. Convexity, which is related to the principle of diversification, implies that the risk of a combined position is less than the combination of individual risks. Non-negativity assures that there is dispersion only for non-constant positions. Range Dominance implies sharp bounds for the functional. Such properties make a generalized deviation measure in the sense of Rockafellar et al. (2006) and Pflug and Römisch (2007). Under the special conditions of Proposition 2, we have that is the closed convex hull of , where

Other very relevant properties in risk/deviation measures literature are, for , Law Invariance: if , then ; and Co-monotonic Additivity: for co-monotone, i.e., . Such properties are directly related to the notion of Spectral and Distortion risk/deviation measures, see Acerbi (2002) and Grechuk et al. (2009), for instance. The intuition is that functionals depend solely on the distribution of random variables and there is no diversification benefit in the case of extreme positive association. Concerning to Co-monotonic Additivity, when is a singleton and is -independent of and , it is satisfied by and because both VaR and ES possess this property.

Regarding Law Invariance, it is not satisfied in general for our approach since both and depend on the joint distributions of pairs and . Matter of fact, we would have to adapt the property for Joint Law Invariance as and implying into , where is the joint distribution of and . An exception is the situation of independence in Proposition 2. Moreover, our approach under a set of probability measures is linked to the -Law Invariance (-based) of Wang and Ziegel (2018) and Righi (2019b) where if , then . Nonetheless, even in such case, we would have to adapt for the joint distributions issue. We let this pursue for future research since it is outside the scope of this paper.

We now focus on the effect of costs and in our risk and deviation measures. This is important since the minimization procedure is directly dependent on such costs, beyond the financial position . Note that we are in fact considering the maps defined as , , and , for some fixed .

Proposition 6.

Let be as in (1). Then it has the following properties for any :

-

(i)

Non-increasing in and non-decreasing in .

-

(ii)

Boundedness in both and .

-

(iii)

Lower semi-continuity in both norm and sense for both and if is continuous and strictly increasing for any . If is a singleton, then it is continuous in both norm and sense.

Proof.

Consider the functions , respectively defined as , and . We then have:

-

(i)

Similar to Monotonicity property for (item (i)) in Proposition 4 by noticing that, for any , both functions and are non-decreasing in the first argument and non-increasing in the second and third arguments.

-

(ii)

For fixed we have for any . Thus, .

-

(iii)

We focus on the proof for . Concerning to , the reasoning is analogous. In this case, we have from Proposition 1 that argmin sets are singleton. We begin with lower semi-continuity in sense. Let , which, from Proposition 1, is a singleton since is continuous and is strictly increasing by hypothesis. Moreover, we have that and , which implies in . Again, such convergence of sets is guaranteed by Theorem 7.33 in Rockafellar and Wets (2009), for instance. We then obtain that

When we have that

Since convergence in norm implies convergence in sense, we have the claim.

∎

The monotone behavior for and is a consequence of the fact that more or less weight is put to overestimation or underestimation, respectively. When argmin sets are singleton, continuity properties imply that when representing the worst possible loss for . On the other side, we have that it assumes the value when representing the best possible loss for , corroborating to the identified monotone behavior.

Proposition 7.

Let be as in (2). Then it has the following properties for any :

-

(i)

Non-decreasing in both and .

-

(ii)

Concavity for both and if is a singleton. Furthermore, we have

, if is a convex set.

-

(iii)

Norm and lower semi-continuity for bounded sequences in both and . If in addition is a singleton, then it is continuous in norm and sense for bounded sequences.

Proof.

We always focus on the case . The reasoning for is quite similar. We then have:

-

(i)

If , , then

Since both minimum and supremum are monotone functions, we have non-decreasing behavior.

-

(ii)

Let for , and . We then have that

Let be convex. We have that defined as

is a bi-concave (concave in both arguments) function. We thus get for with and that

Thus by taking the supremum over pairs we get

By taking the supremum over , which is in fact attained, we get the claim.

-

(iii)

Lower semi-continuity regarding sense follows similar steps to item (vi) in Proposition 5 by considering instead of . Since convergence in norm implies convergence in sense, we have the claim.

∎

For we have that larger values are observed when both costs rise since both and are punitive. The concave behavior intuitively means that marginal costs are non-increasing, which is well sounded in practical matters. Regarding continuity, we have when both extremes cases and occurs that , in consonance with the pattern for .

4 Empirical illustration

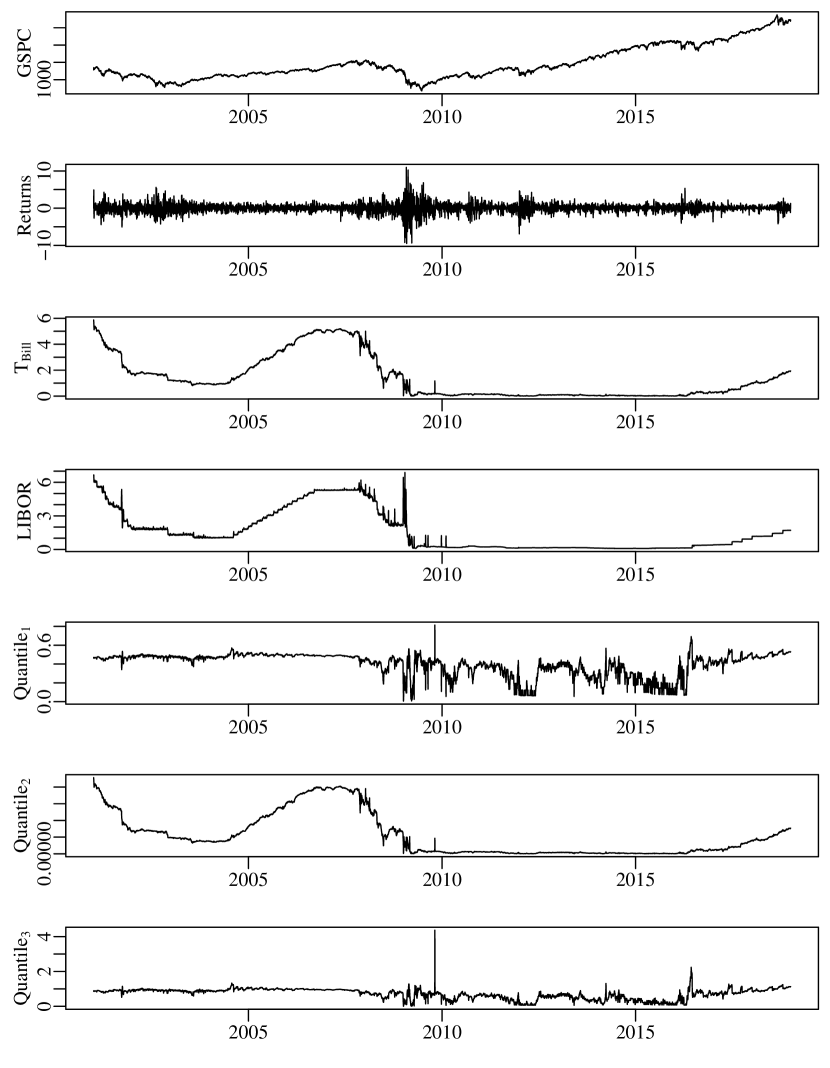

In this section, we expose an empirical illustration of our proposed approach for capital determination problem considering real financial data. We consider , where refers to EL, MSD, ES, EVaR and ML. These measures are described in Example 1. For MSD, we chose to incorporate all the deviation term222Similar value of is used in Righi and Borenstein (2018) to estimate loss-deviation risk measures. Their results showed a better performance of risk measures penalized by deviation in comparison with their counterpart without deviation.. The values of are in the case of ES and for EVaR. The latest revisions of the Committee on Banking Supervision recommend this for ES (see Basel Committee on Banking Supervision (2013)) and for EVaR this value is closely comparable to for a normally distributed (see Bellini and Di Bernardino (2017)).

For the financial position , we consider log-returns of S&P 500 U.S. market index multiplied by 100, which is a typical example of a financial asset used in academic research. Regarding the costs of risk overestimation () and underestimation (), we consider yield rates of the U.S. Treasury Bill with maturity of three months and the U.S. Dollar based Overnight London Interbank Offered Rate (LIBOR)333We emphasize that here our intention is only to illustrate the applicability of our approach. In this way, different costs from risk overestimation () and underestimation () can be considered. In periods of greater instability, more aggressive rates can be used as a cost from underestimation, for example.. These rates represent, respectively, a risk-free investment with high liquidity where the surplus over capital requirement could be safely applied, and a rate for providential loans when capital requirement is not enough. We consider daily data from January 2001 to May 2018, being observations. We convert both yield rates to daily frequency.

In this estimation process of risk measures, we have log-returns defined in some discrete probability space , as , where is the number of observations. For this approach, we consider . This leads to the empirical distribution and expectation, respectively, defined as:

This empirical method of estimation, known as historical simulation (HS), is a non-parametric approach that makes virtually no assumptions about the data. Note that is considered for each choice of as exposed in Example 1. In this case with . Note that in this case any probability is absolutely continuous in relation to . For instance, we have . Under this specification we adapt (1) and compute as:

| (6) |

In this case, the supremum over is attained since it is compact because has finite dimension. We compare the results of our risk measures with those obtained by risk measures using the following loss functions and , which we name and , respectively. These measures are in our illustration because they aim to identify the optimal amount of capital minimizing the costs that link to risk underestimation and overestimation. Although do not explicitly consider , it is a particular case of when . We compute and by procedure exposed on formulation (6), changing the loss function. We also compare our risk measures with those usually considered for capital requirements, which are and , and with ML444The reader should not confuse our risk measures computed under the dual set of ES and ML, and , which generate and , and the Expected Shortfall and Maximum Loss of , and , respectively.. Although VaR is not a coherent risk measure, it is the most common risk measure currently used in the literature and industry.

In Figure 1, we exhibit the graphic illustration of series described and the probability for quantile of represented by for , for , and for , where . Such quantities would be respective solutions in the fashion of Proposition 2 for such loss function and can be considered for benchmarking. We name them, respectively, as Quantile1, Quantile2, and Quantile3. One can note this sample contains both turbulent and calm periods, as visualized by the volatility clusters on log-returns, peaks and bottoms on the price series. Regarding the yield rates, there is a huge change in their dynamics at the end of 2008, possibly due to economic changes generated by the sub-prime crisis. To isolate the two distinct patterns identified for the costs, we divided the sample into two periods (2001–2008 and 2009–2018). So, we expose the results for the whole sample and for the two sub-samples. We consider a rolling estimation window of 250 observations (around one year of business days) to compute risk measures, excluding the year of 2001 for this out-sample forecasting exercise. In this sense, for each day in the out-sample period, we use the last 250 observations to compute the empirical distribution and risk measures.

The change in the dynamics of costs is also observed when analyzing the graphical illustration of probability distribution. Regarding Quantile1, in the first sub-sample, there is a stable evolution around 46%, close to the middle of the distribution function. In the second sub-sample, there is strong variation with values representing smaller probabilities linked to more extreme losses, which affects the value of our risk measures, but not necessarily VaR and ES. Hence, the sample split we make is an interesting feature of our analysis. For the Quantile2 the evolution coincides with the daily rates of , which has values less than , i.e., quantile used in the computation of VaR. Thus, for these measures, we expect more extreme losses compared to the values computed by VaR and ES.

In relation to probability distribution of Quantile3, we note some particularities. In the first sub-sample the variation of probability it fluctuates around 89, while in the second sub-sample is around 57. However, in both sub-samples there are values greater than 100, which contradicts the expected values for a probability. We identify these values because our structure does not impose . For the purpose of insurance , as originally proposed, becomes an interesting alternative since the values of its probability distribution are closer to the upper tail compared to the lower tail. However, our interest is a risk measurement procedure that minimizing the mentioned costs for the determination of capital.

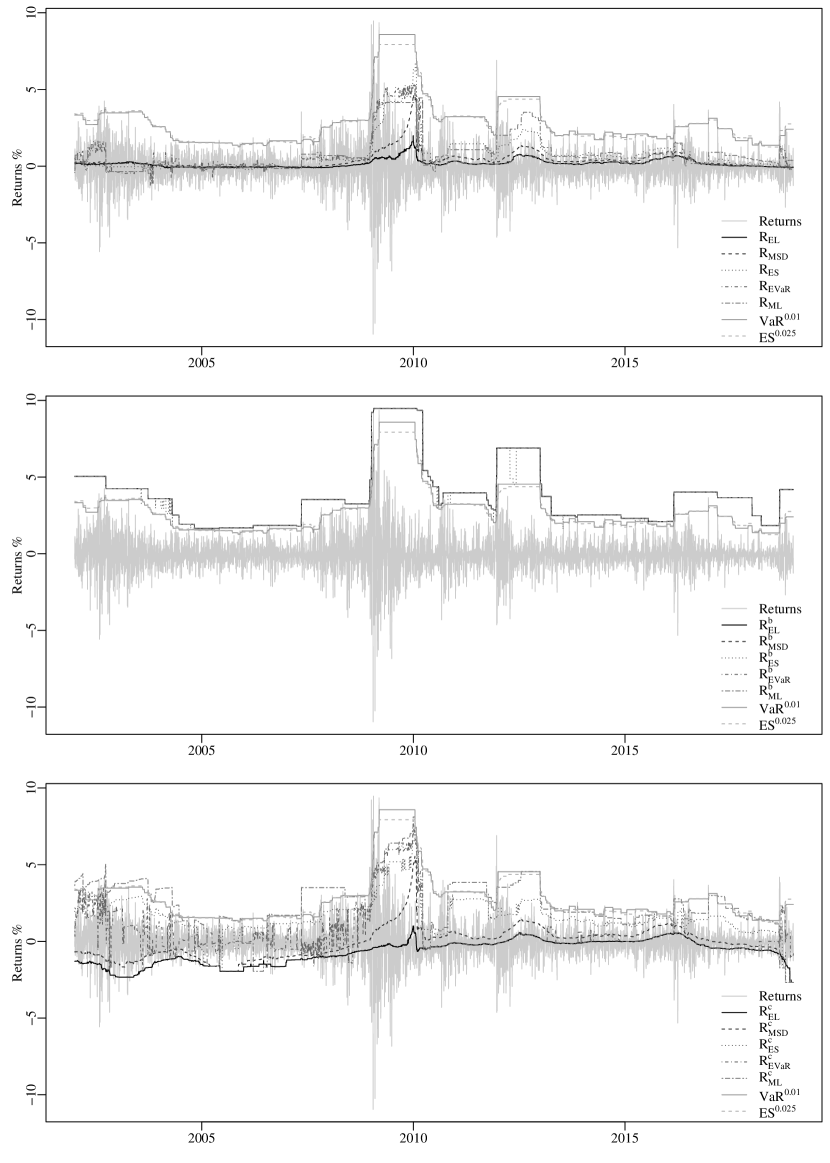

We expose in Figure 2 a plot with the time series of all estimated risk measures in relation to the negative of log-returns. We make this sign conversion because risk measures have their values in terms of losses. Results indicate risk measures estimates follow the evolution of losses on the financial position, as expected. Periods of higher volatility and losses exhibit larger values for risk measures. Complementing, in Table 1, we expose some descriptive statistics of these series, and the cost criteria (sum of daily costs in the sample) linked to the risk measures, which we obtain in the following manner:

| (7) |

where is the predicted value in period with corrected negative sign, of determined risk measure, and is the out-of-sample number of observations. Cost, and refer to metrics for model selection obtained from the loss functions used to compute, respectively, , and .

As observed in Table 1, based on more aggressive risk measures, i.e., those that assume larges values such as ES and ML, tend to display higher values. Our risk measures are well below VaR and ES, exhibit a smoother behavior that is indicated by standard deviations and ranges, beyond much smaller values for cost criterion. We can explain this because our approach considers, beyond past observations of the financial position, costs from underestimation and overestimation, while VaR and ES only deal with the historic position. With respect to , their mean values do not change when using different risk measures and coincide with Maximum Loss, where we quantify risk by the value of worst case. For example, in whole sample, mean value of .

It is also verified that the cost criterion , computed through the three metrics, generally coincide with the values estimated for . The pattern remains in the sub-samples. We can justify this by extreme values observed in their probability distribution, as descriptive statistics and graphical illustration of Quantile2. We also observed that cost criterion, computed by Costb and Costc, can take on negative values, i.e., do not fulfill Non-negativity axiom, and their value, even for the series of returns, is not zero. We justify this because and consider such as the regret cost. For our risk measures, this does not happen because we penalize only the regret costs pertaining to amount where the realized outcome is higher than capital requirement, rather than its total value.

Regarding our sub-samples, we maintain the results, but some discrepancies arise. We observe in the first sub-sample that log-returns have a positive tendency with high volatility. However, risk measures exhibit smaller and less volatile values, in relation to the whole sample. Aggregated costs are higher compared to second sub-sample. This pattern links to the yield rates, with larger values for this period and stable evolution. In the second sub-sample, we inverse all the patterns. Again, the yield rates seem to be the major determining factor.

Concerning the performance of the measures, in relation to Cost and Costc, with the exception of EL and MSD computed under dual set, our risk measures have the best results. As for Costb, we obtain the lower cost criteria by , as expected, and we achieve the highest cost criteria, in general, by . In summary, these findings corroborate the results obtained when using the whole sample, evidencing that our risk measures lead to more parsimonious and less costly capital determinations concerning risk measures recommended by regulatory agencies and measures proposed for a purpose similar to ours. This is explained because they consider not only the losses that are taking into account but also the gain opportunities.

5 Conclusion

In this paper, we propose a risk measurement approach that optimally balances costs from capital determination overestimation and underestimation. The objective is to obtain a real value that minimizes the expected value of the sum between both costs. We adopt a robust framework, where we consider the supremum for such minimizer and minimum based on a set of probability measures. We relate our approach with the dual representation of coherent risk measures since we based it on a supremum of expectations over probabilities. We perform an adaptation of the dual representation of usual discrete probability spaces. We develop some theoretical results that guarantee the solution for this problem, develop properties that our risk measure fulfills, and characterize the resulting minimum cost as a deviation measure.

In an empirical example, we estimate the capital determination using our approach, compared to risk measures that also focus on minimizing costs mentioned and to usual capital requirement determinations implied by Basel and Solvency accords, VaR0.01 and ES0.025. Results indicate our approach leads to less costly and more parsimonious charges. Our risk measures reflect the temporal evolution of the data, indicating their practical utility.

Our results are valid to risk management in other fields, such as reliability, ambient environment, and health, for instance. In these areas, as many others where risk management is a growing concern and research field, to have a measurement procedure that balances costs from excessive protection and lack of safeguards is necessary and desired. It is valid to think of extrapolating such a robust optimization problem over a set of probabilities to other contexts, such as portfolio strategies and outside finance. We also suggest conducting generalizations of our proposed approach to dynamic and multivariate frameworks.

References

- Acerbi (2002) Acerbi, C., 2002. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking & Finance 26, 1505 – 1518.

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.M., Heath, D., 1999. Coherent measures of risk. Mathematical Finance 9, 203–228.

- Basel Committee on Banking Supervision (2013) Basel Committee on Banking Supervision, 2013. Fundamental review of the trading book: A revised market risk framework. Consultative Document URL: https://www.bis.org/publ/bcbs265.pdf.

- Bellini and Di Bernardino (2017) Bellini, F., Di Bernardino, E., 2017. Risk management with expectiles. The European Journal of Finance 23, 487–506.

- Bellini et al. (2014) Bellini, F., Klar, B., Müller, A., Rosazza Gianin, E., 2014. Generalized quantiles as risk measures. Insurance: Mathematics and Economics 54, 41–48.

- Bellini et al. (2019) Bellini, F., Laeven, R.J.A., Gianin, E.R., 2019. Dynamic robust Orlicz premia and Haezendonck–Goovaerts risk measures. European Journal of Operational Research .

- Bellini et al. (2018) Bellini, F., Laeven, R.J.A., Rosazza Gianin, E., 2018. Robust return risk measures. Mathematics and Financial Economics 12, 5–32.

- Cont (2006) Cont, R., 2006. Model uncertainty and its impact on the pricing of derivative instruments. Mathematical Finance 16, 519–547.

- Delbaen (2002) Delbaen, F., 2002. Coherent risk measures on general probability spaces. Advances in Finance and Stochastics , 1–37.

- Delbaen (2012) Delbaen, F., 2012. Monetary utility functions. Osaka University Press.

- Dhaene et al. (2003) Dhaene, J., Goovaerts, M.J., Kaas, R., 2003. Economic capital allocation derived from risk measures. North American Actuarial Journal 7, 44–56.

- Dhaene et al. (2012) Dhaene, J., Tsanakas, A., Valdez, E.A., Vanduffel, S., 2012. Optimal capital allocation principles. Journal of Risk and Insurance 79, 1–28.

- Emmer et al. (2015) Emmer, S., Kratz, M., Tasche, D., 2015. What is the best risk measure in practice? A comparison of standard measures. Journal of Risk 18, 31–60.

- Föllmer and Schied (2016) Föllmer, H., Schied, A., 2016. Stochastic Finance: An Introduction in Discrete Time. 4 ed., de Gruyter.

- Föllmer and Weber (2015) Föllmer, H., Weber, S., 2015. The axiomatic approach to risk measures for capital determination. Annual Review of Financial Economics 7, 301–337.

- Furman et al. (2017) Furman, E., Wang, R., Zitikis, R., 2017. Gini-type measures of risk and variability: Gini shortfall, capital allocations, and heavy-tailed risks. Journal of Banking & Finance 83, 70–84.

- Goovaerts et al. (2005) Goovaerts, M.J., Van den Borre, E., Laeven, R.J.A., 2005. Managing economic and virtual economic capital within financial conglomerates. North American Actuarial Journal 9, 77–89.

- Goovaerts et al. (2010) Goovaerts, M.J., Kaas, R., Laeven, R.J.A., 2010. Decision principles derived from risk measures. Insurance: Mathematics and Economics 47, 294–302.

- Grechuk et al. (2009) Grechuk, B., Molyboha, A., Zabarankin, M., 2009. Maximum Entropy Principle with General Deviation Measures. Mathematics of Operations Research 34, 445–467.

- Guo and Xu (2019) Guo, S., Xu, H., 2019. Distributionally robust shortfall risk optimization model and its approximation. Mathematical Programming 174, 473–498.

- Koch-Medina et al. (2017) Koch-Medina, P., Munari, C., Šikić, M., 2017. Diversification, protection of liability holders and regulatory arbitrage. Mathematics and Financial Economics 11, 63–83.

- Laeven and Goovaerts (2004) Laeven, R., Goovaerts, M., 2004. An optimization approach to the dynamic allocation of economic capital. Insurance: Mathematics and Economics 35, 299–319.

- Pflug and Römisch (2007) Pflug, G., Römisch, W., 2007. Modeling, Measuring and Managing Risk. 1 ed., World Scientific.

- Pflug (2006) Pflug, G.C., 2006. Subdifferential representations of risk measures. Mathematical Programming 108, 339–354.

- Pichler and Schlotter (2020) Pichler, A., Schlotter, R., 2020. Entropy based risk measures. European Journal of Operational Research 285, 223–236. doi:10.1016/j.ejor.2019.01.016.

- Righi (2019a) Righi, M.B., 2019a. A composition between risk and deviation measures. Annals of Operations Research 282, 299–313.

- Righi (2019b) Righi, M.B., 2019b. A theory for combinations of risk measures. Working Paper URL: https://arxiv.org/abs/1807.01977.

- Righi and Borenstein (2018) Righi, M.B., Borenstein, D., 2018. A simulation comparison of risk measures for portfolio optimization. Finance Research Letters 24, 105–112.

- Righi and Ceretta (2016) Righi, M.B., Ceretta, P.S., 2016. Shortfall deviation risk: an alternative for risk measurement. Journal of Risk 19, 81–116.

- Rockafellar and Uryasev (2013) Rockafellar, R., Uryasev, S., 2013. The fundamental risk quadrangle in risk management, optimization and statistical estimation. Surveys in Operations Research and Management Science 18, 33–53.

- Rockafellar et al. (2006) Rockafellar, R.T., Uryasev, S., Zabarankin, M., 2006. Generalized deviations in risk analysis. Finance and Stochastics 10, 51–74.

- Rockafellar and Wets (2009) Rockafellar, R.T., Wets, R.J.B., 2009. Variational analysis. volume 317. Springer Science & Business Media.

- Rüschendorf (2006) Rüschendorf, L., 2006. Law invariant convex risk measures for portfolio vectors. Statistics & Decisions 24, 97–108.

- Shapiro (2017) Shapiro, A., 2017. Distributionally robust stochastic programming. SIAM Journal on Optimization 27, 2258–2275.

- Sion (1958) Sion, M., 1958. On general minimax theorems. Pacific Journal of Mathematics 8, 171–176.

- Sun and Ji (2017) Sun, C., Ji, S., 2017. The least squares estimator of random variables under sublinear expectations. Journal of Mathematical Analysis and Applications 451, 906 – 923.

- Wang and Ziegel (2018) Wang, R., Ziegel, J., 2018. Scenario-based risk evaluation. Working Paper URL: https://arxiv.org/abs/1808.07339.

- Xu and Hu (2012) Xu, M., Hu, T., 2012. Stochastic comparisons of capital allocations with applications. Insurance: Mathematics and Economics 50, 293–298.

- Xu and Mao (2013) Xu, M., Mao, T., 2013. Optimal capital allocation based on the Tail Mean–Variance model. Insurance: Mathematics and Economics 53, 533–543.

- Zaks et al. (2006) Zaks, Y., Frostig, E., Levikson, B., 2006. Optimal pricing of a heterogeneous portfolio for a given risk level. ASTIN Bulletin: The Journal of the IAA 36, 161–185.

- Ziegel (2016) Ziegel, J.F., 2016. Coherence and elicitability. Mathematical Finance 26, 901–918.

| Whole sample (2001 - 2018) | Mean | Dev. | Min. | Max. | Cost | Costb | Costc |

|---|---|---|---|---|---|---|---|

| Returns | -0.02 | 1.19 | -10.96 | 9.47 | 0 | -0.01 | -0.01 |

| 0.17 | 0.26 | -0.12 | 1.99 | 0.16 | 1311.67 | 0.08 | |

| 0.37 | 0.57 | -0.09 | 4.77 | 0.16 | 1113.30 | 0.07 | |

| 0.70 | 1.08 | -0.32 | 6.74 | 0.16 | 942.94 | 0.10 | |

| 0.51 | 1.12 | -1.27 | 5.36 | 0.17 | 1064.63 | 0.11 | |

| 0.85 | 1.14 | -0.95 | 4.45 | 0.18 | 823.51 | 0.12 | |

| 3.80 | 2.05 | 1.65 | 9.47 | 0.59 | 18.01 | 0.58 | |

| 3.80 | 2.05 | 1.65 | 9.47 | 0.59 | 18.01 | 0.58 | |

| 3.77 | 2.03 | 1.45 | 9.47 | 0.59 | 18.57 | 0.58 | |

| 3.80 | 2.05 | 1.65 | 9.47 | 0.59 | 18.01 | 0.58 | |

| 3.80 | 2.05 | 1.65 | 9.47 | 0.59 | 18.01 | 0.58 | |

| -0.69 | 0.77 | -2.68 | 1.01 | 0.33 | 3779.33 | 0.04 | |

| -0.12 | 1.02 | -2.68 | 5.54 | 0.27 | 2594.78 | 0.05 | |

| 1.58 | 1.28 | -2.68 | 6.82 | 0.31 | 592.72 | 0.27 | |

| 0.59 | 1.59 | -1.93 | 7.70 | 0.21 | 1304.19 | 0.14 | |

| 2.43 | 1.80 | -2.68 | 8.11 | 0.49 | 608.32 | 0.43 | |

| 2.86 | 1.67 | 1.26 | 8.58 | 0.44 | 58.24 | 0.43 | |

| 2.83 | 1.56 | 1.24 | 7.93 | 0.44 | 52.94 | 0.44 | |

| 3.80 | 2.05 | 1.65 | 9.47 | 0.59 | 18.01 | 0.58 | |

| Quantile1 | 0.39 | 0.12 | 0.01 | 0.81 | 0.19 | 1004.44 | 0.15 |

| Quantile2 | 0.01 | 0.01 | 0.01 | 0.01 | 0.16 | 1559.62 | 0.09 |

| Quantile3 | 0.71 | 0.30 | 0.01 | 4.36 | 0.25 | 759.13 | 0.22 |

| First sub-sample (2001 - 2008) | Mean | Dev. | Min. | Max. | Cost | Costb | Costc |

| Returns | 0.02 | 1.35 | -10.96 | 9.47 | 0 | -0.01 | -0.01 |

| 0.03 | 0.14 | -0.12 | 0.61 | 0.14 | 751.40 | 0.07 | |

| 0.10 | 0.21 | -0.08 | 1.19 | 0.14 | 690.98 | 0.08 | |

| 0.14 | 0.49 | -0.32 | 2.88 | 0.14 | 683.88 | 0.08 | |

| 0.30 | 0.73 | -1.27 | 4.41 | 0.15 | 603.69 | 0.10 | |

| 0.33 | 0.81 | -0.95 | 4.15 | 0.15 | 592.20 | 0.10 | |

| 3.26 | 1.65 | 1.65 | 9.47 | 0.49 | 8.65 | 0.49 | |

| 3.26 | 1.65 | 1.65 | 9.47 | 0.49 | 8.65 | 0.49 | |

| 3.24 | 1.65 | 1.45 | 9.47 | 0.49 | 8.65 | 0.49 | |

| 3.26 | 1.65 | 1.65 | 9.47 | 0.49 | 8.65 | 0.49 | |

| 3.26 | 1.65 | 1.65 | 9.47 | 0.49 | 8.65 | 0.49 | |

| -1.41 | 0.48 | -2.33 | -0.26 | 0.30 | 2708.23 | 0.04 | |

| -0.93 | 0.55 | -1.95 | 1.01 | 0.24 | 1995.36 | 0.04 | |

| 1.43 | 1.09 | -1.95 | 3.66 | 0.27 | 319.48 | 0.24 | |

| 0.62 | 1.30 | -1.93 | 4.99 | 0.18 | 571.04 | 0.12 | |

| 2.35 | 1.76 | -1.95 | 5.13 | 0.43 | 345.76 | 0.39 | |

| 2.46 | 1.21 | 1.26 | 8.58 | 0.37 | 31.27 | 0.37 | |

| 2.49 | 1.19 | 1.31 | 7.93 | 0.37 | 27.87 | 0.37 | |

| 3.26 | 1.65 | 1.65 | 9.47 | 0.49 | 8.65 | 0.49 | |

| Quantile1 | 0.46 | 0.07 | 0.01 | 0.57 | 0.17 | 485.33 | 0.13 |

| Quantile2 | 0.01 | 0.01 | 0.01 | 0.01 | 0.14 | 779.46 | 0.08 |

| Quantile3 | 0.89 | 0.17 | 0.01 | 1.33 | 0.22 | 333.13 | 0.20 |

| Second sub-sample (2009 - 2018) | Mean | Dev. | Min. | Max. | Cost | Costb | Costc |

| Returns | -0.04 | 0.94 | -5.32 | 6.90 | 0 | -0.01 | -0.01 |

| 0.22 | 0.20 | -0.09 | 0.77 | 0.01 | 467.51 | 0.01 | |

| 0.41 | 0.33 | -0.09 | 1.33 | 0.02 | 373.59 | 0.01 | |

| 0.80 | 0.59 | -0.14 | 2.39 | 0.02 | 251.79 | 0.01 | |

| 0.24 | 0.22 | -0.24 | 1.37 | 0.02 | 456.50 | 0.01 | |

| 0.93 | 0.76 | -0.35 | 3.51 | 0.02 | 223.24 | 0.02 | |

| 3.62 | 1.45 | 1.83 | 6.90 | 0.08 | 9.35 | 0.08 | |

| 3.62 | 1.45 | 1.83 | 6.90 | 0.08 | 9.35 | 0.08 | |

| L | 3.57 | 1.40 | 1.61 | 6.90 | 0.08 | 9.90 | 0.08 |

| 3.62 | 1.45 | 1.83 | 6.90 | 0.08 | 9.35 | 0.08 | |

| 3.62 | 1.45 | 1.83 | 6.90 | 0.08 | 9.35 | 0.08 | |

| -0.15 | 0.45 | -2.68 | 0.58 | 0.02 | 899.79 | 0.01 | |

| 0.30 | 0.59 | -2.68 | 1.41 | 0.02 | 546.55 | 0.01 | |

| 1.36 | 0.93 | -2.68 | 3.09 | 0.03 | 269.65 | 0.02 | |

| 0.01 | 0.42 | -1.04 | 2.31 | 0.02 | 725.03 | 0.01 | |

| 2.10 | 1.37 | -2.68 | 4.55 | 0.05 | 256.51 | 0.03 | |

| 2.61 | 0.92 | 1.36 | 4.72 | 0.05 | 26.96 | 0.05 | |

| 2.57 | 0.88 | 1.24 | 4.59 | 0.05 | 25.05 | 0.05 | |

| 3.62 | 1.45 | 1.83 | 6.90 | 0.08 | 9.35 | 0.08 | |

| Quantile1 | 0.34 | 0.13 | 0.06 | 0.69 | 0.02 | 410.79 | 0.02 |

| Quantile2 | 0.01 | 0.01 | 0.01 | 0.01 | 0.02 | 636.13 | 0.01 |

| Quantile3 | 0.57 | 0.30 | 0.06 | 2.24 | 0.03 | 337.17 | 0.02 |