Inference under Fine-Gray competing risks model with high-dimensional covariates

Abstract

The purpose of this paper is to construct confidence intervals for the regression coefficients in the Fine-Gray model for competing risks data with random censoring, where the number of covariates can be larger than the sample size. Despite strong motivation from biomedical applications, a high-dimensional Fine-Gray model has attracted relatively little attention among the methodological or theoretical literature. We fill in this gap by developing confidence intervals based on a one-step bias-correction for a regularized estimation. We develop a theoretical framework for the partial likelihood, which does not have independent and identically distributed entries and therefore presents many technical challenges. We also study the approximation error from the weighting scheme under random censoring for competing risks and establish new concentration results for time-dependent processes. In addition to the theoretical results and algorithms, we present extensive numerical experiments and an application to a study of non-cancer mortality among prostate cancer patients using the linked Medicare-SEER data.

keywords:

[class=MSC]keywords:

t2Bradic is supported by the NSF DMS grant number #1712481

1 Introduction

High-dimensional regression has attracted increasing interest in statistical analysis and has provided a useful tool in modern biomedical, ecological, astrophysical or economics data pertaining to the setting where the number of parameters is greater than the number of samples (see Bühlmann and van de Geer, (2011) for an overview). Regularized methods (Tibshirani, , 1996; Fan and Li, , 2001) provide straightforward interpretation of resulting estimators while allowing the number of covariates to be exponentially larger than the sample size. While they can be consistent for prediction (i.e. estimating the underlying regression function), confidence intervals cannot be consistently formulated, as firm guarantees of correct variable selection can only be established under a restrictive set of assumptions, including but not limited to the assumption of the minimal signal strength of the true parameter (Wasserman and Roeder, , 2009; Fan and Lv, , 2010; Meinshausen and Yu, , 2009), which cannot be verified in practice. For practical purposes, it is of interest to develop inferential tools, most commonly confidence intervals and p-values, that do not depend on such assumptions and are yet able to provide theoretical guarantees of the quality of estimation and/or testing; and this is the goal of our work here.

For the purposes of constructing confidence intervals or testing significance of the effect from certain covariates, relying on a naive regularized estimation alone is not appropriate; notably, construction of confidence intervals for those coefficients that have been shrunk to zero is impossible. Zhang and Zhang, (2014) and van de Geer et al., (2014) proposed the one-step bias-correction estimator, which can be subsequently used to carry out proper statistical inference. Our work here was motivated by an illustration project of how information contained in patients’ electronic medical records can be harvested for precision medicine. The data set linking the Surveillance, Epidemiology and End Results (SEER) Program database of the National Cancer Institute with the federal health insurance program Medicare database contained prostate cancer patients of age 65 or older. A total of 57,011 patients diagnosed between 2004 and 2009 had information available on 7 relevant clinical variables (age, PSA, Gleason score, AJCC stage, and AJCC stage T, N, M, respectively), 5 demographical variables (race, marital status, metro, registry and year of diagnosis), plus 9321 binary insurance claim codes. Among these patients 1,247 died due to cancer, and 5,221 had deaths unrelated to cancer by December 2013. An important goal of the project was to evaluate the impact of risk factors (clinical, demographical, and claim codes) on the non-cancer versus cancer mortality, with appropriate statistical inference. Cancer and non-cancer versus cancer mortality are known as competing risks in survival analysis, and cannot be handled using linear or generalized linear regression models as considered in Zhang and Zhang, (2014) and van de Geer et al., (2014). Instead, we consider the proportional subdistribution hazards regression model, often known as the Fine-Gray model Fine and Gray, (1999). Under classical low-dimensional setting, Fine and Gray derived the estimation and inference for the model coefficients via the partial likelihood principle, and handled right censoring by inverse probability censoring weighting (IPCW).

Considerable research effort has been devoted to developing regularized methods to handle various regression settings (Ravikumar et al., , 2010; Belloni and Chernozhukov, , 2011; Obozinski et al., , 2011; Meinshausen and Bühlmann, , 2006; Basu and Michailidis, , 2015; Cho and Fryzlewicz, , 2015), including those for right-censored time-to-event data (Sun et al., , 2014; Bradic et al., , 2011; Gaïffas and Guilloux, , 2012; Johnson, , 2008; Lemler, , 2016; Bradic and Song, , 2015; Huang et al., , 2006, among others). However, regression has been little studied for the competing risks setting, with random censoring and high-dimensional covariates. The purpose of this paper has two folds: 1) to study estimators under the Fine-Gray regression model for competing risks data with many more covariates than the number of events; 2) to develop statistical inference procedures in this setting. To our best knowledge, no published work exists on statistical inference for competing risks data that allows high-dimensional models; univariate testing was studied in Cox proportional hazards model – however, our construction allows for the testing of general linear hypothesis.

There are at least three significant challenges for addressing high-dimensional competing risks regression under the Fine-Gray model. The structure of the score function related to the partial likelihood causes a somewhat subtle issue with many of the unobserved factors preventing a simple martingale representation. Additionally, the structure, as well as, size of the sample information matrix renders both methodology and theoretical analysis based on the Hessian matrix problematic. Thirdly, random censoring presents non-trivial challenges in the presence of competing risks and weighting is needed which further complicates the theoretical analysis. Also, although bootstrap has been considered for inference under the Fine-Gray regression model, this approach is no longer applicable given the known problems of the bootstrap in high-dimensional settings. Development of high-dimensional inferential methods for competing risks data and under the Fine-Gray model, in particular, may have been hampered by these considerations.

In this paper, we propose a natural and sensible formulation of inferential procedure for this high-dimensional competing risks regression. We first study a regularized estimator of the high-dimensional parameter of interest and derive its finite-sample properties where the interplay between the sparsity, ambient dimension and the sample size can be directly seen. We then propose a bias-correction procedure by formulating a new pragmatic estimator of the inverse of a large covariance matrix that allows broad dependence structures within the Fine-Gray model. We find that the bias-corrected estimator is effective at capturing strong as well as weak signals, and can be used for statistical inference. This combination leads to an efficient and simple-to-implement procedure under the Fine-Gray model with many covariates.

1.1 Model and notation

For subject in a study, let be the event time, with the event type or cause ; we use the two words interchangeably in the following. Under the Fine-Gray model that we consider below, we assume without loss of generality that the event type of interest is ‘1’, and we code all the other event types as ‘2’ without further specification. In the presence of a potential right-censoring time , the observed time is . We denote the event indicator as . The type of the event is observed, if the event occurs before the censoring time, i.e., when . Let be the vector of covariates that are possibly time-dependent. We focus on the situation that the dimension of , , is larger than the sample size . Assume that the observed data are independent and identically distributed (i.i.d.) for .

Since the cumulative incidence function (CIF) is often the quantity of interest, Fine and Gray, (1999) proposed a proportional subdistribution hazards model where the CIF

| (1.1) |

the -dimensional coefficient is the unknown parameter of interest, and is the baseline subdistribution hazard. Under the model (1.1) corresponding subdistribution hazard . Throughout the paper, we assume that there exists a sparsity factor for some . Note that if we define an improper random variable , then the subdistribution hazard can be seen as the conditional hazard of given .

We denote the counting process for type 1 event as and its observed counterpart as . We also denote the counting process for the censoring time as . Let (note that this is not the ‘at risk’ indicator like under the classic Cox model), and . Note that is always observable, even though or may not. Let and let be the Kaplan-Meier estimator for . Here we assume that is independent of , and . Following the notation of Fine and Gray we call the IPW at-risk process:

| (1.2) |

in other words, the weight for subject is one if , zero after being censored or failure due to cause 1, and after failure due to other causes. The log pseudo likelihood (as recently named in Bellach et al., (2018)) that gives rise to the weighted score function in Fine and Gray, (1999) for is

| (1.3) |

where is the study end time.

In the following, for a vector , let , and . We define for

| (1.4) |

We then have the score function, i.e. derivative of the log pseudo likelihood (1.3),

Regarding notation, let us mention that all constants are assumed to be independent of , and . We use and with corresponding enumerated subscripts to denote “big” and “small” constants. We use to denote intermediate terms used in the statements or the proofs of various results. We label the subscripts by the corresponding order of their appearance.

1.2 Organization of the paper

This paper is organized as follows. In Section 2, we provide the bias corrected estimator, Section 2.1, as well as the confidence interval construction, Section 2.2, for the high-dimensional Fine-Gray model. Construction of a new Hessian estimator, the cornerstone for our bias correction and variance estimation, is presented in Section 2.3. Section 3 presents properties of the developed estimator. Additional notations for theoretical considerations are presented in Section 3.1. Bounds for the prediction error are presented in Section 3.2; Theorem 1 is the main result on estimation. Section 3.3 studies the sampling distribution of a newly develop test statistics while not requiring model selection consistency or minimal signal strength. Theorem 2 is the main result regarding asymptotic distribution. There we present a sequence of intermediate results as well. We examine our regularized estimator and the one-step bias-corrected estimator through simulation experiments in Section 4, and apply them to the SEER-Medicare data in Section 5.

2 Estimation and inference for competing risks with more regressors than events

2.1 One-step corrected estimator

A natural initial estimator to consider under the high dimensional setting is a -regularized estimator, where the particular loss function of interest would be the log pseudo likelihood as defined in (1.3). We note that our results are easily generalizable to any sparsity-inducing and convex penalty functions, but due to the simplicity of presentation we present details only for the regularization. That is, we consider

| (2.1) |

for a suitable choice of the tuning parameter . Whenever possible, we suppress in the notation above and use to denote the -regularized estimator. In the Section 3.2, we quantify the non-asymptotic oracle risk bound and show that the estimator above, as a typical regularized estimator with , converges at a rate slower than root-. This implies that for inferential purposes the bias of the estimator cannot be ignored.

Inspired by the work of Zhang and Zhang, (2014) and van de Geer et al., (2014), we propose the one-step bias-correction estimator

| (2.2) |

where is defined in (2.1), is an estimator of the “asymptotic” precision matrix to be defined later. The above construction of the one-step estimator is inspired by the first order Taylor expansion of ,

| (2.3) |

The notation “” in the above indicates that the equivalence is approximate with the higher order error terms omitted. We aim to find a good candidate matrix , such that , with denoting the identity matrix. Note that when an inverse of the Hessian matrix above would naturally be a good candidate for , but when such an inverse does not necessarily exist. We will elucidate the construction of towards the end of this section.

2.2 Confidence Intervals

To construct the confidence intervals for components of , we need the asymptotic distribution of . We will first establish the asymptotic distribution of the score . With , we have to restrict the space in which we want to establish the asymptotic distribution. The asymptotic distribution for is established in the following sense — for any such that we have

where is the variance-covariance matrix for . We construct the following estimator for :

| (2.4) |

where and are defined as follows:

| (2.5) | |||

| (2.6) | |||

| (2.7) | |||

| (2.8) | |||

| (2.9) | |||

| (2.10) |

As illustrated in (2.1), we have to be asymptotically equivalent to

We may now estimate the variance of using a “sandwich” estimator . Therefore a confidence interval for is

| (2.11) |

with standard normal quantile .

Our proposed approach addresses various practical questions as special cases. First, we can construct confidence interval for a chosen coordinate in . To that end, one needs to consider , the -th natural basis for and apply the result (2.11). Generally, we can construct a confidence interval for any linear contrasts , potentially of any dimension. For example, we can have confidence intervals for the linear predictors if the non-time-dependent covariate is also sparse so that we may assume to be bounded. As the dual problem, we may use the Wald test statistic

| (2.12) |

to test the hypothesis with .

2.3 Construction of the inverse Hessian matrix

Although the early works under the linear model inspire the construction here, the specifics, as well as the theoretical analysis, the latter remains a challenge. We start by writing the negative Hessian of the log pseudolikelihood (1.3):

| (2.13) |

We define

| (2.14) |

Under the regularity conditions, to be specified later, we have as the “asymptotic negative Hessian” in the sense that the element-wise maximal norm converges to zero in probability. Our goal is to estimate its inverse , where ’s are the rows of .

By definition (2.14), the positive semi-definite matrix is also the second moment of the random vector

| (2.15) |

with defined in (1.4). The expectation of is zero,

Hence, to estimate , we may draw inspiration from the early work on inverting the high-dimensional variance-covariance matrix Zhou et al., (2011). Consider the minimizers of the expected loss functions

| (2.16) |

where is the th element of , and is a dimensional vector created by dropping the th element from . We show that the quantities and defined in (2.16) can be used to construct the inverse of . This is because can also be alternatively written as

| (2.17) |

By the convexity of the target function , must satisfy the first order Karush-Kuhn-Tucker conditions (KKT)

| (2.18) |

Applying (2.18) to (2.17), we have

We can then define a vector that satisfies

Without loss of generality, we may define accordingly for , satisfying . The matrix satisfies

therefore is the inverse of . We now utilize the sample form of , (2.14),

| (2.19) |

In particular we observe that is that it can be written as the sample second moment where

| (2.20) |

This form allows us to define the inverse of as a regression between the vectors . For that purpose we define the least squares loss function as

| (2.21) |

where is the th element of , and is a dimensional vector obtained by dropping the th element from . We then define the nodewise LASSO in our context to be

| (2.22) |

Accordingly, we use and to construct

| (2.23) |

By the first order KKT condition, we have and for . Choosing , we achieve that goes to zero. The one-step estimator proposed in (2.2) with such hence converges to the true coefficient approximately at the rate equivalent to , as illustrated in (2.1).

Our proposed nodewise LASSO estimator is innovative in several aspects. Given the difficulty imposed by the model, we cannot make high-dimensional inference by simply inverting the for a design matrix like in a linear or generalized linear model. The log pseudo likelihood (1.3) has dependent entries. The covariates for are allowed to be time-dependent. Nevertheless, we identify for our model that the key element for the high-dimensional inference is each observation’s contribution to the score, the ’s. Our solution generalizes high-dimensional matrix inversion in a non-trivial way to complex models with censoring, non-standard likelihoods and weighting.

3 Theoretical considerations

In this section, we present the theory for the estimators , and the confidence intervals described in the previous section. We will quantify the non-asymptotic oracle risk bound for the estimator above while allowing with a minimal set of assumptions. Theoretical study of this kind is novel, since in the context of competing risks, the martingale structures typically utilized are unavailable and new techniques need to be developed. In particular, we show that the inverse probability weighting has a finite-sample effect that separates this model from the classical Cox model (see comments after Theorem 1). We will also establish that a certain tighter bound can be established whenever the hazard rate is bounded (Theorem 3).

Throughout our work we assume that are i.i.d. with independent of . Moreover, for any , is differentiable, and its hazard function . We also assume that the baseline CIF is differentiable. The baseline subdistribution hazard for all and some and .

3.1 Additional notation

In the following, we introduce some additional notations. The counting process martingales

| (3.1) |

are essentially helpful tools in high-dimensions for establishing theory with dependent partial likelihoods. Unfortunately, the uncensored counting processes are not always observable. The observable counterpart has no known martingale related to it under the observed filtration . The Doob-Meyer compensator for the submartingale under the observed filtration involves the nuisance distribution of . To utilize the martingale structure for our theory, we have to define the “censoring complete” filtration

| (3.2) |

on which we have a martingale related to ,

| (3.3) |

To relate the martingale (3.3) with our log pseudo likelihood , we define its proxy with measurable integrand

| (3.4) |

We define processes related to and its derivatives as

| (3.5) |

They can also be seen as proxies to the processes in (1.4). To see that, observe that by conditioning,

where

| (3.6) |

is the weight with the true censoring distribution . We denote their expectations as

| (3.7) |

Our proxies precisely target those weighted samples, as differs from only at those summands with observed type-2 events.

Note that the Kaplan-Meier estimator for can be written as

To study the convergence of to , we denote a martingale related to , the counting process of observed censoring, . Let the censoring hazard be defined as . Under the “censoring” filtration

| (3.8) |

we have a martingale

| (3.9) |

We use the integration-by-parts arguments (Murphy, , 1994, the Helly-Bray argument on page 727) with random martingale measures, e.g. , in our proof. The total variation of is defined as

| (3.10) |

Since can be decomposed into a nondecreasing counting process minus another nondecreasing compensator , we have a bound for its total variation

| (3.11) |

Similar conclusion also applies to , i.e. we have a bound for its total variation

| (3.12) |

As a convention, from hereon we suppress the in the notation to keep it simple.

3.2 Oracle inequality

We first establish oracle inequality for the initial estimation error based on the following set of conditions that are weaker than those in the next subsection.

-

(C1)

(Design) With probability equal to one, the covariates satisfy

(3.13) The expected at-risk process is bounded away from zero, i.e., for positive and

(3.14) - (C2)

-

(C3)

(Continuity) may have jumps at with minimal gap between jumps bounded away from zero,

Between two consecutive jumps, has at most elements Lipschitz continuous with Lipschitz constant while the rest of the elements are considered to be constant.

Remark 1. Overall, the conditions above are minimal in the sense that they appear in results pertaining to the Cox model (Huang et al., , 2013, see e.g, (3.9) on page 1149; (4.5) and Theorem 4.1 on page 1154).

Remark 2. We consider a finite interval . Due to missing censoring times among those with observed type-2 events, we have to make the additional assumptions to control the weighting errors. Although the weighted at-risk processes ’s are asymptotically unbiased, the approximation errors in the tail are poor for any finite . To avoid unnecessary complications, we set the such that we always have sufficient at-risk subjects; note that (3.14) implies that .

Remark 3. We assume a finite maximal norm of . Condition (3.13) in (C1) is equivalent to the apparently weaker assumption (see for example Huang et al., (2013) equation (3.9)):

| (3.15) |

This can be seen by noting that the Cox type partial likelihood for the proportional hazards model is invariant when subtracting by any deterministic .

Remark 4. Condition (C1) (3.14) carries two facts. First, the at-risk rate for type 1 events is bounded away from zero. Second, relative-risks arbitrarily close to zero is truncated at a finite ; this is necessary in high-dimensions, in order to rule out the irregular cases where the non-zero expectation of the relative risk is dominated by a diminishing proportion of the excessively large relative risks. The same argument applies for (C2) in which a lower bound of the restricted eigenvalue of the negative Hessian Bickel et al., (2009) is defined.

Remark 5. We assume the smoothness of the time-dependent covariates . Subjects with observed type 2 events, remain indefinitely in the risk sets for type 1 events. For time-dependent covariates, continuity is helpful in establishing a slow growing rate of the maximal relative risks among those subjects; something that is a fact for time independent covariates. Note that the coordinate wise continuity in is insufficient as grows to infinity. We propose (C3) taking into account likely practical scenarios, where the covariates are either constant, or change only at finitely many discrete time points.

Under the above assumptions, we are ready to present our estimation error result. Since the result holds in finite samples, we define a sequence of important constants first. For a and constants as well as (introduced in the conditions above)

| (3.16) |

| (3.17) |

where , and

| (3.18) |

In high-dimensional models an additional constant, the so called compatibility factor, plays an important role. For a positive constant , the compatibility factor

| (3.19) |

where denotes the cone set

with denoting the indices of non-zero elements and denoting its compliment.

Theorem 1.

Our proof of Theorem 1 applies to the result with -norm and general -norm for . Namely, under the same conditions we have that

occurs with probability no less than

with the weak cone invertibility condition defined as

A few comments are in order. For a fixed , is of order . Thus, Theorem 1, together with Lemma 2 (see below), guarantee that for chosen to be of the order

The above estimation error rate to the error rate of the simple Cox model (Huang et al., , 2013; Yu et al., , 2019), differing only by a factor of . This factor is brought in by the error induced by the IPCW weights. Therefore, under the rate condition , we obtain an asymptotically -consistent regularized estimator .

The quantity describes the error from IPCW weights through the measurable approximation to processes , . A naïve bound for the measurable approximation is proportional to the magnitude of the relative risks in , naturally of the order , potentially growing in exponential rate of if for some . Such bound grows way too rapidly to deliver any meaningful result. Observing that the summands in and at a particular index differ from each other only when the -th subject has type-2 event we are able to establish a significantly sharper bound. For that purpose, we develop -tail bound of the maximal relative risk among observed type 2 events (see Appendix Lemma B.3). The quantity , involving directly in the definition, gives the bound for the error from the measurable approximation to (See in Appendix Lemma B.5).

For the rest of this section, we provide further details on the proof of Theorem 1, as well as the technical challenges involved. We highlight two results, Lemma 1 and 2. The first establishes properties of the score vector while the second one establishes the properties of the compatibility factor (3.19).

Lemma 1 establishes that such event (of interest in Theorem 1) happens with high probability. This task is not straightforward in the presence of both competing risks and censoring. The greatest challenge is the lack of the martingale property in . Even if we use its martingale proxy (an approach useful in low-dimensions) as the gradient of (3.4)

| (3.20) |

with defined in (3.5), the approximation error between and is difficult to control because the error is determined by with defined in (1.2), which can be significantly amplified when the relative risks grow with the dimension. To prove Lemma 1, we first show that the relative risks among subjects with observed type 2 events has sub-Gaussian tails. This is achieved through the argument that their CIF cannot be arbitrarily close to one; otherwise, these subjects would have probability close to one experiencing type 1 event. As the CIF is monotonically increasing with the relative risks, it is also unlikely to observe excessively large relative risks among the subjects with observed type 2 events. We then use Lemma A.3(i) in the Appendix to establish the concentration of around zero across all observed type 1 event times.

Theorem 1 assumes that converges to zero for a sequence of bounded away from zero, as sample size goes to infinity. In Lemma 2, we show that such event happens with high probability. Using the connection between the compatibility factor and the restricted eigenvalue van de Geer and Bühlmann, (2009), we show that , the compatibility factor in the cone , is bounded away from zero with probability tending to one.

3.3 Asymptotic normality for one-step estimator and honest coverage of confidence intervals

Obtaining the asymptotic normality is technically challenging. The log-likelihood has dependent summands both through the initial lasso estimator as well as the Kaplan-Meier estimator. We establish the asymptotic normality for the one-step estimator and coverage of the confidence intervals without requiring model-selection consistency of the initial estimator. To remove the small-sample bias of IPCW, we need slightly stronger conditions than in the previous section. In this section alone, we use and without subscript to denote the constants independent of , and ; we have only one constant that is allowed to grow with the dimension and is therefore denoted differently.

-

(D1)

(Design) The true linear predictors are uniformly bounded with probability one

(3.21) -

(D2)

(Hessian) The smallest eigenvalue , where is defined in (2.14).

-

(D3)

(Continuity) Each can be represented as

for random processes , and the counting process such that , is uniformly bounded between and uniformly Lipschitz-. Moreover, ’s number of jumps and an intensity function .

-

(D4)

(Dimension) The rows of the matrix are and sparse with sparsities . Lastly, .

We next present Theorem 2 that justifies all the proposed inference procedures in Section 2.2. For that purpose we denote the asymptotic variance of with

| (3.22) |

where

| (3.23) | |||

| (3.24) | |||

| (3.25) | |||

| (3.26) |

Theorem 2.

As a result of the stronger conditions required for Theorem 2, which we will explain in more details below, we are able to achieve an improved estimation error for the initial estimator as stated in the next theorem.

For the rest of this section, we explain the assumptions and theoretical results needed for Theorem 2 summarized in Lemmas 3-7. Condition (D1) is needed whenever the model departs significantly from the linear case (van de Geer et al., , 2014; Fang et al., , 2017). In our case, the asymptotic normality of depends fundamentally on the asymptotic tightness of . As a necessary condition, the predictable quadratic variation under filtration of the martingale

| (3.27) |

must have a finite bound independent of the dimension of the covariates. This requires that the magnitude of the summands in (3.27) either be bounded or have light tails. Hence, we cannot allow the relative risk to grow arbitrarily large. We next observe that (D2) is a standard assumption for the validity of the nodewise penalized regressions (2.22). Finally, note that Theorem 2 utilizes Condition (D3); a condition stronger than (C3) needed for - approximation error between and .

If we define the population versions of the nodewise components defined in (2.20)-(2.22),

| (3.28) |

then the true parameters uniquely define the inverse negative Hessian as described in Section 2.3. We prove this statement in the following Lemma.

Lemma 3.

Under (D2), and . Moreover, , and .

Next, we discuss the properties of estimands , and – defining components of the variance estimate.

The nodewise LASSO in (2.22), unlike van de Geer and Bühlmann, (2009) that has i.i.d. entries, has dependent ’s through the common ; see (2.20). Thus, our error rate takes the multiplicative form , instead of the summation that may be expected under the generalized linear models. In general, we consider our rate to be optimal under our model.

Lemma 5.

Next, we show the asymptotic normality of .

The proof uses the same approach as the initial low-dimensional result in Fine and Gray, (1999). We approximate by the sample average of i.i.d. terms plus an term. We note that the same approach involves nontrivial techniques in order to be valid in high-dimensions. In particular, we discover and exploit the martingale property of the term .

4 Numerical Experiments

To assess the finite sample properties of our proposed methods, we conduct extensive simulation experiments with various dimensions and dependence structure among covariates.

4.1 Setup 1

Our first simulation setup follows closely the one of Fine and Gray, (1999) but considers high-dimensional covariates. In particular, each is a vectors consisting of i.i.d. standard normal random variables. For cause 1, only are non-zero. The cumulative incidence function is:

For cause 2, and , with

We consider four different combinations: , ; ; ; and . Note that this setup considers sparsity for cause 1 but non-sparsity for cause 2 effects. As the Fine-Gray model does not require modeling cause 2 to make inference on cause 1, we expect that the non-sparsity in cause 2 effects should not affect the inference on cause 1.

| True | Mean Est | SD | SE | SE corrected | Coverage | Level/Power | |

| n=200, p=300 | |||||||

| 0.5 | 0.51 | 0.16 | 0.13 | 0.25 | 0.94 | 0.92 | |

| 0.5 | 0.47 | 0.15 | 0.14 | 0.22 | 0.94 | 0.93 | |

| 0 | 0.03 | 0.12 | 0.15 | 0.18 | 0.98 | 0.04 | |

| n=200, p=500 | |||||||

| 0.5 | 0.51 | 0.16 | 0.14 | 0.19 | 0.93 | 0.95 | |

| 0.5 | 0.48 | 0.15 | 0.13 | 0.19 | 0.93 | 0.88 | |

| 0 | -0.01 | 0.10 | 0.14 | 0.16 | 1.00 | 0.01 | |

| n=200, p=1000 | |||||||

| 0.5 | 0.46 | 0.17 | 0.13 | 0.18 | 0.94 | 0.86 | |

| 0.5 | 0.48 | 0.14 | 0.13 | 0.18 | 0.93 | 0.92 | |

| 0 | -0.00 | 0.11 | 0.14 | 0.17 | 0.99 | 0.06 | |

| n=500, p=1000 | |||||||

| 0.5 | 0.51 | 0.10 | 0.08 | 0.14 | 0.99 | 1.00 | |

| 0.5 | 0.50 | 0.10 | 0.08 | 0.15 | 0.99 | 0.99 | |

| 0 | -0.00 | 0.07 | 0.08 | 0.14 | 1.00 | 0.03 | |

The results are presented in Table LABEL:table:simFG. We focus on inference for the two non-zero coefficients and , as well as one arbitrarily chosen zero coefficient . The mean estimates are the average of the one-step over the 100 repetitions, reported together with other quantities described below. We can see from the average estimates column that the one-step is bias-corrected and that the presence of many non-zero coefficients for causet 2 does not affect our inference on cause 1.

In practice the choice of the tuning parameters is particularly challenging; the optimal value is determined up to a constant. Moreover, the theoretical results are asymptotic. These together with the finite sample effects of , lead to suboptimal performance of many proposed one-step correction estimators van de Geer et al., (2014); Fang et al., (2017). Suboptimality is amplified for survival models, due to the nonlinearity of the loss function and the presence of censoring – both require more significant sample size (to observe asymptotic statements in the finite samples). In the following, we propose a finite-sample correction to the construction of confidence intervals and in particular the estimated standard error (SE).

Let denote the asymptotic standard error as given in Section 2.2. As a finite-sample correction we propose to consider in place of , where the variance estimation based on the initial LASSO estimate is replaced by the one-step . This can be viewed as another iteration of the bias-correction formula. The resulting SE is therefore a “two-step” SE estimator. We report the coverage rate of the confidence intervals constructed with this finite-sample correction in Table LABEL:table:simFG and we observe good coverage close to the nominal level of . We note that with 100 simulation runs the margin of error for the simulated coverage probability is about 2.18%, if the true coverage is 95%; that is, the observed coverage can range between 954.36%. We note that the coverage is good for all three coefficients, where non-zero or zero. In contrast, results in the existing literature suffer under-coverage of the non-zero coefficients.

The last column ‘level/power’ in Table LABEL:table:simFG refers to the empirical rejection rate of the null hypothesis that the coefficient is zero, by the two-sided Wald test at a nominal significance level. We see that although is used, the nominal level is well preserved for the zero coefficient , and the power is high for the non-zero coefficients and for the given sample sizes and signal strength.

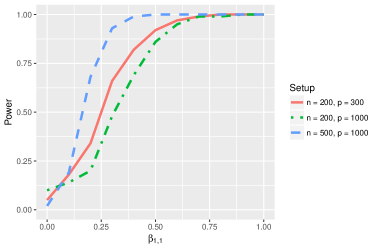

We repeat the above simulations with different values for to investigate the power of the Wald test. The results are illustrated in Figure 1, where we see that the power increases with and decreases with as expected.

4.2 Setup 2

In the second setup we consider the case where the covariates are not all independent, which is more likely the case in practice for high dimensional data. We consider the block dependence structure also used in Binder et al., (2009). We consider , ; , and the rest are all zero. , and the rest of are all zero. The covariates are grouped into four blocks of size , , plus the rest, with the within-block correlations equal to , , and . The four blocks are separated by the horizontal lines in Table LABEL:table:simBinder.

| True | Mean Est | SD | SE | SE corrected | Coverage | Level/Power | |

| n=500, p=1000 | |||||||

| 0.5 | 0.47 | 0.10 | 0.07 | 0.12 | 0.97 | 1.00 | |

| 0.5 | 0.48 | 0.10 | 0.07 | 0.12 | 0.94 | 0.98 | |

| 0.5 | 0.47 | 0.10 | 0.07 | 0.12 | 0.98 | 1.00 | |

| 0.5 | 0.47 | 0.10 | 0.07 | 0.12 | 0.94 | 1.00 | |

| 0.5 | 0.48 | 0.10 | 0.06 | 0.11 | 0.93 | 1.00 | |

| 0.5 | 0.46 | 0.10 | 0.06 | 0.11 | 0.94 | 1.00 | |

| 0.5 | 0.47 | 0.09 | 0.06 | 0.11 | 0.95 | 1.00 | |

| 0.5 | 0.47 | 0.08 | 0.06 | 0.11 | 0.98 | 1.00 | |

| -0.5 | -0.44 | 0.08 | 0.06 | 0.11 | 0.93 | 1.00 | |

| -0.5 | -0.42 | 0.08 | 0.06 | 0.11 | 0.92 | 1.00 | |

| -0.5 | -0.41 | 0.08 | 0.06 | 0.11 | 0.91 | 1.00 | |

| -0.5 | -0.43 | 0.07 | 0.05 | 0.11 | 0.94 | 1.00 | |

| 0 | -0.01 | 0.06 | 0.05 | 0.11 | 0.98 | 0.11 | |

| 0 | -0.02 | 0.05 | 0.05 | 0.11 | 1.00 | 0.06 | |

| 0 | -0.02 | 0.06 | 0.06 | 0.11 | 0.99 | 0.08 | |

| 0 | -0.02 | 0.06 | 0.05 | 0.11 | 1.00 | 0.05 | |

| 0 | -0.00 | 0.05 | 0.06 | 0.11 | 1.00 | 0.01 | |

Table LABEL:table:simBinder shows the inferential results for the non-zero coefficients , as well as the zero coefficients from the third correlated block that also contains some of the non-zero coefficients, and plus arbitrarily chosen zero coefficient . The initial LASSO estimator tended to select only one of every four non-zero coefficients of the correlated covariates (data not shown), as it is known that block dependence structure is particularly challenging for the Lasso type estimators. On the other hand, the one-step estimator performed remarkably well, capturing all of the non-zero coefficients.

Compared to the results in the last part of Table LABEL:table:simFG with the same and , the block correlated covariates led to slightly more bias in , although the CI coverage remained high. The power also remained high, although in the third block with the mixed signal and noise variables the type I error rates appeared slightly high.

5 SEER-Medicare data example

The SEER-Medicare linked database contains clinical information and claims codes for patients diagnosed between and . The clinical and demographic information were collected at diagnosis, and the insurance claim data were from the year prior to diagnosis. The clinical information contained PSA, Gleason Score, AJCC stage and year of diagnosis. Demographic information included age, race, and marital status. The same data set was considered in Hou et al., (2018), where the emphasis was on variable selection and prediction error. Our focus is on testing and construction of confidence intervals.

In the following, we consider 2000 patients diagnosed during the year of 2004. The only cause for loss to follow-up was the administrative censoring at the end of the study which was year 2011. Consequently, the year of enrollment was the only factor affecting the censoring distribution. In our sample, all the subjects share the same year of enrollment 2004, so we may reasonably make the independent censoring assumption. Among them died from the cancer and had deaths unrelated to cancer. The process of identifying of the causes is detailed in Riviere et al., (2019). There were binary claims codes in the data. Here we would like to identify the risk factors for non-cancer mortality using the Fine-Gray model. We kept only the claims codes with at least and at most occurrences. The resulting dataset had covariates. We center and standardize all the covariates before performing the analysis. To determine the penalty parameters and we used 10-fold cross-validation.

In Table LABEL:table:SMdata, we present the result for 21 coefficients. Here, we focused on potential risk factors for non-cancer mortality, such as heart disease and colon cancer (different than prostate cancer); the coefficients to be tested were chosen ahead of time following recommendations from the doctors. We also include the clinical markers associated with the prostate cancer in comparison. A descriptions of the variables is given in Table LABEL:table:code_description. For each coefficient, we report the initial estimate , one-step estimate , corrected SE, the CI constructed with the corrected SE and the Wald test p-value (2-sided) calculated using the uncorrected SE.

| Variables | Initial estimate | One-step estimate and Inference | ||||

| se() | CI | p-value | ||||

| Age | 0.075 | 0.096 | 0.009 | [ 0.078, 0.114] | 2e-24∗ | |

| Marital | 0 | 0.218 | 0.147 | [-0.071, 0.507] | 0.042 | |

| Race.OvW | 0 | -0.213 | 0.224 | [-0.652, 0.225] | 0.317 | |

| Race.BvW | 0.244 | 0.528 | 0.122 | [ 0.288, 0.767] | 1e-04∗ | |

| PSA | 0 | 0.005 | 0.003 | [-0.000, 0.010] | 0.041 | |

| GleasonScore | 0 | 0.084 | 0.050 | [-0.014, 0.182] | 0.085 | |

| AJCC-T2 | 0 | -0.130 | 0.146 | [-0.418, 0.157] | 0.218 | |

| ICD-9 51881 | 0.866 | 1.357 | 0.361 | [ 0.650, 2.064] | 4e-07∗ | |

| ICD-9 4280 | 0.404 | 0.697 | 0.062 | [ 0.576, 0.818] | 2e-06∗ | |

| CPT 93015 | -0.061 | -1.042 | 0.327 | [-1.683, -0.401] | 4e-05∗ | |

| ICD-9 42731 | 0.135 | 0.459 | 0.191 | [ 0.086, 0.833] | 0.001∗ | |

| CPT 72050 | 0 | 3.718 | 0.208 | [ 3.310, 4.125] | 4e-05∗ | |

| ICD-9 6001 | 0 | -2.454 | 0.577 | [-3.585, -1.322] | 0.000∗ | |

| CPT 74170 | 0 | -1.689 | 0.288 | [-2.255, -1.124] | 0.001∗ | |

| ICD-9 2948 | 0.539 | 0.746 | 0.205 | [ 0.343, 1.148] | 0.009 | |

| ICD-9 49121 | 0.150 | 0.476 | 0.215 | [ 0.055, 0.896] | 0.015 | |

| ICD-9 2989 | 0.079 | 0.450 | 0.135 | [ 0.184, 0.715] | 0.062 | |

| ICD-9 79093 | -0.056 | -0.348 | 0.176 | [-0.693, -0.002] | 0.088 | |

| ICD-9 41189 | 0 | 1.332 | 0.434 | [ 0.480, 2.184] | 0.003∗∗ | |

| CPT 45380 | 0 | -2.250 | 0.544 | [-3.318, -1.182] | 0.003∗∗ | |

| ICD-9 3320 | 0 | 0.378 | 0.373 | [-0.353, 1.110] | 0.327 | |

-

denotes % significance after Bonferroni correction for these 21 variables, whereas denotes % significance after Bonferroni correction for these 21 variables

In Table LABEL:table:SMdata, we see that the claims codes ICD-9 4280, CPT 93015, ICD-9 42731 are all related to the heart disease, and are all significant at 5% level Bonferonni correction for the 21 variables included in the table. However, a heart attack indicator variable, ICD-9 41189, shows up significant at 10% level although the naive regularized estimator was not able to select this variable as important; this indicates that our inference procedure is much more delicate (stable) at discovering significant variables. In support of that, an indicator of a possible cancer in the abdomen, CPT 74170, is reported as significant at 5% although the initial Lasso regularized method failed to include such variable. Similar result is seen for the indicator of a fall (CPT 72050) which for an elderly person can be fatal. An indicator of a colon cancer (CPT 45380) turns out to be significant at 10% although the Lasso method set it to zero initially. Therefore, our one-step method is able to recover important risk factors that would have been missed by the initial regularized estimator.

| Code | Description |

| Age | Age at diagnosis |

| Marital | marSt1: married vs other |

| Race.OvW | Race: Other vs White |

| Race.BvW | Race: Black with White |

| PSA | PSA |

| GleasonScore | Gleason Score |

| AJCC-T2 | AJCC stage-T: T2 vs T1 |

| ICD-9 51881 | Acute respiratry failure (Acute respiratory failure) |

| ICD-9 4280 | Congestive heart failure; nonhypertensive [108.] |

| CPT 93015 | Global Cardiovascular Stress Test |

| ICD-9 42731 | Cardiac dysrhythmias [106.] |

| CPT 72050 | Diagnostic Radiology (Diagnostic Imaging) Procedures of the Spine and Pelvis |

| ICD-9 6001 | Nodular prostate |

| CPT 74170 | Diagnostic Radiology (Diagnostic Imaging) Procedures of the Abdomen |

| ICD-9 2948 | Delirium dementia and amnestic and other cognitive disorders [653] |

| ICD-9 49121 | Obstructive chronic bronchitis |

| ICD-9 2989 | Unspecified psychosis |

| ICD-9 41189 | acute and subacute forms of ischemic heart disease, other |

| CPT 45380 | Under Endoscopy Procedures on the Rectum |

| ICD-9 3320 | Parkinsons disease [79.] |

In contrast, non-life-threatening diseases, were not selected as significant predictors for the non-cancer mortality. These include Parkinson’s (ICD-9 3320), Psychosis (ICD-9 2989), Bronchitis (ICD-9 49121) and Dementia (ICD-9 2948) in the table. It is worth noting that some of these were selected by the initial estimate but were then corrected by our test. We also note that the prostate cancer related variables, PSA, Gleason Score ahd AJCC all have large -values for non-cancer mortality. This is consistent with the results in Hou et al., (2018), where under the competing risk models the predictors for a second cause only has secondary importance in predicting the events due to the first cause.

6 Discussion

This article focuses on estimation and inference under the Fine-Gray model with many more covariates than the number of events, which is well-known to be the effective sample size for survival data. The article studies the rate of convergence of a Lasso estimator and develops a new one-step estimator that can be utilized for asymptotically optimal inference: confidence intervals and testing. These results can be generalized to any sparsity-inducing and convex penalty functions including but not limited to one-step SCAD, adaptive LASSO, elastic net, to name a few. Moreover, it is worth noting that the variance estimation is novel in that it regresses a re-weighted score vector onto the score vector; in this way, the usual difficulty with asymptotic Hessian is avoided; it is worth pointing that the sandwich estimator or bootstrap carry biases in high-dimensions.

An often overlooked restriction on the time-dependent covariates , , under the Fine-Gray model is that must be observable even after the -th subject experiences a type 2 event. In practice, should be either time independent or external Kalbfleisch and Prentice, (2002). In our case the continuity conditions (C3) and (D3) are easily satisfied if the majority of the elements in are time independent, which is most likely to be the case in practice. Our theory does not apply in studies involving longitudinal variables that are supposed to be truly measured continuously over time.

We have illustrated that the method based on regularization only (without bias correction) might have severe disadvantages in many complex data situations – for example, it may potentially fail to identify relevant variables that are associated with the response. From the analysis of the SEER-medicare data, we see that variables like CPT 72050 (related to fall) or, CPT 74170 (related to diagnostic imaging of the abdomen, often for suspected malignancies) would not have been discovered as important risk factors for non-cancer mortality by regularization alone. In reality, both can be life-threatening events for an elderly patient. The one-step estimate, on the other hand, was able to detect these, therefore providing a valuable tool for practical applications. The one-step estimator is applicable as long as the model is sparse, and no minimum signal strength is required; this is another important aspect which makes the estimator more desirable for practical use than the LASSO type estimators.

Acknowledgement

We would like to acknowledge our collaboration with Dr. James Murphy of the UC San Diego Department of Radiation Medicine and Applied Sciences on the linked Medicare-SEER data analysis project that motivated this work. We would also like to thank his group for help in preparing the data set.

Appendix

In the appendix, we denote global quantities as and event sets as with subscripts labelled by their order of appearance. Other quantities are all local, i.e. only defined for the current Lemma. We denote the ordered observed type-1 event times as .

Appendix A Concentration Inequalities

Here we give the statements of the inequalities frequently used in our proofs. The notations in this section are all generic.

A.1 Classical Concentration Inequalities

Lemma A.1.

Hoeffding’s Inequality (Theorem 2 of Hoeffding, (1963) p.4) If are independent and , then for

Lemma A.2.

A version of Azuma’s Inequality (Theorem 1 and Remark 7 of Sason, (2013) p.3 and p.5) Let be a discrete-parameter real-valued martingale sequence such that for every , the condition holds almost surely for some non-negative constants . Then

A.2 Concentration Inequalities for Time-dependent Processes

Lemma A.3.

Let be i.i.d. pairs of random processes. Each is a counting process bounded by . Denote its jumps as . Let and . Suppose almost surely. Then,

-

(i)

-

(ii)

Assume in addition that each is càglàd generated by

for some and satisfying and , and for some . We have

Lemma A.4.

Let be a -adapted counting process martingales satisfying . Let be the dimensional -measurable processes such that

For , we have

-

(i)

-

(ii)

Assume in addition and . Then,

Appendix B Proofs of Main Results

We shall present our proofs in the following order. First, we give the proofs to our theorems using the main Lemmas stated in Section 3. Second, we present the auxiliary lemmas necessary for the proofs of main Lemmas. Third, we present the proofs to the main Lemmas. Lastly, we present the proofs to the our concentration inequalities and auxiliary lemmas.

B.1 Proofs of Theorems

[Proof of Theorem 1]

Observe that the same techniques as those of Huang et al., (2013) apply (see for example Lemmas 3.1 and 3.2 therein). The structure of the partial likelihood is the same as that of the Cox model modular the IPW weight functions . Following the same line of proof we can easily obtain on the event , the estimation error of LASSO estimator defined in (2.1) has the bound

| (B.1) |

where is the smaller solution to

| (B.2) |

with in the event . The proof is then completed by applying the conclusion of Lemma 1.

[Proof of Theorem 2]

In Lemma 7, we have shown that is bounded by with probability tending to one. In Lemma 3, we have shown that is bounded by . Then, we can apply Lemmas 4 and 7 to get

Note that we use the following fact

[Proof of Theorem 3]

B.2 Auxiliary Lemmas

Lemma B.1.

Lemma B.2.

Let and be defined as in (3.14). Define

| (B.3) |

Let be the observed type-1 events. Under (C1), the event

| (B.4) |

occurs with probability at least .

On , we have .

Lemma B.3.

Lemma B.4.

Lemma B.5.

Define

with and defined in (1.4) and (3.5). Let be the observed type-1 events for some . Denote and

as in (3.16) and (3.17). Under (C1) and (C3),

| (B.8) |

with , and defined in Lemmas B.2, B.3 and B.4, occurs with probability at least .

On , we have for ,

Lemma B.6.

Denote as in Lemma B.5, with and defined in (1.4) and (3.5), respectively. Under (C1), (D1) - (D3) and (D4),

-

(i)

;

, ,

and are all ;

-

(ii)

Define

(B.9) Let be a differentiable operator uniformly bounded by with , and be a adapted process in with bound . Whenever , we have

(B.10) -

(iii)

for any , ; if ,

Lemma B.7.

Lemma B.8.

Lemma B.9.

Lemma B.10.

B.3 Proof of Main Lemmas

[Proof of Lemma 1]

Let be the observed type-1 events. We may decompose the score as its martingale proxy plus an approximation error,

Recall that the counting process for observed type-1 event can be written as . Moreover, takes the form of the Cox model score with counting process and at-risk process . The “censoring complete” filtration can also be equivalently generated by . Thus, we may apply Lemma 3.3 in Huang et al., (2013) under (3.13) from (C1),

Notice that the inequality is sharper than that in Lemma A.4(i) because the compensator part of is zero.

The concentration result for approximation error

is established in Lemma B.5 on . We obtain the concentration inequality for by adding the bounds and tail probabilities together.

[Proof of Lemma 2]

Our strategy here is the same as that for Lemma 1. We first show that is lower bounded by plus a diminishing error. Since takes the form of a Cox model Hessian, we then may apply the results from Huang et al., (2013).

By Lemma 4.1 in Huang et al., (2013) (for a similar result, see van de Geer and Bühlmann, (2009) Corollary 10.1),

Let be the observed type-1 events. We can write as

with , , and defined in (1.4) and (3.5). By Lemma B.1, and are both bounded by . On the as defined in Lemma B.5, we apply Lemma B.5 once with and twice with to get

with defined in (3.17).

Our (C1) and (C2) contains all the condition for Theorem 4.1 in Huang et al., (2013). Hence, we may apply their result

with probability at least . We have bounded away from zero at all observed type-1 events in , so the term is absorbed into .

[Proof of Lemma 3]

The notations in the proof are defined in Section 2.3. Denote

Without loss of generality, we set . Since we define as the minimizer of a convex function, it must satisfy the first order condition

Recall that . Applying the first order condition, we get

We construct a vector . Then, satisfies

Hence, we have

We can directly bound

By (D2), the minimal eigenvalue of is at least . We obtain through a spectral decomposition that the maximal eigenvalue of is at most . Hence, we have

and

[Proof of Lemma 4]

By Lemma B.9, we may choose and such that defined in Lemma B.8 occurs with probability . Then, we establish the oracle inequality by Lemma B.8,

We have shown that tends to one in Lemma B.11. Hence, .

Define according to (3.28) . By Lemma B.1, . We introduce

and decompose

by the results from Theorem 3, Lemma B.6 and first part of this Lemma. Apparently, is the average of i.i.d. terms. The expectation of the summands in is defined as in (3.28). Hence, we finish the proof by applying Lemma A.1.

Along with Lemma 3, we can prove with the previous results in this Lemma, .

[Proof of Lemma 5]

We decompose

| (B.14) | ||||

| (B.15) |

By Lemma 4, . Each summand in is the integral of minus a weighted average over a counting measure . By the KKT condition and Theorem 3, . Putting these together, we obtain

| (B.16) | ||||

| (B.17) |

By the KKT condition and Theorem 1, . Hence, the first term in (B.14) is . Like in the proof of Lemma 6, we have from Lemma 3.

Define . Applying mean value theorem to , we get

for some . By Theorem 3, we have

By Lemma B.10(ii), . Along with Theorem 3 and Lemma 3, we have

[Proof of Lemma 6]

Since implies thus , we have the equivalence . Recall for the following calculation that

| and |

We decompose

We further decompose into 3 terms

By (D1) and (D3), each has one jump at observed event time and Lipschitz elsewhere. Since the is a set of independent continuous random variables, there is no tie among them with probability one. Hence, we may modify the integrand in and at observed censoring times without changing the integral. Replacing with , we can apply Lemma B.6(ii) to get that and are both .

The total variation of is at most . By Lemma B.6(i), . Hence, we obtain . Similarly, we obtain .

Besides the one in Lemma B.4, has another martingale representation. Denote the Nelson-Aalen estimator

We have a martingale

By Lemma A.4(i), For and ,

with an error

It is the discrepancy between the Kaplan-Meier and the Nelson-Aalen plus a second order Tailer expansion remainder. We shall show that it is . Since

the second order remainder

Under (C1), . Let be an observed censoring time. The increment in at is a second order remainder

Hence, . Applying the Mean Value Theorem, we obtain . Under (C1), is bounded away from zero, and is bounded from above. We have shown that both and are uniformly consistent. We obtain that is bounded away from zero and is bounded with probability tending to one. Putting these together, we obtain

Define

and , . We write as i.i.d. sum plus error through integration by parts,

is already a sum of i.i.d.. We have shown that . Hence, we have . is uniformly bounded by . It has at most one jump and is Lipschitz elsewhere. Hence, we can apply Lemma A.3(ii) to get and . Notice that , and in are all martingales. We may apply Lemmas A.4(i) and A.4(ii) to obtain , and .

By Lemma 3, we can bound the norm of by

Finally, we write as i.i.d. sum

We have because of its martingale structure. We show again by introducing its martingale proxy

The first term above is zero because of the martingale structure. The second term is zero because the IPW weights satisfy . Each is mean zero and bounded by with probability equaling one. The variance has a bounded and non-degenerating limit . Hence, satisfies the Lindeberg condition.

By Lindeberg-Feller CLT,

We conclude the proof of the Lemma.

[Proof of Lemma 7]

We define

with

Under (D1) and (C1), the total variation of is at most with probability tending to one by Lemma B.7. The difference between and is

Then, we study

We have the bound from Lemma B.1. is not measurable, but we can define a new filtration for each , such that

is a martingale. Hence, we can apply Lemma A.4(i) to get

Taking union bound, we get . Hence, .

Recall that and also take a similar form. We can likewise define

and

By Lemmas B.4, B.6(i) and B.6(iii), we have

By Lemma A.3(ii), . We only need to find the rate for

We repeat the trick for . Applying Lemma A.4(ii) to the martingale

and obtain . Hence,

Putting the rates together, we have .

We can directly obtain from Lemma A.3(ii). Define

The total variation of is at most with probability tending to one by Lemma B.7. Using the results so far, we have

The remainder

is a martingale. We can put the martingales in into a vector and apply Lemma A.4(i),

Therefore, we get .

Finally, we decompose

We have shown that . Moreover, is by Lemmas B.1 and B.7. In addition, we observe that is an average of i.i.d. terms whose expectation is defined as . By Lemmas B.1 and B.7, we have the uniform maximal bound

is also . We finish the proof by applying Lemma A.1 to the last term in the decomposition above, .

B.4 Proofs of Auxiliary Lemmas

[Proof of Lemma A.3]

-

(i)

Without loss of generality, let be the first jump time of . By the i.i.d. assumption, is independent of all with . Thus, the sequence

is a martingale with respect to filtration . The increment is bounded as

Applying Lemma A.2 to , we get . Since the dropped first term is also bounded by , we get

We use simple union bound to extend the result to all ’s whose number is at most .

-

(ii)

Define a deterministic set . By the union bound of Hoeffding’s inequality Hoeffding, (1963) , we have

Combining the result from Lemma A.3(i), we obtain

over a grid containing and jumps of . We only need to show that the variation of is sufficiently small inside each bin created by the grid.

Let and be consecutive elements by order in . By our construction, there is no jump of any of the counting processes in the interval . Otherwise, the jump time is another element in between and so that and are not consecutive elements by order. Under the assumption of the lemma, elements of all ’s are Lipschitz in . Moreover, because of the deterministic . Along with the càglàd property, we obtain a bound of variation of in

For any , we bound the variation of by

For arbitrary , we find the the corresponding bin contains . Putting the results together, we have

[Proof of Lemma A.4]

-

(i)

The summands in are the integrals of -measurable processes over -adapted martingales, so is a -adapted martingale (Kalbfleisch and Prentice, , 2002, p.165).

Suppose are the jump times of . We artificially set if has no jump in . Define be the order statistics of . Hence, is a set of ordered stopping times. Applying optional stopping theorem, we get a discrete time martingale adapted to .

The increment of comes from either the counting part or the compensator part, which we can bound separately. By our construction of ’s, each left-open right-closed bin satisfies two conditions. There is at most one jump from in the bin at . The length of the bin is at most . The increment of the martingale over is decomposed into two coordinate-wise integrals, a jump minus a compensator,

With the assumed a.s. upper bound for , we have almost surely the jump of in the bin be bounded by

Additionally with the assumed upper bound for , we have the compensator of increases over the bin by at most

We obtain a uniform concentration inequality for by Lemma A.2

Remark that the uniform version of Lemma A.2 is the application of Doob’s maximal inequality (Durrett, , 2010, Theorem 5.4.2, page 213). For , we use the bounded increment derived above

-

(ii)

Under the additional assumption , we can find for every such that

for any . We apply Lemma A.4(i) to obtain that event

occurs with probability no less than .

[Proof of Lemma B.1]

Notice all ’s are nonnegative. Hence, . We apply Hölder’s inequality for each coordinate

Hence, the maximal norm of is bounded by under (3.13). Similar result can be achieved with the sum replaced by the expectation.

To apply the result above to , and , we set as and .

[Proof of Lemma B.2]

Since are i.i.d. Bernoulli random variable, we may apply Lemma A.1 for lower tail,

By (3.14), we can find lower bounds for the probability

We may relax the inequality at to

Because and , is a lower bound for . The summands in are i.i.d. uniformly bounded by . Thus, we may apply Lemma A.3(i) with one-sided version,

By (C3), the expectation has a lower bound

We relax the inequality at ,

[Proof of Lemma B.3]

Since implies , the probability of observing a type-2 event conditioning on has an upper bound

Hence, we may derive a bound for

if we can bound away from zero with a certain whenever for some .

Under (C3), there is an interval containing of length in which has no jumps. The variation of linear predictor is bounded

So, the relative risk is greater than over . Hence, we get a lower bound for

We finish the proof by taking a union bound over .

[Proof of Lemma B.4]

Recall that is a counting process martingale adapted to complete data filtration . The Kaplan-Meier estimator has the martingale representation (Kalbfleisch and Prentice, , 2002, p.170 (5.45)),

For and ,

so we will be able to establish a concentration result for the error from Kaplan-Meier

if we first obtain a concentration result for . On event , the integrated functions are -adapted with uniform bound . The hazard by (C1). Hence, we may apply Lemma A.4(i) with to obtain

| (B.18) | |||

| (B.19) |

[Proof of Lemma B.5]

A sharper inequality is available if ’s are not time-dependent. We may exploit the martingale structure of . With general time-dependent covariates, we would decompose the approximation error into two parts, the error from Kaplan-Meier estimate and the error from missingness in ’s among the type-2 events.

Define the indicator . Since is non-zero only when , we may alternatively write

We may use the upper bound on . By Lemma B.4,

on .

Define the error from missingness in ’s among the type-2 events as

Since , Fine and Gray, (1999) has shown that

Applying tower property, we have . Hence, we can apply Lemma A.3(i) with

This finishes the proof of the first result.

We prove the other result by decomposing the differences into terms with ,

is the weighted average of , so its maximal norm is bounded by . On the event ,

We can simply plug in the bounds and tail probabilities for and in (B.8).

[Proof of Lemma B.6]

-

(i)

By (C1) and (D1), we have . Thus, all terms involved are bounded. Moreover, jumps only at the jumps of by (D3). Define the outer product of arrays and as

Between two consecutive jumps of ,

Hence, satisfies the continuity condition for Lemma A.3(ii).

Like in Lemma B.5, we first replace by . Denote . By Lemma B.4, . Then, we apply Lemma A.3(ii) to the i.i.d. mean zero process ,

Similarly,

Finally, we extend to results to the quotients by decomposition

The denominators are bounded away from zero by Lemma B.7 by choosing .

-

(ii)

First, we show that is related to the martingales . is non-zero only after an observed type-2 event. To simplify notation, we define the indicator for non-zero , .

Denote the Nelson-Aalen type estimator for censoring cumulative hazard as

Define . Let and be two consecutive observed censoring times greater than . The increment is in fact

For , we have . Thus,

(B.20) Notice does not change beyond if , i.e. an event is observed. Since , we may modify the integrand at countable many points without changing the integral

Hence, (B.20) gives an first order linear integral equation for . The general solution to the related homogeneous problem

has only one unique solution . Thus, we only need to find one specific solution to (B.20). Define an integral operator Then, the solution to can be written as

By inductively using integration by parts, we are able to calculate

Hence, the solution can be calculated as the series

Applying to (B.20), we get

with a martingale

Now, we use the martingale structure to prove the Lemma. Denote the martingale

satisfies the condition for Lemma A.4(i). Hence, we have . Also define

By Lemma B.4, . The total variation of each is at most . Hence, we can apply integration by parts to (B.10),

We have shown that and . By assumption, . As a result, we may replace the in by with with an error. Since ’s are i.i.d. mean zero random variables,

by Lemma A.1. Multiplying the rates together, we get .

can be expanded as

By Lemma B.7, . The integrand in is the product of and a term. Hence, we can apply Lemma A.4(ii) to get .

By (D3), we may further expand into

where . By assumption on and (D3), and are bounded by and , respectively. With and , we may replace the ’s by ’s with an error. Each has mean zero and at most jumps, and it is -Lipschitz between two consecutive jumps under (D3) and conditions on . By applying Lemma A.3(ii), we get

Hence, . By applying Lemma A.3(i) to

we get at the jumps of ’s, at the , satisfy

Hence, . This completes the proof.

-

(iii)

Define and . The subscript means the j-th element of corespondent vector. By mean-value theorem, we have some such that

Since each under (C1), their weighted average

Hence, we have shown that

[Proof of Lemma B.7]

Consider the event

Each is i.i.d. with expectation . Applying Lemma A.1 under (3.14) and (3.21) from (C1) and (D1), we get that occurs with probability .

Apparently, we have . Morevoer, and are both lower bounded by .

On , and

[Proof of Lemma B.8]

To simplify notation, wherever possible we will use .

-

(i)

We want to prove that for all , the differences belong to a certain convex cone.

It follows from the KKT conditions that, for ,

Denote and . For , it follows from the KKT conditions above that on the event

with ,

-

(ii)

Let be the -standardized direction for . By part (i) and convexity of in , any satisfies

We relax the inequality about above to establish an upper bound for . By the definition of , the left hand side can be bounded by

The right hand side can be bounded using the complete square ,

Combining the bounds for both sides in the inequality, we get an upper bound for .

[Proof of Lemma B.9]

We define

is the average of i.i.d. vectors with mean and maximal bound . We can apply Lemma A.1 to the matrix to get

[Proof of Lemma B.10]

- (i)

-

(ii)

We alternatively use the following form

By Lemma B.6(iii), we have

We also have a similar form for

By Lemma B.6(i), we have

Finally, we use the martingale property of

under filtration . The integrands in the first two martingale terms are bounded by . Hence, we can apply Lemma A.4(ii) to obtain that their maximal norms are both . We apply Lemma B.6(i) to the integrand of the third term, equivalently expressed as

Therefore, we obtain .

We put the rates together by the triangle inequality.

[Proof of Lemma B.11]

The proof is similar to that of Lemma 2. Define the compatibility factor for and symmetric matrix as

Apparently, . Notice that

where is a dropping its th row and column. By Lemma 4.1 in Huang et al., (2013) (for a similar result, see van de Geer and Bühlmann, (2009) Corollary 10.1),

For any non-zero , let be its embedding into defined as

Then, we may establish a lower bound for the smallest eigenvalue of by (D2)

Hence, . Using the result in Lemma B.10(i) under (D4), we have

Therefor, if , we must have that occurs with probability tending to one.

References

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43(4):1535–1567.

- Bellach et al., (2018) Bellach, A., Kosorok, M. R., Rüschendorf, L., and Fine, J. P. (2018). Weighted NPMLE for the subdistribution of a competing risk. Journal of the American Statistical Association, page (online access).

- Belloni and Chernozhukov, (2011) Belloni, A. and Chernozhukov, V. (2011). l1-penalized quantile regression in high-dimensional sparse models. The Annals of Statistics, 39(1):82–130.

- Bickel et al., (2009) Bickel, P. J., Ritov, Y., and Tsybakov, A. B. (2009). Simultaneous analysis of LASSO and Dantzig selector. The Annals of Statistics, 37(4):1705–1732.

- Binder et al., (2009) Binder, H., Allignol, A., Schumacher, M., and Beyersmann, J. (2009). Boosting for high-dimensional time-to-event data with competing risks. Bioinformatics, 25(7):890–896.

- Bradic et al., (2011) Bradic, J., Fan, J., and Jiang, J. (2011). Regularization for Cox’s proportional hazards model with NP-dimensionality. The Annals of Statistics, 39(6):3092–3120.

- Bradic and Song, (2015) Bradic, J. and Song, R. (2015). Structured estimation for the nonparametric Cox model. Electronic Journal of Statistics, 9(1):492–534.

- Bühlmann and van de Geer, (2011) Bühlmann, P. and van de Geer, S. (2011). Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media.

- Cho and Fryzlewicz, (2015) Cho, H. and Fryzlewicz, P. (2015). Multiple-change-point detection for high dimensional time series via sparsified binary segmentation. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 77(2):475–507.

- Durrett, (2010) Durrett, R. (2010). Probability: Theory and Examples, 4th edition. Cambridge University Press.

- Fan and Li, (2001) Fan, J. and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96(456):1348–1360.

- Fan and Lv, (2010) Fan, J. and Lv, J. (2010). A selective overview of variable selection in high dimensional feature space. Statistica Sinica, 20(1):101–148.

- Fang et al., (2017) Fang, E. X., Ning, Y., and Liu, H. (2017). Testing and confidence intervals for high dimensional proportional hazards models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79:1415–1437.

- Fine and Gray, (1999) Fine, J. P. and Gray, R. J. (1999). A proportional hazard model for the subdistribution of a competing risk. Journal of the American Statistical Association, 94:496–509.

- Gaïffas and Guilloux, (2012) Gaïffas, S. and Guilloux, A. (2012). High-dimensional additive hazards models and the lasso. Electronic Journal of Statistics, 6:522–546.

- Hoeffding, (1963) Hoeffding, W. (1963). Probability inequalities for sums of bounded random variables. Journal of the American Statistical Association, 58(301):13–30.

- Hou et al., (2018) Hou, J., Paravati, A., Hou, J., Xu, R., and Murphy, J. (2018). High-Dimensional Variable Selection and Prediction under Competing Risks with Application to SEER-Medicare Linked Data. Statistics in Medicine, 37:3486–3502.

- Huang et al., (2006) Huang, J., Ma, S., and Xie, H. (2006). Regularized estimation in the accelerated failure time model with high-dimensional covariates. Biometrics, 62(3):813–820.

- Huang et al., (2013) Huang, J., Sun, T., Ying, Z., Yu, Y., and Zhang, C.-H. (2013). Oracle inequalities for the LASSO in the Cox model. The Annals of Statistics, 41(3):1142–1165.

- Johnson, (2008) Johnson, B. A. (2008). Variable selection in semiparametric linear regression with censored data. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 70(2):351–370.

- Kalbfleisch and Prentice, (2002) Kalbfleisch, J. D. and Prentice, R. L. (2002). The Statistical Analysis of Failure Time Data (2nd ed.). John Wiley & Sons, Inc., Hoboken, New Jersey.

- Lemler, (2016) Lemler, S. (2016). Oracle inequalities for the lasso in the high-dimensional multiplicative Aalen intensity model. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 52(2):981–1008.

- Meinshausen and Bühlmann, (2006) Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the lasso. The Annals of Statistics, pages 1436–1462.

- Meinshausen and Yu, (2009) Meinshausen, N. and Yu, B. (2009). Lasso-type recovery of sparse representations for high-dimensional data. The Annals of Statistics, pages 246–270.

- Murphy, (1994) Murphy, S. A. (1994). Consistency in a proportional hazards model incorporating a random effect. The Annals of Statistics, 22(2):712–731.

- Obozinski et al., (2011) Obozinski, G., Wainwright, M. J., and Jordan, M. I. (2011). Support union recovery in high-dimensional multivariate regression. The Annals of Statistics, 39(1):1–47.

- Ravikumar et al., (2010) Ravikumar, P., Wainwright, M. J., and Lafferty, J. D. (2010). High-dimensional ising model selection using l1-regularized logistic regression. The Annals of Statistics, 38(3):1287–1319.

- Riviere et al., (2019) Riviere, P., Tokeshi, C., Hou, J., Nalawade, V., Sarkar, R., Paravati, A. J., Schiaffino, M., Rose, B., Xu, R., and Murphy, J. D. (2019). Claims-based approach to predict cause-specific survival in men with prostate cancer. JCO Clinical Cancer Informatics, (3):1–7.

- Sason, (2013) Sason, I. (2013). On refined versions of the Azuma-Hoeffding inequality with applications in information theory. ArXiv e-prints:1704.07989.

- Sun et al., (2014) Sun, H., Lin, W., Feng, R., and Li, H. (2014). Network-regularized high-dimensional Cox regression for analysis of genomic data. Statistica Sinica, 24(3):1433–1459.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 58(1):267–288.

- van de Geer and Bühlmann, (2009) van de Geer, S. and Bühlmann, P. (2009). On the conditions used to prove oracle results for the Lasso. Electronic Journal of Statistics, 3:1360–1392.

- van de Geer et al., (2014) van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202.

- Wasserman and Roeder, (2009) Wasserman, L. and Roeder, K. (2009). High dimensional variable selection. The Annals of Statistics, 37(5A):2178–2201.

- Yu et al., (2019) Yu, Y., Bradic, J., and Samworth, R. J. (2019). Confidence intervals for high-dimensional Cox models. to appear in Statistica Sinica.

- Zhang and Zhang, (2014) Zhang, C.-H. and Zhang, S. S. (2014). Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):217–242.

- Zhou et al., (2011) Zhou, S., Rütimann, P., Xu, M., and Bühlmann, P. (2011). High-dimensional covariance estimation based on gaussian graphical models. Journal of Machine Learning Research, 12:2975–3026.