Bayesian inference for Stable Lévy driven Stochastic Differential Equations with high-frequency data

Abstract

In this article we consider parametric Bayesian inference for stochastic differential equations (SDE) driven by a pure-jump stable Lévy process, which is observed at high frequency. In most cases of practical interest, the likelihood function is not available, so we use a quasi-likelihood and place an associated prior on the unknown parameters. It is shown under regularity conditions that there is a Bernstein-von Mises theorem associated to the posterior. We then develop a Markov chain Monte Carlo (MCMC) algorithm for Bayesian inference and assisted by our theoretical results, we show how to scale Metropolis-Hastings proposals when the frequency of the data grows, in order to prevent the acceptance ratio going to zero in the large data limit. Our algorithm is presented on numerical examples that help to verify our theoretical findings.

Keywords: Markov Chain; Monte Carlo; Lévy process; Bayesian inference; high-frequency data

1 Introduction

Stochastic differential equations (SDE) are found in a wide variety of real applications, such as finance and econometrics (see for instance [4] and the references therein), mathematical biology, movement ecology, turbulence, signal processing, to mention just a few. In this article we are concerned with Bayesian parameter estimation of discretely observed SDE driven by a pure-jump stable Lévy process with high-frequency data, which is often found in the afore-mentioned applications. Among others, we refer to [11], [24], and [25] for a comprehensive account of stable distribution and stochastic processes driven by a stable Lévy process.

Often, the main challenge with Bayesian or classical inference with Lévy driven SDE is the lack of tractability of the transition density of the process, hence one cannot evaluate a non-negative and unbiased estimate of the transition density. The latter is often required for inference methods. In such scenarios, one often has to resort to time-discretization. We focus on the time discretization induced by the quasi-likelihood approach, which, under suitable regularity conditions, enables us to deduce several desirable properties, such as consistency and asymptotic (mixed) normality; see [18, 19] and the references therein. As a result, one expects rather favorable properties of the associated posterior distribution in similar settings. In addition, one must construct inference techniques, in this article MCMC, which will turn out to be robust in the high-frequency limit. That is, algorithms that will not collapse in some sense.

Bayesian inference for diffusions and jump diffusions have been considered in many articles. This includes the fully observed (jump) diffusion case [7, 23] and the partially observed jump diffusion case [1, 6, 8, 12]. In particular the work [21] considered some related, but different classes of models to this article, except using approximate Bayesian computation [16] methods with MCMC. We note that most of the previous works do not consider quasi-likelihood and/or the large data limit of the performance of MCMC. Our contributions of this article are roughly summarized as follows:

-

•

To construct an approximate posterior distribution with favorable theoretical properties. That is, under assumptions, that there is a Bernstein-von Mises theorem associated to the posterior.

-

•

To develop an MCMC algorithm and assisted by our theoretical results, show how to scale Metropolis-Hastings proposals when the frequency of the data grows, in order to prevent the acceptance ratio going to zero in the large data limit.

This article is structured as follows. In Section 2, the model setup and an associated Bernstein-von Mises theorem are given. Our MCMC algorithm is also described. In Section 3, our theoretical results for MCMC are stated. Section 4 provides some numerical simulations which confirm our theoretical findings. We also analyze a real data set from the NYSE which features properties often captured well by the processes we study in this article. The appendix features a variety of proofs for our technical results.

2 Stable-Lévy SDEs, Model and Algorithm

2.1 Setup

Let be a complete stochastic basis. Let be a solution to the one-dimensional stochastic differential equation

| (2.1) |

where is the stable Lévy-process independent of the initial variable and such that

where it is assumed throughout that and that . Denote by the -stable density of . We will write for the image measure of associated with the parameter value

with and being bounded convex domains. The true value is denoted by . For brevity, we will also write for as well. Let denote the closure of , and write if for some universal constant .

Assumption 1 (Regularity of the coefficients).

-

1.

The functions and are globally Lipschitz and of class , and is positive for every ;

-

2.

and for each ;

-

3.

.

Assumption 2 (Identifiability conditions).

The random functions and on a.s. coincide if and only if .

The process is observed only at discrete time where with the terminal sampling time being fixed. Let , the available data set. The Euler-Maruyama discretization under is then given by

| (2.2) |

where and . This suggests to consider the following stable quasi-likelihood [19] (the multiplicative constant “” omitted):

| (2.3) |

We define the stable quasi-maximum likelihood estimator by any element

Note that is the true likelihood only when both and are constants.

It follows from [19] that under Assumptions 1 and 2 the estimator is asymptotically mixed-normally distributed: on a suitably extended probability space carrying a -dimensional standard Gaussian random variable independent of , we have

| (2.4) |

where stands for the -stable convergence in law (see [10] for details) and where denotes the a.s. positive definite quasi Fisher-information matrix specified by

with

It is known that the stable quasi-maximum likelihood estimator attains the Hajék-Le Cam minimax lower bound in some special cases, see [3] and [17]. The convergence (2.4) shows that we do have the conventional Studentization (asymptotic standard normality) result without a finite-variance property as well as any stability condition such as ergodicity.

2.2 Posterior and Markov chain Monte Carlo methods

2.2.1 Quasi-posterior distribution

The quasi-posterior distribution is given by

where denotes the prior distribution of . The -stable density does not have a closed form for , hence cannot be computed pointwise and neither then can the posterior up-to a constant; this is required for stochastic simulation algorithms such as MCMC. In general, can be only computed via certain numerical integration, the iteration of which may be rather time-consuming [15]. However, we have access to a non-negative unbiased estimate of the un-normalized posterior, which does suffice to apply (e.g.) MCMC and it may be constructed as follows. Let denote the positive -stable distribution with Laplace transform

Then, the stable distribution is the law of where and , and we have the normal variance-mixture representation:

| (2.5) |

If , and , then . Invoking (2.2) we may expect that the formal distributional approximation

under would be meaningful.

Building on the above observation, we will make use of the “complete” quasi-likelihood

where denotes the standard normal density. The corresponding posterior distribution is

Note that we can still not compute up to a constant. Nevertheless, we will still be able to devise a Metropolis-within-Gibbs MCMC algorithm which mitigates this issue.

2.2.2 MCMC Algorithm

Let . For , generate from where

| (2.6) |

and

Then update and accept with probability

This noise should be properly scaled by the rate matrix

as specified in (2.4). The random variable can be sampled via rejection sampling for each : Generate and accept it with probability

The algorithm is presented in Algorithm 1 (We write for the -dimensional Gaussian distribution with mean and covariance matrix ).

2.3 Bernstein-von Mises theorem

In this section we give a Bernstein-von Mises theorem associated with the stable quasi-likelihood (2.3). Different from the classical version [2], we will look at the convergence of the posterior distribution of the rescaled parameter centered not at , but at .

Assumption 3.

The prior distribution admits a bounded Lebesgue density which is continuous and positive at .

Let

be the logarithmic quasi-likelihood function. Following [26], we introduce the quasi-likelihood ratio random field

defined on the set . For convenience, we extend the domain of into the whole with on . Then, the quasi-posterior distribution of the rescaled parameter admits the density

Let and denote by the convergence in probability. For an -measurable random variable , we keep denoting by the -conditional Gaussian distribution associated with the characteristic function . Let denote the total variation norm of a signed measure .

3 Large sample properties of the Markov chain Monte Carlo method

In this section, we will first introduce a general framework for developing some stability properties of MCMC algorithms, and then apply it to the MCMC algorithms proposed in Section 2.2. In particular, we show how to scale the proposals when the frequency of the data grows.

3.1 Local consistency property

For a moment we step away from the main context. Notations and terminologies in this section generally follow those of [9].

3.1.1 Some general notions

Let be a normed space equipped with the Borel -algebra . For a probability measures and on , let

be the bounded Lipschitz distance between and where denotes the set of any -measurable real-valued function such that and .

Let be a family of statistical experiments and be the corresponding observation. Here, the parameter space be an open set equipped with the Borel -algebra . Let be the -measurable quasi-likelihood function which approximates the true likelihood . Let be the prior distribution for the experiments, and be the quasi-posterior distribution defined by

We shall refer to the Markov chain Monte Carlo method for the experiment if the algorithm generates a Markov chain for each . We shall refer to the empirical distribution of , that is,

for each Borel set of . Let be a non-degenerate -matrix for each . In practice, we expect that Markov chain Monte Carlo methods are robust and does not collapse as . We formalize this favourable property as follows.

Definition 1.

A family is called locally consistent if as

in -probability.

In the next subsection, we introduce a sufficient condition for this property under the general framework.

3.1.2 Sufficient conditions

Let be a probability transition kernel from to , and let be a probability transition kernel from to . Let be a measurable map. Let

where

As probability measures on , we assume that for each ,

Then for each , the probability transition kernel is -reversible, that is,

as probability measures on . Let be the Markov chain Monte Carlo method associated with the transition kernel , that is, for each , the algorithm generates a Markov chain with respect to the probability transition kernel . For simplicity, the initial point is generated from the quasi-posterior distribution, that is, .

Let . Let be a probability transition kernel from an open set to and let be a probability transition kernel from to . Let be a -valued function. For each we define a probability transition kernel

Assumption 4 (Regularity of the limit kernel).

For each , and are continuous in , and

for any compact set of .

Let be a sequence of random variables. The following proposition illustrates a sufficient condition for local consistency. See Appendix B for the proof. In the following, we call that a transition probability kernel is ergodic if it is irreducible and positive recurrent.

Proposition 3.1.

Suppose that is ergodic with invariant probability measure for each . Suppose that is -tight for each . Then, under Assumption 4, the family is locally consistent if in probability for each and

| (3.1) |

converges in -probability to .

3.2 Main result

We now go back to the main context given in Section 2.1. In Algorithm 1, the proposal distribution for observation is

for some non-degenerate matrix . We will set where is defined in Section C.1. By this setting of the proposal distribution, the following convergence is equivalent to the condition (3.1):

The acceptance probability of Algorithm 1 is

Let . We assume that and are -symmetric matrices. In the following theorem, we will show that the scaled version of the acceptance ratio converges to

where

with . By showing this, we prove that Algorithm 1 generates a locally consistent family of Markov chain Monte Carlo methods. In particular, the algorithm will not collapse in the large data limit.

Theorem 3.1 (Metropolis-within-Gibbs algorithm for the jump process).

The proof of the theorem is given in Section C.4.

4 Simulations

4.1 Simulated Example

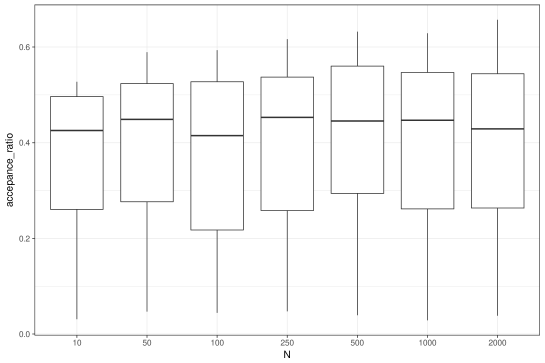

We generated seven data sets from the time discretized models with , , , and . are independently standard normal variables in the prior. Algorithm 1 was run for iterations. All simulations are repeated times. The results are given in Figure 1.

Figure 1 illustrates the average acceptance rate against the number of data. As can be seen the average acceptance rate is stable from small data to large data. In particular, the data increases the algorithm does not collapse and the acceptance rate is very reasonable. The run time of the algorithm for is only about five minutes and was coded in R (code is available upon request); the code could be substantially improved to further reduce the computation time. Note that the update on can be parallelized to improve the running speed.

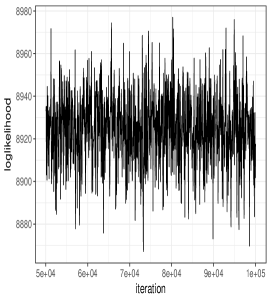

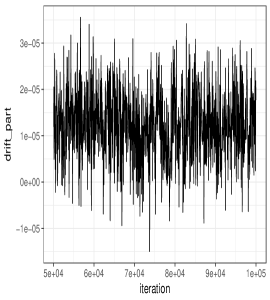

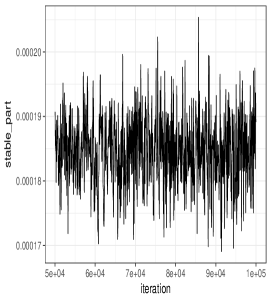

4.2 Application to IBM Stock Data

We return to the data of NYSE. In the model, we set the same model with above, and , , where is measured in minutes () and . The stable index was estimated by applying ‘stableFit’ function in R-package ‘fBasics’ [22] to . The data contains some missing values which are ignored for the purposes of the analysis. are independently normal variables in the prior with mean and standard deviation . Algorithm 1 was run for 100,000 iterations. The algorithm ran in approximately 1 hour and the acceptance rate for the move on the parameters was 0.34.

In Figures 2 and 3 we can observe our results. Figure 2 is a log-likelihood and time average drift and jump coefficients:

For this reasonable size data set, the algorithm performs well, with good mixing over the parameters. The acceptance rate is very reasonable as is the run-time - recall one can improve the code or coding language.

Figure 3 is a p-p plot of the posterior expected value of the standardized residual:

against -stable distribution. This provides an idea of the ability of this model to fit the real NYSE data. We can see that the model, to some extent, can exhibit the behaviour in the real data.

Acknowledgements

We acknowledge JST CREST Grant Number JPMJCR14D7, Japan, for supporting the research. AJ was additionally supported by Ministry of Education AcRF tier 2 grant, R-155-000-161-112, and KK was additionally supported by JSPS KAKENHI Grant Number JP16K00046.

Appendix A Proofs for the Bernstein-von Mises theorem

The purpose of this section is to prove Theorem 2.1. First, we introduce the quadratic random field

By integrating the Gaussian density,

To complete the proof it suffices to show

| (A.1) |

since the left-hand side of (2.7) can be bounded from above by the quantity

We only prove (A.1) for , since the remaining case of , where we have the single localization rate , is completely analogous and simpler.

First we will introduce a good event whose probability can get arbitrarily close to for (see (A.7) below). Let

| (A.2) | ||||

| (A.3) |

both being defined to be zero for . Also define

The random functions and represent quasi-Kullback-Leibler divergences for estimating and , respectively; we can estimate more quickly than in case of . For any matrix we will write for the Frobenius norm of . For later use we mention the following statements, which are given in [19, Section 6] or can be directly deduced from the arguments therein.

-

•

We have (recall (2.4)) under

-

•

There exists an a.s. positive random variable such that for each ,

-

•

In case of , we have

In addition, we will also need the following uniform laws of large numbers with convergence rates:

-

•

There exists a constant for which

(A.4)

A sketch of derivation of (A.4) will be given at the end of this section.

Set

| (A.5) |

with given in (A.4). Then, since

| (A.6) |

up to a multiplicative constant, we see that and ; since , the latter implies that . It is straightforward to deduce from (A.4) that

Let denote the minimum eigenvalue of a square matrix . We now introduce the event for positive constants and :

| (A.7) |

Given any , we can find a triple and an such that

holds for every and . Since the objective here is the convergence in probability, we may and do focus on the event with and being sufficiently large and small, respectively.

We divide the domain of the integration in the definition of : where

and then denote the associated integrals by and , respectively: with

We will deal with these terms separately.

First we show that . We have , where

By the third order Taylor expansion

for some random point on the segment joining and , we see that for on . Hence, under Assumption 3 we obtain

To handle , we introduce the random function

To deduce the required convergence

| (A.8) |

we make use of the subsequence argument: fix any infinite sequence . In view of the estimate

and the dominated convergence theorem, it suffices to show that there exists a further subset along which a.s. for each . We have

Since , it is possible to pick a further subset along which a.s.; note that the random sequence is free from the variable . With this , for each we have

followed by a.s., hence by (A.8). We conclude that .

Now we turn to the proof of , still focusing on the event of (A.7). Note that under (A.5) since implies that . Under the condition (A.5) we have , so that

on . Since is bounded, we are left to show that

Write and observe that (recall (A.2) and (A.3))

Since , we obtain

We will only show that

| (A.9) | ||||

| (A.10) |

Indeed, in view of the definition (A.7) of the good event , in order to deduce

we can follow exactly the same route as in the proofs of (A.9) and (A.10) below, with and replaced by and , respectively.

On we have , so that

Therefore, recalling that outside the set with being bounded, we obtain the following estimate for some positive constants and : on ,

| (A.11) |

Hence (A.9) is obtained.

It follows from (A.11) that there exist and such that for every ,

For every the sequence is tight in , hence we can make the last upper bound arbitrarily small by taking a sufficiently large . This verifies (A.10), and we are left to deduce (A.4).

Proof of (A.4). Let

Let and . Below we will repeatedly make use of several statements in [19, Sections 6.2 and 6.3], hence at this stage it should be noted that, by the localization procedure [19, Section 6.1 and the references therein], without loss of generality we may and do suppose that

for any and . This fact in particular implies that

| (A.12) |

For convenience, for a sequence of random functions on and a positive sequence we will write if .

We can write as

| (A.13) |

The function fulfills the conditions on in Lemmas 6.2 and 6.3 of [19]. Applying the two lemmas to the second and third terms in the right-hand side of (A.13), we can deduce that

Proceeding as in the second equality in Eq.(6.19) of [19], we obtain

| (A.14) |

Using the estimate (A.12) combined with the inequality given in the proof of [19, Lemma 6.4], we can deduce from (A.14) that

Hence holds for .

As for , following a similar line to the case of we can derive

Here, we also made use of [19, Corollary 6.6] (the function is odd) and the arguments in [19, Section 6.3.2]. Then it is not difficult to arrive at for any sufficiently small . In view of (A.6) we conclude that for small enough. The proof of (A.4) is thus complete.

Appendix B Proof for the local consistency of the Metropolis-Hastings algorithm

We prove Proposition 3.1 in this section. Without loss of generality, we can assume in probability for some random variable . For notational simplicity, we write for the rescaled version of the function or measure by , and write

and

The equation (3.1) becomes

By Lemmas 2 and 3 of [13] the following convergence is sufficient for local consistency:

First, we prove the convergence of . By triangular inequality, is dominated above by the sum of

For the former, by Assumption 4,

by the dominated convergence theorem, where . We can prove in the same way. On the other hand, by triangular inequality,

Hence, in probability.

Next, we prove the convergence of . By the same argument as above, it is sufficient to show the convergence of and . We only proves the former. By triangular inequality,

The first term converges to by assumption. Since converges to , and is tight, for any , we can choose a compact set and so that

Thus,

where is the upper bound of the probability density function of when . This completes the proof of in probability, and hence .

Appendix C Convergence of the acceptance ratio

C.1 Setting and notation

We keep using some notation introduced in Section A. We consider an extended probability space

| (C.1) |

where is a measurable space, and is a probability transition kernel from to . We consider a stochastic process

Fix . Set . We now consider random variables , which correspond to the pseudo-data generated in Algorithm 1 from parameter . Thus, for each , the random variables are independent, and

The log likelihood and the augmented-data (pseudo observed data) log likelihood are

Here we omit terms that do not include . We define the Fisher information matrix for the augmented-data model by

with

and that for the pseudo-data model by

with

In the next section, we will use the following law of large numbers.

Proposition C.1.

[Proposition 6.5 of [19]] If and satisfy and for some , then

| (C.2) |

C.2 Some properties of

Let

Recall that by the property of stable law (see pp.88–89 of [25]), we have as for some . Moreover, the probability density function of is bounded above, and as , we have for some , and as the density of the positive stable distribution converges to exponentially fast. Thus is continuous at for . Moreover, we have the following identities and an estimate.

Lemma C.1.

Fix .

-

1.

(C.4) -

2.

(C.5) -

3.

For any ,

(C.6)

Proof.

The expression of can be obtained via simple interchange of the derivative and the integral in the equation (2.6). For the expression of , we have

By (2.5), the second derivative of is

This equation yields the expression in (C.4) by using the identity .

Next, we prove identities (C.5). Applying the change of variable , we have

where is the probability density function of the standard normal distribution. In the same way, by the change of variable, we obtain

Then we have

and

Finally we check (C.6). By the property of stable law,

by the change of variable . Thus, the claim follows. ∎

C.3 Estimates for the likelihood functions

Let and set .

Lemma C.2.

| (C.7) |

in -probability.

Proof.

Observe that

By this fact, we have

and hence

Recall the definition of the extended probability space (C.1). In this setting, the pseudo-data variables are independent conditioned on and generated from . Fix . Since , the random variable is a sum of independent variables in . By the expression of , the covariance matrix of conditioned on becomes

This conditional covariance can be written as where

By (C.6) and Assumption 1, and satisfy the condition of Proposition C.1. On the other hand, for the forth moment on , we have

for some by (C.6) and Assumption 1 together with the Minkowski and Jensen inequalities. Therefore by Proposition C.1,

in -probability. For any infinite elements there exists a further subsequence such that the above convergence satisfies in almost surely in . Therefore, by the central limit theorem,

almost surely. Thus, the claim follows. ∎

Lemma C.3.

| (C.8) |

in -probability, and

| (C.9) |

Proof.

By calculation,

| (C.10) |

The first term of the right-hand side of (C.10) is

Then, the first term is negligible by Proposition C.2 for and by (C.3) for , and the second term is also negligible since it is a sum of independent variables conditioned on , and its variance is . Also, the second term of (C.10) is

and again, the second term is negligible since it is a sum of conditionally independent random variables. Thus, we obtain

by Proposition C.1.

Similarly, we have

The first term is by Proposition C.1 together with the fact , and the second term converges to in since it is a sum of conditionally independent random variables. Then in probability.

In the same way, decomposing the sum into the main term and the sum of independent variables, we have

The first term in the right-hand side converges to and the second term is by Lemma C.1 together with the fact that . Then, we obtain

in probability. Almost the same arguments give convergence of the thrice derivatives. We omit the detail. ∎

C.4 Proof of Theorem 3.1

The proof of Theorem 3.1 is an application of Proposition 3.1. Since and , Assumption 4 is easy to check. Ergodicity is also obvious by irreducibility. The Bernstein-von Mises theorem is already proved in Theorem 2.1 which is a sufficient condition for (3.1) in this case. We will complete the proof by showing the convergence of the acceptance ratio .

Let and . By (C.8) and (C.9) together with Taylor’s expansion, we have the difference of the log quasi-posterior density satisfies

Now we rewrite the two terms in the right-hand side of the above equation. First, observe that difference of the score function at and is

by Taylor’s expansion. Also, by , we have the following identity among Fisher information matrices:

By these facts, we can rewrite by

where

for . By the expression of the difference of the log quasi-posterior density together with the function , we have the expression of the acceptance probabilities:

where . On the other hand, we have

Hence the claim follows.

References

- [1] Barndorff-Nielsen, O. E. & Shephard, N. (2001). Non-Gaussian OU-based models and some of their uses in financial economics (with discussion). J. Roy. Statist. Soc. B, 63, 167–241.

- [2] Borwanker, J., Kallianpur, G., & Rao, B. P. (1971). The Bernstein-von Mises theorem for Markov processes. The Annals of Mathematical Statistics, 43, 1241–1253.

- [3] Clément, E. and Gloter, A. (2015). Local asymptotic mixed normality property for discretely observed stochastic differential equations driven by stable Lévy processes. Stochastic Process. Appl. 125, no. 6, 2316–2352.

- [4] Cont, R. & Tankov, P. (2004). Financial modelling with Jump Processes. Chapman & Hall: London.

- [5] Deligiannidis, G., Doucet, A., and Pitt, M. K. (2015). The Correlated Pseudo-Marginal Method. arXiv:1511.04992v2 (v2).

- [6] Gander, M. P. S. & Stephens, D. A. (2007). Simulation and inference for stochastic volatility models driven by Lévy processes. Biometrika, 94, 627–646.

- [7] Golightly, A., & Wilkinson, D. J. (2008). Bayesian inference for nonlinear multivariate diffusion models observed with error. Comp. Stat. Data Anal., 52, 1674–1693.

- [8] Griffin, J. & Steel, M. (2006). Inference with non-Gaussian Ornstein-Uhlenbeck processes for stochastic volatility. J. Econom., 134, 605–644.

- [9] Ibragimov, I. A. & Has’minskii, R. Z. (1981). Statistical estimation, asymptotic theory. New York : Springer-Verlag.

- [10] Jacod, J., and Protter, P. E. (2011). Discretization of processes. Springer.

- [11] Janicki, A. & Weron, A. (1994). Simulation and chaotic behavior of -stable stochastic processes. Monographs and Textbooks in Pure and Applied Mathematics, 178. Marcel Dekker, Inc., New York.

- [12] Jasra, A., Stephens, D. A., Doucet, A. & Tsagaris, T. (2011). Inference for Lévy driven stochastic volatility models via adaptive sequential Monte Carlo. Scand. J. Statist., 38, 1–22.

- [13] Kamatani, K. (2014). Local consistency of Markov chain Monte Carlo methods. Ann. Inst. Statist. Math., 66, 63–74.

- [14] Kamatani, K. (2017). Ergodicity of Markov chain Monte Carlo with reversible proposal. Journal of Applied Probability 54.

- [15] Matsui, M. & Takemura, A. (2006). Some improvements in numerical evaluation of symmetric stable density and its derivatives. Comm. Statist. Theory Methods, 35(1-3):149–172.

- [16] Marin, J.-M., Pudlo, P., Robert, C.P. & Ryder, R. (2012). Approximate Bayesian computational methods. Statist. Comp., 22, 1167–1180.

- [17] Masuda, H. (2009). Joint estimation of discretely observed stable Lévy processes with symmetric Lévy density. J. Japan Statist. Soc. 39, no. 1, 49–75.

- [18] Masuda, H. (2013). Convergence of Gaussian quasi-likelihood random fields for ergodic Lévy driven SDEs observed at high-frequency. Ann. Statist., 41, 1593–1641.

- [19] Masuda, H. (2017). Non-Gaussian quasi-likelihood estimation of SDE driven by locally stable Lévy process. arXiv:1608.06758 (v3)

- [20] Neal, R. M. (1999). Regression and classification using Gaussian process priors. In Bayesian statistics, 6 (Alcoceber, 1998). Oxford Univ. Press, New York pp. 475–501.

- [21] Peters G.W., Sisson S.A. & Fan Y. (2012). Likelihood-free Bayesian inference for -stable models. Comp. Stat. Data Anal., 56, 3743–3756.

- [22] Rmetrics Core Team, Wuertz, D., Setz, T., and Chalabi, Y. fBasics: Rmetrics - Markets and Basic Statistics, 2014. R package version 3011.87.

- [23] Roberts, G. O. & Stramer, O. (2001). On inference for partially observed nonlinear diffusion models using the Metropolis–Hastings algorithm. Biometrika, 88, 603–621.

- [24] Samorodnitsky, G. & Taqqu, M. S. (1994). Stable non-Gaussian random processes. Stochastic models with infinite variance. Chapman & Hall, New York.

- [25] Sato, K. (1999). Lévy processes and infinitely divisible distributions, volume 68 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge.

- [26] Yoshida, N. (2011). Polynomial type large deviation inequalities and quasi-likelihood analysis for stochastic differential equations. Ann. Inst. Statist. Math., 63, 431–479.