On the restricted almost unbiased Liu estimator in the Logistic regression model

Abstract

It is known that when the multicollinearity exists in the logistic regression model, variance of maximum likelihood estimator is unstable. As a remedy, in the context of biased shrinkage ridge estimation, Chang (2015) introduced an almost unbiased Liu estimator in the logistic regression model. Making use of his approach, when some prior knowledge in the form of linear restrictions are also available, we introduce a restricted almost unbiased Liu estimator in the logistic regression model. Statistical properties of this newly defined estimator are derived and some comparison result are also provided in the form of theorems. A Monte Carlo simulation study along with a real data example are given to investigate the performance of this estimator.

keywords:

Almost unbiased Liu estimator; Eigenvalue; Liu estimator; Mean squared error matrix; Restricted almost unbiased Liu estimatorAMS Subject Classification: Primary 62J02, Secondary 62J07

1 Introduction

Consider the following logistic regression model

| (1) |

where

| (2) |

is the expectation of when the ith value of the dependent variable is Bernoulli with parameter , denotes the unknown -vector of regression coefficients, denotes the ith row of , the data matrix, and s are independent random errors, each having zero mean and variance .

In the estimation process of coefficient , one often uses the maximum likelihood (ML) approach. Making use of the iteratively weighted least squares algorithm, the MLE is obtained as

| (3) |

where , with and .

In the context of linear regression model, when the multicollinearity exists, the ordinary least squares (OLS) estimator is no longer an efficient estimator. To overcome the problem of multicollinearity, new biased shrinkage estimators have been proposed. As such, Liu (1993) proposed the Liu estimator, the almost unbiased Liu estimator proposed by Akdeniz and Kaçıranlar (1995), the restricted Liu estimator proposed by Kaçıranlar et al. (1999), the restricted almost unbiased Liu estimator introduced by Xu and Yang (2011a,b) and more recently Asar et al. (2015) developed a two-parameter restricted Liu estimator.

In the logistic regression model, when the explanatory variables are highly correlated, the variance of the MLE becomes inflated. Dealing with such a problem, some estimators are proposed. One of them is the ridge estimator of Schaefer et al. (1984). When some prior information, in the form of restrictions on regression coefficients, are available, Duffy and Santner (1989) suggested to use the restricted MLE (RMLE).

Now, suppose we are provided with some prior information about in the form of linear restrictions

| (4) |

where is a () known matrix and denotes a vector of pre-specified known constants.

Considering such a case, Duffy and Santner (1989) defined the RMLE given by

| (5) |

where .

Mansson et al. (2011) defined the Liu estimator (LE) of in the logistic regression model given by

| (6) |

where is the biasing parameter.

Şiray et al. (2015) combined the LE and RMLE, to introduce a restricted Liu estimator (RLE) in the logistic regression model as follows

| (7) |

where is the biasing parameter.

In order to reduce the bias of LE, Chang (2015) proposed an almost unbiased Liu estimator (AULE) which has form

| (8) |

In this paper, using the latter result, a restricted almost unbiased Liu estimator will be exhibited in the logistic regression model when both multicollinearity and restrictions are present.

We organize the paper as follows: Section 2 contains the introduction of the new estimator along with some preliminary lemmas. Comparisons between this estimator with other existing ones are considered in section 3, while a numerical example is conducted in section 4. The work is concluded in section 5.

2 Proposed Estimator

In the same fashion as in Şiray et al. (2015), the AULE and RLE will be combined to obtain a new estimator namely restricted almost unbiased Liu estimator (RAULE) with form

| (9) |

where and is the biasing parameter.

Letting , the RAULE can be expressed as

| (10) |

For comparison sake and in order to derive characteristics of the RAULE, we need the following lemmas.

Lemma 2.1. (Shi, 2001) Under the assumptions of section 1, the following matrix is nonnegative definite and has rank .

Lemma 2.2. (Baksalary and Kala, 1983) Suppose that be a nonnegative definite matrix and be a vector, then

where denotes the Moore-Penrose inverse of .

Lemma 2.3.(Wang, 1994) Suppose that be a positive definite matrix and be a nonnegative definite matrix, then

Lemma 2.4.(Wang, 1994) Suppose that both and are nonnegative definite matrices, then

where is invariant of the choice of , and stands for the generalized inverse of .

In the forthcoming section, we will be deriving some properties of the proposed estimator and compare it with some existing competitors.

3 Properties & Comparison

Let be an estimator of the parameter . The matrix mean squared error (MMSE) of is defined by

| (11) |

where is the covariance matrix and

The scalar mean squared error (MSE) of is defined as

| (12) |

For two given estimators and of , the estimator is said to be superior to estimator in the sense of MMSE criterion, if and only if

| (13) |

Now, we derive the MMSE of the new estimator (RAULE).

Proposition 3.1. Under the assumptions of the logistic regression model (1), when the restrictions (4) hold, the MMSE of the new estimator is given by

| (14) |

where .

Proof: Using Eq. (9), the covariance and bias of the new estimator are respectively evaluated as

| (15) |

| (16) |

Then we obtain

| (17) |

Lemma 3.2. Under the assumptions of the logistic regression model (1), MMSE of the MLE, AULE and RMLE are respectively given by

| (18) |

| (19) |

| (20) |

In the following result, we will be presenting the necessary and sufficient conditions for the new estimator to be superior to the RMLE in the MMSE sense.

Theorem 3.3. Under the assumptions of the logistic regression model (1), assume and . Then, the RAULE is superior to the RMLE in the MMSE sense if and only if

| (21) |

where .

Proof:

The difference in MMSE is given by

| (22) | |||||

| (23) |

Since and , making use of Lemma 2.4, under the given assumptions, one obtains . Then, the result follows by applying Lemma 2.2.

Now, necessary and sufficient conditions for the new estimator to be superior to the RMLE in the MSE sense, will be given.

Theorem 3.4. Under the assumptions of the logistic regression model (1), the RAULE is superior to the RMLE in the MSE sense, if the biasing parameter satisfies the following inequality

where are the ordered eigenvalues of , is the ith diagonal element of the matrix and is the ith elements of for the orthogonal matrix .

Proof. Consider the MSE difference

| (24) | |||||

| (25) | |||||

| (26) |

Differentiating with respect to , gives

| (27) | |||||

The result follows whenever

Now, we give comparison result between the RAULE and MLE in the MMSE sense.

Theorem 3.5. Under the assumptions of the logistic regression model (1), when

,

RAULE is superior to the

MLE in the MMSE sense if

and only if

| (28) |

where .

Proof.

The difference in MMSE is given by

| (29) | |||||

| (30) |

Since and , applying Lemma 2.3 yields . Then the result follows applying Lemma 2.2.

Theorem 3.6. Under the assumptions of the logistic regression model (1), when

the RAULE is superior to MLE in the sense of MSE criterion.

Proof. Consider the MSE difference given by

| (31) | |||||

| (32) | |||||

| (34) | |||||

Since

we have . Hence , using Theorem 3.4.

Finally we present the comparison between the RAULE and AULE in the MMSE sense.

Theorem 3.7. Under the assumptions of the logistic regression model (1), the RAULE is always superior to AULE in the MMSE sense.

Proof.

Consider the following difference in MMSE

| (35) | |||||

| (36) | |||||

| (37) |

Making use of Lemma 2.1, and the proof is complete.

Corollary 3.1. The RAULE is always superior to the AULE in the MSE sense.

4 Monte Carlo Simulation

4.1 The design of the simulation

In this section, we conduct a Monte Carlo simulation to compare the performances of the MLE, AULE, RMLE and RAULE under different scenarios. Since we want to compare the estimators when there multicollinearity is present, the main factor of the simulation is the degree of correlation among the explanatory variables. Hence, following Gibbons (1981) and Kibria (2003), we use the following formula to generate correlated variables:

| (38) |

where s are independent standard normal pseudo-random numbers. We consider three different values of the degree of correlation corresponding to and .

The number of observations is generated using the Bernoulli distribution with parameter such that

| (39) |

for the dependent variable.

We fit logistic regression models having and explanatory variables. We consider the sample sizes and . The parameter values of are chosen so that .

Following Månsson et al. (2015), we use different restriction matrices, to capture the effect of imposing restrictions on estimators, as follows:

I) with when and

II) with when .

The simulation is replicated times and estimated MSE is evaluated using

where is any estimator considered in this study, in the rth repetition.

4.2 Results of the simulation

We summarized the estimated MSE values of the estimators in Tables 1-6. It can be observed that an increase in the degree of correlation affects the MSE values of the estimators negatively. It is also observed that MSE has the worst performance (having the most MSE values) in all of the situations considered. The RMLE has always less MSE than that of MLE.

The performances of the AULE and RAULE depend on the parameter . The smaller the value of , the better performance. The RMLE has lesser MSE value than AULE when in almost all cases.

Moreover, it can be deduced that our new estimator RAULE has always the least MSE value. Especially, the RAULE is the most robust option against the correlation when the value of is small.

From tables, it is realized that an increase in the sample size causes a decrease in the MSE values. Increasing the number of explanatory variables also affects the performances of the estimator negatively. Again the newly proposed RAULE is the most robust option for this situation.

| MLE | 14.6207 | 14.6207 | 14.6207 | 14.6207 | 14.6207 | 14.6207 | 14.6207 | 14.6207 | 14.6207 | 14.6207 |

|---|---|---|---|---|---|---|---|---|---|---|

| AULE | 2.4696 | 4.0121 | 5.8178 | 7.7198 | 9.5737 | 11.2573 | 12.6704 | 13.7354 | 14.3966 | 14.6185 |

| RMLE | 3.3376 | 3.3376 | 3.3376 | 3.3376 | 3.3376 | 3.3376 | 3.3376 | 3.3376 | 3.3376 | 3.3376 |

| RAULE | 0.9280 | 1.2590 | 1.6281 | 2.0065 | 2.3691 | 2.6946 | 2.9658 | 3.1692 | 3.2950 | 3.3372 |

| MLE | 122.8774 | 122.8774 | 122.8774 | 122.8774 | 122.8774 | 122.8774 | 122.8774 | 122.8774 | 122.8774 | 122.8774 |

| AULE | 6.3439 | 18.3859 | 34.4887 | 52.5983 | 70.9343 | 87.9906 | 102.5346 | 113.6079 | 120.5258 | 122.8537 |

| RMLE | 17.6015 | 17.6015 | 17.6015 | 17.6015 | 17.6015 | 17.6015 | 17.6015 | 17.6015 | 17.6015 | 17.6015 |

| RAULE | 1.4451 | 3.2122 | 5.4877 | 8.0031 | 10.5255 | 12.8580 | 14.8392 | 16.3440 | 17.2826 | 17.5983 |

| MLE | 2988.9881 | 2988.9881 | 2988.9881 | 2988.9881 | 2988.9881 | 2988.9881 | 2988.9881 | 2988.9881 | 2988.9881 | 2988.9881 |

| AULE | 109.4131 | 389.4573 | 779.6334 | 1226.2873 | 1682.9183 | 2110.1799 | 2475.8795 | 2754.9782 | 2929.5914 | 2988.3912 |

| RMLE | 279.7609 | 279.7609 | 279.7609 | 279.7609 | 279.7609 | 279.7609 | 279.7609 | 279.7609 | 279.7609 | 279.7609 |

| RAULE | 10.7511 | 37.0637 | 73.5805 | 115.3140 | 157.9420 | 197.8068 | 231.9161 | 257.9424 | 274.2231 | 279.7052 |

| MLE | 5.7257 | 5.7257 | 5.7257 | 5.7257 | 5.7257 | 5.7257 | 5.7257 | 5.7257 | 5.7257 | 5.7257 |

|---|---|---|---|---|---|---|---|---|---|---|

| AULE | 2.5062 | 3.0270 | 3.5549 | 4.0642 | 4.5327 | 4.9417 | 5.2757 | 5.5229 | 5.6746 | 5.7252 |

| RMLE | 1.7583 | 1.7583 | 1.7583 | 1.7583 | 1.7583 | 1.7583 | 1.7583 | 1.7583 | 1.7583 | 1.7583 |

| RAULE | 1.1074 | 1.2195 | 1.3292 | 1.4325 | 1.5259 | 1.6063 | 1.6714 | 1.7192 | 1.7484 | 1.7582 |

| MLE | 50.0384 | 50.0384 | 50.0384 | 50.0384 | 50.0384 | 50.0384 | 50.0384 | 50.0384 | 50.0384 | 50.0384 |

| AULE | 4.2987 | 9.4622 | 15.9754 | 23.1044 | 30.2129 | 36.7629 | 42.3141 | 46.5238 | 49.1475 | 50.0294 |

| RMLE | 9.8945 | 9.8945 | 9.8945 | 9.8945 | 9.8945 | 9.8945 | 9.8945 | 9.8945 | 9.8945 | 9.8945 |

| RAULE | 1.5374 | 2.5562 | 3.7795 | 5.0856 | 6.3692 | 7.5410 | 8.5281 | 9.2737 | 9.7373 | 9.8929 |

| MLE | 461.9003 | 461.9003 | 461.9003 | 461.9003 | 461.9003 | 461.9003 | 461.9003 | 461.9003 | 461.9003 | 461.9003 |

| AULE | 18.9701 | 62.9223 | 123.3250 | 192.0703 | 262.1311 | 327.5616 | 383.4969 | 426.1535 | 452.8284 | 461.8091 |

| RMLE | 124.0645 | 124.0645 | 124.0645 | 124.0645 | 124.0645 | 124.0645 | 124.0645 | 124.0645 | 124.0645 | 124.0645 |

| RAULE | 5.5594 | 17.3608 | 33.5400 | 51.9347 | 70.6708 | 88.1627 | 103.1129 | 114.5124 | 121.6405 | 124.0402 |

| MLE | 2.4237 | 2.4237 | 2.4237 | 2.4237 | 2.4237 | 2.4237 | 2.4237 | 2.4237 | 2.4237 | 2.4237 |

|---|---|---|---|---|---|---|---|---|---|---|

| AULE | 1.8950 | 1.9963 | 2.0899 | 2.1743 | 2.2481 | 2.3100 | 2.3592 | 2.3949 | 2.4165 | 2.4237 |

| RMLE | 1.1825 | 1.1825 | 1.1825 | 1.1825 | 1.1825 | 1.1825 | 1.1825 | 1.1825 | 1.1825 | 1.1825 |

| RAULE | 1.0220 | 1.0532 | 1.0818 | 1.1074 | 1.1297 | 1.1484 | 1.1632 | 1.1739 | 1.1803 | 1.1825 |

| MLE | 18.7164 | 18.7164 | 18.7164 | 18.7164 | 18.7164 | 18.7164 | 18.7164 | 18.7164 | 18.7164 | 18.7164 |

| AULE | 3.4884 | 5.5229 | 7.8305 | 10.2190 | 12.5219 | 14.5982 | 16.3327 | 17.6356 | 18.4430 | 18.7137 |

| RMLE | 4.8649 | 4.8649 | 4.8649 | 4.8649 | 4.8649 | 4.8649 | 4.8649 | 4.8649 | 4.8649 | 4.8649 |

| RAULE | 1.4912 | 1.9655 | 2.4871 | 3.0174 | 3.5228 | 3.9750 | 4.3508 | 4.6321 | 4.8061 | 4.8643 |

| MLE | 168.3497 | 168.3497 | 168.3497 | 168.3497 | 168.3497 | 168.3497 | 168.3497 | 168.3497 | 168.3497 | 168.3497 |

| AULE | 8.5172 | 24.9718 | 47.0305 | 71.8658 | 97.0272 | 120.4414 | 140.4116 | 155.6186 | 165.1198 | 168.3173 |

| RMLE | 52.5252 | 52.5252 | 52.5252 | 52.5252 | 52.5252 | 52.5252 | 52.5252 | 52.5252 | 52.5252 | 52.5252 |

| RAULE | 3.0800 | 8.1803 | 15.0086 | 22.6921 | 30.4739 | 37.7139 | 43.8883 | 48.5895 | 51.5267 | 52.5151 |

| MLE | 141.9664 | 141.9664 | 141.9664 | 141.9664 | 141.9664 | 141.9664 | 141.9664 | 141.9664 | 141.9664 | 141.9664 |

|---|---|---|---|---|---|---|---|---|---|---|

| AULE | 8.3150 | 22.3253 | 40.8815 | 61.6607 | 82.6499 | 102.1456 | 118.7542 | 131.3918 | 139.2840 | 141.9395 |

| RMLE | 42.1899 | 42.1899 | 42.1899 | 42.1899 | 42.1899 | 42.1899 | 42.1899 | 42.1899 | 42.1899 | 42.1899 |

| RAULE | 3.5096 | 7.7610 | 13.2181 | 19.2412 | 25.2760 | 30.8532 | 35.5891 | 39.1851 | 41.4281 | 42.1823 |

| MLE | 1270.2249 | 1270.2249 | 1270.2249 | 1270.2249 | 1270.2249 | 1270.2249 | 1270.2249 | 1270.2249 | 1270.2249 | 1270.2249 |

| AULE | 48.8557 | 168.8119 | 334.8236 | 524.3276 | 717.7695 | 898.6031 | 1053.2906 | 1171.3026 | 1245.1183 | 1269.9726 |

| RMLE | 368.8009 | 368.8009 | 368.8009 | 368.8009 | 368.8009 | 368.8009 | 368.8009 | 368.8009 | 368.8009 | 368.8009 |

| RAULE | 15.1951 | 50.3383 | 98.5839 | 153.4681 | 209.3890 | 261.6062 | 306.2416 | 340.2786 | 361.5626 | 368.7282 |

| MLE | 46865.2930 | 46865.2930 | 46865.2930 | 46865.2930 | 46865.2930 | 46865.2930 | 46865.2930 | 46865.2930 | 46865.2930 | 46865.2930 |

| AULE | 1693.7814 | 6076.5807 | 12192.7161 | 19198.8276 | 26364.0035 | 33069.7799 | 38810.1409 | 43191.5188 | 45932.7934 | 46855.9216 |

| RMLE | 12492.1038 | 12492.1038 | 12492.1038 | 12492.1038 | 12492.1038 | 12492.1038 | 12492.1038 | 12492.1038 | 12492.1038 | 12492.1038 |

| RAULE | 452.1749 | 1620.7160 | 3251.0570 | 5118.4698 | 7028.1898 | 8815.4162 | 10345.3121 | 11513.0044 | 12243.5835 | 12489.6063 |

| MLE | 26.2009 | 26.2009 | 26.2009 | 26.2009 | 26.2009 | 26.2009 | 26.2009 | 26.2009 | 26.2009 | 26.2009 |

|---|---|---|---|---|---|---|---|---|---|---|

| AULE | 4.6742 | 7.4254 | 10.6324 | 14.0028 | 17.2834 | 20.2599 | 22.7567 | 24.6377 | 25.8052 | 26.1969 |

| RMLE | 11.8713 | 11.8713 | 11.8713 | 11.8713 | 11.8713 | 11.8713 | 11.8713 | 11.8713 | 11.8713 | 11.8713 |

| RAULE | 2.7895 | 4.0017 | 5.3773 | 6.8017 | 8.1754 | 9.4141 | 10.4490 | 11.2264 | 11.7082 | 11.8697 |

| MLE | 309.5121 | 309.5121 | 309.5121 | 309.5121 | 309.5121 | 309.5121 | 309.5121 | 309.5121 | 309.5121 | 309.5121 |

| AULE | 14.7981 | 44.9405 | 85.5269 | 131.3111 | 177.7461 | 220.9848 | 257.8793 | 285.9813 | 303.5420 | 309.4521 |

| RMLE | 141.9314 | 141.9314 | 141.9314 | 141.9314 | 141.9314 | 141.9314 | 141.9314 | 141.9314 | 141.9314 | 141.9314 |

| RAULE | 7.5535 | 21.5523 | 40.1706 | 61.0585 | 82.1795 | 101.8102 | 118.5408 | 131.2744 | 139.2280 | 141.9042 |

| MLE | 3051.3774 | 3051.3774 | 3051.3774 | 3051.3774 | 3051.3774 | 3051.3774 | 3051.3774 | 3051.3774 | 3051.3774 | 3051.3774 |

| AULE | 113.5289 | 400.3017 | 798.8422 | 1254.5856 | 1720.2427 | 2155.7995 | 2528.5172 | 2812.9323 | 2990.8567 | 3050.7692 |

| RMLE | 1382.3472 | 1382.3472 | 1382.3472 | 1382.3472 | 1382.3472 | 1382.3472 | 1382.3472 | 1382.3472 | 1382.3472 | 1382.3472 |

| RAULE | 52.1509 | 182.3238 | 362.9193 | 569.2861 | 780.0596 | 977.1620 | 1145.8025 | 1274.4772 | 1354.9689 | 1382.0721 |

| MLE | 6.6427 | 6.6427 | 6.6427 | 6.6427 | 6.6427 | 6.6427 | 6.6427 | 6.6427 | 6.6427 | 6.6427 |

|---|---|---|---|---|---|---|---|---|---|---|

| AULE | 3.9466 | 4.4224 | 4.8819 | 5.3103 | 5.6947 | 6.0240 | 6.2895 | 6.4841 | 6.6028 | 6.6423 |

| RMLE | 4.1607 | 4.1607 | 4.1607 | 4.1607 | 4.1607 | 4.1607 | 4.1607 | 4.1607 | 4.1607 | 4.1607 |

| RAULE | 2.6886 | 2.9525 | 3.2052 | 3.4393 | 3.6483 | 3.8268 | 3.9703 | 4.0752 | 4.1392 | 4.1604 |

| MLE | 74.7216 | 74.7216 | 74.7216 | 74.7216 | 74.7216 | 74.7216 | 74.7216 | 74.7216 | 74.7216 | 74.7216 |

| AULE | 7.8025 | 15.6628 | 25.3268 | 35.7714 | 46.1097 | 55.5915 | 63.6028 | 69.6663 | 73.4407 | 74.7088 |

| RMLE | 39.4314 | 39.4314 | 39.4314 | 39.4314 | 39.4314 | 39.4314 | 39.4314 | 39.4314 | 39.4314 | 39.4314 |

| RAULE | 5.0776 | 9.2535 | 14.2768 | 19.6453 | 24.9242 | 29.7452 | 33.8072 | 36.8760 | 38.7842 | 39.4249 |

| MLE | 815.6036 | 815.6036 | 815.6036 | 815.6036 | 815.6036 | 815.6036 | 815.6036 | 815.6036 | 815.6036 | 815.6036 |

| AULE | 33.8851 | 111.8311 | 218.6004 | 339.9454 | 463.5184 | 578.8710 | 677.4549 | 752.6211 | 799.6205 | 815.4430 |

| RMLE | 411.3009 | 411.3009 | 411.3009 | 411.3009 | 411.3009 | 411.3009 | 411.3009 | 411.3009 | 411.3009 | 411.3009 |

| RAULE | 18.0382 | 57.6046 | 111.4736 | 172.5361 | 234.6310 | 292.5449 | 342.0125 | 379.7161 | 403.2862 | 411.2203 |

5 Application

In this section, we present a real data application in order to show the benefit of using the newly proposed RAULE. For our purpose, we used a data set available at an official web page of Statistics Sweden (http://www.scb.se/). The observations are 83 municipalities which are the urban regions belonging to the functional analysis regions Stockholm, Malmo and Goteborg. Asar and Genc (2015) and Mansson et al. (2012) also analyzed similar data sets. We model the data using a binary logistic regression model such that the dependent variable is coded as 1 if there is an increase in the pupation and 0 if there is a decrease. The dependent variable is explained by the following explanatory variables:

X1: The population,

X2: The number of unemployed people,

X3: The number of newly constructed buildings,

X4: The number of bankrupt firms.

The correlation matrix of this data set is given in Table 7. It is

observed from Table 7 that all the bivariate correlations between

the explanatory variables are larger than 0.95. The condition

number, being a measure of the degree of multicollinearity, is

computed according to

which shows that there exists a severe multicollinearity problem.

| X1 | X2 | X3 | X4 | |

|---|---|---|---|---|

| X1 | 1.0000 | 0.9937 | 0.9707 | 0.9514 |

| X2 | 0.9937 | 1.0000 | 0.9527 | 0.9222 |

| X3 | 0.9707 | 0.9527 | 1.0000 | 0.9765 |

| X4 | 0.9514 | 0.9222 | 0.9765 | 1.0000 |

| d | MSE | ||||

|---|---|---|---|---|---|

| 0.1 | 5.0078 | -3.1222 | 0.8875 | -2.0282 | 70.9595 |

| 0.2 | 9.2699 | -6.1203 | 1.5128 | -3.9040 | 248.9311 |

| 0.3 | 13.0305 | -8.7656 | 2.0645 | -5.5592 | 496.2849 |

| 0.4 | 16.2896 | -11.0583 | 2.5427 | -6.9937 | 779.1508 |

| 0.5 | 19.0474 | -12.9982 | 2.9473 | -8.2075 | 1068.1749 |

| 0.6 | 21.3038 | -14.5854 | 3.2784 | -9.2006 | 1338.5192 |

| 0.7 | 23.0587 | -15.8199 | 3.5359 | -9.9730 | 1569.8617 |

| 0.8 | 24.3122 | -16.7017 | 3.7198 | -10.5248 | 1746.3963 |

| 0.9 | 25.0644 | -17.2307 | 3.8301 | -10.8558 | 1856.8330 |

| 0.99 | 25.3126 | -17.4053 | 3.8666 | -10.9650 | 1894.0204 |

| d | MSE | ||||

|---|---|---|---|---|---|

| 0.1 | 0.5427 | 0.5772 | 0.4917 | -0.8105 | 4.3052 |

| 0.2 | 0.8249 | 0.8521 | 0.7846 | -1.5974 | 12.2573 |

| 0.3 | 1.0739 | 1.0947 | 1.0430 | -2.2917 | 23.0005 |

| 0.4 | 1.2896 | 1.3050 | 1.2670 | -2.8934 | 35.1374 |

| 0.5 | 1.4722 | 1.4829 | 1.4565 | -3.4026 | 47.4568 |

| 0.6 | 1.6216 | 1.6284 | 1.6115 | -3.8192 | 58.9338 |

| 0.7 | 1.7378 | 1.7416 | 1.7321 | -4.1432 | 68.7299 |

| 0.8 | 1.8208 | 1.8225 | 1.8183 | -4.3747 | 76.1930 |

| 0.9 | 1.8706 | 1.8710 | 1.8699 | -4.5135 | 80.8572 |

| 0.99 | 1.8870 | 1.8870 | 1.8870 | -4.5594 | 82.4270 |

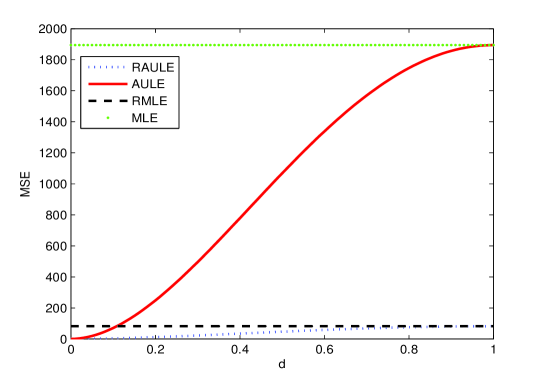

We computed the estimated theoretical MSE values along with the coefficients of the estimators. The MSE of MLE is 1894.398 which is the largest among others. The coefficients of MLE are 25.3151, -17.4071, 3.8669 and -10.9661. The MSE of RMLE is 82.4430 and the coefficients of RMLE are 1.8872, 1.8872, 1.8872 and -4.5598. MSE values and the coefficients of AULE and RAULE are given in Tables 8 and 9 respectively for different biasing parameter varying from zero to one.

According to Tables 8-9, the RAULE has the least MSE value for all values of the parameter . When , the MSE of RAULE becomes equal to that of RMLE as expected. The MSE of AULE is lower than that of RMLE when . We also provided the plot of the MSE versus in Figure 1. According to Figure 1, the RAULE has the best performance among other estimators.

6 Conclusions

In this paper, we proposed a restricted almost unbiased Liu estimator in the logistic regression model. Then, its performance compared with other competitors including the MLE, AULE, RMLE in the logistic regression model through providing some theorems, a Monte Carlo simulation as well as a real example. We concluded that our proposed estimator is superior compared to all others in the sense of having smaller MSE value.

References

- [1] Akdeniz, F. and Kaçıranlar, S. (1995). On the almost unbiased generalized Liu estimator and unbiased estimation of the bias and MSE. Comm. Statist. Theo. Meth. 24:1789-1797.

- [2] Asar, Y., Genc, A. (2015). New Shrinkage Parameters for the Liu-type Logistic Estimators. Comm. Statist. Sim. Comp.. DOI:10.1080/03610918.2014.995815.

- [3] Asar, Y., Erisoglu M. and Arashi, M. (2015). Developing a restricted two-parameter Liu-type estimator: A comparison of restricted estimators in the binary logistic regression model. Comm. Statist. Theo. Meth.. Accepted.

- [4] Baksalary, J.K., Kala, R. (1983). Partial orderings between matrices one of which is of rank one. Bull. Polish Academy Sci.. Mathematics, 31:5-7.

- [5] Duffy, D. E., Santner, T. J . (1989). On the small sample properties of norm-restricted maximum likelihood estimators for logistic regression models. Comm. Statist. Theo. Meth.. 18:959-980.

- [6] Kaçıranlar, S ., Sakalloglu, S., Akdeniz, F., Styan, G. P. H., Werner, H. J . (1999). A new biased estimator in linear regression and a detailed analysis of the widely analyzed dataset on Portland cement. Sankhya. 31:443-459.

- [7] Kibria, B . M . G. (2003). Performance of some new ridge regression estimators. Comm. Statist. Theo. Meth. 32:419-435

- [8] Liu, K. (1993). A new class of biased estimate in linear regression. Comm. Statist. Theo. Meth.. 22:393-402.

- [9] Mansson, K., Kibria, B. M. G., Shukur, G. (2011). On Liu estimators for the logit regression model. Royal Inst. Tech.(CESIS). Sweden, Paper No. 259.

- [10] Mansson, K., Kibria, B. G., Shukur, G. (2012). On Liu estimators for the logit regression model. Economic Model., 29(4):1483-1488.

- [11] Muniz, G., Kibria, B. M. G. (2009). On some ridge regression estimators: An Empirical Comparisons. Comm. Statist. Sim. Comp.. 38:621-630.

- [12] Schaefer, R . L ., Roi, L. D., Wolfe, R . A. (1984). A ridge logistic estimator. Comm. Statist. Theo. Meth.. 13:99-113.

- [13] Şiray, G.U., Toker, S., Kaçıranlar, S. (2015). On the Restricted Liu Estimator in the Logistic Regression Model. Comm. Statist. Sim. Comp. 44:217-232.

- [14] Shi, J.H. (2001). The conditional ridge-type estimation of regression coefficient in restricted linear regression model. J. Shanxi Teachers Univ. Natural Sci. Ed.. 15:10-16.

- [15] Wang, S. (1994). The Inequalities of Matrices. (Hefei: The Education of Anhui Press).

- [16] Xu, J. W., Yang, H, (2011a). More on the bias and variance comparisons of the restricted almost unbiased estimators. Comm. Statist. Theo. Meth. 40:4053-4064.

- [17] Xu, J. W., Yang, H., (2011b). On the restricted almost unbiased estimators in linear regression. J. Appl. Statist. 38:605-617.

- [18] Gibbons, D.G., (1981). A simulation study of some ridge estimators, J. Amer. Statist. Assoc. 76:131–139.

- [19] Månsson, K., Golam Kibria, B. M., and Shukur, G. (2015). A restricted Liu estimator for binary regression models and its application to an applied demand system. J. Appl. Statist., 1-9. http://dx.doi.org/10.1080/02664763.2015.1092110