Asymptotically Optimal Load Balancing Topologies

Abstract

We consider a system of servers inter-connected by some underlying graph topology . Tasks with unit-mean exponential processing times arrive at the various servers as independent Poisson processes of rate . Each incoming task is irrevocably assigned to whichever server has the smallest number of tasks among the one where it appears and its neighbors in .

The above model arises in the context of load balancing in large-scale cloud networks and data centers, and has been extensively investigated in the case is a clique. Since the servers are exchangeable in that case, mean-field limits apply, and in particular it has been proved that for any , the fraction of servers with two or more tasks vanishes in the limit as . For an arbitrary graph , mean-field techniques break down, complicating the analysis, and the queue length process tends to be worse than for a clique. Accordingly, a graph is said to be -optimal or -optimal when the queue length process on is equivalent to that on a clique on an -scale or -scale, respectively.

We prove that if is an Erdős-Rényi random graph with average degree , then with high probability it is -optimal and -optimal if and as , respectively. This demonstrates that optimality can be maintained at -scale and -scale while reducing the number of connections by nearly a factor and compared to a clique, provided the topology is suitably random. It is further shown that if contains bounded-degree nodes, then it cannot be -optimal. In addition, we establish that an arbitrary graph is -optimal when its minimum degree is , and may not be -optimal even when its minimum degree is for any . Simulation experiments are conducted for various scenarios to corroborate the asymptotic results.

1 Introduction

Background and motivation.

In the present paper we explore the impact of the network topology on the performance of load-balancing schemes in large-scale systems. Load balancing algorithms play a key role in distributing service requests or tasks (e.g. compute jobs, data base look-ups, file transfers, transactions) among servers in parallel-processing systems. Well-designed load balancing schemes provide an effective mechanism for improving relevant performance metrics experienced by users while achieving high resource utilization levels. The analysis and design of load balancing algorithms has attracted strong renewed interest in recent years, mainly urged by huge scalability challenges in large-scale cloud networks and data centers with immense numbers of servers.

In order to examine the impact of the network topology, we focus on a system of servers inter-connected by some underlying graph . Tasks with unit-mean exponential processing times arrive at the various servers as independent Poisson processes of rate . Each incoming task is immediately assigned to whichever server has the smallest number of tasks among the one where it arrives and its neighbors in .

The above model has been extensively investigated in case is a clique. In that case, each task is assigned to the server with the smallest number of tasks across the entire system, which is commonly referred to as the Join-the-Shortest Queue (JSQ) policy. Under the above Markovian assumptions, the JSQ policy has strong stochastic optimality properties [8, 34, 24, 25]. Specifically, the queue length process is better balanced and smaller in a majorization sense than under any alternative non-anticipating task assignment strategy that does not have advance knowledge of the service times. By implication, the JSQ policy minimizes the mean overall queue length, and hence the mean waiting time as well. Since the servers are exchangeable in a clique topology, the queue length process is in fact quite tractable via mean-field limits. In particular, it can be shown that for any , the stationary fraction of servers with two or more tasks as well as the mean waiting time vanish in the limit as .

Unfortunately, however, implementation of the JSQ policy in a clique topology raises two fundamental scalability concerns. First of all, for each incoming task the queue lengths need to be checked at all servers, giving rise to a prohibitive communication overhead in large-scale systems with massive numbers of servers. Second, executing a task commonly involves the use of some data, and storing such data for all possible tasks on all servers will typically require an excessive amount of storage capacity [35, 32]. These two burdens can be effectively mitigated in sparser graph topologies where tasks that arrive at a specific server are only allowed to be forwarded to a subset of the servers . For the tasks that arrive at server , queue length information then only needs to be obtained from servers in , and it suffices to store replicas of the required data on the servers in . The subset containing the peers of server can be naturally viewed as its neighbors in some graph topology . In the present paper we consider the case of undirected graphs, but most of the analysis can be extended to directed graphs.

While sparser graph topologies relieve the scalability issues associated with a clique, they defy classical mean-field techniques, and the queue length process will be worse (in the majorization sense) because of the limited connectivity. Surprisingly, however, even much sparser graphs can asymptotically match the optimal performance of a clique, provided they are suitably random, as we will further describe below.

Related work.

The above model has been studied in [11, 28], focusing on certain fixed-degree graphs and in particular ring topologies. The results demonstrate that the flexibility to forward tasks to a few neighbors, or even just one, with possibly shorter queues significantly improves the performance in terms of the waiting time and tail distribution of the queue length. This resembles the so-called ‘power-of-two’ effect in the classical case of a complete graph where tasks are assigned to the shortest queue among servers selected uniformly at random. As shown by Mitzenmacher [16, 17] and Vvedenskaya et al. [31], such a ‘power-of-’ scheme provides a huge performance improvement over purely random assignment, even when , in particular super-exponential tail decay, translating into far better waiting-time performance. Further related problems have been investigated in [15, 2, 14, 18]. However, the results in [11, 28] also establish that the performance sensitively depends on the underlying graph topology, and that selecting from a fixed set of neighbors typically does not match the performance of re-sampling alternate servers for each incoming task from the entire population, as in the power-of- scheme in a complete graph. In contrast, when the number of neighbors grows with the total number of servers , our results indicate that the performance impact of the graph topology diminishes, and that, remarkably, a broad class of suitably random topologies match the asymptotically optimal performance that is achieved in a clique or when alternate servers are resampled for each incoming task [20].

If tasks do not get served and never depart but simply accumulate, then our model as described above amounts to a so-called balls-and-bins problem on a graph. Viewed from that angle, a close counterpart of our problem is studied in Kenthapadi and Panigrahy [13], where in our terminology each arriving task is routed to the shortest of randomly selected neighboring queues. In this setup they show that if the underlying graph is almost regular with degree , where is not too small, the maximum number of balls in a bin scales as . This scaling is the same as in the case when the underlying graph is a clique [3]. In a more recent paper by Peres, Talwar, and Weider [23] the balls-and-bins problem has been analyzed in the context of a -choice process, where each ball goes to a random bin with probability and to the lesser loaded of the two bins corresponding to the nodes of a random edge of the graph with probability . In particular, for this process they show that the difference between the maximum number of balls in a bin and the typical number of balls in the bins is , where is the edge expansion property of the underlying graph. The classical balls-and-bins problem with a power-of- scheme (often referred to as ‘multiple-choice’ algorithm), without any graph topology, has also been studied extensively [3, 5]. Just like in the queueing scenario mentioned above, the power-of- scheme provides a major improvement over purely random assignment () where the maximum number of balls in a bin scales as [12]. Several further variations and extensions have been considered subsequently [30, 1, 4, 6, 7, 10, 21, 22], and we refer to [33] for a recent survey.

As alluded to above, there are natural parallels between the balls-and-bins setup and the queueing scenario as considered in the present paper. These commonalities are for example reflected in the fact that the power-of- scheme yields a similar dramatic performance improvement over purely random assignment in both settings. However, there are also quite fundamental differences between the balls-and-bins setup and the queueing scenario, even in a clique topology, besides the obvious contrasts in the performance metrics. The distinction is for example evidenced by the fact that a simple round-robin strategy produces a perfectly balanced allocation in a balls-and-bins setup but is far from optimal in a queueing scenario. In particular, the stationary fraction of servers with two or more tasks under a round-robin strategy remains positive in the limit as , whereas it vanishes under the JSQ policy. On a related account, since tasks get served and eventually depart in a queueing scenario, less balanced allocations with a large portion of vacant servers will generate fewer service completions and result in a larger total number of tasks. Thus different schemes yield not only various degrees of balance, but also variations in the aggregate number of tasks in the system. These differences arise not only in case of a clique, but also in arbitrary graph topologies, and hence our problem requires a fundamentally different approach than developed in [13] for the balls-and-bins setup. Moreover, [13] considers only the scaling of the maximum queue length, whereas we analyze a more detailed time-varying evolution of the entire system along with its stationary behavior.

Approach and key contributions.

As mentioned above, the queue length process in a clique will be better balanced and smaller (in a majorization sense) than in an arbitrary graph . Accordingly, a graph is said to be -optimal or -optimal when the queue length process on is equivalent to that on a clique on an -scale or -scale, respectively. Roughly speaking, a graph is -optimal if the fraction of nodes with tasks, for , behaves as in a clique as . Since the latter fraction is zero in the limit for all in a clique in stationarity, the fraction of servers with two or more tasks vanishes in any graph that is -optimal, implying that the mean waiting time vanishes as well. Furthermore, recent results for the JSQ policy [9] imply that in a clique of nodes in the heavy-traffic regime the number of nodes with zero tasks and that with two tasks both scale as as . Again loosely speaking, a graph is -optimal if in the heavy-traffic regime the number of nodes with zero tasks and that with two tasks when scaled by both evolve as in a clique as . Formal definitions of asymptotic optimality on an -scale or -scale will be introduced in Section 2.

As one of the main results, we will demonstrate that, remarkably, asymptotic optimality can be achieved in much sparser Erdős-Rényi random graphs (ERRGs). We prove that a sequence of ERRGs indexed by the number of vertices with as , is -optimal. We further establish that the latter growth condition for the average degree is in fact necessary in the sense that any graph sequence that contains bounded-degree vertices cannot be -optimal. This implies that a sequence of ERRGs with finite average degree cannot be -optimal. The growth rate condition is more stringent for optimality on -scale in the heavy-traffic regime. Specifically, we prove that a sequence of ERRGs indexed by the number of vertices with as , is -optimal.

The above results demonstrate that the asymptotic optimality of cliques on an -scale and -scale can be achieved in graphs that are far from fully connected, where the number of connections is reduced by nearly a factor and , respectively, provided the topologies are suitably random in the ERRG sense. This translates into equally significant reductions in communication overhead and storage capacity, since both are roughly proportional to the number of connections.

While considerably sparser graphs can achieve asymptotic optimality in the presence of randomness, the worst-case graph instance may even in very dense regimes (high average degree) not be optimal. In particular, we prove that any graph sequence with minimum degree is -optimal, but that for any one can construct graphs with minimum degree which are not -optimal for some . Loosely speaking, this happens due to an imbalance of arrival flows between two large parts of the network, as will be explained in Section 3 in greater detail.

The key challenge in the analysis of load balancing on arbitrary graph topologies is that one needs to keep track of the evolution of the number of tasks at each vertex along with their corresponding neighborhood relationship. This creates a major problem in constructing a tractable Markovian state descriptor, and renders a classical mean-field analysis of such processes elusive. Consequently, even asymptotic results for load balancing processes on an arbitrary graph have remained scarce so far. To the best of our knowledge, the present paper is the first to establish the process-level as well as steady-state limits of the occupancy states have been rigorously established for a wide class of non-trivial (possibly random) topologies. Since the mean-field techniques do not apply in the current scenario, we take a radically different approach and aim to compare the load balancing process on an arbitrary graph with that on a clique. Specifically, rather than analyze the behavior for a given class of graphs or degree value, we explore for what types of topologies and degree properties the performance is asymptotically similar to that in a clique.

Our proof methodology builds on some recent advances in the analysis of the power-of- algorithm where grows with [20, 19]. Specifically, we view the load balancing process on an arbitrary graph as a ‘sloppy’ version of that on a clique, and thus construct several other intermediate sloppy versions. By constructing novel couplings, we develop a method of comparing the load balancing process on an arbitrary graph and that on a clique. In particular, we bound the difference between the fraction of vertices with or more tasks in the two systems for , to obtain asymptotic optimality results. From a high level, conceptually related graph conditions for asymptotic optimality were examined using quite different techniques by Tsitsiklis and Xu [27, 26] in a dynamic scheduling framework (as opposed to load balancing context).

Organization of the paper.

The remainder of the paper is organized as follows. In Section 2 we present a detailed model description and introduce some useful notation and preliminaries. Sufficient and necessary criteria for asymptotic optimality of deterministic graph sequences are developed in Sections 3 and 4, respectively. In Section 5 we analyze asymptotic optimality of a sequence of random graph topologies. In Section 6 we present simulation experiments to support the analytical results, and examine the performance of topologies that are not analytically tractable. We make a few brief concluding remarks and offer some suggestions for further research in Section 7. Proofs of statements marked () have been provided in the appendix. We adopt the usual notations O(), o(), , and to describe asymptotic comparisons. For a sequence of probability measures , the sequence of events is said to hold with high probability if as . Also, for some positive function , we write a sequence of random variables is or if is a tight sequence of random variables or converges to zero as , respectively. The symbols ‘’ and ‘’ will denote convergences in distribution and in probability, respectively.

2 Model description and preliminaries

Let be a sequence of simple graphs indexed by the number of vertices . For the -th system with servers, we assume that the servers are inter-connected by the underlying graph topology , where server is identified with vertex in , . Tasks with unit-mean exponential processing times arrive at the various servers as independent Poisson processes of rate . Each server has its own queue with a fixed buffer capacity (possibly infinite). When a task appears at a server , it is immediately assigned to the server with the shortest queue among server and its neighborhood in . If there are multiple such servers, one of them is chosen uniformly at random. If , and server and all its neighbors have tasks (including the ones in service), then the newly arrived task is discarded. The service order at each of the queues is assumed to be oblivious to the actual service times, e.g. First-Come-First-Served (FCFS).

For , denote by the queue length at the -th server at time (including the one possibly in service), and by the queue length at the -th ordered server at time when the servers are arranged in nondecreasing order of their queue lengths (ties can be broken in some way that will be evident from the context). Let denote the number of servers with queue length at least at time , , and denote the corresponding fractions. It is important to note that is itself not a Markov process, but the joint process is Markov.

Proposition 1.

For any , the joint system occupancy process has a unique steady state . Also, the sequence of marginal random variables is tight with respect to the -topology.

Proof of Proposition 1.

Note that if , the process is clearly ergodic for all . When , to prove the ergodicity of the process, first fix any and observe that the ergodicity of the queue length processes at the various vertices amounts to proving the ergodicity of the total number of tasks in the system. Using the S-coupling and Proposition LABEL:prop:det_ord in Appendix LABEL:app:stoch we obtain for all ,

| (1) |

provided the inequality holds at time , where is the collection of isolated vertices. Thus in particular, the total number of tasks in the system with is upper bounded by that with . Now the queue length process on is clearly ergodic since it is the collection of independent subcritical M/M/1 queues. Next, for the -tightness of , we will use the following tightness criterion: Define

| (2) |

as the set of all possible fluid-scaled occupancy states equipped with -topology.

Lemma 2 ([20, Lemma 4.7]).

Let be a sequence of random variables in . Then the following are equivalent:

-

(i)

is tight with respect to product topology, and for all

(3) -

(ii)

is tight with respect to topology.

Note that since takes value in , which is compact with respect to the product topology, Prohorov’s theorem implies that is tight with respect to the product topology. To verify the condition in (3), note that for each , Equation (1) yields

Since , taking the limit , the right side of the above inequality tends to zero, and hence, the condition in (3) is satisfied. ∎

Asymptotic behavior of occupancy processes in cliques. We now describe the behavior of the occupancy processes on a clique as the number of servers grows large. Rigorous descriptions of the limiting processes are provided in Appendix LABEL:app:jsq.

The behavior on -scale is observed in terms of the fractions of servers with queue length at least at time . When , on any finite time interval,

| (4) |

as , where is some deterministic process. Furthermore, in steady state

| (5) |

as . Note that is the fraction of non-empty servers. Thus is the steady-state scaled departure rate which should be equal to the scaled arrival rate . Surprisingly, however, we observe that the steady-state fraction of servers with a queue length of two or larger is asymptotically negligible.

To analyze the behavior on -scale, we consider a heavy-traffic scenario (a.k.a. Halfin-Whitt regime) where the arrival rate at each server is given by with

| (6) |

In order to describe the behavior in the limit, let

be a properly centered and scaled version of the occupancy process , with

| (7) |

. The reason why is centered around while , , are not, is because for , the fraction of servers with a queue length of exactly one tends to one, whereas the fraction of servers with a queue length of two or larger tends to zero as , as mentioned above. Recent results for [9] show that from a suitable starting state,

| (8) |

as , where is some diffusion process. A precise description of the limiting diffusion process is provided in Theorem LABEL:diffusionjsqd in Appendix LABEL:app:jsq. This implies that over any finite time interval, there will be servers with queue length zero and servers with a queue length of two or larger, and hence all but servers have a queue length of exactly one.

Asymptotic optimality. As stated in the introduction, a clique is an optimal load balancing topology, as the occupancy process is better balanced and smaller (in a majorization sense) than in any other graph topology. In general the optimality is strict, but it turns out that near-optimality can be achieved asymptotically in a broad class of other graph topologies. Therefore, we now introduce two notions of asymptotic optimality, which will be useful to characterize the performance in large-scale systems.

Definition 1 (Asymptotic optimality).

A graph sequence is called ‘asymptotically optimal on -scale’ or ‘-optimal’, if for any , on any finite time interval, the scaled occupancy process converges weakly to the process given by (4).

Intuitively speaking, if a graph sequence is -optimal or -optimal, then in some sense, the associated occupancy processes are indistinguishable from those of the sequence of cliques on -scale or -scale. In other words, on any finite time interval their occupancy processes can differ from those in cliques by at most or , respectively. For brevity, -scale and -scale are often referred to as fluid scale and diffusion scale, respectively. In particular, due to the -tightness of the scaled occupancy processes as stated in Proposition 1, we obtain that for any -optimal graph sequence ,

| (9) |

as , implying that the stationary fraction of servers with queue length two or larger and the mean waiting time vanish.

3 Sufficient criteria for asymptotic optimality

In this section we develop a criterion for asymptotic optimality of an arbitrary deterministic graph sequence on different scales. In Section 5 this criterion will be leveraged to establish optimality of a sequence of random graphs.

We start by introducing some useful notation, and two measures of well-connectedness. Let be any graph. For a subset , define to be the set of all vertices that are disjoint from , where . For any fixed define

| (10) |

The next theorem provides sufficient conditions for asymptotic optimality on -scale and -scale in terms of the above two well-connectedness measures.

Theorem 3.

For any graph sequence ,

-

(i)

is -optimal if for any , , as

-

(ii)

is -optimal if for any , , as

The next corollary is an immediate consequence of Theorem 3.

Corollary 4.

Let be any graph sequence and be the minimum degree of . Then (i) If , then is -optimal, and (ii) If , then is -optimal.

The rest of the section is devoted to a discussion of the main proof arguments for Theorem 3, focusing on the proof of -optimality. The proof of -optimality follows along similar lines. We establish in Proposition 5 that if a system is able to assign each task to a server in the set of the nodes with shortest queues (ties broken arbitrarily), where is , then it is -optimal. Since the underlying graph is not a clique however (otherwise there is nothing to prove), for any not every arriving task can be assigned to a server in . Hence we further prove in Proposition 6 a stochastic comparison property implying that if on any finite time interval of length , the number of tasks that are not assigned to a server in is , then the system is -optimal as well. The -optimality can then be concluded when is , which we establish in Proposition 7 under the condition that as as stated in Theorem 3.

To further explain the idea described in the above proof outline, it is useful to adopt a slightly different point of view towards load balancing processes on graphs. From a high level, a load balancing process can be thought of as follows: there are servers, which are assigned incoming tasks by some scheme. The assignment scheme can arise from some topological structure as considered in this paper, in which case we will call it topological load balancing, or it can arise from some other property of the occupancy process, in which case we will call it non-topological load balancing. As mentioned earlier, under Markovian assumptions, the JSQ policy or the clique is optimal among the set of all non-anticipating schemes, irrespective of being topological or non-topological. Also, load balancing on graph topologies other than a clique can be thought of as a ‘sloppy’ version of that on a clique, when each server only has access to partial information on the occupancy state. Below we first introduce a different type of sloppiness in the task assignment scheme, and show that under a limited amount of sloppiness optimality is retained on a suitable scale. Next we will construct a scheme which is a hybrid of topological and non-topological schemes, whose behavior is simultaneously close to both the load balancing process on a suitable graph and that on a clique.

A class of sloppy load balancing schemes. Fix some function , and recall the set as before. Consider the class where each arriving task is assigned to one of the servers in . It should be emphasized that for any scheme in , we are not imposing any restrictions on how the ties are broken to select the specific set , or how the incoming task should be assigned to a server in . The scheme only needs to ensure that the arriving task is assigned to some server in with respect to some tie breaking mechanism. The next proposition provides a sufficient criterion for asymptotic optimality of any scheme in .

Proposition 5 ().

For , let be any scheme. (i) If as then is -optimal, and (ii) If as then is -optimal.

A bridge between topological and non-topological load balancing. For any graph and , we first construct a scheme called , which is an intermediate blend between the topological load balancing process on and some kind of non-topological load balancing on servers. The choice of will be clear from the context.

To describe the scheme , first synchronize the arrival epochs at server in both systems, . Further, the servers in both systems are arranged in non-decreasing order of the queue lengths, and the departure epochs at the -th ordered server in the two systems are synchronized, . When a task arrives at server at time say, it is assigned in the graph to a server according to its own statistical law. For the assignment under the scheme , first observe that if

| (11) |

then there exists some tie-breaking mechanism for which belongs to under . Pick such an ordering of the servers, and assume that is the -th ordered server in that ordering, for some . Under assign the arriving task to the -th ordered server (breaking ties arbitrarily in this case). Otherwise, if (11) does not hold, then the task is assigned to one of the servers with minimum queue lengths under uniformly at random.

Denote by the cumulative number of arriving tasks up to time for which Equation (11) is violated under the above coupling. The next proposition shows that the load balancing process under the scheme is close to that on the graph in terms of the random variable .

Proposition 6 ().

The following inequality is preserved almost surely

| (12) |

provided the two systems start from the same occupancy state at .

In order to conclude optimality on -scale or -scale, it remains to be shown that for any , is sufficiently small. The next proposition provides suitable asymptotic bounds for under the conditions on and stated in Theorem 3.

Proposition 7.

For any the following holds.

-

(i)

There exist and with as , such that if as , then

-

(ii)

There exist and with as , such that if as , then

The proof of Theorem 3 then readily follows by combining Propositions 5-7 and observing that the scheme belongs to the class by construction.

Proof of Proposition 7.

Fix any and choose . With the coupling described above, when a task arrives at some vertex say, Equation (11) is violated only if none of the vertices in is a neighbor of . Thus, the total instantaneous rate at which this happens is

irrespective of what this set actually is. Therefore, for any fixed ,

where represents a unit-rate Poisson process. This can then be leveraged to show that is small on an -scale and -scale, respectively, under the conditions stated in the proposition, by choosing a suitable .

Specifically, if , then there exists with such that for all , and hence . It then follows that with high probability,

Likewise, if , then there exists with such that for all , and hence . It then follows that with high probability,

∎

Proof of Theorem 3.

(i) In order to prove the fluid-level optimality of , fix any . Observe from Proposition 6 and Proposition 7 (i) that there exists such that with high probability

Furthermore, since and , Proposition 5 yields

Thus since is arbitrary, we obtain that with high probability as ,

for all , which completes the proof of Part (i).

(ii) To prove the diffusion-level optimality of , again fix any . As in Part (i), using Proposition 6 and Proposition 7 (ii), there exists

Furthermore, since and , Proposition 5 yields

as , where the process given by (8). Since is arbitrary, we thus obtain

as , which completes the proof of Part (ii). ∎

4 Necessary criteria for asymptotic optimality

From the conditions of Theorem 3 it follows that if for all , and are and , respectively, then the total number of edges in must be and , respectively. Theorem 8 below states that the super-linear growth rate of the total number of edges is not only sufficient, but also necessary in the sense that any graph with edges is asymptotically sub-optimal on -scale.

Theorem 8.

Let be any graph sequence, such that there exists a fixed integer with

| (13) |

where is the degree of the vertex . Then is sub-optimal on -scale.

Proof of Theorem 8.

For brevity, denote by the set of all vertices with degree at most . Since from (13) we have a convergent subsequence with , such that , as . For the rest of the proof we will consider the asymptotic statements along this subsequence, and hence omit the subscript .

Let the system start from an occupancy state where all the vertices in are empty. We will show that in finite time, a positive fraction of vertices in will have at least two tasks. This will prove the fluid limit sample path cannot agree with that of the sequence of cliques, and hence cannot be -optimal. The idea of the proof is as follows: If a graph contains bounded degree vertices, then starting from all empty servers, in any finite time interval there will be servers say, for which all the servers in have at least one task. For all such servers an arrival at must produce a server of queue length two. Thus, it shows that the instantaneous rate at which servers of queue length two are formed is bounded away from zero, and hence servers of queue length two are produced in finite time.

Let be a vertex with degree or less in . Consider the event that at time all vertices in have at least one job. Note that since is fixed, for any , for some , for all . To see this, note that is the probability that before time there are arrivals at vertex and no departure has taken place. Also observe that for two vertices with degrees at most ,

| (14) |

Indeed the probability of the event can be lower bounded by the probability of the event that before time there are arrivals at vertex , arrivals at vertex , and no departure has taken place from . Thus, at time , the fraction of vertices in for which all the neighboring vertices have at least one task, is lower bounded by . Now the proof is completed by considering the following: let be a vertex of degree for which all the neighbors have at least one task. Then at such an instance if a task arrives at server , it must be assigned to a server with queue length one, and hence a server with queue length two will be formed. Therefore the total scaled instantaneous rate at which the number of queue length two is being formed at time is at least , which also gives the total rate of increase of the fraction of vertices with at least two tasks. ∎

Worst-case scenario. Next we consider the worst-case scenario. Theorem 9 below asserts that a graph sequence can be sub-optimal for some even when the minimum degree is .

Theorem 9.

For any , such that with , there exists , and a graph sequence with , such that is sub-optimal on -scale.

To construct such a sub-optimal graph sequence, consider a sequence of complete bipartite graphs , with and as . If this sequence were -optimal, then starting from all empty servers, asymptotically the fraction of servers with queue length one would converge to , and the fraction of servers with queue length two or larger should remain zero throughout. Now note that for large the rate at which tasks join the empty servers in is given by , whereas the rate of empty server generation in is at most . Choosing , one can see that in finite time each server in will have at least one task. From that time onward with at least instantaneous rate , servers with queue length two start forming. The range for stated in Theorem 9 is only to ensure that there exists with .

Proof sketch of Theorem 9.

Fix a . Construct the graph sequence as a sequence of complete bipartite graphs with size of one partite set of the -th graph to be , i.e., , such that and , and the edge set is given by . Note that , as . We will show that for any , there exists , such that is sub-optimal on -scale.

Assume on the contrary that is -optimal. Denote by and the number of vertices with at least tasks in partite sets and , respectively. Also define and . Assume , for all . Observe that as long as by a non-vanishing margin, any external arrival to servers in will be assigned to an empty server in with probability . Similarly, as long as by a non-vanishing margin, any external arrival to servers in will be assigned to an empty server in with probability . Thus one can show that as , until hits , the processes and converges weakly to a deterministic process described by the following set of ODE’s:

| (15) |

Since the total scaled arrival rate into the system of servers is , should the above system follow the fluid-limit trajectory of the occupancy process for a clique, starting from an all-empty state, must approach as , and and both remain 0 for all , . When , (15) implies that in finite time hits . Consequently, should approach as . Now we claim that when , if a task appears at a server in that has queue length one, then with probability , it will be assigned to a server in . To see this, note that at such an arrival if there is an empty server in , then the arriving task is clearly assigned to the idle server, otherwise, when there is no empty server in , the arriving task is assigned uniformly at random among the vertices in having queue length one. Since there are vertices in with queue length one, the arriving task with probability joins a server in . Therefore, the total scaled rate of tasks arriving at the servers in is at least , whereas the total scaled rate at which tasks can leave from servers in is at most . Thus if , then in finite time, a positive fraction of servers in will have queue length two or larger. Now observe that

and for any . This completes the proof of Theorem 9. ∎

5 Asymptotically optimal random graph topologies

In this section we use Theorem 3 to investigate how the load balancing process behaves on random graph topologies. Specifically, we aim to understand what types of graphs are asymptotically optimal in the presence of randomness (i.e., in the average case scenario). Theorem 10 below establishes sufficient conditions for asymptotic optimality of a sequence of inhomogeneous random graphs. Recall that a graph is called a supergraph of if and .

Theorem 10.

Let be a graph sequence such that for each , is a supergraph of the inhomogeneous random graph where any two vertices share an edge with probability .

-

(i)

If is , then is -optimal.

-

(ii)

If is , then is -optimal.

The proof of Theorem 10 relies on Theorem 3. Specifically, if satisfies conditions (i) and (ii) in Theorem 10, then the corresponding conditions (i) and (ii) in Theorem 3 hold.

Proof of Theorem 10.

In this proof we will verify the conditions stated in Theorem 3 for fluid and diffusion level optimality. Fix any .

(i) Observe that for as described in Theorem 10 (i), we have with as . For any two subsets , , denote by the number of cross-edges between and . Now, for any function ,

| (16) |

where the first equality is due to the fact that if there are two sets of vertices and with and , such that there is no edge between and , then the graph must contain two sets and of sizes exactly equal to and , respectively, such that there is no edge between and , and vice-versa. Choosing say, it can be seen that for any such that as , and the above probability goes to 0. Therefore for any , (16) yields

as .

As an immediate corollary to Theorem 10 we obtain an optimality result for the sequence of Erdős-Rényi random graphs.

Corollary 11.

Let be a graph sequence such that for each , is a supergraph of , and . Then (i) If as , then is -optimal. (ii) If as , then is -optimal.

Theorem 3 can be further leveraged to establish the optimality of the following sequence of random graphs. For any and such that is even, construct the erased random regular graph on vertices as follows: Initially, attach half-edges to each vertex. Call all such half-edges unpaired. At each step, pick one half-edge arbitrarily, and pair it to another half-edge uniformly at random among all unpaired half-edges to form an edge, until all the half-edges have been paired. This results in a uniform random regular multi-graph with degree [29, Proposition 7.7]. Now the erased random regular graph is formed by erasing all the self-loops and multiple edges, which then produces a simple graph.

Theorem 12.

Let be a sequence of erased random regular graphs with degree . Then (i) If as , then is -optimal. (ii) If as , then is -optimal.

Proof of Theorem 12.

We will again verify the conditions stated in Theorem 3 for fluid and diffusion level optimality. For , denote Fix any .

(i) For any function ,

| (18) |

Choosing say, it can be seen that for any such that as , and the above probability goes to 0. Therefore for any , (18) yields

(ii) Again, as in Part (i), for any function ,

| (19) |

Now, choosing , it can be seen that as and the above probability converges to 0. Therefore for any , (19) yields

as . ∎

Note that due to Theorem 8, we can conclude that the growth rate condition on degrees for -optimality in Corollary 11 (i) and Theorem 12 (i) is not only sufficient, but necessary as well. Thus informally speaking, -optimality is achieved under the minimum condition required as long as the underlying topology is suitably random.

6 Simulation experiments

In this section we present extensive simulation results to illustrate the fluid and diffusion-limit results, and compare the performance of various graph topologies in terms of mean waiting times.

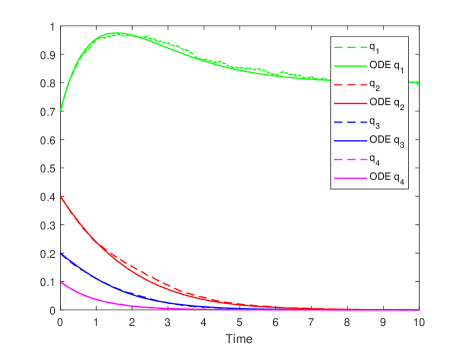

Convergence of sample paths to fluid and diffusion-limit trajectories. The fluid-limit trajectory for is illustrated in Figure 1 along with a simulation for servers. The solid curves represent the case of a clique (i.e. corresponding to the limit of the occupancy states for the ordinary JSQ policy) as described in Theorem LABEL:fluidjsqd in the appendix. The dotted lines correspond to the empirical occupancy process when the underlying graph topology is a single instance of the Erdős-Rényi random graph (ERRG) on vertices with edge probability , so the average degree is 100. Even for a topology much sparser than a clique and finite -value, the simulated path matches closely with the limiting ODE. In particular, the above suggests that for a large but finite degree, the behavior may be hard to distinguish from the optimal one for all practical purposes, and there seems to be no prominent effect of graph topologies provided the underlying topology is suitably random.

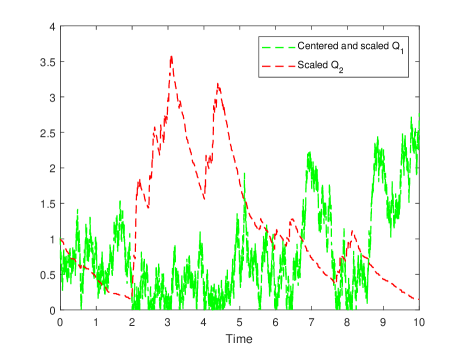

The diffusion-scaled trajectory has been simulated for servers in Figure 2. The system load is quite close to 1. The underlying graph topology is taken to be a single instance of the ERRG on vertices with edge probability . The green and red curves in Figure 2 correspond to the centered and scaled occupancy state processes and , respectively. As stated in Corollary 11, the centered and diffusion-scaled trajectories can be observed to be recurrent, and the rate of decrease seems to be proportional to its value — resembling some properties of the reflected Ornstein-Uhlenbeck process as in the case of a clique (i.e. the limit of the ordinary JSQ policy) as stated in Theorem LABEL:diffusionjsqd in the appendix.

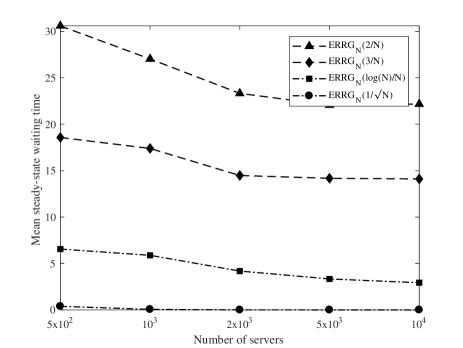

Convergence of steady-state waiting times. Figure 3 exhibits convergence of mean steady-state waiting times to their limiting values as . By virtue of Little’s law, note that the asymptotic mean steady-state waiting time can be expressed in terms of the fixed point of the fluid limit as . For each and average degree with , 3, , and , an instance of ERRG on vertices with average degree is taken and the time-averaged value of is plotted. The average is taken over the time interval 0 to 200 or 250 depending on the value of . The figure shows that if the average degree grows with , then the mean steady-state waiting time converges to zero, while it stays bounded away from zero in case the average degree is constant. It can further be observed that the convergence is notably fast for a higher growth rate of the average degree.

Effect of the topology in sparse case. When the average degree is fixed, the effect of the topology seems to be quite prominent. This has also been observed in prior work [28, 11]. Specifically, when comparing graphs with average degree 2, it can be seen in the top chart in Figure 4 that the ring topology has a lower mean steady-state waiting time than random topologies (ERRG or RGG). In case of average degree 4, the (toric) grid topology performs worse for small -values, but the performance improves as increases. There are two crucial effects at play here: (i) The regularity in degrees of the vertices: Given a mean degree, higher variability (e.g. presence of many isolated vertices) is expected to degrade the performance and (ii) The locality of the connections: Higher diversity in the connections (i.e., graphs with good expander properties) is expected to improve the performance. The RGG has a disadvantage in both these aspects: it contains many isolated vertices and also, its connections are highly localized, and thus its performance is consistently worse in both top and bottom charts in Figure 4. The ERRG and the lattice graphs (ring/grid) are good with respect to the degree variability and the connection locality, respectively. However, the presence of many isolated vertices hurts more than the benefit provided by the non-local connections when the average degree is small, as exhibited in Figure 4. In case of higher average degree, the number of isolated vertices in the ERRG is relatively small, and thus the benefit from the non-local connections becomes somewhat prominent for smaller -values. It is therefore worthwhile to note that in case of increasing average degrees, the effect of topology becomes less significant, and so the behavior of random topologies (ERRG, RGG, or random regular graphs) turns out to be as good as the clique.

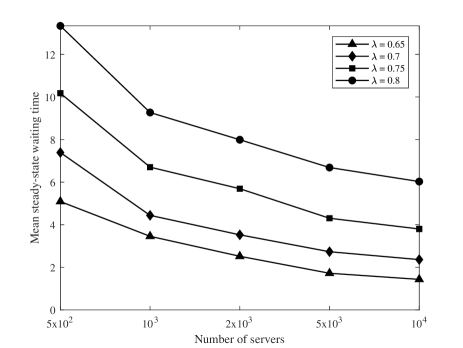

Effect of load on the growth rate of the average degree. It is expected that if the system is heavily loaded (i.e., close to 1), then the rate of convergence of the steady-state measure, and hence that of the mean steady-state waiting time becomes slower. This can be observed in Figure 5. For moderately loaded systems viz. or , the convergence is fast even for topologies that are far from fully connected with average degree as low as .

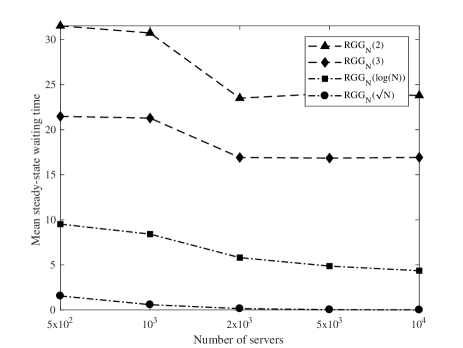

Performance for spatial random network models. The conditions stated in Theorem 3 demand that any two large portions of the graph share many cross edges. This property is often violated in spatial graph models, where vertices that are closer to each other have a higher tendency to share an edge. A canonical model for spatial networks is the random geometric graph (RGG), where vertices correspond to uniform random locations on with periodic boundary, and any two vertices share an edge if they are less than a distance apart. Note that the average degree in that case is given by . In other words, for fixed values of and , the distance scales as . To analyze the load balancing process on spatial random graph models, we simulated the processes where the underlying topologies are instances of RGGs on vertices and average degrees 2, 3, , and , and plotted the corresponding mean steady-state waiting times for increasing values of in Figure 6.

The surprising resemblance with the ERRG scenario as depicted in Figure 3 hints that the asymptotic optimality result can be preserved even under possibly a relaxed set of conditions. This motivates future study of the asymptotic optimality beyond the classes of graphs we considered.

7 Conclusion

We have considered load balancing processes in large-scale systems where the servers are inter-connected by some graph topology. For arbitrary topologies we established sufficient criteria for which the performance is asymptotically similar to that in a clique, and hence optimal on suitable scales. Leveraging these criteria we showed that unlike fixed-degree scenarios (viz. ring, grid) where the topology has a prominent performance impact, the sensitivity to the topology diminishes in the limit when the average degree grows with the number of servers. In particular, a wide class of suitably random topologies are provably asymptotically optimal. In other words, the asymptotic optimality of a clique can be achieved while dramatically reducing the number of connections. In the context of large-scale data centers, this translates into significant reductions in communication overhead and storage capacity, since both are roughly proportional to the number of connections.

Although a growing average degree is necessary in the sense that any graph with finite average degree is sub-optimal, it is in no way sufficient. Load balancing performance can be provably sub-optimal even when the minimum degree is with . What happens for is an open question. Our proof technique relies heavily on a connectivity property entailing that any two sufficiently large portions of vertices share a lot of edges. This property does not hold however in many networks with connectivity governed by spatial attributes, such as geometric graphs, although the simulation experiments hint that the family of topologies that are asymptotically optimal is likely to be broader than the ERRG and random regular class as considered in the present paper. In future research we aim to examine asymptotic optimality properties of such spatial network models.

Acknowledgment

The authors thank Nikhil Bansal for helpful discussions in the early stage of this work, and also for pointing out several relevant references. The work was financially supported by The Netherlands Organization for Scientific Research (NWO) through Gravitation Networks grant 024.002.003 and TOP-GO grant 613.001.012.

References

- [1] M. Adler, S. Chakrabarti, M. Mitzenmacher, and L. Rasmussen. Parallel randomized load balancing. In Proc. STOC ’95, pages 238–247, 1995.

- [2] S. Albers, M. Charikar, and M. Mitzenmacher. Delayed information and action in on-line algorithms. Inform. Comput., 170(2):135–152, 2001.

- [3] Y. Azar, A. Z. Broder, A. R. Karlin, and E. Upfal. Balanced allocations. In Proc. STOC ’94, pages 593–602, 1994.

- [4] P. Berenbrink, A. Czumaj, A. Steger, and B. Vöcking. Balanced allocaton: The heavily loaded case. In Proc. STOC ’00, pages 745–754, 2000.

- [5] P. Berenbrink, A. Czumaj, A. Steger, and B. Vöcking. Balanced allocations: The heavily loaded case. SIAM J. Comput., 35(6):1350–1385, 2006.

- [6] A. Czumaj, F. Meyer auf der Heide, and V. Stemann. Shared memory simulations with triple-logarithmic delay. In Lecture Notes in Computer Science, pages 46–59. Springer, Berlin, Heidelberg, 1995.

- [7] M. Dietzfelbinger and F. Meyer auf der Heide. Simple, efficient shared memory simulations. In Proc. SPAA ’93, pages 110–119, 1993.

- [8] A. Ephremides, P. Varaiya, and J. Walrand. A simple dynamic routing problem. IEEE Trans. Autom. Control, 25(4):690–693, 1980.

- [9] P. Eschenfeldt and D. Gamarnik. Join the shortest queue with many servers. The heavy traffic-asymptotics. Math. Oper. Res., 43(3):867–886, 2018.

- [10] D. Fotakis, R. Pagh, P. Sanders, and P. Spirakis. Space efficient hash tables with worst case constant access time. Theory Comput. Syst., 38(2):229–248, 2005.

- [11] N. Gast. The power of two choices on graphs: the pair-approximation is accurate. In Proc. MAMA workshop 2015, pages 69–71, 2015.

- [12] G. H. Gonnet. Expected length of the longest probe sequence in hash code searching. J. ACM, 28(2):289–304, 1981.

- [13] K. Kenthapadi and R. Panigrahy. Balanced allocation on graphs. In Proc. SODA ’06, pages 434–443, 2006.

- [14] C. Kenyon and M. Mitzenmacher. Linear waste of best fit bin packing on skewed distributions. In Proc. FOCS ’00, pages 582–589, 2000.

- [15] M. Mitzenmacher. Load balancing and density dependent jump Markov processes. In Proc. FOCS ’96, pages 213–222, 1996.

- [16] M. Mitzenmacher. The power of two choices in randomized load balancing. PhD thesis, University of California, Berkeley, 1996.

- [17] M. Mitzenmacher. The power of two choices in randomized load balancing. IEEE Trans. Parallel Distrib. Syst., 12(10):1094–1104, 2001.

- [18] M. Mitzenmacher, B. Prabhakar, and D. Shah. Load balancing with memory. In Proc. FOCS ’02, pages 799–808, 2002.

- [19] D. Mukherjee, S. C. Borst, J. S. H. Van Leeuwaarden, and P. A. Whiting. Asymptotic optimality of power-of-d load balancing in large-scale systems. arXiv:1612.00722, 2016.

- [20] D. Mukherjee, S. C. Borst, J. S. H. van Leeuwaarden, and P. A. Whiting. Universality of Power-of-d Load Balancing in Many-Server Systems. Stoch. Syst., 8(4):265–292, 2018.

- [21] R. Pagh and F. F. Rodler. Cuckoo hashing. J. Algorithms, 51(2):122–144, 2004.

- [22] R. Panigrahy. Efficient hashing with lookups in two memory accesses. In Proc. SODA ’05, pages 830–839, 2005.

- [23] Y. Peres, K. Talwar, and U. Wieder. Graphical balanced allocations and the (1 + )-choice process. Random Struct. Algor., 47(4):760–775, 2015.

- [24] P. D. Sparaggis, D. Towsley, and C. G. Cassandras. Sample path criteria for weak majorization. Adv. Appl. Probab., 26(1):155–171, 1994.

- [25] D. Towsley. Application of majorization to control problems in queueing systems. In P. Chrétienne, E. G. Coffman, J. K. Lenstra, and Z. Liu, editors, Scheduling Theory and its Applications, chapter 14. John Wiley & Sons, Chichester, 1995.

- [26] J. N. Tsitsiklis and K. Xu. Queueing system topologies with limited flexibility. In Proc. SIGMETRICS ’13, pages 167–178, 2013.

- [27] J. N. Tsitsiklis and K. Xu. Flexible queueing architectures. Oper. Res., 65(5):1398–1413, 2017.

- [28] S. R. Turner. The effect of increasing routing choice on resource pooling. Probab. Eng. Inf. Sci., 12(01):109–124, 1998.

- [29] R. Van der Hofstad. Random Graphs and Complex Networks, volume 1. Cambridge University Press, Cambridge, 2017.

- [30] B. Vöcking. How asymmetry helps load balancing. In Proc. FOCS ’99, pages 131–140, 1999.

- [31] N. D. Vvedenskaya, R. L. Dobrushin, and F. I. Karpelevich. Queueing system with selection of the shortest of two queues: An asymptotic approach. Problemy Peredachi Informatsii, 32(1):20–34, 1996.

- [32] W. Wang, K. Zhu, L. Ying, J. Tan, and L. Zhang. MapTask Scheduling in MapReduce with Data Locality: Throughput and Heavy-Traffic Optimality. IEEE/ACM Trans. Netw., 24(1):190–203, 2016.

- [33] U. Wieder. Hashing, load balancing and multiple choice. Found. Trends Theoretical Computer Science, 12(3–4):275–379, 2017.

- [34] W. Winston. Optimality of the shortest line discipline. J. Appl. Probab., 14(1):181–189, 1977.

- [35] Q. Xie, A. Yekkehkhany, and Y. Lu. Scheduling with multi-level data locality: Throughput and heavy-traffic optimality. In Proc. INFOCOM ’16, pages 1–9, 2016.