Dynamic Semiparametric Models for Expected Shortfall (and

Value-at-Risk)††thanks: For helpful comments we thank Tim Bollerslev, Rob

Engle, Jia Li, Nour Meddahi, and seminar participants at the Bank of Japan,

Duke University, EPFL, Federal Reserve Bank of New York, Hitotsubashi

University, New York University, Toulouse School of Economics, the University

of Southern California, and the 2015 Oberwolfach Workshop on Quantitative Risk

Management where this project started. The first author would particularly

like to thank the finance department at NYU Stern, where much of his work on

this paper was completed. Contact address: Andrew Patton, Department of

Economics, Duke University, 213 Social Sciences Building, Box 90097, Durham NC

27708-0097. Email: andrew.patton@duke.edu.

Andrew J. Patton

Duke University

Johanna F. Ziegel

University of Bern

Rui Chen

Duke University

(First version: 5 December 2015. This version: 11 July 2017.)

Abstract

Expected Shortfall (ES) is the average return on a risky asset conditional on

the return being below some quantile of its distribution, namely its

Value-at-Risk (VaR). The Basel III Accord, which will be implemented in the

years leading up to 2019, places new attention on ES, but unlike VaR, there is

little existing work on modeling ES. We use recent results from statistical

decision theory to overcome the problem of “elicitability” for ES by jointly modelling ES

and VaR, and propose new dynamic models for these risk measures. We provide

estimation and inference methods for the proposed models, and confirm via

simulation studies that the methods have good finite-sample properties. We

apply these models to daily returns on four international equity indices, and

find the proposed new ES-VaR models outperform forecasts based on GARCH or

rolling window models.

The financial crisis of 2007-08 and its aftermath led to numerous changes in

financial market regulation and banking supervision. One important change

appears in the Third Basel Accord (Basel Committee, 2010), where new emphasis

is placed on “Expected Shortfall” (ES) as

a measure of risk, complementing, and in parts substituting, the more-familiar

Value-at-Risk (VaR) measure. Expected Shortfall is the expected return on an

asset conditional on the return being below a given quantile of its

distribution, namely its VaR. That is, if is the return on some asset

over some horizon (e.g., one day or one week) with conditional (on information

set ) distribution , which we assume to be strictly

increasing with finite mean, the -level VaR and ES are:

(1)

(2)

(3)

As Basel III is implemented worldwide (implementation is expected to

occur in the period leading up to January 1, 2019), ES will

inevitably gain, and require, increasing attention from risk managers and

banking supervisors and regulators. The new “market

discipline” aspects of Basel III mean that ES and VaR will

be regularly disclosed by banks, and so a knowledge of these measures will

also likely be of interest to these banks’ investors and counter-parties.

There is, however, a paucity of empirical models for expected shortfall. The

large literature on volatility models (see Andersen et al. (2006) for

a review) and VaR models (see Komunjer (2013) and McNeil et al. (2015)), have

provided many useful models for these measures of risk. However, while ES has

long been known to be a “coherent” measure

of risk (Artzner, et al. 1999), in contrast with VaR, the literature

contains relatively few models for ES; some exceptions are discussed below.

This dearth is perhaps in part because regulatory interest in this risk

measure is only recent, and perhaps also due to the fact that this measure is

not “elicitable.” A risk measure (or

statistical functional more generally) is said to be “elicitable” if there exists a loss function such that the

measure is the solution to minimizing the expected loss. For example, the mean

is elicitable using the quadratic loss function, and VaR is elicitable using

the piecewise-linear or “tick” loss

function. Having such a loss function is a stepping stone to building dynamic

models for these quantities. We use recent results from Fissler and

Ziegel (2016), who show that ES is jointlyelicitable

with VaR, to build new dynamic models for ES and VaR.

This paper makes three main contributions. Firstly, we present some novel

dynamic models for ES and VaR, drawing on the GAS framework of Creal,

et al. (2013), as well as successful models from the volatility

literature, see Andersen et al. (2006). The models we propose are

semiparametric in that they impose parametric structures for the dynamics of

ES and VaR, but are completely agnostic about the conditional distribution of

returns (aside from regularity conditions required for estimation and

inference). The models proposed in this paper are related to the class of

“CAViaR” models proposed by Engle and

Manganelli (2004a), in that we directly parameterize the measure(s) of risk

that are of interest, and avoid the need to specify a conditional distribution

for returns. The models we consider make estimation and prediction fast and

simple to implement. Our semiparametric approach eliminates the need to

specify and estimate a conditional density, thereby removing the possibility

that such a model is misspecified, though at a cost of a loss of efficiency

compared with a correctly specified density model.

Our second contribution is asymptotic theory for a general class of dynamic

semiparametric models for ES and VaR. This theory is an extension of results

for VaR presented in Weiss (1991) and Engle and Manganelli (2004a), and

draws on identification results in Fissler and Ziegel (2016) and results

for M-estimators in Newey and McFadden (1994). We present conditions under

which the estimated parameters of the VaR and ES models are consistent and

asymptotically normal, and we present a consistent estimator of the asymptotic

covariance matrix. We show via an extensive Monte Carlo study that the

asymptotic results provide reasonable approximations in realistic simulation

designs. In addition to being useful for the new models we propose, the

asymptotic theory we present provides a general framework for other

researchers to develop, estimate, and evaluate new models for VaR and ES.

Our third contribution is an extensive application of our new models and

estimation methods in an out-of-sample analysis of forecasts of ES and VaR

for four international equity indices over the period January 1990 to December

2016. We compare these new models with existing methods from the literature

across a range of tail probability values used in

risk management. We use Diebold and Mariano (1995) tests to identify the

best-performing models for ES and VaR, and we present simple regression-based

methods, related to those of Engle and Manganelli (2004a) and Nolde

and Ziegel (2017), to “backtest” the ES forecasts.

Some work on expected shortfall estimation and prediction has appeared in the

literature, overcoming the problem of elicitability in different ways: Engle

and Manganelli (2004b) discuss using extreme value theory, combined with

GARCH or CAViaR dynamics, to obtain forecasts of ES. Cai and Wang (2008)

propose estimating VaR and ES based on nonparametric conditional

distributions, while Taylor (2008) and Gschöpf et al. (2015)

estimate models for “expectiles” (Newey

and Powell, 1987) and map these to ES. Zhu and Galbraith (2011) propose using

flexible parametric distributions for the standardized residuals from models

for the conditional mean and variance. Drawing on Fissler and Ziegel (2016),

we overcome the problem of elicitability more directly, and open up new

directions for ES modeling and prediction.

In recent independent work, Taylor (2017) proposes using the asymmetric

Laplace distribution to jointly estimate dynamic models for VaR and ES. He

shows the intriguing result that the negative log-likelihood of this

distribution corresponds to one of the loss functions presented in Fissler and

Ziegel (2016), and thus can be used to estimate and evaluate such models.

Unlike our paper, Taylor (2017) provides no asymptotic theory for his proposed

estimation method, nor any simulation studies of its reliability. However,

given the link he presents, the theoretical results we present below can be

used to justify ex post the methods of his paper.

The remainder of the paper is structured as follows. In Section 2

we present new dynamic semiparametric models for ES and VaR and compare them

with the main existing models for ES and VaR. In Section 3 we

present asymptotic distribution theory for a generic dynamic semiparametric

model for ES and VaR, and in Section 4 we study the

finite-sample properties of the asymptotic theory in some realistic Monte

Carlo designs. Section 5 we apply the new models to daily

data on four international equity indices, and compare these models both

in-sample and out-of-sample with existing models. Section 6

concludes. Proofs and additional technical details are presented in the

appendix, and a supplemental web appendix contains detailed proofs and

additional analyses.

2 Dynamic models for ES and VaR

In this section we propose some new dynamic models for expected shortfall (ES)

and Value-at-Risk (VaR). We do so by exploiting recent work in Fissler and

Ziegel (2016) which shows that these variables are elicitable

jointly, despite the fact that ES was known to be not elicitable

separately, see Gneiting (2011a). The models we propose are based on the GAS

framework of Creal, et al. (2013) and Harvey (2013), which we

briefly review in Section 2.2 below.

2.1 A consistent scoring rule for ES and VaR

Fissler and Ziegel (2016) show that the following class of loss functions (or

“scoring rules”), indexed by the functions

and is consistent for VaR and ES. That is, minimizing the

expected loss using any of these loss functions returns the true VaR and ES.

In the functions below, we use the notation and for VaR and ES.

(4)

where is weakly increasing, is strictly increasing and

strictly positive, and We will refer to the

above class as “FZ loss functions.”111Consistency of the FZ loss function for VaR and ES also requires

imposing that which follows naturally from the definitions of ES

and VaR in equations (1) and (2). We discuss how we impose this restriction

empirically in Sections 4 and 5

below. Minimizing any member of this class yields VaR and ES:

(5)

Using the FZ loss function for estimation and forecast evaluation requires

choosing and We choose these so that the loss function

generates loss differences (between competing forecasts) that are homogeneous

of degree zero. This property has been shown in volatility forecasting

applications to lead to higher power in Diebold-Mariano (1995) tests in Patton

and Sheppard (2009). Nolde and Ziegel (2017) show that there does not

generally exist an FZ loss function that generates loss differences that are

homogeneous of degree zero. However, zero-degree homogeneity may be attained

by exploiting the fact that, for the values of that are of interest

in risk management applications (namely, values ranging from around 0.01 to

0.10), we may assume that a.s. The following

proposition shows that if we further impose that a.s.

then, up to irrelevant location and scale factors, there is only

one FZ loss function that generates loss differences that are

homogeneous of degree zero.222If VaR can be positive, then there is one

free shape parameter in the class of zero-homogeneous FZ loss functions

( in the notation of the proof of Proposition

1). In that case, our use of the loss function in equation

(6) can be interpreted as setting that shape parameter to zero.

This shape parameter does not affect the consistency of the loss function, as

it is a member of the FZ class, but it may affect the ranking of misspecified

models, see Patton (2016). The fact that the loss function defined

below is unique has the added benefit that there are, of course, no remaining

shape or tuning parameters to be specified.

Proposition 1

Define the FZ loss difference for two forecasts and as Under the assumption that

VaR and ES are both strictly negative, the loss differences generated by a FZ

loss function are homogeneous of degree zero iff and

The resulting “FZ0” loss

function is:

(6)

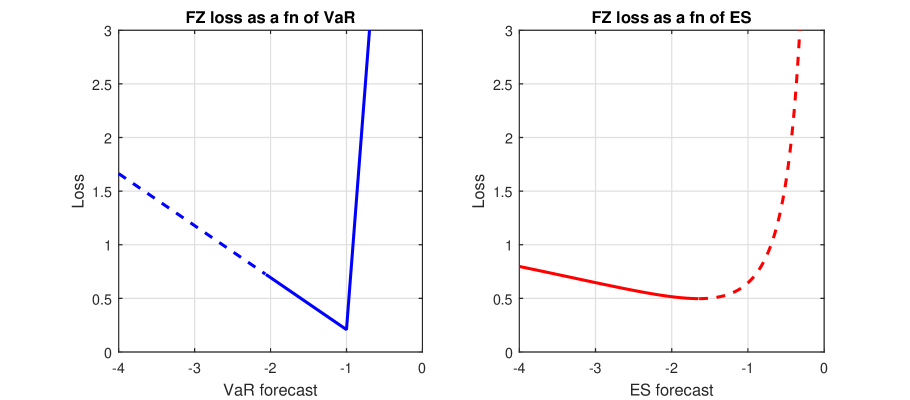

All proofs are presented in Appendix A. In Figure 1 we plot

when In the left panel we fix and vary and in

the right panel we fix and vary (These values for are the VaR and ES from a standard Normal

distribution.) As neither of these are the complete loss function, the minimum

is not zero in either panel. The left panel shows that the implied VaR loss

function resembles the “tick” loss function

from quantile estimation, see Komunjer (2005) for example. In the right panel

we see that the implied ES loss function resembles the “QLIKE” loss function from volatility forecasting, see Patton

(2011) for example. In both panels, values of where

are presented with a dashed line, as by definition is

below and so such values that would never be considered in

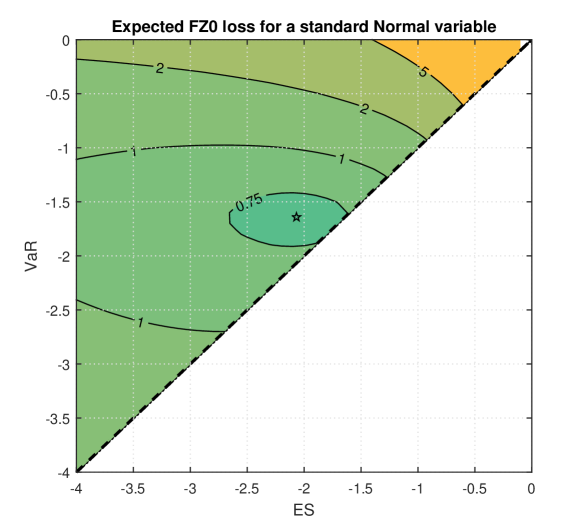

practice. In Figure 2 we plot the contours of expected FZ0

loss for a standard Normal random variable. The minimum value, which is

attained when , is marked

with a star, and we see that the “iso-expected

loss” contours are convex. Fissler (2017) shows that

convexity of iso-expected loss contours holds more generally for the FZ0 loss

function under any distribution with finite first moments, unique -quantiles, continuous densities, and negative ES.

With the FZ0 loss function in hand, it is then possible to consider

semiparametric dynamic models for ES and VaR:

(7)

that is, where the true VaR and ES are some specified parametric functions of

elements of the information set, The

parameters of this model are estimated via:

(8)

Such models impose a parametric structure on the dynamics of VaR and ES,

through their relationship with lagged information, but require no

assumptions, beyond regularity conditions, on the conditional distribution of

returns. In this sense, these models are semiparametric. Using theory for

M-estimators (see White (1994) and Newey and McFadden (1994) for example) we

establish in Section 3 below the asymptotic properties of such

estimators. Before doing so, we first consider some new dynamic specifications

for ES and VaR.

2.2 A GAS model for ES and VaR

One of the challenges in specifying a dynamic model for a risk measure, or any

other quantity of interest, is the mapping from lagged information to the

current value of the variable. Our first proposed specification for ES

and VaR draws on the work of Creal, et al. (2013) and Harvey

(2013), who proposed a general class of models called “generalized autoregressive score” (GAS) models by the

former authors, and “dynamic conditional

score” models by the latter author. In both cases the models

start from an assumption that the target variable has some parametric

conditional distribution, where the parameter (vector) of that distribution

follows a GARCH-like equation. The forcing variable in the model is the lagged

score of the log-likelihood, scaled by some positive definite matrix, a common

choice for which is the inverse Hessian. This specification nests many well

known models, including ARMA, GARCH (Bollerslev, 1986) and ACD (Engle and

Russell, 1998) models. See Koopman et al. (2016) for an overview of

GAS and related models.

We adopt this modeling approach and apply it to our M-estimation problem. In

this application, the forcing variable is a function of the derivative and

Hessian of the loss function rather than a log-likelihood. We will

consider the following GAS(1,1) model for ES and VaR:

(9)

where is a vector and

and are matrices. The forcing

variable in this specification is comprised of two components, the first is

the score:333Note that the expression given for only holds for As we assume that

is continuously distributed, this holds with probability one.

(14)

(15)

(16)

The scaling matrix, is related to the Hessian:

(17)

The second equality above exploits the fact that under the assumption that the dynamics for

VaR and ES are correctly specified. The first element of the matrix

depends on the unknown conditional density of We

would like to avoid estimating this density, and we approximate the term

as being proportional to This

approximation holds exactly if is a zero-mean location-scale random

variable, , where as in that case we have:

(18)

where is a

constant with the same sign as . We define to equal

with the first element replaced using the approximation in

the above equation.444Note that we do not use the fact that

the scaling matrix is exactly the inverse Hessian (e.g., by invoking the

information matrix equality) in our empirical application or our theoretical

analysis. Also, note that if we considered a value of for which

then and we cannot justify our approximation using

this approach. However, we focus on cases where and so we are

comfortable assuming making invertible. The

forcing variable in our GAS model for VaR and ES then becomes:

(19)

Notice that the second term in the model is a linear combination of the two

elements of the forcing variable, and since the forcing variable is

premultiplied by a coefficient matrix, say we can

equivalently use

(20)

We choose to work with the parameterization, as the

two elements of this forcing variable are not directly correlated, while the elements of

are correlated due to the overlapping

term () appearing in both elements. This aids the

interpretation of the results of the model without changing its fit.

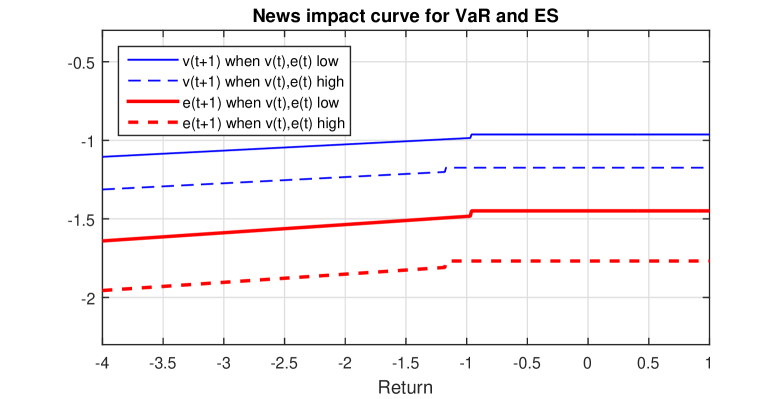

To gain some intuition for how past returns affect current forecasts of ES and

VaR in this model, consider the “news impact

curve” of this model, which presents as a function of through its impact on

holding all other variables constant. Figure 3 shows

these two curves for using the estimated parameters for this

model when applied to daily returns on the S&P 500 index (details are

presented in Section 5 below). We consider two values for the

“current” value of :

10% above and below the long-run average for these variables. We see that for

values where the news impact curves are flat, reflecting the

fact that on those days the value of the realized return does not enter the

forcing variable. When we see that ES and VaR react

linearly to and this reaction is through the forcing

variable; the reaction through the forcing variable is a

simple step (down) in both of these risk measures.

The specification in Section 2.2 allows ES and VaR to evolve as two

separate, correlated, processes. In many risk forecasting applications, a

useful simpler model is one based on a structure with only one time-varying

risk measure, e.g. volatility. We will consider a one-factor model in this

section, and will name the model in Section 2.2 a “two-factor” GAS model.

Consider the following one-factor GAS model for ES and VaR, where both risk

measures are driven by a single variable, :

(21)

The forcing variable, in the evolution equation for

is obtained from the FZ0 loss function, plugging in for . Using details provided in Appendix

B.2, we find that the score and Hessian are:

(22)

(23)

where is a negative constant and lies between zero

and one. The Hessian, , turns out to be a constant in this case, and

since we estimate a free coefficient on our forcing variable, we simply set

to one. Note that the VaR score, , turns out to drop out from the forcing variable. Thus the one-factor GAS

model for ES and VaR becomes:

(24)

Using the FZ loss function for estimation, we are unable to identify

as there exists such that both triplets yield identical

sequences of ES and VaR estimates, and thus identical values of the objective

function. We fix and forfeit identification of the level of the

series for , though we of course retain the ability to model and

forecast ES and VaR.555This one-factor model for ES and VaR can also be

obtained by considering a zero-mean volatility model for , with

standardized residuals, say denoted In this case, is

the log conditional standard deviation of , and and (We

exploit this interpretation when linking these models to GARCH models in

Section 2.5.1 below.) The lack of identification of means that

we do not identify the level of log volatility. Foreshadowing the empirical

results in Section 5, we find that this one-factor GAS model

outperforms the two-factor GAS model in out-of-sample forecasts for most of

the asset return series that we study.

2.4 Existing dynamic models for ES and VaR

As noted in the introduction, there is a relative paucity of dynamic models

for ES and VaR, but there is not a complete absence of such models. The

simplest existing model is based on a simple rolling window estimate of these

quantities:

(25)

where denotes the sample quantile of over the period

Common choices for the window size,

include 125, 250 and 500, corresponding to six months, one year and two years

of daily return observations respectively.

A more challenging competitor for the new ES and VaR models proposed in this

paper are those based on ARMA-GARCH dynamics for the conditional mean and

variance, accompanied by some assumption for the distribution of the

standardized residuals. These models all take the form:

(26)

where and are specified to follow some ARMA

and GARCH model, and is some arbitrary,

strictly increasing, distribution with mean zero and variance one. What

remains is to specify a distribution for the standardized residual, . Given a choice for VaR and ES forecasts are obtained as:

(27)

Two parametric choices for are common in the literature:

(28)

There are various skew distributions used in the literature; in the

empirical analysis below we use that of Hansen (1994). A nonparametric

alternative is to estimate the distribution of using the empirical

distribution function (EDF), an approach that is also known as

“filtered historical simulation,” and one

that is perhaps the best existing model for ES, see the survey by Engle and

Manganelli (2004b).666Some authors have also considered modeling the

tail of using extreme value theory, however for the relatively

non-extreme values of we consider here, past work (e.g., Engle and

Manganelli (2004b), Nolde and Ziegel (2016) and Taylor (2017)) has found EVT

to perform no better than the EDF, and so we do not include it in our

analysis. We consider all of these models in our empirical analysis

in Section 5.

2.5 GARCH and ES/VaR estimation

In this section we consider two extensions of the models presented above, in

an attempt to combine the success and parsimony of GARCH models with this

paper’s focus on ES and VaR forecasting.

2.5.1 Estimating a GARCH model via FZ minimization

If an ARMA-GARCH model, including the specification for the distribution of

standardized residuals, is correctly specified for the conditional

distribution of an asset return, then maximum likelihood is the most efficient

estimation method, and should naturally be adopted. If, on the other hand, we

consider an ARMA-GARCH model only as a useful approximation to the true

conditional distribution, then it is no longer clear that MLE is optimal. In

particular, if the application of the model is to ES and VaR forecasting, then

we might be able to improve the fitted ARMA-GARCH model by estimating the

parameters of that model via FZ loss minimization, as discussed in Section

2.1. This estimation method is related to one discussed in Remark 1 of

Francq and Zakoïan (2015).

Consider the following model for asset returns:

(29)

The variable is the conditional variance and is assumed to

follow a GARCH(1,1) process. This model implies a structure analogous to the

one-factor GAS model presented in Section 2.3, as we find:

(30)

Some further results on VaR and ES in dynamic location-scale models are

presented in Appendix B.3. To apply this model to VaR and ES forecasting, we

also have to estimate the VaR and ES of the standardized residual, denoted

Rather than estimating the parameters of this model

using (Q)MLE, we consider here estimating the via FZ loss minimization. As in

the one-factor GAS model, is unidentified and we set it to one, so

the parameter vector to be estimated is .

This estimation approach leads to a fitted GARCH model that is tailored to

provide the best-fitting ES and VaR forecasts, rather than the best-fitting

volatility forecasts.

2.5.2 A hybrid GAS/GARCH model

Finally, we consider a direct combination of the forcing variable suggested by

a GAS structure for a one-factor model of returns, described in equation

(24), with the successful GARCH model for volatility. We specify:

(31)

The variable is the log-volatility, identified up to scale. As

the latent variable in this model is log-volatility, we use the lagged log

absolute return rather than the lagged squared return, so that the units

remain in line for the evolution equation for . There are five

parameters in this model and we

estimate them using FZ loss minimization.

3 Estimation of dynamic models for ES and VaR

This section presents asymptotic theory for the estimation of dynamic ES

and VaR models by minimizing FZ loss. Given a sample of observations and a constant ,

we are interested in estimating and forecasting the conditional

quantile (VaR) and corresponding expected shortfall of . Suppose

is a real-valued random variable that has, conditional on information

set , distribution function and corresponding density function . Let and

be some initial conditions for VaR and ES and

let where is a vector of exogenous variables

or predetermined variables, be the information set available for forecasting

. The vector of unknown parameters to be estimated is .

The conditional VaR and ES of at probability level that is

and

, are assumed to

follow some dynamic model:

(32)

The unknown parameters are estimated as:

(33)

and the FZ loss function is defined in equation (6).

Below we provide conditions under which estimation of these parameters via FZ

loss minimization leads to a consistent and asymptotically normal estimator,

with standard errors that can be consistently estimated.

Assumption 1

(A) obeys the uniform law of large numbers.

(B)(i) is a compact subset of for

(ii) is a strictly stationary process. Conditional

on all the past information , the distribution of

is which, for all belongs

to a class of distribution functions on with finite first moments

and unique -quantiles. (iii) , both and are -measurable and

continuous in . (iv) If , then

Theorem 1 (Consistency)

Under Assumption 1, as

The proof of Theorem 1, provided in Appendix A, is

straightforward given Theorem 2.1 of Newey and McFadden (1994) and Corollary

5.5 of Fissler and Ziegel (2016). Note that a variety of uniform laws of large

numbers (our Assumption 1(A)) are available for the time series applications

we consider here, see Andrews (1987) and Pötscher and Prucha (1989) for

example. Zwingmann and Holzmann (2016) show that if the -quantile is

not unique (violating our Assumption 1(B)(iii)), then the convergence rate and

asymptotic distribution of are

non-standard, even in a setting with data. We do not consider such

problematic cases here.

We next turn to the asymptotic distribution of our parameter estimator. In the

assumptions below, denotes a finite constant that can change from line to

line, and we use to denote the Euclidean

norm of a vector

Assumption 2

(A) For all , we have (i) and are twice continuously differentiable in ,

(ii) .

(B) For all , we have (i) Conditional on all the past information

, has a continuous density that satisfies and , (ii) , for some .

(C) There exists a neighborhood of , , such that for all we have (i)

, (ii) there exist some (possibly stochastic)

-measurable functions ,

, , , which satisfy : , , , , and

.

(D) For some and for all we have (i) , , , , (ii)

,(iii)

,

(E) The matrix defined in Theorem 2 has

eigenvalues bounded below by a positive constant for sufficiently large.

(F) The sequence obeys

the CLT, where

(34)

(35)

(G) is -mixing of size for some

Most of the above assumptions are standard. Assumption 2(A)(i) imposes that

the VaR is negative, but given our focus on the left-tail of asset returns, this is not likely a binding constraint.

Assumptions 2(B),(C) and (E) are similar to those in Engle and Manganelli

(2004a). Assumption 2(B)(ii) requires at least moments of returns

to exist, however 2(D) may actually increase the number of required moments,

depending on the VaR-ES model employed. For the familiar GARCH(1,1) process,

used in our simulation study, it can be shown that we only need to assume that

moments exist. Assumption 2(F) allows for some CLT for mixing data

to be invoked, and 2(G) is a standard assumption on the time series dependence

of the data.

Theorem 2 (Asymptotic Normality)

Under Assumptions 1 and 2, we have

(36)

where

(37)

(38)

and is defined in Assumption 2(F).

An outline of the proof of this theorem is given in Appendix A, and the

detailed lemmas underlying it are provided in the supplemental appendix. The

proof of Theorem 2 builds on Huber (1967), Weiss (1991)

and Engle and Manganelli (2004a), who focused on the estimation of quantiles.

Finally, we present a result for estimating the asymptotic covariance matrix

of thereby enabling the reporting of standard

errors and confidence intervals.

Assumption 3

(A) The deterministic positive sequence satisfies and

.

(B)(i) , where

is defined in Theorem 2.

(ii) .

(iii) .

Theorem 3

Under Assumptions 1-3, and , where

This result extends Theorem 3 in Engle and Manganelli (2004a) from dynamic

VaR models to dynamic joint models for VaR and ES. The key choice in

estimating the asymptotic covariance matrix is the bandwidth parameter in

Assumption 3(A). In our simulation study below we set this to and

we find that this leads to satisfactory finite-sample properties.

The results here extend some very recent work in the literature: Dimitriadis

and Bayer (2017) consider VaR-ES regression, but focus on data and

linear specifications.777Dimitriadis and Bayer (2017) also consider a

variety of FZ loss functions, in contrast with our focus on the FZ0 loss

function, and they consider both and GMM (or , in their

notation) estimation, while we focus only on estimation. Barendse

(2017) considers “interquantile expectation

regression,” which nests VaR-ES regression as a special

case. He allows for time series data, but imposes that the models are linear.

Our framework allows for time series data and nonlinear models.

4 Simulation study

In this section we investigate the finite-sample accuracy of the asymptotic

theory for dynamic ES and VaR models presented in the previous section. For

ease of comparison with existing studies of related models, such as volatility

and VaR models, we consider a GARCH(1,1) for the DGP, and estimate the

parameters by FZ-loss minimization. Specifically, the DGP is

(39)

(40)

We set the parameters of this DGP to We consider two choices for the distribution

of : a standard Normal, and the standardized skew distribution

of Hansen (1994), with degrees of freedom and skewness parameters in the

latter set to Under this DGP, the ES and VaR are

proportional to , with

(41)

We make the dependence of the coefficients of proportionality on explicit here, as we consider a

variety of values of in this simulation study: Interest in VaR and ES from regulators

focuses on the smaller of these values of but we also consider the

larger values to better understand the properties of the asymptotic

approximations at various points in the tail of the distribution.

For a standard Normal distribution, with CDF and PDF denoted and

we have:

(42)

For Hansen’s skew distribution we can obtain from the inverse

CDF, but no closed-form expression for is available; we instead

use a simulation of 10 million draws to estimate it. As noted above, FZ

loss minimization does not allow us to identify in the GARCH model,

and in our empirical work we set this parameter to 1. To facilitate

comparisons of the accuracy of estimates of in our simulation study we instead set at its true value.

This is done without loss of generality and merely eases the presentation of

the results. To match our empirical application, we replace the parameter

with and so our parameter

vector becomes

We consider two sample sizes, corresponding

to 10 and 20 years of daily returns respectively. These large sample sizes

enable us to consider estimating models for quantiles as low as 1%, which are

often used in risk management. We repeat all simulations 1000 times.

Table 1 presents results for the estimation of this model on standard Normal

innovations, and Table 2 presents corresponding results for skew

innovations. The top row of each panel present the true parameter values, with

the latter two parameters changing across The second row presents

the median estimated parameter across simulations, and the third row presents

the average bias in the estimated parameter. Both of these measures indicate

that the parameter estimates are nicely centered on the true parameter values.

The penultimate row presents the cross-simulation standard deviations of the

estimated parameters, and we observe that these decrease with the sample size

and increase as we move further into the tails (i.e., as decreases),

both as expected. Comparing the standard deviations across Tables 1 and 2, we

also note that they are higher for skew innovations than Normal

innovations, again as expected.

The last row in each panel presents the coverage probabilities for 95%

confidence intervals for each parameter, constructed using the estimated

standard errors, with bandwidth parameter . For we see that the coverage is reasonable,

ranging from around 0.88 to 0.96. For or the

coverage tends to be too low, particularly for the smaller sample size. Thus

some caution is required when interpreting the standard errors for the models

with the smallest values of In Table S1 of the Supplemental Appendix

we present results for (Q)MLE for the GARCH model corresponding to the results

in Tables 1 and 2, using the theory of Bollerslev and Wooldridge (1992). In

Tables S2 and S3 we present results for CAViaR estimation of this model, using

the “tick” loss function and the theory of

Engle and Manganelli (2004a).888In (Q)MLE, the parameters to be

estimated are In “CAViaR” estimation, which is done by minimizing the

“tick” loss function, the parameters to be

estimated are since in this case

the parameter is again unidentified. As for the study of FZ

estimation, we set to its true value to facilitate interpretation of

the results. We find that (Q)MLE has better finite sample properties than FZ

minimization, but CAViaR estimation has slightly worse properties than FZ minimization.

[INSERT TABLES 1 AND 2 ABOUT HERE ]

In Table 3 we compare the efficiency of FZ estimation relative to (Q)MLE and

to CAViaR estimation, for the parameters that all three estimation methods

have in common, namely As expected, when the

innovations are standard Normal, FZ estimation is substantially less efficient

than MLE, however when the innovations are skew the loss in efficiency

drops and for some values of FZ estimation is actually more efficient

than QMLE. This switch in the ranking of the competing estimators is

qualitatively in line with results in Francq and Zakoïan (2015). In

Panel B of Table 3, we see that FZ estimation is generally, though not

uniformly, more efficient than CAViaR estimation.

In many applications, interest is more focused on the forecasted values of VaR

and ES than the estimated parameters of the models. To study this, Table 4

presents results on the accuracy of the fitted VaR and ES estimates for the

three estimation methods: (Q)MLE, CAViaR and FZ estimation. To obtain

estimates of VaR and ES from the (Q)ML estimates, we follow common empirical

practice and compute the sample VaR and ES of the estimated standardized

residuals. In the first column of each panel we present the mean absolute

error (MAE) from (Q)MLE, and in the next two columns we present the

relative MAE of CAViaR and FZ to (Q)MLE. Table 4 reveals that (Q)MLE

is the most accurate estimation method. Averaging across values of

CAViaR is about 40% worse for Normal innovations, and 24% worse for skew

innovations, while FZ fares somewhat better, being about 30% worse for Normal

innovations and 16% worse for skew innovations. The superior performance

of (Q)MLE is not surprising when the innovations are Normal, as that

corresponds to (full) maximum likelihood, which has maximal efficiency.

Weighing against the loss in FZ estimation efficiency is the

robustness that FZ estimation offers relative to QML. For

applications even further from Normality, e.g. with time-varying skewness or

kurtosis, the loss in efficiency of QML is likely even greater.

[INSERT TABLES 3 AND 4 ABOUT HERE ]

Overall, these simulation results show that the asymptotic results of the

previous section provide reasonable approximations in finite samples, with the

approximations improving for larger sample sizes and less extreme values of

Compared with MLE, estimation by FZ loss minimization is generally

less accurate, while it is generally more accurate than estimation using

the CAViaR approach of Engle and Manganelli (2004a). The latter

outperformance is likely attributable to the fact that FZ estimation draws on

information from two tail measures, VaR and ES, while CAViaR was designed to

only model VaR.

5 Forecasting equity index ES and VaR

We now apply the models discussed in Section 2 to the forecasting

of ES and VaR for daily returns on four international equity indices. We

consider the S&P 500 index, the Dow Jones Industrial Average, the NIKKEI 225

index of Japanese stocks, and the FTSE 100 index of UK stocks. Our sample

period is 1 January 1990 to 31 December 2016, yielding between 6,630 and 6,805

observations per series (the exact numbers vary due to differences in holidays

and market closures). In our out-of-sample analysis, we use the first ten

years for estimation, and reserve the remaining 17 years for evaluation and

model comparison.

Table 5 presents full-sample summary statistics on these four return series.

Average annualized returns range from -2.7% for the NIKKEI to 7.2% for the

DJIA, and annualized standard deviations range from 17.0% to 24.7%. All

return series exhibit mild negative skewness (around -0.15) and substantial

kurtosis (around 10). The lower two panels of Table 5 present the sample VaR

and ES for four choices of

Table 6 presents results from standard time series models estimated on these

return series over the in-sample period (Jan 1990 to Dec 1999). In the first

panel we present the estimated parameters of the optimal ARMA models, where the choice of is made using

the BIC. The values from the optimal models never rises above 1%,

consistent with the well-known lack of predictability of these series. The

second panel presents the parameters of the GARCH(1,1) model for conditional

variance, and the lower panel presents the estimated parameters the skew

distribution applied to the standardized residuals. All of these parameters

are broadly in line with values obtained by other authors for these or similar series.

[ INSERT TABLES 5 AND 6 ABOUT HERE ]

5.1 In-sample estimation

We now present estimates of the parameters of the models presented in Section

2, along with standard errors computed using the theory from

Section 3.999Computational details on the estimation of

these models are given in Appendix C. In the interests of space, we only

report the parameter estimates for the S&P 500 index for . The

two-factor GAS model based on the FZ0 loss function is presented in the left

panel of Table 7. This model allows for separate dynamics in VaR and ES, and

we present the parameters for each of these risk measures in separate columns.

We observe that the persistence of these processes is high, with the estimated

parameters equal to 0.973 and 0.977, similar to the persistence found in

GARCH models (e.g., see Table 6). The model-implied average values of VaR

and ES are -2.001 and -2.556, similar to the sample values of these measures

reported in Table 5. We also observe that in neither equation is the

coefficient on statistically significant: the -statistics on

are both well below one. The coefficients on are both

larger, and more significant (the -statistics are 1.58 and 1.75),

indicating that the forcing variable from the ES part of the FZ0 loss function

is the more informative component. However, the overall imprecision of the

four coefficients on the forcing variables is suggestive that this model is over-parameterized.

The right panel of Table 7 shows three one-factor models for ES and VaR. The

first is the one-factor GAS model, which is nested in the two-factor model

presented in the left panel. We see a slight loss in fit (the average loss is

slightly greater) but the parameters of this model are estimated with greater

precision. The one-factor GAS model fits slightly better than the GARCH model

estimated via FZ loss minimization (reported in the penultimate

column).101010Recall that in all of the one-factor models, the intercept

in the GAS equation is unidentified. We fix it at

zero for the GAS-1F and Hybrid models, and at one for the GARCH-FZ model.

This has no impact on the fit of these models for VaR and ES, but it means

that we cannot interpret the estimated parameters as

the VaR and ES of the standardized residuals, and we no longer expect the

estimated values to match the sample estimates in Table 5. The

“hybrid” model, augmenting the one-factor

GAS model with a GARCH-type forcing variable, fits better than the other

one-factor models, and also better than the larger two-factor GAS model, and

we observe that the coefficient on the GARCH forcing variable is significantly different from zero (with a -statistic of 2.07).

[ INSERT TABLE 7 ABOUT HERE ]

5.2 Out-of-sample forecasting

We now turn to the out-of-sample (OOS) forecast performance of the models

discussed above, as well as some competitor models from the existing

literature. We will focus initially on the results for given

the focus on that percentile in the extant VaR literature. (Results for other

values of are considered later, with details provided in the

supplemental appendix.) We will consider a total of ten models for forecasting

ES and VaR. Firstly, we consider three rolling window methods, using window

lengths of 125, 250 and 500 days. We next consider ARMA-GARCH models, with the

ARMA model orders selected using the BIC, and assuming that the distribution

of the innovations is standard Normal or skew or estimating it

nonparametrically using the sample ES and VaR of the estimated standardized

residuals. Finally we consider four new semiparametric dynamic models for ES

and VaR: the two-factor GAS model presented in Section 2.2, the

one-factor GAS model presented in Section 2.3, a GARCH model estimated

using FZ loss minimization, and the “hybrid” GAS/GARCH model presented in Section 2.5. We estimate these

models using the first ten years as our in-sample period, and retain those

parameter estimates throughout the OOS period.

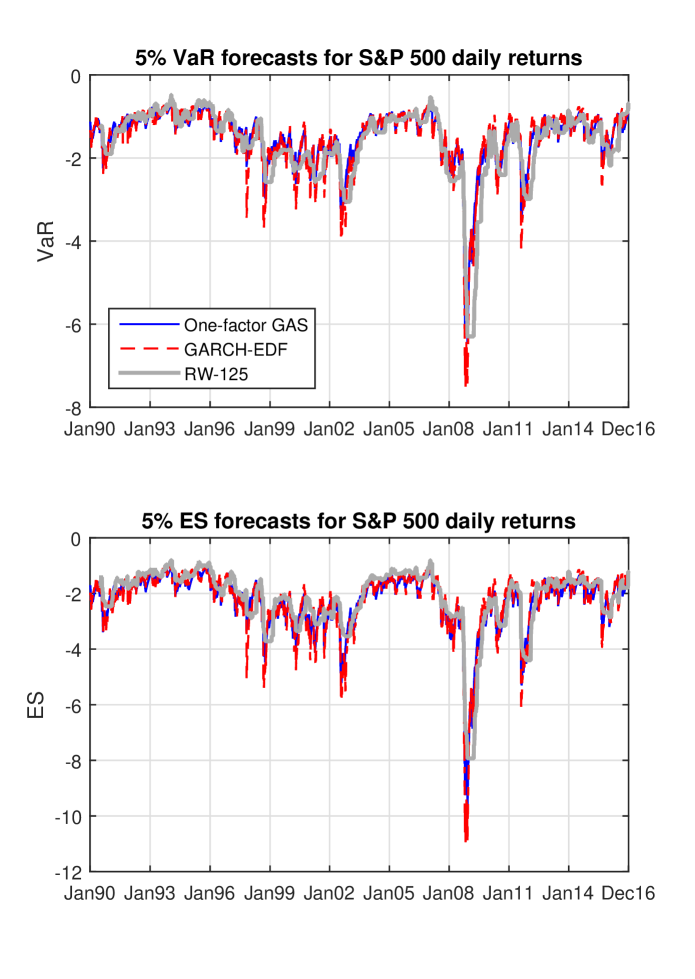

In Figure 4 below we plot the fitted 5% ES and VaR for the S&P

500 return series, using three models: the rolling window model using a window

of 125 days, the GARCH-EDF model, and the one-factor GAS model. This figure

covers both the in-sample and out-of-sample periods. The figure shows that the

average ES was estimated at around -2%, rising as high as around -1% in the

mid 90s and mid 00s, and falling to its most extreme values of around -10%

during the financial crisis in late 2008. Thus, like volatility, ES fluctuates

substantially over time.

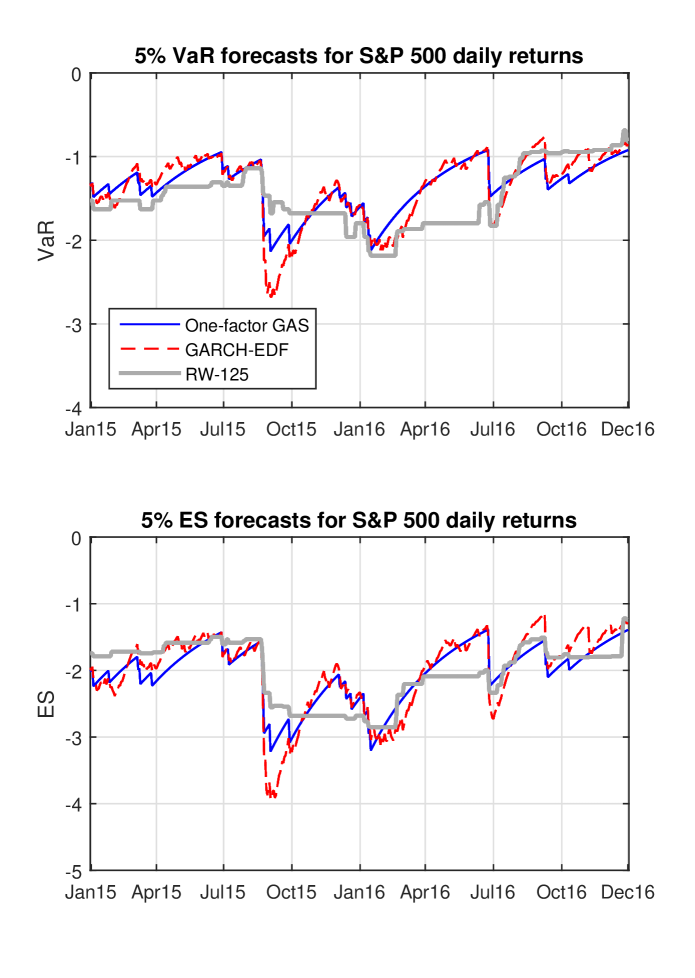

Figure 5 zooms in on the last two years of our sample period, to

better reveal the differences in the estimates from these models. We observe

the usual step-like movements in the rolling window estimate of VaR and ES, as

the more extreme observations enter and leave the estimation window. Comparing

the GARCH and GAS estimates, we see how they differ in reacting to returns:

the GARCH estimates are driven by lagged squared returns, and thus move

stochastically each day. The GAS estimates, on the other hand, only use

information from returns when the VaR is violated, and on other days the

estimates revert deterministically to the long-run mean. This generates a

smoother time series of VaR and ES estimates. We investigate below which of

these estimates provides a better fit to the data.

The left panel of Table 8 presents the average OOS losses, using the FZ0 loss

function from equation (6), for each of the ten models, for the

four equity return series. The lowest values in each column are highlighted in

bold, and the second-lowest are in italics. We observe that the one-factor

GAS model, labelled FZ1F, is the preferred model for the two US equity

indices, while the Hybrid model is the preferred model for the NIKKEI and

FTSE indices. The worst model is the rolling window with a window length of

500 days.

While average losses are useful for an initial look at OOS forecast

performance, they do not reveal whether the gains are statistically

significant. Table 9 presents Diebold-Mariano t-statistics on the loss

differences, for the S&P 500 index. Corresponding tables for the other three

equity return series are presented in Table S4 of the supplemental appendix.

The tests are conducted as “row model minus column

model” and so a positive number indicates that the column

model outperforms the row model. The column “FZ1F” corresponding to the one-factor GAS model contains all

positive entries, revealing that this model out-performed all competing

models. This outperformance is strongly significant for the comparisons to the

rolling window forecasts, as well as the GARCH model with Normal innovations.

The gains relative to the GARCH model with skew or nonparametric

innovations are not significant, with DM -statistics of 1.48 and 1.16

respectively. Similar results are found for the best models for each of the

other three equity return series. Thus the worst models are easily separated

from the better models, but the best few models are generally not

significantly different.111111Table S5 in the supplemental appendix

presents results analogous to Table 8, but with alpha=0.025, which is the

value for ES that is the focus of the Basel III accord. The rankings and

results are qualitatively similar to those for alpha=0.05 discussed here.

[ INSERT TABLES 8 AND 9 ABOUT HERE ]

To complement the study of the relative performance of these models for ES

and VaR, we now consider goodness-of-fit tests for the OOS forecasts of VaR

and ES. Under correct specification of the model for VaR and ES, we know

that

(43)

and we note that this implies that where

are defined in equations

(15)-(16). Thus the variables and

can be considered as a form of “generalized

residual” for this model. To mitigate the impact of serial

correlation in these measures (which comes through the persistence of

and ) we use standardized versions of these residuals:

(44)

These standardized generalized residuals are also conditionally mean zero

under correct specification, and we note that the standardized residual for

VaR is simply the demeaned “hit” variable,

which is the focus of well-known tests from the VaR literature, see

Christoffersen (1998) and Engle and Manganelli (2004a). We adopt the

“dynamic quantile (DQ)” testing approach of

Engle and Manganelli (2004a), which is based on simple regressions of these

generalized residuals on elements of the information set available at the time

the forecast was made. Consider, then the following “DQ” and “DES” regressions:

(45)

We test forecast optimality by testing that all terms ( and ) in these regressions are zero, against the

usual two-sided alternative. Similar “conditional

calibration” tests are presented in Nolde and Ziegel

(2017). One could also consider a joint test of both of the above null

hypotheses, however we will focus on these separately so that we can determine

which variable is well/poorly specified.

The right two panels of Table 8 present the -values from the tests of the

goodness-of-fit of the VaR and ES forecasts. Entries greater than 0.10

(indicating no evidence against optimality at the 0.10 level) are in bold, and

entries between 0.05 and 0.10 are in italics. For the S&P 500 index and the

DJIA, we see that only one model passes both the VaR and ES tests: the

one-factor GAS model. For the NIKKEI we see that all of the dynamic models

pass these two tests, while all three of the rolling window models fail. For

the FTSE index, on the other hand, we see that all ten models considered here

fail both the goodness-of-fit tests. The outcomes for the NIKKEI and the FTSE

each, in different ways, present good examples of the problem highlighted

in Nolde and Ziegel (2017), that many different models may pass a

goodness-of-fit test, or all models may fail, which makes discussing their

relative performance difficult. To do so, one can look at Diebold-Mariano

tests of differences in average loss, as we do in Table 9.

Finally, in Table 10 we look at the performance of these models across four

values of to see whether the best-performing models change with how

deep in the tails we are. We find that this is indeed the case: for

the best-performing model across the four return series is the

GARCH model estimated by FZ loss minimization, followed by the GARCH model

with nonparametric residuals. These two models are also the (equal) best two

models for . For and the two best

models are the one-factor GAS model and the Hybrid model. These rankings are

perhaps related to the fact that the forcing variable in the GAS model depends

on observing a violation of the VaR, and for very small values of

these violations occur only infrequently. In contrast, the GARCH model uses

the information from the squared residual, and so information from the data

moves the risk measures whether a VaR violation was observed or not. When

is not so small, the forcing variable suggested by the GAS model

applied to the FZ loss function starts to out-perform.

[ INSERT TABLE 10 ABOUT HERE ]

6 Conclusion

With the implementation of the Third Basel Accord in the next few years, risk

managers and regulators will place greater focus on expected shortfall (ES)

as a measure of risk, complementing and partly substituting previous emphasis

on Value-at-Risk (VaR). We draw on recent results from statistical decision

theory (Fissler and Ziegel, 2016) to propose new dynamic models for ES and

VaR. The models proposed are semiparametric, in that they impose parametric

structures for the dynamics of ES and VaR, but are agnostic about the

conditional distribution of returns. We also present asymptotic distribution

theory for the estimation of these models, and we verify that the theory

provides a good approximation in finite samples. We apply the new models and

methods to daily returns on four international equity indices, over the period

1990 to 2016, and find the proposed new ES-VaR models outperform forecasts

based on GARCH or rolling window models.

The asymptotic theory presented in this paper facilitates considering a large

number of extensions of the models presented here. Our models all focus on a

single value for the tail probability and extending

these to consider multiple values simultaneously could prove fruitful. For

example, one could consider the values 0.01, 0.025 and 0.05, to capture

various points in the left tail, or one could consider 0.05 and 0.95 to

capture both the left and right tails simultaneously. Another natural

extension is to make use of exogenous information in the model; the models

proposed here are all univariate, and one might expect that information from

options markets, high frequency data, or news announcements to also help

predict VaR and ES. We leave these interesting extensions to future research.

Appendix A: Proofs

Proof of Proposition 1. Theorem C.3 of Nolde and Ziegel (2017)

shows that under the assumption that ES is strictly negative, the loss

differences generated by a FZ loss function are homogeneous of degree zero iff

and with and . Denote the

resulting loss function as and notice that:

Under the assumption that the third term vanishes. The second term is

purely a function of and so can be disregarded; we can set

without loss of generality. The first term is affected by a scaling parameter

and we can set without loss of generality.

Thus we obtain the given in equation (6). If can be

positive, then setting is interpretable as fixing this shape

parameter value at a particular value.

Proof of Theorem 1. The proof is based on Theorem 2.1 of

Newey and McFadden (1994). We only need to show that is

uniquely minimized at , because the other assumptions of

Newey and McFadden’s theorem are clearly satisfied. By Corollary (5.5) of

Fissler and Ziegel (2016), given Assumption 1(B)(iii) and the fact that our

choice of the objective function satisfies the condition as in

Corollary (5.5) of Fissler and Ziegel (2016), we know that is

uniquely minimized at which equals

under

correct specification. Combining this assumption and Assumption 1(B)(iv), we

know that is a unique minimizer of , completing the proof.

Outline of proof of Theorem 2. We consider the population

objective function and take a mean-value

expansion of around We show in Lemma 1 that:

In the supplemental appendix we prove Lemma 1 by building on and

extending Weiss (1991), who extends Huber (1967) to non-iid data. We

draw on Weiss’ Lemma A.1, and we verify that all five assumptions (N1-N5 in

his notation) for that lemma are satisfied: N1, N2 and N5 are obviously

satisfied given our Assumptions 1-2, and we show in Lemmas 3 -

6 that assumptions N3 and N4 are satistfied. Assumption 2(F)

allows a CLT to be applied: the asymptotic covariance matrix is and we denote as leading to the stated result.

Proof of Theorem 3. Given Assumption 3B(i) and the result in

Theorem 1, the proof that is standard and omitted. Next, define

To prove the result we will show that and .

Firstly, consider

The last line above was shown to be in the proof of Theorem 2. The

difficult quantity in the first term (over the first six lines above) is the

indicator, and following the same steps as in Engle and Manganelli (2004a),

that term is also Next, consider :

Following Engle and Manganelli (2004a), assumptions 1-3 are sufficient to

show and the result follows.

Appendix B: Derivations

Appendix B.1: Generic calculations for the FZ0 loss function

The FZ0 loss function is:

(46)

Note that this is not homogeneous, as for any , but this loss function generates loss differences that

are homogenous of degree zero, as the additive additional term above drops out.

We will frequently use the first derivatives of this loss function, and the

second derivatives of the expected loss for an absolutely continuous random

variable with density and CDF . These are (for ):

(47)

(48)

where

(49)

(50)

and

(51)

(52)

(53)

Appendix B.2: Derivations for the one-factor GAS model for ES and

VaR

Here we present the calculations to compute and for this

model. Below we use:

(54)

(55)

And so we find (for )

(56)

(57)

(58)

Thus, the term drops out of and we are left with

Next we calculate

(59)

But note that under correct specification,

(60)

and so the Hessian simplifies to:

(61)

(62)

(63)

Thus although the Hessian couldvary with time, as it is a

derivative of the conditional expected loss, in this specification it

simplifies to a constant.

Appendix B.3: ES and VaR in location-scale models

Dynamic location-scale models are widely used for asset returns and in this

section we consider what such a specification implies for the dynamics of ES

and VaR. Consider the following:

(64)

where, for example, is some ARMA model and is some

GARCH model. For asset returns that follow equation (64) we have:

(65)

and we we can recover from :

(66)

Thus under the conditional location-scale assumption, we can back out the

conditional mean and variance from the VaR and ES. Next note that if then , where . Daily asset returns often have means that are close to zero,

and so this restriction is one that may be plausible in the data. A related,

though less plausible, restriction is that and in that case we have the simplification that , where

Appendix C: Estimation using the FZ0 loss function

The FZ0 loss function, equation (6), involves the indicator

function and so necessitates

the use of a numerical search algorithm that does not rely on

differentiability of the objective function; we use the function

fminsearch in Matlab. However, in preliminary simulation analyses we

found that this algorithm was sensitive to the starting values used in the

search. To overcome this, we initially consider a “smoothed” version of the FZ0 loss function, where we replace

the indicator variable with a Logistic function:

(67)

(68)

where is the smoothing parameter, and the smoothing function

converges to the indicator function as In GAS models

that involve an indicator function in the forcing variable, we alter the

forcing variable in the same way, to ensure that the objective function as a

function of is differentiable. In these cases the loss

function and the model itself are slightly altered through this smoothing.

In our empirical implementation, we obtain “smart” starting values by first estimating the model using

the “smoothed FZ0” loss function with

This choice of gives some smoothing for values of

that are roughly within of Call the resulting parameter

estimate Since this

objective function is differentiable, we can use more familiar gradient-based

numerical search algorithms, such as fminunc or fmincon in

Matlab, which are often less sensitive to starting values. We then re-estimate

the model, using as the

starting value, setting and obtain This value of smoothes values of

within roughly of and so this objective function is closer

to the true objective function. Finally, we use as the starting value in the optimization of the

actual FZ0 objective function, with no artificial smoothing, using the

function fminsearch, and obtain . We found

that this approach largely eliminated the sensitivity to starting values.

References

[1]Andersen, T.G., Bollerslev, T., Christoffersen, P., Diebold, F.X.,

2006. Volatility and Correlation Forecasting, in (ed.s) G. Elliott, C.W.J.

Granger, and A. Timmermann, Handbook of Economic Forecasting, Vol. 1.

Elsevier, Oxford.

[2]Andrews, D.W.K., 1987, Consistency in nonlinear econometric models:

ageneric uniform law of large numbers, Econometrica, 55, 1465–1471.

[3]Artzner, P., F. Delbaen, J.M. Eber and D. Heath, 1999, Coherent

measures of risk, Mathematical Finance, 9, 203-228.

[4]Barendse, S., 2017, Interquantile Expectation Regression, Tinbergen

Institute Discussion Paper, TI 2017-034/III.

[5]Basel Committee on Banking Supervision, 2010, Basel III: A Global

Regulatory Framework for More Resiliant Banks and Banking Systems, Bank for

International Settlements. http://www.bis.org/publ/bcbs189.pdf

[7]Bollerslev, T. and J.M. Wooldridge, 1992, Quasi-Maximum Likelihood

Estimation and Inference in Dynamic Models with Time Varying Covariances,

Econometric Reviews, 11(2), 143-172.

[8]Cai, Z. and X. Wang, 2008, Nonparametric estimation of conditional

VaR and expected shortfall, Journal of Econometrics, 147, 120-130.

[9]Creal, D.D., S.J. Koopman, and A. Lucas, 2013, Generalized

Autoregressive Score Models with Applications, Journal of Applied

Econometrics, 28(5), 777-795.

[10]Creal, D.D., S.J.Koopman, A. Lucas, and M. Zamojski, 2015,

Generalized Autoregressive Method of Moments, Tinbergen Institute Discussion

Paper, TI 2015-138/III.

[11]Diebold, F.X. and R.S. Mariano, 1995. Comparing predictive

accuracy, Journal of Business & Economic Statistics,13(3), 253–263.

[12]Dimitriadis, T. and S. Bayer, 2017, A Joint Quantile and Expected

Shortfall Regression Framework, working paper, available at

arXiv:1704.02213v1.

[13]Du, Z. and J.C. Escanciano, 2017, Backtesting Expected

Shortfall: Accounting for Tail Risk, Management Science, 63(4), 940-958.

[14]Engle, R.F. and S. Manganelli, 2004a, CAViaR: Conditional

Autoregressive Value at Risk by Regression Quantiles, Journal of

Business & Economic Statistics, 22, 367-381.

[15]Engle, R.F. and S. Manganelli, 2004b, A Comparison of Value-at-Risk

Models in Finance, in Giorgio Szego (ed.) Risk Measures for the 21st

Century, Wiley.

[16]Engle, R.F. and J.R. Russell, 1998, Autoregressive Conditional

Duration: A New Model for Irregularly Spaced Transaction Data,

Econometrica, 66, 1127-1162.

[17]Fissler, T., 2017, On Higher Order Elicitability and Some

Limit Theorems on the Poisson and Weiner Space, PhD thesis, University of Bern.

[18]Fissler, T., and J. F. Ziegel, 2016, Higher order elicitability

and Osband’s principle, Annals of Statistics, 44(4), 1680-1707.

[19]Francq, C. and J.-M. Zakoïan, 2015, Risk-parameter estimation

in volatility models, Journal of Econometrics, 184, 158-173.

[20]Gerlach, R. and C.W.S. Chen, 2015, Bayesian Expected Shortfall

Forecasting Incorporating the Intraday Range, Journal of Financial

Econometrics, 14(1), 128-158.

[21]Gneiting, T., 2011, Making and Evaluating Point Forecasts,

Journal of the American Statistical Association, 106(494), 746-762.

[22]Gschöpf, P., W.K. Härdle, and A. Mihoci, Tail Event Risk

Expectile based Shortfall, SFB 649 Discussion Paper 2015-047.

[23]Hansen, B.E., 1994, Autoregressive Conditional Density Estimation,

International Economic Review, 35(3), 705-730.

[24]Harvey, A.C., 2013, Dynamic Models for Volatility and Heavy

Tails, Econometric Society Monograph 52, Cambridge University Press, Cambridge.

[25]Huber, P.J., 1967, The behavior of maximum likelihood estimates

under nonstandard conditions, in (ed.s) L.M. Le Cam and J. Neyman

Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics

and Probability, Vol. 1, University of California Press, Berkeley.

[26]Komunjer, I., 2005, Quasi-Maximum Likelihood Estimation for

Conditional Quantiles, Journal of Econometrics, 128(1), 137-164.

[27]Komunjer, I., 2013, Quantile Prediction, in (ed.s) G. Elliott, and

A. Timmermann, Handbook of Economic Forecasting, Vol. 2. Elsevier, Oxford.

[28]Koopman, S.J., A. Lucas and M. Scharth, Predicting Time-Varying

Parameters with Parameter Driven and Observation-Driven Models, Review

of Economics and Statistics, 98(1), 97-110.

[29]Newey, W.K. and D. McFadden, 1994, Large Sample Estimation and

Hypothesis Testing, in R.F. Engle and D.L. McFadden (eds.) Handbook of

Econometrics,Vol. IV, Elsevier.

[30]Newey, W.K. and J.L. Powell, 1987, Asymmetric least squares

estimation and testing, Econometrica, 55(4), 819-847.

[31]Nolde, N. and J. F. Ziegel, 2017, Elicitability and backtesting:

Perspectives for banking regulation, Annals of Applied Statistics, forthcoming.

[32]Patton, A.J., 2011, Volatility Forecast Comparison using Imperfect

Volatility Proxies, Journal of Econometrics, 160(1), 246-256.

[33]Patton, A.J., 2016, Comparing Possibly Misspecified Forecasts,

working paper, Duke University.

[34]Patton, A.J. and K. Sheppard, 2009, Evaluating Volatility and

Correlation Forecasts, in T.G. Andersen, R.A. Davis, J.-P. Kreiss and T.

Mikosch (eds.) Handbook of Financial Time Series, Springer Verlag.

[35]Pötscher, B.M. and I.R. Prucha, 1989, A uniform law of large

numbers for dependent and heterogeneous data processes, Econometrica,

57, 675–683.

[36]Taylor, J.W., 2008, Estimating Value-at-Risk and Expected

Shortfall using Expectiles, Journal of Financial Econometrics, 231-252.

[37]Taylor, J.W., 2017, Forecasting Value at Risk and Expected

Shortfall using a Semiparametric Approach Based on the Asymmetric Laplace

Distribution, Journal of Business & Economic Statistics, forthcoming.

[38]Weiss, A.A., 1991, Estimating Nonlinear Dynamic Models Using Least

Absolute Error Estimation, Econometric Theory, 7(1), 46-68.

[39]White, H. 1994, Estimation, Inference and Specification

Analysis, Econometric Society Monographs No. 22, Cambridge University Press.

[40]Zhu, D. and J.W. Galbraith, 2011, Modeling and forecasting expected

shortfall with the generalized asymmetric Student- and asymmetric

exponential power distributions, Journal of Empirical Finance, 18, 765-778.

[41]Zwingmann T. and H. Holzmann, 2016, Asymptotics for Expected

Shortfall, working paper, available at arXiv:1611.07222.

Table 1: Simulation results for Normal innovations

True

0.900

0.050

-2.665

0.873

0.900

0.050

-2.665

0.873

Median

0.901

0.049

-2.615

0.882

0.899

0.049

-2.671

0.877

Avg bias

-0.017

0.015

-0.108

0.008

-0.011

0.006

-0.089

0.004

St dev

0.077

0.076

1.095

0.022

0.049

0.033

0.805

0.015

Coverage

0.868

0.827

0.875

0.919

0.884

0.876

0.888

0.937

True

0.900

0.050

-2.338

0.838

0.900

0.050

-2.338

0.838

Median

0.899

0.047

-2.329

0.842

0.897

0.048

-2.392

0.841

Avg bias

-0.017

0.007

-0.137

0.004

-0.011

0.002

-0.111

0.002

St dev

0.066

0.044

0.852

0.017

0.050

0.024

0.656

0.012

Coverage

0.898

0.870

0.911

0.931

0.912

0.888

0.925

0.923

True

0.900

0.050

-2.063

0.797

0.900

0.050

-2.063

0.797

Median

0.901

0.048

-2.051

0.800

0.899

0.049

-2.094

0.799

Avg bias

-0.013

0.005

-0.097

0.002

-0.008

0.002

-0.081

0.001

St dev

0.062

0.046

0.707

0.015

0.041

0.021

0.511

0.010

Coverage

0.913

0.874

0.916

0.947

0.923

0.907

0.927

0.948

True

0.900

0.050

-1.755

0.730

0.900

0.050

-1.755

0.730

Median

0.900

0.048

-1.769

0.730

0.898

0.048

-1.778

0.730

Avg bias

-0.015

0.006

-0.103

0.000

-0.009

0.001

-0.072

0.000

St dev

0.065

0.052

0.623

0.013

0.040

0.020

0.435

0.009

Coverage

0.917

0.883

0.925

0.954

0.922

0.902

0.934

0.960

True

0.900

0.050

-1.400

0.601

0.900

0.050

-1.400

0.601

Median

0.898

0.048

-1.391

0.602

0.899

0.048

-1.417

0.602

Avg bias

-0.017

0.008

-0.091

0.000

-0.010

0.002

-0.064

0.000

St dev

0.078

0.072

0.547

0.014

0.044

0.022

0.374

0.010

Coverage

0.925

0.881

0.934

0.948

0.941

0.923

0.945

0.954

Notes: This table presents results from 1000 replications of the

estimation of VaR and ES from a GARCH(1,1) DGP with standard Normal

innovations. Details are described in Section 4. The top row

of each panel presents the true values of the parameters. The second, third,

and fourth rows present the median estimated parameters, the average bias, and

the standard deviation (across simulations) of the estimated parameters. The

last row of each panel presents the coverage rates for 95% confidence

intervals constructed using estimated standard errors.

Table 2: Simulation results for skew innovations

True

0.900

0.050

-4.506

0.730

0.900

0.050

-4.506

0.730

Median

0.893

0.049

-4.376

0.750

0.895

0.048

-4.562

0.741

Avg bias

-0.047

0.038

-0.399

0.018

-0.028

0.014

-0.340

0.009

St dev

0.150

0.134

2.687

0.048

0.094

0.065

1.983

0.034

Coverage

0.797

0.797

0.809

0.894

0.837

0.853

0.839

0.936

True

0.900

0.050

-3.465

0.695

0.900

0.050

-3.465

0.695

Median

0.895

0.047

-3.448

0.705

0.896

0.048

-3.520

0.701

Avg bias

-0.028

0.014

-0.254

0.008

-0.017

0.005

-0.198

0.004

St dev

0.101

0.069

1.591

0.034

0.068

0.033

1.192

0.023

Coverage

0.855

0.835

0.877

0.921

0.874

0.893

0.887

0.939

True

0.900

0.050

-2.767

0.651

0.900

0.050

-2.767

0.651

Median

0.896

0.048

-2.760

0.656

0.898

0.048

-2.795

0.654

Avg bias

-0.021

0.007

-0.187

0.005

-0.011

0.003

-0.114

0.003

St dev

0.081

0.049

1.085

0.025

0.053

0.025

0.782

0.017

Coverage

0.906

0.883

0.921

0.937

0.916

0.904

0.922

0.951

True

0.900

0.050

-2.122

0.577

0.900

0.050

-2.122

0.577

Median

0.897

0.048

-2.121

0.579

0.898

0.048

-2.140

0.578

Avg bias

-0.017

0.006

-0.125

0.003

-0.008

0.002

-0.069

0.002

St dev

0.066

0.045

0.745

0.020

0.040

0.022

0.510

0.014

Coverage

0.931

0.900

0.937

0.949

0.926

0.925

0.927

0.947

True

0.900

0.050

-1.514

0.431

0.900

0.050

-1.514

0.431

Median

0.899

0.050

-1.485

0.432

0.899

0.049

-1.503

0.432

Avg bias

-0.019

0.006

-0.089

0.001

-0.008

0.002

-0.049

0.001

St dev

0.089

0.047

0.618

0.018

0.042

0.022

0.380

0.012

Coverage

0.916

0.888

0.922

0.938

0.929

0.916

0.940

0.944

Notes: This table presents results from 1000 replications of the

estimation of VaR and ES from a GARCH(1,1) DGP with skew innovations.

Details are described in Section 4. The top row of each panel

presents the true values of the parameters. The second, third, and fourth rows

present the median estimated parameters, the average bias, and the standard

deviation (across simulations) of the estimated parameters. The last row of

each panel presents the coverage rates for 95% confidence intervals

constructed using estimated standard errors.

Table 3: Sampling variation of FZ estimation

relative to (Q)MLE and CAViaR

Normal innovations

Skew t innovations

Panel A: FZ/(Q)ML

0.01

1.209

5.940

1.701

3.731

1.577

4.830

2.533

3.723

0.025

1.034

3.394

1.764

2.694

1.055

2.485

1.853

1.905

0.05

0.980

3.576

1.431

2.377

0.850

1.784

1.426

1.458

0.10

1.021

4.074

1.406

2.302

0.698

1.627

1.095

1.250

0.20

1.224

5.558

1.543

2.497

0.939

1.710

1.145

1.242

Panel B: FZ/CAViaR

0.01

0.982

1.162

0.951

0.975

1.062

1.384

0.912

1.465

0.025

0.965

1.139

0.971

1.042

0.976

1.030

0.974

0.997

0.05

0.925

1.238

0.910

0.930

0.885

0.819

0.920

0.903

0.10

0.940

1.283

0.847

0.827

0.831

0.903

0.816

0.819

0.20

0.855

0.671

0.703

0.510

0.736

0.437

0.503

0.515

Notes: This table presents the ratio of cross-simulation standard

deviations of parameter estimates obtained by FZ loss minimization and (Q)MLE

(Panel A), and CAViaR (Panel B). We consider only the parameters that are

common to these three estimation methods, namely the GARCH(1,1) parameters

and Ratios greater than one indicate the FZ estimator is

more variable than the alternative estimation method; ratios less than one

indicate the opposite.