Fastest Convergence for Q-Learning

Abstract

The Zap Q-learning algorithm introduced in this paper is an improvement of Watkins’ original algorithm and recent competitors in several respects. It is a matrix-gain algorithm designed so that its asymptotic variance is optimal. Moreover, an ODE analysis suggests that the transient behavior is a close match to a deterministic Newton-Raphson implementation. This is made possible by a two time-scale update equation for the matrix gain sequence.

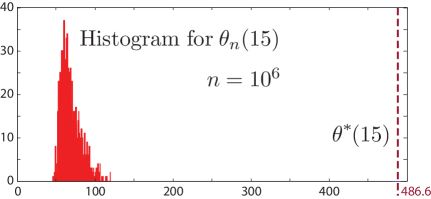

The analysis suggests that the approach will lead to stable and efficient computation even for non-ideal parameterized settings. Numerical experiments confirm the quick convergence, even in such non-ideal cases. The comparison plot on this first page, taken from Fig. 9 of this paper, is an illustration of the amazing acceleration in convergence using the new algorithm.

A secondary goal of this paper is tutorial. The first half of the paper contains a survey on reinforcement learning algorithms, with a focus on minimum variance algorithms.

Keywords: Reinforcement learning, Q-learning, Stochastic optimal control

2000 AMS Subject Classification: 93E20, 93E35

![[Uncaptioned image]](/html/1707.03770/assets/x1.png)

1 Introduction

It is recognized that algorithms for reinforcement learning such as TD- and Q-learning can be slow to converge. The poor performance of Watkins’ Q-learning algorithm was first quantified in [31], and since then many papers have appeared with proposed improvements, such as [10, 1].

An emphasis in much of the literature is computation of finite-time PAC (probably almost correct) bounds as a metric for performance. Explicit bounds were obtained in [31] for Watkins’ algorithm, and in [1] for the “speedy” Q-learning algorithm that was introduced by these authors. A general theory is presented in [21] for stochastic approximation algorithms.

In each of the models considered in prior work, the update equation for the parameter estimates can be expressed

| (1) |

in which is a positive gain sequence, and is a martingale difference sequence. This representation is critical in analysis, but unfortunately is not typical in reinforcement learning applications outside of these versions of Q-learning. For Markovian models, the usual transformation used to obtain a representation similar to (1) results in an error sequence that is the sum of a martingale difference sequence and a telescoping sequence [16]. It is the telescoping sequence that prevents easy analysis of Markovian models.

This gap in the research literature carries over to the general theory of Markov chains. Examples of concentration bounds for i.i.d. sequences or martingale-difference sequences include the finite-time bounds of Hoeffding and Bennett. Extensions to Markovian models either offer very crude bounds [19], or restrictive assumptions [15, 11]; this remains an active area of research [23].

In contrast, asymptotic theory for stochastic approximation (as well as general state space Markov chains) is mature. Large Deviations or Central Limit Theorem (CLT) limits hold under very general assumptions [3, 14, 5].

The CLT will be a guide to algorithm design in the present paper. For a typical stochastic approximation algorithm, this takes the following form: denoting to be the error sequence, under general conditions the scaled sequence converges in distribution to a Gaussian distribution, . Typically, the scaled covariance is also convergent:

| (2) |

The limit is known as the asymptotic covariance.

An asymptotic bound such as (2) may not be satisfying for practitioners of stochastic optimization or reinforcement learning, given the success of finite- performance bounds in prior research. There are however good reasons to apply this asymptotic theory in algorithm design:

-

(i)

The asymptotic covariance has a simple representation as the solution to a Lyapunov equation. It is easily improved or optimized by design.

-

(ii)

As shown in examples in this paper, the asymptotic covariance is often a good predictor of finite-time performance, since the CLT approximation is accurate for reasonable values of .

Two approaches are known for optimizing the asymptotic covariance. First is the remarkable averaging technique of Polyak and Juditsky [24, 25] and Ruppert [27] ([12] provides an accessible treatment in a simplified setting). Second is what we will call Stochastic Newton-Raphson, based on a special choice of matrix gain for the algorithm. The second approach underlies the analysis of the averaging approach.

We are not aware of theory that distinguishes the performance of Polyak-Ruppert averaging as compared to the Stochastic Newton-Raphson method. It is noted in [21] that the averaging approach often leads to very large transients, so that the algorithm should be modified (such as through projection of parameter updates). This may explain why averaging is not very popular in practice. In our own numerical experiments it is observed that the rate of convergence of CLT in this case is slow when compared to matrix gain methods.

In addition to accelerating the convergence rate of standard algorithms for reinforcement learning, it is hoped that this paper will lead to entirely new algorithms. In particular, there is little theory to support Q-learning in non-ideal settings in which the optimal “-function” does not lie in the parameterized function class. Convergence results have been obtained for a class of optimal stopping problems [37], and for deterministic models [17]. There is now intense practical interest, despite an incomplete theory. A stronger supporting theory will surely lead to more efficient algorithms.

Contributions

A new class of algorithms is proposed, designed to more accurately mimic the classical Newton-Raphson algorithm. It is based on a two time-scale stochastic approximation algorithm, constructed so that the matrix gain tracks the gain that would be used in a deterministic Newton-Raphson method.

The application of this approach to reinforcement learning results in the new Zap Q-learning algorithms. A full analysis is presented for the special case of a complete parameterization (similar to the setting of Watkins’ original algorithm). It is found that the associated ODE has a remarkable and simple representation, which implies consistency under suitable assumptions. Extensions to non-ideal parameterized settings are also proposed, and numerical experiments show dramatic variance reductions. Moreover, results obtained from finite- experiments show close solidarity with asymptotic theory.

The potential complexity introduced by the matrix gain is not of great concern in many cases, because of the dramatically acceleration in the rate of convergence. Moreover, the main contribution of this paper is not a single algorithm but a class of algorithms, wherein the computational complexity can be dealt with separately. For example, in a parameterized setting, the basis functions can be intelligently pruned via random projection [2].

The remainder of the paper is organized as follows. Background on computing and optimizing the asymptotic covariance is contained in Section 2. Application to Q-learning, and theory surrounding the new Zap Q-learning algorithm is developed in Section 3. Numerical results are surveyed in Section 4, and conclusions are contained in Section 5. The proofs of the main results are contained in the Appendix; the final page contains Table 2 containing a list of notation.

2 Stochastic Newton Raphson and TD-Learning

This first section is largely a tutorial on reinforcement learning. It is shown that the LSTD() learning algorithm of [8, 7, 22] is an instance of the “SNR algorithm”, in which there is only one time-scale for the parameter and matrix-gain updates. The original motivation for the LSTD() algorithm had no connection with asymptotic variance. It was shown later in [13] that the LSTD () algorithm is the minimum asymptotic variance version of the TD () algorithm of [30].

The focus is on fixed point equations associated with an uncontrolled Markov chain, denoted , on a measurable state space . It is assumed to be -irreducible and aperiodic [20]. In Section 3 we specialize to a finite state space.

In control applications and analysis of learning algorithms, it is necessary to construct a Markov chain , of which is a component. Other components may be an input process, or a sequence of “eligibility vectors” that arise in TD-learning. It will be assumed throughout that there is a unique stationary realization of , with unique marginal distribution denoted .

2.1 Motivation from SA & ODE fundamentals

The goal of stochastic approximation is to compute the solution for a function . If the function is easily evaluated, then successive approximation can be used, and under stronger conditions the Newton-Raphson algorithm:

| (3) |

Under general conditions the convergence rate of (3) is quadratic (much faster than geometric), which is not generally true of successive approximation.

Stochastic approximation is itself an approximation of successive approximation. It is assumed that , where and is a random variable with distribution . The standard stochastic approximation algorithm is defined by

| (4) |

For simplicity it is assumed that is the stationary realization of the Markov chain. It is always assumed that the scalar gain sequence is non-negative, and satisfies:

| (5) |

While convergent under general conditions, the rate of convergence of (4) can often be improved dramatically through the introduction of a matrix gain. This is explained first in a simple linear setting.

2.2 Optimal covariance for linear stochastic approximation

In many applications of reinforcement learning we arrive at a linear recursion of the form

| (6) |

where is a matrix and is a vector, . Let denote the respective steady-state means:

| (7) |

It is assumed throughout this section that is Hurwitz: the real part of each eigenvalue is negative. Under this assumption, and subject to mild conditions on , it is known that converges with probability one to [3, 14, 5].

Convergence of the recursion (6) will be assumed henceforth. It is also assumed that the gain sequence is given by , .

Under general conditions, the asymptotic covariance defined in (2) is the non-negative semi-definite solution to the Lyapunov equation:

| (8) |

A solution is guaranteed only if each eigenvalue of has real part that is strictly less than . If there exists an eigenvalue which does not satisfy this property, then under general conditions the asymptotic covariance is infinity (see Thm. 2.1). Hence the Hurwitz assumption must be strengthened to ensure that the asymptotic covariance is finite.

The matrix is obtained as follows: based on (6), the error sequence evolves according to a deterministic linear system driven by “noise”:

in which is the sum of three terms:

| (9) |

with , . The third term vanishes with probability one. The “noise covariance matrix” has the following two equivalent forms:

| (10) |

in which , and

where the expectation is in steady-state. It is assumed that the CLT holds for sample-averages of the noise sequence:

| (11) |

where the limit is in distribution. This is a mild requirement when is Markovian [20].

A finite asymptotic covariance can be guaranteed by increasing the gain: choose in (6), with sufficiently large so that the eigenvalues of satisfy the required bound. More generally, a matrix gain can be introduced:

| (12) |

in which is a matrix. Provided the matrix satisfies the eigenvalue bound, the corresponding asymptotic covariance is finite and solves a modified Lyapunov equation:

| (13) |

The choice is analogous to the gain used in the Newton-Raphson algorithm (3). With this choice, the asymptotic covariance is finite and given by

| (14) |

It is a remarkable fact that this choice is optimal in the strongest possible statistical sense: For any other gain , the two asymptotic covariance matrices satisfy

That is, the difference is positive semi-definite [3, 14, 5].

The following theorem summarizes the results on the asymptotic covariance for the matrix-gain recursion (12). The proof is contained in Section A.1 of the Appendix.

Theorem 2.1.

Suppose that the eigenvalues of lie in the strict left half plane, and that the noise sequence satisfies the CLT (11) with finite covariance . Then, the stochastic approximation recursion defined in (12) is convergent, and the following also hold:

-

(i)

Suppose that is an eigenvalue-eigenvector pair satisfying

, , and , where denotes the conjugate transpose of the vector . Then

and consequently, the asymptotic covariance is not finite.

-

(ii)

If all the eigenvalues of satisfy , then the corresponding asymptotic covariance is finite, and can be obtained as the solution to the Lyapunov equation (13)

-

(iii)

For any matrix gain the asymptotic covariance admits the lower bound

This lower bound is achieved using .

Thm. 2.1 inspires improved algorithms in many settings. The first, which is essentially known, e.g. [27, 14, p. 331], will be called stochastic Newton-Raphson (SNR).

Stochastic Newton-Raphson

This algorithm is obtained by estimating the mean simultaneously with the estimation of : recursively define

| (15) | ||||

where and are initial conditions.

If the steady-state mean (defined in (7)) is invertible, then is invertible for all sufficiently large.

The sequence admits a simple recursive representation that implies the following alternative representation of the SNR parameter estimates:

Proposition 2.2.

Suppose is invertible for each . Then, the sequence of estimates obtained using (15) are identical to the direct estimates:

Based on the proposition, it is obvious that the SNR algorithm is consistent whenever the Law of Large Numbers holds for the sequence . Under the assumptions of Thm. 2.1, the resulting asymptotic covariance is identical to what would be obtained with the constant matrix gain .

Algorithm design in this linear setting is simplified in part because is an affine function of , so that the gain appearing in the standard Newton-Raphson algorithm (3) does not depend upon the parameter estimates . However, an ODE analysis of the SNR algorithm suggests that even in this linear setting, the dynamics are very different from its deterministic counterpart:

| (16) | ||||

While evidently converges to exponentially fast in the linear model, with a poor initial condition we might expect poor transient behavior.

In extending the SNR algorithm to a nonlinear stochastic approximation algorithm, an ODE approximation of the form (16) will be possible under general conditions, but the matrix will depend on . In addition to poor transient behavior, the coupled equations may be difficult to analyze. And, just as in the linear model, the continuous time system looks very different from the deterministic Newton-Raphson recursion (3).

The next class of algorithms are designed so that the associated ODE more closely matches the deterministic recursion.

2.3 Zap Stochastic Newton-Raphson

This is a two time-scales algorithm with a higher step-size for the matrix recursion. In the linear setting of this section, it is defined by the variant of (15):

| (17) | ||||

It is different from the original Stochastic Newton-Raphson algorithm because of the two time-scale construction: The second step-size sequence is non-negative, satisfies (5), and also

| (18) |

We again take , .

The asymptotic covariance is again optimal. The ODE associated with the sequence is far simpler, and exactly matches the usual Newton-Raphson dynamics:

| (19) |

This simplicity is also revealed in application to Q-learning, in which depends on the parameter.

A key point to note here is that the Zap version of the SNR algorithm plays a significant role in analysis as well as in performance improvement of general non-linear function approximation problems. We briefly discuss these in the following.

2.3.1 Zap SNR for non-linear stochastic approximation

Consider a stochastic approximation algorithm of the form (4) with , a non-linear function of the parameter vector . The ODE of the two algorithms: SNR and Zap-SNR look significantly different in this case; it is found that this difference is reflected in the rate of convergence of the stochastic recursion (as we will see in the case of Q-learning). The SNR algorithm is essentially the same as (15):

| (20) | ||||

Note that the function may or may not be readily accessible, and this is application specific. In the case of Q-learning with linear function approximation, though the function is iteslf non-linear in , is readily computable.

The Zap-SNR algorithm is a generalization of (17):

| (22) | ||||

where once again the step-size sequence satisfies (5), and (18). Similar to (19), the ODE of this algorithm is identical to the deterministic Newton-Raphson dynamics:

| (23) |

The general convergence and stability analysis of both (20) and (22) is open. In Section 3 we show that when applied to Q-learning, the algorithms do converge under certain technical conditions. However, the assumptions under which the single time-scale algorithm (20) converges is far more restrictive than the assumptions under which the the two-time-scale algorithm (22) converges.

2.3.2 Dealing with complexity: An () Zap-SNR algorithm

It is common to discard the idea of second order methods because of their computational complexity. Before we move on to the specific applications in Reinforcement Learning, we propose an enhancement of the SNR algorithms that will result in complexity that is comparable to first order methods.

We believe that we have convinced the readers that the two-timescale Zap-SNR algorithm (22) is of more interest to us (we will make this more precise in Section 3), and hence restrict to extensions of this algorithm here.

It is assumed that there is no complexity in “calculating” the gradient function , and that it is readily available. This is not be true in all applications, but holds in the applications of interest in this paper. Under these assumptions, computational complexity arises from the operations that are performed in manipulating these quantities.

The per-iteration complexity of the first order algorithm (1) is , since . If the algorithm is run for iterations (assuming we have a data sequence of length ), the total complexity is . The per iteration complexity in the case of the Zap-SNR algorithm (22) is , because it involves the product of a matrix inverse (of dimension ) and a vector (of dimension ). The total complexity of the algorithm after running for iterations is .

The essential idea behind the Zap-SNR algorithm is to perform the complexity steps only once every iterations, so that the total computational complexity for a data sequence of length is ; essentially resulting in the complexity of the first order method if . This is done by “batching” the data sequence into mini-sequences of length , and applying recursions (22) for each batch as follows: For

| (24) | ||||

where,

| (25) | ||||

The first two definitions in (25) are straightforward; the expression for is obtained in such a way that the recursions in (24) very closely resemble the recursions in (22)111This deserves more explanation and we plan to provide one in a future version of the paper..

A remarkable (but almost obvious) property of the Zap-SNR algorithm (24) is that it has the same asymptotic properties (specifically, the asymptotic covariance) as that of the original Zap-SNR algorithm (22). This once again is made more precise in a future version of the paper. The specific application of this algorithm to Q-learning is discussed in Section 3.7.

2.4 Application to temporal-difference algorithms

The general theory is illustrated here, through application to TD()-learning algorithms.

Let denote the transition semigroup for the Markov chain : For each , , and ,

The standard operator-theoretic notation is used for conditional expectation: for any measurable function ,

In a finite state space setting, is the -step transition probability matrix of the Markov chain, and the conditional expectation appears as matrix-vector multiplication:

Let denote a cost function, and a discount factor. The discounted-cost value function is defined as , which is the unique solution to the Bellman equation

| (26) |

TD-learning algorithms are designed to obtain approximations of within a finite-dimensional parameterized class.

Consider the case of a -dimensional linear parameterization. A function is chosen, which is viewed as a collection of basis functions. Each vector is associated with the approximate value function . There are two standard criteria for defining optimality of the parameter. Most natural is the minimum norm approach:

| (27) |

in which the choice of norm is part of the design of the algorithm. Most common is

| (28) |

where the expectation is in steady-state.

In the Galerkin approach, a -dimensional stationary stochastic process is constructed that is adapted to a stationary realization of . An algorithm is designed to obtain the vector that satisfies

| (29) |

in which the expectation is again in steady state. The -dimensional stochastic process is called the sequence of eligibility vectors.

The motivation for the first criterion (27) is clear, but algorithms that solve this problem often suffer from high variance. The Galerkin approach is used because it is simple and generally applicable. Also, if the basis functions are chosen such that for some , and if the solution to (29) is unique, then the Galerkin approach will yield the exact solution .

The goal of the TD() learning algorithm is to solve the Galerkin relaxation (29) in which the eligibility vectors are obtained by passing through the corresponding first-order low-pass filter: , . It is always assumed that . It is shown in [33] that the solutions to the Galerkin fixed point equation (29) and the minimum norm problem (27) coincide if , with the norm defined by (28).

TD() algorithm:

For initialization , the sequence of estimates are defined recursively:

| (30) | ||||

The recursion (30) can be placed in the form (6) in which , and

| (31) |

Based on this representation, it can be shown that the TD() algorithm is consistent provided the basis vectors are linearly independent, in the sense that .

It is also easy to construct an example for which the asymptotic covariance is infinite: Take any consistent example, and scale the basis vectors by a small constant . Using the basis , the resulting matrix is scaled by . Hence, for sufficiently small , each eigenvalue of will have real part that is strictly greater than .

An application of the SNR matrix gain algorithm (15) results in an algorithm with optimal asymptotic covariance. This results in the coupled recursions:

| (32) | |||

| (33) |

where , for .

The following proposition follows directly from Prop. 2.2:

Proposition 2.3.

3 Q-Learning

The class of algorithms considered next is designed for a controlled Markov model, whose input process is denoted . It is assumed that the state space and the action space on which evolves are both finite. Denote and .

3.1 Notation and assumptions

It is convenient to maintain the operator-theoretic notation used in the uncontrolled setting. There is now a controlled transition matrix that acts on functions via

For any non-anticipative input sequence we have on the event and .

There is a finite number of deterministic stationary policies that are enumerated as , with . A randomized stationary policy is defined by a pmf on the integers and such that for each ,

| (35) |

where is an i.i.d. sequence on satisfying , and for all and .

For any deterministic stationary policy , let denote the substitution operator, defined for any function by . If the policy is randomized, of the form (35), then we denote

With viewed as a single matrix with rows and columns, and viewed as a matrix with rows and columns, the following interpretations hold:

Lemma 3.1.

Suppose that is defined using a stationary policy (possibly randomized). Then, both and the pair process are Markovian, and

-

(i)

is the transition matrix for .

-

(ii)

is the transition matrix for .

A cost function is given together with a discount factor . For any (possibly randomized) stationary policy , the resulting value function is denoted

| (36) |

The minimal value function is denoted , which is the unique solution to the discounted-cost optimality equation (DCOE):

| (37) |

The minimizer defines a stationary policy that is optimal over all input sequences [4].

The associated “Q-function” is defined to be the term within the brackets, . The DCOE implies a similar fixed point equation for the Q-function:

| (38) |

in which for any function .

For any function , let denote an associated policy satisfying

| (39) |

for each . It is assumed to be specified uniquely as follows:

| (40) |

The fixed point equation (38) becomes

| (41) |

In the analysis that follows it is necessary to consider the Q-function associated with all possible cost functions simultaneously: given any function , let denote the corresponding solution to the fixed point equation (38), with replaced by . That is, the function is the solution to the fixed point equation,

| (42) |

For a pmf defined on the set of policy indices , denote

| (43) |

so that is the “-function” obtained with the cost function , and the randomized stationary policy defined by (see also discussion of the SARSA algorithm following the proof of Lemma 3.6). It follows that the functional can be expressed as the minimum over all pmfs :

| (44) |

There is a single degenerate pmf that attains the minimum for each (the optimal stationary policy is deterministic) [4].

Lemma 3.2.

The mapping is a bijection on the set of real-valued functions on . It is also piecewise linear, concave and monotone.

Proof.

A Galerkin approach to approximating is formulated as follows: Consider a linear parameterization , with and , and denote . Obtain a -dimensional stationary stochastic process that is adapted to , and define to be a solution to

| (45) |

where the expectation is in steady-state.

Similar to TD()-learning, a possible approach to estimate is the following:

Q() algorithm:

3.2 Watkins algorithm

The basic Q-learning algorithm of [36, 35] is a particular instance of the Galerkin approach with in (46). The basis functions are taken to be indicator functions:

| (47) |

where is an enumeration of all state-input pairs. The goal of this approach is to compute the function exactly.

The parameter is identified with the estimate , and hence with . The basic stochastic approximation algorithm to solve (45) coincides with Watkins algorithm:

| (48) |

Only one entry of the approximation is updated at each time point, corresponding to the previous state-input pair observed.

Assumption Q1: The input is defined by a randomized stationary policy of the form (35). The joint process is an irreducible Markov chain. That is, it has a unique invariant pmf satisfying for each .

Assumption Q2: The optimal policy is unique.

The ODE for stability analysis takes on the following simple form:

| (49) |

in which as defined below (38). This ODE is stable under Assumption Q1, which then implies that the parameter estimates converge to a.s. [6].

Under Assumption Q2 there exists such that

This justifies a linearization of the ODE (49), in which is replaced by .

Although the algorithm is consistent, it should be clear that the asymptotic covariance of this algorithm is typically infinite.

Theorem 3.3.

Suppose that Assumptions Q1 and Q2 hold. Then, the sequence of parameters obtained using the Q-learning algorithm (48) converges to a.s.. Suppose moreover that the conditional variance of is positive:

| (50) |

and . Then, in the case ,

The assumption is satisfied whenever .

The proof of convergence can be found in [36, 35]. The proof of infinite asymptotic covariance is given in Section A.2 of the Appendix. An eigenvector for is constructed with strictly positive entries, and with real eigenvalue satisfying . Interpreted as a function , this eigenvector satisfies

| (51) |

Assumption (50) ensures that the right hand side is strictly positive, as required in Thm. 2.1 (i).

3.3 SNR and Zap Q-Learning

For a sequence of matrices and , the matrix-gain Q() algorithm is described as follows:

-Q() algorithm:

For initialization , the sequence of estimates are defined recursively:

| (52) | ||||

The special case based on stochastic Newton-Raphson (17) is called the Zap-Q() algorithm:

It is assumed that a projection is employed to ensure that is a bounded sequence — this is most easily achieved using the Matrix Inversion Lemma.

The analysis that follows is specialized to and the basis (47) that is used in Watkins’ algorithm. The resulting Zap-Q algorithm is defined as follows, after identifying and :

| (53) | |||

| (54) |

where , and denotes a projection, chosen so that is a bounded sequence. In Thm. 3.4 it is established that the projection is required only for a finite number of iterations: is a bounded sequence, where a.s..

An equivalent representation for the parameter recursion (53) is

| (55) |

in which and are treated as -dimensional vectors rather than functions on , and

| (56) |

It would seem that the analysis is complicated by the fact that the sequence depends upon through the policy sequence . Part of the analysis is simplified by obtaining a recursion for the following -dimensional sequence:

| (57) |

where is the diagonal matrix with entries . This admits a very simple recursion in the special case . In the other case considered, wherein the step-size sequence satisfies (18), the recursion for is more complex, but the ODE analysis is simplified.

3.4 Main results

Conditions for convergence of the Zap-Q algorithm (53,54) are summarized in Thm. 3.4. The following assumption is used to address the discontinuity in the recursion for resulting from the dependence of on .

Assumption Q3: The sequence of policies satisfies:

| (58) |

Theorem 3.4.

Suppose that Assumptions Q1–Q3 hold, with the gain sequences and satisfying

| (59) |

for some fixed . Then,

- (i)

-

(ii)

The asymptotic covariance (2) is minimized over all -Q() matrix gain versions of Watkins’ Q-learning algorithm.

-

(iii)

An ODE approximation holds for the sequence , by continuous functions satisfying

(60) This ODE approximation is exponentially asymptotically stable, with .

See Section 3.6.2 and standard references such as [5] for the precise meaning of the ODE approximation (60).

Proof of Thm. 3.4.

Boundedness of the sequences and is established in Lemmas A.3 and A.6, where a.s.. The ODE approximation is established in Prop. A.7. These two results combined with standard arguments establishes (i) [5].

Result (ii) follows from convergence of the algorithm, just as in the case of TD-learning. Uniqueness of the optimal policy is needed so that the recursion for admits a linearization around .

In the case , the three consequences hold under a stronger assumption than Q3:

Proposition 3.5.

The convergence assumption in Prop. 3.5 is far stronger than Q3: Recall that the policies evolve in a finite set . Convergence means that for some integer-valued random variable , and all sufficiently large.

The proof of Prop. 3.5 is based on a simple inverse dynamic programming argument: it is easily shown that is convergent to in the case , and it is also easily established that in this case. The proof of Thm. 3.4 is more delicate, and is based on extensions of ODE arguments in [6].

The simplicity of the proof of Prop. 3.5 suggests that this case would be preferred. However, when we do not know how to relax the assumption that is convergent. Analysis is complicated by the fact that is obtained as a uniform average of .

3.5 ODE and Policy Iteration

Recall the definition of in (43). The ODE approximation (60) can be expressed

| (61) |

where is any pmf satisfying , and the derivative exists for a.e. (see Lemma A.10 for full justification). This has an interesting geometric interpretation. Without loss of generality, assume that the cost function is non-negative, so that evolves in the positive orthant whenever its initial condition lies in this domain.

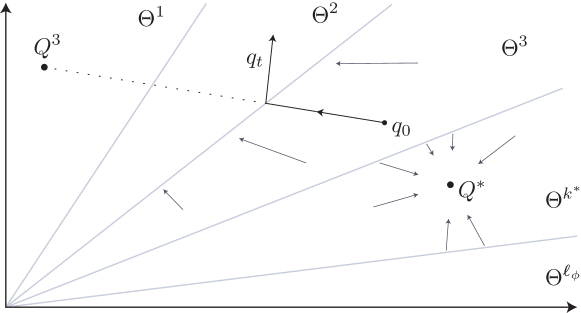

A typical solution to the ODE is shown in Fig. 1: the trajectory is piecewise linear, with changes in direction corresponding to changes in the policy . Each set shown in the figure corresponds to a deterministic policy:

Lemma 3.6.

For each the set is a convex polyhedron, and also a positive cone. When then

Proof.

The power series expansion holds:

For each we have , which together with (36) implies the desired result.

The function is the fixed-policy Q-function considered in the SARSA algorithm [18, 26, 32]. While evolves in the interior of the set , it moves in a straight line towards the function . On reaching the boundary, it then moves in a straight line to the next Q-function. This is something like a policy iteration recursion, since the policy is obtained as the argmin over of .

Of course, it is far easier to establish stability of the equivalent ODE (60).

3.6 Overview of proofs

This final subsection is dedicated to the proof of Prop. 3.5, and the main ideas in the proof of Thm. 3.4. It is assumed throughout the remainder of this section that Assumptions Q1–Q3 hold. Proofs of technical lemmas are contained in Appendix A.3.

We require the usual probabilistic foundations: There is a probability space that supports all random variables under consideration. The probability measure may depend on an initialization of the Markov chain. All stochastic processes under consideration are assumed adapted to a filtration denoted .

We begin with the proof of the simpler Prop. 3.5.

3.6.1 Inverse Dynamic Programming Analysis

Proposition 3.7.

Suppose that Assumptions Q1–Q3 hold. Suppose moreover that each of the matrices is invertible for some that is a.s. finite. Then, the following recursion holds for :

| (62) | ||||

where is defined in (56).

Proof of Prop. 3.5.

The assumption that the sequence of policies converges to a (possibly random) limit has the following consequences: First, this implies that defined in (54) converges:

| (63) |

Second, for all sufficiently large the following identities hold, by applying the definitions of and :

| (64) |

From (63), since the limit on the right hand side is invertible and the set of all invertible matrices is open, it follows that there is an integer that is finite a.s., and such that is invertible for .

Now applying Prop. 3.7, the recursion (62) is reduced to the following in the case that :

This is essentially a Monte-Carlo average of . Since the steady state expectation of is equal to , convergence follows from the Law of Large Numbers:

| (65) |

Combining equations (63), (64), and (65) implies

Lemma 3.2 completes the proof: .

3.6.2 ODE Analysis

The remainder of this section is devoted to a high-level view of the proof of the ODE approximation for the two time-scale algorithm, with and defined in (59).

The construction of an approximating ODE involves first defining a continuous time process. Denote

| (66) |

and define for these values, with the definition extended to via linear interpolation. We say that the ODE approximation holds if we have the approximation,

where the error process satisfies, for each ,

Such approximations will be represented using the more compact notation:

| (67) |

An ODE approximation holds for Watkins algorithm, with defined by the right hand side of (49), or in more compact notation:

| (68) |

The significance of this representation is that is the Q-function associated with the “cost function” : .

The same notation will be used in the following treatment of Zap Q-learning. Along with the piecewise linear continuous-time process , denote by the piecewise linear continuous-time process defined similarly, with , , and for .

To construct an ODE, it is convenient first to obtain an alternative and suggestive representation for the pair of equations (53,54). A vector-valued sequence of random variables will be called ODE-friendly if it admits the decomposition,

| (69) |

in which is a martingale-difference sequence satisfying a.s. for some finite and all , is a bounded sequence, and the final sequence is bounded and satisfies

| (70) |

Lemma 3.8.

The assertion that are ODE-friendly follows from standard arguments based on solutions to Poisson’s equation for zero-mean functions of the Markov chain [29]. The proof of Lemma 3.9 is based on an extension of this technique to the present setting.

Lemma 3.9.

For each ,

where is a martingale difference sequence with uniformly bounded second moment, and the sequences are also bounded. If Assumption Q3 holds then satisfies (70).

The representation in Lemma 3.8 appears similar to an Euler approximation of the solution to an ODE:

It is discontinuity of the function that presents the most significant challenge in analysis of the algorithm — this violates standard conditions for existence and uniqueness of solutions to the ODE without disturbance.

Fortunately there is special structure that will allow the construction of an ODE approximation. Some of this structure is highlighted in the lemma that follows. These approximations are taken from Lemmas A.3 and A.6.

Lemma 3.10.

For each ,

| (72) | ||||

| (73) |

where when for some , and extended to all by linear interpolation.

The “gain” appearing in (73) converges to infinity rapidly as : Based on the definitions in (59), it follows from (66) that for large , and consequently for large . This suggests that the integrand should converge to zero rapidly with . This intuition is made precise in the Appendix. Through several subsequent transformations, these integral equations are shown to imply the ODE approximation in Thm. 3.4.

3.7 An Zap-Q learning algorithm

In this subsection, we introduce an Zap-Q learning algorithm, which is basically the Zap-SNR algorithm described in Section 2.3.2 specialized to Q-learning.

4 Numerical Results

Results from numerical experiments are surveyed here to illustrate the performance of the Zap Q-learning algorithm (53,54). Comparisons are made with several existing algorithms, including Watkins Q-learning (48), Watkins Q-learning with Ruppert-Polyak-Juditsky (RPJ) averaging [28, 24, 25], Watkins Q-learning with a “polynomial learning rate” [10], and the more recent Speedy Q-learning algorithm [1].

In addition, the Watkins algorithm with a scalar gain is considered, with chosen so that the algorithm has finite asymptotic covariance. When the value of is optimized and numerical conditions are favorable (e.g., the condition number of is not too large) it is found that the performance is nearly as good as the Zap-Q algorithm. However, there is no free lunch:

-

(i)

Design of the scalar gain depends on approximation of , and hence . While it is possible to estimate via Monte-Carlo in Zap Q-learning, it is not known how to efficiently update approximations for an optimal scalar gain.

-

(ii)

A reasonable asymptotic covariance required a large value of . Consequently, the scalar gain algorithm had massive transients, resulting in a poor performance in practice.

-

(iii)

Transient behavior could be tamed through projection to a bounded set. However, this again requires prior knowledge of the region in the parameter space to which belongs.

Projection of parameters was also necessary for RPJ averaging.

The following batch mean method was used to estimate the asymptotic covariance.

Batch Mean Method

At stage of the algorithm we will be interested in the distribution of a vector-valued random variable of the form , where is possibly dependent on . The batch mean method is used to estimate its statistics: For each algorithm, parallel simulations are run with initialized i.i.d. according to some distribution. Denoting to be the vector corresponding to the simulation, the distribution of the random variable is estimated based on the histogram of the independent samples .

An important special case in this paper is . However, since the limit is not available, the empirical mean is substituted:

| (76) |

The estimate of the covariance of is then obtained as the sample covariance of . This corresponds to the estimate of the asymptotic covariance defined in (2).

The value is used in all of the experiments surveyed here.

4.1 Finite state-action MDP

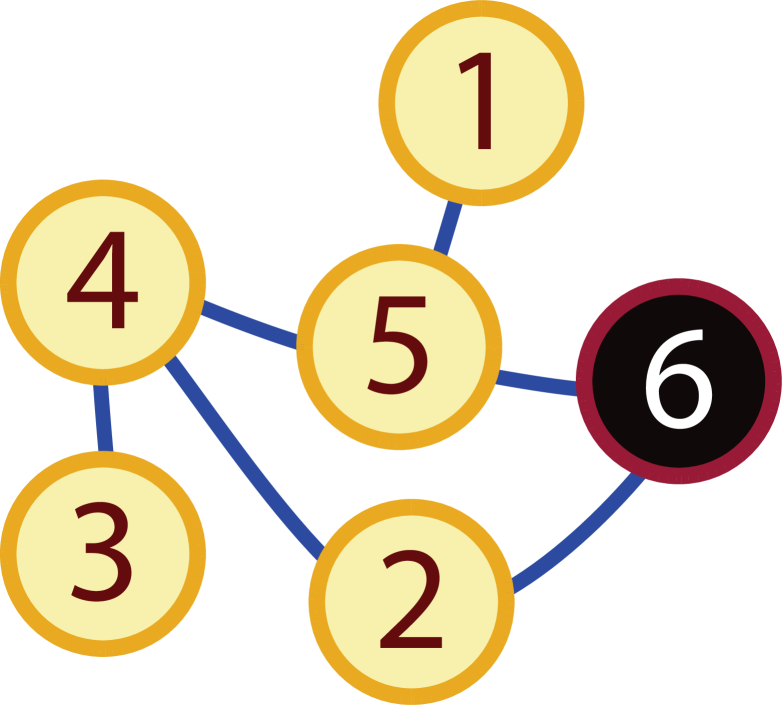

Consider first a simple stochastic-shortest-path problem. The state space coincides with the six nodes on the un-directed graph shown in Fig. 2. The action space , , consists of all feasible edges along which an agent can travel, including each “self-loop”, . The number of state-action pairs for this example coincides with the number of nodes plus twice the number of edges: .

The controlled transition matrix is defined as follows: If , and , then with probability , and with probability , the next state is randomly chosen between all neighboring nodes. The goal is to reach the state and maximize the time spent there. This is modeled through a discounted-reward optimality criterion with discount factor . The one-step reward is defined as follows:

The solution to the discounted-cost optimal control problem can be computed numerically for this model; the optimal policy is unique and independent of .

Six different variants of Q-learning were tested:

-

1.

Watkins’ algorithm with scalar gain , so that

-

2.

Watkins’ algorithm using RPJ averaging, with

-

3.

Watkins’ algorithm with the polynomial learning rate

-

4.

Speedy Q-learning

-

5.

Zap Q-learning with

-

6.

Zap Q-learning with

The basis was taken to be the same as in Watkins Q-learning algorithm. In each case, the randomized policy was taken to be uniform: feasible transitions were sampled uniformly at each time.

Discount factors and were considered. In each case, the unique optimal parameter was obtained numerically.

Asymptotic Covariance

Speedy Q-learning cannot be represented as a standard stochastic approximation, so standard theory cannot be applied to obtain its asymptotic covariance. The Watkins’ algorithm with polynomial learning rate has infinite asymptotic covariance.

For the other four algorithms, the asymptotic covariance was computed by solving the Lyapunov equation (13) based on the matrix gain that is particular to each algorithm. Recall that in the case of either of the Zap-Q algorithms.

The matrices and appearing in (13) are defined with respect to Watkins’ Q-learning algorithm with . The first matrix is under the standing assumption that the optimal policy is unique. The proof that this is a linearization comes first from the representation of the ODE approximation (49) in vector form:

| (77) |

Uniqueness of the optimal policy implies that is locally linear: there exists such that

The matrix was also obtained numerically, without resorting to simulation.

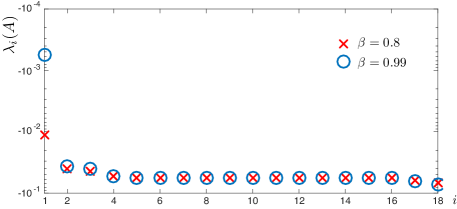

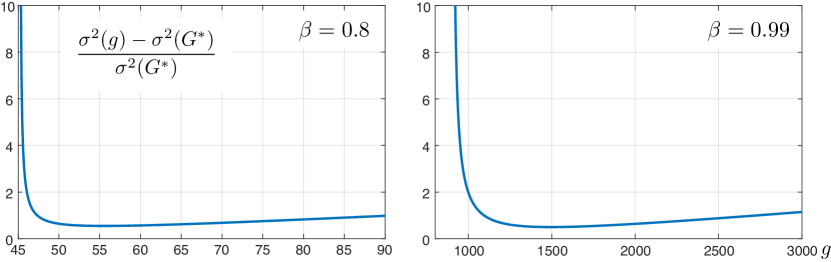

The eigenvalues of the matrix are real in this example, as shown in Fig. 3 for both values of . To ensure that the eigenvalues of are all strictly less than in a scalar gain algorithm requires the (approximate) lower bounds for , and for . Thm. 2.1 implies that the asymptotic covariance is finite for this range of in the Watkins algorithm with . Fig. 4 shows the normalized trace of the asymptotic covariance as a function of , and the significance of and .

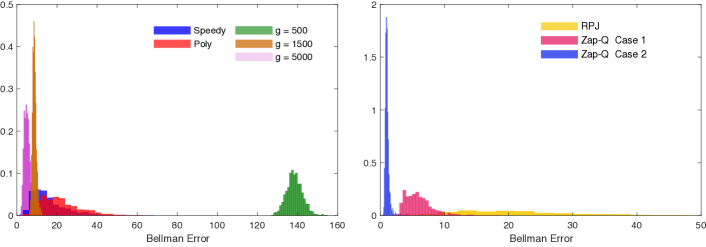

Based on this analysis or on Thm. 3.3, it follows that the asymptotic covariance is not finite for the standard Watkins’ algorithm with . In simulations it was found that the parameter estimates are not close to even after many millions of samples. This is illustrated for the case in Fig. 5, which shows a histogram of estimates of with (other entries showed similar behavior).

It was found that the algorithm performed very poorly in practice for any scalar gain algorithm. For example, more than half of the experiments using and resulted in values of exceeding by (with ), even with . The algorithm performed well with the introduction of projection in the case . With , the performance was unacceptable for any scalar gain, even with projection.

The results presented next used a gain of in the case , and projection of each entry of the estimates to the interval . Fig. 6 shows normalized histograms of , as defined in (76), with .

The Central Limit Theorem holds: is expected to be approximately normally distributed: , when is large. Of the entries of the vector , with , it was found that the asymptotic variance matched the histogram nearly perfectly for , while showed the worst fit.

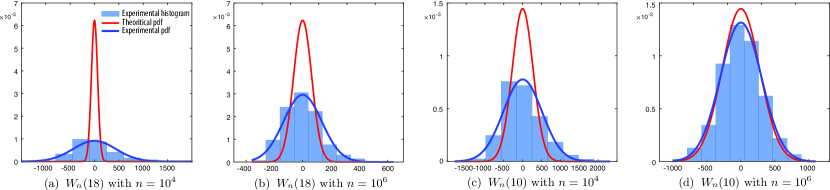

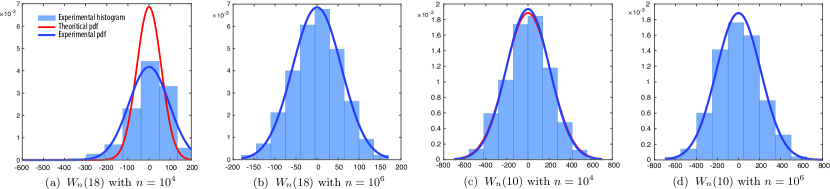

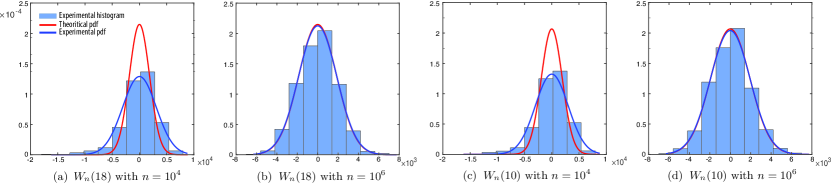

These experiments were repeated for each of the Zap-Q algorithms, for which the asymptotic variance is obtained using the formula (14). Plots are shown only for Case 2: the two time-scale algorithm, with . Histograms in the case of are shown in Fig. 7, and Fig. 8 for . The covariance estimates and the Gaussian approximations match the theoretical predictions remarkably well for .

Bellman Error

The Bellman error at iteration is denoted:

This is identically zero if and only if . If converges to then for all sufficiently large , and the CLT holds for whenever it holds for . Moreover, on denoting the maximal error

| (78) |

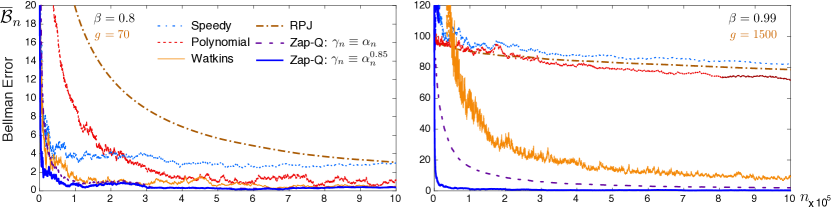

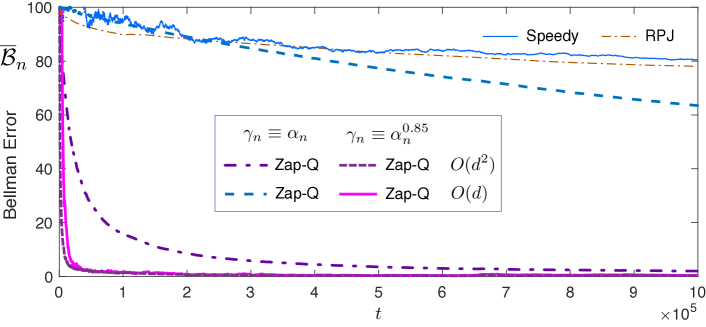

the sequence also converges in distribution as . Fig. 9 contains plots of for the six different Q-learning algorithms.

For large , the two versions of Zap Q-learning exhibit similar behavior since converges to in both algorithms. Though all six algorithms perform reasonably well when , Zap Q-learning is the only one that achieves near zero Bellman error within iterations in the case . Moreover, the performance of the two time-scale algorithm is clearly superior to the one time-scale algorithm.

Fig. 9 shows only the typical behavior — repeated trails were run to investigate the range of possible outcomes. For each algorithm, the outcomes of independent simulations resulted in samples , with uniformly distributed on the interval for and for .

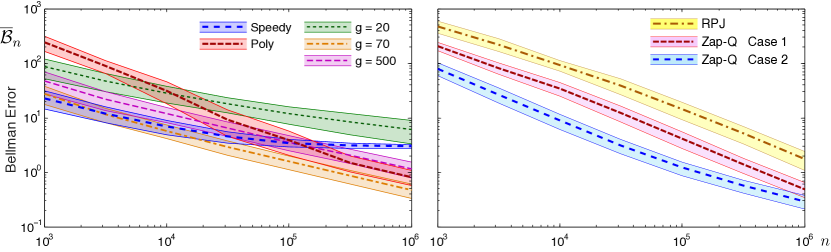

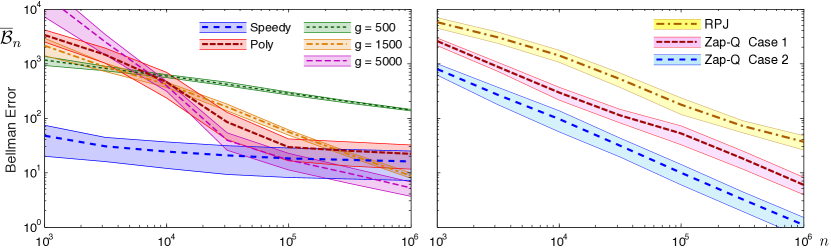

The batch means method was used to obtain estimates of the mean and variance of for a range of values of . Plots of the mean and confidence intervals are shown in Fig. 10 for the case , and plots for are shown in Fig. 11.

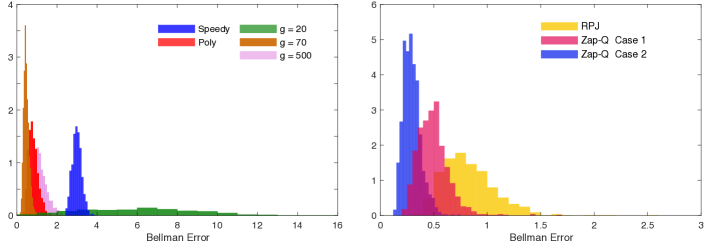

Fig. 12 and Fig. 13 shows histograms of , for all the six algorithms; this corresponds to the data shown in Fig. 10 and Fig. 11 at .

4.1.1 Performance of the Zap-Q learning algorithm

In this subsection, we test the performance of the Zap-Q learning algorithm that was defined in equations (74) and (75) of Section 3.7 by applying it to the stochastic shortest path problem. We restrict to the comparison of the Bellman errors (defined in (78)) of the different algorithms, and we consider the case .

Fig. 14 contains plots of for the different Q-learning algorithms. For the Zap-Q learning algorithms, the batch size was set to ( in this problem). We notice in the figure that the algorithm performs nearly as well as the algorithm when the step-sizes () are chosen appropriately. Furthermore, the naive batching technique applied to a single-time-scale Stochastic Newton-Raphson algorithm ( and therefore ) performs extremely poorly.

4.2 Finance model

The next example is taken from [34, 9]. The reader is referred to these references for complete details of the problem set-up and the reinforcement learning architecture used in this prior work. The example is of interest because it shows how the Zap Q-learning algorithm can be used with a more general basis, and also how the technique can be extended to optimal stopping time problems.

The Markovian state process considered in [34, 9] is the vector of ratios:

in which is a geometric Brownian motion (derived from an exogenous price-process). This uncontrolled Markov chain is positive Harris recurrent on the state space [20].

The “time to exercise” is modeled as a stopping time . The associated expected reward is defined as , with and fixed. The objective of finding a policy that maximizes the expected reward is modeled as an optimal stopping time problem.

The value function is defined to be the supremum over all stopping times:

| (79) |

This solves the Bellman equation:

| (80) |

The associated Q-function is denoted , which solves a similar fixed point equation:

A stationary policy assigns an action for each state as

Each policy defines a stopping time and associated average reward, denoted

The optimal policy is expressed as

The corresponding optimal stopping time that solves the supremum in (79) is achieved using this policy: [34].

The objective here is to find an approximation for in a parameterized class , where is a vector of basis functions. For a fixed parameter vector , the associated value function is denoted

| (81) | ||||

The function was estimated using Monte-Carlo in the numerical experiments surveyed below.

Approximations to the Optimal Stopping Time Problem

To obtain the optimal parameter vector , in [34] the authors apply the Q()-learning algorithm:

| (82) |

This is one of the few parameterized Q-learning settings for which convergence is guaranteed [34].

In [9] the authors attempt to improve the performance of the Q() algorithm through the use of the sequence of matrix gains and a special choice for the :

| (83) |

where and are positive constants. The resulting recursion is the -Q() algorithm:

Through trial and error the authors find that , gives good performance. These values were also used in the experiments described in the following.

The limiting matrix gain is given by

where the expectation is in steady-state. The asymptotic covariance is the unique positive semi-definite solution to the Lyapunov equation (13), provided all eigenvalues of satisfy .

The Zap Q-learning algorithm for this example is defined by the following recursion:

| (84) | |||||

It is conjectured that the asymptotic covariance is obtained using (14), where the matrix is the limit of :

Experimental Results

The experimental setting of [34, 9] is used to define the set of basis functions and other parameters. The dimension of the parameter vector was chosen to be , with the basis functions defined in [9]. The objective here is to compare the performances of -Q() and the Zap-Q algorithms in terms of both parameter convergence, and with respect to the resulting average reward (81).

The asymptotic covariance matrices and were estimated through the following steps: The matrices and were estimated via Monte-Carlo. Estimation of requires an estimate of ; this was taken to be , with , obtained using the Zap-Q two timescale algorithm with and . This estimate of was also used to estimate the covariance matrix defined in (10) using the batch means method. The matrices and were then obtained using (13) and (14), respectively.

It was found that the trace of was about times greater than that of .

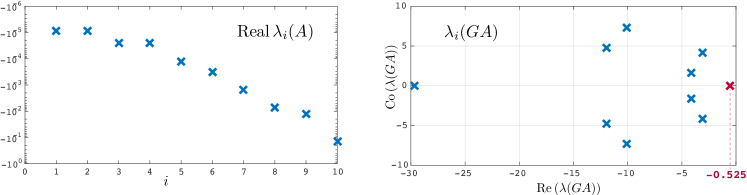

High performance despite ill-conditioned matrix gain

The real part of the eigenvalues of are shown on a logarithmic scale on the left-hand side of Fig. 15. The eigenvalues of the matrix have a wide spread: The condition-number is of the order . This presents a challenge in applying any method. In particular, it was found that the performance of any scalar-gain algorithm was extremely poor, even with projection of parameter estimates.

This is a consequence of the fact that the basis functions are nearly linearly dependent. A better basis should be considered in future work, but the main objective here is to test the new methods in a challenging setting, and to compare with prior approaches.

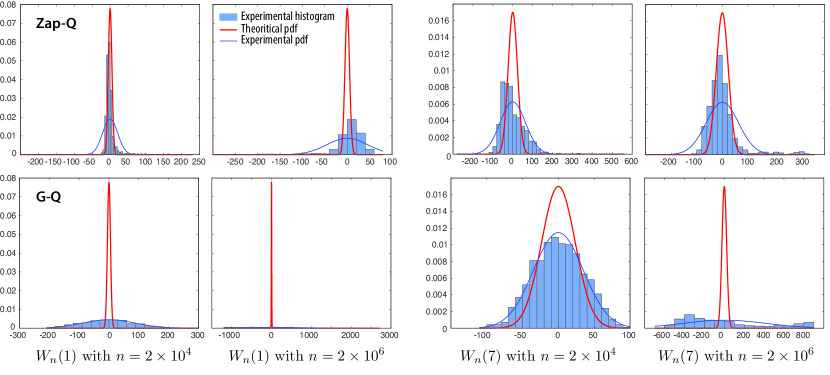

In applying the Zap Q-learning algorithm it was found that the estimates in (84) are nearly singular. Despite the unfavorable setting for this approach, the performance of the algorithm was much better than any alternative that was tested. The upper row of Fig. 16 contains normalized histograms of for the Zap-Q algorithm. The variance for finite is close to the theoretical predictions based on the asymptotic covariance . The histograms were generated for two values of , and . Of the possibilities, the histogram for had the worst match with theoretical predictions, and was the closest.

The eigenvalues corresponding to the matrix are shown on the right hand side of Fig. 15. It is found that one of these eigenvalues is very close to , and the sufficient condition for is barely satisfied. It is worth stressing that the finite asymptotic covariance was not a design goal in this prior work. It is only now on revisiting this paper that we find that the sufficient condition is satisfied.

The lower row of Fig. 16 contains the normalized histograms of for the -Q() algorithm for and , and , along with the theoretical predictions based on the asymptotic covariance .

Asymptotic variance of the discounted reward

Denote , with . Histograms of the average reward were obtained for , , and various values of , based on independent simulations. The plots shown in Fig. 17 are based on , for . Omitted in this figure are outliers: values of the reward in the interval . Table 1 lists the number of outliers for each and each algorithm.

Recall that the asymptotic covariance of the -Q() algorithm was not far from optimal (its trace was about 15 times larger than obtained using Zap Q-learning). However, it is observed that this algorithm suffers from much larger outliers. It can also be seen that doubling the scalar gain (causing the largest eigenvalue of to be ) results in slightly better performance.

| -Q() | 827 | 775 | 680 |

|---|---|---|---|

| -Q() | 824 | 725 | 559 |

| Zap-Q | 820 | 541 | 625 |

| Zap-Q | 236 | 737 | 61 |

| Zap-Q | 386 | 516 | 74 |

| -Q() | 811 | 755 | 654 |

|---|---|---|---|

| -Q() | 806 | 706 | 537 |

| Zap-Q | 55 | 0 | 0 |

| Zap-Q | 0 | 0 | 0 |

| Zap-Q | 0 | 0 | 0 |

| -Q() | 774 | 727 | 628 |

| -Q() | 789 | 688 | 525 |

| Zap-Q | 4 | 0 | 0 |

| Zap-Q | 0 | 0 | 0 |

| Zap-Q | 0 | 0 | 0 |

| -Q() | 545 | 497 | 395 |

| -Q() | 641 | 518 | 390 |

| Zap-Q | 0 | 0 | 0 |

| Zap-Q | 0 | 0 | 0 |

| Zap-Q | 0 | 0 | 0 |

5 Conclusions

Watkins’ Q-learning algorithm is elegant, but subject to two common and valid constraints: it can be very slow to converge, and it is not obvious how to extend this approach to obtain a stable algorithm in non-trivial parameterized settings. This paper addresses both concerns with the new Zap Q() algorithms that are motivated by asymptotic theory of stochastic approximation.

There are many avenues for future research. It would be valuable to find an alternative to Assumption Q3 that is readily verified. Based on the ODE analysis, it seems likely that the conclusions of Thm. 3.4 hold without this additional assumption. No theory has been presented here for non-ideal parameterized settings. It is conjectured that conditions for stability of Zap Q()-learning will hold under general conditions. Consistency is a more challenging problem and is a focus of current research.

In terms of algorithm design, it is remarkable to see how well the scalar-gain algorithms perform, provided projection is employed and the condition number of is not too large. It is possible to estimate the optimal scalar gain based on estimates of the matrix that is central to this paper. How to do so without introducing high complexity is an open question.

On the other hand, the performance of RPJ averaging is unpredictable. In many experiments it is found that the asymptotic covariance is a poor indicator of finite- performance when using this approach. There are many suggestions in the literature for improving this technique (see discussion after Theorem 3 of [21]) .

The results in this paper suggest new approaches that we hope will simultaneously

-

(i)

Reduce complexity and potential numerical instability of matrix inversion,

-

(ii)

Improve transient performance, and

-

(iii)

Maintain optimality of the asymptotic covariance

References

- [1] M. G. Azar, R. Munos, M. Ghavamzadeh, and H. Kappen. Speedy Q-learning. In Advances in Neural Information Processing Systems, 2011.

- [2] K. Barman and V. S. Borkar. A note on linear function approximation using random projections. Systems & Control Letters, 57(9):784–786, 2008.

- [3] A. Benveniste, M. Métivier, and P. Priouret. Adaptive algorithms and stochastic approximations, volume 22 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1990. Translated from the French by Stephen S. Wilson.

- [4] D. P. Bertsekas. Dynamic Programming and Optimal Control, volume 2. Athena Scientific, 4th edition, 2012.

- [5] V. S. Borkar. Stochastic Approximation: A Dynamical Systems Viewpoint. Hindustan Book Agency and Cambridge University Press (jointly), Delhi, India and Cambridge, UK, 2008.

- [6] V. S. Borkar and S. P. Meyn. The ODE method for convergence of stochastic approximation and reinforcement learning. SIAM J. Control Optim., 38(2):447–469, 2000. (also presented at the IEEE CDC, December, 1998).

- [7] J. A. Boyan. Technical update: Least-squares temporal difference learning. Mach. Learn., 49(2-3):233–246, 2002.

- [8] S. J. Bradtke and A. G. Barto. Linear least-squares algorithms for temporal difference learning. Mach. Learn., 22(1-3):33–57, 1996.

- [9] D. Choi and B. Van Roy. A generalized Kalman filter for fixed point approximation and efficient temporal-difference learning. Discrete Event Dynamic Systems: Theory and Applications, 16(2):207–239, 2006.

- [10] E. Even-Dar and Y. Mansour. Learning rates for Q-learning. Journal of Machine Learning Research, 5(Dec):1–25, 2003.

- [11] P. W. Glynn and D. Ormoneit. Hoeffding’s inequality for uniformly ergodic Markov chains. Statistics and Probability Letters, 56:143–146, 2002.

- [12] V. R. Konda and J. N. Tsitsiklis. Convergence rate of linear two-time-scale stochastic approximation. Ann. Appl. Probab., 14(2):796–819, 2004.

- [13] V. V. G. Konda. Actor-critic algorithms. PhD thesis, Massachusetts Institute of Technology, 2002.

- [14] H. J. Kushner and G. G. Yin. Stochastic approximation algorithms and applications, volume 35 of Applications of Mathematics (New York). Springer-Verlag, New York, 1997.

- [15] R. B. Lund, S. P. Meyn, and R. L. Tweedie. Computable exponential convergence rates for stochastically ordered Markov processes. Ann. Appl. Probab., 6(1):218–237, 1996.

- [16] D.-J. Ma, A. M. Makowski, and A. Shwartz. Stochastic approximations for finite-state Markov chains. Stochastic Process. Appl., 35(1):27–45, 1990.

- [17] P. G. Mehta and S. P. Meyn. Q-learning and Pontryagin’s minimum principle. In IEEE Conference on Decision and Control, pages 3598–3605, Dec. 2009.

- [18] S. P. Meyn and A. Surana. TD-learning with exploration. In 50th IEEE Conference on Decision and Control, and European Control Conference, pages 148–155, Dec 2011.

- [19] S. P. Meyn and R. L. Tweedie. Computable bounds for convergence rates of Markov chains. Ann. Appl. Probab., 4:981–1011, 1994.

- [20] S. P. Meyn and R. L. Tweedie. Markov chains and stochastic stability. Cambridge University Press, Cambridge, second edition, 2009. Published in the Cambridge Mathematical Library. 1993 edition online.

- [21] E. Moulines and F. R. Bach. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. In Advances in Neural Information Processing Systems 24, pages 451–459. Curran Associates, Inc., 2011.

- [22] A. Nedic and D. Bertsekas. Least squares policy evaluation algorithms with linear function approximation. Discrete Event Dynamic Systems: Theory and Applications, 13(1-2):79–110, 2003.

- [23] D. Paulin. Concentration inequalities for Markov chains by Marton couplings and spectral methods. Electron. J. Probab., 20:32 pp., 2015.

- [24] B. T. Polyak. A new method of stochastic approximation type. Avtomatika i telemekhanika (in Russian). translated in Automat. Remote Control, 51 (1991), pages 98–107, 1990.

- [25] B. T. Polyak and A. B. Juditsky. Acceleration of stochastic approximation by averaging. SIAM J. Control Optim., 30(4):838–855, 1992.

- [26] G. A. Rummery and M. Niranjan. On-line Q-learning using connectionist systems. Technical report 166, Cambridge Univ., Dept. Eng., Cambridge, U.K. CUED/F-INENG/, 1994.

- [27] D. Ruppert. A Newton-Raphson version of the multivariate Robbins-Monro procedure. The Annals of Statistics, 13(1):236–245, 1985.

- [28] D. Ruppert. Efficient estimators from a slowly convergent Robbins-Monro processes. Technical Report Tech. Rept. No. 781, Cornell University, School of Operations Research and Industrial Engineering, Ithaca, NY, 1988.

- [29] A. Shwartz and A. Makowski. On the Poisson equation for Markov chains: existence of solutions and parameter dependence. Technical Report, Technion—Israel Institute of Technology, Haifa 32000, Israel., 1991.

- [30] R. S. Sutton. Learning to predict by the methods of temporal differences. Mach. Learn., 3(1):9–44, 1988.

- [31] C. Szepesvári. The asymptotic convergence-rate of Q-learning. In Proceedings of the 10th International Conference on Neural Information Processing Systems, pages 1064–1070. MIT Press, 1997.

- [32] C. Szepesvári. Algorithms for Reinforcement Learning. Synthesis Lectures on Artificial Intelligence and Machine Learning. Morgan & Claypool Publishers, 2010.

- [33] J. N. Tsitsiklis and B. Van Roy. An analysis of temporal-difference learning with function approximation. IEEE Trans. Automat. Control, 42(5):674–690, 1997.

- [34] J. N. Tsitsiklis and B. Van Roy. Optimal stopping of Markov processes: Hilbert space theory, approximation algorithms, and an application to pricing high-dimensional financial derivatives. IEEE Trans. Automat. Control, 44(10):1840–1851, 1999.

- [35] C. J. C. H. Watkins. Learning from Delayed Rewards. PhD thesis, King’s College, Cambridge, Cambridge, UK, 1989.

- [36] C. J. C. H. Watkins and P. Dayan. -learning. Machine Learning, 8(3-4):279–292, 1992.

- [37] H. Yu and D. P. Bertsekas. Q-learning and policy iteration algorithms for stochastic shortest path problems. Annals of Operations Research, 208(1):95–132, 2013.

Appendix A Appendices

A.1 Asymptotic covariance for Markov chains

As an illustration of the Lyapunov equation (8) that is solved by the asymptotic covariance, consider the error recursion for a one-dimensional version of (6) in which , and the algorithm is scaled by a gain parameter :

When this is a standard Monte-Carlo average. For general the Lyapunov equation admits the solution:

This grows without bound as or , as illustrated below:

![[Uncaptioned image]](/html/1707.03770/assets/x19.png)

Conditions to ensure that the covariance is infinite are presented in the following:

Proposition A.1.

Consider the linear recursion

| (85) |

in which is a martingale difference sequence satisfying as .

-

(i)

Suppose that is an eigenvalue-eigenvector pair satisfying , , and . Then,

-

(ii)

Suppose that all the eigenvalues of satisfy , then the asymptotic covariance is finite, and is obtained as a solution to the Lyapunov equation (13).

Proof.

Define and . A standard Taylor-series approximation of results in the following recursive definition of :

| (86) |

The assumptions of part (i) of the proposition implies:

and therefore , implying the result in part (i) of the proposition. Under the assumptions of part (ii), (86) implies that , where is obtained as a solution to the Lyapunov equation (13).

A.2 Proof of Thm. 3.3

Recall that denotes the diagonal matrix with entries , and the matrix is a function of :

In a neighborhood of , the operator coincides with , and we denote .

To prove the result we construct an eigenvector for whose entries are strictly positive. Next, under the assumptions of the proposition, we show that the corresponding eigenvalue satisfies , and the result then follows from Prop. A.1 combined with (51).

Recall from Lemma 3.1 that is a transition matrix, and so is the following

The construction of an eigenvector is via the representation . Since this is a positive and irreducible matrix, we can apply Perron-Frobenius theory to conclude that there is a maximal eigenvalue and an everywhere positive eigenvector satisfying

The Perron-Frobenius eigenvalue coincides with the spectral radius of :

The vector is also an eigenvector for with associated eigenvalue

Thus, under the assumptions of the proposition.

A.3 Proof of Thm. 3.4

The remainder of the Appendix is devoted to the proof of Thm. 3.4.

Lemma 3.9 is used to establish the “ODE friendly” property for the error sequences appearing in the ODE approximations.

Proof of Lemma 3.9.

Let solve Poisson’s equation:

with . The following representation is immediate:

where

and the final term is the martingale difference sequence:

The telescoping sequence is thus,

and

which satisfies (70) under Assumption Q3.

Recall the “” notation used in (67) is interpreted in a functional sense. It is a function of two variables: , satisfying for each ,

The notation for a vector-valued function of has an analogous interpretation:

This notation will also be used in the standard setting in which the variable is absent. In particular, simply means that as .

Recall the definitions of , , and in (59) and (66); was defined to be a piecewise linear function with when for some , and extended to all by linear interpolation. Recall that for large under (59). For fixed , let denote the cumulative distribution function on the interval :

| (87) |

This CDF defines a probability measure on the interval with the following properties:

Lemma A.2.

The probability measure associated with has a density on and a single point mass at zero. Its total mass is concentrated near : For any ,

An associated pmf on the set of policy indices is defined as follows:

| (88) |

Lemma A.3.

Proof.

The representation (73) directly follows from Lemmas 3.8 and 3.9. For , the solution to this linear time varying system is the sum of three terms:

| (92) | ||||

in which , and

and for each , is the integer satisfying .

We begin with a proof of boundedness of , considering the three terms in (92) separately. The first term vanishes as for each fixed . The second term admits the uniform bound:

| (93) |

in which is an upper bound on . It is shown next that the final term converges to zero as . Applying integration by parts:

where the second equation used and . Using this identity and the same arguments used to bound then gives

| (94) |

Using (93) and (94) in (92) establishes boundedness of :

and hence also boundedness of the sequence .

Lemma A.4.

The linear systems representation holds:

| (96) |

Furthermore, for a constant , and each ,

| (97a) | ||||

| (97b) | ||||

Proof.

Boundedness of in Lemma A.3 (i) implies that for in recursion (71). Representation (96) then follows from Lemmas 3.8 and 3.9. The evolution equation (96) implies:

Denoting

| (98) |

and applying Lemma A.3 (i),

The factor before the integral in the second inequality comes from choosing large enough, so that . Equation (97a) is then obtained by applying the Grönwall lemma [5].

Applying the triangle inequality to (97a), and choosing such that for all gives

| (99) |

In particular, the above inequality is true for . Furthermore, the following holds under the assumption that the sequence is projected prior to inversion: For a constant ,

| (100) |

Lemma A.5.

For each , the following holds:

| (101a) | ||||

| (101b) | ||||

Proof.

Equation (90) of Lemma A.3 implies the following representation:

Subtracting from each side and taking norms gives the bound,

| (102) |

Lemma 3.2 implies that the mappings and are Lipschitz: for a constant ,

Substituting into (102) gives

where the second inequality uses equation (97a) of Lemma A.4, and the last approximation follows from Lemma A.2.

Lemma A.6.

-

(i)

.

-

(ii)

For ,

(103a) (103b) (103c)

Proof.

With these results established, the ODE approximation will quickly follow. For a fixed but arbitrary time-horizon , define a family of uniformly bounded and uniformly Lipschitz continuous functions , where for each and some integer . The family of functions is constructed from the following familiar components: for ,

More precisely, is a function of two variables, and . To say that is uniformly bounded and uniformly Lipschitz continuous means that there exists with measure one such that for each , the family of functions , is uniformly bounded and Lipschitz. The bound and the Lipschitz constant may depend on , but are independent of .

Any sub-sequential limit of will be denoted . To maintain consistency with the notation in Thm. 3.4, the first two components are denoted

The ODE limit is recast as follows:

Proposition A.7.

Any sub-sequential limit of must have the following form: for ,

-

(i)

.

-

(ii)

.

-

(iii)

For a.e. , there is a pmf such that

The first relation, that , is obvious because the mapping is continuous. The proofs of (ii) and (iii) are similar: prior results and a few results that follow are reinterpreted as properties of that are preserved in any sub-sequential limit. For example, (103c) admits the representation in terms of :

| (105) |

The following result establishes that the left hand side represents a continuous functional of :

Lemma A.8.

For fixed , , and , let denote the set of all functions satisfying , and are Lipschitz continuous with Lipschitz constant :

The set is compact as a subset of . Moreover, the following real-valued functional is Lipschitz continuous on :

Proof.

Since is bilinear, it is sufficient to obtain Lipschitz constants in either variable.

For a fixed function , and any two functions ,

which implies Lipschitz continuity of in its first variable, with Lipschitz constant .

A similar result is obtained for a fixed . Using integration by parts:

For any two functions ,

This proves Lipschitz continuity of in its second variable, with Lipschitz constant .

The next result implies another continuous relationship for :

Lemma A.9.

For each and , there exists a pmf such that

with defined in (88). That is, the matrix lies in the compact set .

Lemma A.10.

For any sub-sequential limit , let denote a point at which both and are differentiable. Let be any pmf satisfying . Then,

Proof.

This is an instance of the chain rule. A proof is provided since is not smooth.

These two functions are approximated by a line at this time point:

| (106) | ||||

where , are the respective derivatives. The lemma asserts that .

Denote , , . Applying (44) we have for each :

Differentiability of at then implies the desired conclusion: .

Proof of Prop. A.7.

Recall that (i) has been established. Result (iii) is established next, which will quickly lead to (ii).

Lemma A.9 implies the following relationship for : For each and , there exists a pmf such that

It follows that the same is true for any sub-sequential limit : There is a parameterized family of pmfs such that

In the pre-limit we have for each and . It can be shown using Laplace transform arguments that the same must be true in the limit for a.e. , giving the first half of (iii).

Next, we prove the second half of (iii): for a.e. . From equation (101a) of Lemma A.5,

In notation:

Lemma A.8 asserts that the left hand side of the above equation defines a continuous functional of , and therefore the relationship also holds in the limit:

This establishes the second half of part (iii) of the lemma.

| Symbol | Type | Description |

|---|---|---|

| set; is a component | state space of the Markov chain | |

| set; is a component | action space of the Markov chain | |

| function | cost function | |

| scalar | discount factor | |

| vector; | parameter vector | |

| function | basis functions for TD-learning | |

| function | basis functions for Q-learning | |

| scalar; | step-size sequence | |

| scalar; | step-size sequence | |

| function | value function | |

| function | a linear approximation to : | |

| function | SARSA Q-function for an uncontrolled Markov chain | |

| function | a linear approximation to : | |

| vector; | optimal parameter vector satisfying: or | |

| vector; | error in the parameter vector: | |

| operator | given , | |

| function | eligibility vector for TD-learning | |

| function | eligibility vector for Q-learning | |

| sequence | uncontrolled Markov chain evolving on | |

| sequence | Markov chain of interest when applying stochastic approximation | |

| function | steady state distribution / probability mass function of | |

| sequence | error sequence | |

| function | policy | |

| scalar | number of elements in : | |

| scalar | number of elements in : | |

| scalar | number of possible policies: | |

| operator | tr. kernel (controlled): | |

| operator | tr. kernel (uncontrolled): | |

| operator | given , | |

| function | value function for a given policy | |

| function | -optimal policy: | |

| function | value function for an uncontrolled Markov chain with policy | |

| function | optimal value function | |

| operator | given , is the optimal -function for cost | |

| function | optimal -function for cost | |

| function | Bellman error for the -function approximation | |

| matrix | diagonal matrix: | |

| matrix | outer product of the basis functions: | |

| sequence | arbitrary sequence of matrix gains | |

| matrix | steady state mean of | |

| ; | matrix | linearization in stochastic approximation; s.s. mean |

| ; | vector | vector sequence; s.s. mean |

| matrix | -step Monte-Carlo estimate of | |

| vector | -step Monte-Carlo estimate of |