Modeling the price of Bitcoin with geometric fractional Brownian motion: a Monte Carlo approach

Abstract

The long-term dependence of Bitcoin (BTC), manifesting itself through a Hurst exponent , is exploited in order to predict future BTC/USD price. A Monte Carlo simulation with geometric fractional Brownian motion realisations is performed as extensions of historical data. The accuracy of statistical inferences is 10%. The most probable Bitcoin price at the beginning of 2018 is 6358 USD.

keywords:

Bitcoin , Cryptocurrency , Hurst exponent , Geometric fractional Brownian motionJEL classification: G12 , E47 , C22

1 Introduction

Bitcoin, after being introduced by Nakamoto [2008], has been constantly gaining popularity. Its price and volume have increased by several orders of magnitude. Being the so-called cryptocurrency, i.e. an asset derived from mathematical cryptography, it is based on a new technology called the blockchain [Bradbury, 2013, Ali et al., 2014]. Its other fundamental characteristics are: being decentralised, and having a fixed total number of coins: 21 million, with more than 16 million already in circulation.111https://www.worldcoinindex.com/, accessed on 2017-07-06. Bitcoin is still very young, especially considering the fact that the last coin is to be mined around year 2140 [Vranken, 2017].

While Bitcoin does not have the features of a currency [Baek & Elbeck, 2015, Dyhrberg, 2016] and is highly volatile [Dwyer, 2015, Katsiampa, 2017], it can serve as an effective diversifier [Brière et al., 2015, Bouri et al., 2017] and be a complement to fiat currencies [Carrick, 2016]. Moreover, it recently entered the phase of being weakly efficient [Urquhart, 2016, Nadarajah & Chu, 2017] in the sense of the market efficiency hypothesis [Mantegna & Stanley, 2000]. On the other hand, Bitcoin market exhibits speculative bubbles [Shiller, 2014, Cheah & Fry, 2015, Cheung et al., 2015]. Its high volatility and substantial speculative component are related to the fact that Bitcoin is still more a trading asset than a currency [Dyhrberg, 2016, Katsiampa, 2017].

The Bitcoin exchange rates have been already modeled and predicted by means of a noncausal autoregressive process [Hencic & Gouriéroux, 2015]. On the other hand, financial time series, e.g. stocks, exchange rates, bonds or commodities, are characterised by the Hurst exponent [Liu et al., 1999, Carbone et al., 2004, Di Matteo et al., 2005, Sánchez Granero et al., 2008, Zunino et al., 2017], and share the scaling properties with the fractional Brownian motion (fBm) [Lo, 1991, Cheridito, 2003, Bayraktar et al., 2004, Cont, 2005, Gu et al., 2012, Areerak, 2014, Vukovic, 2015]. Therefore, in this work Bitcoin price forecasts are done via Monte Carlo simulations of a large sample () of geometric fBms as a stochastic process governing the price. The most probable prices are then derived from the empirical cumulative distribution function (CDF).

2 Data and method

Data

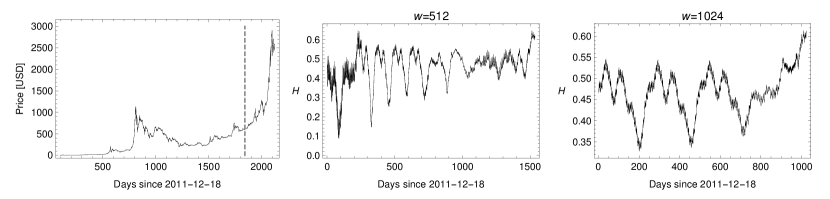

The examined data set spans from 2011-12-18 to 2017-07-06. The daily weighted prices were downloaded from BitcoinCharts.222https://bitcoincharts.com/charts, accessed on 2017-07-06. A three-day gap from 2015-01-06 to 2015-01-08 was linearly interpolated based on prices on 2015-01-05 and 2015-01-09. The total number of data points is 2028. The data is displayed in Fig. 1.

Hurst exponent

To compute the Hurst exponent , the wavelet approach using the Haar wavelet as a basis is employed [Tarnopolski, 2016]; the error is the standard error of the slope of the fitted linear dependence of the logarithmic variance of the wavelet coefficients’ versus octave (see Tarnopolski 2016 and references therein for details). In order to make the size a power of 2, the examined data sets were padded left with zeros. For the whole dataset, . To verify the validity of the employed method, the set of prices until the end of 2016 is examined. It is characterised by and consists of 1841 data points. The time dependence of for two sliding windows is displayed in Fig. 1. An increase in the instantaneous value of could be observed recently.

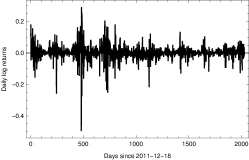

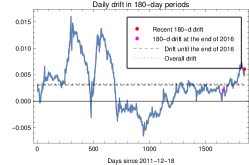

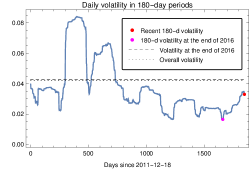

To verify the approach from the next paragraph, the drift and volatility (taken as the mean and standard deviation, respectively, of the daily log returns; see Fig. 2) are computed for daily log returns until the end of 2016 (yielding and ), and for future forecasts the values appropriate for the whole historical data set are employed ( and ). The time dependencies of the drift and volatility of the whole period under examination are displayed in Fig. 2.

|

|

|

Methodology

The idea exploited herein is to generate a large number () of fractional Brownian motion (fBm) realisations with Hurst exponent , and insert them into the solution [Dai1996, Biagini et al., 2008, Gu et al., 2012, Nguyen2013]

| (1) |

of the stochastic differential equation describing a geometric fractional Brownian motion:

| (2) |

where is the initial price of the extensions, taken as the last price in the historical data set, and and are drift and volatility, respectively. The fBms are generated with and the same as the historical prices yield: . From the set of last prices of each realisation, an empirical CDF, , is constructed, and probabilities of reaching prices lower than : , or higher than : , are computed. The approach is first tested on a set of prices until the end of 2016, and then a prediction is made for the future 180 days. The computer algebra system Mathematica is applied throughout this paper; in particular, fBms are generated as FractionalBrownianMotionProcess[,,H].

The distribution of from Eq. (1) follows a log-normal distribution , with mean: , median: , and mode: , which in turn follow . Trivially, .

3 Results

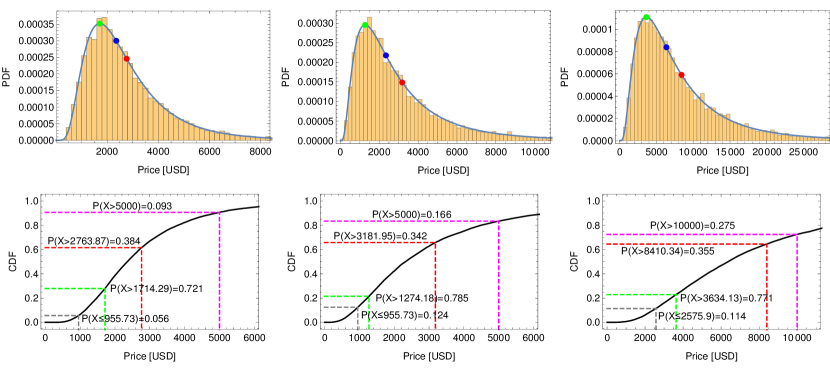

First, the set of prices until the end of 2016 is examined. It is characterised by and consists of 1841 data points. realisations of fBm (of length 187 each) are generated. Fig. 3 displays the results in its left column. The histogram is the empirical probability density function (PDF) of prices taken as the last value of the generated fBms (i.e., 2028 days after 2011-12-18, or on the 187th day of 2017), overlaid with a log-normal fit which yielded a mean of 2763.87 USD (red dot), and mode of 1714.29 USD (green dot). The probabilities of attaining a given price are calculated via the CDF; 955.73 USD is the price on 2016-12-31, and there was a 5.3% chance of reaching a price smaller than this. Exceeding the mean 2763.87 USD had a 38.4% probability, exceeding the mode 1714.29 USD had a 72.1% chance of occuring, and a threshold of 5000 USD or more yielded a probability of 9.3%. The median was at 2357.07 USD (blue dot).

The mean, mode and median for a log-normal distribution are different, as noted in Sect. 2, but a log-transform of the data is normally distributed. For a normal distribution the the mean, mode and median are all equal to , which denotes the most probable value, and through an inverse transform it turns into the median of a log-normal distribution, . Hence, the prediction of the Bitcoin price is taken as the median.

The middle column of Fig. 3 is the same as the left one, but with an updated , i.e. the value for the whole historical data set. This is performed as the value of increased in the last months. Employing the actual yielded a mean price of 3181.95 USD, and a mode of 1274.18 USD. The probability of falling below 955.73 USD was 12.4%, of exceeding the mean was 34.2%, of exceeding the mode has a 78.5%, and rising above the threshold of 5000 USD had 16.6% chance of occurence. The median was at 2345.34 USD. Overall, the predicted price (i.e., the median) is about 10% lower than the attained one, being a good agreement given the recent sudden rise in price, which lead to an increase of the instantaneous value of (compare with Fig. 1).

To make predictions about the Bitcoin price 180 days from 2017-06-07, again fBm realisations were generated and inserted into Eq. (1). The results are displayed in the right column of Fig. 3. The probability of falling below the current price of 2575.9 USD is 11.4%, of exceeding the mean of 8410.34 USD is 35.5%, of excedding the mode of 3634.13 USD is 77.1%, and reaching a price higher than 10,000 USD has a chance of 27.5%. The median is at 6358.32 USD, i.e. this is the predicted price to be attained in the beginning of 2018.

4 Concluding remarks

The Bitcoin price was modeled as a geometric fBm [Biagini et al., 2008], and price predictions were put forward through a Monte Carlo approach with realisations. The predicted mid-2017 price, based on historical values until the end of 2016, taken as the median, was slightly—i.e., by about 10%—underestimated. This is considered as a good agreement, thus justifying the applicability of the model. Therefore, price predictions for the beginning of 2018 were made in the same way. It is found, via the log-normal PDF and its CDF, that the price predicted as the median of a log-normally distributed set of realisations is 6358 USD. On the other hand, the chance of falling below the current price of 2575.9 USD is 11.4%.

While the agreement of the predictions with reality is remarkable (i.e., considering the mean and median), it is well-known that large fluctuations in the market are more common than geometric fBm predicts. In fact, extreme events—like the 1987’s Black Monday or the 2008-9 market crash—are virtually impossible under usual assumptions [Jackwerth & Rubinstein, 1996]. This is true for the classical Black & Scholes [1973] model as well. In case of Bitcoin, such an extreme event might be caused by the upcoming SegWit/UASF on 2017-08-01.333http://www.uasf.co/ A possible improvement might be to account for time variation of the volatility [Areerak, 2014] and the Hurst exponent. On the other hand, other models that incorporate bullish and bearish parameters to account for big upward and downward jumps, e.g. [Câmara & Heston, 2008], are perspective.

Disclaimer

This manuscript is for information and illustrative purposes only. It is not, and should not be regarded as investment advice or as a recommendation regarding a course of action. The reader will make their own independent decision with respect to any course of action in connection herewith, as to whether such course of action is appropriate or proper based on their own judgment and their specific circumstances and objectives. The reader should seek a duly licensed professional for investment advice.

References

References

- Ali et al. [2014] Ali, R., Barrdear, J., Clews, R., & Southgate, J. (2014). The economics of digital currencies. Bank of England Quarterly Bulletin, 54, 276–286. URL: http://EconPapers.repec.org/RePEc:boe:qbullt:0148.

- Areerak [2014] Areerak, T. (2014). Mathematical model of stock prices via a fractional brownian motion model with adaptive parameters. ISRN Applied Mathematics, 2014, 791418. URL: http://dx.doi.org/10.1155/2014/791418. doi:10.1155/2014/791418.

- Baek & Elbeck [2015] Baek, C., & Elbeck, M. (2015). Bitcoins as an investment or speculative vehicle? a first look. Applied Economics Letters, 22, 30–34. URL: http://dx.doi.org/10.1080/13504851.2014.916379. doi:10.1080/13504851.2014.916379.

- Bayraktar et al. [2004] Bayraktar, E., Poor, H. V., & Sircar, K. R. (2004). Estimating the fractal dimension of the s&p index using wavelet analysis. International Journal of Theoretical and Applied Finance, 07, 615–643. URL: http://www.worldscientific.com/doi/abs/10.1142/S021902490400258X. doi:10.1142/S021902490400258X.

- Biagini et al. [2008] Biagini, F., Hu, Y., Øksendahl, B., & Zhang, T. (2008). Stochastic Calculus for Fractional Brownian Motion and Applications. Springer, London. doi:10.1007/978-1-84628-797-8.

- Black & Scholes [1973] Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81, 637–54. URL: http://www.jstor.org/stable/1831029.

- Bouri et al. [2017] Bouri, E., Molnár, P., Azzi, G., Roubaud, D., & Hagfors, L. I. (2017). On the hedge and safe haven properties of bitcoin: Is it really more than a diversifier? Finance Research Letters, 20, 192 – 198. URL: http://www.sciencedirect.com/science/article/pii/S1544612316301817. doi:https://doi.org/10.1016/j.frl.2016.09.025.

- Bradbury [2013] Bradbury, D. (2013). The problem with bitcoin. Computer Fraud & Security, 2013, 5 – 8. URL: http://www.sciencedirect.com/science/article/pii/S1361372313701015. doi:http://dx.doi.org/10.1016/S1361-3723(13)70101-5.

- Brière et al. [2015] Brière, M., Oosterlinck, K., & Szafarz, A. (2015). Virtual currency, tangible return: Portfolio diversification with bitcoin. Journal of Asset Management, 16, 365–373. URL: http://dx.doi.org/10.1057/jam.2015.5. doi:10.1057/jam.2015.5.

- Câmara & Heston [2008] Câmara, A., & Heston, S. L. (2008). Closed-form option pricing formulas with extreme events. Journal of Futures Markets, 28, 213–230. URL: http://dx.doi.org/10.1002/fut.20298. doi:10.1002/fut.20298.

- Carbone et al. [2004] Carbone, A., Castelli, G., & Stanley, H. E. (2004). Time-dependent Hurst exponent in financial time series. Physica A Statistical Mechanics and its Applications, 344, 267–271. URL: http://www.sciencedirect.com/science/article/pii/S0378437104009471. doi:10.1016/j.physa.2004.06.130.

- Carrick [2016] Carrick, J. (2016). Bitcoin as a complement to emerging market currencies. Emerging Markets Finance and Trade, 52, 2321–2334. URL: http://dx.doi.org/10.1080/1540496X.2016.1193002. doi:10.1080/1540496X.2016.1193002.

- Cheah & Fry [2015] Cheah, E.-T., & Fry, J. (2015). Speculative bubbles in bitcoin markets? an empirical investigation into the fundamental value of bitcoin. Economics Letters, 130, 32 – 36. URL: http://www.sciencedirect.com/science/article/pii/S0165176515000890. doi:http://dx.doi.org/10.1016/j.econlet.2015.02.029.

- Cheridito [2003] Cheridito, P. (2003). Arbitrage in fractional brownian motion models. Finance and Stochastics, 7, 533–553. URL: http://dx.doi.org/10.1007/s007800300101. doi:10.1007/s007800300101.

- Cheung et al. [2015] Cheung, A. W.-K., Roca, E., & Su, J.-J. (2015). Crypto-currency bubbles: an application of the phillips–shi–yu (2013) methodology on mt. gox bitcoin prices. Applied Economics, 47, 2348–2358. URL: http://dx.doi.org/10.1080/00036846.2015.1005827. doi:10.1080/00036846.2015.1005827.

- Cont [2005] Cont, R. (2005). Long range dependence in financial markets. In J. Lévy-Véhel, & E. Lutton (Eds.), Fractals in Engineering: New Trends in Theory and Applications (pp. 159–179). London: Springer London. URL: http://dx.doi.org/10.1007/1-84628-048-6_11. doi:10.1007/1-84628-048-6_11.

- Di Matteo et al. [2005] Di Matteo, T., Aste, T., & Dacorogna, M. M. (2005). Long-term memories of developed and emerging markets: Using the scaling analysis to characterize their stage of development. Journal of Banking & Finance, 29, 827 – 851. URL: http://www.sciencedirect.com/science/article/pii/S0378426604001438. doi:http://dx.doi.org/10.1016/j.jbankfin.2004.08.004.

- Dwyer [2015] Dwyer, G. P. (2015). The economics of bitcoin and similar private digital currencies. Journal of Financial Stability, 17, 81 – 91. URL: http://www.sciencedirect.com/science/article/pii/S1572308914001259. doi:http://dx.doi.org/10.1016/j.jfs.2014.11.006.

- Dyhrberg [2016] Dyhrberg, A. H. (2016). Bitcoin, gold and the dollar – a garch volatility analysis. Finance Research Letters, 16, 85 – 92. URL: http://www.sciencedirect.com/science/article/pii/S1544612315001038. doi:http://dx.doi.org/10.1016/j.frl.2015.10.008.

- Gu et al. [2012] Gu, H., Liang, J.-R., & Zhang, Y.-X. (2012). Time-changed geometric fractional brownian motion and option pricing with transaction costs. Physica A: Statistical Mechanics and its Applications, 391, 3971 – 3977. URL: http://www.sciencedirect.com/science/article/pii/S0378437112002567. doi:http://dx.doi.org/10.1016/j.physa.2012.03.020.

- Hencic & Gouriéroux [2015] Hencic, A., & Gouriéroux, C. (2015). Noncausal autoregressive model in application to bitcoin/usd exchange rates. In V.-N. Huynh, V. Kreinovich, S. Sriboonchitta, & K. Suriya (Eds.), Econometrics of Risk (pp. 17–40). Springer International Publishing. URL: http://dx.doi.org/10.1007/978-3-319-13449-9_2. doi:10.1007/978-3-319-13449-9_2.

- Jackwerth & Rubinstein [1996] Jackwerth, J., & Rubinstein, M. (1996). Recovering probability distributions from option prices. Journal of Finance, 51, 1611–32. URL: http://www.jstor.org/stable/2329531. doi:10.2307/2329531.

- Katsiampa [2017] Katsiampa, P. (2017). Volatility estimation for bitcoin: A comparison of garch models. Economics Letters, 158, 3 – 6. URL: http://www.sciencedirect.com/science/article/pii/S0165176517302501. doi:https://doi.org/10.1016/j.econlet.2017.06.023.

- Liu et al. [1999] Liu, Y., Gopikrishnan, P., Cizeau, P., Meyer, M., Peng, C.-K., & Stanley, H. E. (1999). Statistical properties of the volatility of price fluctuations. Phys. Rev. E, 60, 1390–1400. URL: https://link.aps.org/doi/10.1103/PhysRevE.60.1390. doi:10.1103/PhysRevE.60.1390.

- Lo [1991] Lo, A. W. (1991). Long-term memory in stock market prices. Econometrica, 59, 1279–1313. URL: http://www.jstor.org/stable/2938368. doi:10.2307/2938368.

- Mantegna & Stanley [2000] Mantegna, R. N., & Stanley, H. E. (2000). An Introduction to Econophysics: Correlations and Complexity in Finance. Cambridge University Press, New York.

- Nadarajah & Chu [2017] Nadarajah, S., & Chu, J. (2017). On the inefficiency of bitcoin. Economics Letters, 150, 6 – 9. URL: http://www.sciencedirect.com/science/article/pii/S0165176516304426. doi:https://doi.org/10.1016/j.econlet.2016.10.033.

- Nakamoto [2008] Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system, . URL: http://bitcoin.org/bitcoin.pdf/.

- Sánchez Granero et al. [2008] Sánchez Granero, M. A., Trinidad Segovia, J. E., & García Pérez, J. (2008). Some comments on hurst exponent and the long memory processes on capital markets. Physica A: Statistical Mechanics and its Applications, 387, 5543 – 5551. URL: http://www.sciencedirect.com/science/article/pii/S0378437108004895. doi:http://dx.doi.org/10.1016/j.physa.2008.05.053.

- Shiller [2014] Shiller, R. J. (2014). Speculative asset prices. American Economic Review, 104, 1486–1517. URL: http://www.aeaweb.org/articles?id=10.1257/aer.104.6.1486. doi:10.1257/aer.104.6.1486.

- Tarnopolski [2016] Tarnopolski, M. (2016). On the relationship between the hurst exponent, the ratio of the mean square successive difference to the variance, and the number of turning points. Physica A: Statistical Mechanics and its Applications, 461, 662 – 673. URL: http://www.sciencedirect.com/science/article/pii/S0378437116302722. doi:http://dx.doi.org/10.1016/j.physa.2016.06.004.

- Urquhart [2016] Urquhart, A. (2016). The inefficiency of bitcoin. Economics Letters, 148, 80 – 82. URL: http://www.sciencedirect.com/science/article/pii/S0165176516303640. doi:http://dx.doi.org/10.1016/j.econlet.2016.09.019.

- Vranken [2017] Vranken, H. (2017). Sustainability of bitcoin and blockchains. Current Opinion in Environmental Sustainability, 28, 1 – 9. URL: http://www.sciencedirect.com/science/article/pii/S1877343517300015. doi:https://doi.org/10.1016/j.cosust.2017.04.011.

- Vukovic [2015] Vukovic, O. (2015). Analysing the chinese stock market using the hurst exponent, fractional brownian motion and variants of a stochastic logistic differential equation. International Journal of Design & Nature and Ecodynamics, 10, 300–309. URL: https://www.witpress.com/elibrary/dne-volumes/10/4/1010. doi:10.2495/DNE-V10-N4-300-309.

- Zunino et al. [2017] Zunino, L., Olivares, F., Bariviera, A. F., & Rosso, O. A. (2017). A simple and fast representation space for classifying complex time series. Physics Letters A, 381, 1021 – 1028. URL: http://www.sciencedirect.com/science/article/pii/S0375960116316681. doi:https://doi.org/10.1016/j.physleta.2017.01.047.