11email: sme@tpu.ru, 11email: master.daulet@gmail.com

Portfolio Risk Assessment using Copula Models111Submitted to the International Conference on Applied Research in Economics, Perm, Russia, 2017

Abstract

In the paper, we use and investigate copulas models to represent multivariate dependence in financial time series. We propose the algorithm of risk measure computation using copula models. Using the optimal mean- portfolio we compute portfolio’s Profit & Loss series and corresponded risk measures curves. Value-at-risk and Conditional-Value-at-risk curves were simulated by three copula models: full Gaussian, Student’s and regular vine copula. These risk curves are lower than historical values of the risk measures curve. All three models have superior prediction ability than a usual empirical method. Further directions of research are described.

Keywords: value-at-risk, risk assessment, optimal portfolio, vine copula, multivariate dependence.

1 Introduction

Common measures of risk used in risk management are "value at-risk" () and "conditional value at-risk" () which can be determined for different levels of significance. In the paper [25] it is shown that in the presence of a correlation of profits and losses series of assets, one-dimensional risks’ measures and assess the portfolio risk incorrectly. Therefore, to assess the portfolio risk, it is necessary to use -dimensional measures determined through the multivariate dependence.

There are many different approaches that actively used in applications to represent multivariate dependence, for instance, principal component analysis, Bayesian networks, fuzzy techniques, factor analysis, and joint distribution function [17, 24]. The dependence among the random variables , is completely described by the joint distribution function . The idea of separating in two parts – the one which describes the dependence structure, and the other one which describes the marginal behavior, leads to the concept of copula. In 1959 A. Sklar [36] first proved the theorem that a collection of marginal distributions can be coupled together via a copula to form a multivariate distribution. The copula contains all the information about the dependence structure of the involved variables. In the paper [32] the author introduced copula-models’ concepts and its application to the different financial issues including the task of risk measurement.

Many ways to describe financial data using Gaussian (normal) distribution exist today. It is well known [41] that a full Gaussian copula, i.e., a Gaussian copula constructed by Gaussian (normal) marginals, is another way to describe Markowitz’s mean-variance portfolio theory. On the other hand, a lot of empirical studies have shown that Gaussian distribution has a lot of problem in dependence description of financial data [33, 27, 40]. Moreover, in the standard [12] is proposed that Gaussian copulas are not to be used for operational risk modelling. For instance, a Student’s copula with few integer degrees of freedom (three or four) in most cases appears more appropriate. Closed-form expressions to calculate the sensitivity of the risk measure, , were proposed in the paper [37].

The primary objective of this paper is to compare the financial risk measures in framework of portfolio management by deriving the relevant parameters of the copula models from prices of traded assets.

Studies [41, 28, 1, 24] of price risks in framework of portfolio management in many respects are similar to each other and differ only in the used data and insignificant variations in the copula models estimation. Among set studies, we single out the paper by Ane et al [1] that was one of the first where authors selected the dependence structure of international stock index returns through the Clayton copula. Lourme et al [28] address the issue of testing the the full Gaussian and Student’s copulas in a risk management framework. They proposed the -dimensional compact Gaussian and Student’s confidence area inside of which a random vector with uniform margins on falls with probability . The results evidence that the Student’s copula model is an attractive alternative to the Gaussian one. A portfolio of stocks, bonds and real estate was considered [24] to determine the importance of selecting the right copula for risk management. The Gaussian, the Student’s and the Gumbel copulas to model the dependence of the daily returns on indexes that approximate these three asset classes were tested. Then with Value-at-Risk computations was established that the Gaussian copula is too optimistic on the diversification benefits of the assets, while the Gumbel copula is too pessimistic.

Estimation of the unknown parameters is an important problem. At present, many algorithms for constructing copulas have been designed. For copula model estimation, there exist three methods: the full parametric method [31], the semiparametric method [6, 28], and the nonparametric method [13, 22]. The full parametric method is implemented via two-stage maximum likelihood estimation (MLE) proposed by H. Joe [19, 20]. The copula is fitted using the two-stage parametric MLE approach, also referred to as the Inference Functions for Margins (IFM) method. This method fits a copula in two steps: (1) estimate the parameters of the marginals, and (2) fix the marginal parameters to the values estimated in first step, and subsequently estimate the copula parameters.

For the the bivariate case, the main families of copulas are: ellipse (Gaussian, Student’s ), archimedean (Clayton, Frank, Joe), and extreme (Gumbel, Cauchy). In the dissertation research [41], the two-stage MLE method was applied, while the author uses all possible combinations of different marginal distributions (Gaussian, the Student’s , and skewed distribution) and different archimedian copulas in the estimation and testing process. The decision of choosing the marginal distribution is taken after the second step of MLE method. For this purpose, a modification of the superior predictive ability of the Hansen test [15] was proposed; it allows one to identify a copula that has superior forecasting ability.

Multivariate copulas based on the one distribution (for instance, normal or Student’s ) or on one the generator function lack the flexibility of accurately modeling the dependence among larger numbers of variables [5]. These lacks predetermined the direction of further research, as a result of which the regular vine copulas’ (R-vine) concept was proposed by Joe [18] and developed in more detail in [5, 9]. R-vine copulas are a flexible graphical model for describing multivariate copulas built up using a cascade of bivariate copulas (two-dimensional function). This copula is easier to be interpreted and visualized, and we have a lot of methods to work with it today [9, 10, 11]. For instance, in the study [11] a novel algorithms for evaluating a regular vine copula parameters and simulating from specified R-vines were proposed. The selection of the R-vine tree structure based on a maximum spanning tree algorithm (MST), where edge weights are chosen appropriately to reflect large dependencies.

In this paper, we perform the computation of the copula models on the four time series of closing daily prices of futures. We use the two-stage maximum likelihood estimation by Joe [19, 20] for the copula models.

The contributions of this article are threefold. First, we show that full Gaussian and Student’s as well as regular vine copula models can be used to represent multivariate dependence in short finance time series (253 observations only). While the impact of copulas has been studied in relation to long time series [24, 28, 11]. Second, we use non-normal marginal distributions: the Hyperbolic [2], stable Paretian [33] and Meixner [35] distributions, as the possible forms of marginal distributions. Stoyanov et al [37] address this issue, but only consider the symmetric stable Paretian, and the Student’s , and generalized normal distributions. Third, constructing the regular vine copula model the we use non-integer degrees of freedom for two-parameter copulas that substantially extends the possibility of copulas’ models in framework of portfolio risk management.

In order to compare the performances of the different risk measures (, ), we propose to use the Monte-Carlo simulation on the mean-CVaR optimal portfolio. The advantage of the portfolio optimization is that one can formulate the mean- portfolio optimization problem as a linear programming problem [34]. We plot and compare the historical Profit & Loss series with and curves at the different levels estimated through copula models.

The rest of the paper is arranged as follows. In Section 2, we introduce the methodology and the dataset, on which our approach has been tested. In Section 3 we calculate future portfolios, and examined the financial risk measures on the proposed portfolios. Finally, the conclusion is included.

2 Dataset and Methodology

2.1 Dataset

In this research, we examine time series of closing daily prices of stock futures for companies: MMC Norilsk Nickel PJSC (GMKR), Gazprom PJSC (GAZP), Sberbank PJSC (SBER) respectively, and the future on RTS index (RTS). Our sample covers the period of one year from to December 16, 2015, to December 16, 2016. Denote them as GMKR, GAZP, SBRF and RTS respectively. All that data regarding the futures prices were collected from the Finam Holdings service (finam.ru).

2.2 Data Processing

First, we have converted an initial data set to logarithmic returns (log-returns) so that we could use a stable data set that can be used for time series modeling and subsequent transformation. Equation (1) transforms a price series into a log-returns series for each asset:

| (1) |

where , is the number of assets, is a time point, in our case , .

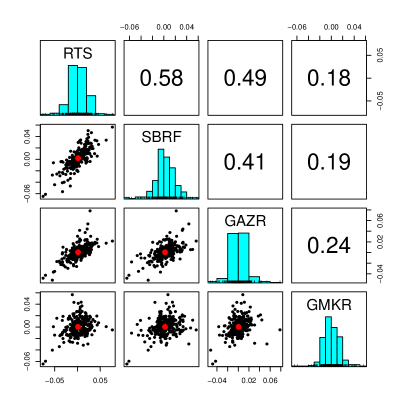

Since we are going to deal with financial time-series, which has a nonlinear dependence, we use rank correlation coefficients: Kendall’s and Spearman’s . In further calculations, we used Kendall’s [11]. Correlation matrices are shown in Table 1.

| Spearman’s | Kendall’s | |||||||

|---|---|---|---|---|---|---|---|---|

| log-returns | RTS | SBRF | GAZP | GMKR | RTS | SBRF | GAZP | GMKR |

| RTS | 1 | 0.78 | 0.67 | 0.27 | 1 | 0.58 | 0.49 | 0.18 |

| SBRF | 0.78 | 1 | 0.58 | 0.29 | 0.58 | 1 | 0.41 | 0.19 |

| GAZP | 0.67 | 0.58 | 1 | 0.35 | 0.49 | 0.41 | 1 | 0.24 |

| GMKR | 0.27 | 0.29 | 0.35 | 1 | 0.18 | 0.19 | 0.24 | 1 |

2.3 Estimate the parameters of the marginals

Many ways to describe financial data using Gaussian (normal) distribution exist today [21]. On the other hand, a lot of empirical studies have shown that Gaussian distribution has a lot of problem in description of financial data [33, 27, 40]. Various non-normal distributions have been proposed for modeling extreme events, we choose the Hyperbolic [2], Stable [30, 33, 37] and Meixner [35] distributions as the three possible forms of marginal distributions. For the sake of brevity, the well-known formulae corresponding to the three possible forms of marginal distributions are not reported here, but are available in [2, 30, 33, 37, 35].

A hyperbolic distribution is four parameter distribution [2] that determines with is the steepness of the distribution, determines the symmetry, the distribution is symmetrical about the location parameter if , and is the scale parameter. A stable distribution is described by four parameters [33, 30, 37]. The parameters and their meaning are: , which determines the tail weight or the distribution’s and a kurtosis, , which determines the distribution’s skewness, is a scale parameter, and is a location parameter. A Meixner distribution has four parameters: is the location parameter, is the scale parameter, is the skewness parameter, and is the shape parameter [35].

The first two parameters of mentioned above distributions are the most important as they identify two fundamental properties that are atypical of the normal distribution –– heavy tails and asymmetry [37]. Parameters for hyperbolic distribution have been estimated by the Nelder-Mead method, for the stable and the Meixner distribution –– by the Cramér–von Mises distance. The results obtained for the log-returns are shown in Table 2.

| Parameters | RTS | SBRF | GAZP | GMKR \bigstrut | |

|---|---|---|---|---|---|

| Hyperbolic | 0.08291 | 0.12785 | 0.06765 | 0.24050 | |

| 1.83534 | 0.00317 | 0.67834 | 0.01527 | ||

| 0.01918 | 0.00004 | 0.00618 | 0.00017 | ||

| 0.00445 | 0.00123 | 0.00090 | 0.00479 | ||

| Stable | 1.86195 | 1.80091 | 1.85290 | 1.75151 | |

| 0.19345 | 0.90962 | 0.84324 | 0.87382 | ||

| 0.01236 | 0.01019 | 0.00816 | 0.00920 | ||

| 0.00160 | 0.00072 | 0.00059 | 0.00153 | ||

| Meixner | 0.01925 | 0.02726 | 0.02209 | 0.00464 | |

| 0.47214 | 0.68221 | 0.26678 | 2.12144 | ||

| 1.74613 | 0.67245 | 0.69809 | 4.22827 | ||

| 0.00575 | 0.00345 | 0.00158 | 0.03413 | ||

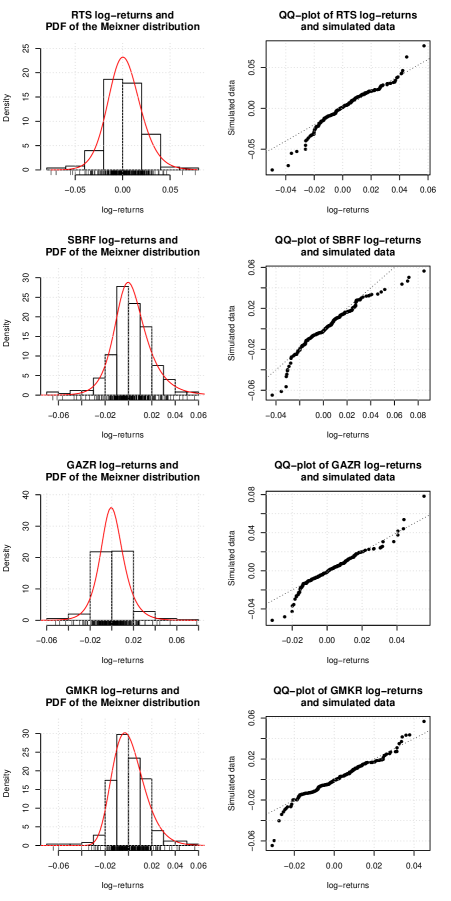

We computed the Kolmogorov–Smirnov (KS) test, Anderson–Darling (AD) test and Cramér–von Mises (CvM) test between the empirical marginals and the fitted marginals, the associated -values are reported in Table 3, respectively. Since in all the cases the -values are quite high, it indicates that the proposed marginal distributions are indeed a good model for data set. According to results of the CvM test, we take the Mexiner distribution as the marginal for each underlying asset (denoted by grey in Table 3). Fig. 1 shows comparison of each observations set and corresponding distribution on the histogram and the - plot, respectively.

| Test | Marginal | RTS | SBRF | GAZP | GMKR \bigstrut |

|---|---|---|---|---|---|

| Kolmogorov–Smirnov | Hyperbolic | 0.73 | 0.14 | 0.96 | 0.25 |

| Stable | 0.89 | 0.83 | 0.98 | 0.96 | |

| Meixner | 0.92 | 0.86 | 1.00 | 0.97 | |

| Anderson–Darling | Hyperbolic | 0.69 | 0.39 | 0.98 | 0.22 |

| Stable | 0.70 | 0.26 | 0.72 | 0.73 | |

| Meixner | 0.49 | 0.52 | 0.98 | 0.00 | |

| Cramér–von Mises | Hyperbolic | 0.65 | 0.34 | 0.98 | 0.22 |

| Stable | 0.78 | 0.73 | 0.99 | 0.89 | |

| Meixner | 0.81 | 0.79 | 1.00 | 0.95 |

2.4 Estimate the copula parameters

At this stage, we suggest the constructing of copula using two type of copula models: multivariate copula and regular vine (R-vine) copula. For the sake of brevity, the known formulae corresponding to the copulas are not reported here, but are available in [29, 20, 10, 9].

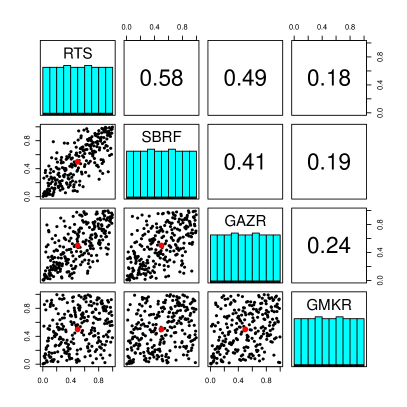

First, we should generate points of the empirical copula, called as pseudo-observations. Considering Eq. (1) for all historical observations (log-returns) , then pseudo-observations are defined via the Eq. (2):

| (2) |

where denotes the rank of (from lowest to highest) of the observed values [16]. Each element is between and . Pairs plots of the joint distribution of observed data and the pseudo-observations are shown on Fig. 2.

In this study we use elliptical copulas of two families: Gaussian (normal) and Student’s copulas. To estimate the copula parameters we use pseudo-observations Eq. (2). The decision of choosing the copula parameters is taken by <<Inversion of Kendall’s tau>> method [23]. Then we execute a parametric bootstrap-based goodness-of-fit (GoF) test of elliptical copulas to check their quality [14]. Estimated parameters and the test results are shown in Table 4. As one can see the parameters of elliptical copulas and results of GoF test are very close each to other.

The negative side of using multivariate copula model is that we can not (a) check the quality, and (b) construct the cumulative distribution function of Student’s copula with non-integer degrees of freedom. Alternative way to construct copula models is using R-vine copulas. As we know from [3], a -dimensional vine is a copula constructed of usual bivariate copulas. The main advantage of this type of models is that each component copula of vine represents a pair-copula (two-dimensional function). This copula is easier to be interpreted and visualized, and we have a lot of methods to work with it today [9, 10, 11].

Following the study [11] we use absolute empirical Kendall’s as a measure of dependence, since it makes it independently of the assumed distribution. We use the same method [23] to estimate the parameters as we did it with multivariate copulas. Also, we can use non-integer degrees of freedom for copulas with two parameters. In addition, we choose different families for each pair [38, 8, 4]. Using abbreviations for copula types: – Survival Gumbel, – Survival Clayton, – Survival Clayton-Gumbel, – Joe-Clayton, – independence copula, the estimated R-vine copula is given by [10]:

| (10) |

where is the matrix of the R-vine array structure, numbers 1, 2, 3, and 4 denote the log-returns of RTS, SBRF, GAZP, GMKR series respectively, is the matrix containing information about family and parameters of each bivariate (one- or two parameter) copula of R-vine.

| Copula | Parameters | GoF test results \bigstrut | |

| Statistic | -value \bigstrut | ||

| Gaussian | 0.00495 \bigstrut | ||

| Student’s | 0.00495 \bigstrut | ||

| R-vine | see Eq. (10) | 0.95 \bigstrut | |

| –- the correlation copula parameter, \bigstrut[t] | |||

| –- degrees of freedom of Student’s copula. \bigstrut[b] | |||

To check the estimated parameters, we use a goodness fit tests based on the Cramer-von Mises statistic, , [23] and the White’s information matrix equality, , [39]. The result of test implementation is shown in Table 4. As one can see the -values of elliptical copulas are less than corresponding -value of the R-vine copula.

3 Portfolio Application

In this section, we present some simulation results to compare the performances of the Value-at-Risk () and the Conditional Value-at-Risk () on an equally weighted portfolio composed of assets. Then we applied the above results to compute the optimal weights of each asset, which is one of the major concerns in the field of portfolio risk management.

3.1 Mean-Conditional-Value-at-Risk Portfolio Optimization

The advantage of the portfolio optimization is that we can formulate the mean- portfolio optimization problem as a linear programming problem [34]. If we can find a portfolio with a low , then it will also have a low [7]. We assume a "full investment" portfolio with only long positions, furthermore, to avoid a corner portfolio case, let the minimal weight be limited by . The mean- portfolio weights we obtained are , , , and for RTS, SBRF, GAZP, and GMKR respectively.

Now let us compare and of equally weighted and mean-CVaR optimal portfolio obtaining for historical scenario by empirical methods [34]. Take as a level for and computation. It is clear from the simulation results (Table 5) that values of risk measures for optimal portfolio are distinctively better, as expected. We will considering further the optimal portfolio only.

| Level, % | \bigstrut | |||||

|---|---|---|---|---|---|---|

| Optimal | Equiweighted | Bias \bigstrut | ||||

| 99.9 | / | / | / | \bigstrut[t] | ||

| 99.5 | / | / | / | |||

| 99.0 | / | / | / | |||

| 95.0 | / | / | / | |||

| 90.0 | / | / | / | \bigstrut[b] | ||

3.2 Efficient Algorithm of Risk Measure Computation using Copula Models

Now we propose the following algorithm based on Monte-Carlo simulation of pseudo-observations to compute the risk measures. Here we use the estimation results of the copula models (Section 2, Tables 2, 4).

Algorithm 1 represents the method we used to compute and . Method is based on Monte-Carlo simulation of pseudo-observations using proposed copula models with estimated parameters. In order to generate random samples (line 2) we used Gaussian and Student’s copula parameters (Table 4) and the R-vine array structure, Eq. (10). Then we transform each univariate pseudo-observation series to quantiles: (lines 3–11). In order to implement the transformation we take a quantile of each log-returns series using simulated pseudo-observations throw all dimensions of the copula as probabilities (line 8). Using optimal mean- portfolio weights we compute portfolio’s Profit & Loss series (line 14) and risk measures (line 16).

The obtained results for VaR and CVaR are shown in Table 6 and 7 respectively. As we can see, we have all negative values of bias for vine copula. It means, that we will not loose more than we predict by this model. Thus, we can say that the R-vine copula model has superior forecasting ability than the Gaussian and the Student’s one.

| Level, % | Empirical, | Simulated, | Bias, \bigstrut | ||||

|---|---|---|---|---|---|---|---|

| 99.9 | / | / | / | / | \bigstrut[t] | ||

| 99.5 | / | / | / | / | |||

| 99.0 | / | / | / | / | |||

| 95.0 | / | / | / | / | |||

| 90.0 | / | / | / | / | \bigstrut[b] | ||

| Level, % | Empirical, | Simulated, | Bias, \bigstrut | ||||

|---|---|---|---|---|---|---|---|

| 99.9 | / | / | / | / | \bigstrut[t] | ||

| 99.5 | / | / | / | / | |||

| 99.0 | / | / | / | / | |||

| 95.0 | / | / | / | / | |||

| 90.0 | / | / | / | / | \bigstrut[b] | ||

3.3 Stability Study and Risk Measure Curve

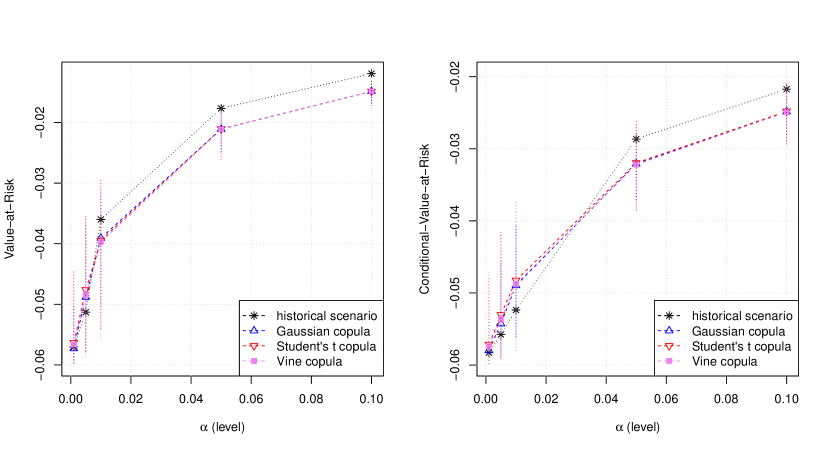

Now let us make a stability research of proposed method. For this, we make bootstrap procedure replicating Algorithm 1. The obtained results are shown in Table 8, 9 and illustrated on Fig. 3.

We report the bias, the standard deviation (SD) and the mean square error (MSE) based on replications. The bias value is better at lower levels: 99%, 95%, 90% for , and 95%, 90% for . The SD and the MSE metrics show the greater instability of vine copula related to Gaussian (the most stable one) and Student’s model.

Level, % Bias, SD, MSE, \bigstrut 99.9 / / / / / / / / \bigstrut[t] 99.5 / / / / / / / / 99.0 / / / / / / / / 95.0 / / / / / / / / 90.0 / / / / / / / / \bigstrut[b]

Level, % Bias, SD, MSE, \bigstrut 99.9 / / / / / / / / \bigstrut[t] 99.5 / / / / / / / / 99.0 / / / / / / / / 95.0 / / / / / / / / 90.0 / / / / / / / / \bigstrut[b]

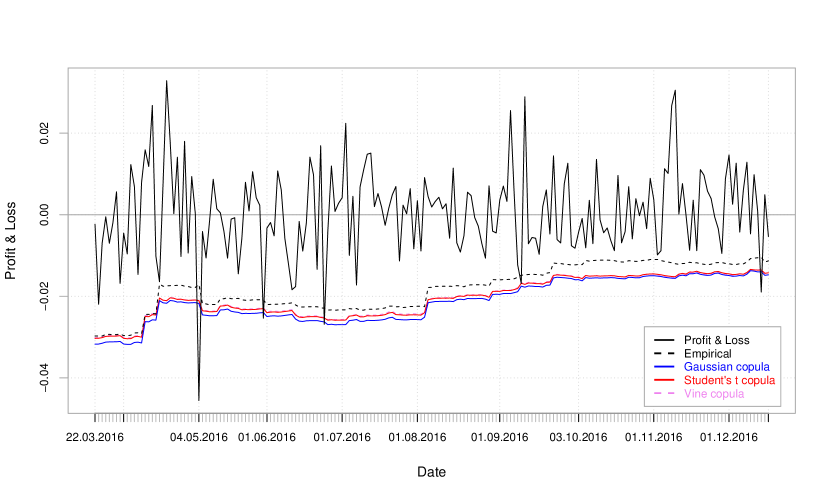

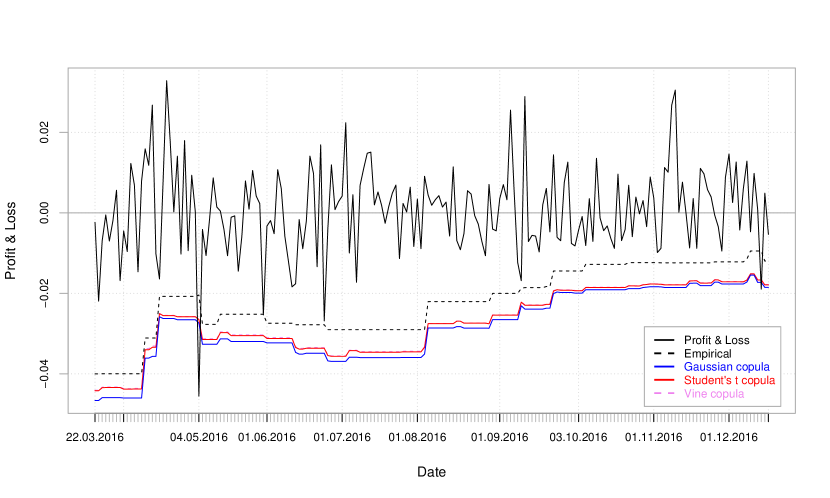

Fig. 4 and 5 show the dynamics of Profit & Loss series and the movement of 95%-level and respectively. and curves simulated by copula models are lower than a historical value. The -values of the Kupiec’s test [26] for all proposed copula models are greater than the critical level . All three models have superior prediction ability than usual empirical method.

4 Conclusion

In the paper we have examined copula models as an approach to describe multivariate dependence in time series to compare the financial risk measures in framework of portfolio management. Throughout this paper we make use of time series of closing daily prices of stock futures for companies: MMC Norilsk Nickel PJSC (GMKR), Gazprom PJSC (GAZP), Sberbank PJSC (SBRF) respectively, and the future on RTS index (RTS) during a period of one year from to 17 December, 2015 to 16 Devember, 2016 (four series composed of 253 observations).

We used the two-stage parametric maximum likelihood estimation approach and two copula models – multivariate copula and regular vine (R-vine) copula – have been fitted. We choose the four-parameter hyperbolic, stable and Meixner distributions as the three possible forms of marginal distributions.

Multivariate finance data has been analyzed using three possible distribution models, and it is observed that the all proposed models provide a quite satisfactorily fit to the above data set. According to results of the Cramér–von Mises test, we take the Mexiner distribution as the marginal for all underlying assets.

Using the "Inversion of Kendall’s tau" method we estimated the parameters for multivariate Gaussian, Student’s , and R-vine copulas and then we executed the parametric bootstrap-based goodness-of-fit test. The estimated R-vine copula is given by six pairs based on the Survival Gumbel, the Survival Clayton, the Survival Clayton-Gumbel, the Joe-Clayton and the Independence copulas. By analyzing the full Gaussian, Student’s and R-vine copulas for the risk management of a portfolio of futures, we find that the impact of copula selection is large. The tests do not reject the R-vine copula, but do reject the Gaussian and Student’s copula.

We proposed the algorithm based on Monte-Carlo simulation of pseudo-observations to compute the and of the optimal portfolio. and curves simulated by copula models are lower than a historical value. All three copula models have superior prediction ability than a usual empirical method.

The further research of our study can be continued in the following directions. At first, we will compute the associated 95% confidence intervals of the the unknown parameters. At second, we will also investigate the usage the set of spanning trees (for instance, top-10 spanning trees) instead of using just the one maximum spanning tree in the selection of the R-vine array structure. At third, we will show how one can detect and exclude arbitrage opportunity and avoid these in method of generation scenario trees using copula models. Thereby, we will be consistent with financial asset pricing theory.

References

- [1] Ané, T., Kharoubi, C.: Dependence structure and risk measure. Journal of Business 76(3), 411–438 (2003)

- [2] Barndorff-Nielsen, O., Blæsild, P.: Hyperbolic distributions. Encyclopedia of Statistical Sciences 3, 700–707 (1983)

- [3] Bedford, T., Cooke, R.: Vines – a new graphical model for dependent random variables. Annals of Statistics 30(4), 1031–1068 (2002)

- [4] Belgorodski, N.: Selecting pair-copula families for regular vines with application to the multivariate analysis of European stock market indices. Diploma thesis, Technische Universitaet Muenchen (2010), http://mediatum.ub.tum.de/?id=1079284

- [5] Brechmann, E.C., Schepsmeier, U.: Modeling dependence with C- and D-Vine copulas: The R package CDVine. Journal of Statistical Software 52(3), 527–556 (2013)

- [6] Chen, X., Fan, Y.: Estimation of copula-based semiparametric time series models. Journal of Econometrics 130, 307–335 (2006)

- [7] Cho, W.N.: Robust portfolio optimization using conditional value at risk. Final report, Imperial College London (2008)

- [8] Clarke, K.: A simple distribution-free test for nonnested model selection. Political Analysis 15, 347–363 (2007)

- [9] Cooke, R., Kurowicka, D., Wilson, K.: Sampling, conditionalizing, counting, merging, searching regular vines. Journal of Multivariate Analysis 138, 4–18 (2015)

- [10] Czado, C.: Pair-copula constructions of multivariate copulas, p. 93–109. Springer (2010)

- [11] Dißmann, J., Brechmann, E., Czado, C., Kurowicka, D.: Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics & Data Analysis 59(1), 52–69 (2013)

- [12] European Banking Authority: Final Draft RTS on AMA Assessment for Operational Risk. Tech. rep., European Banking Authority (June 2015), https://www.eba.europa.eu/documents/10180/1100516/EBA-RTS-2015-02+RTS+on+AMA+assesment.pdf

- [13] Fermanian, J., Scaillet, O.: Nonparametric estimation of copulas for time series. Journal of Risk 5(4), 25–54 (2003)

- [14] Genest, C., Rémillard, B., Beaudoin, D.: Goodness-of-fit tests for copulas: A review and a power study. Insurance: Mathematics and Economics 44, 199–214 (2009)

- [15] Hansen, P.: A test for superior predictive ability. Journal of Business and Economic Statistics 23, 365–380 (2005)

- [16] Hofert, M., Kojadinovic, I., Maechler, M., Yan, J.: Copula: Multivariate Dependence with Copulas (2017), https://cran.r-project.org/package=copula

- [17] Huynh, V.N., Kreinovich, V., Sriboonchitta, S.: Modeling Dependence in Econometrics: Selected Papers of the Seventh International Conference of the Thailand Econometric Society, Faculty of Economics, Chiang Mai University, Thailand, January 8-10, 2014. Advances in Intelligent Systems and Computing 251, Springer International Publishing, 1 edn. (2014)

- [18] Joe, H.: "Families of m-Variate Distributions with Given Margins and m(m-1)/2 Bivariate Dependence Parameters", Distributions with Fixed Marginals and Related Topics, pp. 212–248. Institute of Mathematical Statistics, Hayward (1996)

- [19] Joe, H.: Multivariate Models and Dependence Concepts. Chapman & Hall, London (1997)

- [20] Joe, H.: Dependence modeling with copulas. Taylor & Francis Group (2014)

- [21] Johnson, N.L.: Systems of frequency curves generated by methods of translation. Biometrika 36, 149–176 (1949)

- [22] Kim, G., Silvapulle, M., Silvapulle, P.: Comparison of semiparametric and parametric methods for estimating copulas. Computational Statistics & Data Analysis 51, 2836–2850 (2007)

- [23] Kojadinovic, I., Yan, J.: Comparison of three semiparametric methods for estimating dependence parameters in copula models. Insurance: Mathematics and Economics 47, 52–63 (2010)

- [24] Kole, E., Koedijk, K., Verbeek, M.: Selecting copulas for risk management. Journal of Banking & Finance 31(8), 2405–2423 (2007)

- [25] Kritski, O., Ulyanova, M.: Assessment of multivariate financial risks of a stock share portfolio. Applied Econometrics 4(8), 3–17 (2007)

- [26] Kupiec, P.H.: Techniques for verifying the accuracy of risk measurement models. Journal of Derivatives 3(2), 73–84 (1995)

- [27] Limpert, E., Stahel, W.A.: Problems with using the normal distribution – and ways to improve quality and efficiency of data analysis. PLoS ONE 6(7), 1–8 (2011)

- [28] Lourme, A., Maurer, F.: Testing the Gaussian and Student’s t copulas in a risk management framework. Economic Modelling (2016), http://dx.doi.org/10.1016/j.econmod.2016.12.014

- [29] Nelsen, R.: An Introduction to Copulas. Lecture Notes in Statistics. Springer, New York (1999)

- [30] Nolan, J.P.: Stable Distributions – Models for Heavy Tailed Data. Birkhauser, Boston (2009)

- [31] Patton, A.: Modeling asymmetric exchange rate dependence. International Econometric Review 47, 527–556 (2006)

- [32] Penikas, H.: Financial applications of copula-models. Journal of the New Economic Association 7, 24–44 (2010)

- [33] Rachev, S.T., Menn, C., Fabozzi, F.J.: Fat-Tailed and Skewed Asset Return Distributions: Implications for Risk Management, Portfolio Selection, and Option Pricing. John Wiley & Sons, Hew Jersey (2005)

- [34] Rockafellar, R.T., Uryasev, S.: Optimization of conditional value-at-risk. Journal of Risk 2(3), 21–41 (2000)

- [35] Schoutens, W.: Meixner processes: Theory and applications in finance. Eurandom Report 2002-004, Eindhoven, Eindhoven, Netherlands (2002)

- [36] Sklar, A.: Fonctions de repartion a n dimension et leurs marges. Universite de Paris 8, 229–231 (1959)

- [37] Stoyanov, S., Rachev, S., Fabozzi, F.: CVaR sensitivity with respect to tail thickness. Journal of Banking & Finance 37(3), 977–988 (2013)

- [38] Vuong, Q.H.: Ratio tests for model selection and non-nested hypotheses. Econometrica 57(2), 307–333 (1989)

- [39] White, H.: Maximum likelihood estimation of misspecified models. Econometrica 50, 1–26 (1982)

- [40] Wilmott, P.: Frequently Asked Questions in Quantitative Finance. John Wiley & Sons, Ltd (2007)

- [41] Xu, Q.: Estimating and Evaluating the Archimedean-Copula-Based Models in Financial Risk Management. Dissertation thesis, Massey University, New Zealand, Auckland (2008)