OPTION PRICING WITH DELAYED INFORMATION

We propose a model to study the effects of delayed information on option pricing. We first talk about the absence of arbitrage in our model, and then discuss super replication with delayed information in a binomial model, notably, we present a closed form formula for the price of convex contingent claims. Also, we address the convergence problem as the time-step and delay length tend to zero and introduce analogous results in the continuous time framework. Finally, we explore how delayed information exaggerates the volatility smile.

Keywords: Delayed information, binomial model, continuous-time limit, incomplete market, super replication, volatility smile.

1 Introduction

All participants in financial markets have access only to delayed information. Delay adds more uncertainty to the market, and it is of great importance to study it. A universal assumption in options pricing literature is that a trader makes his decisions with full access to the prices of the assets (i.e, no delayed information). However, in practice, there is a lag between when the order is decided and its execution time. In particular, there are two important types of delays in financial markets. First is the delay in order execution, that is, the order would be executed with some delay after the trader places it. For example, if the order is made in the morning, it would be executed in the afternoon. Second is the delay in receiving information, that is, the trader observes the prices and other important information with some delay, usually because of the technological barriers, exacerbated by having long physical distance from the exchange.

In the view of traders, these two types of delays act similarly. In both cases, orders are executed with prices which are unknown at the time they are made. In other words, the source of the delayed information does not change the decisions of the trader. For example, let be a discrete trading horizon. If there exists a delay with length of period, then regardless of what the source of delay is, no trade happens at time , and in later times trades happen based on the information available up until the previous period. The reason is that if the delay is only in receiving information, then, at time the trader does not have any information, so he waits till time to get time- prices to make a trade and those trades would of course be executed with time- prices. If the delay is only in order execution, then at time- and based on time- prices, the trader makes an order, but that order would be executed with time- prices.

In this work, we start with the binomial model proposed by Cox et al., (1979) and consider fixed periods of delay in the flow of information. Therefore, agents have an information stream smaller than the information flow of the traded asset. We show that the market with delayed information is incomplete, and it is not possible to perfectly replicate most contingent claims. Incomplete markets pose various challenges and for a review of different approaches, we refer to Staum, (2007). We take the worst case scenario approach, that is super replication, to price and replicate convex contingent claims. This approach is first suggested by El Karoui and Quenez, (1995) in their seminal paper. We derive recursive and closed-form formulas for pricing convex contingent claims in the discrete time model. Later, we study the continuous time limit as the time-step and delay length tend to zero. We show that the price process under our pricing measure converges to the Black-Scholes price process, but with enlarged volatility.

A very interesting aspect of our model is the way it shows how delayed information affects the volatility smile. Our model confirms the intuition of traders that delayed information would exaggerate the volatility smile, but it does not cause it. We show that in the continuous limit, volatility is constant and there is no smile, but in the discrete model, we can observe volatility smile. In other words, it suggests the idea that the smile observed in the market might not all be by the market itself, and it could have been exaggerated because of the way we interact with delayed information.

Our model with delayed information has some similarities with the models with transaction costs, notably in both models, we encounter similar limit theorems and both risky asset price processes converge to the Black-Scholes price process with some enlarged volatility. In other words, enlarging volatility can be considered as the way to take into account both transaction costs and delayed information. Leland, (1985) is first to discuss transaction costs in option pricing models. Boyle and Vorst, (1992) studies transaction costs in binomial models, and Kusuoka, (1995) provides rigorous limit theorems for such models. Some recent works in this area are Bank and Dolinsky, (2016), Bank et al., (2017) and Dolinsky and Soner, (2016) For extensive literature on option pricing with transaction costs, we refer to Kabanov and Safarian, (2009).

Kabanov and Stricker, (2006) provides an absence of arbitrage condition in discrete time models with delayed information. Kardaras, (2013) studies market viability in scenarios that the agent has delayed or limited information. Also, Bouchard and Nutz, (2015), Burzoni et al., 2016a and Burzoni et al., 2016b are some very related works in discrete time arbitrage theory.

In the literature, in markets with delayed information, risk-minimizing hedging strategies, which is another hedging approach in incomplete markets, have been studied. Using this approach, Di Masi et al., (1995) models lack of information by letting the assets to be observed only at discrete times, and Schweizer, (1994) presents the general case of restricted information. Some other works in this direction are Frey, (2000), Mania et al., (2008), Kohlmann and Xiong, (2007) and Ceci et al., (2017).

The paper is organized as follows. In section 2, we set up the discrete time model with delayed information and define the super-replication price. We discuss the super-replicating strategy in an -period binomial model with periods of delay in subsection 2.4, and we generalize the results to an -period binomial model with periods of delay in subsection 2.5 using both dynamic programming and direct approaches. A geometrical representation of the strategy is presented in subsection 2.6. In section 3, we study the asymptotic behavior of the model as the time step and delay length tend to zero. In particular, subsection 3.2 is devoted to the discussion of how delayed information affects the volatility smile.

2 Discrete Time Model

Before introducing delays, let us recall the -period binomial tree model of Cox et al., (1979) for a financial market with a single risky asset and a single risk-free asset (e.g., stock). Given , let us denote by a probability space for the canonical space of -period binomial tree with the Borel -algebra generated by . For every we define a coordinate map by for each . Let be the probability measure under which , are independent, Bernoulli random variables with , . Define the filtration , where is the -field generated by the first variables for and is the trivial -field, i.e., .

In the -period binomial tree model, the risky asset price and its discounted price , discounted by instantaneous rate , at time , are defined by

| (2.1) |

where is a given initial price of risky asset at time , and (or ) is a fixed ratio by which the price process goes up (or down) in one period with . The price processes are adapted to the filtration .

2.1 Delayed Filtration

We shall introduce delays in the flow of information in the -period binomial model. For simplicity, let us consider the situation where an investor sends buy or sell orders to the market at time , but her orders are not executed until time with delay periods. The investor herself knows that she has delay periods when she is sending orders. Then we define the delayed filtration , where , for , and

| (2.2) |

In other words, is the information set of the price process until time , rather than time . In the following, we shall consider investments based on this delayed information.

Let be the set of all -adapted stochastic processes with , . Here, each represents a strategy for this investor based on the delayed information, that is, the positive (the negative , respectively) corresponds to the total number of shares of the risky asset that the investor decides to own (to owe, respectively) at time , given information . In other words, the order made at time to buy or sell shares of the risky asset, gets executed at time with price (not ), because of periods of delay. Thus the investor has to deal with the risk of price changes between the time of order submission and execution.

For an initial investment of in the risk free asset and a strategy , we shall consider the portfolio value process , , . The first order submitted at time is executed at time , and the portfolio value process is not observed until time . Thus we define

| (2.3) |

and in general

| (2.4) |

For , the first term in the portfolio value process () in (2.4) corresponds to the initial investment in the risk free asset. The second term () is due to the cash flow in the risk free asset up until time , and the third term () relates to the investment in the risky asset at time . We call , the value process from the strategy .

By construction, the changes in the portfolio value process () in (2.4) starting from its first realization at time , are only due to the variation in asset prices. In other words, no money is added to or withdrawn from the portfolio.

Note that the initial portfolio value in (2.3) is a random variable, not a constant. This is because it is defined by discounting the time- portfolio value , which is the first time the portfolio value is observed due to the existence of delay.

For , is -measurable, but is -measurable. Thus is -measurable for . In this sense, the portfolio is constructed based on the delayed information.

2.2 Absence of Arbitrage

We shall first introduce the notion of arbitrage in our model. In general, arbitrage means that one cannot reap any benefit for free, that is without taking any risk. In our model with delayed information, as it is shown in (2.3), the initial portfolio value is a random variable, because of the existence of delay. Therefore, we need to adjust the classical notion of arbitrage in the domain of strategies, to take this into account.

Definition 2.1 (Arbitrage).

An arbitrage opportunity is the strategy such that

| (2.5) | |||||

The primary difference with the classical definition of arbitrage is the condition that the maximum of time- portfolio value needs to be zero (). It is obvious that in the case of complete information (i.e, ), this definition boils down to the classical definition of arbitrage opportunity.

We need to show that there is no arbitrage in our discrete time model with delayed information. Kabanov and Stricker, (2006) proves that in a general discrete time model with restricted information, there does not exist classical arbitrage, if and only if there exists a probability measure equivalent to such that the optional projection under of the discounted stock price on the delayed filtration, is a -martingale The setup of our model is a bit different than that in Kabanov and Stricker, (2006), given that our first order to buy/ sell the risky asset is executed at time , rather than at time (i.e. , ). This makes the initial portfolio value () a random variable, rather than always a constant. Theorem 2.1 shows that still in our model, there does not exists arbitrage, in the sense of Definition 2.1.

Theorem 2.1.

There does not exists any arbitrage opportunity in our discrete time model, in the domain of strategies.

Proof.

According to Definition 2.1, absence of arbitrage means that for any strategy such that , the condition implies that .

In the domain of , according to (2.3), the condition is equivalent to

which means that in all -period binomial models starting from time , the initial values for the strategy are non-positive.

If we consider all these -period binomial models individually, they lie in the general discrete time model framework in Kabanov and Stricker, (2006). Therefore, in each of these models, even if we consider the initial values of the strategy to be zero, the condition implies , given that we show that there exists a probability measure such that the -optional projection of the discounted stock price on the delayed filtration, is a -martingale, that is

| (2.6) |

Define the probability measure such that the coordinate maps are still independent Bernoulli random variables, but with parameters

which are the risk-neutral probabilities in the usual binomial model without any delay.

Remark 2.1.

The domain of strategies in Theorem (2.1) does not include all -adapted strategies, but only those which are -adapted. In other words, we are excluding the case that an agent with full information comes and exploits the advantage over the investors with delayed information in the market. If we include all -adapted strategies, it is likely to have arbitrage opportunities.

2.3 Super-Replication Price

Given that there is no arbitrage in the market, it now makes sense to discuss about pricing.

Definition 2.2 (Super-replication price and the value process of super-replicating portfolio).

For any contingent claim with payoff function and expiration time , its super-replication price is defined as the minimal initial value of portfolio which exceeds the value at time , i.e.,

| (2.7) |

where

| (2.8) |

If there exists a pair that attains the infimum in (2.7), i.e., , then the time- super replicating portfolio value is defined as

| (2.9) |

and consequently, .

Remark 2.2.

The super-replication price is the most conservative pricing approach for the seller of the option, considering the worst-case scenario. In other words, it is straightforward to show that any price greater than the super-replication price causes arbitrage in the market.

Remark 2.3.

It is remarkable to note that call-put parity does not hold anymore. The reason is that the super-replication price is a coherent risk measure on the space of payoff functions, and therefore it is subadditive.

All of the results in this paper are for European-style contingent claims with convex payoff functions. In section 2.4, we consider first the case and determine the super-replication price and the corresponding strategy. This would make the building block for the general case discussed in section 2.5. The case for non-convex payoff functions is computationally more demanding as we do not have access to all the machinery developed for convex functions.

2.4 An -period binomial model with periods of delay

We determine the super-replication price and the corresponding strategy for the European contingent claims when . Having periods of delayed information means that at time the risky asset price is observed, but the order , sent by the investor at time , would be executed at time . For example, when and , the order sent at time is executed at time with two possible prices or (see Figure 1).

Let us observe that in the case of , the terminal value in (2.4) is simplified to

| (2.10) |

There are possible values of , in (2.1) and there are only two controls in the terminal value. Since there are constraints and only two controls, the minimization problem in (2.7) has possibly infinitely many solutions. In other words, in an economic sense, the market is not complete. To learn more about pricing in incomplete markets, we refer to Staum, (2007).

Theorem 2.2.

For a European-style contingent claim with payoff for some convex function in the -period binomial model with periods of delay, the super-replication price is

| (2.11) |

where the corresponding strategy is given by , ,

| (2.12) |

Proof.

First, we shall prove that for any , in (2.12) satisfies

| (2.13) |

Here the infimum is taken over the set in (2.8), that is, and must satisfy almost surely. Note that in (2.10) is realized as the value at of linear function with the slope and the -intercept in the coordinates. Moreover, since the payoff function is convex, by Jensen’s inequality, one can verify

That is, in order to check whether the inequality holds with probability one, it suffices to check it just at the extreme cases, in which the asset price at time is the minimum or the maximum in the binomial tree model. Then it is easy to check that the choice in (2.12) belongs to the set as we have , . In other words, the minimization problem is reduced to a linear programming problem

Define the Lagrangian as

where and are the Lagrangian multipliers. Then, it is easy to check that the quantities

satisfy the Karush-Kuhn-Tucker conditions for the minimization. Hence, (2.13) follows, and it is the key to prove that

| (2.15) |

Thus, we get

| (2.16) |

Then, the proof is completed by the following observation

∎

By using Theorem 2.2, the portfolio value in (2.9) at time of the super-replicating strategy can be calculated as

| (2.18) |

Here are probability measures on defined by

Remark 2.4.

We can conclude from the form in (2.4) that , the value of the super-replicating portfolio at time , is a function of and . In other words

Therefore, the value process for the super-replicating portfolio is path dependent, due to the existence of periods of lag between the times of order submission and execution.

Thus, the super-replication price can be calculated as

| (2.20) |

where the third equality follows similarly as in (2.4).

Notation: From now on, we use as and as , since and correspond to the measures at the extreme points and respectively.

2.5 An -Period binomial Model with Periods of Delay

We extend our considerations from section 2.4 and generalize the model to the -period binomial model with periods of delay. We determine the super-replication price and the corresponding strategy for European style contingent claims with convex payoff functions. Here we shall solve the problem from both a dynamic programming (or backward induction) approach and a direct approach.

2.5.1 Dynamic Programming Approach

First, let us define the tree of length as the set of nodes , such that there are ups and downs from the node with , i.e.,

Then define its -period subtree starting from the node at time by

for every such that .

We shall identify all subtrees starting from the nodes at time (i.e, ). We use the results in section 2.4 and consider the value process of the super-replicating portfolio at time as the new payoffs for the next round of ()-period subtrees starting from the nodes at time . Then, we keep super-replicating backwards in the same manner.

Remark 2.5.

Therefore, let us define the payoff for the subtree starting from the node at time at its leaf node (i.e, ) by

for , and , where .

Intuitively, for the subtree starting at time , there are only two -period subtrees, and , starting at time that can induce payoff at time . So, we need to take the maximum of the two possible value process as the new payoff because we always consider worst case scenario in super replication. Note that at the edge points, there exists only one value process.

Example 2.1.

In the -period binomial tree model (as in Figure 2) with , what new payoff we need to consider on the node depends on whether we are considering this node as part of the subtree or . As part of the subtree , the payoff would be the maximum of the corresponding value processes of the subtrees and , while as part of the subtree , the payoff would be the corresponding value processes of the subtrees .

One important ingredient in the dynamic programming approach is that when we start from a convex payoff function, the payoff in (2.5.1) for all the intermediary -period subtrees needs to be convex with respect to the corresponding risky asset prices, in order to be able to use Theorem (2.2) in each step and keep super-replicating backwards. Theorem (2.3) formalizes this relation.

Theorem 2.3.

For a European-style contingent claim with payoff for some convex function in the -period binomial model with periods of delay, the payoff function , in (2.5.1) for all the intermediary -period subtrees are convex with respect to the corresponding risky asset prices.

Proof.

Note that for , the payoff functions for all intermediary -period subtrees are convex, since the final payoff function is convex.

Now we show that all the payoff functions , will be convex, if all the payoff functions , are convex. By induction this completes the proof.

Given that the payoff function is convex, by Theorem (2.2), there exists and such that we define

Similarly, there exists and such that we define

we can define

| (2.31) |

Note that where , given that is convex, and (2.5.1).

The discrete function is convex if for any and such that , we have

| (2.32) |

where , and .

Depending on the choice of and , there are 4 cases:

Case 1: and . Then, given the form in (2.31), we have . Then, it is straightforward to show that (2.32) follows by linearity of the function .

Case 2: and . This case follows similar to that of case 1.

Case 3: and . Then, would equal to either or . Without loss of generality assume that . Then given that , we conclude by the form in (2.31) that . So, we derive

where the last inequality follows by the linearity of the function.

Case 4: and . This case follows similar to that of case 3.

∎

Therefore, given Theorem (2.3), we can apply the dynamic programming approach, and derive the portfolio value in (2.21) at level , of the super-replicating strategy, using representation (2.4), as

| (2.33) | |||

where and , are defined as in (2.4).

Plugging in (2.5.1) for , we obtain the key recursive formula

| (2.34) | |||

Remark 2.6.

Therefore, similar to (2.4), the super-replication price can be finally calculated as

| (2.35) |

2.5.2 Direct Approach

In this section, we solve the recursive equation (2.5.1) and obtain the value process for the super-replicating strategy explicitly. As Remark (2.6) suggests, when we super-replicate backwards, we just need the value process at the extreme points, that is and , .

Define probability spaces for with , the Borel -algebra on , and . For every , we define a coordinate map by for each .

Let be the probability measure under which with initial position is a Markov chain, and for , it has transition matrix

| (2.38) |

Besides, for ,

The risky asset price satisfies

| (2.40) |

Remark 2.7.

Under measures , , is the probability of an upward move preceded with an upward move, is the probability of a downward move preceded with an upward move, is the probability of an upward move preceded with a downward move, and is the probability of a downward move preceded with a downward move. Besides, equations (2.5.2) are to ensure that the last moves are all either upward or downward.

Remark 2.8.

Under measures , , probability of a downward move preceded by a downward move () is higher than the probability of a downward move preceded by an upward move (). Similar is also true for upward moves. So, the variance of the risky asset price is higher under these measures than the initial measure .

Remark 2.9.

Theorem (2.4) expresses and , as expectations under the measure .

Theorem 2.4.

For a European-style contingent claim with payoff for some convex function , , the value process and , for the super-replicating strategy, in an -period binomial model with periods of delay, can be calculated as

| (2.41) |

| (2.42) |

Proof.

We need to show that (2.41) and (2.42) satisfy the recursive equation (2.5.1) for , and equation (2.5.1) for . For , it is already shown in (2.4), and for , by conditioning on , (2.41) satisfies

Note that by the way the spaces and are constructed,

Also, and . Therefore,

which completes the proof. Similarly, it can also be shown for (2.42). ∎

Remark 2.10.

If we are interested just to find out the time- super-replication price , we only need the probability space where . Then, we would have

| (2.43) |

Lemma 2.1, whose proof can be found in the appendix, calculates , . For . Define

| (2.44) |

Also for , define

| (2.45) | |||||

Lemma 2.1.

For a function , , the conditional expectation can be explicitly calculated as

| (2.46) |

where is given by

| (2.56) |

Similarly, Lemma 2.2 calculates , . Also for , define

| (2.57) | |||||

For , define

| (2.58) |

Lemma 2.2.

For a function , , the conditional expectation can be explicitly calculated as

| (2.59) |

where is given by

| (2.69) |

Proof.

The proof follows very similarly as that of Lemma 2.1 with only this difference that since , we look for upward groups instead of downward groups. ∎

2.6 Geometrical Representation

In this subsection, we first discuss Theorem 2.2 from a geometrical perspective Then, we represent the dynamic programming approach in subsection 2.5.1 geometrically For convenience, assume that interest rate , and in this subsection.

In Theorem 2.2, we discussed that in an -period binomial model with periods of delay, for a European-style convex contingent claim with payoff function , there exist and such that

| (2.70) |

This suggests that there exists a line with slope and intercept such that the super-replicating value function lie on that line. Figure 3 shows this optimal line, the super-replication price, and the super-replicating value functions in a -period binomial model with period of delay.

It is more intuitive to demonstrate the dynamic programming approach in subsection 2.5.1 geometrically. Figure 2 shows a -period binomial model with -period delay. Figure 4 shows how to geometrically find the super-replication price for a contingent claim with convex payoff function (). For convenience and to avoid a clutter of points on the -axis, suppose , so some of the points in the model lie on each other.

Now in order to find the super-replication prices at time , it is necessary to consider the three -period binomial models with -period delay , and . In Figure 4, the lines (), () and () show the optimal super-replication lines for each of these models respectively. As it can be seen, there are two payoffs at either of the nodes and depending on which subtree is used for pricing (i.e. depending on what is). Now, we go one period further back to find out the payoffs at time . We need to consider two -period models and . Note that in each of these two models, the corresponding payoff at nodes (out of two payoffs and ) and (out of two payoffs and ) needs to be chosen. As Theorem (2.3) suggests, the payoff functions for both of these models are convex. The lines () and () demonstrate the optimal lines for these models. Similarly, to calculate the payoff at time , the -period model needs to be used and the line () shows the optimal line for this model. Finally, we have the super-replication price .

3 Continuous Time Model

In this section, we discuss the asymptotic behavior of the model. We define the probability spaces , such that , and is the Borel -algebra on . For every , we define a coordinate map by for each . Define the filtration , where is the -field generated by the first variables for and is the trivial -field.

Let , , (fixed time horizon) and define the sequences

| (3.1) |

where the order , as in Donsker’s theorem.

Remark 3.1.

characterizes the number of periods we have delayed information, which is constant in the asymptotic analysis. However, is the amount of time we have delayed information, which should vanish in the limit. Otherwise, the super-replication price would explode and converge to the maximum of the contingent claim payoff function.

3.1 Price Process Asymptotic

Define the probability measures , similar to (2.38) and (2.5.2), such that with initial position is a Markov chain, and for , it has transition matrix

| (3.4) |

Besides, for ,

where and are defined, similar to (2.4) with , as

| (3.6) |

Then, the risky asset price , similar to (2.1), satisfies

| (3.7) |

where . The following Lemma 3.1 provides asymptotic for and .

Lemma 3.1.

We have

| (3.8) | |||

| (3.9) |

Proof.

The proof simply follows by applying Taylor’s expansion to , and , and plugging them in (3.6). ∎

Discretize the time interval by setting . By interpolating over the intervals in a piecewise constant manner with (, ), we get the risky asset price process

| (3.10) |

where is the floor function.

The process has trajectories which are right continuous with left limits. Note that in particular

Here, under measure is distributed according to a probability measure on the Skorokhod space of right continuous functions with left limits. Theorem 3.1 provides a weak convergence for the sequence .

Theorem 3.1.

The sequence of processes converges in distribution to the process with dynamics

| (3.11) |

where is a Brownian motion, and we have the enlarged volatility

| (3.12) |

Proof.

First, note that

According to Lemma 3.1, we conclude that

where in the notation of Gruber and Schweizer, (2006)

Now we apply a functional central limit theorem for generalized, correlated random walks in Gruber and Schweizer, (2006) with and for their Theorem 1 and Remark 3. It follows from the continuous mapping theorem that , regardless of the initial distribution of , converges in distribution to in (3.11). In particular, since , we see the volatility

is constant, and larger than , where .

∎

Remark 3.2.

The enlarged volatility in the limit is due to the gap in (3.1) which is caused because of the delay in the flow of information (it would be zero when the number of delayed periods ). In fact, this is the main source making the price process under the pricing measure more volatile.

3.2 Exaggerated Volatility Smile

In this subsection, we discuss the volatility smile of the model, and how it evolves with the number of periods (). Volatility smile is the graph of Black-Scholes implied volatility with respect to the strike price. Implied volatility is the value of the volatility in the Black-Scholes pricing model which generates a price equal to that of our model. Several market features, such as crashphobia, have been attributed as the culprits of the market smile. The volatility smile has been one of the central topics in option pricing literature, and many models have been developed to capture it. We refer to Gatheral, (2011) for more discussion in this regard.

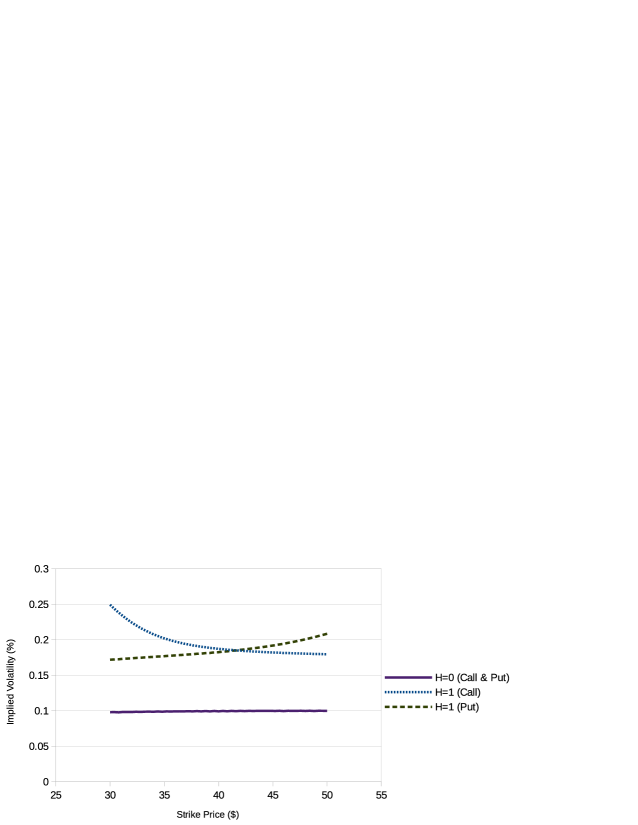

Our model with delayed information shows that delayed information exaggerates the smile. Figure 5 plots the volatility smiles for call and put options in the model with and without delayed information when . In the model with delayed information (), we observe volatility smile, on the contrary with the model without delayed information where we get an almost flat smile, which is expected according to the Remark 2.9. Note that in the model with delayed information, we have different smiles for call and put option, and that is because there is not any call-put parity, as discussed in Remark 2.3.

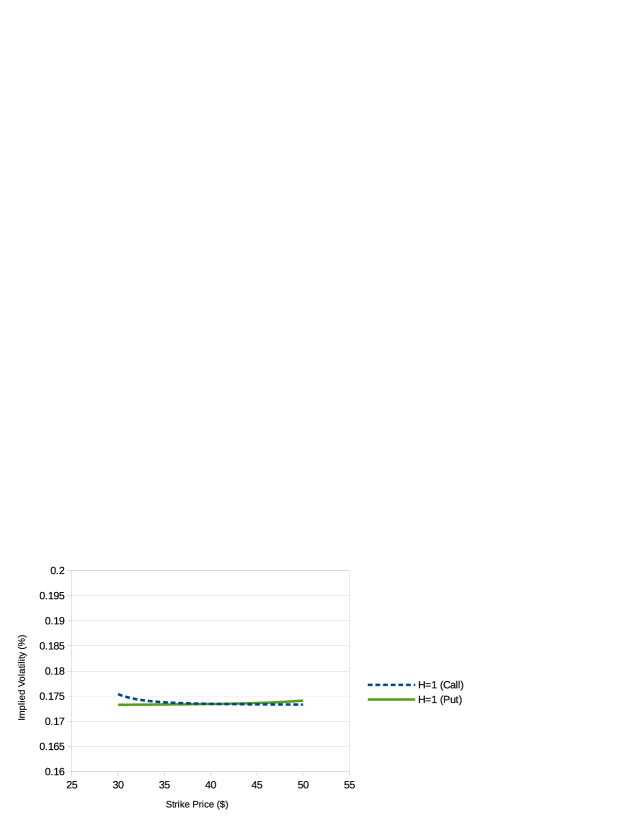

Figure 5 plots the volatility smiles for call and put options when the number of periods is very big () for the model with delayed information (). We observe almost the same flat volatility smiles for both call and put options, which can be also calculated by the theoretical results in 3.12.

These volatility smiles in Figures 5 and 6 confirm the intuition of traders that delayed information would exaggerate the volatility smile, but it is not its culprit. This is because in the continuous limit, volatility is constant and there is no smile, but in the discrete model, we can observe volatility smile. Therefore, it conveys that the smile observed in the market might have been exaggerated by the way we interact with delayed information, and the smile might not be caused all by the market itself.

Appendix A Proof of Lemma 2.1

Proof.

Note that , is the sum of several products of elements chosen out of , and each product term corresponds to a path in the tree starting from the node , and ending in the node .

Given equations (2.5.2), the last moves need to be either upward or downward, and they contribute to as just one single move. Since it is conditioned on , according to Remark (2.7), the first element in all of the product terms is either or . For , the last ()-period move to can be both downward and upward.

In the case that it is upward, we need to consider all the paths starting from to which consist of upward moves and downward ones. There are of such paths, but these paths are not all equivalent and result in different product terms of elements chosen out of , based on the location of the downward moves in the path.

Note that all paths which have the same number of downward groups result in the same product terms, where a downward group is any number of consecutive downward moves preceded (if any) by an upward move and also succeeded (if any) by an upward move. For example, both of the sequences and have two groups of moves. The reason for studying downward groups is that the starting element in all of them is .

In this notation, corresponds to the number of groups which starts from (assuming that there exists at least one downward move) and can reach to . Notice that there are paths which have exactly groups. Therefore, along those path the power of both and is and consequently, the powers of and are respectively and . Here in equation (2.44) corresponds to these paths.

The second case is that the last ()-period move is downward. Then, we need to consider all the paths starting from the node to which consist of upward moves and downward ones. Here not only the number of downward moves is important, but also the direction (upward or downward) of the move from time to is also relevant.

Note that there are paths which have exactly groups such that the last -period move from to is downward, so the corresponding product term is , and there are paths which have exactly groups such that the last -period move from to is upward. The function in equation (2.45) takes all these paths into account.

For , it is necessary to use both and to take into account that the last ()-period move can be both upward and downward. The same reasoning works for and , but here the last ()-period move can only be downward for and upward for . For when the last ()-period move is downward and , the functions and cannot be used because in all of the paths from to , there is not any downward move at all to make a downward group (i.e., ). ∎

References

- Bank and Dolinsky, (2016) Bank, P. and Dolinsky, Y. (2016). Super-replication with fixed transaction costs. arXiv preprint arXiv:1610.09234.

- Bank et al., (2017) Bank, P., Dolinsky, Y., and Perkkiö, A.-P. (2017). The scaling limit of superreplication prices with small transaction costs in the multivariate case. Finance and Stochastics, 32:487–508.

- Bouchard and Nutz, (2015) Bouchard, B. and Nutz, M. (2015). Arbitrage and duality in nondominated discrete-time models. Annals of Applied Probability, 25(2):823–859.

- Boyle and Vorst, (1992) Boyle, P. P. and Vorst, T. (1992). Option replication in discrete time with transaction costs. Journal of Finance, 47(1):271–293.

- (5) Burzoni, M., Frittelli, M., Hou, Z., Maggis, M., and Obłój, J. (2016a). Pointwise arbitrage pricing theory in discrete time. arXiv preprint arXiv:1612.07618.

- (6) Burzoni, M., Frittelli, M., and Maggis, M. (2016b). Universal arbitrage aggregator in discrete time markets under uncertainty. Finance and Stochastics, 20(1):1–50.

- Ceci et al., (2017) Ceci, C., Colaneri, K., and Cretarola, A. (2017). The föllmer–schweizer decomposition under incomplete information. To appear in Stochastics, pages 1–35.

- Cox et al., (1979) Cox, J. C., Ross, S. A., and Rubinstein, M. (1979). Option pricing: A simplified approach. Journal of Financial Economics, 7(3):229–263.

- Di Masi et al., (1995) Di Masi, G., Platen, E., and Runggaldier, W. (1995). Hedging of options under discrete observation on assets with stochastic volatility. In Seminar on Stochastic Analysis, Random Fields and Applications, pages 359–364. Springer.

- Dolinsky and Soner, (2016) Dolinsky, Y. and Soner, H. M. (2016). Convex duality with transaction costs. Mathematics of Operations Research, 42(2):448–471.

- El Karoui and Quenez, (1995) El Karoui, N. and Quenez, M.-C. (1995). Dynamic programming and pricing of contingent claims in an incomplete market. SIAM journal on Control and Optimization, 33(1):29–66.

- Frey, (2000) Frey, R. (2000). Risk minimization with incomplete information in a model for high-frequency data. Mathematical Finance, 10(2):215–225.

- Gatheral, (2011) Gatheral, J. (2011). The volatility surface: a practitioner’s guide, volume 357. John Wiley & Sons.

- Gruber and Schweizer, (2006) Gruber, U. and Schweizer, M. (2006). A diffusion limit for generalized correlated random walks. Journal of Applied Probability, 43(01):60–73.

- Kabanov and Safarian, (2009) Kabanov, Y. and Safarian, M. (2009). Markets with transaction costs: Mathematical Theory. Springer Science & Business Media.

- Kabanov and Stricker, (2006) Kabanov, Y. and Stricker, C. (2006). The Dalang–Morton–Willinger theorem under delayed and restricted information. Séminaire de Probabilités XXXIX In Memoriam Paul-André Meyer, 209–213. Springer.

- Kardaras, (2013) Kardaras, C. (2013). Generalized supermartingale deflators under limited information. Mathematical Finance, 23(1):186–197.

- Kohlmann and Xiong, (2007) Kohlmann, M. and Xiong, D. (2007). The mean-variance hedging of a defaultable option with partial information. Stochastic Analysis and Applications, 25(4):869–893.

- Kusuoka, (1995) Kusuoka, S. (1995). Limit theorem on option replication cost with transaction costs. Annals of Applied Probability, pages 198–221.

- Leland, (1985) Leland, H. E. (1985). Option pricing and replication with transactions costs. Journal of Finance, 40(5):1283–1301.

- Mania et al., (2008) Mania, M., Tevzadze, R., and Toronjadze, T. (2008). Mean-variance hedging under partial information. SIAM Journal on Control and Optimization, 47(5):2381–2409.

- Schweizer, (1994) Schweizer, M. (1994). Risk-minimizing hedging strategies under restricted information. Mathematical Finance, 4(4):327–342.

- Staum, (2007) Staum, J. (2007). Incomplete markets. Handbooks in Operations Research and Management Science, 15:511–563.