Numerical Scheme for Dynkin Games under Model Uncertainty

Abstract.

We introduce an efficient numerical scheme for continuous time Dynkin games under model uncertainty. We use the Skorokhod embedding in order to construct recombining tree approximations. This technique allows us to determine convergence rates and to construct numerically optimal stopping strategies. We apply our method to several examples of game options.

Key words and phrases:

Dynkin Games, Model Uncertainty, Skorokhod Embedding2010 Mathematics Subject Classification:

91A15, 91G20, 91G601. Introduction

In this paper, we propose an efficient numerical scheme for the computations of values of Dynkin games under volatility uncertainty. We consider a finite maturity, continuous–time robust Dynkin game with respect to a non dominated set of mutually singular probabilities on the canonical space of continuous paths. In this game, Player 1 who negatively/conservatively thinks that the nature is also against him, will pay the following payment to Player 2 if the two players choose stopping strategies and respectively,

| (1.1) |

We model uncertainty by assuming that the stochastic processes are path–independent functions of an underlying asset which is an exponential martingale with volatility in a given interval. Thus, our setup can be viewed as a Dynkin game variant of Peng’s G–expectation (see [26]).

For finite maturity optimal stopping problems/games, there are no explicit solutions even in the relatively simple framework where the probabilistic setup is given and the payoffs are path–independent functions of the standard Brownian motion. Hence, numerical schemes come naturally into the picture.

In [1], the authors presented a recombining trinomial tree based approximations for what is now known as a –expectation in the sense of Peng ([26]). However, they did not provide a rigorous proof for the convergence of their scheme and did not obtain error estimates. Moreover, a priori, it is not clear whether the tree approximations from [1] can be applied for optimal stopping problems/games.

In this paper, we modify slightly the trinomial trees from [1]. For the modified (recombining) trees we construct a discrete time version of the Dynkin game given by (1.1). The main idea is to apply the Skorokhod embedding technique in order to prove the existence of an exact scheme along stopping times with the required properties. More precisely, for any exponential martingale with volatility in a given interval we prove that there exists a sequence of stopping times such that the ratio of the martingale between two sequel times belongs to some fixed set of the form and the expectation of the difference between two sequel times is approximately equal to . Here is the right endpoint of the volatility uncertainty interval, is the number of time steps and is the maturity date. This machinery also allows to go in the reverse direction, namely for a given distribution on the trinomial tree we can find a ”close” distribution on the canonical space which lies in our set of model uncertainty.

We prove the convergence of the discrete time approximations to the original control problem. Moreover, we provide error estimates of order . The recombining structure of the trinomial trees allows to compute the corresponding value with complexity where is the number of time steps.

The idea of using the Skorokhod embedding technique in order to obtain an exact sequence along stopping times was also employed in a recent work [2] where the authors approximated a one dimensional time–homogeneous diffusion by recombining trinomial trees (and obtained the same error of order ). In [2], the authors were able to construct explicitly the stopping times. The construction relies heavily on the well established theory for exit times of one dimensional time–homogeneous diffusion processes. This theory cannot be applied in the present work, since the martingales in the volatility uncertainty setup are not necessarily diffusions, or even Markov processes. Thus, the case of model uncertainty requires additional machinery which we develop in Section 3. Moreover, since the martingales may not be Markovian we cannot provide an explicit construction of the stopping times (as done in [2]), but only prove their existence.

Let us remark that the multidimensional version of the above described result is an open question which requires a completely different approach. In particular, it is not clear how to derive recombining tree models which will approximate volatility uncertainty in the multidimensional setup. We leave this challenging question for future research.

Since its introduction in [10], Dynkin games have been analyzed in discrete and continuous time models for decades (see, for instance, [3, 5, 21, 23, 25]). In Mathematical Finance, the theory of Dynkin games can be applied to pricing and hedging game options and their derivatives, see [9, 15, 16, 19, 22] and the references in the survey paper [17]. In particular, the nondominated version of the optional decomposition theorem developed in [24] provides a direct link (as we will see rigorously) between Dynkin games and pricing game options in the model uncertainty framework. In general, the theme of Dynkin games is a central topic in stochastic control.

In [8], the authors connected Dynkin games to backward stochastic differential equations (BSDEs) with two reflecting barriers. This link inspired a very active research in the field of Dynkin games in a Brownian framework, see e.g. [4, 7, 12, 13, 14, 27]. Motivated by Knightian uncertainty, recently there is also a growing interest in Dynkin games under model uncertainty, see [6, 9, 14, 28]). In [6] the authors analyzed a robust version of the Dynkin game over a set of mutually singular probabilities. They proved that the game admits a value. Moreover, they established submartingale properties of the value process. These results will be essential in the present work.

The rest of the paper is organized as follows. In the next section we formulate our main result (Theorem 2.2). In Section 3, we introduce our main tool which is Skorokhod embedding under model uncertainty. In Section 4, we complete the proof of the main result. Section 5 is devoted to some auxiliary estimates which are used in the proof of Theorem 2.2. In Section 6, we provide numerical analysis for several examples of game options. Moreover, we argue rigorously the link between Dynkin games and pricing of game options in the current setup of model uncertainty.

2. Preliminaries and Main Result

Let be the space of continuous paths equipped with the topology of locally uniform convergence and the Borel –field ). We denote by , the canonical process and by , the natural filtration generated by . For any , denotes the set of all stopping times with values in . We denote by the set of all stopping times (we allow the stopping times to take the value ).

For a closed interval and let be the set of all probability measures on under which the canonical process is a strictly positive martingale such that –a.s., the quadratic variation is absolutely continuous a.s. and a.s. Observe that if we define the local martingale , then from Itô Isometry we get . Thus is a true martingale and , is the Doléans–Dade exponential of . In other words, the set is the set of all probability measures (on the canonical space) such that the canonical process (which starts in ) is a Doléans–Dade exponential of a true martingale with volatility in the interval .

From mathematical finance point of view, the set describes the set of all possible distributions of the (discounted) stock price process. We assume that is a finite interval, i.e. . This implies that the set is weakly compact and so we can apply the results form [6] related to the existence of the optimal strategy of the Dynkin game. Moreover, the assumption is essential for constructing an appropriate sequence of trinomial models . In addition, we assume that , in other words the model uncertainty setup is ”noisy enough”. This assumption is technical and will be needed for obtaining uniform bounds on the expectation of the hitting times related to the canonical process.

We consider a Dynkin game with maturity date and a payoff given by (1.1) with , , where satisfy and the following Lipschitz condition

| (2.1) | |||

for some constant .

For any define the lower value and the upper value of the game at time given that the canonical process satisfies

and

From Theorem 4.1 in [6] it follows that the lower value and the upper value coincide and thus the game has a value

| (2.2) |

Our goal is to calculate numerically the value . Moreover, from Theorem 4.1 in [6] it follows that the stopping time is an optimal exercise time for Player 1. In Section 6, we use this formula for numerical calculations of Player 1’s optimal strategy.

Remark 2.1.

Our setup is slightly different from the one considered in [6]. If we use our notations, then the control problem studied in [6] is

| (2.3) |

Theorem 4.1 in [6] shows that the above infimum and supremum can be exchanged. Furthermore, the authors showed that is an optimal stopping time for Player 2 which can be viewed as the holder of the corresponding game option. The term given in (2.3) is the lowest arbitrage free price of the corresponding game option.

Clearly, if we replace by and replace , then the above control problem is equivalent to

| (2.4) |

This is almost the same control problem as we consider, up to the following change. In our setup, on the event Player 1 pays the low payoff while in (2.4) Player 1 pays the high payoff . Still, Theorem 4.1 in [6] can be extended to this setup as well by following the same proof. Furthermore, analogously, the optimal exercise time for Player 1 is given by . Namely, Theorem 4.1 in [6] provides an optimal exercise time for the player which plays against nature. In our setup, this is Player 1 who can be seen as the seller of the game option. The term given by (2.2) is the highest arbitrage free price of the game option.

Next, we describe the trinomial models and the main result. Fix . Let be random variables with values in the set and let be the filtration generated by , . Denote by the set of all stopping times (with respect to the filtration ) with values in the set .

For a given and consider the geometric random walk

Clearly, the process lies on the grid , . Denote by the set of all probability measures on such that for any

| (2.5) | |||

| (2.6) | |||

| (2.7) |

Let us explain the intuition behind the definition of the set . First, we observe that for any and , , i.e. is indeed a probability measure. Moreover, from (2.6)–(2.7) it follows that for any

Hence, is a martingale with respect to any probability measure . Finally, from (2.5)–(2.6) we have that for any and the conditional expectation of the ratio of the square of the return and the time step satisfy

In the above union of intervals, the first interval is exactly the square of the model uncertainty interval , and the second interval vanishing as . This is the reason that we expect that the set will be a good approximation of the set restricted to the interval . We emphasis that although the interval is vanishing, it will be essential for the Skorokhod embedding procedure.

Next, we define the corresponding Dynkin game under model uncertainty. Introduce the lower value and the upper value of the game

and

We argue that the above two values coincide. In [19], the authors proved a similar statement for the setup where the set of probability measures is the set of equivalent martingale measures. However, the only property that was used in their proof is that there exists a a reference measure. Namely, that there exists a measure such that all the probability measures in the model uncertainty set are absolutely continuous with respect to . In our case the probability measures in are defined on a finite sample space which supports the random variables . Thus, there exists a reference measure for the set . For instance, take to be the probability measure for which are i.i.d. and taking the values with the same probability . Following the proof of Theorem 2.2 in [19] we conclude that the lower value and the upper value coincide and so the game has a value

Moreover, by using standard dynamical programming for Dynkin games (see [25]) we can calculate by the following backward recursion. Define the functions

| (2.8) |

For

| (2.9) | |||

where the last equality follows from the fact that the supremum (maximum) on an interval of a linear function (with respect to ) is achieved at the end points. We get that

| (2.10) |

Hence, we see that the computation of is very simple and its complexity is . Next, we formulate our main result.

Theorem 2.2.

There exists a constant such that for all ,

From (2.8)–(2.9) and the backward induction it follows that

for a fixed the function is

continuous. This together with (2.10) and Theorem 2.2 gives immediately the following

Corollary.

Corollary 2.3.

The function is continuous.

3. Skorokhod Embedding under Model Uncertainty

In this section we fix an arbitrary . For any and stopping time (recall that is the set of all stopping times with respect to the canonical filtration) consider the stopping times

| (3.1) | |||

where the infimum over an empty set is equal to . Set

Observe that . As usual, we use the convention to denote a random variable ( is deterministic) that is uniformly (in time and space) bounded after dividing by .

We start with the following lemma.

Lemma 3.1.

Proof.

Denote . From the fact that is a –martingale with volatility bonded away from zero, it follows that . Thus, , –a.s., and from the martingale property we have

Hence,

| (3.5) |

From the Itô isometry and the fact that under , the process is an exponential martingale with volatility less or equal then we obtain

where the last inequality follows from the fact that for . This together with (3.5) yields

| (3.6) |

Next, we notice that for we have , a.s. Moreover, if then a.s. Hence, from the Monotone Convergence Theorem

| (3.7) |

Let be the set of rational numbers. Define the random variable

Clearly, is –measurable. Moreover, from the monotonicity property of and (3.6)–(3.7), we obtain for the stopping time that

Next, for a given initial stock price , we construct an embedding of probability measures . Choose . There exists functions

such that (2.5) holds true with

Recall the canonical space . On this sample space we define a sequence of random variables by the following recursion. Let and be the unique solution of the equation

Recall the definition given by (3.1). For set , and on the event define to be the unique solution of the equation

On the event we set . Define the random variables by

| (3.9) | |||

Observe that on the event we have . Thus, the fact that the volatility interval is bounded away from zero implies that there exists a unique probability measure such that , and that for any , on the random interval a.s.

Lemma 3.2.

The joint distribution of under is equal to the joint distribution of under . Moreover, for any , and

Proof.

For any we have and . Fix . We argue that

| (3.10) | |||

Indeed, from (3.1), the definition of and the martingale property of we get

as required. In particular . Furthermore, from the definition of , we conclude that the joint distribution of is equal to the joint distribution of .

Finally, we estimate . From (3.9) and the inequality

we get

This together with (3.3)–(3.4) and (3.10) yields

| (3.11) | |||

From the Itô isometry and the fact that (under the probability measure ) the volatility of the canonical process is constant (equal to ) on the interval we obtain

Thus, from (3.11) it follows that , and the proof is completed. ∎

4. Proof Theorem 2.2

For simplicity, we assume that the starting time is . For a general the proof is done in the same way. Denote by the initial stock price.

4.1. Proof of the inequality

Proof.

Fix and choose . There exists a probability measure and a stopping time such that

| (4.1) |

From Lemma 3.1 it follows that we can choose a sequence of stopping times such that a.s., for any

and where is given before Lemma 3.1. In words, we apply the Skorokhod embedding technique given by Lemma 3.1 in order to construct a sequence of stopping times such that the ratio of between two sequel times belongs to . Moreover, the expectation of the difference between two sequel times is . The last fact will be used via the Auxiliary Lemmas 5.3–5.4.

Now, comes the main idea of the proof. Recall the geometric random walk and the trinomial models given by the set of probability measures . From (2.5)–(2.7) and the above properties of the probability measure it follows that there exists a probability measure such that the distribution of under equals to the distribution of under . Moreover, using similar arguments as in Lemma 3.2 we obtain that for any , The above two properties give

Hence, we conclude

| (4.2) | |||

The final step is technical. We are using (4.1)–(4.2) in order to bound from above the difference .

Introduce the stopping time . In view of (4.2) there exists a stopping time such that

| (4.3) | |||

Define the stopping time . From (4.1) and (4.3) we obtain that

| (4.4) | |||

From technical reasons we extend the function to the domain by . Clearly, the extended is satisfying the Lipschitz condition given by (2.1) on the domain . We observe that if , then . This together with (2.1), which in particular implies that , and (4.4) gives

| (4.5) | |||

From the definition of the stopping times and it follows that and

Hence, from the Cauchy–Schwarz inequality, the Jensen inequality, Lemma 5.1 and Lemma 5.3 it follows that

| (4.6) | |||

Similarly, from the Itô isometry we obtain

This together with the Jensen inequality, (4.5)–(4.6) and Lemma 5.4 gives that

and by letting we complete the proof. ∎

4.2. Proof of the inequality

Proof.

The proof is very similar to the proof of the first inequality. Fix and choose . We abuse notations and denote by a probability measure in which satisfy

| (4.7) | |||

Recall the definition of and the stopping times given before Lemma 3.2. Denote by the set of all stopping times with respect to the filtration with values in the set . By applying Lemma 3.2 and the same arguments as before (4.2) it follows that

| (4.8) | |||

The equality (4.8) is the cornerstone of the proof. The remaining part is technical, and we use (4.7)–(4.8) to estimate from above the difference . Indeed, from (4.7)–(4.8) it follows that there exists (again we abuse notations) such that

Define the stopping time . Clearly, there exists a stopping time such that

Next, introduce the stopping time . We observe that if then . Thus, similarly to (4.5) we get

Finally, by using the same estimates as in Section 4.1, we obtain that

and by letting we complete the proof. ∎

Remark 4.1.

Let us notice that in the present setup of model uncertainty we get the same error estimates as in the case with no uncertainty which was studied in [2]. The main reason is that Lemma 5.3 which is essential for the proof cannot be improved even for the most simple case where the canonical process is a geometric Brownian motion with constant volatility. Namely, the Skorokhod embedding technique cannot provide error estimates of order better than even for the approximations of American or game options in the Black–Scholes model. For details, see [18]. Fortunately, same estimates can be obtained for the volatility uncertainty setup.

5. Auxiliary Lemmas

In this section we derive the estimates that we used in Section 4. We fix and a probability measure . Furthermore, we fix a sequence of stopping times for which we assume that for any , –a.s.,

and . Observe that the stopping times from both Section 4.1 and Section 4.2 satisfy the above conditions.

We start with proving the following bound.

Lemma 5.1.

Proof.

Clearly, for any ,

Hence, . This together with the Doob inequality gives that

| (5.1) |

Next, we notice that the inequality together with the Itô formula implies that , is a super–martingale. In particular, . Thus, from the Doob inequality and (5.1) we obtain

and the proof is completed. ∎

Next, we prove the following.

Lemma 5.2.

For any , .

Proof.

Choose . From the Burkholder–Davis–Gundy inequality, the inequality and the fact that for it follows that

and the result follows. ∎

We arrive to our next estimate.

Lemma 5.3.

Proof.

Set , . We use the fact that the expectation of the difference between two sequel times equals approximately to the time step. Formally, for any , we have . Hence,

In view of the inequality , it remains to prove that . From the Jensen inequality and Lemma 5.2 it follows that for all . This together with the inequality implies that for all . Thus, from the Burkholder–Davis–Gundy inequality applied to the martingale , , and the inequality , , we obtain

as required. ∎

We end this section with proving the next estimate.

Lemma 5.4.

Proof.

Clearly,

where

We have . Hence, from the bound , Lemma 5.1 and the Jensen inequality it follows that

Next, we estimate . We observe that the stochastic process

is a martingale. Thus, from the Doob inequality, the Cauchy–Schwarz inequality, Lemmas 5.1–5.2 and the above bound on we obtain

From the Jensen inequality we conclude that .

6. Game Options and Numerical Results

In this section we apply Theorem 2.2 and provide numerical analysis for path–independent game options with the payoffs and , , and we set . First (for the above payoffs), we establish the connection between the super–hedging price of game options and Dynkin games, in the model uncertainty setup.

6.1. Game Options

A game contingent claim (GCC) or game option, which was introduced in [16], is defined as a contract between the seller and the buyer of the option such that both have the right to exercise it at any time up to a maturity date (horizon) . We consider the following GCC with Markovian payoffs. If the buyer exercises the contract at time then he receives the payment , but if the seller exercises (cancels) the contract before the buyer then the latter receives . The difference is the penalty which the seller pays to the buyer for the contract cancellation. In short, if the seller will exercise at a stopping time and the buyer at a stopping time then the former pays to the latter the amount given by (1.1).

Next, we introduce the setup of super–hedging for the seller (the buyer setup is symmetrical). Recall the natural filtration, , . We denote by the set of all –predictable processes such that for any , the stochastic (Itô) integral , is well defined and a super–martingale with respect to . We define a hedge for the seller as a triplet which consists of an initial capital , a trading strategy and a stopping time . A hedge is perfect if for any stopping time (for the buyer) we have the inequality

The super–hedging price is defined by

Lemma 6.1.

The super–hedging price is given by Moreover, there exists a perfect hedge with initial capital .

Proof.

As usual, the inequality is immediate. Indeed if is a perfect hedge then from the super–martingale property of , we obtain that for any and

Thus as required.

It remains to show that there exists a perfect hedge with initial capital . We apply Theorem 4.1 in [6] which not only gives the optimal stopping time for the player which plays against nature but also a sub–martingale property up to the optimal time. Once again taking Remark 2.1 into account, for our setup the sub–martingale property becomes a super–martingale property. More precisely, Theorem 4.1 in [6] implies that for the stopping time we have the following property. For any , the process , is a –super–martingale with respect to the natural filtration , .

We apply the nondominated version of the optional decomposition theorem . Since quadratic variation can be defined in a pathwise form then the condition is invariant under equivalent change of measure. Hence the set is a saturated set (using [24] terminology) of martingale measures. Namely, if and is a martingale measure on the canonical space then . Thus, from Theorem 2.4 in [24] it follows that there exists a process such that for any probability measure

| (6.1) |

We claim that is a perfect hedge. Indeed, let be a stopping time for the buyer and . First consider the event . On this event we have (recall the definition of ) and so from (6.1)

Finally, we consider the event . Applying (6.1) and the trivial inequality for all we obtain

and the proof is completed. ∎

Remark 6.2.

It seems that by applying Theorem 4.1 in [6] and the optional decomposition Theorem 2.4 in [24], Lemma 6.1 can be extended to path dependent options as long as the regularity assumptions from [6] are satisfied. Since we are motivated by numerical applications, then for simplicity we considered path–independent payoffs. Still, a challenging open question, is whether Lemma 6.1 can be obtained under weaker (than Lipschitz or uniform type of continuity) regularity conditions.

6.2. Numerical Results

In view of Lemma 6.1 we use Theorem 2.2 and provide a numerical analysis for the super–hedging price of path–independent game options. We assume that the interest rate in the market is a constant , and so the stock price before discounting is given by , where, recall that is the canonical process. The payoffs before discounting are of the form , where . In order to compute the game option price we need to consider the discounted payoffs and so during this section we put , and .

In [11] (see Section 4), the author proved that for game options (with finite or infinite maturity) with continuous path–independent payoffs satisfying

| (6.2) |

the price is non decreasing in the volatility. Thus, (if the above assumption is satisfied) the price under volatility uncertainty which is given by the interval is the same as the price in the complete Black–Scholes market with a constant volatility . The later value can be approximated by the standard binomial models (see [18]). In particular, this is the case for game put options given by

In Table 1, we test numerically the above statement from [11] for game put options. This is done by comparing our numerical results with previous numerics which was obtained in [20] for game put options in the Black–Scholes model.

| Values obtained with | |||||

|---|---|---|---|---|---|

| n = 200 | n = 400 | n = 700 | n = 1200 | Black–Scholes with | |

| 80 | 20.7003 | 20.6719 | 20.6593 | 20.6532 | 20.6 |

| 90 | 12.4932 | 12.4787 | 12.4938 | 12.4683 | 12.4 |

| 100 | 5.00 | 5.00 | 5.00 | 5.00 | 5.00 |

| 110 | 3.7609 | 3.7240 | 3.6862 | 3.6916 | 3.64 |

| 120 | 2.6169 | 2.5897 | 2.5822 | 2.5729 | 2.54 |

Game call options

Next, we deal with game call options given by

We observe that in this case (6.2) is not satisfied and so we expect that the price for the model uncertainty interval will be strictly bigger than the game call option price in the Black–Scholes model with volatility . We take , namely we consider game call options with constant penalty.

First, we compare (Table 2) the option prices under model uncertainty with the prices in the Black–Scholes model (with the highest volatility). Since we could not find previous numerical results for finite maturity game call options in the Black–Scholes model, we compute it by applying the binomial trees from [18]. These trees are ”almost” the same as our trees for the case where the volatility uncertainty interval contains only one point. We observe that for call options the prices in general should not coincide.

| Values obtained under model uncertainty | ||||

|---|---|---|---|---|

| n = 200 | n = 400 | n = 700 | n = 1200 | |

| 80 | 2.0805 | 2.0893 | 2.0847 | 2.0948 |

| 85 | 2.8138 | 2.7964 | 2.8055 | 2.8018 |

| 90 | 3.6553 | 3.5966 | 3.6241 | 3.6064 |

| 95 | 4.5827 | 4.4682 | 4.5050 | 4.4874 |

| 105 | 5.00 | 5.00 | 5.00 | 5.00 |

| 110 | 10.00 | 10.00 | 10.00 | 10.00 |

| 115 | 15.00 | 15.00 | 15.00 | 15.00 |

| 120 | 20.00 | 20.00 | 20.00 | 20.00 |

| Values obtained for Black–Scholes | ||||

| n = 200 | n = 400 | n = 700 | n = 1200 | |

| 80 | 2.0625 | 2.0359 | 2.0244 | 2.0210 |

| 85 | 2.7706 | 2.7301 | 2.7274 | 2.7143 |

| 90 | 3.5066 | 3.4889 | 3.4968 | 3.4798 |

| 95 | 4.3497 | 4.3124 | 4.3056 | 4.2481 |

| 105 | 5.00 | 5.00 | 5.00 | 5.00 |

| 110 | 10.00 | 10.00 | 10.00 | 10.00 |

| 115 | 14.9355 | 14.9304 | 14.9275 | 14.9260 |

| 120 | 19.7812 | 19.7735 | 19.7691 | 19.7669 |

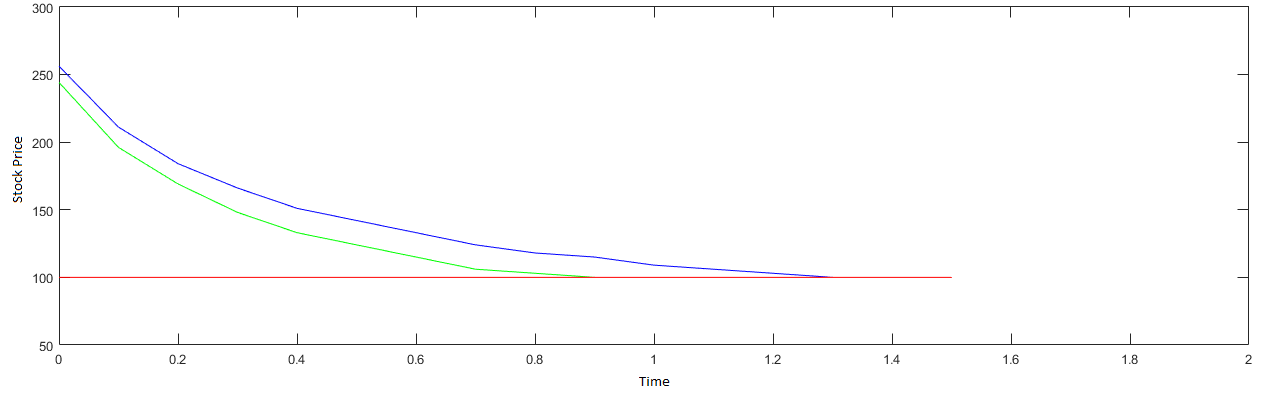

Finally, we calculate numerically the stopping regions. We observe that the discounted payoff , is a sub–martingale with respect to any probability measure in the set . Thus, the buyer’s optimal stopping time is just .

For the seller, the optimal stopping time is (see Theorem 4.1 in [6])

Introduce the function

where as before , is the stock price. The term is the price of a game call option with maturity date and initial stock price . We observe that , where is the stopping region (of course it depends on the maturity date ) given by

In [29], the authors studied the structure of the stopping region for game call options in the complete Black–Scholes market. They proved (see Theorem 4.2) that the stopping region is of the form

where and can be computed numerically.

In Figure 1 we calculate numerically the stopping regions (for the seller) for game call options both in the model uncertainty setup given by the interval and in the complete Black–Scholes model with volatility . We obtain that the structure from [29] is valid for the model uncertainty case as well. Furthermore, for both cases is the same, while and are different. Up to date, there is no theoretical results related to the explicit structure of stopping regions for game options under model uncertainty.

References

- [1] M. Avellaneda , A. Levy and A. Parás, Pricing and hedging derivative securities in markets with uncertain volatilities, Applied Mathematical Finance, 2, 73–88, (1995).

- [2] E.Bayraktar, Y.Dolinsky and J.Guo, Recombining Tree Approximations for Optimal Stopping for Diffusions, to appear in SIAM Journal on Financial Mathematics. arXiv:1610.00554.

- [3] A. Bensoussan and A. Friedman, Nonlinear variational inequalities and differential games with stopping times, J.Functional Analysis, 16, 305–352, (1974).

- [4] R. Buckdahn and J. Li, Probabilistic interpretation for systems of Isaacs equations with two reflecting barriers, NoDEA Nonlinear Differential Equations Appl., 16, 381–420, (2009).

- [5] E. Bayraktar and M. Sîrbu, Stochastic Perron’s method and verification without smoothness using viscosity comparison: obstacle problems and Dynkin games, Proceedings of the American Mathematical Society, 142, 1399–1412, 2014.

- [6] E. Bayraktar and S. Yao, On the Robust Dynkin Game, Appear in Annals of Applied Probability, 27, 1702–1755, (2017).

- [7] E. Bayraktar and S. Yao, Doubly reflected BSDEs with integrable parameters and related Dynkin games, Stochastic Process. Appl., 125, 4489–4542, (2015).

- [8] J. Cvitanic and I. Karatzas, Backward stochastic differential equations with reflection and Dynkin games, Annals of Applied Probability, 24, 2024–2056, (1996).

- [9] Y. Dolinsky, Hedging of Game Options under Model Uncertainty in Discrete Time, Electronic Communications in Probability, 19, 1–11, (2014).

- [10] E. Dynkin, Game variant of a problem on optimal stopping, Soviet Math. Dokl, 10, 270–274, (1967).

- [11] E. Ekström, Properties of game options, Math. Methods Oper. Res 63, 221–238, (2006).

- [12] S. Hamad‘ene, Mixed zero-sum stochastic differential game and American game options, SIAM J. Control Optim., 45, 496–518, (2006).

- [13] S. Hamad‘ene and M. Hassani, BSDEs with two reflecting barriers: the general result., Probab. Theory Relat. Fields, 132, 237–264, (2005).

- [14] S. Hamad‘ene and I. Hdhiri, Backward stochastic differential equations with two distinct reflecting barriers and quadratic growth generator, J. Appl. Math. Stoch. Anal., (2006), pp. Art. ID 95818, 28.

- [15] S. Hamad‘ene and J. Zhang, The continuous time nonzero-sum Dynkin game problem and application in game options, SIAM J. Control Optim., 48, 3659–3669, (2009–2010).

- [16] Y. Kifer, Game options, Finance and Stoch. 4, 443–463, (2000).

- [17] Y. Kifer, Dynkin games and Israeli options, ISRN Probability and Statistics, Volume 2013. Article ID 856458.

- [18] Y. Kifer, Error estimates for binomial approximations of game options, Annals of Appl. Probab. 16, 984–1033, (2006).

- [19] J. Kallsen and C. Kühn, Convertible bonds: Financial derivatives of game type, Exotic Option Pricing and Advanced Levy Models, 277–291. Wiley, New York, (2005).

- [20] C. Kühn, A. Kyprianou and K. van Schaik, Pricing Isreali options: a pathwise approach, Stochastics, 79, 117–137, (2007).

- [21] J.P. Lepeltier and M.A. Maingueneau, Le jeu de Dynkin en théeorie générale sans l’hypothèse de Mokobodski, Stochastics, 13, 25–44, (1984).

- [22] J.Ma and J.Cvitanic, Reflected forward-backward SDEs and obstacle problems with boundary conditions, J. Appl. Math. Stochastic Anal., 14, 113–138, (2001).

- [23] J. Neveu, Discrete–parameter martingales, North–Holland Publishing Co., Amsterdam, revised ed., 1975. Translated from the French by T. P. Speed, North-Holland Mathematical Library, Vol. 10.

- [24] M. Nutz, Robust Superhedging with Jumps and Diffusion Stochastic Processes and their Applications, 125, 4543–4555, (2015).

- [25] Y. Ohtsubo, Optimal Stopping in Sequential Games With or Without a Constraint of Always Terminating, Mathematics of Operations Research, 11, 591–607, (1986).

- [26] S. Peng. Multi-dimensional -Brownian motion and related stochastic calculus under -expectation, Stochastic Process. Appl., 118(12), 2223–2253, (2008).

- [27] M. Xu, Reflected backward SDEs with two barriers under monotonicity and general increasing conditions, J. Theoret. Probab., 20, 1005–1039, (2007).

- [28] J. Yin, Reflected backward stochastic differential equations with two barriers and Dynkin games under Knightian uncertainty, Bull. Sci. Math., 136, 709–729, (2012).

- [29] S.C.P. Yam, S.P. Yung and W. Zhou, Game call options revisted, Mathematical Finance, 24, 173–206, (2014).