Fast model-fitting of Bayesian variable selection regression using the iterative complex factorization algorithm

Abstract

Bayesian variable selection regression (BVSR) is able to jointly analyze genome-wide genetic datasets, but the slow computation via Markov chain Monte Carlo (MCMC) hampered its wide-spread usage. Here we present a novel iterative method to solve a special class of linear systems, which can increase the speed of the BVSR model-fitting tenfold. The iterative method hinges on the complex factorization of the sum of two matrices and the solution path resides in the complex domain (instead of the real domain). Compared to the Gauss-Seidel method, the complex factorization converges almost instantaneously and its error is several magnitude smaller than that of the Gauss-Seidel method. More importantly, the error is always within the pre-specified precision while the Gauss-Seidel method is not. For large problems with thousands of covariates, the complex factorization is 10 – 100 times faster than either the Gauss-Seidel method or the direct method via the Cholesky decomposition. In BVSR, one needs to repetitively solve large penalized regression systems whose design matrices only change slightly between adjacent MCMC steps. This slight change in design matrix enables the adaptation of the iterative complex factorization method. The computational innovation will facilitate the wide-spread use of BVSR in reanalyzing genome-wide association datasets.

doi:

0000keywords:

and

note1Quan Zhou did most of his work when he was a PhD student in the program of Quantitative and Computational Biosciences, Baylor College of Medicine.

fund1 This work was supported by United States Department of Agriculture/Agriculture Research Service under contract number 6250-51000-057 and National Institutes of Health under award number R01HG008157.

1 Introduction

Bayesian variable selection regression (BVSR) can jointly analyze genome-wide genetic data to produce the posterior probability of association for each covariate and estimate hyperparameters such as heritability and the number of covariates that have nonzero effects (Guan and Stephens, 2011). But the slow computation due to model averaging using Markov chain Monte Carlo (MCMC) hampered its otherwise warranted wide-spread usage. Here we present a novel iterative method to solve a special class of linear systems, which can increase the speed of the BVSR model-fitting tenfold.

1.1 Model and priors

We first briefly introduce the BVSR method. Our model, prior specification and notation follow closely those of Guan and Stephens (2011). Consider the linear regression model

| (1) |

where is an column-centered matrix with , denotes an identity matrix of proper dimension, and are -vectors, is an -vector, and MVN stands for multivariate normal distribution. Let be an indicator of the -th covariate having a nonzero effect and write . A spike-and-slab prior for (the -th component of ) is specified below,

| (2) | ||||

where is the proportion of covariates that have non-zero effects and is the variance of prior effect size (scaled by ). We will specify priors for both later. We use noninformative priors on the parameters and ,

| (3) | |||||

where Gamma is in the shape-rate parameterization. As pointed out in Guan and Stephens (2011), prior (3) is equivalent to , which is known as Jeffreys’ prior (Ibrahim and Laud, 1991; O’Hagan and Forster, 2004). In practice, this means to use a diffuse prior for both and . Some may favor a simpler form , which makes no practical difference (Berger et al., 2001; Liang et al., 2008).

Given and , after integrating out , , and letting , , the Bayes factor with reference to the null model can be computed in closed form,

| (4) |

where denotes the submatrix of with columns for which , denotes matrix determinant, and is the posterior mean for given by

| (5) |

The null-based Bayes factor is proportional to the marginal likelihood , and evaluating is easier than evaluating the marginal likelihood due to cancellation of constants. The limiting prior (3) not only makes the Bayes factor expression simpler (compared to that with finite value of and positive values of and ), but also makes it invariant with respect to the shifting and scaling of .

We now discuss the prior specification for the two hyperparameters, and . To specify the prior for , Guan and Stephens (2011) introduced a hyperparameter (which stands for heritability) such that

| (6) |

where denotes the variance of the -th covariate. Conditional on , specifying a prior on will induce a prior on , so henceforth we may write to emphasize is a function of and . Since is motivated by the narrow-sense heritability, its prior is easy to specify and we use

| (7) |

by default to reflect our lack of knowledge of heritability, although one can impose a strong prior by specifying a uniform distribution on a narrow support. A bonus of specifying the prior on through is that when , the induced prior on is heavy-tailed (Guan and Stephens, 2011).

Up till now, we follow faithfully the model and the prior specification of Guan and Stephens (2011). The prior on can be induced by the prior on . Guan and Stephens (2011) specified the prior on as uniform on its log scale, , which is equivalent to for , and sampled . But here we do something slightly different by integrating out analytically. This is sensible because is very informative on . Specifically, we integrate over such that to obtain the marginal prior on ,

| (8) |

where the finite integral is related to the truncated Beta distribution and can be evaluated conveniently. If goes to and goes to we have an improper prior and the marginal prior on becomes

| (9) |

where we recall is the total number of covariates, is the number of selected covariates in the model, and denotes the Gamma function. is always a proper probability distribution because it is defined on a finite set.

1.2 Posterior inference and computation

The joint posterior distribution of is given by

| (10) |

The posterior inferences typically include computing the posterior inclusion probability , which measures the strength of marginal association of the -th covariate, the posterior distribution of the model size , and the posterior distribution of the heritability , which measures the proportion of phenotypic variance explained by the selected models. We use MCMC to sample this joint posterior of . Our sampling scheme follows closely that of Guan and Stephens (2011). In each MCMC iteration, to evaluate (10) for a proposed parameter pair , we need to compute the marginal likelihood , which is proportional to (4). Two time-consuming calculations are the matrix determinant and defined in (5), both of which have cubic complexity (in ). The computation of the determinant can be avoided by using a MCMC sampling trick which we will discuss later. The main focus of the paper is a novel algorithm to evaluate (5), which reduces its complexity from cubic to quadratic.

The rest of the paper is structured as follows. Section 2 introduces the iterative complex factorization (ICF) algorithm. Section 3 describes how to incorporate the ICF algorithm into BVSR. Both sections contain numerical examples, including a real dataset from genome-wide association studies. A short discussion concludes the paper.

2 The iterative complex factorization

In this section, we propose a novel algorithm for solving the following linear system

| (11) |

where is a diagonal matrix with positive (but not necessarily identical) entries on the diagonal, and is an matrix. Clearly (5) is a special case of (11). In the context of BVSR, should be understood as and . We assume , where the sample size ranges from several hundreds to tens of thousands. The computational advancement we will introduce, however, can be applied to scenarios where (see discussion in Section 4).

Note that is the familiar ridge regression estimator (Draper and Van Nostrand, 1979). It may appear that an algorithm designed for solving ridge regression can be borrowed to solve (11). But a unique feature of BVSR is that in each iteration of MCMC, the design matrix usually changes only by one or a few columns. Thus, and its Cholesky decomposition can be obtained conveniently (details will follow). This unique feature allows us to design a much more efficient algorithm.

2.1 Existing methods

In Guan and Stephens (2011), the linear system (11) was solved using the Cholesky decomposition of , which requires flops (Trefethen and Bau III, 1997, Lec. 23). Although computing from requires flops, when only changes by a few columns, the majority of the entries in do not change and updating only requires flops.

Iterative methods sometimes can be used to reduce the computational time. Define

| (12) |

where () is the strictly lower (upper) triangular component and contains only the diagonals. Then three popular iterative procedures can be summarized as follows:

The successive over-relaxation (SOR) method is a generalization of the Gauss-Seidel method, where is called the relaxation parameter. When is positive definite, the Gauss-Seidel method always converges and the SOR method converges for (Golub and Van Loan, 2012, Chap. 10.1.2). For all three iterative methods, each iteration requires flops. Thus, whether an iterative method is more efficient than the Cholesky decomposition depends on how many iterations it takes to converge. Another notable class of iterative methods is called Krylov subspace methods. Two famous examples are the steepest descent and the conjugate gradient (Trefethen and Bau III, 1997, Lec. 38).

In principle, all methods developed to solve ridge regression can be used here to solve (11), as we alluded to earlier. For example, the methods of Eldén (1977), Lawson and Hanson (1995) and Turlach (2006) were developed for solving (11) with fixed but changing , while Hawkins and Yin (2002) devised a method for fixed but changing . Modern least square solvers (Rokhlin and Tygert, 2008; Avron et al., 2010; Meng et al., 2014) typically considered the case where is extremely large, sparse, or ill-conditioned, and under such conditions, these least square solvers outperform solving directly via Cholesky decomposition; see Meng et al. (2014, Sec. 5) for how to apply least square solvers to ridge regression. But all methods quoted above are less effective (or not applicable) in the context of BVSR, because they are not designed for solving (11) millions of times, each time with a slightly different and a different , and they did not take advantage of the feature of BVSR that the Cholesky decomposition of can be obtained efficiently.

2.2 The iterative complex factorization (ICF) algorithm

Let be the Cholesky decomposition of , where is upper triangular. In the context of BVSR, given the Cholesky decomposition of , the Cholesky decomposition of a new matrix can be obtained efficiently since (the proposed new design matrix) differs from only by one or a few columns (see Section 3.1). So we consider solving the linear system

| (13) |

Contrary to our intuition, the Cholesky decomposition of cannot be obtained efficiently. This was also noticed in Zhou et al. (2013, p. 6). We instead perform the following decomposition

| (14) | ||||

where is the imaginary unit. Then we have the update

where the right-hand side is a complex vector, and can be obtained by a forward and a backward substitution involving two complex triangular matrices, and . This update, however, diverges from time to time. Examining the details of the observed divergent cases reveals that the culprit is the imaginary part of . Because the solution is real, discarding the imaginary part of at the end of each iteration will not affect the fixed point to which the iterative method converges. Denoting the real part of a complex entity (scalar or vector) by , the generalized update of our algorithm ICF (Iterative Complex Factorization) becomes

| (15) |

where we have also introduced a relaxation parameter . Intuitively makes the update lazy to avoid over-shooting. The revised update converges almost instantaneously, in a few iterations, compared to a few dozen to a few hundred iterations with the Gauss-Seidel method. Each iteration of (15) requires flops, thrice that required by a Gauss-Seidel iteration, because ICF operates complex (instead of real) matrices and vectors. The right-hand side of (15) can be reorganized as Note that can be computed via forward and backward substitutions and does not require matrix inversion.

2.3 ICF converges to the right target

Proposition 1.

Denote Then ICF in (15) converges for any starting point if where denotes the spectral radius.

Proof.

The true solution satisfies , which, after some algebra, gives . The statement then follows faithfully from Theorem 10.1.1 of Golub and Van Loan (2012). ∎

Theorem 2.

There exists such that the ICF update detailed in (15) converges to the true solution.

Proof.

Using the notation defined in (12) and (14), we have . Since , we have

Using the fact that is invertible, we can solve the above system and obtain

Both and are real matrices, and by the Woodbury identity we have

| (16) |

Immediately, for a fixed , the spectrum of is fully determined by the spectrum of . Because is skew-symmetric, we have . Since is symmetric, so does Then we have , which means is also skew-symmetric. Hence the eigenvalues of , which are identical to those of , are conjugate pairs of pure imaginary numbers or zero. Let be such a pair with and be the eigenvector corresponding to the eigenvalue . We have , which implies , where denotes the conjugate transpose of . Since is a Hermitian positive definite matrix,

Since is also positive definite, we have and

| (17) |

By (16), the eigenvalues of are identical pairs equal to (this includes the case ). Proposition 1 just requires , or equivalently,

| (18) |

holds for all . Thus the existence of follows from (17). ∎

By Proposition 1, the spectral radius of determines how fast the error converges to zero. We provide a theory-guided procedure to adaptively tune the relaxation parameter , which relies on the following proposition that connects with and .

Proposition 3.

Proof.

By (16) and (17), the smallest and the largest eigenvalue of are and with . After adjusting for their signs, we obtain (19). The right-hand side of (19) is a function of , with the first item decreasing linearly in and the second item increasing linearly in . Hence the minimum of (19) is attained when the two quantities in the braces are equal, which proves (20). ∎

Our adaptive strategy for choosing assumes that is zero, which holds trivially for odd by the property of skew-symmetric matrices. When is even, our numerical studies found is still a valid assumption in practice (Supplementary S3). We start the ICF update with . Suppose at the -th iteration we can produce an estimate for the spectral radius of . Then using (19), can be estimated by Plugging this into (20) we obtain an update for

Note that the update does not involve , but only and , and is a decreasing function of . Finally, to estimate the spectral radius of we use

where denotes the -norm. This update strategy borrows the idea of power iteration and is motivated by the observation that if were fixed (see also Proposition 1). The procedure works well in our numerical studies. To take care of the boundary conditions, we use for .

2.4 ICF outperforms other methods

Our numerical comparison studies were based on real datasets of genome-wide association studies downloaded from dbGaP. The details of the datasets can be found in Section 3.3. Because the convergence of iterative methods is sensitive to the collinearity in the design matrix , our comparison studies used two datasets: the first one contains K SNPs sampled across the whole genome, and the other contains K SNPs that are physically adjacent. The first dataset has little or no collinearity (henceforth referred to as IND), and the second has collinearity due to linkage disequilibrium (henceforth referred to as DEP). The sample size is for both datasets. Our numerical studies compared different methods (detailed below) for their speed and accuracy of solving (11). Given , for one experiment we sampled without replacement columns from the IND (or DEP) dataset to obtain , simulated under the null , and solved (11) using different methods with which corresponded to For each we conducted independent experiments.

Our initial studies compared ICF with six other methods: the Cholesky decomposition (Chol), the Jacobi method, the Gauss-Seidel method (GS), the successive over-Relaxation (SOR) method, the steepest descent method, and the conjugate gradient (CG) method. We excluded the Jacobi method and the steepest descent method due to their poor performance. To ensure a fair comparison in the context of BVSR, the starting point for Chol, GS, and SOR was being obtained, and the starting point for ICF was the upper triangular matrix such that being obtained. For GS, we tried the preconditioning method of Kohno et al. (1997), which is the most efficient among the methods surveyed in Niki et al. (2004), but we observed no improvement, most likely because is well-conditioned due to the regularization. For SOR, we need choose a value for the relaxation parameter (denoted by ), which is known to be very difficult. A solution was provided by Young (1954) (see also Yang and Matthias, 2007), but we observed that it did not apply when . After trial and error, we settled on using , which appeared to be optimal in our numerical studies. For all iterative methods, we started from and stopped if

| (21) |

or the number of iterations exceeded . The computer code for different methods was written in C++ and was run in the same environment. The Cholesky decomposition was implemented using GSL (GNU Scientific Library) (Gough, 2009), and GS and SOR were implemented in a manner that accounted for the sparsity of the triangular matrices and to obtain maximum efficiency (Golub and Van Loan, 2012, Chap. 10.1.2). Lastly, we included in the comparison the LAPACK routine DGELS, the most widely used least square solver, as a baseline reference.

| Dataset | Time (in seconds) | Convergence failures | |||||||||

| DGELS | Chol | ICF | GS | SOR | CG | ICF | GS | SOR | CG | ||

| IND | 50 | 7.3 | 0.034 | 0.019 | 0.016 | 0.025 | 0.054 | 0 | 0 | 0 | 0 |

| 100 | 26 | 0.20 | 0.07 | 0.07 | 0.09 | 0.24 | 0 | 0 | 0 | 0 | |

| 200 | 115 | 1.38 | 0.30 | 0.34 | 0.39 | 1.15 | 0 | 1 | 1 | 0 | |

| 500 | 679 | 21.0 | 2.7 | 3.6 | 2.9 | 9.8 | 0 | 2 | 1 | 0 | |

| 1000 | 2948 | 161 | 14 | 36 | 25 | 60 | 0 | 11 | 7 | 0 | |

| DEP | 50 | 7.3 | 0.035 | 0.020 | 0.029 | 0.031 | 0.056 | 0 | 8 | 6 | 0 |

| 100 | 27 | 0.20 | 0.08 | 0.23 | 0.19 | 0.26 | 0 | 29 | 20 | 0 | |

| 200 | 116 | 1.39 | 0.45 | 2.13 | 1.69 | 1.34 | 0 | 125 | 93 | 0 | |

| 500 | 683 | 21.0 | 5.5 | 36.1 | 32.8 | 15.1 | 0 | 621 | 514 | 0 | |

| 1000 | 2984 | 160 | 36 | 183 | 180 | 133 | 0 | 979 | 951 | 0 | |

The results are summarized in Table 1. For the IND dataset, three iterative methods (ICF, GS and SOR) appear on par with each other for smaller . For , ICF outperforms the other two, and is 10 times faster than the Cholesky decomposition. On average it took ICF iterations to converge, and ICF never failed to converge in all experiments. On the other hand, both GS and SOR failed to converge, at least once, for large . For the DEP dataset, we note that ICF is the fastest among all the methods compared. For larger , ICF is 4 – 5 times faster than the Cholesky decomposition, and 5 – 6 times faster than the other three methods. Both GS and SOR had difficulty in converging within iterations for large . DGELS is always the slowest since it assumes is unknown and solves (11) by QR decomposition. Advanced least square solvers (Avron et al., 2010; Meng et al., 2014) have similar performance to DGELS and can only beat it by a small margin when is very large. We also tweaked simulation conditions to check whether the results were stable. For example, we tried to simulate under the alternative instead of the null, and to initialize in different manners, such as using unpenalized linear estimates. The results remained essentially unchanged under different tweaks.

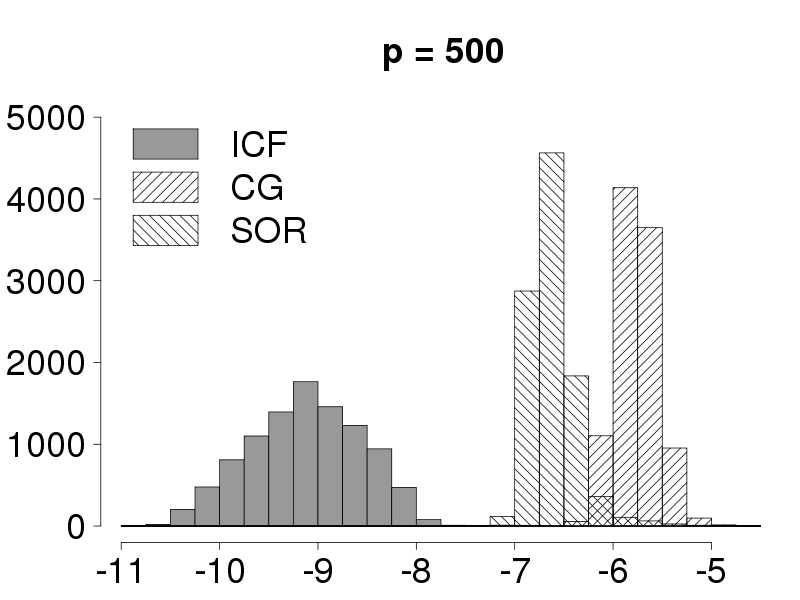

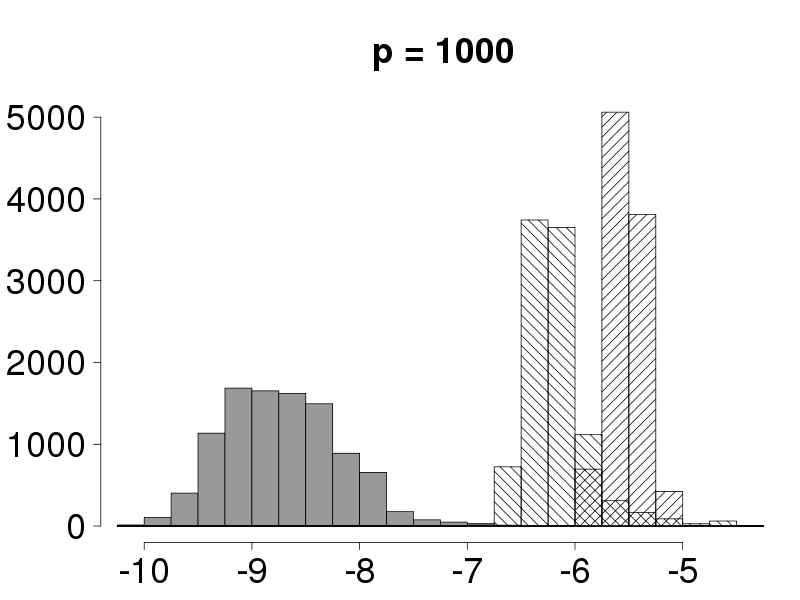

Next, we compared the accuracy of different iterative methods, where the truth was obtained from the Cholesky decomposition. In this experiment we used the IND dataset and compared for and . Each method was repeated for experiments. The maximum entry-wise deviation (denoted by ) was obtained for each method, each experiment, under each simulation condition. Only those converged experiments were included in the comparison. Figure 1 shows the distributions of for three methods. Clearly, ICF outperforms CG and SOR by a large margin. (GS is omitted since its accuracy is poorer than that of SOR in almost every experiment.) Because in real applications we are oblivious to the truth (or the truth is expensive to obtain), a method is more desirable if its deviation from the truth is within the pre-specified precision. Figure 1 shows that ICF always achieves the pre-specified precision () while the other two methods do not. Moreover, the deviation of ICF is 2 – 3 orders of magnitude smaller than that of SOR, and 3 – 4 orders of magnitude smaller than that of the CG method. We repeated the experiments for the DEP dataset and made the same observations.

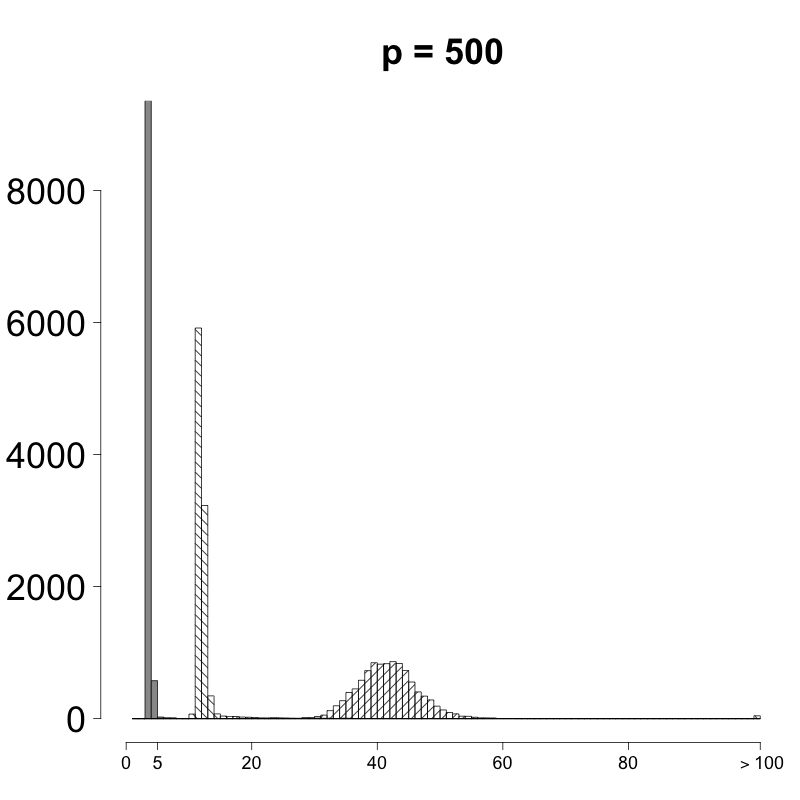

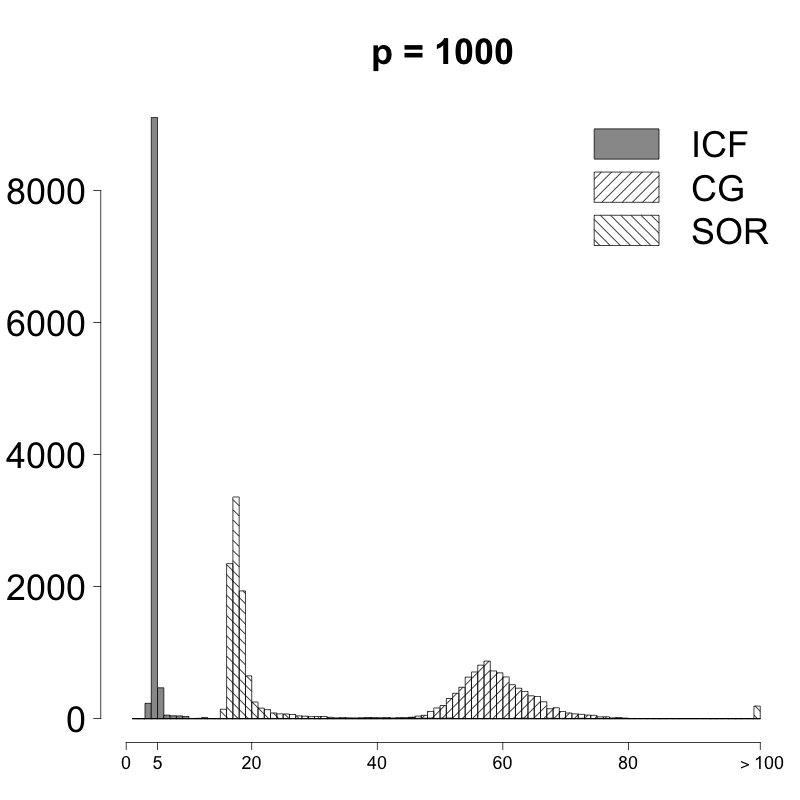

Figure 2 compares the number of iterations used to converge for different iterative methods for large . ICF takes a few iterations to converge, SOR a dozen iterations, CG about iterations. More numerical experiments can be found in Supplementary S2 where we investigated how and affects convergence rates. We also compared the performance of the iterative methods when the design matrix is beyond the counts of reference alleles, such as normal or log-normal distributed (Supplementary S1), and when has a different degree of collinearity (Supplementary S2.2). ICF exhibits an overwhelming advantage in every scenario.

3 ICF dramatically increases the speed of BVSR

3.1 Incorporating ICF into BVSR

As we mentioned in the introduction, for BVSR the most time-consuming step in MCMC is the computation of (4) for every proposed (superscript ′ denotes the proposed value). To successfully incorporate ICF into BVSR, we need to overcome two hurdles: avoiding the computation of the determinant term in (4) and efficiently obtaining the Cholesky decomposition .

Computing matrix determinant has a cubic complexity. If this is not avoided, using ICF to compute becomes pointless. When evaluating (4), we need to compute the determinant which takes operations. Identifying that the determinant is a normalization constant, avoiding computation of the determinant becomes a well studied problem in the MCMC literature that deals with the so-called “doubly-intractable distributions,” i.e. distributions with two nested unknown normalization constants (Møller et al., 2006; Murray et al., 2012). Recall that we want to sample

| (22) | ||||

where , and it is the computation of that we want to avoid. For a naive Metropolis-Hastings algorithm, if the current state is and the proposed move is , we need to evaluate the Hastings ratio

| (23) |

where

| (24) | ||||

and is the proposal distribution for proposing from The proposed move is accepted with probability which is called the Metropolis rule. Apparently, both and need to be evaluated in a naive MCMC implementation.

To avoid computing , notice that

| (25) |

holds for all , and if is sampled from , the ratio becomes a one-sample importance-sampling estimate of . Hence we can plug in to replace and compute the Hastings ratio by

| (26) |

This is the exchange algorithm of Murray et al. (2012), which can be viewed as a special case of the pseudo-marginal method (Andrieu and Roberts, 2009). In the Appendix we prove that the stationary distribution of this MCMC is the desired posterior distribution Since the Bayes factor (4) is invariant to the scaling and shifting of , we can simply assume and when sampling .

To tackle the second difficulty, notice that in each MCMC iteration, usually only one or a few entries of are flipped between and . Such proposals are often called “local” proposals, and Markov chains using local proposals usually have high acceptance ratios, which indicate the chains are “mixing” well (Guan and Krone, 2007). When one covariate is added into the model, the new Cholesky decomposition, , can be obtained from the previous decomposition by a forward substitution. When one covariate is deleted from the model, we simply delete the corresponding column from and introduce new zeros by Givens rotation (Golub and Van Loan, 2012, Chap. 5.1), which requires flops if the -th predictor is removed. We provide a toy example in Appendix to demonstrate the update on the Cholesky decomposition.

3.2 Numerical examples

We developed a software package, fastBVSR, to fit the BVSR model by incorporating ICF and the exchange algorithm into the MCMC procedure. The algorithm is summarized in Supplementary S4. The software is written in C++ and available at http://www.haplotype.org/software.html. In fastBVSR, we also implemented Rao-Blackwellization, as described in Guan and Stephens (2011), to reduce the variance of the estimates for and . By default, Rao-Blackwellization is done every 1000 iterations.

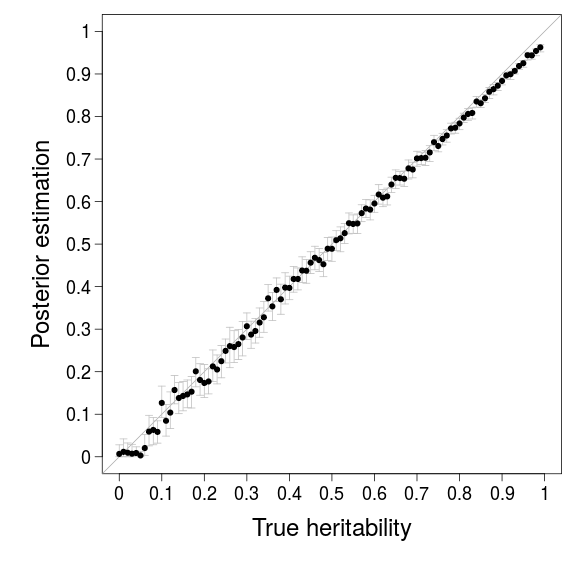

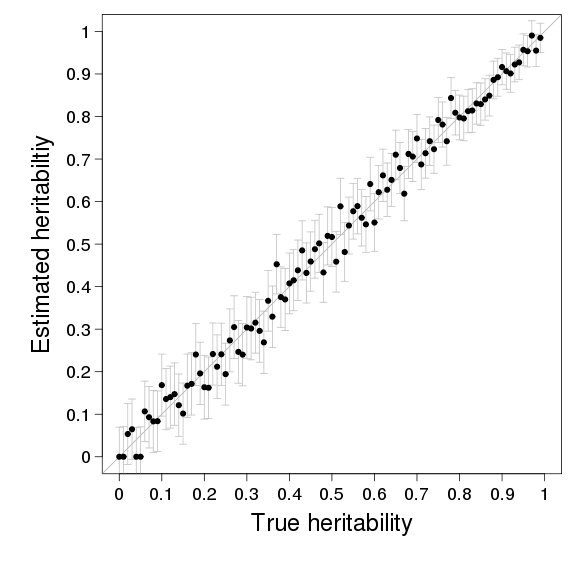

To check the performance of fastBVSR, we performed simulation studies based on a real dataset described in Yang et al. (2010) (henceforth the Height dataset). The Height dataset contains subjects and common SNPs (minor allele frequency ) after routine quality control (c.f. Xu and Guan, 2014). We sampled SNPs across the genome to perform simulation studies. Our aim was to check whether fastBVSR can reliably estimate the heritability in the simulated phenotypes. To simulate phenotypes of different heritability, we randomly selected causal SNPs (out of ) to obtain . For each selected SNP we drew its effect size from the standard normal distribution to obtain (the subvector of that contains nonzero entries). Then we simulated the standard normal error term to obtain , and scaled the simulated effect sizes simultaneously using such that and the heritability, , was (taking values in ). This was the same procedure as that of Guan and Stephens (2011). For each simulated phenotype, we ran fastBVSR to obtain the posterior estimate of heritability. We compared fastBVSR with GCTA (Yang et al., 2011), which is a software package to estimate heritability and do prediction using the linear mixed model. For heritability estimation, GCTA has been shown to be unbiased and accurate in a wide range of settings (Yang et al., 2010; Lee et al., 2011). The result is shown in Figure 3. Both fastBVSR and GCTA can estimate the heritability accurately; the mean absolute error is for fastBVSR and for GCTA. Noticeably, fastBVSR has a smaller variance but a slight bias when the true heritability is large.

Next we compare the predictive performance of fastBVSR and GCTA. We first define the mean squared error as a function of ,

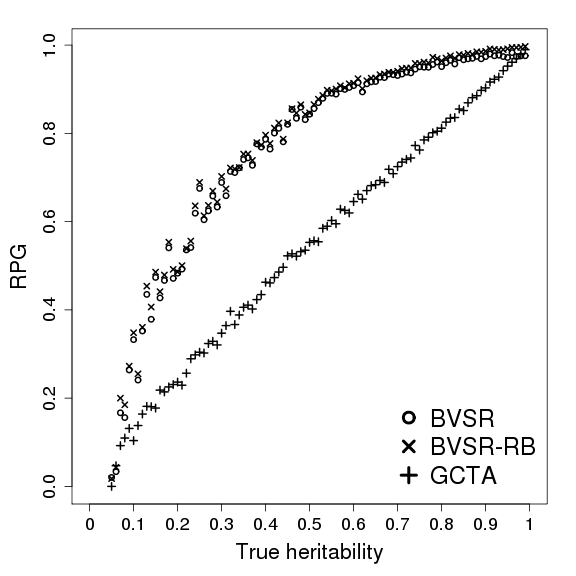

Then following Guan and Stephens (2011) we define relative prediction gain (RPG) to measure the predictive performance of

The advantage of RPG is that the scaling of does not contribute to RPG so that simulations with different heritability can be compared fairly. Clearly when , ; when , . Figure 4 shows that fastBVSR has much better predictive performance than GCTA, which reflects the advantage of BVSR over the linear mixed model. This advantage owes to the model averaging used in BVSR (Raftery et al., 1997; Broman and Speed, 2002). Besides, note that BVSR with Rao-Blackwellization performs slightly better than BVSR alone.

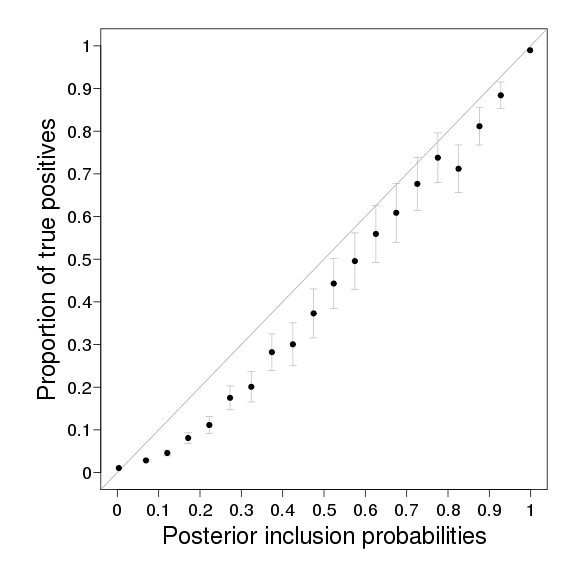

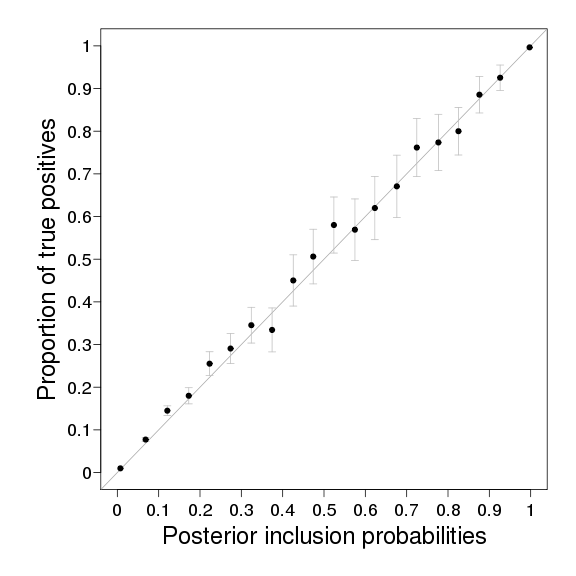

Lastly we check the calibration of the posterior inclusion probability (PIP), . We pool the results of the simulation sets with different heritability (from to at increment of ). In each set there are estimated PIPs, one for each SNP, and in total there are PIP estimates. We group these PIPs into bins, for , and for each bin we compute the fraction of true positives. If the PIP estimates are well calibrated, we expect that in each bin, the average of the PIPs roughly equals the fraction of true positives. Figure 5 shows that the PIP estimated by BVSR is conservative, which agrees with the previous study (Guan and Stephens, 2011), and the PIP estimated by Rao-Blackwellization is well cablibrated.

3.3 Analysis of real GWAS datasets

We applied fastBVSR to analyze GWAS datasets concerning intraocular pressure (IOP). We applied and downloaded two GWAS datasets from the database of Genotypes and Phenotypes (dbGaP), one for glaucoma (dbGaP accession number: phs000238.v1.p1) and the other for intraocular hypertension (dbGaP accession number: phs000240.v1.p1). The combined dataset contains autosomal SNPs and subjects, and was used previously by Zhou and Guan (2017) to examine the relationship between p-values and Bayes factors.

We conducted five independent runs with different random seeds. The sparsity parameters for BVSR were set as and , which reflected a prior of 30 – 3000 marginally associated SNPs. The posterior mean model size in each run ranges from to (Table 2). The average number of iterations for ICF to converge is (% interval = ), which suggests that ICF is effective in analyzing real datasets. The speed improvement of fastBVSR over piMASS (a BVSR implementation that uses the Cholesky decomposition to fit Bayesian linear regression, a companion software package of Guan and Stephens (2011)) is dramatic: with model size around and more than individuals, fastBVSR took hours to run million MCMC iterations, compared to more than hours used by piMASS on problems of matching size. Out of concern for the cumulative error in obtaining the matrix by updating the Cholesky decomposition (detailed in Section 3.1), we compared every steps the updated Cholesky decomposition with the directly computed Cholesky decomposition, and results suggested that the entry-wise difference was absolutely negligible.

We examine the inference of the hyperparameters, namely, the narrow-sense heritability , the model size , and the sparsity parameter . Table 2 shows the inferences of the three parameters are more or less consistent across five independent runs, and thus we combine the results from five independent runs in the following discussion. The posterior mean for is with credible interval This estimate of the heritability is smaller than those reported in the literature: from a twin study (Carbonaro et al., 2008), from a sibling study (Chang et al., 2005), and from an extended pedigree study (van Koolwijk et al., 2007). For comparison, using the same dataset, the heritability estimated by GCTA is with standard error . The underestimation of using fastBVSR is perhaps due to over-shrinking of the effect sizes (the posterior mean of prior effect size is ). The posterior mean for is , which suggests that IOP is a very much polygenic phenotype, agreeing with the complex etiology of glaucoma (Weinreb et al., 2014), to which high IOP is a precursor phenotype.

| Combined | Run1 | Run2 | Run3 | Run4 | Run5 | |

| 0.28 | 0.27 | 0.26 | 0.32 | 0.28 | 0.26 | |

| 474 | 446 | 395 | 622 | 476 | 430 | |

| 0.0016 | 0.0015 | 0.0013 | 0.0021 | 0.0016 | 0.0014 |

Lastly, we examine the top marginal signals detected by fastBVSR. Table 3 lists top SNPs based on PIP inferred from fastBVSR, at an arbitrary PIP threshold of . Table 3 also includes PPA (posterior probability of association) based on the single SNP test for two choices of prior effect sizes: which is the posterior mean of inferred from fastBVSR and which is a popular choice for single SNP analysis. We use the posterior mean inferred from fastBVSR as the prior odds of association. Multiplying a Bayes factor and the prior odds we obtain the posterior odds, from which we obtain the First the two columns of PPAs are highly similar in both ranking and magnitude. This observation agrees with our experience and theoretical studies (Zhou and Guan, 2017) that modest prior effect sizes produce similar evidence for association. Second, PPA and PIP have significantly different rankings (Wilcox rank test p-value ). There are two related explanations for this observation: if two SNPs are correlated, the PIPs tend to split between the two; conditioning on the other associated SNPs, the marginal associations tend to change significantly. Three known GWAS signals, rs12150284, rs2025751, rs7518099/rs4656461, which were replicated in our previous single-SNP analysis (Zhou and Guan, 2017), all show appreciable PIPs. Moreover, we note a potential novel association first reported in Zhou and Guan (2017): two SNPs located in PEX14, rs12120962, rs12127400, have PIPs of and respectively.

| SNP | Chr | Pos (Mb) | |||

|---|---|---|---|---|---|

| rs12120962 | 1 | 10.53 | 0.85 | 0.84 | 0.57 |

| rs12127400 | 1 | 10.54 | 0.74 | 0.74 | 0.27 |

| rs4656461 | 1 | 163.95 | 1.0 | 0.96 | 0.36 |

| rs7518099 | 1 | 164.00 | 1.0 | 0.98 | 0.42 |

| rs7645716 | 3 | 46.31 | 0.62 | 0.56 | 0.35 |

| rs2025751 | 6 | 51.73 | 0.81 | 0.82 | 0.68 |

| rs10757601 | 9 | 26.18 | 0.47 | 0.55 | 0.31 |

| rs9783190 | 10 | 106.76 | 0.39 | 0.31 | 0.32 |

| rs1381143 | 12 | 86.76 | 0.27 | 0.37 | 0.31 |

| rs4984577 | 15 | 93.76 | 0.43 | 0.49 | 0.42 |

| rs12150284 | 17 | 9.97 | 0.99 | 0.97 | 0.92 |

4 Discussion

We developed a novel algorithm, iterative complex factorization, to solve a class of penalized linear systems, proved its convergence, and demonstrated its effectiveness and efficiency through simulation studies. The novel algorithm can dramatically increase the speed of BVSR, which we demonstrated by analyzing a real dataset. In our simulation studies we only considered (in BVSR is the size of the selected model). When , the ICF can be implemented with the dual variable method of Saunders et al. (1998) (see also Lu et al., 2013), which hinges on the identity .

One limitation of ICF is that it requires the Cholesky decomposition to obtain the effective complex factorization. Nevertheless, ICF still has a range of potential applications. The general ridge regression (Draper and Van Nostrand, 1979) is an obvious one, and here we point out two other examples. The first is the Bayesian sparse linear mixed model (BSLMM) of Zhou et al. (2013), which can be viewed as a generalization of BVSR. BSLMM has two components, one is the linear component that corresponds to and the other is the random effect component. The linear component requires one to solve a system that is similar to (11) (Text S2 Zhou et al., 2013); therefore ICF can be applied to BSLMM to make it more efficient. Another example of ICF application is using the variational method to fit the BVSR (Carbonetto and Stephens, 2012; Huang et al., 2016). In particular, Huang et al. (2016) estimated using an iterative method. In each iteration, the posterior mean for is updated by solving a linear system that has the same form as (11), where the dimension is equal to the number of covariates with nonzero PIP estimates, and the diagonal matrix depends on the PIP estimates. Applying ICF to the variational method might be more beneficial compared to BVSR because the dimension of the linear system is exceedingly larger in the variational method.

The iterative complex factorization method converges almost instantaneously, and it is far more accurate than other iterative algorithms such as the Gauss-Seidel method. Why does it converge so fast and at the same time so accurate? Our intuition is that the imaginary part of the update in (15) , which involves the skew-symmetric matrix , whose Youla decomposition (Youla, 1961) suggests that it rotates , scales and flips its coordinates and rotates back, and which then appends itself to be the imaginary part of , provides a “worm hole” through the imaginary dimension in an otherwise purely real, unimaginary, solution path. Understanding how this works mathematically will have a far-reaching effect on Bayesian statistics, statistical genetics, machine learning, and computational biology.

Finally, we hope our new software fastBVSR, which is 10 – 100 times faster than the previous implementation of BVSR, will facilitate the wide-spread use of BVSR in analyzing or reanalyzing datasets from genome-wide association (GWA) and expression quantitative trait loci (eQTL) studies.

Supplementary material

The online appendix includes additional numerical studies (S1 – S3), a summary of the MCMC algorithm (S4), examples for updating the Cholesky decomposition (S5) and a proof for the stationary distribution of the exchange algorithm (S6). S1 compares the performance of the iterative methods using simulated datasets; S2 studies the behavior of the convergence rates of the iterative methods; S3 provides numerical evidence for the assumption used in Section 2.3.

References

- Andrieu and Roberts (2009) Andrieu, C. and Roberts, G. O. (2009). “The pseudo-marginal approach for efficient Monte Carlo computations.” The Annals of Statistics, 697–725.

- Avron et al. (2010) Avron, H., Maymounkov, P., and Toledo, S. (2010). “Blendenpik: Supercharging LAPACK’s least-squares solver.” SIAM Journal on Scientific Computing, 32(3): 1217–1236.

- Berger et al. (2001) Berger, J. O., Pericchi, L. R., Ghosh, J., Samanta, T., De Santis, F., Berger, J., and Pericchi, L. (2001). “Objective Bayesian methods for model selection: introduction and comparison.” Lecture Notes-Monograph Series, 135–207.

- Broman and Speed (2002) Broman, K. W. and Speed, T. P. (2002). “A model selection approach for the identification of quantitative trait loci in experimental crosses.” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 64(4): 641–656.

- Carbonaro et al. (2008) Carbonaro, F., Andrew, T., Mackey, D., Spector, T., and Hammond, C. (2008). “Heritability of intraocular pressure: a classical twin study.” British Journal of Ophthalmology, 92(8): 1125–1128.

- Carbonetto and Stephens (2012) Carbonetto, P. and Stephens, M. (2012). “Scalable variational inference for Bayesian variable selection in regression, and its accuracy in genetic association studies.” Bayesian analysis, 7(1): 73–108.

- Chang et al. (2005) Chang, T. C., Congdon, N. G., Wojciechowski, R., Muñoz, B., Gilbert, D., Chen, P., Friedman, D. S., and West, S. K. (2005). “Determinants and heritability of intraocular pressure and cup-to-disc ratio in a defined older population.” Ophthalmology, 112(7): 1186–1191.

- Draper and Van Nostrand (1979) Draper, N. R. and Van Nostrand, R. C. (1979). “Ridge regression and James-Stein estimation: review and comments.” Technometrics, 21(4): 451–466.

- Eldén (1977) Eldén, L. (1977). “Algorithms for the regularization of ill-conditioned least squares problems.” BIT Numerical Mathematics, 17(2): 134–145.

- Golub and Van Loan (2012) Golub, G. H. and Van Loan, C. F. (2012). Matrix computations, 3rd edition. JHU Press.

- Gough (2009) Gough, B. (2009). GNU scientific library reference manual. Network Theory Ltd.

- Guan and Krone (2007) Guan, Y. and Krone, S. M. (2007). “Small-world MCMC and Convergence to Multi-modal Distributions: From Slow Mixing to Fast Mixing.” Annals of Applied Probability, 17: 284–304.

- Guan and Stephens (2011) Guan, Y. and Stephens, M. (2011). “Bayesian variable selection regression for genome-wide association studies and other large-scale problems.” The Annals of Applied Statistics, 1780–1815.

- Hawkins and Yin (2002) Hawkins, D. M. and Yin, X. (2002). “A faster algorithm for ridge regression of reduced rank data.” Computational statistics & data analysis, 40(2): 253–262.

- Huang et al. (2016) Huang, X., Wang, J., and Liang, F. (2016). “A Variational Algorithm for Bayesian Variable Selection.” arXiv preprint arXiv:1602.07640.

- Ibrahim and Laud (1991) Ibrahim, J. G. and Laud, P. W. (1991). “On Bayesian analysis of generalized linear models using Jeffreys’s prior.” Journal of the American Statistical Association, 86(416): 981–986.

- Kohno et al. (1997) Kohno, T., Kotakemori, H., Niki, H., and Usui, M. (1997). “Improving the modified Gauss-Seidel method for Z-matrices.” Linear Algebra and its Applications, 267: 113–123.

- Lawson and Hanson (1995) Lawson, C. L. and Hanson, R. J. (1995). Solving least squares problems. SIAM.

- Lee et al. (2011) Lee, S. H., Wray, N. R., Goddard, M. E., and Visscher, P. M. (2011). “Estimating missing heritability for disease from genome-wide association studies.” The American Journal of Human Genetics, 88(3): 294–305.

- Liang et al. (2008) Liang, F., Paulo, R., Molina, G., Clyde, M. A., and Berger, J. O. (2008). “Mixtures of g priors for Bayesian variable selection.” Journal of the American Statistical Association, 103(481).

- Lu et al. (2013) Lu, Y., Dhillon, P., Foster, D. P., and Ungar, L. (2013). “Faster ridge regression via the subsampled randomized hadamard transform.” In Advances in neural information processing systems, 369–377.

- Meng et al. (2014) Meng, X., Saunders, M. A., and Mahoney, M. W. (2014). “LSRN: A parallel iterative solver for strongly over-or underdetermined systems.” SIAM Journal on Scientific Computing, 36(2): C95–C118.

- Møller et al. (2006) Møller, J., Pettitt, A. N., Reeves, R., and Berthelsen, K. K. (2006). “An efficient Markov chain Monte Carlo method for distributions with intractable normalising constants.” Biometrika, 93(2): 451–458.

- Murray et al. (2012) Murray, I., Ghahramani, Z., and MacKay, D. (2012). “MCMC for doubly-intractable distributions.” arXiv preprint arXiv:1206.6848.

- Niki et al. (2004) Niki, H., Harada, K., Morimoto, M., and Sakakihara, M. (2004). “The survey of preconditioners used for accelerating the rate of convergence in the Gauss–Seidel method.” Journal of Computational and Applied Mathematics, 164: 587–600.

- O’Hagan and Forster (2004) O’Hagan, A. and Forster, J. J. (2004). Kendall’s advanced theory of statistics, volume 2B: Bayesian inference, volume 2. Arnold.

- Raftery et al. (1997) Raftery, A. E., Madigan, D., and Hoeting, J. A. (1997). “Bayesian model averaging for linear regression models.” Journal of the American Statistical Association, 92(437): 179–191.

- Rokhlin and Tygert (2008) Rokhlin, V. and Tygert, M. (2008). “A fast randomized algorithm for overdetermined linear least-squares regression.” Proceedings of the National Academy of Sciences, 105(36): 13212–13217.

- Saunders et al. (1998) Saunders, C., Gammerman, A., and Vovk, V. (1998). “Ridge regression learning algorithm in dual variables.”

- Trefethen and Bau III (1997) Trefethen, L. N. and Bau III, D. (1997). Numerical linear algebra, volume 50. Siam.

- Turlach (2006) Turlach, B. A. (2006). “An even faster algorithm for ridge regression of reduced rank data.” Computational statistics & data analysis, 50(3): 642–658.

- van Koolwijk et al. (2007) van Koolwijk, L. M., Despriet, D. D., van Duijn, C. M., Cortes, L. M. P., Vingerling, J. R., Aulchenko, Y. S., Oostra, B. A., Klaver, C. C., and Lemij, H. G. (2007). “Genetic contributions to glaucoma: heritability of intraocular pressure, retinal nerve fiber layer thickness, and optic disc morphology.” Investigative ophthalmology & visual science, 48(8): 3669–3676.

-

Weinreb et al. (2014)

Weinreb, R., Aung, T., and Medeiros, F. (2014).

“The pathophysiology and treatment of glaucoma: A review.”

JAMA, 311(18): 1901–1911.

URL +http://dx.doi.org/10.1001/jama.2014.3192 - Xu and Guan (2014) Xu, H. and Guan, Y. (2014). “Detecting Local Haplotype Sharing and Haplotype Association.” Genetics, 197(3): 823–838.

- Yang et al. (2010) Yang, J., Benyamin, B., McEvoy, B. P., Gordon, S., Henders, A. K., Nyholt, D. R., Madden, P. A., Heath, A. C., Martin, N. G., Montgomery, G. W., et al. (2010). “Common SNPs explain a large proportion of the heritability for human height.” Nature genetics, 42(7): 565–569.

- Yang et al. (2011) Yang, J., Lee, S. H., Goddard, M. E., and Visscher, P. M. (2011). “GCTA: a tool for genome-wide complex trait analysis.” The American Journal of Human Genetics, 88(1): 76–82.

- Yang and Matthias (2007) Yang, S. and Matthias, K. G. (2007). “The optimal relaxation parameter for the SOR method applied to a classical model problem.” Technical report, Technical Report number TR2007-6, Department of Mathematics and Statistics, University of Maryland, Baltimore County.

- Youla (1961) Youla, D. C. (1961). “A normal form for a matrix under the unitary congruence group.” Canad. J. Math., 13: 694–704.

- Young (1954) Young, D. (1954). “Iterative methods for solving partial difference equations of elliptic type.” Transactions of the American Mathematical Society, 76(1): 92–111.

- Zhou and Guan (2017) Zhou, Q. and Guan, Y. (2017). “On the Null Distribution of Bayes Factors in Linear Regression.” Journal of American Statistical Association, to appear.

- Zhou et al. (2013) Zhou, X., Carbonetto, P., and Stephens, M. (2013). “Polygenic modeling with Bayesian sparse linear mixed models.” PLoS Genet, 9(2): e1003264.

We thank the two anonymous reviewers for their helpful comments that improved the quality of our presentation.

Fast model-fitting of Bayesian variable selection regression using the iterative complex factorization algorithm (Supplementary)

Quan Zhou and Yongtao Guan

S1 Numerical comparison studies of the iterative methods using simulated datasets

In Section 2.4, we performed numerical comparison studies using real GWAS datasets, where each covariate follows a binomial distribution. For comparison, we conducted the same experiment using simulated datasets where is continuous variable. Let be an arbitrary row of . First, we sampled from a multivariate normal distribution with fixed pairwise correlation ; that is, is an independent sample from where if and otherwise. Second, we sampled from a multivariate log-normal distribution such that . For both cases, we tried . Note that for the log-normal case, the pairwise correlation is then equal to respectively. Then we applied the same procedure and parameter values described in Section 2.4 ( and ) and collected the wall time usage of the iterative methods for solving independent linear systems with form (11). The only difference is that we used the relaxation parameter for the successive over-relaxation method since it appeared to produce best overall performance. The results are summarized in Table S1. In almost every scenario, ICF exhibits an overwhelming advantage, especially when the data is heavy-tailed (the log-normal case). The only exception is the normal data with , where CG also works well. Compared with the results given in Section 2.4, the advantage of ICF over the Cholesky decomposition becomes more prominent. Lastly, we note that GS and SOR work poorly when the pairwise correlation , and as grows larger, they quickly become ineffective. This phenomenon will be discussed in the next section.

| Dataset | Time (in seconds) | Convergence failures | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Chol | ICF | GS | SOR | CG | ICF | GS | SOR | CG | ||

| Normal | 50 | 0.031 | 0.017 | 0.017 | 0.063 | 0.023 | 0 | 0 | 0 | 0 |

| 100 | 0.19 | 0.06 | 0.06 | 0.25 | 0.09 | 0 | 0 | 0 | 0 | |

| 200 | 1.35 | 0.25 | 0.29 | 1.08 | 0.38 | 0 | 0 | 0 | 0 | |

| 500 | 20.6 | 1.8 | 2.7 | 9.7 | 3.2 | 0 | 0 | 0 | 0 | |

| 1000 | 159 | 7.3 | 21 | 72 | 21 | 0 | 0 | 0 | 0 | |

| Normal | 50 | 0.032 | 0.017 | 0.180 | 0.089 | 0.025 | 0 | 0 | 0 | 0 |

| 100 | 0.19 | 0.06 | 1.82 | 0.61 | 0.10 | 0 | 525 | 0 | 0 | |

| 200 | 1.36 | 0.25 | 7.21 | 6.19 | 0.38 | 0 | 1000 | 31 | 0 | |

| 500 | 20.6 | 1.8 | 44.6 | 44.5 | 3.6 | 0 | 1000 | 1000 | 0 | |

| 1000 | 159 | 7.7 | 205 | 204 | 23 | 0 | 1000 | 1000 | 0 | |

| Normal | 50 | 0.032 | 0.018 | 0.527 | 0.368 | 0.026 | 0 | 1000 | 0 | 0 |

| 100 | 0.19 | 0.07 | 1.90 | 1.91 | 0.09 | 0 | 1000 | 1000 | 0 | |

| 200 | 1.35 | 0.26 | 7.21 | 7.22 | 0.46 | 0 | 1000 | 1000 | 0 | |

| 500 | 20.6 | 2.0 | 44.6 | 44.5 | 3.2 | 0 | 1000 | 1000 | 0 | |

| 1000 | 159 | 10 | 195 | 195 | 20 | 0 | 1000 | 1000 | 0 | |

| Normal | 50 | 0.033 | 0.027 | 0.527 | 0.530 | 0.027 | 0 | 1000 | 1000 | 0 |

| 100 | 0.19 | 0.10 | 1.90 | 1.91 | 0.10 | 0 | 1000 | 1000 | 0 | |

| 200 | 1.35 | 0.42 | 7.21 | 7.22 | 0.40 | 0 | 1000 | 1000 | 0 | |

| 500 | 20.7 | 3.0 | 44.6 | 44.5 | 3.5 | 0 | 1000 | 1000 | 0 | |

| 1000 | 159 | 12 | 190 | 189 | 18 | 0 | 1000 | 1000 | 0 | |

| Log-normal | 50 | 0.032 | 0.011 | 0.015 | 0.058 | 0.026 | 0 | 0 | 0 | 0 |

| 100 | 0.19 | 0.04 | 0.06 | 0.23 | 0.10 | 0 | 0 | 0 | 0 | |

| 200 | 1.35 | 0.17 | 0.28 | 1.00 | 0.43 | 0 | 0 | 0 | 0 | |

| 500 | 20.6 | 1.7 | 2.5 | 8.9 | 3.5 | 0 | 0 | 0 | 0 | |

| 1000 | 159 | 7.4 | 21 | 69 | 23 | 0 | 0 | 0 | 0 | |

| Log-normal | 50 | 0.032 | 0.016 | 0.091 | 0.072 | 0.030 | 0 | 0 | 0 | 0 |

| 100 | 0.19 | 0.06 | 0.84 | 0.34 | 0.12 | 0 | 0 | 0 | 0 | |

| 200 | 1.37 | 0.25 | 7.18 | 2.84 | 0.56 | 0 | 958 | 0 | 0 | |

| 500 | 20.7 | 1.8 | 44.5 | 44.4 | 4.9 | 0 | 1000 | 980 | 0 | |

| 1000 | 159 | 7.6 | 205 | 205 | 37 | 0 | 1000 | 1000 | 0 | |

| Log-normal | 50 | 0.033 | 0.018 | 0.519 | 0.196 | 0.034 | 0 | 815 | 0 | 0 |

| 100 | 0.19 | 0.06 | 1.90 | 1.80 | 0.17 | 0 | 1000 | 494 | 0 | |

| 200 | 1.36 | 0.25 | 7.21 | 7.22 | 0.76 | 0 | 1000 | 1000 | 0 | |

| 500 | 20.5 | 1.8 | 44.6 | 44.5 | 7.4 | 0 | 1000 | 1000 | 0 | |

| 1000 | 159 | 7.5 | 195 | 194 | 56 | 0 | 1000 | 1000 | 0 | |

| Log-normal | 50 | 0.032 | 0.018 | 0.527 | 0.530 | 0.044 | 0 | 1000 | 1000 | 0 |

| 100 | 0.19 | 0.07 | 1.90 | 1.91 | 0.19 | 0 | 1000 | 1000 | 0 | |

| 200 | 1.35 | 0.32 | 7.22 | 7.23 | 0.96 | 0 | 1000 | 1000 | 0 | |

| 500 | 20.5 | 2.4 | 44.6 | 44.5 | 9.3 | 0 | 1000 | 1000 | 0 | |

| 1000 | 159 | 13 | 203 | 202 | 74 | 0 | 1000 | 1000 | 0 | |

S2 Numerical studies on the convergence rates of the iterative methods

S2.1 Symmetric Toeplitz systems

In this section, we assume the covariance matrix of is a symmetric Toeplitz matrix, which we will define shortly, denoted by . Instead of sampling , we simply let and consider the linear system

We will use several typical choices of to study how the convergence rates of the iterative methods change with and . As shown by Proposition 1, the convergence rate of ICF is given by the spectral radius of . For SOR, using the notation introduced in (12), the convergence rate is the spectral radius of , which we denote by . By letting , we get the convergence rate of GS, which is . Let and be the largest and smallest eigenvalue of and thus the condition number of is . Then the convergence rate of CG can be bounded from above by . Note that we cannot compute the exact convergence rate of CG, and in fact, CG can be regarded as a direct method since it always converges within iterations (Trefethen and Bau III, 1997, Lec. 38).

We denote a symmetric Toeplitz matrix by , which satisfies , i.e.

We consider two structured choices of .

-

(i)

. For a regression problem, this is equivalent to up to sign flipping of the regression coefficients.

-

(ii)

where and . This can be seen as the covariance matrix of a discretized Ornstein-Uhlenbeck process.

Note that in this setup, since

the convergence rates of the iterative methods only depend on and the product . Hence we can simply let be an arbitrary positive constant, and we used . However, for a real scatter matrix , one should be careful when since is then rank deficient. Such ill-conditioned systems will be studied in Section S2.2.

We first fixed and studied how the convergence rates change with using five covariance matrices: . The results are summarized in Table S2. As expected, as grows larger, the convergence rate becomes slower for every method. For the covariance matrix , since decreases exponentially as increases, the impact of larger values of is not significant. Strikingly, ICF has a much faster convergence rate than all the other methods, even if we simply choose . In contrast, the convergence rates of GS and SOR quickly approach as increases. This is probably because GS, SOR (and also Jacobi iteration) favor diagonally dominant matrices for . Hence, if for each row of , the sum of off-diagonal entries increases linearly with , these methods would easily run into convergence difficulties.

Next, we fixed and studied how the convergence rates change with using and . The results are summarized in Table S3. As expected, a smaller value of makes diagonally more dominant, and as a result, GS and SOR converge faster. However, ICF exhibits an opposite trend: as increases, ICF converges faster. This is probably due to the use of the Cholesky decomposition of , which implies that if , ICF would converge immediately. Note that, because it is the product that really matters, if and are fixed and increases, ICF will converge faster while the other methods become slower.

|

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 1.23 | 0.9999 | 0.95 | 2.3e-04 | 1.2e-04 | 0.104 | 0.080 | 0.102 | |||

| 100 | 1.42 | 0.9997 | 0.90 | 6.0e-04 | 3.0e-04 | 0.214 | 0.171 | 0.172 | |||

| 200 | 1.74 | 0.9993 | 0.81 | 0.0013 | 6.5e-04 | 0.395 | 0.321 | 0.269 | |||

| 500 | 2.46 | 0.999 | 0.61 | 0.0027 | 0.0014 | 0.700 | 0.576 | 0.421 | |||

| 1000 | 3.33 | 0.998 | 0.42 | 0.0040 | 0.0020 | 0.875 | 0.745 | 0.538 | |||

| 50 | 2.56 | 0.998 | 0.63 | 0.0032 | 0.0016 | 0.710 | 0.602 | 0.438 | |||

| 100 | 3.47 | 0.998 | 0.42 | 0.0046 | 0.0023 | 0.883 | 0.764 | 0.553 | |||

| 200 | 4.81 | 0.997 | 0.26 | 0.0060 | 0.0030 | 0.963 | 0.871 | 0.656 | |||

| 500 | 7.50 | 0.996 | 0.12 | 0.0078 | 0.0039 | 0.993 | 0.945 | 0.765 | |||

| 1000 | 10.6 | 0.996 | 0.06 | 0.0089 | 0.0044 | 0.998 | 0.972 | 0.827 | |||

| 50 | 7.11 | 0.993 | 0.22 | 0.013 | 0.0066 | 0.985 | 0.939 | 0.753 | |||

| 100 | 10.0 | 0.992 | 0.12 | 0.016 | 0.0077 | 0.996 | 0.969 | 0.818 | |||

| 200 | 14.1 | 0.991 | 0.06 | 0.017 | 0.0087 | 0.9990 | 0.984 | 0.868 | |||

| 500 | 22.3 | 0.990 | 0.03 | 0.020 | 0.0097 | 0.9998 | 0.994 | 0.914 | |||

| 1000 | 31.5 | 0.990 | 0.01 | 0.021 | 0.010 | 0.99996 | 0.997 | 0.938 | |||

| 50 | 9.51 | 0.984 | 1.06 | 0.032 | 0.016 | 0.747 | 0.719 | 0.810 | |||

| 100 | 9.74 | 0.984 | 1.07 | 0.032 | 0.016 | 0.772 | 0.748 | 0.814 | |||

| 200 | 9.81 | 0.984 | 1.08 | 0.032 | 0.016 | 0.792 | 0.774 | 0.815 | |||

| 500 | 9.84 | 0.984 | 1.05 | 0.032 | 0.016 | 0.804 | 0.797 | 0.815 | |||

| 1000 | 9.84 | 0.984 | 1.02 | 0.032 | 0.016 | 0.809 | 0.806 | 0.815 | |||

| 50 | 51.4 | 0.838 | 1.00 | 0.387 | 0.162 | 0.965 | 0.965 | 0.962 | |||

| 100 | 64.1 | 0.837 | 1.06 | 0.388 | 0.163 | 0.970 | 0.970 | 0.969 | |||

| 200 | 74.4 | 0.837 | 1.00 | 0.389 | 0.163 | 0.973 | 0.973 | 0.973 | |||

| 500 | 81.7 | 0.837 | 0.95 | 0.389 | 0.163 | 0.976 | 0.975 | 0.976 | |||

| 1000 | 83.7 | 0.837 | 0.94 | 0.389 | 0.163 | 0.977 | 0.976 | 0.976 |

|

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 4.82 | 0.999992 | 0.25 | 1.5e-05 | 7.5e-06 | 0.963 | 0.871 | 0.656 | |||

| 1 | 4.82 | 0.9992 | 0.25 | 0.0015 | 7.5e-04 | 0.963 | 0.871 | 0.656 | |||

| 0.5 | 4.81 | 0.997 | 0.26 | 0.0060 | 0.0030 | 0.963 | 0.871 | 0.656 | |||

| 0.2 | 4.76 | 0.982 | 0.26 | 0.038 | 0.018 | 0.961 | 0.868 | 0.653 | |||

| 0.1 | 4.58 | 0.931 | 0.27 | 0.148 | 0.069 | 0.956 | 0.858 | 0.642 | |||

| 0.05 | 4.05 | 0.788 | 0.33 | 0.539 | 0.212 | 0.932 | 0.821 | 0.604 | |||

| 10 | 10.0 | 0.99996 | 1.07 | 8.1e-05 | 4.1e-05 | 0.799 | 0.779 | 0.818 | |||

| 1 | 9.96 | 0.996 | 1.08 | 0.0081 | 0.0040 | 0.798 | 0.777 | 0.817 | |||

| 0.5 | 9.81 | 0.984 | 1.08 | 0.032 | 0.016 | 0.793 | 0.774 | 0.815 | |||

| 0.2 | 8.96 | 0.912 | 1.05 | 0.193 | 0.088 | 0.761 | 0.755 | 0.799 | |||

| 0.1 | 7.10 | 0.749 | 0.99 | 0.672 | 0.251 | 0.698 | 0.697 | 0.753 | |||

| 0.05 | 4.56 | 0.547 | 0.87 | 1.66 | 0.453 | 0.600 | 0.556 | 0.640 |

S2.2 Ill-conditioned systems

Our last numerical study concerned ill-conditioned linear systems. Let be the covariance matrix of and consider the linear system where

The matrix is always full rank due to the shrinkage/regularization term ; however, it can be ill-conditioned if is ill-conditioned and is large.

We still fixed and tried different values for . For , we considered the following three choices so that it is ill-conditioned: Toeplitz matrices and (see the last section for definition) and the matrix defined by

That is, represents the scenario where there are duplicate pairs of covariates ( and , and , , and ), and all the remaining pairs have correlation equal to . Hence, the matrix has rank equal to . The results are summarized in Table S4. ICF is still much better than all the other methods except when the covariance matrix is and . For a given covariance matrix, ICF favors larger values of while the other methods favor small values of . Hence, we can also conclude that for an ill-conditioned covariance matrix and a fixed , ICF converges faster for larger sample sizes, which is a very appealing property since the other methods usually fail in such cases. Lastly, for the rank-deficient covariance matrix , the optimal relaxation parameter for ICF appears to be around and the corresponding convergence rate is about . Interestingly, we tried with other values for and , and made the same observation.

|

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 10 | 61.6 | 0.9997 | 0.03 | 5.2e-04 | 2.6e-04 | 0.99997 | 0.9992 | 0.968 | |||

| 1 | 61.0 | 0.974 | 0.03 | 0.053 | 0.026 | 0.99997 | 0.9992 | 0.968 | |||

| 0.5 | 59.3 | 0.900 | 0.03 | 0.221 | 0.100 | 0.99997 | 0.9991 | 0.967 | |||

| 0.2 | 50.3 | 0.518 | 0.03 | 1.86 | 0.482 | 0.99996 | 0.999 | 0.961 | |||

| 0.1 | 35.6 | 0.132 | 0.04 | 13.2 | 0.868 | 0.99991 | 0.998 | 0.945 | |||

| 10 | 417.4 | 0.995 | 1.05 | 0.0100 | 0.0050 | 0.998 | 0.998 | 0.995 | |||

| 1 | 296.6 | 0.668 | 0.92 | 0.995 | 0.332 | 0.997 | 0.997 | 0.993 | |||

| 0.5 | 187.6 | 0.336 | 0.71 | 3.95 | 0.664 | 0.996 | 0.995 | 0.989 | |||

| 0.2 | 82.3 | 0.080 | 0.42 | 23.0 | 0.920 | 0.996 | 0.987 | 0.976 | |||

| 0.1 | 41.7 | 0.030 | 0.27 | 65.4 | 0.970 | 0.996 | 0.972 | 0.953 | |||

| 10 | 4244.1 | 0.666 | 1.36 | 1.00 | 0.334 | 0.99998 | 0.99996 | 0.9995 | |||

| 1 | 424.4 | 0.664 | 0.32 | 1.01 | 0.336 | 0.99993 | 0.9996 | 0.995 | |||

| 0.5 | 212.2 | 0.660 | 0.17 | 1.03 | 0.340 | 0.99993 | 0.9993 | 0.991 | |||

| 0.2 | 84.9 | 0.651 | 0.08 | 1.07 | 0.349 | 0.99991 | 0.998 | 0.977 | |||

| 0.1 | 42.5 | 0.635 | 0.04 | 1.15 | 0.365 | 0.9999 | 0.996 | 0.954 |

| IND | DEP | ||||||

| mean() | max() | mean() | mean() | max() | mean() | ||

| 20 | 10 | 0.0020 | 0.023 | 0.34 | 0.0020 | 0.026 | 0.35 |

| 20 | 20 | 0.00099 | 0.016 | 0.77 | 0.0010 | 0.021 | 0.77 |

| 50 | 10 | 0.00057 | 0.0087 | 0.11 | 0.00066 | 0.0087 | 0.11 |

| 50 | 20 | 0.00029 | 0.0063 | 0.3 | 0.00035 | 0.0042 | 0.31 |

| 50 | 50 | 0.00016 | 0.0021 | 0.91 | 0.00016 | 0.0025 | 0.91 |

| 100 | 10 | 0.00017 | 0.0022 | 0.035 | 0.00017 | 0.0020 | 0.035 |

| 100 | 20 | 9.3e-05 | 0.0014 | 0.097 | 9.5e-05 | 0.0014 | 0.1 |

| 100 | 50 | 3.8e-05 | 0.00046 | 0.39 | 4.2e-05 | 0.0005 | 0.4 |

| 200 | 10 | 5.2e-05 | 0.00096 | 0.0099 | 5.5e-05 | 0.00059 | 0.011 |

| 200 | 20 | 2.3e-05 | 0.00029 | 0.028 | 2.8e-05 | 0.00035 | 0.031 |

| 200 | 50 | 1.1e-05 | 0.00016 | 0.11 | 1.1e-05 | 0.00018 | 0.12 |

S3 Numerical evidence for

Recall that in Section 2.3, when we introduced our adaptive strategy for choosing for ICF, we assumed that is zero. Using (19) and (20), one can show that by omitting sufficiently small , the induced error on is for some . Hence, it is fine to neglect as long as it is less than, say . We only need to verify this assumption for even , since if is odd, is always zero. It turned out that this assumption holds very generally, once we have a moderately large sample size and is not too small.

We used the two GWAS datasets described in the main text, IND and DEP, to examine how fast decreases to zero. As will be shown later in the results, decreases as either or increases; therefore, we only considered small values for and in this study. For each pair , we randomly sampled data matrices from each dataset, and computed the mean and the maximum of the associated values of . We still used . The results shown in Table S5 indicate that it is very safe to assume when the sample size is large, say greater than . We did the same experiments with our simulated datasets used in Section S1 and made very similar observations. We did observe that tends to be larger when the data has strong collinearity or a heavy-tailed distribution (i.e. the log-normal data). But as long as and , it is safe to assume that is negligible (less than ). Table S5 also includes the mean of . By direct calculations, one can verify that the induced relative error on is approximately , which is still very small in every case we considered.

S4 Summary of the MCMC algorithm of fastBVSR

S5 Examples for updating the Cholesky decomposition

Suppose we start with

such that

Add a covariate

To add one covariate, we attach it to the last column of and denote the new matrix by . Suppose

To compute the new Cholesky decomposition , we solve

which requires only one forward substitution to get

Remove a covariate

Consider removing the second covariate of and denote the new matrix by to get

is obtained by removing the second column from . Note that . To make zero, we introduce the Givens rotation matrix

Note , and . The new Cholesky decomposition is then given by

and the bottom row of zeros can be removed without affecting subsequent calculations.

S6 Proof for the exchange algorithm

We prove that the posterior is the stationary distribution of the exchange algorithm by checking the detailed balance condition, i.e.

where and

Let . Then,

Thus the detailed balance condition holds and the exchange algorithm leaves the posterior invariant. For a more general proof, see Andrieu and Roberts (2009).