.

Asymptotics for the Discrete-Time Average of the Geometric Brownian Motion and Asian Options

Abstract.

The time average of geometric Brownian motion plays a crucial role in the pricing of Asian options in mathematical finance. In this paper we consider the asymptotics of the discrete-time average of a geometric Brownian motion sampled on uniformly spaced times in the limit of a very large number of averaging time steps. We derive almost sure limit, fluctuations, large deviations, and also the asymptotics of the moment generating function of the average. Based on these results, we derive the asymptotics for the price of Asian options with discrete-time averaging in the Black-Scholes model, with both fixed and floating strike.

Key words and phrases:

Asian options, central limit theorems, Berry-Esseen bound, large deviations.2010 Mathematics Subject Classification:

91G20,91G80, 60F05,60F101. Introduction

Asian (or average) options are widely traded instruments in the financial markets, which involve the time average of the price of an asset . Most commonly is a stock price or a commodity futures contract price, for example oil or natural gas futures. An Asian call option has payoff of the form

| (1) |

where is a sequence of strictly increasing times, called sampling or averaging dates. Under risk-free neutral pricing, the price of such an option is given by the expectation of the payoff in the risk-neutral measure. Assuming the Black-Scholes model one is led to study the distributional properties of the discrete time average of the asset price

| (2) |

under the assumption that follows a geometric Brownian motion

| (3) |

where is a standard Brownian motion, is the risk-free rate, is the dividend yield and is the volatility.

The main technical difficulty for pricing Asian options is that the probability distribution of the discrete time average (2) does not have a simple expression. If the averaging times are uniformly distributed, the time average can be well approximated, for sufficiently small time step, by a continuous average

| (4) |

When follows a geometric Brownian motion, the problem is reduced to the study of the distributional properties of the time integral of the geometric Brownian motion, which has been extensively studied in the literature. See [16] for a review of the main results and their applications to the Asian options pricing.

A wide variety of methods have been proposed for pricing Asian options, and a brief survey is given below.

1. PDE methods [42, 49, 50, 35]. The pricing of an Asian option can be reduced to the solution of a 1+1 partial differential equation, which is solved numerically. This method can be applied both to continuous-time and discrete-time averaging Asian options [1]. See also Alziary et al. [2].

2. The Laplace transform method [24, 7]: the Asian option price with random exponentially distributed maturity can be found in closed form for the case when the asset price follows a geometric Brownian motion. This reduces the problem of the Asian option pricing to the inversion of a Laplace transform.

3. Spectral method [33]. The probability distribution of the time integral of the geometric Brownian motion can be related to that of a Bessel process [14, 13]. The transition density of this Bessel process can be expanded in an eigenfunction series [53], and Asian option prices can be evaluated using the eigenfunction expansion, truncated to a sufficient high order [33].

4. Bounds and control variates methods. There is a large literature on deriving bounds on Asian option prices. Both lower and upper bounds have been given, see [35] for an overview. They can be used also in conjunction with Monte Carlo methods as control variates. One precise method of this type which is popular in practice was given by Curran [9]. Other methods which take into account the discrete time averaging have been proposed in [22, 23, 21].

5. Monte Carlo simulation. See e.g. Kemna and Vorst [29], Fu, Madan, Wang [20], Lapeyre and Teman [30].

6. Analytical approximations. Various numerical methods have been proposed which approximate the distribution of the arithmetic average using parametric forms, such as log-normal [32] or inverse Gamma distributions [36].

We note also the more general approach of [52] which can be applied for a wide class of models.

Most of the theoretical results in the literature concerning the distribution of the time average of the geometric Brownian motion refer to the continuous time average. The discrete sum of the geometric Brownian motion is a particular case of the sum of correlated log-normals which has been studied extensively in the literature, see [3] for an overview. Dufresne has obtained in [15] limit distribution for the discrete time average in the limit of very small volatility . A recent work by the present authors [39] studied the properties of the discrete time average at fixed in the limit , and its convergence to the continuous time average as the time step .

In this paper, we concentrate on the discrete time average of the geometric Brownian motion, . We assume the Black-Scholes model, that is, the asset price follows a geometric Brownian motion

| (5) |

where is a standard Brownian motion. We would like to study the distributional properties of the average of the discretely sampled asset price (2) defined on the discrete times uniformly spaced with time step .

We will derive in this paper asymptotic results about in the limit by keeping fixed the following combinations of model parameters

| (6) | |||

| (7) |

Note that is always positive but can be both positive and negative. We also note that the conditions (6) and (7) can be replaced by and and all the results in this paper will still hold.

The constraints (6), (7) include two interesting regimes:

- •

- •

We emphasize that we do not make any assumptions about the values of , and they can be arbitrary. The validity of our asymptotic results require only that , such that these regimes cover most cases of practical interest, provided that the number of averaging times is sufficiently large.

We present in this paper three asymptotic results for the distributional properties of the discrete time average of a geometric Brownian motion in the limit of a large number of averaging time steps : i) almost sure limit and fluctuation results for , ii) an asymptotic result for the moment generating function of the partial sums for , and iii) large deviations results for . Using these asymptotic results, we derive rigorously asymptotics for the prices of out-of-the-money, in-the-money and at-the-money Asian options.

Section 2 presents the almost sure and fluctuations results for in the limit. Section 3 presents an asymptotic result for the Laplace transform of the finite sum of the geometric Brownian motion sampled on discrete times , in the limit . In Section 4 we consider the asymptotics of fixed strike Asian options following from the large deviations result iii), and in Section 5 we treat the case of the floating strike Asian options. These asymptotic results can be used to obtain approximative pricing formulas for Asian options, and in Section 6 we compare the numerical performance of the asymptotic result against alternative methods for pricing Asian options under the BS model. Some of the proposed methods are known to be less efficient numerically in the small maturity and/or small volatility limit [24, 33]. The asymptotic results derived in this paper are of practical interest as they complement these approaches in a region where their numerical performance is not very good. We demonstrate good agreement of our asymptotic results with alternative pricing methods for Asian options with realistic values of the model parameters.

2. Asymptotics for the discrete time average of geometric Brownian motion

We have the almost sure limit:

Proposition 1.

We have

| (8) |

Proof.

Note that and from the property of Brownian motion, a.s. as . Moreover, as uniformly in . Therefore, can be approximated by uniformly in , that is, a.s. as . Finally, notice that

| (9) |

Hence, we proved the desired result. ∎

We have also the following fluctuation result:

Proposition 2.

The time average converges in distribution to a normal distribution in the limit

| (10) |

with

| (11) |

Proof.

We have

| (12) | |||

| (13) | |||

| (14) |

where with a standard Brownian motion. We can rewrite the second term in (14) as

| (15) | ||||

as .

The first term in (14) can be written further as

| (16) |

where we defined

| (17) |

We claim that in probability as .

We have the following upper bound on .

| (18) |

The upper bound is a non-negative random variable since for any real . The expectation of can be computed exactly

| (19) | ||||

This goes to zero as . The Markov inequality implies that in probability as .

Next, let us estimate the lower bound on . We have

| (20) | ||||

where we used again in the second step the inequality .

The first term in (16) is a normal random variable and converges in distribution to a normal distribution with mean zero and variance to be determined.

| (21) |

This can be computed by writing with i.i.d. normally distributed random variables with mean zero and unit variance. The sum can be written as

| (22) | ||||

We can compute the variance of this random variable as

| (23) | |||

as , where we can compute that

| (24) |

∎

3. Moment generating function

Define the moment generating function of as

| (25) |

For , this is the Laplace transform of the distribution function of .

We are interested in the limit . We will compute this limit using the theory of large deviations. Before we proceed, recall that a sequence of probability measures on a topological space satisfies the large deviation principle with rate function if is non-negative, lower semicontinuous and for any measurable set , we have

| (26) |

Here, is the interior of and is its closure. The rate function is said to be good if for any , the level set is compact. We refer to Dembo and Zeitouni [10] or Varadhan [48] for general background of large deviations and the applications.

We have the following limit theorem for the generating function in the limit at fixed .

Theorem 3.

For any , and for any ,

| (27) |

Proof.

Since for any for any log-normal random variable , it is clear that for any . Next, for any ,

| (28) | ||||

where , , are i.i.d. random variables. Note that is defined as . By Mogulskii theorem, see e.g. [10], satisfies a large deviation principle on with the good rate function

| (29) |

if , i.e., absolutely continuous and and otherwise, where

| (30) |

Let . Then,

| (31) |

Moreover, we claim that

| (32) |

is a continuous map. Let be any sequence in so that in . Observe that for any .

| (33) |

Let be sufficiently large so that . Therefore, we have

which converges to as . Hence the map is continuous. Let us recall the celebrated Varadhan’s lemma from large deviations theory, see e.g. [10]. if satisfies a large deviation principle with good rate function , and if is a continuous map and

| (34) |

then

In our case,

is a continuous map. Moreover, for , and thus the condition (34) is trivially satisfied. Hence we can apply the Varadhan’s lemma and get,

| (35) | |||

Finally, notice that

| (36) | ||||

Hence, for any ,

| (37) | |||

∎

3.1. Solution of the Variational Problem

The variational problem in Theorem 3 can be re-stated as

| (38) |

where is the solution of the variational problem

| (39) |

Here we have .

This variational problem can be solved explicitly, and the solution is given by the following result.

Proposition 4.

Proof.

The proof will be given in the Appendix. ∎

Let us recall that , and in the short maturity limit at constant , we have . Therefore, the special case is of practical interest when considering the short maturity limit. For this case it is clear that only (43) has a solution for so we get the simpler result.

Corollary 5.

The function in the limit is given by

| (44) |

where is the solution of the equation

| (45) |

In conclusion, the result of Theorem 3 and Proposition 4 gives an asymptotic expression for the Laplace transform of the discrete sum of the geometric Brownian motion in the limit , of the form . This result could be used for numerical simulations of , similar to the approach presented in [31] using an asymptotic result for the Laplace transform of the sum of correlated log-normals. Another possible application would be to obtain a first-order approximation of Asian options prices in the asymptotic limit using the Carr-Madan formula [6].

In the next Section we present the leading asymptotics for the Asian option prices using the theory of large deviations.

4. Asymptotics for Asian options prices

Asymptotics for the option pricing is a well studied subject in mathematical finance. There is a vast literature on the asymptotics for option pricing, especially the asymptotics for the vanilla option pricing and the corresponding implied volatility for various continuous-time models, see e.g. [4, 25, 17, 18, 46]. We are interested in the asymptotics for the pricing of the Asian options in the discrete time setting, under the assumptions (6) and (7).

Let us consider an Asian option with strike price , in the Black-Scholes model with volatility , risk free rate and dividend yield . The prices of the put and call options at time zero are given by

| (46) | |||

| (47) |

respectively, where and the expectation are taken under the risk-neutral probability measure under which the asset price satisfies the SDE . Also notice that . Recall that we have proved that a.s. as . Since , by the bounded convergence theorem from real analysis, we have

| (48) |

From put-call parity,

as . Therefore,

| (49) |

4.1. Out-of-the-Money Case

When , and the put option is out-of-the-money and the decaying rate of to zero as is governed by the left tail of the large deviations of . When , and the call option is out-of-the-money and the decaying rate of to zero as is governed by the right tail of the large deviations of . Before we proceed, let us first derive the large deviation principle for .

Proposition 6.

satisfies a large deviation principle with rate function

| (50) |

for and otherwise.

Proof.

We proved already that , where and the map is continuous in the supremum norm. Since satisfies a large deviation principle on with rate function if and otherwise. From the contraction principle, and the fact that uniformly in , we conclude that satisfies a large deviation principle with rate function defined in (50). Finally, notice that is positive and thus for any . ∎

Remark 7.

in (50) if and only if the optimal satisfies which is equivalent to since . This gives us . Thus if and only if which is consistent with the a.s. limit of as .

Remark 8.

We have proved that exists for any and is differentiable and for any . Since for any , we cannot use Gärtner-Ellis theorem to obtain large deviations for . One may speculate that we might have subexponential tails. But the intriguing fact is that we still have large deviations as stated in Proposition 6.

We can further analyze and solve the variational problem (50). For , the solution is given by the following result.

Proposition 9.

The rate function of the discrete time average of the geometric Brownian motion is given by

| (51) |

with

| (52) |

where

| (53) | |||

| (54) |

and are the solutions of the equations

| (55) |

and

| (56) |

Proof.

The proof is given in the Appendix. ∎

Remark 10.

We note that the equations for can be put into a unique form by denoting . Expressed in terms of this variable we have

| (57) | |||

where is the solution of the equation

| (58) |

Remark 11.

The rate function vanishes for , as expected from the general properties of the rate function. Since we have for any , this zero occurs for . We note that the rate function vanishes at . Both these values of satisfy (55) with , which corresponds to . However, the true solution of the variational problem (50) corresponds to which gives the optimal function , see (135).

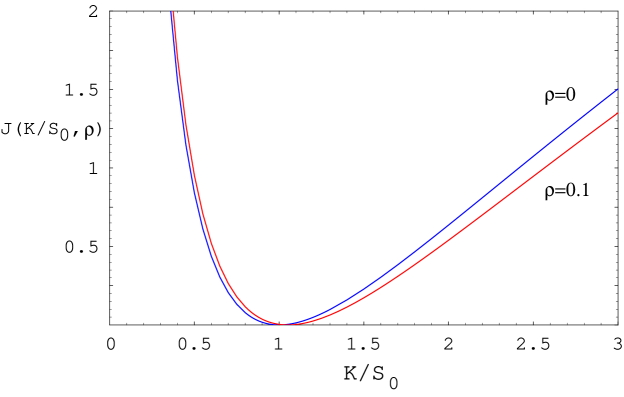

For the solution to the variational problem (50) simplifies and is given as follows.

Corollary 12.

For the special case ,

| (59) |

and otherwise, where is the unique solution of the equation

| (60) |

and is the unique solution in of the equation

| (61) |

It can be shown that this is identical to the rate function for the short maturity asymptotics of Asian options with continuous time averaging in the Black-Scholes model [40]. The rate function can be evaluated numerically using the result of Proposition 9. The plot of is shown in Figure 1 for .

Using the large deviations results for , we can obtain the asymptotics of the out-of-the-money Asian options prices. This is given by the following result.

Proposition 13.

Proof.

For any ,

| (64) |

Therefore, . Since it holds for any , we conclude that

| (65) |

On the other hand,

| (66) |

which implies that . Hence, we proved the (62).

For any ,

| (67) |

Therefore, . Since it holds for any , we have

| (68) |

For any , , by Hölder’s inequality,

| (69) | ||||

By Jensen’s inequality, for any , it is clear that for any , . Therefore, for any ,

| (70) |

We can compute that

| (71) | ||||

where we used the reflection principle for the Brownian motion and the Brownian scaling property. Note that is finite for any . Hence, from (69), (70), (71), we conclude that for any (and thus , where ),

| (72) |

Since it holds for any , by letting , we proved (63). ∎

4.2. In-the-Money Case

We consider the case of in-the-money Asian options, that is for the put option (and for the call option). Since a.s. we get from the bounded convergence theorem and put-call parity, that and . The next results concern the speed of the convergence.

Proposition 14.

When and ,

| (73) |

and when and ,

| (74) |

The case is similar. When ,

| (75) |

and when ,

| (76) |

4.3. At-the-Money Case

Consider next the case of at-the-money Asian options, that is . Since a.s., using the bounded convergence theorem, we have as . Put-call parity implies that as as well. Note that in the case of out-of-the-money, we have already seen that both and decay to zero exponentially fast in , where the exponent is given by . The next result is about the speed that and decay to zero as for at-the-money Asian options. We will see that, unlike the out-of-the-money Asian options, whose asymptotics are governed by the large deviations results, the asymptotics for at-the-money case are governed by the normal fluctuations from the central limit theorem and non-uniform Berry-Esseen bound.

Proposition 15.

When the Asian option is at-the-money, that is, ,

| (79) | |||

| (80) |

as .

Proof.

| (81) | ||||

We have proved in Proposition 2 that as . Intuitively, it is clear that where . But in order to prove this, the central limit theorem is not sufficient. We need a non-uniform Berry-Esseen bound [37, 5], which we recall next. See e.g. Pinelis [38] for a survey on this subject.

Theorem 16 (Non-uniform Berry-Esseen bound).

For any independent and not necessarily identically distributed random variables with zero means and finite variances and , where , let be the cumulative distribution function of and the standard normal cumulative distribution function, that is .

We have proved that

| (83) |

where

| (84) |

where are i.i.d. random variables and

| (85) |

The plan of the proof will be to show that the contributions from the second and third terms in (83) are negligible, and to apply the non-uniform Berry-Esseen bound to the first term in (83).

From (83), we have

| (86) |

which implies that

| (87) |

We have proved already that and as . Next, notice that

| (88) | ||||

where , and , so that . Recall that we already proved that

| (89) |

The expectation on the right-hand side of (88) can be written as

| (90) | ||||

for any . The second term is bounded from above by the Cauchy-Schwarz inequality

| (91) | ||||

as . The first term in (90) can be written furthermore as

| (92) | ||||

The second term in (92) is negative and is bounded in absolute value as

| (93) | ||||

as by the central limit theorem.

Next, we need to estimate the first term in (92). We first give an upper bound,

| (94) |

Next, we give a lower bound,

| (95) | ||||

This can be written further as

| (96) | ||||

By following the same argument as in (91), we have

| (97) |

The bounds (94) and (95) can be combined with the bounds (93) to obtain simpler bounds on the expectation in (92) in the limit. By (90)-(97), these bounds translate into corresponding bounds for the expectation (93). We get for any

| (98) | |||

and

| (99) |

Finally, take the limit, which gives

| (100) |

The non-uniform Berry-Esseen bound can be applied to compute the expectation on the right-hand side.

The sums of third moments appearing in the non-uniform Berry-Esseen bound are estimated as follows. Recalling that where are defined in terms of i.i.d. random variables as given in (84), we find

| (101) | ||||

where depends only on . Therefore, by the non-uniform Berry-Esseen bound, we have

| (102) |

for any , where is the cumulative distribution function of , and is another constant. Hence, we have, with

| (103) | ||||

which goes to zero as . We conclude that we have

| (104) |

as , where . The expectation is given explicitly by

| (105) |

This completes the proof of the asymptotics for the at-the-money call option . The asymptotics for the price of the at-the-money put option can be obtained by using put-call parity. The proof is complete. ∎

5. Asymptotics for Floating Strike Asian Options

We consider in this section the floating strike Asian options, which are a variation of the standard Asian option. The floating strike Asian call option with strike and weight has payoff at maturity and the floating strike put option has payoff at maturity .

The floating-strike Asian option is more difficult to price than the fixed-strike case because the joint law of and is needed. Also, the one-dimensional PDE that the floating-strike Asian price satisfies after a change of numéraire is difficult to solve numerically as the Dirac delta function appears as a coefficient, see e.g. [28], [42], [2]. See [41, 8, 27] for alternative methods which have been proposed to deal with this problem.

It has been shown by Henderson and Wojakowski [27] that the floating-strike Asian options with continuous time averaging can be related to fixed strike ones. These equivalence relations have been extended to discrete time averaging Asian options in [47]. According to these relations we have

| (106) | ||||

| (107) |

The expectations on the right-hand side are taken with respect to a different measure , where the asset price follows the process

| (108) |

with a standard Brownian motion in the measure.

We are interested in the asymptotics of the price of the Asian call/put options with payoffs and ,

| (109) | |||

| (110) |

As , a.s. When the call option is out-of-the-money and the put option is in-the-money. When , the call option is in-the-money and the put option is out-of-the-money. When , the call and put options are at-the-money.

For the expectations on the right-hand side of the equivalence relations (106), (107) we have that as , a.s. We conclude that for these equivalence relations map an out-of-money floating strike call (put) Asian option onto an out-of-money fixed strike put (call) Asian option. For a similar relation holds between the respective in-the-money Asian options.

Let us derive the asymptotics of the price of the floating strike Asian options. This could be expressed in terms of the asymptotics of the fixed strike Asian options obtained in the previous sections, with the help of the equivalence relations. An alternative way is to derive directly the large deviation result for the floating strike Asian options. Then we will relate the rate function to that for the fixed strike Asian options, and show that this is consistent with the equivalence relations.

We have the following result for the asymptotics of floating strike Asian options.

Proposition 17.

(i) When , the call option is out-of-the-money,

| (111) |

and the put option is in-the-money,

| (112) |

(ii) When , the put option is out-of-the-money

| (113) |

and the call option is in-the-money,

| (114) |

The rate function in (i) and (ii) is given by

| (115) |

(iii) When , the call and put options are in-the-money,

| (116) |

where is a normal random variable with mean and variance

| (117) |

Proof.

The proof is similar to the fixed-strike case. The sketch of the proof will be given in the Appendix. ∎

We show next that the rate function can be simply related to defined in (50). Recall that we showed explicitly the dependence of of the respective rate functions and . Abusing the notations a bit to emphasize the dependence on , let and . We have the following result, which is clearly consistent with the equivalence relations (106), (107).

Proposition 18.

The rate functions for the fixed strike and floating strike Asian options are related as

| (118) |

Proof.

The functionals in the variational problems for and are identical, and the only difference is in the constraints on . The constraints can be related as follows.

Let us express in the variational problem for in terms of a new function defined as . This function satisfies the constraint . The rate function is now given by

| (119) |

It is easy to see that this variational problem is identical to that for the rate function , identifying and . This concludes the proof of the relation (118). ∎

6. Implied volatility and numerical tests

It has become accepted market practice to quote European option prices in terms of their implied volatility. This is defined as that value of the log-normal volatility which, upon substitution into the Black-Scholes formula, reproduces the market option prices. A similar normal implied volatility can be defined in terms of the Bachelier formula.

Although Asian options are quoted in practice by price, and not by implied volatility, it is convenient to define an equivalent implied volatility also for these options. We will define the equivalent log-normal implied volatility of an Asian option with strike and maturity as that value of the volatility which reproduces the Asian option price when substituted into the Black-Scholes formula for an European option with the same parameters

| (120) | ||||

where

| (121) |

and

| (122) |

The equivalent log-normal volatility defined in this way exists for any Asian option call price satisfying the Merton bounds [43]. For finite the price of the Asian option is bounded as111The lower bound follows from the convexity of the payoff and the upper bound follows from . with , so the required bounds are satisfied for .

One can define also a normal equivalent volatility of an Asian option, as that volatility which reproduces the Asian option price when substituted into the Bachelier option pricing formula.

We would like to study the implications of the asymptotic results for Asian option prices derived in Section 4 for the equivalent log-normal volatility , and for the equivalent normal volatility . This is given by the following result.

Proposition 19.

i) The asymptotic normal and log-normal equivalent implied volatilities of an OTM Asian option in the limit at constant are given by

| (123) | ||||

| (124) |

where is related to the rate function as in (51), and is given by Proposition 9.

ii) The equivalent log-normal implied volatility for of an at-the-money Asian option is

| (125) |

and the corresponding result for the equivalent normal implied volatility is

| (126) |

Proof.

The proof is given in the Appendix. ∎

We note that in (123) depends implicitly on as the limit is taken at fixed . In particular, in the fixed maturity regime fixed, we have such that both and approach 0 as , in such a way that their ratio approaches a finite non-zero value. We will use this relation for finite to approximate the equivalent log-normal implied volatility as

| (127) |

and analogously for . These volatilities can be used together with (120) to obtain approximations for Asian option prices.

We show in Table 2 numerical results for the asymptotic approximation for the Asian options obtained from (120), for a few scenarios proposed in [20]. They are compared against a few alternative methods considered in the literature: the method of Linetsky [33], PDE methods [19, 50], inversion of Laplace transform [11, 44], and the log-normal approximation [32] corresponding to continuous-time averaging.

The numerical agreement of the asymptotic result with the precise results of the spectral expansion [33] is very good, and the difference is always below in relative value. A more appropiate test compares the difference to the option Vega : the approximation error of the asymptotic result is always below (compared with the log-normal approximation which has an error as large as (for scenario 7)). This is smaller than the typical precision on around the ATM point, and compares well with typical bid-ask spreads for Asian options which can be for maturities up to 1-2Y.

Remark 20.

We comment on the relation of the asymptotic implied volatility (123) to the log-normal approximation [32]. The log-normal approximation [32] corresponds to a flat equivalent log-normal volatility . In contrast, the asymptotic equivalent log-normal implied volatility given by (123) has a non-trivial dependence on strike. It can be easily shown that the log-normal implied volatility reproduces the asymptotic equivalent implied volatility at the ATM point in the limit .

The results of Table 2 show that the asymptotic result is an improvement over the log-normal approximation.

Remark 21.

The results of [20, 33] are obtained using continuous-time averaging, while our result (123) was derived for discrete time Asian options. However, we note that the result (123) does not depend on the size of the time step , so it should hold for arbitrarily small time step. It is shown elsewhere [40] that a result similar to (123) holds for the small maturity limit of continuous time Asian options at fixed , with the substitution . The limiting procedure adopted in this paper, of taking at fixed , allows one to take into account the dependence on in the short maturity expansion.

| Scenario | |||||

|---|---|---|---|---|---|

| 1 | 0.02 | 1 | 2 | 2 | 0.1 |

| 2 | 0.18 | 1 | 2 | 2 | 0.3 |

| 3 | 0.0125 | 2 | 2 | 2 | 0.25 |

| 4 | 0.05 | 1 | 1.9 | 2 | 0.5 |

| 5 | 0.05 | 1 | 2 | 2 | 0.5 |

| 6 | 0.05 | 1 | 2.1 | 2 | 0.5 |

| 7 | 0.05 | 2 | 2 | 2 | 0.5 |

| Scenario | FPP3 | MAE3 | Mellin500 | Vecer | PZ | LN | Linetsky |

|---|---|---|---|---|---|---|---|

| 1 | 0.055986 | 0.055986 | 0.056036 | 0.055986 | 0.055998 | 0.056054 | 0.055986 |

| 2 | 0.218387 | 0.218369 | 0.218360 | 0.218388 | 0.218480 | 0.219829 | 0.218387 |

| 3 | 0.172267 | 0.172263 | 0.172369 | 0.172269 | 0.172460 | 0.173490 | 0.172269 |

| 4 | 0.193164 | 0.193188 | 0.192972 | 0.193174 | 0.193692 | 0.195379 | 0.193174 |

| 5 | 0.246406 | 0.246382 | 0.246519 | 0.246416 | 0.246944 | 0.249791 | 0.246416 |

| 6 | 0.306210 | 0.306139 | 0.306497 | 0.306220 | 0.306744 | 0.310646 | 0.306220 |

| 7 | 0.350040 | 0.349909 | 0.348926 | 0.350095 | 0.351517 | 0.359204 | 0.350095 |

In order to address the performance of the asymptotic results in the small volatility and maturity regime we compare our results against those in Table 4 of [19]. As pointed out in [44, 20], some of the methods proposed in the literature have numerical issues in these regimes of the model parameters. The scenarios considered for this test correspond to , and three choices of maturity and strike as shown in Table 3. For reasons of space economy, we present only a subset of the test results in Table 4 of [19], which show the best agreement with a Monte Carlo calculation. The asymptotic results are in very good agreement with the alternative methods shown. We note that the computing time required by the asymptotic method is very good, as it requires only the solution of a simple non-linear algebraic equation, and the evaluation of a function.

| PZ | FPP3 | MAE3 | Mellin500 | ||

|---|---|---|---|---|---|

| 0.25 | 99 | 1.60739 | |||

| 0.25 | 100 | 0.621359 | |||

| 0.25 | 101 | 0.0137615 | |||

| 1.00 | 97 | 5.2719 | |||

| 1.00 | 100 | 2.41821 | |||

| 1.00 | 103 | 0.0724339 | |||

| 5.00 | 80 | 26.1756 | |||

| 5.00 | 100 | 10.5996 | |||

| 5.00 | 120 |

We present in Table 4 a comparison with the test results for discretely sampled Asian options corresponding to the scenarios considered in Table B of [50]. These scenarios have parameters . The results are compared against those obtained in [50, 45, 9]. The asymptotic results agree with the alternative methods up to about 1%-1.5% in relative error.

| Vecer | |||

| 8.4001 | 11.1600 | 14.3073 | |

| 8.3826 | 11.1416 | 14.2881 | |

| 8.3741 | 11.1322 | 14.2786 | |

| 8.3661 | 11.1233 | 14.2696 | |

| Tavella-Randall | |||

| 8.3972 | 11.1573 | 14.3054 | |

| 8.3804 | 11.1392 | 14.2866 | |

| 8.3719 | 11.1300 | 14.2771 | |

| 8.3640 | 11.1215 | 14.2681 | |

| Curran | |||

| 8.3972 | 11.1572 | 14.3048 | |

| 8.3801 | 11.1388 | 14.2857 | |

| 8.3715 | 11.1296 | 14.2762 | |

| PZ | 8.3789 | 11.1362 | 14.2818 |

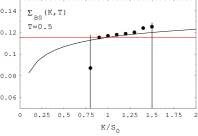

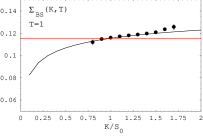

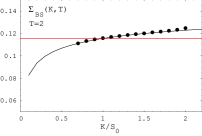

Finally, in order to test the asymptotic relation (123) for the equivalent log-normal implied volatility we show in Figure 2 the equivalent log-normal implied volatility of several Asian options obtained by numerical simulation (black dots). These results are obtained by Monte Carlo pricing of Asian options with parameters

| (128) |

and averaging dates. The Monte Carlo calculation used samples. The strikes considered cover a region around the ATM point ; the numerical precision of the simulation decreases rapidly outside of this region. We note very good agreement with the asymptotic result of Proposition 19, even for as low as 50.

Acknowledgements

We are grateful to an anonymous referee and the editor for their helpful comments and suggestions. D. P. would like to thank Dyutiman Das and Roussen Roussev for useful discussions about Asian options in financial practice. L. Z. is partially supported by NSF Grant DMS-1613164.

7. Appendix

Proof of Proposition 4.

The variational problem appearing in equation (39) can be written equivalently by introducing the function as

| (129) |

The functional appearing in this variational problem can be rewritten as

| (130) | ||||

In the second line we integrated by parts and wrote where we took into account the constraint . Although in Proposition 4 we have , the variational problems in Section 4 require also the case of negative . For this reason we will treat here both cases of positive and negative .

The optimal function satisfies the Euler-Lagrange equation

| (131) |

with the boundary conditions

| (132) |

The second boundary condition (at ) is a transversality condition.

We observe that the quantity

| (133) |

is a constant of motion of the differential equation (131). Its value was expressed in terms of by taking and using the boundary condition (132). Taking the integral of this relation over can be used to eliminate the integral of in the functional . This can be put into the equivalent form

| (134) |

The Euler-Lagrange equation (131) can be solved exactly. Two independent solutions of this equation are

| (135) | ||||

| (136) |

The first solution was given in [26] where a related differential equation appears in the context of optimal sampling for Monte Carlo pricing of Asian options. It is easy to see by direct substitution into (131) that these functions satisfy this equation, with the appropriate boundary condition at . Requiring that the coefficient in this equation and the boundary condition are satisfied gives two conditions.

For we have the conditions

| (137) |

Eliminating between these two equations as gives an equation for :

| (138) |

For we obtain the conditions

| (139) |

The second relation allows one to eliminate as

| (140) |

We obtain the equation for

| (141) |

Finally, the integral appearing in can be computed in closed form for each solution, and we have

| (142) | |||

| (143) |

Substituting these results into (134), we find the following results for the function

| (144) | |||

| (145) | |||

where and are given by the solutions of the equations (138) and (141), respectively. For given , only one of these two equations has a solution, which determines the optimal function uniquely, and the function . This completes the proof of Proposition 4. ∎

Proof of Proposition 9.

The variational problem (50) can be written equivalently in terms of defined as in (51), by introducing the function as

| (146) |

The integral constraint on is taken into account by introducing a Lagrange multiplier and defining an auxiliary functional

| (147) | ||||

The solution of this variational problem satisfies the Euler-Lagrange equation

| (148) |

with boundary conditions (the condition at is a transversality condition)

| (149) |

This differential equation and the associated boundary conditions are identical to the equation appearing in the proof of Proposition 4. As shown, this can be solved exactly, and the solutions are given in (135), (136). The details of the proof will be slightly different, as in the present case the coefficient (the Lagrange multiplier) is not known, but is one of the unknowns of the variational problem. However, we will show that it can be determined using the integral constraint

| (150) |

Before proceeding with the solution of the variational problem, we give a preliminary result which expresses the rate function only in terms of .

Lemma 22.

The rate function is given by

| (151) |

Proof.

The Euler-Lagrange equation (148) conserves the following quantity

| (152) |

which gives

| (153) |

Taking the integral of this relation over , and using the constraint (150) gives the result (151).

∎

The only remaining part of the proof is determining . This can be done from the constraint (150). Substituting (135) into this constraint gives

| (154) |

which is an equation for . This equation has solutions only for . Once are known, the Lagrange multiplier is determined using the relation (137). Substituting into (151) we find the rate function

| (155) | ||||

A similar calculation using gives

| (156) |

Both and must be in the range. The equation (156) has solutions only for .

Using the solution for , the Lagrange multiplier is found from (139). Substituting into (151) we find the rate function

| (157) |

This completes the proof of Proposition 9.

∎

Proof of Proposition 17.

Start by noting that can be written equivalently as in distribution where are i.i.d. random variables. Let us also recall that . The terms , are uniformly bounded and negligible and if we let , then . The map is continuous in the supremum norm and by contraction principle, satisfies a large deviation principle with the rate function

| (158) |

As , a.s. When , the call option is out-of-the-money and

| (159) |

and by put-call parity, when ,

| (160) | ||||

Therefore, as , the asymptotics for in-the-money put option is

| (161) |

When ,

| (162) |

When , i.e., at-the-money, the asymptotics for and are governed by the central limit theorem. can be approximated by

| (163) |

with i.i.d. random variables. The variance of this expression converges to

| (164) | ||||

We can further use the nonuniform Berry-Esseen bound for the central limit theorem to obtain the following asymptotics,

| (165) |

where is a normal random variable with mean and variance

| (166) |

When , the put option is out-of-the-money and

| (167) |

and when , we have for in-the-money call option

| (168) |

and when ,

| (169) |

∎

Proof of Proposition 19.

i) The price of an undiscounted European option in the Black-Scholes model depends only on and with the forward asset price. In our case given by (120) we have , and we denote this dependence as , with .

By definition of the equivalent log-normal implied volatility we have

| (170) |

We get thus, setting ,

Recalling that this is written equivalently as

| (174) |

which reproduces the result (123).

ii) At-the-money Asian option. The Black-Scholes formula gives for this case

| (175) | ||||

The large asymptotics of the ATM Asian option given in Proposition 15 reads

| (176) |

The two results are related as . Recalling that we have we obtain the asymptotics of the equivalent implied volatility of the ATM Asian option

| (177) |

This reproduces equation (125).

The proof of (124) proceeds in a similar way, starting with the Bachelier formula for the call option prices.

∎

References

- [1] Andreasen, J. (1998). The pricing of discretely sampled Asian and lookback options: A change of numeraire approach. J. Comp. Finance 2, 5-23.

- [2] Alziary, B., Decamps, J. P., and Koehl, P. F. (1997). A PDE approach to Asian options: Analytical and Numerical evidence. Journal of Banking and Finance. 21, 613-640.

- [3] Asmussen, S., Jensen, J. L. and Rojas-Nandayapa, L. (2011). A literature review on log-normal sums. University of Queensland preprint.

- [4] Berestycki, H., Busca, J. and Florent, I. (2004). Computing the implied volatility in stochastic volatility models. Communications on Pure and Applied Mathematics. LVII, 1352-1373.

- [5] Bikelis, A. (1966). Estimates of the remainder term in the central limit theorem. Litovsk. Mat. Sb. 6, 323-346.

- [6] Carr, P. and Madan, D. (1999). Option valuation using the fast Fourier transform. J. Comp. Finance. 2(4), 61-73.

- [7] Carr, P. and Schröder, M. (2003). Bessel processes, the integral of geometric Brownian motion, and Asian options. Theory of Probability and its Applications. 48, 400-425.

- [8] Chung, S. L., Shackleton, M. and Wojakowski, R. (2000). Efficient quadratic approximation of floating strike Asian option values. Working paper, Lancaster University Management School.

- [9] Curran, M. (1994). Valuing Asian options and portfolio options by conditioning on the geometric mean price. Management Science 40, 1705-1711.

- [10] A. Dembo and Zeitouni, O. (1998). Large Deviations Techniques and Applications. 2nd Edition, Springer, New York.

- [11] Dewynne, J. N. and Shaw, W T. (2008) Differential equations and asymptotic solutions for arithmetic Asian options: ‘Black-Scholes formulae’ for Asian rate calls. European J. Appl. Math. 19, 353-391.

- [12] Dewynne, J. N. and Wilmott, P. (1995). A note on average rate options with discrete sampling. SIAM J. Appl. Math. 55, 267-276.

- [13] Donati-Martin, C., Ghomrasni, R. and Yor, M. (2001). On certain Markov processes attached to exponential functionals of Brownian motion; application to Asian options. Rev. Math. Iberoam. 17, 179-193.

- [14] Dufresne, D. (1990). The distribution of a perpetuity with applications to risk theory and pension funding. Scand. Act. J. 9, 39-79.

- [15] Dufresne, D. (2004). The log-normal approximation in financial and other computations. Adv. Appl. Prob. 36, 747-773.

- [16] Dufresne, D. (2005). Bessel processes and a functional of Brownian motion, in M. Michele and H. Ben-Ameur (Ed.), Numerical Methods in Finance, 35-57, Springer.

- [17] Feng, J., Forde, M. and Fouque, J. P. (2010). Short maturity asymptotics for a fast mean-reverting Heston stochastic volatility model. SIAM Journal on Financial Mathematics. 1, 126-141.

- [18] Forde, M. and Jacquier, A. (2009). Small time asymptotics for implied volatility under the Heston model. International Journal of Theoretical and Applied Finance. 12, 861-876.

- [19] Foschi, P., Pagliarani, S. and Pascucci, A. (2013). Approximations for Asian options in local volatility models. Journal of Computational and Applied Mathematics. 237, 442-459.

- [20] Fu, M., Madan, D. and Wang, T. (1998). Pricing continuous time Asian options: a comparison of Monte Carlo and Laplace transform inversion methods. J. Comput. Finance. 2, 49-74.

- [21] Fusai, G., Marazzina, D. and Marena, M. (2011). Pricing discretely monitored Asian options by maturity randomization SIAM J. Fin. Math. 2, 383-403.

- [22] Fusai, G., Marena, M. and Roncoroni, A. (2008). Analytical pricing of discretely monitored Asian-Style options: Theory and application to commodity markets, Journal of Banking and Finance 32, 2033-2045.

- [23] Fusai, G. and Meucci, A. (2008). Pricing of discretely monitored Asian options under Lévy processes Journal of Banking and Finance 32, 2076-2088.

- [24] Geman, H. and Yor, M. (1993). Bessel processes, Asian options and perpetuities. (1993). Math. Fin. 3, 349-375.

- [25] Gatheral, J. , Hsu, E. P., Laurent, P. Ouyang, C. and T.-H. Wang (2012). Asymptotics of implied volatility in local volatility models. Math. Fin. 3, 591-620.

- [26] Guasoni, P. and Robertson, S. (2008). Optimal importance sampling with explicit formulas in continuous time, Fin. Stoch. 12, 1-19.

- [27] Henderson, V. and Wojakowski, R. (2002). On the equivalence of floating and fixed-strike Asian options, J. Appl. Prob. 39, 391-394.

- [28] Ingersoll, J. (1988). Theory of Financial Decision Making. Rowman and Littlefeild, Totowa, NJ.

- [29] Kemna, A. G. and Vorst, A. C. F. (1990). A pricing method for options based on average asset values. Journal of Banking and Finance. 14, 113-130.

- [30] Lapeyre, B. and Teman, E. (1999). Competitive Monte Carlo methods for pricing Asian options. Working paper, CERMICS, Ecole Nationale des Points et Chaussees.

- [31] Laub, P. J. , S. Asmussen, J. L. Jensen and L. Rojas-Nandayapa (2015). Approximating the Laplace transform of the sum of dependent log-normals. Adv. Appl. Prob. 48(A), 203-215.

- [32] Levy, E. (1992). Pricing European average rate currency options. Journal of International Money and Finance. 11, 474-491.

- [33] Linetsky, V. (2004). Spectral expansions for Asian (average price) options. Operations Research 52, 856-867.

- [34] V. Linetsky. (2002). Exotic spectra. Risk. 15, 85-89.

- [35] Lord, R. (2006). Partially exact and bounded approximations for arithmetic Asian options. J. Comp. Finance 10(2), 1-52 (2006).

- [36] Milevsky, M., and Posner, S. (1998). Asian options, the sum of lognormals, and the reciprocal gamma distribution. J. Fin. Quant. Analysis 33, 409-442.

- [37] Nagaev, S. V. (1965). Some limit theorems for large deviations. Teor. Verojatnost. i Primenen. 10, 231-254.

- [38] Pinelis, I. (2013). On the nonuniform Berry-Esseen bound. arXiv:1301.2828.

- [39] Pirjol, D. and Zhu, L. (2016). Discrete sums of geometric Brownian motions, annuities and Asian options. Insurance: Mathematics and Economics. 70, 19-37.

- [40] Pirjol, D. and Zhu, L. (2016). Short maturity Asian options in local volatility models. Working paper.

- [41] Ritchken, P., Sankarasubramanian, L, and Vijh, A. M. (1993). The valuation of path-dependent contracts on the average. Management Science. 39, 1202-1213.

- [42] Rogers, L. C. G. and Shi, Z. (1995). The value of an Asian option. J. Appl. Prob. 32, 1077-1088.

- [43] Roper, M. and M. Rutkowski (2009). On the relationship between the call price surface and the implied volatility surface close to expiry. IJTAF 12, 427-441.

- [44] Shaw, W. T. (2003). Pricing Asian options by contour integration, including asymptotic methods for low volatility. Working paper.

- [45] Tavella, D. and Randall, C. (2000). Pricing financial instruments - the finite difference method. Wiley.

- [46] Tehranchi, M. (2009). Asymptotics of implied volatility far from maturity. Journal of Applied Probability. 46, 629-650.

- [47] Vanmaele, M., Deelstra, G., Liinev, J., Dhaene, J. and Goovaerts, M. J. (2006). Bounds for the price of discrete arithmetic Asian options. J. Comp. Appl. Math. 185, 51-90.

- [48] Varadhan, S. R. S. (1984). Large Deviations and Applications, SIAM, Philadelphia.

- [49] Vecer, J. (2001). A new PDE approach for pricing arithmetic average Asian options, J. Comp. Finance 4(4), 105-113.

- [50] Vecer, J. (2002). Unified Asian pricing. Risk. 15, 113-116.

- [51] Vecer, J. and Xu, M. (2004). Pricing Asian options in a semimartingale model. Quantitative Finance. 4, 170-175.

- [52] Vecer, J. (2014). Black-Scholes representation for Asian options. Math. Finance. 24, 598-626.

- [53] Wong, E. (1964). The construction of a class of stationary Markoff processes, in R. Bellman (ed.), Stochastic processes in mathematical physics and engineering, Providence, R. I.: AMS, 264-276.