The effect of the behavior of an average consumer on the public debt dynamics

Abstract

An important issue within the present economic crisis is understanding the dynamics of the public debt of a given country, and how the behavior of average consumers and tax payers in that country affects it. Starting from a model of the average consumer behavior introduced earlier by the authors, we propose a simple model to quantitatively address this issue. The model is then studied and analytically solved under some reasonable simplifying assumptions. In this way we obtain a condition under which the public debt steadily decreases.

pacs:

89.65GhI Introduction

Understanding consumption is a key issue in macroeconomics. The links between individual consumption decisions and outcomes for the whole economy have been deeply investigated by A. Deaton DeatonBook , who was awarded the Nobel prize in 2015 NobelPrize . In fact, since the beginning, research focused on the relation between income (and the interest rate) and consumption. Within this framework, Friedman’s permanent income hypothesis friedman and Modigliani’s life-cycle theory modigliani1 ; modigliani2 ; modigliani3 contributed to suggest how income variables might enter the consumption function. In particular life-cycle theory provides a useful framework for thinking about saving and related mechanism, and paves the way for undestanding the link between saving and growth of a country. Furthermore, the theory predicts that saving rates are higher in more rapidly growing economies, even in the short run, therefore establishing a correlation between growth and savings rates. However, more recent studies pointed out that the range of applicability of the above mechanism is quite limited study1 ; study2 ; study3 ; study4 , so that it alone does not succeed in explaining the international correlation between saving and economic growth.

Macroeconomists and policy-makers have traditionally been concerned with the issue of the sustainability of public debt in developing and emerging market countries. However, starting from the appearance of the global financial crisis, the attention has been shifted to developed economies, which suffer from rising debt-Gross Domestic Product (GDP) ratios in the face of stagnant or contracting output. As a matter of fact, in most European countries debt is at an unprecedented level in the last fifty years. In some cases, the increases since 2007 have exceeded 20 percentage points of GDP while the level of the debt was already high consolidation1 .

The correct definition and measurement of public debt were given by barro ; DeHaan . The relation between public debt and economic growth is the object of much work today GreinerFincke ; Herndon ; Panizza ; Smyth ; Nastanski1 ; Reichlin . If debt growth rates are lower than those of GDP, the debt is not bad. The economic growth restores the income part of the budget, which is used to pay interest on debt. Vice versa, with low economic growth rates, public debt becomes a serious macroeconomic problem for the country. In such a case governments have to pay a large amount of public revenue to the creditors, which results in fewer resources for education and public investments. An unsustainable level of debt is obtained in correspondence to a high debt to GDP ratio Nastanski1 . In particular, interest rates rise on the basis of a greater probability of a default on debt obligations, with a negative influence on private investment and consumption. The debt-relief Laffer curve Miles provides information about the negative impact of high debt on output growth; in particular a point can be found, where outstanding debt is so large that output growth gets reduced and the probability of debt repayment lowers. In this scenario, inflation could be a viable solution to the government debt problem inflation1 ; inflation2 , while the effectiveness of fiscal consolidation and of austerity requirements, such as the reduction in governments expenditure, is widely debated (see e.g. consolidation1 and references therein).

Actually, new provisions in the Stability and Growth Pact (SGP) require European countries with a debt to GDP ratio higher than 60 per cent to act to decrease it in the next few years. It is thus important to assess under which conditions this is possible. This is the purpose of the present paper, in which a simple model is proposed to try to find such conditions.

Since the model uses the representative agent framework, it is subject to all its limitations, as it does not take into account the differences between individuals. The use of the representative agent in economy has been criticized mainly in Kirman1992 . Progress in providing alternatives to the ad hoc assumptions of the representative agent approach has recently been made by using the tools of Statistical Mechanics (see e.g. DeMartinoMarsili1 and references therein).

Another related limiting aspect of the present analysis concerns the absence of private enterprises in this scenario. In fact, the presence of this type of agent can generate earnings that can substantially help in paying back public debt. However, if we assume that the economic behavior of private enterprises can be included in the representative agent picture, the present model could be still adopted in this more general setting.

In a previous paper noi the authors proposed a simple mathematical model, based on a hydrodynamic analog, to quantitatively describe the time evolution of the amount of money an average consumer decides to spend, depending on his/her available budget. In the present paper we couple this model, or better, its difference equation version, to the standard equation for the time evolution of the public debt given in ref. barro . The resulting dynamical model is then analytically solved under some reasonable simplifying assumptions. The result is a range of the parameters of the model for which the public debt steadily decreases. The model is presented in Section 2, and its dynamics is studied in Section 3. Finally, in Section 4, some conclusions are drawn, and some comments and perspectives of our work are outlined.

II The model

The typical strategy adopted by a Government to decrease its public debt is to burden the average consumer with additional taxation, which may also be applied to the amount of money present, at a certain date, on the consumer’s bank account. Let us write the tax payed by a single average consumer in the k-th year by

| (1) |

where is the yearly income, which we assume fixed, is the average yearly bank deposit, and is the yearly expenditure of the consumer. , and are the average taxation rates for these quantities, respectively. The Kronecker delta picks a fraction of the amount only in the m-th year.

The dynamics of the public debt . calculated at the year and normalized to the number of consumers, is described by the difference equation barro

| (2) |

where is the yearly pro capite deficit at the time , is the fixed rate of return on public and private debts, is the pro capite amount of money the State utilizes for funding education, health, welfare, and all public activities. Plugging (1) into (2) we get

| (3) |

To describe the behavior of the consumer we may adopt the leaking bucket model noi :

| (4) |

where is the expendable part of the salary, i.e. . Substituting this definition into (4), we get

| (5) |

Substituting as in noi 111we assume that all consumers have no debts, i.e. a positive budget, cfr. noi we get

| (6) |

This equation should of course be coupled to the public debt evolution equation (3). Let us now study the latter with the simplifying assumption and the functional relation :

| (7) |

or

| (8) |

where we defined . The solution of this difference equation is

| (9) |

The sum in the above equation is

so that

| (11) | |||||

In the above two equations it is understood that the last term is present only if . We notice that the first equality in eq. (II) is similar to the formula for the price of a coupon bond Baaquie .

III Maximum State expense in paying back public debt

In this section we study the dynamics governed by Eqs. (6) and (11) under some specific simplifying assumptions. First of all, we exclude the possibility of direct taxation of the amount , so that . Also, we take , since in many countries these rates are in fact quite close. In this way, Eqs. (6) and (11) get rewritten respectively as

| (12) |

and

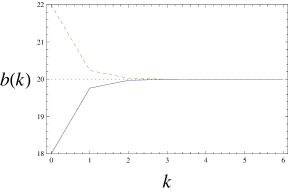

In Fig.1 we show the dynamics of the consumer budget described by Eq.(12), where we set and , and we assume that , as is reasonable for an average consumer in a european country. We notice that the fixed point is reached after few steps.

Let us find the fixed point of Eq.(12). The condition gives

| (14) |

Assuming that the average consumer does indeed start with an initial budget close to , we may rewrite Eq. (III) as follows

| (15) | |||||

The public debt starts decreasing if there is some value of such that . This implies the independent relation

| (16) |

If this condition is met, then, a independent decrease of the public debt is possible, therefore reducing the debt to GDP ratio, as required by SGP. For example, in a country where , , Eq. (16) reads

| (17) |

If , we have , which indicates that the value of cannot be higher of , in order to have decreasing values of for .

This result tells that decreasing the salaries and wages of consumers may not be the right choice for a government to reduce the public debt.

IV The rôle of the public expenditure

In this section we consider our model under some more general assumptions. In particular we relax the assumption that the public expenditure is constant. Moreover we consider a more general income-expenditure relation for the consumer, i.e.

| (18) |

where we excluded a linear behavior in order to model the existence of a threshold. In this case the stable fixed point is given by

| (19) |

Assuming as above that the consumer is in proximity of this fixed point we get, in place of Eq. (15):

| (20) | |||||

Notice that the assumption of being at the fixed point has again erased the dependence on the coefficient . The condition in this case gives

| (21) |

where is the expenditure at year 1. Let us now assume that the expenditure in the subsequent years has the form

| (22) |

where . In this way , so that the sign of determines wether the public expenditure grows or decreases over the years. The condition (23) then specializes to

| (23) |

where . For the last term in the rhs is negligible, therefore our conclusions of the previous section are still valid.

V Discussion and conclusions

In this paper, building on a simple quantitative description of the behavior of an average consumer over a brief period noi , and on Barro’s theory of the public debt barro , we propose a model for the description of the influence of the former on the dynamics of the public debt, with the aim of establishing the condition for its decrease. Our result are clearly limited in scope by the use of the concept of average consumer and by the fact that it is valid only over a short period. We obtained analytical results under the simplifying assumptions of equal average taxation rates for the yearly income and expenditure of the consumer, respectively. Furthermore the possibility of direct taxation of consumer’s average yearly bank deposit has been excluded. Besides extending the model to overcome its shortcomings, it would be interesting to further relax the above simplifying assumptions and see when and how the condition we found gets enhanced.

An interesting issue to investigate is how the above results would get modified by generalizing the leaking bucket model for the average consumer behavior noi , in such a way to include the effect of different goods on the level of consumer demand.

Another interesting generalization of the present model could be the inclusion of private enterprises as a different agent in the economic landscape.

The proposed model could finally be rephrased in terms of the debt to GDP ratio in order to study the impact of fiscal consolidations on public debt dynamics and how it is related to fiscal multipliers consolidation1 .

Author contribution statement

All the authors contributed equally to the paper.

References

- (1) A. Deaton, Understanding Consumption, Clarendon Press, Oxford, 1992.

- (2) http://www.nobelprize.org/nobel_prizes/economic-sciences/laureates/2015/announcement.html

- (3) M. Friedman, A theory of the consumption function, Princeton University Press, Princeton, 1957.

- (4) F. Modigliani, Social Research 33, (1966) 160.

- (5) F. Modigliani, in: Induction, growth and trade: Essays in Honour of Sir Roy Harrod, W. A. Eltis et al. (Eds.), Clarendon Press, London, 1970.

- (6) F. Modigliani, American Economic Review 76 (1986), 297.

- (7) C. D. Carroll, L. H. Summers, in: National saving and economic performance, B. D. Bernheim and J. B. Shoven (Eds.), Chicago University Press, Chicago, 1991.

- (8) B. Bosworth, G. Burtless, G. Sabelhaus, Brookings Papers on Economic Activity 1 (1991), 183.

- (9) C. Paxson, European Economic Review 40 (1996), 255.

- (10) A. Deaton, C. Paxson, Review of Economics and Statistics 82 (2000), 212.

- (11) J. Boussard, F. de Castro, M. Salto, Fiscal Multipliers and Public Debt Dynamics in Consolidations, European Economy - Economic Papers 2008-2015, European Commission, n. 460 (2012).

- (12) R. J. Barro, Journal of Political Economy 87, (1979) 940.

- (13) J. De Haan, De Economist 135(3) (1987), 367.

- (14) A. Greiner, B. Fincke, Public Debt, Sustainability and Economic Growth: Theory and Empirics, Springer (2015).

- (15) T. Herndon, M. Ash, R. Pollin, Camb. Jour. Economics 38 (2014), 257.

- (16) U. Panizza, A. F. Presbitero, Swiss Jour. Econ. Stat., 149 (2013), 175.

- (17) D. J. Smyth, Y. Hsing, Contemp. Econ. Policy 13 (1995), 51.

- (18) A. Nastansky, H. G. Strohe, Econometrics 1(47) (2015), 9.

- (19) A. Caruso, L. Reichlin, G. Ricco, The Legacy Debt and the Joint Path of Public Deficit and Debt in the Euro Area, European Economy Discussion Papers, n. 010 (2015).

- (20) D. Miles, A. Scott, F. Breedon, Macroeconomics: Understanding the Global Economy, Wiley (2012).

- (21) C. M. Reinhart, K. S. Rogoff, This Time is Different: Eight Centuries of Financial Folly, Princeton University Press, Princeton, 2009.

- (22) C. M. Reinhart, M. Sbrancia, The liquidation of government debt, NBER Working Paper Series, n. 16893 (2011).

- (23) A. P. Kirman, J.Econ.Persp. 6 (1992), 117.

- (24) A. De Martino, M. Marsili, J. Phys. A: Math. Gen. 39 (2006), R465.

- (25) R. De Luca, M. Di Mauro, A. Falzarano and A. Naddeo, Eur. Phys. J. B 89 (2016), 184.

- (26) B. E. Baaquie, Interest Rates and Coupon Bonds in Quantum Finance, Cambridge University Press, Cambridge, 2010.