Multivariate Geometric Skew-Normal Distribution

Abstract

Azzalini [3] introduced a skew-normal distribution of which normal distribution is a special case. Recently Kundu [9] introduced a geometric skew-normal distribution and showed that it has certain advantages over Azzalini’s skew-normal distribution. In this paper we discuss about the multivariate geometric skew-normal distribution. It can be used as an alternative to Azzalini’s skew normal distribution. We discuss different properties of the proposed distribution. It is observed that the joint probability density function of the multivariate geometric skew normal distribution can take variety of shapes. Several characterization results have been established. Generation from a multivariate geometric skew normal distribution is quite simple, hence the simulation experiments can be performed quite easily. The maximum likelihood estimators of the unknown parameters can be obtained quite conveniently using expectation maximization (EM) algorithm. We perform some simulation experiments and it is observed that the performances of the proposed EM algorithm are quite satisfactory. Further, the analyses of two data sets have been performed, and it is observed that the proposed methods and the model work very well.

Key Words and Phrases: Skew-normal distribution; moment generating function; infinite divisible distribution; maximum likelihood estimators; EM algorithm; Fisher information matrix.

AMS 2000 Subject Classification: Primary 62F10; Secondary: 62H10

1Department of Mathematics and Statistics, Indian Institute of Technology Kanpur, Kanpur, Pin 208016, India. e-mail: kundu@iitk.ac.in.

1 Introduction

Azzalini [3] proposed a class of three-parameter skew-normal distributions which includes the normal one. Azzalini’s skew normal (ASN) distribution has received a considerable attention in the last two decades due to its flexibility and its applications in different fields. The probability density function (PDF) of ASN takes the following form:

where and denote the standard normal PDF and standard normal cumulative distribution function (CDF), respectively, at the point . Here , and are known as the location, scale and skewness or tilt parameters, respectively. ASN distribution has an unimodal PDF, and it can be both positively or negatively skewed depending on the skewness parameter. Arnold and Beaver [2] provided an interesting interpretation of this model in terms of hidden truncation. This model has been used quite effectively to analyze skewed data in different fields due to its flexibility.

Later Azzalini and Dalla Valle [5] constructed a multivariate distribution with skew normal marginals. From now on we call it as Azzalini’s multivariate skew-normal (AMSN) distribution, and it can be defined as follows. A random vector is a -dimensional AMSN distribution, if it has the following PDF

where denotes the PDF of the -dimensional multivariate normal distribution with standardized marginals, and correlation matrix . We denote such a random vector as SN. Here the vector is known as the shape vector, and it can be easily seen that the PDF of AMSN distribution is unimodal and can take different shapes. It has several interesting properties, and it has been used quite successfully to analyze several multivariate data sets in different areas because of its flexibility.

Although ASN distribution is a very flexible distribution, it cannot be used to model moderate or heavy tail data; see for example Azzalini and Capitanio [4]. It is well known to be a thin tail distribution. Since the marginals of AMSN are ASN, multivariate heavy tail data cannot be modeled by using AMSN. Due to this reason several other skewed distributions, often called skew-symmetric distributions, have been suggested in the literature using different kernel functions other than the normal kernel function and using the same technique as Azzalini [3]. Depending on the kernel function the resulting distribution can have moderate or heavy tail behavior. Among different such distributions, skew-t distribution is quite commonly used in practice, which can produce heavy tail distribution depending on the degrees of freedom of the associated -distribution. It has a multivariate extension also. For a detailed discussions on different skew-symmetric distribution, the readers are referred to the excellent monograph by Azzalini and Capitanio [4].

Although ASN model is a very flexible one dimensional model, and it has several interesting properties, it is well known that computing the maximum likelihood estimators (MLEs) of the unknown parameters of an ASN model is a challenging issue. Azzalini [3] has shown that there is a positive probability that the MLEs of the unknown parameters of a ASN model do not exist. If all the data points have same sign, then the MLEs of unknown parameters of the ASN model may not exist. The problem becomes more severe for AMSN model, and the problem exists for other kernels also.

Recently, the author [9] proposed a new three-parameter skewed distribution, of which normal distribution is a special case. The proposed distribution can be obtained as a geometric sum of independent identically distributed (i.i.d.) normal random variables, and it is called as the geometric skew normal (GSN) distribution. It can be used quite effectively as an alternative to an ASN distribution. It is observed that the GSN distribution is a very flexible distribution, as its PDF can take different shapes depending on the parameter values. Moreover, the MLEs of the unknown parameters can be computed quite conveniently using the EM algorithm. It can be easily shown that the ‘pseudo-log-likelihood’ function has a unique maximum, and it can be obtained in explicit forms. Several interesting properties of the GSN distribution have also been developed by Kundu [9].

The main aim of this paper is to consider the multivariate geometric skew-normal (MGSN) distribution, develop its various properties and discuss different inferential issues. Several characterization results and dependence properties have also been established. It is observed that the generation from a MGSN distribution is quite simple, hence simulation experiments can be performed quite conveniently. Note that the -dimensional MGSN model has unknown parameters. The MLEs of the unknown parameters can be obtained by solving non-linear equations. We propose to use EM algorithm, and it is observed that the ’pseudo-log-likelihood’ function has a unique maximum, and it can be obtained in explicit forms. Hence, the implementation of the EM algorithm is quite simple, and the algorithm is very efficient. We perform some simulation experiments to see the performances of the proposed EM algorithm and the performances are quite satisfactory. We also perform the analyses of two data sets to illustrate how the proposed methods can be used in practice. It is observed that the proposed methods and the model work quite satisfactorily.

The main motivation to introduce the MGSN distribution can be stated as follows. Although there are several skewed distributions available in one-dimension, the same is not true in . The proposed MGSN distribution is a very flexible multivariate distribution which can produce variety of shapes. The joint PDF can be unimodal or multimodal and the marginals can have heavy tails depending on the parameters. It has several interesting statistical properties. Computation of the MLEs can be performed in a very simple manner even in high dimension. Hence, if it is known that the data are obtained from a multivariate skewed distribution, the proposed model can be used for analysis purposes. Generating random samples from a MGSN distribution is quite simple, hence any simulation experiment related to this distribution can be performed quite conveniently. Further, it is observed that in one of our data example the MLEs of AMSN do not exist, whereas the MLEs of MGSN distribution exist. Hence, in certain cases the implementation of MGSN distribution becomes easier than the AMSN distribution. The proposed MGSN distribution provides a choice to a practitioner of a new multivariate skewed distribution to analyze multivariate skewed data.

Rest of the paper is organized as follows. In Section 2, first we briefly describe the univariate GSN model, and discuss some of its properties, and then we describe MGSN model. Different properties are discussed in Section 3. In Section 4, we discuss the implementation of the EM algorithm, and some testing of hypotheses problems. Simulation results are presented in Section 5. The analysis of two data sets are presented in Section 6, and finally we conclude the paper in Section 7.

2 GSN and MGSN Distributions

We use the following notations in this paper. A normal random variable with mean and variance will be denoted by N. A -variate normal random variable with mean vector and dispersion matrix will be denoted by N. The corresponding PDF and CDF at the point will be denoted by and , respectively. A geometric random variable with parameter will be denoted by GE, and it has the probability mass function (PMF): for

2.1 GSN Distribution

Suppose GE and are i.i.d. Gaussian random variables. It is assumed that and ’s are independently distributed. Then the random variable

is known as GSN random variable and its distribution will be denoted by GSN. Here, ‘’ means equal in distribution. The GSN distribution can be seen as one of the compound geometric distributions. The PDF of takes the following form:

When = 0 and = 1, we say that has a standard GSN distribution, and it will be denoted by GSN.

The standard GSN is symmetric about 0, and unimodal, but the PDF of GSN can take different shapes. It can be unimodal or multimodal depending on , and values. The hazard function is always an increasing function. If GSN, then the moment generating function (MGF) of becomes

| (1) |

where

The corresponding cumulant generating (CGF) function of is

| (2) |

From (2), the mean, variance, skewness and kurtosis can be easily obtained as

| (3) | |||||

| (4) | |||||

respectively. It is clear from the expressions of (3) and (4) that as , and diverge to . It indicates that GSN model can be used to model heavy tail data. It has been shown that the GSN law is infinitely divisible, and an efficient EM algorithm has been suggested to compute the MLEs of the unknown parameters.

2.2 MGSN Distribution

A -variate MGSN distribution can be defined as follows. Suppose GE, are i.i.d. N random vectors and all the random variables are independently distributed. Define

| (5) |

then is said to have a -variate geometric skew-normal distribution with parameters , and , and its distribution will be denoted by MGSN. If MGSN, then the CDF and PDF of become

and

respectively. Here and denote the CDF and PDF of a -variate normal distribution, respectively, with the mean vector and dispersion matrix .

If and , we say that is a standard -variate MGSN random variable, and its distribution will be denoted by MGSN. The PDF of MGSN is symmetric and unimodal, for all values of and , whereas the PDF of MGSN may not be symmetric, and it can be unimodal or multimodal depending on parameter values. The MGF of MGSN can be obtained in explicit form. If MGSN, then the MGF of is

| (6) |

where

Further the generation of MGSN distribution is very simple. The following algorithm can be used to generate samples from a MGSN random variable.

Algorithm 1:

-

•

Step 1: Generate from a GE

-

•

Step 2: Generate N.

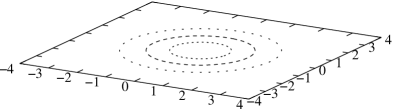

In Figure 1 we provide the joint PDF of a bivariate geometric skew normal distribution for different parameter values: (a) = 0.75, = 0, = 2, , (b) = 0.5, = 2.0, = 1, , (c) = 0.15, = 2.0, = 1.0, = 1, , (d) = 0.15, = 0.5, = -2.5, = 1.0, .

3 Properties

In this section we discuss different properties of a MGSN distribution. We use the following notations:

| (7) |

Here the vectors and are of the order each, and the matrix is of the order . Rest of the quantities are defined, so that they are compatible. The following result provides the marginals of a MGSN distribution.

We further have the following results similar to the multivariate normal distribution. The result may be used for testing simultaneously a set of linear hypothesis on the parameter vector or it may have some independent interest also; see for example Rao [12].

Theorem 1: If MGSN, then MGSN, where is a matrix of rank .

Proof: The MGF of the random vector is

where

Hence the result follows.

If MGSN, and if we denote , , then the moments and cumulants of , for , can be obtained from the MGF as follows:

| (8) |

Hence,

| (9) |

| (10) |

and

| (11) |

It is clear from (11) that the correlation between and for , not only depends on , but it also depends on and . For fixed , , if and , then 1, and if and , then -1. From (11) it also follows that if is a standard -variate MGSN random variable, i.e. for , = 0, hence = 0. Therefore, in this case although and are uncorrelated, they are not independent.

Now we would like to compute the multivariate skewness indices of the MGSN distribution. Different multivariate skewness measures have been introduced in the literature. Among them the skewness index of Mardia [10, 11] is the most popular one. To define Mardia’s multivariate skewness index let us introduce the following notations of a random vector .

where . Mardia [10] defined the multivariate skewness index as

here for denotes the -th element of the inverse of the dispersion matrix of the random vector . In case of MGSN distribution

| (12) |

It is clear from (12) that if = 1 then = 0. Also if = 0 for all , then = 0. Moreover, if for some , then the skewness index may diverge to or as . Therefore, for MGSN distribution Mardia’s multivariate skewness index varies from to .

If MGSN and if we denote the mean vector and dispersion matrix of , as and , respectively, then from (8), (9) and (10), we have the following relation:

The following result provides the canonical correlation between and . It may be mentioned that canonical correlation is very useful in multivariate data analysis. In an experimental context suppose we take two sets of variables, then the canonical correlation can be used to see what is common among these two sets of variables; see for example Rao [12].

Theorem 2: Suppose MGSN. Further and are partitioned as in (7). Then for and such that and , the maximum corr = , where is the maximum root of the -degree polynomial equation

Proof: From Theorem 1, we obtain

Therefore, using (11), it follows that the problem is to find and such that it maximizes

subject to the restrictions and . Now following the same steps as in the multivariate normal cases, Anderson [1], the result follows.

The following result provides the characteristic function of the Wishart type matrix based on MGSN random variables.

Theorem 3: Suppose are i.i.d. random variables, and MGSN. Let us consider the Wishart type matrix

If with is a matrix, then the characteristic function of , is

Proof:

Now we would like to compute . For a real symmetric matrix , there is a real matrix such that

Here, means a diagonal matrix with diagonal entries as . If we make the transformation , then using Theorem 1, MGSN. Using the definition MGSN distribution it follows that

here GE, and ’s are i.i.d. random vectors, and N. We use the following notation

Hence, , for . Therefore,

Theorem 4: If for any , GSN for a dimensional random vector , then there exists a -dimensional vector and a symmetric matrix such that MGSN. Here are functions of .

Proof: If we denote the mean vector and dispersion matrix of the random vector , as and , respectively, then we have and . Hence from (3) and (4), we have

| (13) |

Therefore, from (1), using = 1, it follows that

| (14) |

Let us define a -dimensional vector and a symmetric matrix as given below:

| (15) |

Therefore,

and (14) can be written as

Hence the result follows.

Therefore, combining Theorems 1 and 2, we have the following characterization results for a -variate MGSN distribution.

Theorem 5: If a -dimensional random vector has a mean vector and a dispersion matrix , then MGSN, here and are as defined in (15), if and only if for any , GSN, where and are as in (13).

Now we provide another characterization of the MGSN distribution.

Theorem 6: Suppose is a sequence of i.i.d. -dimensional random vectors, and GE, for . Consider a new -dimensional random vector

Then MGSN for , if and only if has a MGSN distribution.

Proof: If part. Suppose MGSN, then the MGF of for , can be written as

here .

Only if part. Suppose MGSN for some , and the MGF of is . We have the following relation:

| (16) |

From (16), we obtain

for . Therefore, MGSN.

Stochastic ordering plays a very important role in the distribution theory. It has been studied quite extensively in the statistical literature. For its importance and different applications, interested readers are referred to Shaked and Shantikumar [14]. Now we will discuss the multivariate total positivity of order two (MTP2) property, in the sense of Karlin and Rinott [8], of the joint PDF of MGSN distribution. We shall be using the following notation here. For any two real numbers and , let = min, and = max. For any vector and , let and . Let us recall the definition of MTP2 property. A function is said to have MTP2 property, in the sense of Karlin and Rinott [8], if , for all . We then have the following result for MGSN distribution.

Theorem 7: Let MGSN, and all the off-diagonal elements of are less than or equal to zero, then the PDF of has MTP2 property.

Proof: To prove that the PDF of has MTP2 property, it is enough to show that

| (17) |

for any and . If the elements of are denoted by , for , then proving (17) is equivalent to showing

For all ,

which can be easily shown by taking any ordering of . Now the result follows since .

The following two decompositions of a MGSN distribution are possible. We use the following notations. The distribution of a negative binomial random variable with parameters and , where is a non-negative integer and , will be denoted by NB. If NB, then the MGF of is

A discrete random variable is said to have a logarithmic distribution with parameter , for , if the PMF of is

and it will be denoted by LD. Now we provide two decompositions of MGSN distribution.

Decomposition 1: Suppose MGSN. Further, for any positive integer and for any , suppose

where NB and , ’s are i.i.d. N, and ’s are independently distributed, then

Proof: The MGF of can be written as

It implies that MGSN law is infinitely divisible. The following decomposition is also possible.

Decomposition 2: Suppose is a Poisson random variable with parameter , and is a sequence of i.i.d. random variables having logarithmic distribution with the following probability mass function for ;

and all the random variables are independently distributed. If MGSN, then the following decomposition is possible

| (18) |

here N for , and they are independently distributed, N, and it is independent of , and for all

Proof: First note that the probability generating function of and are as follows:

The MGF of for , such that , can be obtained as

Therefore, the MGF of the right hand side of (18) can be written as

The following results will be useful for further development. Let us consider the random vector , where and are same as defined in (5). The joint PDF of can be written as

for and for any positive integer . Therefore, the conditional probability mass function of given becomes

Therefore,

| (19) |

and

| (20) |

4 Statistical Inference

4.1 Estimation

In this section we discuss the maximum likelihood estimators (MLEs) of the unknown parameters, when . When = 1, the MLEs of and can be easily obtained as the sample mean and the sample variance covariance matrix, respectively. Suppose is a random sample of size from MGSN, then the log-likelihood function becomes

| (21) | |||||

The maximum likelihood estimators (MLEs) of the unknown parameters can be obtained by maximizing (21) with respect to the unknown parameters. It involves solving a dimensional optimization problem. Therefore, for large , it is a challenging issue.

To avoid that problem, first it is assumed that is known. For a known , we estimate the MLEs of and by using EM algorithm, say and , respectively. We maximize to compute , the MLE of . Finally we obtain the MLE of and as and , respectively. Now we will show how to compute and , for a given using EM algorithm. We treat the problem as a missing value problem, and the main idea is as follows.

It is assumed that is known. Suppose we have the complete observations of the form from . Then the log-likelihood function based on the complete observation becomes (without the additive constant)

Therefore, if we define the MLEs of and based on the complete observations as and , respectively, then for ,

| (22) |

and

| (23) | |||||

Note that is obtained by taking derivative of with respect to , and equate it to zero. Similarly, is obtained by using Lemma 3.2.2 of Anderson [1].

Now we are ready to provide the EM algorithm for a given . The EM algorithm consists of maximizing the conditional expectation of the complete log-likelihood function, based on the observed data and the current value of , say , in an iterative two-step algorithm process, see for example Dempster et al. [6]. The E-step is to compute the conditional expectation denoted by , and the M-step is maximizing , with respect to . We use the following notations:

E-Step: It consists of calculating , being the current parameter value.

M-Step: It involves maximizing with respect to , to obtain , where

Here, means the value of for which the function takes the maximum value. From (22) and (23), we obtain

and

| (24) |

We propose the following algorithm to compute the MLEs of and for a known .

Algorithm 2:

-

•

Step 1: Choose an initial guess of , say .

-

•

Step 2: Obtain

-

•

Step 3: Continue the process until convergence takes place.

Once for a given , the MLEs of and are obtained, say and , respectively, then the MLE of can be obtained by maximizing the profile log-likelihood function of , i.e. , with respect to . If it is denoted by , then the MLEs of and become and , respectively. The details will be explained in Section 5. We have used the sample mean vector and the sample variance covariance matrix as the initial guess of and , respectively, of the proposed EM algorithm for all .

4.2 Testing of Hypotheses

In this section we discuss three different testing of hypotheses problems which can be useful in practice. We propose to use the likelihood ratio test (LRT) in all the cases, and we indicate the asymptotic distribution of the LRT tests under the null hypothesis in each case. With the abuse of notations, in each case if is any unknown parameter, the MLE of under the null hypothesis will be denoted by .

Test 1:

| (25) |

The above testing problem (25) is important in practice as it tests the normality of the distribution. In this and , respectively, can be obtained as the sample mean and the sample variance covariance matrix. Since in this case is in the boundary, the standard results do not work. But using result 3 of Self and Liang [13] it follows that under the null hypothesis

Test 2:

| (26) |

The above testing problem (26) is important as it tests the symmetry of the distribution. In this case under the null hypothesis the MLEs of and can be obtained as follows. For a given , the MLE of can be obtained using the EM algorithm as before, and then the MLE of can be obtained by maximizing the profile likelihood function. In this case the ’E-step’ and ’M-Step’ can be obtained from (4.1) and (24), respectively, by replacing . Under , then

Test 3:

| (27) |

The above testing problem (27) is important as it tests the uncorrelatedness of the components. In this case the diagonal elements of the matrix will be denoted by , i.e. . Now we will mention how to compute the MLEs of the unknown parameters , and , under the null hypothesis. In this case also as before for a given , we use EM algorithm to compute the MLEs of and , and finally the MLE of can be obtained by maximizing the profile likelihood function. Now we will describe how to compute the MLEs of and , for a given , by using the EM algorithm. We use the following notation for further development. The matrix is a matrix with all the entries 0, except the -th element which is 1. Now under , the ‘E-Step’ of the EM algorithm can be written as follows:

| (28) | |||||

The ‘M-Step’ involves maximizing (28) with respect to , to obtain updated , , say , , respectively. From (28), we obtain

and

Here for a square matrix , denotes the -th diagonal element of the matrix . Under the null hypothesis

5 Simulations and Data Analysis

In this section we perform some Monte Carlo simulations to show how the proposed EM algorithm performs and we perform the analyses of two data sets analysis to show how the proposed model and the methods can be used in practice.

5.1 Simulation Results

For simulation purposes we have used the following sample size and the parameter values;

Now to show the effectiveness of the EM algorithm we have considered both the cases namely when (a) is known and (b) is unknown. We have generated samples from the above configuration and computed the MLEs of and using EM algorithm. In all the cases we have used the sample mean and the sample variance covariance matrix as the initial guesses of the EM algorithm. We replicate the process 1000 times and report the average estimates and the associated mean squared errors (MSEs). For known , the results are reported in Tables 1 and 3 and for unknown , the results are reported in Tables 2 and 4. In each box of a table, the first figure, second figure and the third figure represent the true value, the average estimate and the corresponding MSE, respectively.

It is clear that the performances of the proposed EM algorithm are quite satisfactory. It is observed that the sample mean and the sample variance covariance matrix can be used as good initial guesses of the EM algorithm. In all the cases considered it is observed that the EM algorithm converges within 30 iterations, hence it can be used in practice quite conveniently. Further, it is observed that the profile likelihood method is also quite effective in estimating , when it is unknown.

| 0.0000 | 0.0000 | 1.0000 | 1.0000 | |

|---|---|---|---|---|

| 0.0053 | 0.0047 | 1.0097 | 1.0055 | |

| (0.0984) | (0.1213) | (0.1430) | (0.1237) | |

| 2.0000 | 2.0000 | 1.0000 | 0.0000 | |

| 2.0024 | 1.9984 | 0.9942 | -0.0060 | |

| (0.3299) | (0.3602) | (0.2879) | (0.2262) | |

| 2.0000 | 3.0000 | 2.0000 | 1.0000 | |

| 1.9984 | 2.9922 | 1.9907 | 0.9907 | |

| (0.3602) | (0.4932) | (0.4130) | (0.3092) | |

| 1.0000 | 2.0000 | 3.0000 | 2.0000 | |

| 0.9942 | 1.9907 | 2.9757 | 1.9823 | |

| (0.2879) | (0.4130) | (0.5350) | (0.4054) | |

| 0.0000 | 1.0000 | 2.0000 | 2.0000 | |

| -0.0060 | 0.9907 | 1.9823 | 1.9859 | |

| (0.2262) | (0.3092) | (0.4054) | (0.3675) |

| 0.0000 | 0.0000 | 1.0000 | 1.0000 | |

| -0.0067 | -0.0079 | 1.0094 | 1.0122 | |

| (0.1029) | (0.1255) | (0.1553) | (0.1390) | |

| 2.0000 | 2.0000 | 1.0000 | 0.0000 | |

| 2.0105 | 2.0103 | 1.0055 | 0.0011 | |

| (0.3579) | (0.3964) | (0.3165) | (0.2377) | |

| 2.0000 | 3.0000 | 2.0000 | 1.0000 | |

| 2.0103 | 3.0194 | 2.0095 | 1.0091 | |

| (0.3964) | (0.5420) | (0.4443) | (0.3233) | |

| 1.0000 | 2.0000 | 3.0000 | 2.0000 | |

| 1.0055 | 2.0095 | 2.9987 | 2.0006 | |

| (0.3165) | (0.4443) | (0.5577) | (0.4161) | |

| 0.0000 | 1.0000 | 2.0000 | 2.0000 | |

| 0.0011 | 1.0091 | 2.0006 | 2.0058 | |

| (0.2377) | (0.3233) | (0.4161) | (0.3827) | |

| 0.5000 | ||||

| 0.5068 | ||||

| (0.0433) | ||||

| 0.0000 | 0.0000 | 1.0000 | 1.0000 | |

|---|---|---|---|---|

| 0.0057 | 0.0046 | 1.0118 | 1.0068 | |

| (0.1205) | (0.1481) | (0.1605) | (0.1350) | |

| 2.0000 | 2.0000 | 1.0000 | 0.0000 | |

| 2.0015 | 1.9969 | 0.9923 | -0.0065 | |

| (0.3126) | (0.3416) | (0.2720) | (0.2099) | |

| 2.0000 | 3.0000 | 2.0000 | 1.0000 | |

| 1.9969 | 2.9906 | 1.9887 | 0.9898 | |

| (0.3416) | (0.4645) | (0.3875) | (0.2907) | |

| 1.0000 | 2.0000 | 3.0000 | 2.0000 | |

| 0.9923 | 1.9897 | 2.9778 | 1.9864 | |

| (0.2720) | (0.3875) | (0.4848) | (0.3864) | |

| 0.0000 | 1.0000 | 2.0000 | 2.0000 | |

| -0.0065 | 0.9898 | 1.9864 | 1.9903 | |

| (0.2099) | (0.2907) | (0.3684) | (0.3320) |

| 0.0000 | 0.0000 | 1.0000 | 1.0000 | |

| 0.0047 | 0.0035 | 1.0141 | 1.0093 | |

| (0.1392) | (0.1704) | (0.1938) | (0.1615) | |

| 2.0000 | 2.0000 | 1.0000 | 0.0000 | |

| 2.0183 | 2.0258 | 1.0263 | 0.0121 | |

| (0.3793) | (0.4260) | (0.3453) | (0.2620) | |

| 2.0000 | 3.0000 | 2.0000 | 1.0000 | |

| 2.0258 | 3.0351 | 2.0272 | 1.0088 | |

| (0.4260) | (0.5807) | (0.4842) | (0.3448) | |

| 1.0000 | 2.0000 | 3.0000 | 2.0000 | |

| 1.0263 | 2.0272 | 3.0120 | 1.9961 | |

| (0.3453) | (0.4842) | (0.5897) | (0.4256) | |

| 0.0000 | 1.0000 | 2.0000 | 2.0000 | |

| 0.0121 | 1.0088 | 1.9961 | 1.9892 | |

| (0.2620) | (0.3448) | (0.4256) | (0.3726) | |

| 0.7500 | ||||

| 0.7575 | ||||

| (0.0446) | ||||

In this section we present the analysis of two data sets namely (i) one simulated data set and (ii) one real data set mainly to illustrate how the proposed EM algorithm and the other testing procedures can be used in practice.

5.2 Simulated Data Set

We have generated a data set using the Algorithm 1 as suggested in Section 2, with the following specification:

It is available in http://home.iitk.ac.in/kundu/fort.76. We present some basic statistics of the data set. The sample mean vector, and the sample variance covariance matrix are as follows:

| (29) |

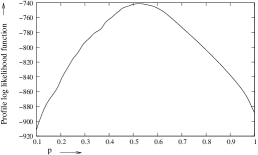

We start the EM algorithm for each with the above initial guesses. The profile log-likelihood function is plotted in Figure 2.

Finally, the MLEs of the unknown parameters are obtained as follows:

and the associated log-likelihood value is -741.347. It may be mentioned for each , the EM algorithm is continued for 20 iterations, and the log-likelihood value (21) is calculated based on the first 50 terms of the infinite series. The program is written in FORTRAN-77, and it is available in http://home.iitk.ac.in/kundu/mv-geo-sn-em-punknown-data.for.

For illustrative purposes, we would like to perform the test:

Under , the MLEs of and become and , respectively, as given in (29), and the associated log-likelihood value is -887.852. Therefore, the value of the test statistic = 293.01, and the associated value is less than 0.00001. Hence, we reject . Next we consider the following testing problem

In this case under , the MLEs of and are as follows

and the associated log-likelihood value is -917.674. In this case the value of the test statistics = 352.654. Since the associated value is less than 0.00001, we reject the null hypothesis. Finally we consider the testing problem:

In this case under , the MLEs of the unknown parameters are as follows:

and

The associated log-likelihood value is -1036.80. The value of = 590.91. In this case also we reject , as the associated values is less than 0.00001.

5.3 Stiffness Data Set

In this section we present the analysis of a real data set to show how the proposed model and the methodologies work in practice. The data set represents the four different measurements of stiffness, of ‘Shock’ and ‘Vibration’ of each of 30 boards. The first measurement (Shock) involves sending a shock wave down the board and the second measurement (Vibration) is determined while vibrating the board. The last two measurements are obtained from static tests. The data set is available in Johnson and Wichern [7]. For easy reference it is presented in Table 5. Since all the entries of the data set are non-negative, if we want to the fit the multivariate skew normal distribution to this data set, the MLEs of the unknown parameters may not exist. In fact we have tried to fit univariate skew-normal distribution to and it is observed that the likelihood function is an increasing function of the ‘tilt’ parameter for fixed location and scale parameters. Therefore, the MLEs do not exist in this case. It is expected the same phenomenon even for skew- distribution for large values of the degrees of freedom.

| No. | No. | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1 | 1889 | 1651 | 1561 | 1778 | 2 | 2403 | 2048 | 2087 | 2197 |

| 3 | 2119 | 1700 | 1815 | 2222 | 4 | 1645 | 1627 | 1110 | 1533 |

| 5 | 1976 | 1916 | 1614 | 1883 | 6 | 1712 | 1712 | 1439 | 1546 |

| 7 | 1943 | 1685 | 1271 | 1671 | 8 | 2104 | 1820 | 1717 | 1874 |

| 9 | 2983 | 2794 | 2412 | 2581 | 10 | 1745 | 1600 | 1348 | 1508 |

| 11 | 1710 | 1591 | 1518 | 1667 | 12 | 2046 | 1907 | 1627 | 1898 |

| 13 | 1840 | 1841 | 1595 | 1741 | 14 | 1867 | 1685 | 1493 | 1678 |

| 15 | 1859 | 1649 | 1389 | 1714 | 16 | 1954 | 2149 | 1180 | 1281 |

| 17 | 1325 | 1170 | 1002 | 1176 | 18 | 1419 | 1371 | 1251 | 1308 |

| 19 | 1828 | 1634 | 1602 | 1755 | 20 | 1725 | 1594 | 1313 | 1646 |

| 21 | 2276 | 2189 | 1547 | 2111 | 22 | 1899 | 1614 | 1422 | 1477 |

| 23 | 1633 | 1513 | 1290 | 1516 | 24 | 2061 | 1867 | 1646 | 2037 |

| 25 | 1856 | 1493 | 1356 | 1533 | 26 | 1727 | 1412 | 1238 | 1469 |

| 27 | 2168 | 1896 | 1701 | 1834 | 28 | 1655 | 1675 | 1414 | 1597 |

| 29 | 2326 | 2301 | 2065 | 2234 | 30 | 1490 | 1382 | 1214 | 1284 |

Before progressing further we have divided all the measurements by 100, and it is not going to make any difference in the inferential procedure. The sample mean vector and the sample variance covariance matrix of the transformed data are

| (30) |

Based on the EM algorithm and using the profile likelihood method, we obtain the MLEs of the unknown parameters as follows:

and the associated log-likelihood value is -271.969. Now to check whether the proposed MGSN distribution provides a better fit than the multivariate normal distribution or not, we perform the following test:

Under , the MLEs of and are provided in (30), and the associated log-likelihood value is -277.761. Therefore, the value of the test statistic = 11.584, and the associated value is 0.0000025. Hence, we reject the null hypothesis, and it indicates that the proposed MGSN distribution provides a better fit than the multivariate normal distribution to the given stiffness data set. AIC also prefers MGSN distribution than the multivariate normal distribution for this data set.

6 Conclusion

In this paper we have discusses different properties of the MGSN distribution in details. Different characterization results and dependence properties have been established. The -dimensional MGSN distribution has unknown parameters. We have proposed to use EM algorithm and the profile likelihood method to compute the MLEs of the unknown parameters, and it is observed that the proposed algorithm can be implemented very easily. We have discussed some testing of hypothesis problems also. Two data sets have been analyzed to show the effectiveness of the proposed methods, and it is observed that for the real ’stiffness’ data set MGSN provides a better fit than the multivariate normal distribution. Hence, this model can be used as an alternative to Azzalini’s multivariate skew normal distribution.

Acknowledgements

The author would like to thank Prof. Dimitris Karlis from the Athens University of Economics and Business, Greece, for his helpful comments. The author is really thankful to two reviewers and the associate editor for their careful reading and providing constructive comments.

References

- [1] Anderson, T.W. (1984), An introduction to multivariate statistical analysis, 2nd-edition, John-Wiley & Sons, New York.

- [2] Arnold, B.C. and Beaver, R.J. (2000), “Hidden truncation models”, Sankhya, Ser. A, vol. 62, 23 - 35.

- [3] Azzalini, A.A. (1985), “A class of distributions which include the normal”, Scandinavian Journal of Statistics, vol. 12, 171 - 178.

- [4] Azzalini, A.A. and Capitanio, A. (2014), The skew-normal and related families, Cambridge University Press, Cambridge, United Kingdom.

- [5] Azzalini, A.A. and Dalla Valle, A. (1996), “The multivariate skew normal distribution”, Biometrika, vol. 83, 715 - 726.

- [6] Dempster, A.P., Laird, N.M. and Rubin, D.B. (1977), “Maximum likelihood from incomplete data via EM algorithm”, Journal of the Royal Statistical Society, Ser. B., vol. 39, 1 - 38.

- [7] Johnson, R. A. and Wichern, D.W. (2013), Applied multivariate Statistical Analysis, 6-th edition, Pearson New International Edition, New York, USA.

- [8] Karlin, S. and Rinott, Y. (1980), “Classes of orderings of measures and related correlation inequalities, I, Multivariate totally positive distributions”, Journal of Multivariate Analysis, vol. 10, 467 - 498.

- [9] Kundu, D. (2014), “Geometric skew normal distribution”, Sankhya, Ser. B, vol. 76, 167 - 189.

- [10] Mardia, K.V. (1970), “Measures of multivariate skewness and kurtosis with applications”, Biometrika, vol. 57, 519–530.

- [11] Mardia, K. V. (1974), “Applications of some measures of multivariate skewness and kurtosis in testing normality and robustness studies”, Sankhya, Ser. B, vol. 36, 115 – 128.

- [12] Rao, C.R. (1973), Linear Statistical Inference and its Applications, 2nd. edition, Wiley and Sons, New York.

- [13] Self, S.G. and Liang, K-L. (1987), “Asymptotic properties of the maximum likelihood estimators and likelihood ratio test under non-standard conditions”, Journal of the American Statistical Association, vol. 82, 605 - 610.

- [14] Shaked, M. and Shantikumar, J.G. (1994), Stochastic Orders and their Applications, Acadmic Press, London, UK.