An Explicit Default Contagion Model and Its Application to Credit Derivatives Pricing 111We would like to thank Tahir Choulli, Liuren Wu, Zhengyu Cui, Ping Li, Shiqi Song, Xianhua Peng, Chao Shi for their insightful comments. The research of Jun Deng is supported by the National Natural Science Foundation of China (11501105) and UIBE Excellent Young Research Funding (302/871703). The research of Bin Zou is supported by a start-up grant from the University of Connecticut. Declarations of interest: none

Abstract

We propose a novel credit default model that takes into account the impact of macroeconomic information and contagion effect on the defaults of obligors. We use a set-valued Markov chain to model the default process, which is the set of all defaulted obligors in the group. We obtain analytic characterizations for the default process, and use them to derive pricing formulas in explicit forms for synthetic collateralized debt obligations (CDOs). Furthermore, we use market data to calibrate the model and conduct numerical studies on the tranche spreads of CDOs. We find evidence to support that systematic default risk coupled with default contagion could have the leading component of the total default risk.

Key words: credit risk; collateral default obligation (CDO); Markov chain; jump diffusion; tranche spread

1 Introduction

In the aftermath of the financial crisis of 2007-2009, there have been burgeoning interests in studying the causes and remedies of this crisis from academic scholars, practitioners, and regulators around the world. Financial-Crisis-Inquiry-Commission-Report, (2011) concludes that this financial crisis is avoidable and mainly caused by the failure of financial regulations and supervisions, especially on structured finance products. The collapsing mortgage-lending standards and mortgage related financial products, such as mortgage-backed securities (MBS) and collateralized debt obligations (CDOs), lit and spread the flame of contagion and crisis. In Basel Accords II, the calibration of default risk neglects the significant impact of default contagion among different obligors. After the financial crisis, Basel Accords III is proposed, and one of its key principles is to emphasize the modeling of default contagion, which contributes significantly to the collapse of financial systems during the crisis.

In the literature, there are three main strands on the modeling of default risk. We review them briefly in what follows, but are by no means exhaustive here. The first line includes the structure models, pioneered by Merton, (1974), which follows from the option pricing theory of Black and Scholes, (1973). A default event occurs if the company’s asset value is below its debt at the time maturity. Black and Cox, (1976) extends Merton’s structure model by postulating that a default occurs at the first passage time when the firm’s asset value drops below a certain time-dependent barrier. However, structure models lack accuracy in explaining the cross-section of credit spreads, measured by the yield difference between risky corporate bonds and riskless bonds, and underpredict short-term default probabilities, see, e.g., Eom et al., (2004). We refer to Sundaresan, (2013) for an excellent review on structure models. The second strand is the Copula models, first proposed by Li, (2000). In the seminal work of Li, (2000), the author uses Gaussian Copula to model the default correlations and joint distribution, and applies the results to credit derivative pricing and hedging. However, Copula models do not fit well with the market data and have difficulty in explaining model parameters. Representative works using copula for credit modeling include, but certainly are not limited to, Frey et al., (2001), Schönbucher and Schubert, (2001), Laurent and Gregory, (2005), and Hull and White, (2006).

Our paper falls into the third strand, which includes the intensity based models. In the intensity based credit modeling literature, two well-established modeling approaches are the top-down approach and the bottom-up approach, both of them are capable of fitting the market data.222More mathematical details about these two methods are presented in Section 2. In the top-down approach, models are built for the cumulative default intensity of the whole portfolio, without specifying the underlying single obligor. While in comparison, under the bottom-up approach, models are constructed with specified individual default intensity. The default time, either for the whole portfolio or individual obligor, is usually modeled as the first jump time of a process, such as Cox process or doubly-stochastic Poisson process. Top-down models are introduced and investigated in Errais et al., (2007), Errais et al., (2010), Giesecke et al., (2011), and Cont and Minca, (2013), among others. Under the framework of bottom-up approach, single name default intensity based models are introduced in Jarrow and Turnbull, (1995), Lando, (1998), and Duffie and Singleton, (1999). Mortensen, (2006) postulates that the default risk of obligor is given in the form of , where captures the systematic default risk component and captures the idiosyncratic default risk component which is assumed to be independent of and , for all obligors . The default propagation and correlations are channeled by the common systematic component . However, both approaches can not account for the contagion effect on idiosyncratic default risk induced by systematic default risk . Das et al., (2007) and Duffie et al., (2009) demonstrate the presence of frailty correlated default and the incapability of doubly stochastic assumption to capture default contagion or frailty (unobservable explanatory variables that are correlated across firms).

In this paper, we consider a group of defaultable obligors (or names), labeled by , where the default of one obligor might impact the remaining obligors in the group. The default contagion arises from two components: defaulted obligors and macroeconomic factor. Specifically, we denote by (a nonnegative random variable) the occurrence time of the default event, and the default process, where is the set of all the obligors that have defaulted by time . The dynamics of the macroeconomic factor are described by an exogenous process that might affect the occurrence of default events in the group, precisely through and .

Our new default framework, taking default dependence and contagion into account, gives explicitly the dynamics of the default process and can be tailored to price CDOs, CDX, iTraxx, et cetera. Before diving into technical details, we explain the leitmotif behind our treatment. A synthetic CDO is a portfolio consisting of single-name CDS’s on obligors with individual default times and recovery rates . It is standard to assume that all obligors have the same nominal values, denoted by . The accumulated loss is then given by

| (1.1) |

Instead of modeling default obligors individually as in the bottom-up approach, we use a set-valued process (default process) to characterize the evolution of default events in the group. Hence, the loss process is fully characterized by the set-valued process . The interaction between the macroeconomic factor and the default process is channeled through a conditional Markov process with default intensity , which will be specified later (see Assumption 3.2). The process has the same flavor of intensity based approach as in Jarrow and Turnbull, (1995), Lando, (1998), and Collin-Dufresne et al., (2004), to name a few.

This paper has several contributions to the intensity based credit risk modeling literature. First, we explicitly construct the set-valued default process through its intensity family . As a result, our model integrates macroeconomic impact and intergroup default contagion effect dynamically, which both top-down and bottom-up models can not capture. Markov (set-valued and real-valued) default models have been studied both theoretically and empirically by Jarrow et al., (1997) and Bielelcki et al., (2011); however our model leads to a more tractable formulation in pricing and hedging credit derivatives. Second, we provide a closed-form pricing formula for CDOs without using matrix exponential as in Bielelcki et al., (2011). This gives significant computational advantages beyond its tractability, especially when the obligors is large. We illustrate this in a particular homogeneous contagion model where could be as large as 125. Finally, our set-valued Markov model can be easily extended and applied to study other credit derivatives such as first-to-default, -th default, et cetera. We will leave the investigation of those derivatives in future research.

The paper is organized as follows. In Section 2, we introduce the default contagion model. In Section 3, we provide analytic characterizations for the default process. In Section 4, we derive the pricing formulas of credit derivatives. In Section 5, we conduct a sensitivity analysis on tranche spreads and use market data to calibrate the model. We conclude in Section 6. In Appendixes A and B, we present technical proofs.

2 The Setup

In this paper, we model the macroeconomic information (or factors) by an exogenous process , which is defined on a stochastic basis . Here the filtration is taken to be the augmented filtration generated by the process , satisfying the usual hypotheses of right continuity and completeness, and . The measure is the risk neutral probability measure associated with a constant risk-free rate . In the economy, we consider defaultable obligors, labeled as , where . For each obligor , denote by its individual default time, where . If obligor defaults, we assume there is a proportional nominal loss of . As a standard market practice, is often set to be 40% for all , see ISDA standard CDS converter specification.333http://www.cdsmodel.com/cdsmodel/assets/cds-model/docs

In our studies, a credit derivative is a contingent claim with payoff depending on the loss process , which is defined by

| (2.1) |

where is an indicator function. Without loss of generality, we have assumed a unitary face value for all obligors in the above definition of . In the literature, there are two standard approaches (models) for the pricing and hedging problems of credit derivatives: the bottom-up and top-down approaches. The bottom-up approach specifies the intensity process 444Throughout this paper, for a stochastic process, if the subscript is reserved for special meaning, then we write time variable in parenthesis, see, e.g., ; otherwise, we may write time variable in subscript or parenthesis exchangeably (e.g., as or ). of each obligor such that, for all

| (2.2) |

see, e.g., Duffie et al., (2000) and Collin-Dufresne et al., (2004). On the other hand, the top-down approach specifies the constituent intensity process of the loss process such that

| (2.3) |

see, e.g., Errais et al., (2007) and Giesecke et al., (2011). In the top-down approach, the constituent intensity can be recovered by random thinning to decompose the aggregate portfolio intensity into a sum of constituent intensities, see Giesecke et al., (2011).

Unlike in the bottom-up approach, we do not model the individual default time for each obligor , but instead consider the ordered default times of all obligors. Namely, is the occurrence time of the -th default among all obligors. Hence, we have

| (2.4) |

Denote by the default process, and define as the set of obligors that have defaulted by time . is then a set-valued process taking values in the subsets of . For instance, if , then obligors , , and have defaulted by time . With the usual conventions, we set and . The following assumptions on the defaults modeling will be imposed throughout the paper.

Assumption 2.1.

We assume that (i) no more than one default occurs at the same time; and (ii) obligors will not recover after the default.

Remark 2.2.

Under Assumption 2.1, we have the following results.

-

(i)

(no default at time ) = 1 - (one default at time ) and .

-

(ii)

is a non-decreasing process, i.e., 555In this paper, the notation “” may contain equality, i.e., it is possible that and hold at the same time. If is a true subset of , we denote by . for all .

-

(iii)

The cardinality of the default process, denoted by at time , jumps up by size 1 at default time . Hence, , where and . Here, denotes the set difference of two sets and , i.e., the set of all elements that belong to but not .

In our setup, the defaults of all obligors are fully characterized by the pair . By using them, we rewrite the default process and the loss process by

| (2.5) |

In the above expression, we take . Since records the last default among all obligors, it is clear that for all .

One of the novelties of our framework is to characterize defaults directly through the dynamics of the default process , which is modeled by an -conditional Markov chain with intensity family , where . Here, denotes the sigma-algebra consisting of all the subsets of . To account for the dependence among defaults in the group, the intensity family may depend on the macroeconomic factor and/or intergroup contagion. Introduce notations as the augmented filtration generated by the process . We present two important definitions below.

Definition 2.3.

A continuous time -valued stochastic process is called an -conditional Markov chain if, for all and , the following condition holds:

| (2.6) |

Here, the operator stands for the sigma-algebra generated by two sigma-fields and .

Definition 2.4.

A family of -adapted processes or is called the default intensity family of an -valued process , if for any , the process is an -martingale, where

| (2.7) |

and .

Similar to the bottom-up and top-down approaches, the intensity family ir in our framework plays an important role in the compensator of the default process , with representing the conditional default rate at time when obligors in set have already defaulted. Notice that the condition (i) in Assumption 2.1 is equivalent to

| (2.8) |

To make our framework more applicable in empirical studies, we assume the existence of the intensity family (or ) and the macroeconomic factor process first, not the default process directly. The motivation follows from the fact that one could apply the market credit derivative prices or spreads to recover the default intensity or contagion rate. We refer interested readers to Cont et al., (2010), Cont and Minca, (2013), Nickerson and Griffin, (2017), and the references therein, for related studies. However, it is rather difficult and technical to show the existence of an -conditional Markov chain for a given intensity family , which is a main subject of the next section.

3 Characterizations of the Default Process

In this section, we provide characterizations for the default process , introduced in the previous section, in three steps. First, we formulate the conditions that guarantee the existence of an -conditional Markov chain , which is used to model the default process in our framework, see Assumptions 3.1 and 3.2 and Theorem 3.4 in Section 3.1. Second, we derive the dynamics of through computing its conditional probabilities and expectations. The key results under the general default intensity family are obtained in Theorem 3.5, which is essential in pricing and hedging problems of credit derivatives. Third, we specify a class of processes for the intensity family in Assumption 3.7 and simplify the results of Theorem 3.5 to more tractable forms in Corollaries 3.9 and 3.11.

3.1 The Existence of the Default Process

In this subsection, we characterize the existence of an -conditional Markov chain under Assumptions 3.1 and 3.2, and present results in Theorem 3.4. As mentioned in the introduction, such a Markov chain will be used to model the default process in our framework.

To construct an -conditional Markov chain , we begin with a given exogenous -valued stochastic process , which captures the macroeconomic information (or factors). In this section, to obtain generality, we do not specify the dynamics of . We consider the pricing problems in the next section when is modeled by an affine jump-diffusion process. In addition, we are given a family of stochastic processes which are described below.

Assumption 3.1.

is a family of Poisson processes with intensity equal to one, where and . Furthermore, the Poisson family and the macroeconomy process are mutually independent.

Next, we summarize the conditions that the intensity family (or ) should satisfy, and assume those conditions hold in the rest of the paper.

Assumption 3.2.

The intensity family , where , is a family of -adapted processes, which satisfy the following conditions for all :

-

(A1)

(or ), if or , where .

-

(A2)

. For notation simplicity, let and .

-

(A3)

is an increasing function of , with .

-

(A4)

for all and

Remark 3.3.

The essential part of Assumption 3.2 is (A1), and it is equivalent to condition (i) in Assumption 2.1. (A2) is the Markov transition density requirement. (A3) and (A4) are essential to impose positivity assumption on the family . We do not make any further assumptions on the structure of the intensity family or , which shall give our framework more flexibility and versatility to capture default contagion.

We end this subsection by the following crucial theorem which addresses the existence question of the default process when the exogenous process and the intensity family are given.

Theorem 3.4.

Proof.

The construction of such an -conditional Markov chain is achieved by carefully counting the jump times of a family of non-homogenous Poisson processes and by verifying the conditions in Definitions 2.3 and 2.4. The existence of is obtained under very general assumptions, and our framework embraces a broad class of credit risk models. The detailed proof is separated into three parts, which are delayed to Appendix A. ∎

3.2 The Dynamics of the Default Process

In this subsection, using the results from Theorem 3.4, we obtain the dynamics of the default process through deriving its conditional probabilities and expectations, see Theorem 3.5.

To proceed, we introduce some notations to facilitate the presentation of key results below. For any satisfying and , denote by the set of all the permutations of . Here, is set “minus” set , namely, . For any , define the sequence of sets by

| (3.1) |

The theorem below contains the key results regarding the dynamics of the default process .

Theorem 3.5.

Theorem 3.5 explicitly describes the conditional dynamics of under once the default intensity is known. Given the dynamics of in Theorem 3.5, the loss process in (2.5) is completely characterized and employed to price credit derivatives in the next section. One interesting and important feature of Theorem 3.5 is that the functional (serves as the transition kernel from set to set ) only involves the default intensity . Notice that when the intensity family is completely arbitrary, the calculation complexity of the conditional probabilities in (3.2) is tremendous, since permutations of are involved. However, if we assign a more tractable structure to , the computation of (3.2) will be simplified dramatically. This gives us computational advantage when pricing and hedging credit derivatives, see examples in the next section.

In our modeling, there are obligors, where is a positive integer. When or 2, the results in Theorem 3.5 can be to much simpler forms, as in the corollary below.

Corollary 3.6.

When (the case of two obligors), we observe that, starting from , the probability that hits state or achieves its maximum when . Furthermore, both probabilities are increasing when and decreasing when .

3.3 The Modeling of the Intensity Family

In the previous subsection, we have obtained the dynamics of the default process in Theorem 3.5, which is fully determined by the default intensity family . When the number of obligors in the economy is small (), we have simplified the results of Theorem 3.5 to more tractable forms in Corollary 3.6. However, is usually large in many financial products, such as iTraxx and CDX, and that makes the computation of conditional probabilities in (3.2) time consuming and inefficient. One remedy is to model the intensity family of the default process in specific forms, then develop a more applicable version of Theorem 3.5. The rest of this subsection is then devoted to the modeling of the intensity family , taking the dependence of the macroeconomic factor and intergroup contagion into account. We consider the following model for the intensity family , which satisfies all the conditions imposed in Assumption 3.2.

Assumption 3.7.

Let and be nonnegative constants, and be a positive real-valued function with . We define, for all , that

| (3.12) | ||||

| (3.13) |

Remark 3.8.

In Assumption 3.7, the function describes the default rate inherited from the macroeconomic factors, such as economic downturn, business cycles and financial crises. The function describes the intergroup default contagion rate induced by the defaulted obligors in on the survivor , and is the aggregate impact of defaulted obligors in on all survivors in ; while is the individual contagion rate from to . The function measures the magnitude of intergroup contagion. Hence, the model of , given by (3.14), is able to capture the impact of macroeconomic factors and intergroup contagion on the default intensity. We end this remark by noting that the model (3.14) embraces a broad class of default contagion models, such as the homogeneous contagion model and the near neighbor contagion model, see Herbertsson, (2008).

The intergroup contagion magnitude function and the contagion rate matrix , in the definition of , may have opposite effects on the severity of the total default risk. For instance, Jorion and Zhang, (2007) find that, in the CDS market, credit events could have contagion and competition effects, i.e., there are good and bad credit contagions. By adopting their findings, the function may have positive () or negative () effect on credit spreads. In the numerical studies of Section 5, we take , where is calibrated from the CDO tranche quotes. Our findings show that is positive for both 5Y and 7Y CDX.NA.HY, which imply the credit events in CDX.NA.HY group have a overall competition (negative) effect.

Recall that contains all the permutations of . Take with , where is a positive integer no greater than , and select any , define

| (3.15) |

Let be different real numbers, where is a positive integer. For all and , we define

| (3.16) |

with .

When the intensity family is given by (3.14), we simplify the results of Theorem 3.5 in the corollary below, which is the key result of this subsection.

Corollary 3.9.

Suppose the macroeconomy process is given, and Assumptions 3.1 and 3.7 hold. Choose any with and . If whenever and , then given , we have for all that

| (3.17) |

and further, for any nonnegative (or bounded) -measurable random variable ,

| (3.18) |

where and are defined by (3.13) and (3.15), and , with given by (3.16).

Remark 3.10.

Similar to Corollary 3.6, when there is only one obligor, we can further reduce the results in Corollary 3.9 to much simpler forms, which are summarized in the corollary below. The results obtained in Corollary 3.11 coincide with those in the classical intensity model, see, e.g. Duffie et al., (2000) and Collin-Dufresne et al., (2004).

Corollary 3.11.

Proof.

The results follow immediately by calculating that , , , , , and . ∎

Remark 3.12.

From assertion in Corollary 3.11, we obtain

Hence, we could interpret as the instantaneous default risk premium at time , and price a defaultable bond with maturity as a risk-free bond under a risk-adjusted discount rate .

4 Credit Derivatives Pricing under Affine Jump Diffusion Intensity

In this section, we apply the results in Corollary 3.9 to price synthetic CDOs and CDX indexes under our default contagion model. The intensity family is given by (3.14) under an affine jump diffusion model, as specified in Assumption 4.1. The general results are obtained in Proposition 4.4, and those under two special models in Propositions 4.6 and 4.8.

4.1 Affine Jump Diffusion Intensity

In Section 3.3, we specify the structure of the intensity family in Assumption 3.7, in which the function and the macroeconomy process are in general forms. To obtain explicit pricing formulas of credit derivatives, we further make the following assumptions for and .

Assumption 4.1.

Let Assumption 3.7 hold and the intensity process be given by (3.14). Take for all and suppose the dynamics of are governed by the following one-dimensional affine jump diffusion process:

| (4.1) |

where , and are (positive) constants, is a standard Brownian motion, is a compound Poisson process with jump times from a Poisson distribution with intensity and jump sizes exponentially distributed with mean . The processes and are mutually independent.

Remark 4.2.

In the above model (4.1), the parameter is the mean-reversion rate of to the long-term level . The jumps of the compound Poisson process capture the sudden credit deterioration events, which may lead to defaults of the obligors in the economy. Such an affine jump diffusion model is considered in Duffie et al., (2000) and Ding et al., (2009). A special case is the no-jump () model of Feller, (1951), which is used by Cox et al., (1985) to model stochastic interest rates.

The following lemma is needed when deriving the pricing formula of credit derivatives in the sequel, see, e.g., Appendix of Duffie and Garleanu, (2001) and Mortensen, (2006).

Lemma 4.3.

Let Assumption 4.1 hold. For any and , we have

| (4.2) |

where and are given by

| (4.3) | ||||

| (4.4) |

with , , , , , and .

4.2 Index and Tranche Spreads

A synthetic collateralized debt obligation (CDO) is a portfolio consisting of single-name credit default swaps (CDS) on obligors, with default times and recovery rates . It is standard to assume that all obligors have the same nominal values, as in the cases of iTraxx and CDX. Without loss of generality, the nominal value is set to one. Then the accumulated loss is given by (2.5). Usually, is represented as a percentage of the total nominal value at time 0 (which is equal to ). In the following, with slight abuse of notations, we set

| (4.5) |

where . Notice that, with the notation of , the numerator in (4.5) is the loss in (2.5).

A CDO is specified by the attachment points and the corresponding trances , where . An agreement on tranche is a bilateral contract, in which the protection seller agrees to pay the protection buyer all credit losses occurred in the interval . The payments from the seller are then made at the corresponding default times before or at . In exchange for protection, the buyer pays a periodic premium fee proportional to the current outstanding value on tranche up to , probably reduced by the occurred default losses. The accumulated loss of tranche is defined by

| (4.6) |

Suppose the premium fees from the buyer are paid at discrete times , with time increment for , and the risk-free interest rate is constant . It is often assumed in practice that premiums are paid quarterly, i.e., , which is exactly the parameter we choose in the numerical studies. At the inception of an agreement, depending on different product structures, such as CDX and iTraxx to name a few, the buyer is usually required to pay an upfront fee. In a typical CDO tranche with upfront rate and swap spread , the cash flows are as follows:

-

•

(Default Leg) The protection seller covers tranche losses , given by (4.6).

-

•

(Premium Leg) The protection buyer pays at inception and at each payment time , where .

Therefore, the value of the default leg must agree with that of the premium leg, which gives the spread of tranche by

| (4.7) |

where denotes the expectation taken under the risk neutral probability measure . Note that in (4.7) we have assumed that defaults only occur at the start point of each time interval . In the literature, the end point and the middle point of each time interval are both used as well, see, e.g. Mortensen, (2006), Errais et al., (2010) and Cont and Minca, (2013). However, these different assumptions will only slightly affect our calibration results, but will not lead to different conclusions. As a direct consequence of Corollary 3.9 and formulas (4.2) and (4.6), the tranche spread is further computed in the proposition below.

Proposition 4.4.

Suppose the macroeconomy process is given, and Assumptions 3.1 and 4.1 hold. For the above specified CDO, we have the following results.

- (i)

-

(ii)

If all the obligors have the same recovery rate , the accumulated loss and its expected value are respectively given by

(4.9) (4.10) where

(4.11) and is the integer part of .

Proof.

It follows immediately from Corollary 3.9. The computations are omitted here. ∎

4.3 Pricing Examples

In this subsection, we simplify the results of Proposition 4.4 under two specific contagion models: (1) homogeneous contagion model (HCM) in Proposition 4.6 and (2) near neighbor contagion model (NCM) in Proposition 4.8. Both models are special cases of the intensity model in Assumption 3.7.

Assumption 4.5 (Homogeneous Contagion Model).

Let the intensity family be given by Assumption 3.7. We further assume that the default contagion is homogeneous among obligors. To be specific, we assume for all , and , where is a constant and can be interpreted as the contagion recovery rate.

The homogeneous contagion model (HCM) introduced in Assumption 4.5 is different from that in Frey and Backhaus, (2010) and Laurent et al., (2011), where the authors specify their default intensity only through a homogeneous Poisson process, while our family of default intensities consists of two components: one from macroeconomic factor and the other from intergroup contagion matrix . Modeling all heterogeneous intergroup contagion leads to a large scale of parameters and numerical issues, such as computational inefficiency and loss of robustness in model parameters calibration. As a result, we will mainly restrict to HCM in our numerical studies. We remark that HCM is a reasonable assumption for CDO tranches on large indexes such as iTraxx and CDX, although this may be an issue with equity tranches for which idiosyncratic risk is playing an important role. Under the above HCM, we obtain the following results.

Proposition 4.6.

Proof.

Please refer to Appendix B.3 for the proof. ∎

Next, we consider the near neighbor contagion model (NCM), where each obligor can only impact its neighbors and . We describe the model in Assumption 4.7 and obtain related results in Proposition 4.8.

Assumption 4.7 (Near Neighbor Contagion Model).

Let the intensity family be given by Assumption 3.7. We further assume that each obligor can only impact its neighbors and . To be specific, we set , and

| (4.14) |

where , , are constants.

Proposition 4.8.

Proof.

The proof is placed in Appendix B.4. ∎

5 Numerical Studies

In Section 5.1, we demonstrate how to apply theoretical results from Propositions 4.6 and 4.8 to compute CDO index and tranche spreads, and calculate the attachment/detachment times in a toy example. Furthermore, we carry out a sensitivity analysis to investigate the impact of various model parameters on tranche spreads. In Section 5.2, we mainly focus on calibrating the homogeneous contagion model to market data and validate the practical use of our novel default risk model.

Throughout this section, the intensity family and the macroeconomic factor are specified as in Assumption 4.1. We consider two specific default models in the studies, namely the homogeneous contagion model (HCM) from Assumption 4.5 and the near neighbor contagion model (NCM) from Assumption 4.7. We choose the following base parameters for our default contagion models.

-

•

The number of obligors is (e.g., the constitutes of iTraxx); the risk-free interest rate is ; the payments of CDS premiums are made quarterly, i.e., ; the recovery rates are the same for all obligors, and .

- •

- •

- •

The programming codes for all numerical studies in this section are written in Python and performed on a Thinkpad PC with Intel(R) 2.50 GHz processor and 8.0GB RAM.

5.1 Sensitivity Analysis

We first compute the 5-year CDO tranche spreads using the formulas from Proposition 4.6 (for HCM) and Proposition 4.8 (for NCM), and list them in bp (1bp = ) in Table 1. In this example, we take the same attachment points as those of iTraxx Europe, and the upfront rates are set from 500 bp to 0 bp, from equity tranche to super senior tranche. The upfront rates are artificial, only for illustrative purpose. For example, the equity spread of the iTraxx Europe is the upfront premium on the tranche nominal, quoted in percentage, plus the running fee 500 bp. In the example, since and the CDO has 5 years maturity, the number of payments is . The CPU running time for the HCM and NCM are respectively 5.73 seconds and 2.41 seconds.

| Tranches | Upfront Rate(bp) | HCM. Spread(bp) | NCM. Spread(bp) |

|---|---|---|---|

| 500 | 1002 | 418 | |

| 400 | 840 | 190 | |

| 300 | 795 | 211 | |

| 200 | 777 | 235 | |

| 100 | 739 | 259 | |

| 0 | 619 | 283 |

Next, we calculate the attachment and detachment times (in years) under HCM. From the results in Table 2, we observe that the equity tranche will endure losses in half a year and be wiped out in 1.25 years. However, higher tranches and would take decades to be wiped out.

| Tranches | Detachment Default Obligors | Attachment Time (year) | Detachment Time (year) |

|---|---|---|---|

| 6 | 0.5 | 1.25 | |

| 13 | 1.25 | 1.75 | |

| 19 | 1.75 | 2.25 | |

| 25 | 2.25 | 3 | |

| 46 | 3 | 11 | |

| 125 | 11 | 294 |

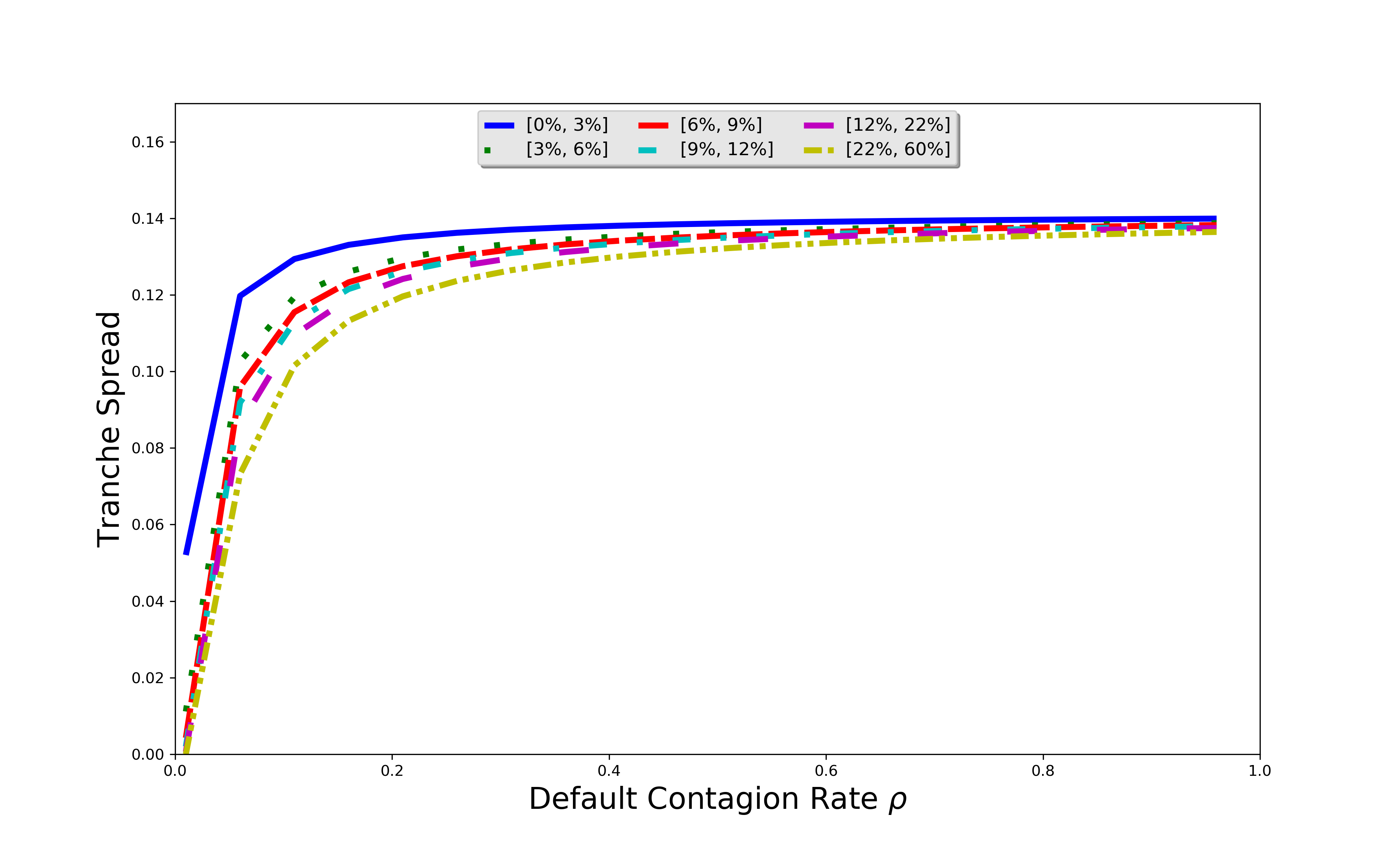

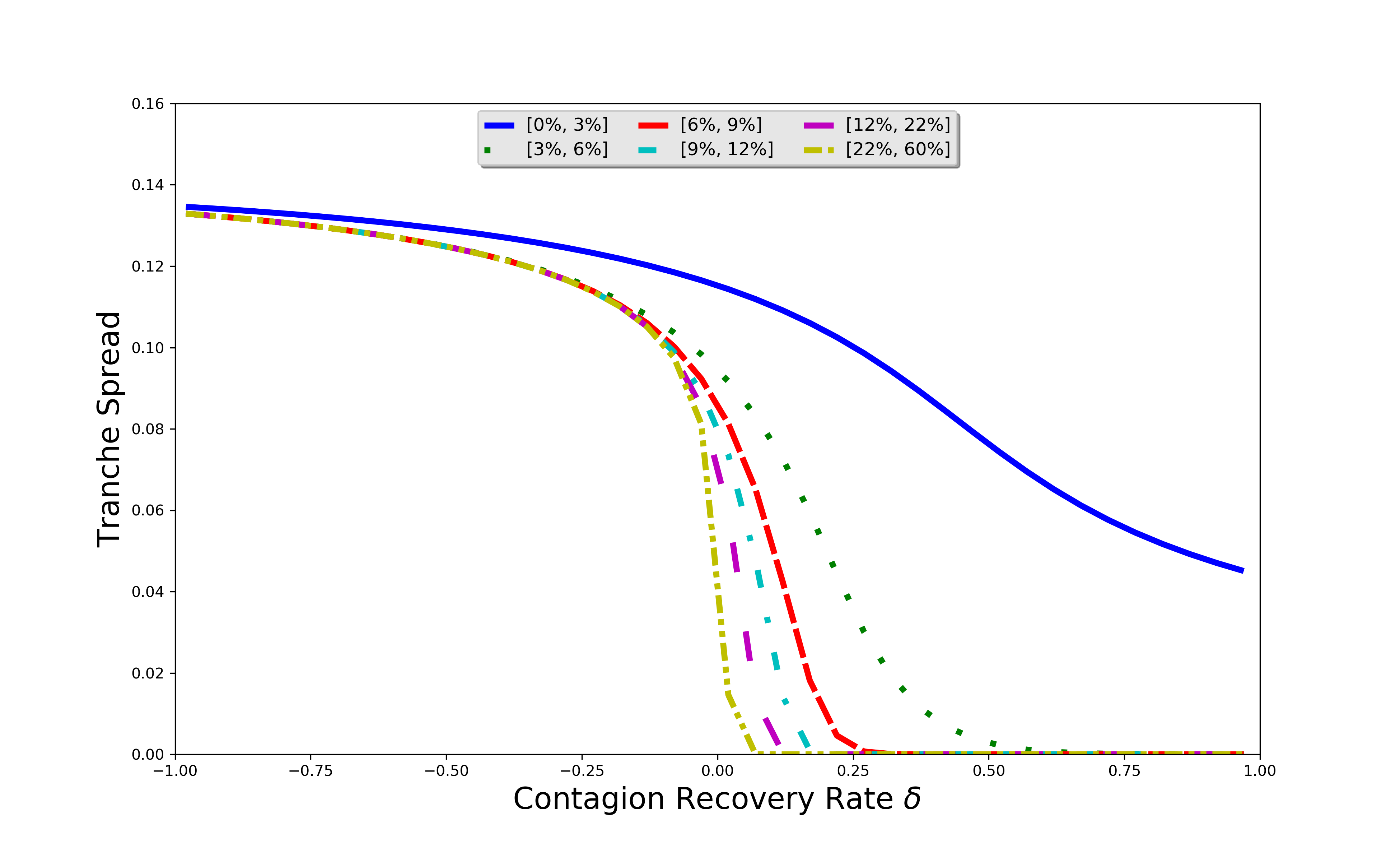

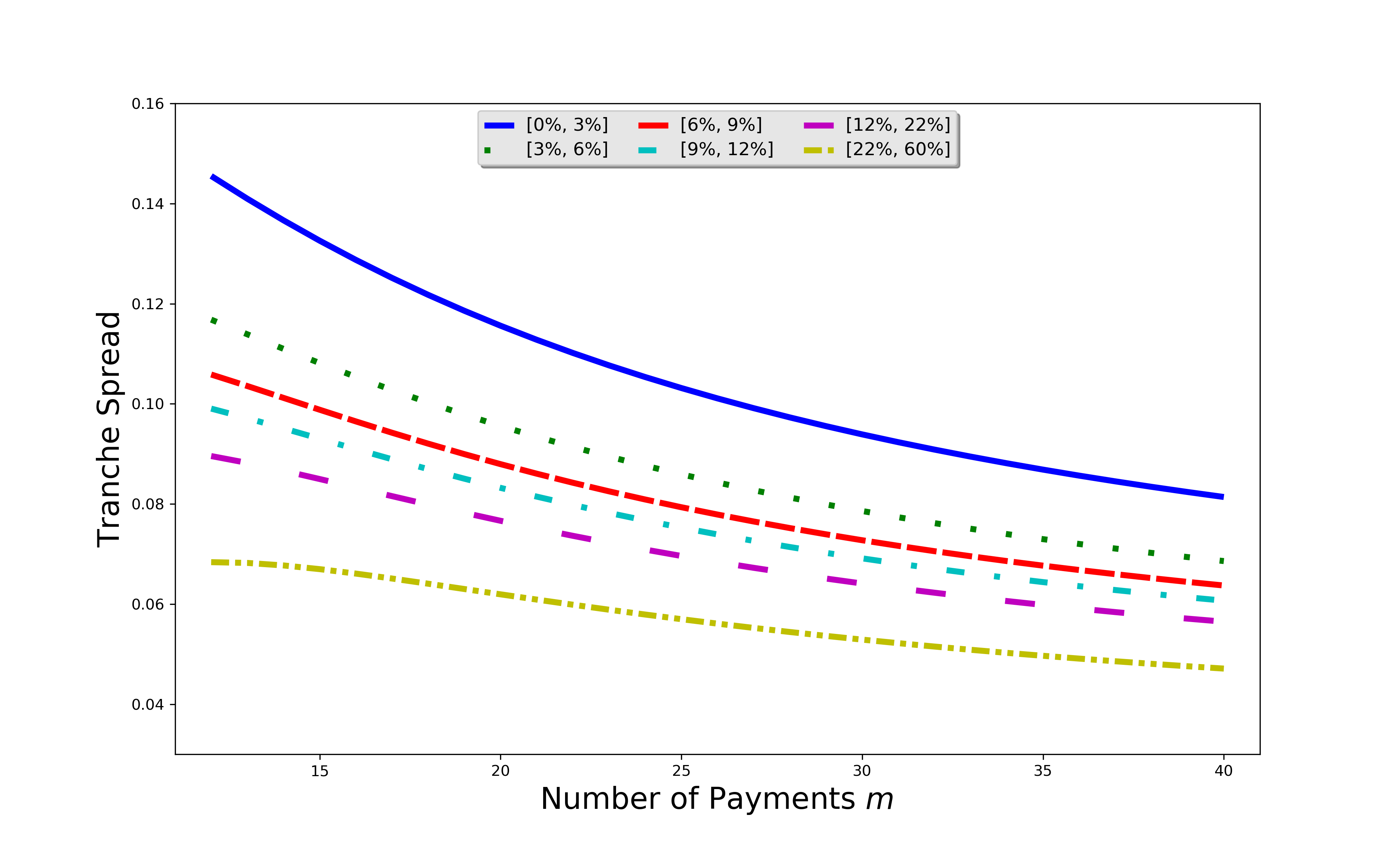

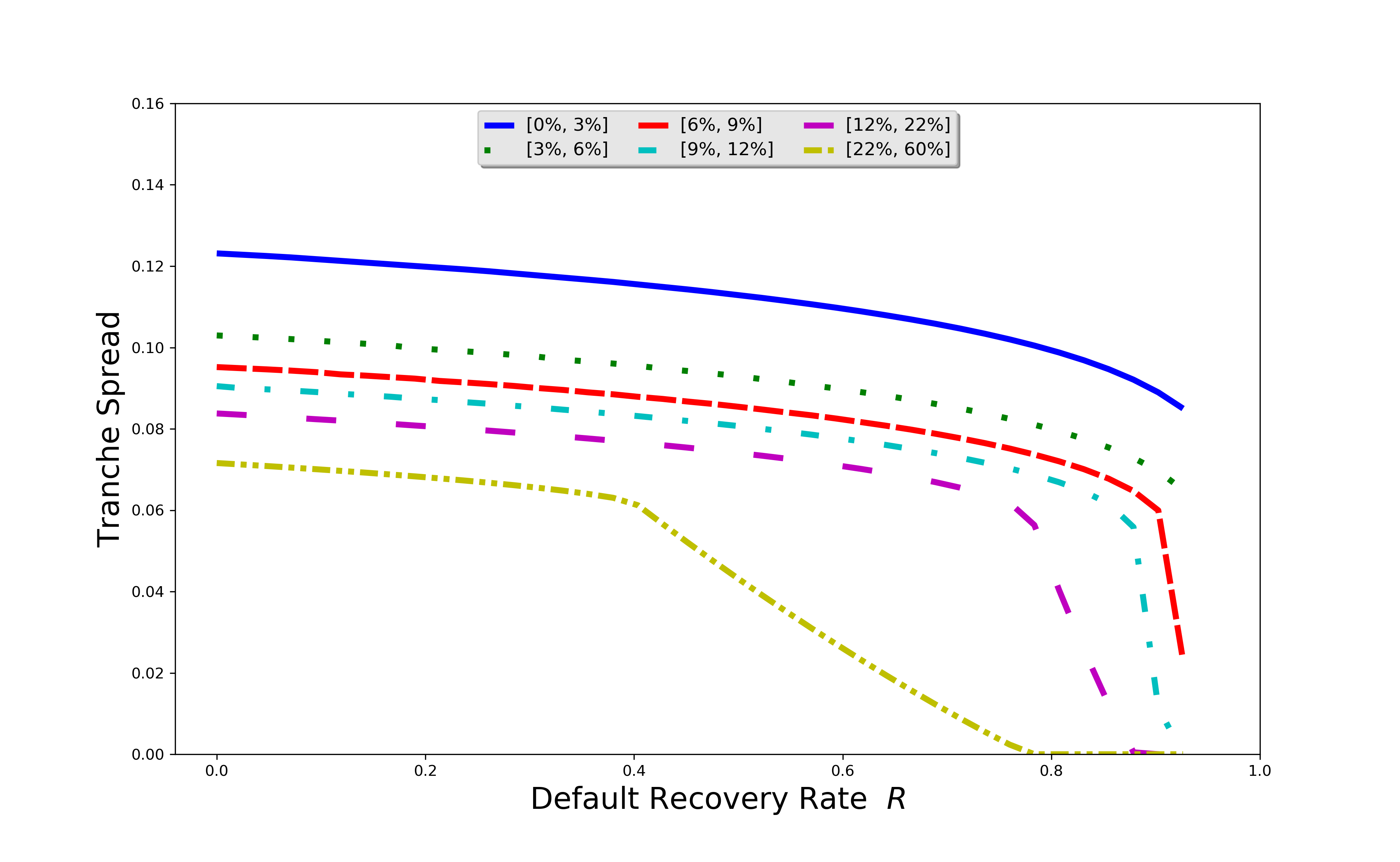

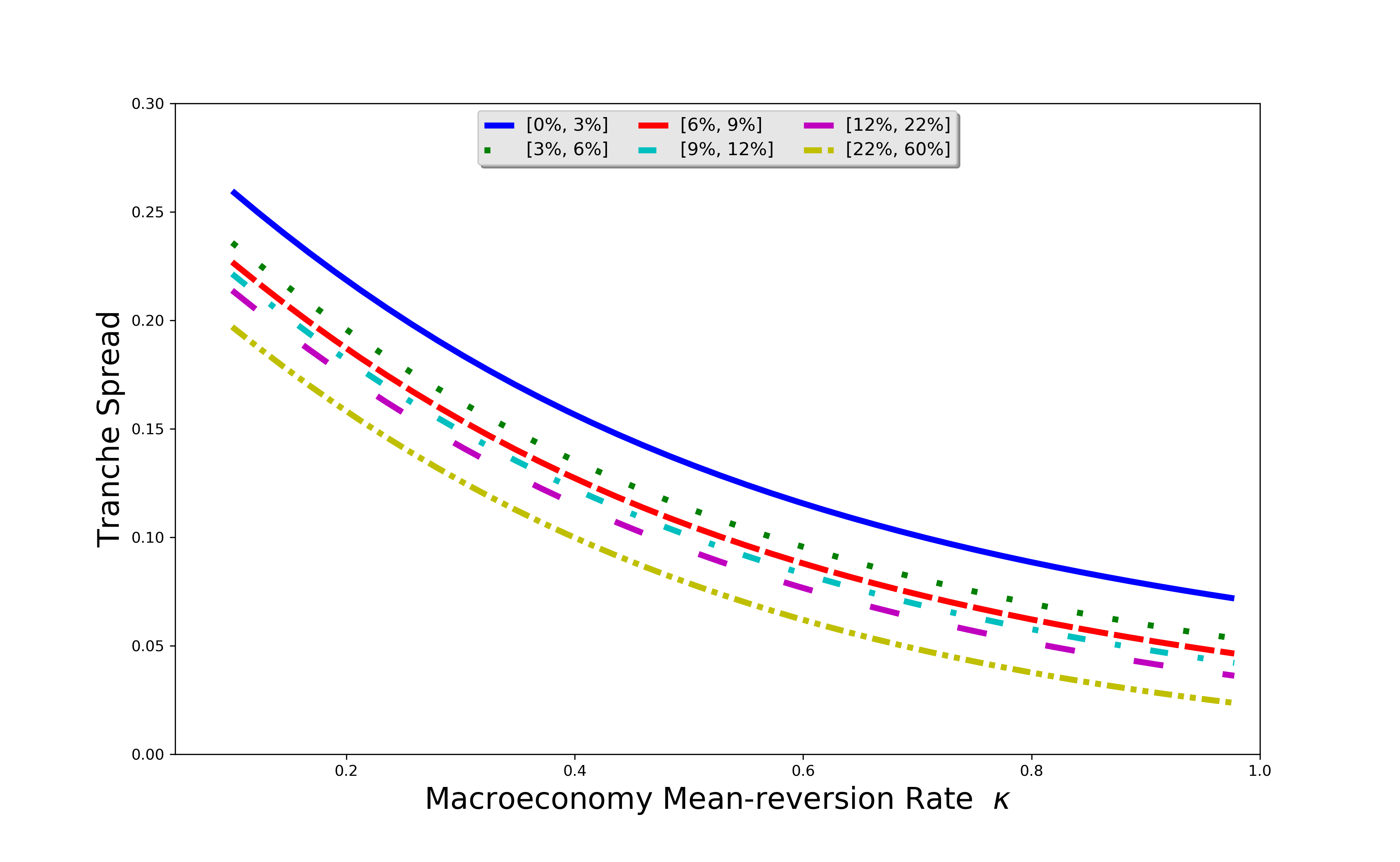

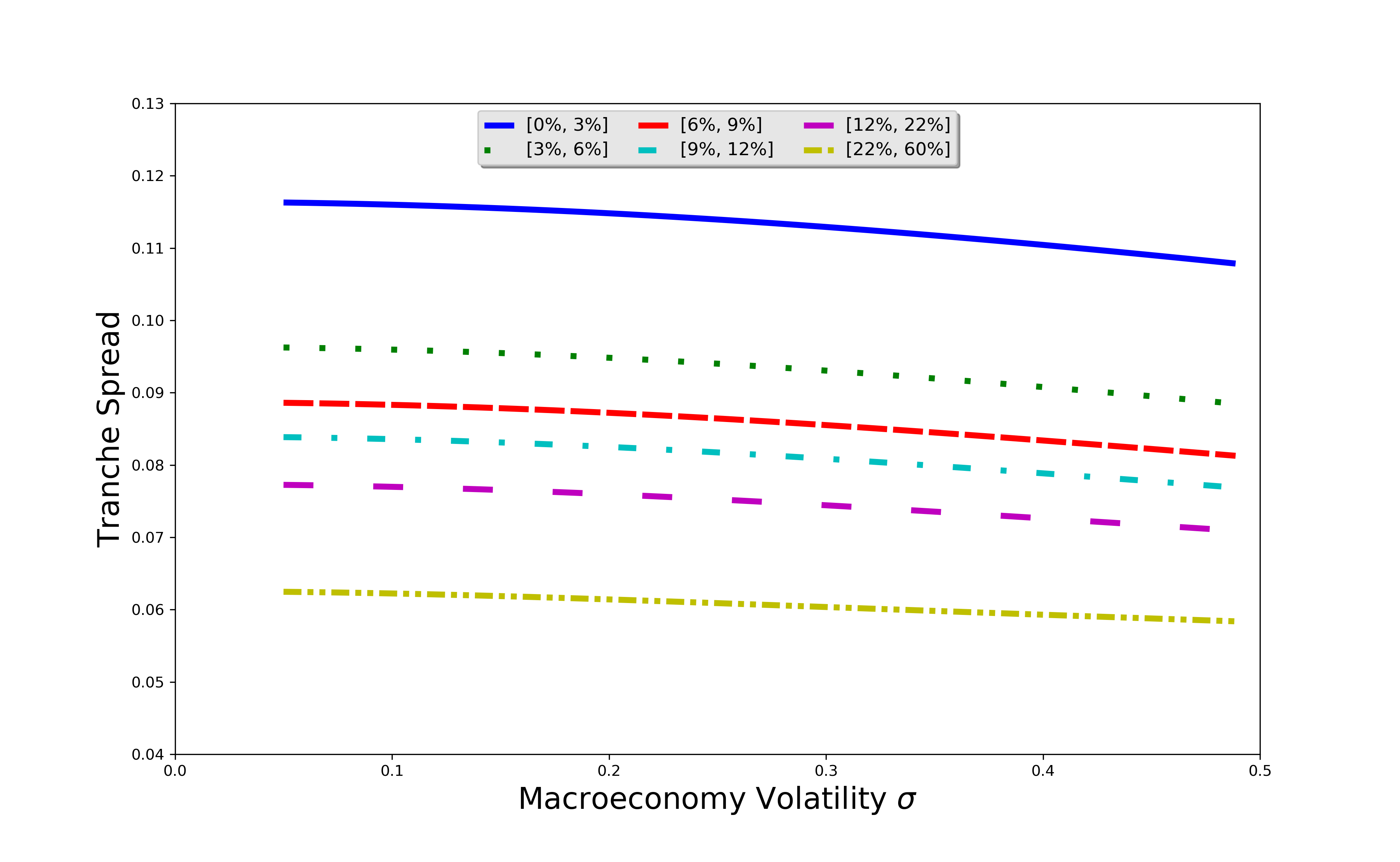

We then focus on the sensitivity analysis of various factors on the CDO tranche spreads under HCM. In the sensitivity studies, we investigate only one factor each time, and keep other factors the same as in the setup of base parameters. The factors we consider are default contagion rate , contagion recovery rate , number of payments , default recovery rate , macroeconomy mean-reversion rate and volatility . For illustrative purpose, we choose upfront rate for all tranches. According to the graphs in Figure 1, we arrive at the following conclusions.

-

•

The CDO tranche spreads are very sensitive to all factors considered here, except for the macroeconomy volatility .

-

•

Among all six factors considered, only the default contagion rate is positively related with respect to the tranche spreads, while the rest shows negative relation.

-

•

The tranche spreads are extremely elastic to the default contagion rate and contagion recovery rate . One can interpret as the government intervene or self recovery rate of the group. The equity tranche is less sensitive to comparing with other tranches.

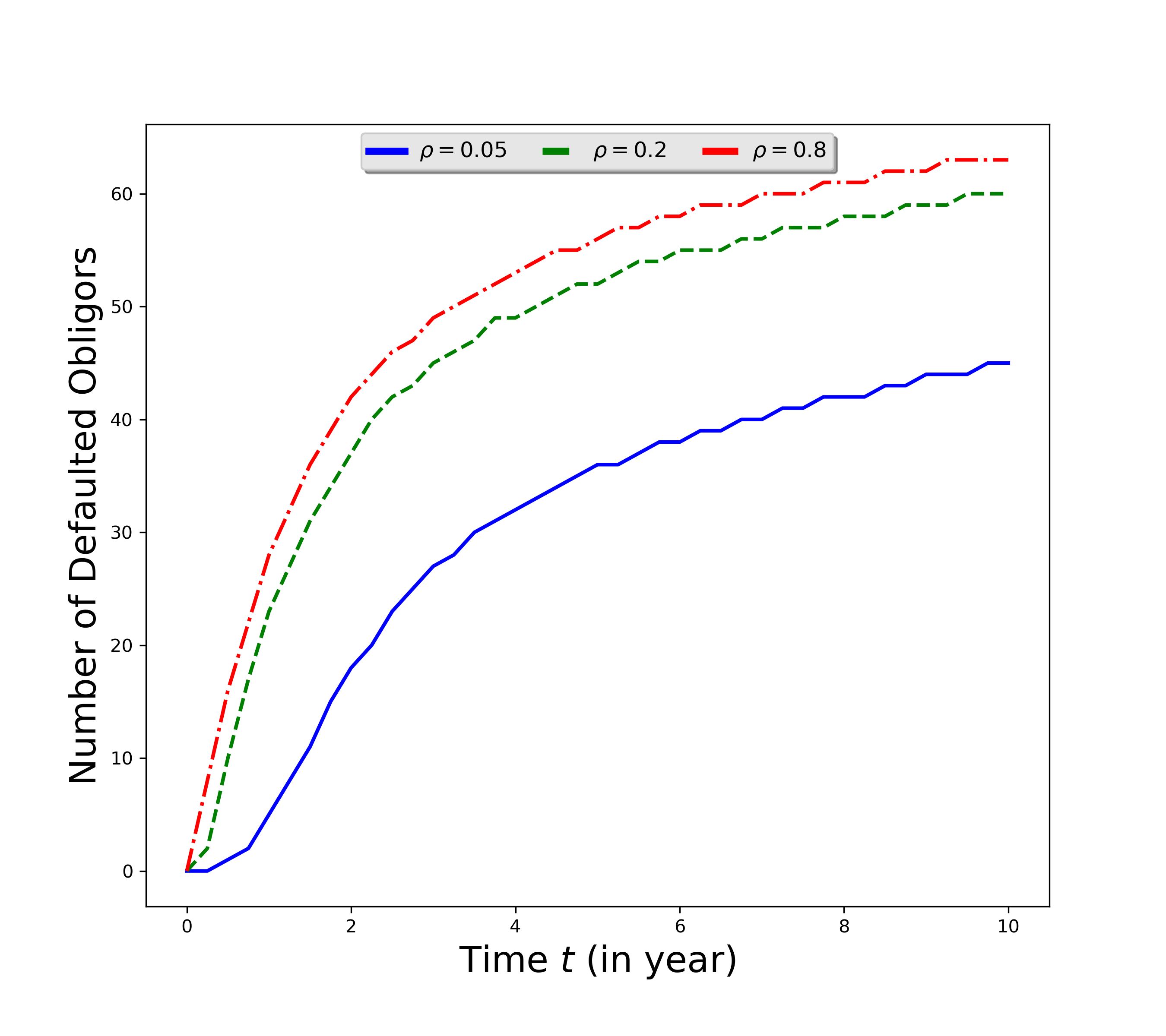

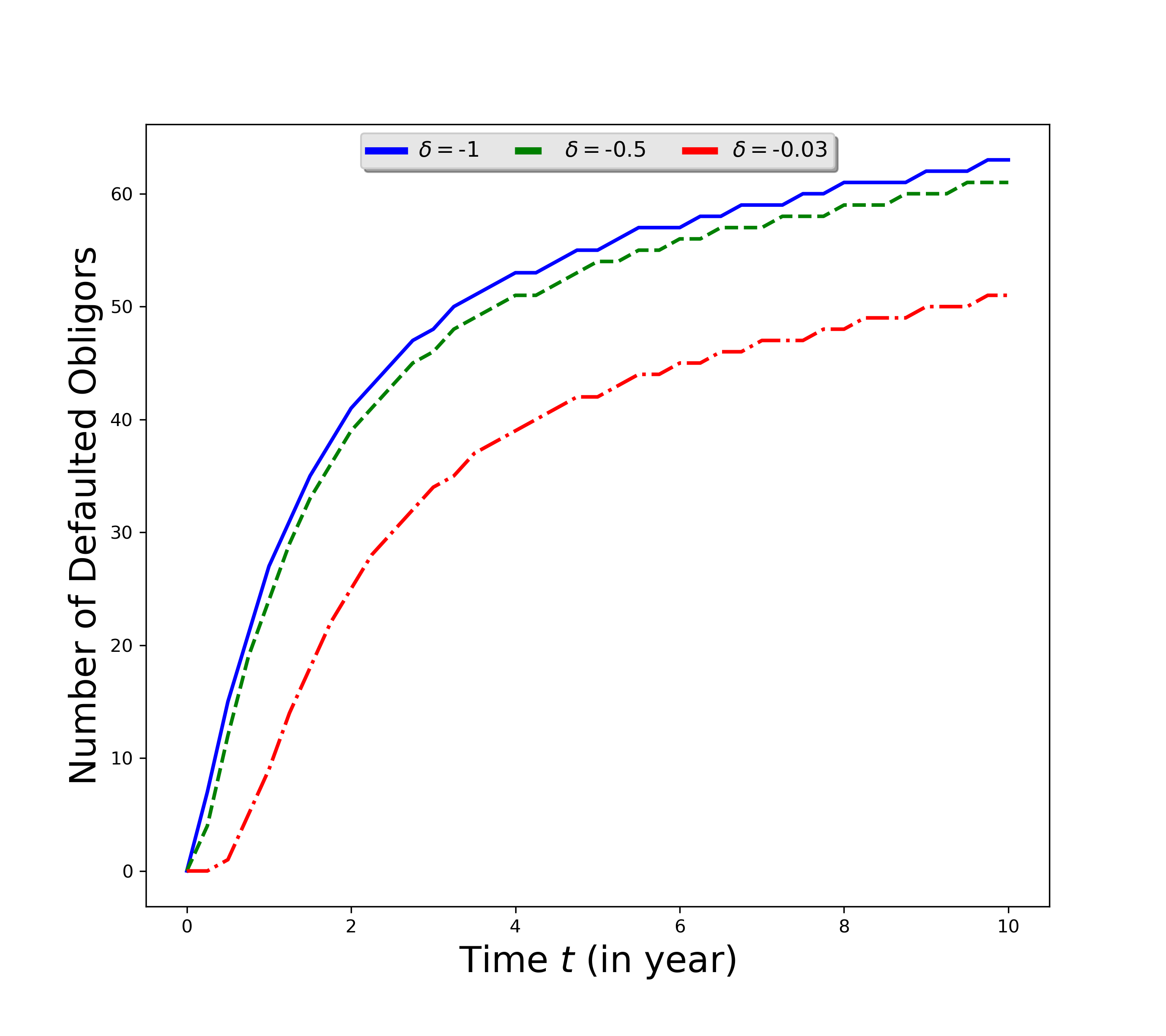

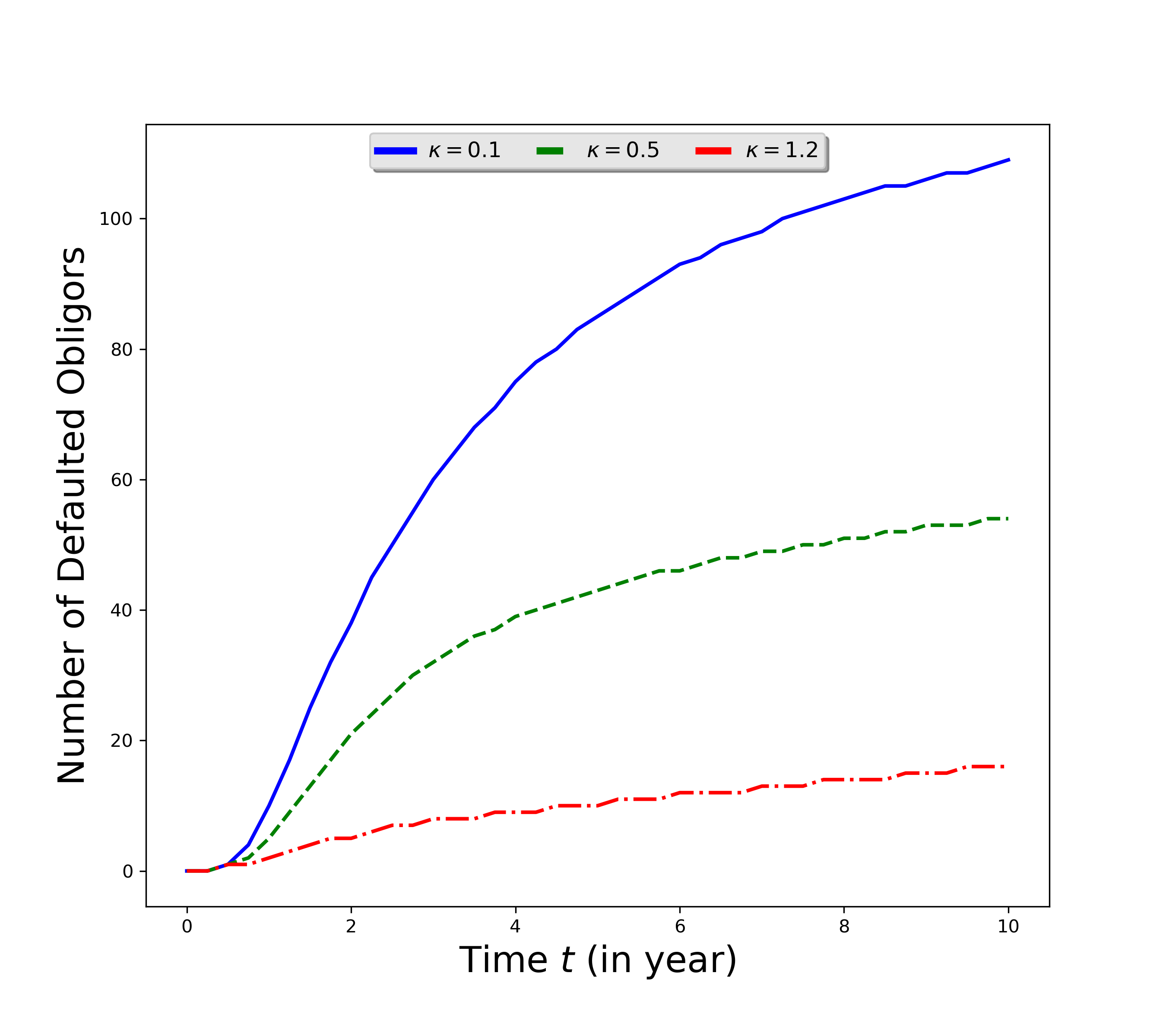

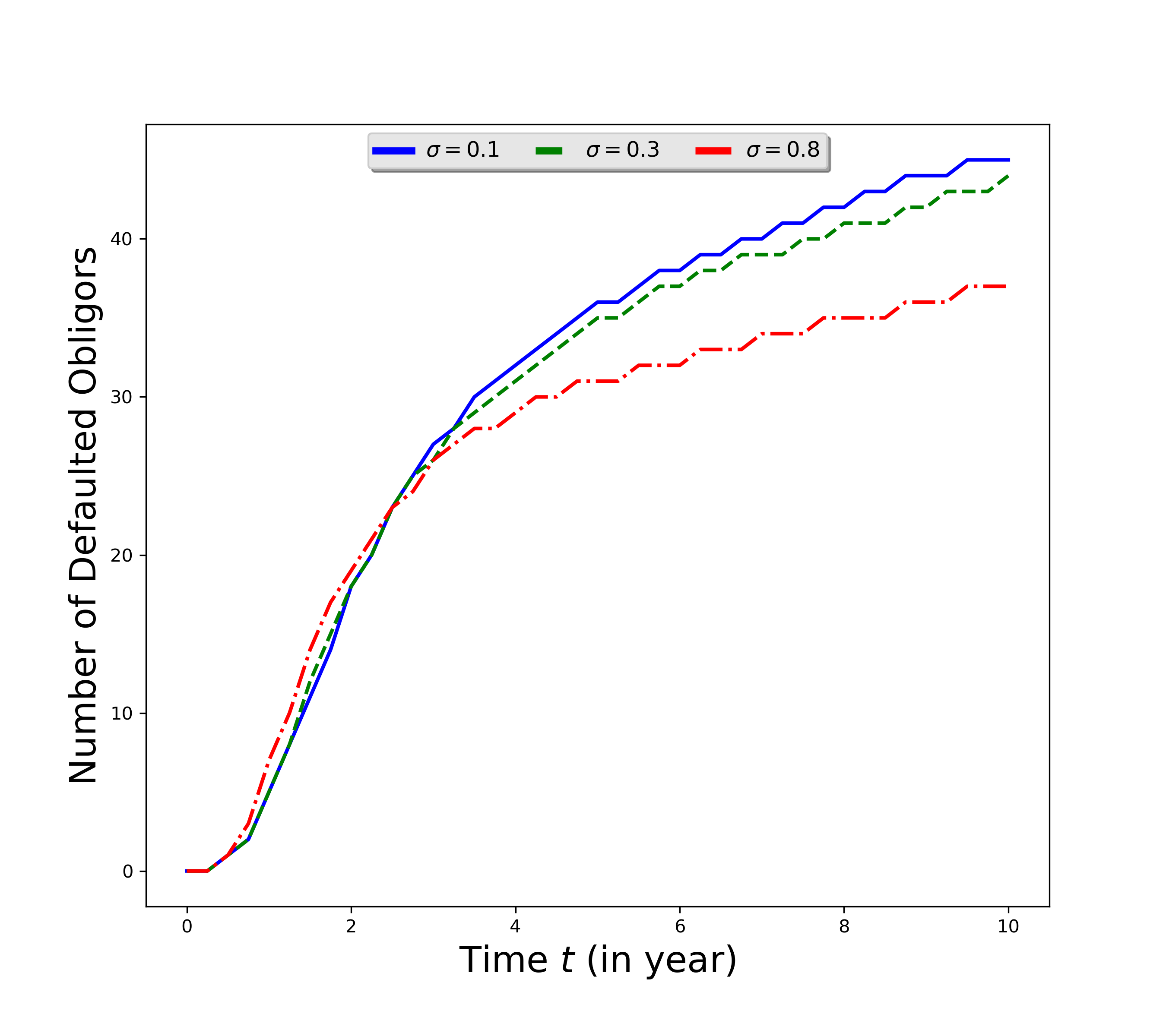

Last, we study how the number of defaulted obligors evolves in time with respects to four factors , , and . The results are plotted in Figure 2. We find that the increase of the default contagion rate leads to the increase of defaulted obligors, since directly measures the default contagion rate. In the meantime, the number of defaulted obligors reduces when , or increases since it alleviates the severity of contagions .

5.2 Market Calibration

In Section 5.1, the base parameters are pre-selected, not calibrated using market data. In this subsection, we use the market data666We use the data from Giesecke and Kim, (2007). of the CDX North American High Yield (CDX.NA.HY) index and its spreads observed on to calibrate the parameters of the default intensity family . The CDX.NA.HY index constitutes of equally weighted obligors with attachments points . The first two tranches and are quoted as a percentage of the upfront fee, while the others are quoted as a percentage of the running spread fee.

In the remaining studies, we only consider the homogeneous contagion model (HCM), introduced in Assumption 4.5, since the near neighbor contagion model (NCM) does not fit the market data well. As a result, we aim to use the CDX.NA.HY market data to estimate the parameters vector . To obtain the best fit , we solve the following minimization problem

| (5.2) |

where .777Giesecke et al., (2011) consider similar feasible region in their studies. Changing the feasible region will only slightly affect calibration. is tranche ’s spread under HCM (see Proposition 4.6). is the average of tranche ’s bid-ask quote, where , and is the CDX.NA.HY index.

We consider both 5Y and 7Y CDX.NA.HY indexes in the calibration. We apply the sequential least squares programming (SLSQP) method built in Python Scipy package to solve the above minimization problem. The step size used for numerical approximation of the Jacobian is set to 1.49e-10, and the precision goal for the minimization value of the stopping criterion is 1e-15. We first calibrate the model parameters to two indexes separately and list the results in Table 3.

The calibrated optimal parameters for 5Y CDX.NA.HY are The calibrated optimal parameters for 7Y CDX.NA.HY are The average absolute percentage errors (AAPE) of the 5Y and 7Y CDX.NA.HY indexes are and respectively, both of which are on reasonable levels since liquidity risk and market makers’ premium are included in the market prices. We share the same view as Mortensen, (2006) that it is difficulty to rule out supply and demand effects caused by market segments or market inefficiency, and a prefect fit to the market prices should perhaps not be expected.

| Tranche | 5Y-Bid | 5Y-Ask | 5Y-Model | 7Y-Bid | 7Y-Ask | 7Y-Model |

|---|---|---|---|---|---|---|

| 70.50% | 70.75% | 66.70% | 80.13% | 80.38% | 78.39% | |

| 34.25% | 34.50% | 32.89% | 55.50% | 55.75% | 53.44% | |

| 316.00 | 319.00 | 337.72 | 582.00 | 587.00 | 626.24 | |

| 79.00 | 81.00 | 78.82 | 180.00 | 183 .00 | 180.07 | |

| Index | 262.85 | 263.10 | 248.00 | 307.50 | 307.75 | 278.43 |

| MinObj | 0.011 | 0.016 | ||||

| AAPE | 4.36% | 4.73% |

Next, we use the joint data of two indexes and redo the calibration. The results are obtained in Table 4. In the case of joint calibration, the optimal model parameters are .

| Tranche | 5Y-Bid | 5Y-Ask | 5Y-Model | 7Y-Bid | 7Y-Ask | 7Y-Model |

|---|---|---|---|---|---|---|

| 70.50% | 70.75% | 67.22% | 80.13% | 80.38% | 77.61% | |

| 34.25% | 34.50% | 33.72% | 55.50% | 55.75% | 54.26% | |

| 316.00 | 319.00 | 342.02 | 582.00 | 587.00 | 604.84 | |

| 79.00 | 81.00 | 77.46 | 180.00 | 183.00 | 174.16 | |

| Index | 262.85 | 263.10 | 245.87 | 307.50 | 307.75 | 273.66 |

| MinObj | 0.031 | |||||

| AAPE | 4.83% |

Under both top-down and bottom-up approaches, the contributions of systematic and idiosyncratic default risks are independent. Precisely, the individual default intensity is assumed to take the form of , where and are independent processes representing the systematic and idiosyncratic components respectively, see Mortensen, (2006). Our numerical studies show that the systematic default risk coupled with default contagion risk (which is model by the individual contagion rate matrix under our framework) could have the leading component of the total default risk even without individual idiosyncratic factor. Such a key finding is consistent with the conclusions in Jorion and Zhang, (2007). For single name CDS, individual idiosyncratic risk might play a key role; while for CDS index such as CDX and iTraxx, idiosyncratic risk is less significant in the aggregate default effect.

Last, we are concerned with an important parameter in HCM, the default contagion rate , see Assumption 4.5. Using the separately calibrated parameters (except ) for the 5Y and 7Y CDX.NA.HY indexes, we calculate the implied default contagion rate and present the results for the corresponding tranches in Table 5. Note that the implied of tranche is the one that solves the equation , similar to the implied volatility of call/put options. We observe a “smile” pattern of the implied default contagion rate , similar to the volatility “smile” of options and the implied correlation “smile” in CDX tranches, see O’Kane and Livesey, (2004). One possible explanation is that, the CDO tranches are segmented and each tranche contains a mixture of effects, including systematic and idiosyncratic credit risk, liquidity effect, and supply and demand for certain tranches.

| Tranche | 5Y-Implied | 7Y-Implied |

|---|---|---|

| 0.0027 | 0.010 | |

| 0.00092 | 0.0082 | |

| 0.0026 | 0.0075 | |

| 0.0026 | 0.0072 | |

| Index | 0.0027 | 0.0082 |

6 Conclusion

We propose a novel default contagion framework on credit risk modeling, which takes into consideration the dynamical contagion effect among obligors and the impact of macroeconomic factors. We consider a group of defaultable obligors and model the default process by a set-valued Markov process , where is the set of all obligors that have defaulted by time . We are able to derive the dynamics of the default process in explicit forms, and apply the results to obtain analytic pricing formulas for credit debt obligations (CDOs). The homogeneous contagion model (HCM) and near neighbor contagion model (NCM) are studied as special cases within our general framework.

In numerical studies, we demonstrate how analytic pricing results can be easily programed to compute the tranche spreads, and investigate the impact of various model factors on the tranche spreads. Furthermore, we use the 5Y and 7Y CDX.NA.HY market data to calibrate the HCM and validate the practical applications of our new framework. The model fits the 5Y and 7Y CDX.NA.HY tranche spreads and indexes reasonably well. Our empirical findings support that systematic default risk coupled with default contagion among obligors could have the leading component of the total default risk, which is in line with the results of Jorion and Zhang, (2007).

Appendix

Appendix A Construction and Characterization of the Default Process

In this section, under Assumptions 3.1 and 3.2, we construct the default process through the pair in Appendix A.1, and prove the conditional Markov property of in Appendix A.2 and the martingale property of in Appendix A.3, respectively. Theorem 3.4 then follows immediately once the construction of is done, and the Markov and martingale properties are shown.

Recall , where is the number of obligors in the group, and is the -algebra of consisting of all the subsets of . To proceed, we make the following definitions:

| (A.1) | ||||

| (A.2) |

Under a complete probability space , an exogenous -valued stochastic process is given. Suppose a family of Poisson processes with intensity one is chosen according to Assumption 3.1. As an immediate consequence of Assumption 3.1, the processes and are mutually independent for all . In addition, a family of processes is given, which satisfies all the conditions imposed in Assumption 3.2.

For any and , let and define the process by

| (A.3) |

and the -fields below

| (A.4) | ||||

| (A.5) |

Here, the operator stands for the sigma-algebra generated by all indexed (the index set could be uncountable). Recall Assumption 3.2, if where , then for all . The proposition regarding below is straightforward to check, and hence the proof is omitted.

Proposition A.1.

Essentially, Proposition A.1 shows that, for any fixed and , the process is an -conditional inhomogeneous Poisson process with intensity .

A.1 Construction of the Default Process

In this subsection, we construct the default process by induction on the pair . Recall that under our framework, is the -th default time and is the set of obligors that have defaulted by time . Once are constructed for all , we follow (2.5) and define the default process by

| (A.10) |

where and . Note that for all .

The induction algorithm below allows us to construct a sequence for the pair .

-

Step 1.

As convention, let and .

-

Step 2.

Assume are defined for and satisfy that

-

(i)

Both and are -measurable, and .

-

(ii)

.

-

(i)

-

Step 3.

For any with , and , define

(A.11) (A.12) (A.13)

Intuitively, is the default time of obligor , given that obligors in set have already defaulted, where . is the -th default time, given that the default process at is . It is worth pointing out that the set is not empty, since is finite. The following lemma completes the definition of .

Lemma A.2.

Proof.

(i) Since and are -measurable, is -measurable by construction. For any , we have

| (A.14) | ||||

| (A.15) |

Hence, we conclude is -measurable.

(ii) To show , it suffices to show that for all and . Since , we obtain

| (A.16) | ||||

| (A.17) | ||||

| (A.18) | ||||

| (A.19) |

where to derive the last equality, we have used the assumption that as .

For any with , and with , assertion (iii) of Proposition A.1 implies that is -conditional independent of . Therefore, we have for all and 888Indepdent Poisson processes do not jump simultaneously., and thus

| (A.20) | ||||

| (A.21) |

The same argument leads to . Then, we conclude that . This ends the proof. ∎

At this stage, the construction of the default process is complete. Before we move on to show the Markov property of , we present essential results in the proposition below, which are key to the proofs in the next subsection. The following notations are used in the sequel:

| (A.22) |

Proposition A.3.

Proof.

(i) is obvious.

(ii) For any with , since are -conditional independent of , we obtain

| (A.27) | ||||

| (A.28) | ||||

| (A.29) |

The second equality can be proved by following the same argument.

(iii) For , with , and , we have

| (A.30) | ||||

| (A.31) | ||||

| (A.32) | ||||

| (A.33) | ||||

| (A.34) |

Since and , we have for some and . Denote

| (A.35) | ||||

| (A.36) |

It is easy to see and Hence, on the set , we obtain . By the existence of regular conditional probability, there exists a random measure , where such that is equal to . Since

| (A.37) |

we obtain, for all , that

Therefore, for any measurable function on ,

| (A.38) | ||||

| (A.39) | ||||

| (A.40) |

which completes the proof. ∎

A.2 Conditional Markov Property and Transition Probability of

In this subsection, our main goal is to show the conditional Markov property of the default process , and characterize its transition probability. The related conclusions are presented in Proposition A.4.

Proposition A.4.

Proof.

(i) Recall defined in (A.22). We first show, for any , and ,

| (A.43) |

where is defined in (3.4). Suppose , where . We prove (A.43) by induction.

Step 1: If , i.e., . By assertion (ii) of Proposition A.3, we have

| (A.44) | ||||

| (A.45) | ||||

| (A.46) | ||||

| (A.47) | ||||

| (A.48) | ||||

| (A.49) |

Step 2: Suppose that (A.43) holds for all pairs with , where . Now consider a pair with . By (ii) and (iii) of Proposition A.3, we deduce

| (A.50) | ||||

| (A.51) | ||||

| (A.52) | ||||

| (A.53) | ||||

| (A.54) | ||||

| (A.55) | ||||

| (A.56) | ||||

| (A.57) | ||||

| (A.58) | ||||

| (A.59) | ||||

| (A.60) | ||||

| (A.61) | ||||

| (A.62) | ||||

| (A.63) |

which shows equality (A.43) holds true for .

Now by taking in (A.43) as , we get

| (A.64) | ||||

| (A.65) | ||||

| (A.66) | ||||

| (A.67) |

The second equality of (A.41) follows from the fact that is -measurable. This completes the proof of assertion (i).

(ii) Notice that, for any and , using (A.41) in (i), we derive

| (A.68) | ||||

| (A.69) |

Hence, it is enough to prove, for all , that

| (A.70) |

or, equivalently, , , , and

| (A.71) |

which is obvious by (i). The proof is then complete. ∎

A.3 Martingale Property of

In this subsection, we complete the last part of the proof to Theorem 3.4 by showing that the family as specified by Assumption 3.2 is the default intensity of the default process . The key results are summarized in the proposition below.

Proposition A.5.

For any , the process , defined by

| (A.72) |

is an -martingale, where .

Proof.

It is enough to prove, for all , , with , that i.e.,

| (A.73) |

By the monotone class theorem, for any and , without loss of generality, we take arbitrary , , and show that

| (A.74) |

In the following, we will prove (A.74) for the cases and . Recall functionals and defined in (3.4) and (3.6).

Case 1: . Without loss of generality, we assume and Then, using assertions (i) and (ii) in Proposition A.4, we have

| (A.75) | |||||

| (A.77) | |||||

| (A.79) | |||||

Take any , and recall the definitions of in (3.1) and , we obtain

| (A.80) | |||||

| (A.81) | |||||

| (A.82) | |||||

| (A.83) | |||||

| (A.85) | |||||

| (A.86) |

Thus,

| (A.87) | |||||

| (A.88) | |||||

| (A.89) | |||||

| (A.90) |

Finally, we are able to show that

| (A.91) | |||||

| (A.92) | |||||

| (A.93) | |||||

| (A.94) |

which completes the proof for the case of .

Case 2: . Since , we derive

This proves the case of , and thus completes the proof of the proposition. ∎

Appendix B Technical Proofs

B.1 Proof of Theorem 3.5

Proof.

The proof of Corollay 3.9 relies on the following lemma.

Lemma B.1.

Let be a nonnegative function defined on and be a nonnegative function on given by . Let be real numbers, where is a positive integer. For any , define the sequence by

| (B.3) |

and .

B.2 Proof of Corollary 3.9

B.3 Proof of Proposition 4.6

Proof.

For any with , and , we have

| (B.13) |

In addition, recall , we have

| (B.14) |

and, for any doubled indexed sequence ,

| (B.15) |

where and is the integer part of . Recall is defined by (4.11) in Proposition 4.4. Using the above results, we derive

where and . Since for all , by letting , we derive

The desired result is then obtained. ∎

B.4 Proof of Proposition 4.8

Proof.

Recall the definition of in (3.15). Due to the contagion structure of NCM model, each obligor will only impact its two nearest neighbors. Hence, is non-zero only if is a consecutive sequence of the circle . Denote by the sequence which has elements and starts with , i.e., . Here, stands for the residue of two integers. We have:

| (B.16) | ||||

| (B.17) |

where is the combination number of taking distinct elements out of elements.

Using the above result, we derive

Notice that we have

Now we are ready to calculate from assertion (ii) of Proposition A.4

| (B.18) | ||||

| (B.19) | ||||

| (B.20) | ||||

| (B.21) | ||||

| (B.22) |

where in the last equality above, we used the fact , and for a positive integer . Since for all , by letting , it gives This completes the proof. ∎

References

- Bielelcki et al., (2011) Bielelcki, T. R., Crépey, S., and Herbertsson, A. (2011). Markov chain models of portfolio credit risk. In The Oxford Handbook of Credit Derivatives.

- Black and Cox, (1976) Black, F. and Cox, J. C. (1976). Valuing corporate securities: Some effects of bond indenture provisions. Journal of Finance, 31(2):351–367.

- Black and Scholes, (1973) Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3):637–654.

- Collin-Dufresne et al., (2004) Collin-Dufresne, P., Goldstein, R., and Hugonnier, J. (2004). A general formula for valuing defaultable securities. Econometrica, 72(5):1377–1407.

- Cont et al., (2010) Cont, R., Deguest, R., and Kan, Y. H. (2010). Default intensities implied by cdo spreads: Inversion formula and model calibration. SIAM Journal on Financial Mathematics, 1(1):555–585.

- Cont and Minca, (2013) Cont, R. and Minca, A. (2013). Recovering portfolio default intensities implied by cdo quotes. Mathematical Finance, 23(1):94–121.

- Cox et al., (1985) Cox, J., Ingersoll Jr, J., and Ross, S. (1985). A theory of the term structure of interest rates. Econometrica, 53(2):385–408.

- Das et al., (2007) Das, S. R., Duffie, D., Kapadia, N., and Saita, L. (2007). Common failings: How corporate defaults are correlated. Journal of Finance, 62(1):93–117.

- Ding et al., (2009) Ding, X., Giesecke, K., and Tomecek, P. (2009). Time-changed birth processes and multiname credit derivatives. Operations Research, 57(4):990–1005.

- Duffie et al., (2009) Duffie, D., Eckner, A., Horel, G., and Saita, L. (2009). Frailty correlated default. Journal of Finance, 64(5):2089–2123.

- Duffie and Garleanu, (2001) Duffie, D. and Garleanu, N. (2001). Risk and valuation of collateralized debt obligations. Financial Analysts Journal, 57(1):41–59.

- Duffie et al., (2000) Duffie, D., Pan, J., and Singleton, K. (2000). Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68(6):1343–1376.

- Duffie and Singleton, (1999) Duffie, D. and Singleton, K. (1999). Modeling term structures of defaultable bonds. Review of Financial Studies, 12(4):687–720.

- Eom et al., (2004) Eom, Y. H., Helwege, J., and Huang, J.-z. (2004). Structural models of corporate bond pricing: An empirical analysis. Review of Financial Studies, 17(2):499–544.

- Errais et al., (2010) Errais, E., Giesecke, K., and Goldberg, L. (2010). Affine point processes and portfolio credit risk. SIAM Journal on Financial Mathematics, 1(1):642–665.

- Errais et al., (2007) Errais, E., Giesecke, K., Goldberg, L., and Barra, M. (2007). Pricing credit from the top down with affine point processes. Numerical Methods for Finance, pages 195–201.

- Feller, (1951) Feller, W. (1951). Two singular diffusion problems. Annals of Mathematics, pages 173–182.

- Financial-Crisis-Inquiry-Commission-Report, (2011) Financial-Crisis-Inquiry-Commission-Report (2011). The financial crisis inquiry report, authorized edition: Final report of the National Commission on the Causes of the Financial and Economic Crisis in the United States. Public Affairs.

- Frey and Backhaus, (2010) Frey, R. and Backhaus, J. (2010). Dynamic hedging of synthetic cdo tranches with spread risk and default contagion. Journal of Economic Dynamics and Control, 34(4):710–724.

- Frey et al., (2001) Frey, R., McNeil, A., and Nyfeler, M. (2001). Copulas and credit models. Risk, 10(111114.10).

- Giesecke et al., (2011) Giesecke, K., Goldberg, L. R., and Ding, X. (2011). A top-down approach to multiname credit. Operations Research, 59(2):283–300.

- Giesecke and Kim, (2007) Giesecke, K. and Kim, B. (2007). Estimating tranche spreads by loss process simulation. In Proceedings of the 39th Conference on Winter Simulation, pages 967–975. IEEE Press.

- Herbertsson, (2008) Herbertsson, A. (2008). Pricing synthetic cdo tranches in a model with default contagion using the matrix analytic approach. Journal of Credit Risk, 4:3–35.

- Hull and White, (2006) Hull, J. C. and White, A. D. (2006). Valuing credit derivatives using an implied copula approach. Journal of Derivatives, 14(2):8.

- Jarrow et al., (1997) Jarrow, R. A., Lando, D., and Turnbull, S. M. (1997). A markov model for the term structure of credit risk spreads. Review of Financial Studies, 10(2):481–523.

- Jarrow and Turnbull, (1995) Jarrow, R. A. and Turnbull, S. M. (1995). Pricing derivatives on financial securities subject to credit risk. Journal of Finance, 50(1):53–85.

- Jorion and Zhang, (2007) Jorion, P. and Zhang, G. (2007). Good and bad credit contagion: Evidence from credit default swaps. Journal of Financial Economics, 84(3):860–883.

- Lando, (1998) Lando, D. (1998). On cox processes and credit risky securities. Review of Derivatives Research, 2(2-3):99–120.

- Laurent et al., (2011) Laurent, J.-P., Cousin, A., and Fermanian, J.-D. (2011). Hedging default risks of cdos in markovian contagion models. Quantitative Finance, 11(12):1773–1791.

- Laurent and Gregory, (2005) Laurent, J.-P. and Gregory, J. (2005). Basket default swaps, cdos and factor copulas. Journal of Risk, 7(4):103–122.

- Li, (2000) Li, D. X. (2000). On default correlation: A copula function approach. Journal of Fixed Income, 9(4):43–54.

- Merton, (1974) Merton, R. C. (1974). On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance, 29(2):449–470.

- Mortensen, (2006) Mortensen, A. (2006). Semi-analytical valuation of basket credit derivatives in intensity-based models. Journal of Derivatives, 13(4):8–26.

- Nickerson and Griffin, (2017) Nickerson, J. and Griffin, J. M. (2017). Debt correlations in the wake of the financial crisis: What are appropriate default correlations for structured products? Journal of Financial Economics, 125(3):454–474.

- O’Kane and Livesey, (2004) O’Kane, D. and Livesey, M. (2004). Base correlation explained. Lehman Brothers, Fixed Income Quantitative Credit Research, 346.

- Schönbucher and Schubert, (2001) Schönbucher, P. J. and Schubert, D. (2001). Copula-dependent default risk in intensity models. In Working paper, Department of Statistics, Bonn University. Citeseer.

- Sundaresan, (2013) Sundaresan, S. (2013). A review of merton’s model of the firm’s capital structure with its wide applications. Annual Review of Financial Economics, 5(1):21–41.