Modeling credit default swap premiums with stochastic recovery rate

Abstract

There are many studies on development of models for analyzing some derivatives such as credit default swaps (CDS). A continuous-time autoregressive

moving average (CARMA) driven by Lévy process is applied for modeling the CDS premia. It is based on the stochastic recovery rate which is

time-varying during the maturity stage and makes the model suitable for evaluating the premium leg. We show that this model is a class of affine term

structure model.

By simulating the CARMA(2,1) process the effectiveness of this model in determining the most appropriate parameters are illustrated. Also, a real data set of daily CDS premia of some companies is used and a comparison of the Bayesian information criterion between the models is given.

Keywords CDS spread. Stochastic recovery rate. CARMA model

JEL Classification C15. C32. G13

1 Introduction

In financial markets, derivatives enable parties to trade specific financial risks and help to improve market efficiencies.

Derivatives are financial contracts which derive their value of a spot price time-series such as forwards, futures, options and swaps. One of the most

important and applicable derivatives is a credit default swap (CDS).

There are many studies about the valuation, hedging and modeling of credit risk [4]. As with any swap, valuing CDS involves calculating the

present value of two legs of the transaction, premium leg and default leg. Wemmenhove described a model for CDS spread form and presented a forecasting

model for it [20]. Also, the determinants at CDS spread of European credit derivatives are analyzed [12].

A Markov model with the bankruptcy process following a discrete state space Markov chain in credit ratings are provided and the parameters of this

process are estimated using the observable data [14].

The recovery rate and default probability have an important role in bond prices and there are many studies that attempted to model recovery and

comprehend their impact on depth values [3]. Also, modeling and empirically investigating the relationship between the components of

default risk as the probability of default and recovery rate are presented [1].

Jaskowaki et al. proposed a parsimonious reduced form continuous-time model that estimates expected recovery rates and the parameters were estimated by

using a Bayesian MCMC algorithm [13].

A class of models which has proven to be remarkable flexible structure for examining the dynamics of default-risk free bonds is an affine term

structure (ATS) model. This model suggests that interest rates at any point in time are a time-invariant linear function of a small set of common

factors. ATS models start from the assumption that there are no arbitrage opportunities in financial markets and implies the existence of a positive

stochastic process that prices the assets [9]. These models have been shown to work well in approximating true yield dynamics.

The statistical models for continuous-time dynamics based on CDS premiums of different reference entities are presented [10]. The sampled

reversion of Lévy-driven continuous-time ARMA (CARMA) process is used as an appropriate model for modeling the CDS premium leg. Brockwell et al.

introduced the CARMA processes and estimated the parameters of the model based on discrete form specially in equally spaced samples

[8], [7], [6].

A new representation of the calculated quasi-likelihood to compute maximum Gaussian likelihood for estimating the

parameters of time series with irregularly spaced data are presented [19].

For Lévy-driven CARMA processes, estimation procedures which take into account the generally non-Gaussian nature of the measure are less well

developed.

Recovery rates play a critical role in the estimation and pricing of credit risk derivatives and it is often assumed to be constant and independent of

default but it is not realistic and fair. It is shown that the recovery rates can be volatile and moreover dependent to default intensity.

In order to different risks in a company and determining the default leg, we consider the stochastic recovery rate model and compare the results. We

provide the new model under term structure time series model and the fair default payment which is applied in a risky companies contract are

considered. We study on a certain class of background Lévy CARMA process for modeling the CDS premium with stochastic recovery rate (CDSP-SRR). This

process is a stationary solution of a stochastic differential equation, so for the first step in real data analysis we use a test for stationarity and

then we apply a method for finding the best model for CDSP-SRR. Selecting appropriate order for CARMA(p,q) process in CDSP-SRR model is the same as

modeling the CDS premium with constant recovery rate (CDSP-CRR) [10].

Also, the results of data analysis for some companies show that the distributions of jumps can be compound Poisson, Normal Inverse Gaussian (NIG) and

other Lévy processes.

The rest of the paper is organized as follows. Section 2 is devoted to the preliminaries and CARMA models driven by Lévy processes, ATS models and

basic definitions of CDS contracts . We show that the Lévy-driven CARMA model is ATS, in section 3. In section 4, the dynamic of CDSP-SRR is

presented. Also, in section 5, we simulate the CDSP-SRR model and the certain CARMA process. The developed model is illustrated and compared with

CDSP-CRR. For comparing the estimated models we use the Bayesian information criteria (BIC) and chose the model giving the smallest BIC over the whole

set of candidates. We use a data set of daily CDS premia across 242 firms from the European and North American markets.

2 preliminaries

In this section we present the linear stationary CARMA model which is driven by Lévy process. Then we provide descriptions of some concepts as ATS model and CDS.

2.1 Lévy-driven CARMA model

We discuss on Lévy-driven CARMA processes and review the definition and properties of them [7].

Definition 2.1

A second-order Lévy-driven continuous-time ARMA (p,q) process is defined in terms of the following state-space representation of the formal equation. For

| (2.1) |

where D denotes differential with respect to t and is a Lévy process with finite second moments, and

| (2.2) | ||||

| (2.3) |

where the coefficients are complex-valued coefficients such that

and for .

To avoid trivial and easily eliminated complications, we assume that a(z) and b(z) have no common factors. The state-space representation consists of the observation and state equations,

| (2.4) | |||

| (2.5) |

where is a state process which is the solution of the equation and

| (2.6) |

For the matrix is equal to .

Proposition 2.1

If is independent of the Lévy process where then is a second-order stationary process if and only if the eigenvalues , of the matrix all have negative real parts.

Remark 2.2

The eigenvalues of the matrix are the same as the zeroes of autoregressive polynomial .

Under the specific condition on the eigenvalues is a causal function of . So have the following moving average representation

| (2.7) |

and equivalently . Also, under this condition and distinct eigenvalues and by the fact that CARMA process can be written as a linear combination of some continuous-time autoregressive process of order one driven by Lévy, the background driving Lévy process is recoverable and the kernel can be written as

where is the first derivative of the polynomial . Thus the above equations provide a more general definition of CARMA processes in terms of the Levy process. We used a sampled process in equally space to estimate the parameters of the underlying continuous-time processes. The non-decreasing property of the driving Lévy process and the non-negativity of the corresponding discrete-time increments permits and an efficiency estimation procedure.

2.2 Affine term structure

In an ATS model, the interest rates and some derivatives at any point in time are time invariant. This model has flexible structure for controlling the dynamics of default risk free bonds [5]. ATS model starts from the assumption that there are no arbitrage opportunities in financial markets and implies the existence of a strictly positive stochastic process.

Definition 2.2

If the term structure has the form

| (2.8) |

where

| (2.9) |

and A,B are deterministic functions, then the model is said to possess an ATS. The function A and B are two real variables function of t and T but conceptually it is easier to think of A and B as being functions of t, while T serves as a parameter.

It turns out that the existence of an ATS is extremely pleasing from an analytical and a computational point of view. So we are interested to understand when such a structure appears.

2.3 Credit default swap

CDS is a derivative which the documentation identifies reference entity or reference obligation. The reference entity is the issuer of the debt

instrument and can be a corporation, a sovereign government or a bank load. When there is a reference entity, the party to the CDS has an option to

deliver one of the issuer’s obligation subject to pre-specified constraints [2].

In a single name CDS, B agrees to pay the default payment to A if a default has happened. If there is no default of the reference security until the

maturity of the default swap, counter party B pays nothing. A pays a fee for the default protection and the fee can be either a regular fee at interval

until default. If a default occurs between two fee payment dates, A still has to pay the fraction of the next fee payment that has occurs until the

time of default.

A premium leg (PL) of a CDS contract is a constant premium (the CDS spread) which has to be paid by the protection buyer at the maturity of the

contract. The opposed default leg (DL) which is the credit event that occurs before maturity has to be reduced by the protection seller, otherwise

there is no payment due. The fair payment is calculated by the following formula.

| (2.10) |

where is the present value, the conditional expected value with respect to measure which is the market information available up to time and also is the premium process which is starting at time with maturity . There are several models that deal with CDS to explore the intensity and survival probability such as structural and reduced form models and both of them are used to model credit risk.

Definition 2.3

(Default time). The default time is a random time representing the time of the credit event of the reference entity. It’s corresponding default process which is denoted by .

We assume that for every , where denotes the filtration representing the default-free, information and denotes the natural filtration of the default process , representing the defaultable, obligor-specific information. Therefore, is econompassing all default-free and defaultable information available to market participants up to time . As usual, we assume that satisfies the conditions of right continuity and completeness. Note that is a stopping time with respect to and consequently to , but not with respect to .

Definition 2.4

Let be a filtered probability space. The -algebra on generated by all sets of the form , , and is said to be predictable -algebra for the filtration .

Definition 2.5

A real-valued process is called with respect to filtration , or -predictable, if as a mapping from it is measurable with respect to the predictable algebra generated by this filtration.

Proposition 2.3

Every predictable process is progressively measurable.

Definition 2.6

A process is called intensity process of default rate of , if it is an -progressive

process with the following properties for every

(i)

(ii) a.s

(iii) for , the conditional survival probability is given by

| (2.11) |

In the content of CDS, we apply Key Lemma in [4] to satisfy PL and DL.

Lemma 2.4

(Key Lemma). Let be an -measurable random variable and

an

-predictable (bounded) process. Then

(i) for all , we have

| (2.12) |

(ii) For all , we have

| (2.13) |

Proposition 2.5

CDS is fair default if

| (2.14) |

and

| (2.15) |

where is the premium, discount factor, the default time and is a stochastic recovery rate function.

3 Affine term structure of CARMA model

ATS model is often used to give an account of any arbitrage-free model in which bond yields are affine functions of some state vector . Affine models are a special class of term structure models, which yield of a -period bond as for coefficients and that depend on maturity . The functions and make these yield equations consistent with each other for different values of and the state dynamics. The main advantage of affine models is to have tractable solutions for bond yields which are used because otherwise they are costly computed. The functional form of bond yields is obtained from computing risk-adjusted expectations of future short rates. Now by the following proposition we show that the Lévy-driven CARMA process is ATS.

Proposition 3.1

ATS of the Lévy-driven CARMA process by the dynamic is

| (3.1) |

where

| (3.2) |

and

| (3.3) |

where the matrix and the vector are introduced in subsection 2.1.

Proof: The ATS systems of equations of CARMA models are

| (3.4) |

and

| (3.5) |

with initial values and . For fixed , the system (3.4) is a simple linear first order differential equation, so we get to the equation in (3.3). To verify the correctness, we observe that and by replacing it in (3.4) we have

Now we find and for this, we get integral from (3.5) as

Therefore

and by replacing the equation we get to equation (3.2). So we can write the CARMA model as an ATS model.

4 Premium leg under stochastic recovery rate

Many companies try to reduce the risks that they encounter daily. So it is important to decrease the risk of large losses and to increase a financial

firm’s resilience. One factor that determines the extent of losses is the recovery rate on loans and bonds that are in default. Financial companies and

researchers commonly assume that the recovery rate is constant but in

practice actual recovery rates vary with respect to time. This assumption is important because additional risk is introduced when the recovery rate is

not

constant. We develop the credit risk models by considering the stochastic recovery rate in the purpose of profitably pricing the CDS premium leg.

Before studying the CDSP-SRR model we give a description of CDSP-CRR model.

The constant recovery rate of a reference entity is the fraction of the notional debt outstanding by the reference entity and is to be recoverable

after the default event. The constant parameter is denoted by which is between 0 and 1.

In CDS contracts one fixes this parameter with respect to amount of contract.

The loss compensation payment of amounts is . By denoting the random time of the credit event and the random cash flows of the swap legs’

the CDS price is provided [10]. Since the parameters in real market are stochastic, they affect on each other and estimate by a variety of

conditions. It is essential to be aware of the feature of the parameters and try to choose them in the right way.

Now we assume that the recovery rate is stochastic and depends on the default intensity and then find a model for it. This should fulfill

three necessary properties.

First, the domain of the stochastic recovery rate is on . The second crucial condition is, in order to ensure a negative correlation of

default probabilities with recovery rates, we need to use a function that has a negative or non-positive first derivative. It is known that realized

recovery

rates are negatively related to aggregate default rates. Therefore, we impose the same condition on implied recovery rates. So we have which is between 0 and 1. A convenient possibility is an exponential function where by considering the above

properties we have .

Now by these assumptions we present an intensity based representation of CDSP-SRR model and then find an innovative model for CDS default leg.

Proposition 4.1

Let r be the short rate and its corresponding discount factor be -predictable then the fair CDS default has the following intensity-based expression

| (4.1) |

Proof: By applying Lemma 2.4 and using the result of Bielecki et al. [4] we have

Therefore, equating both present values in the above equation we get to the result.

Proposition 4.2

(Credit triangle) We assume that the continuously paid premium is not fixed at the starting date and it is time-varying during the contractual tenor , named floating premium. Then the CDS default is equal for all tenors T flat spread, and

| (4.2) |

where the stochastic recovery rate is .

Observations are made on a daily basis, however punctual gaps may occur in our data, so for , we model the log-returns of the CDS premia equivalently to the log-returns of the default rate process by the followings

| (4.3) |

therefore

| (4.4) |

where is the Lévy-driven CARMA process as the log-return which is described in Section 2.

5 Simulation Study and Real Data

In this section, the CARMA processes with different orders are simulated. We show that how to simulate the CARMA. We explain the schematic representation of the model by compound Poisson process with normal distributed jumps in subsection 5.1. In subsection 5.2, we use a real data from entity companies (242 firms) to compare the CDSP-CRR model and the introduced CDSP-SRR model. In this case we apply the log-likelihood and BIC for comparing these models.

5.1 Simulation

We evaluate the performance of CDSP-SRR by using CAR(1), CAR(2) and CARMA(2,1) processes. We

modify the Yuima package [16] corresponding to the presented models and describe the required steps as the following.

1. As a default in function a continuous process is sampled at equally spaced time instants where is the

number of observations and is the step length. In this case, , and daily time is required. We set an initial value for the parameters

of CARMA model processes. Also, we use moving averages of length 5 to handle the missing data.

2. In the introduced model, we are to estimate the parameters that govern the implied recovery rate in this step. For the model with stochastic

recovery rate, we estimate the parameters and while for the model with constant recovery rate just we set

as a constant parameter. The Markov Chain Mont Carlo method allows a straight forward calculation of confidence interval, to

determine credible intervals for parameters.

3. We use quasi-maximum likelihood estimation method for estimating the parameters of the CARMA model. The arguments in the function provide

the new function with estimated Lévy increments.

4. Finally we compare BIC of the CDSP-CRR and the CDSP-SRR models to select the suitable model for CDS premia. We implement the simulation technique

through the following simulation example and show the results in the Tables 1 and 2.

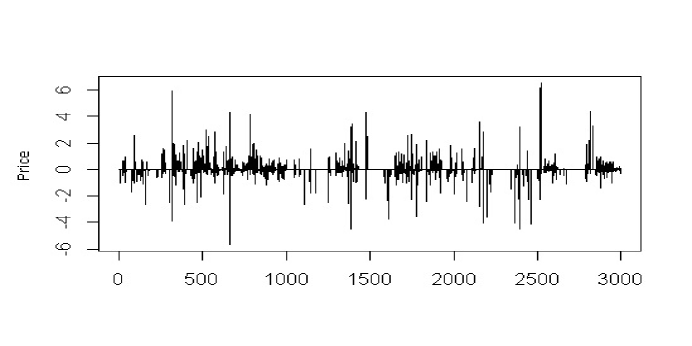

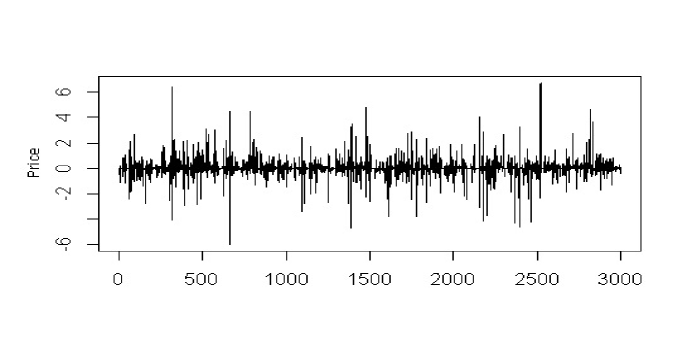

Following the simulation steps we illustrate the CARMA(2,1) processes under CDSP-CRR and CDSP-SRR models in Figures 1 and 2. It is shown that

the CDSP-SRR model because of the time-varying recovery rate has more fluctuation than the others.

Example 5.1

We simulate the sample path of CAR(1) with coefficients as . We choose , and . The simulations of the CDSP-CRR and CDSP-SRR models are plotted in Figures 1 and 2 and the results in comparing them are recorded in Table 1.

| Model | BIC | log-likelihood |

|---|---|---|

| CDSP-SRR | 2123.2826 | -1033.6413 |

| CDSP-CRR | 4562.5487 | -2269.2648 |

Example 5.2

According to the simulation, we generate a set of sample path of

CARMA(2,1) with parameters , ,

and . The corresponding stochastic differential equation of the process is

We choose appropriate , and . Then, we generate the data based on CDSP-CRR and CDSP-SRR models

which are defined in (4.4). The results of BIC and log-likelihood values are recorded in Table 2.

| Model | BIC | log-likelihood |

|---|---|---|

| CDSP-SRR | 4801.2438 | -2380.6068 |

| CDSP-CRR | 8740.4511 | -4350.2096 |

These differences can affect the price of the CDS premia in a real market and all companies are affected by the stochastic recovery rate.

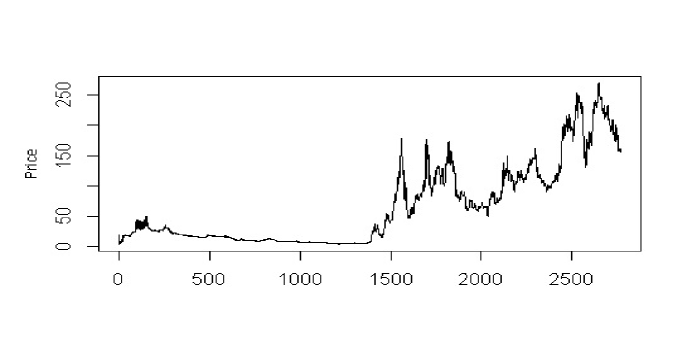

5.2 Real Data

To compare the performance of the proposed model, we consider 5-years CDS spread (T=5) observed daily between January 2002 until November 2012 (2829

trading days) for N=242 firms. The reference entities are from European and North American companies including different sectors such as Banks,

Electric power and other financial companies. For any company we have different staring dates and ending date by maturity time

with uniform step size .

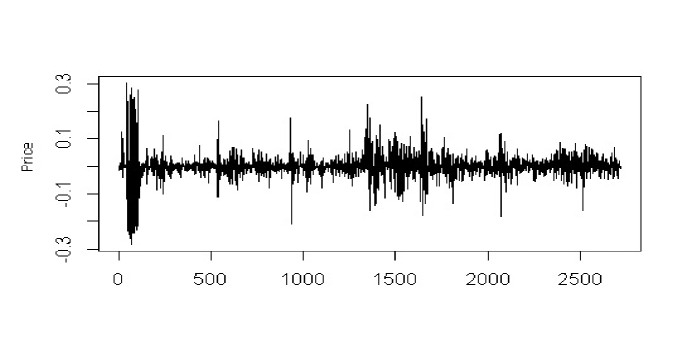

Our model is based on the observed (one-period) log-returns denoting the discrete-time observations defined by (4.4). Figures 1 and 2 reveal that

the ING bank of the real data, clarifies the effects of CDSP-SRR model. By applying the CDSP-CRR and CDSP-SRR models to every credit entity of CDS we

fit CARMA models to data and then estimate the parameters. Also, we compare some of the companies in terms of the BIC in Table 3. In this table, we show that the CDSP-SRR model has smaller BIC either than the CDSP-CRR model.

| Companies | CDSP-SRR model | CDSP-CRR model |

|---|---|---|

| AMERICANEXPRESS | -10137.9672 | -9228.8668 |

| BMW | -11448.7974 | -10104.0573 |

| SANO | -12684.5042 | -11175.8189 |

| KPN | -12889.6028 | -11596.5878 |

| DAIMLER | -11892.0160 | -10742.6483 |

| ING | -8114.2239 | -7088.9918 |

| DEUTSCHE | -11218.7720 | -9945.8812 |

| CONOCO PHILLIPS | -11113.9200 | -9626.3721 |

| WAL-MART | -10856.7632 | -9825.9177 |

| MCDONALDS | -11676.4504 | -10211.3201 |

| COMCAST | -5211.7253 | -4661.1184 |

Conclusion

To modeling the financial time series data such as CDS spread, we review the introduced model and generalized it. Considering the fact that the recovery rate of a CDS is not constant, we improve this model by considering the stochastic recovery rate. This assumption makes a better and more flexible model than the previous one. A continuous-time ARMA process driven by Lévy which is stationary is used to fit the premium of a CDS. According to the log-likelihood value and BIC, we get the results that CDS-SRR model has better performance for NIG distribution of the jumps. The empirical studies of this paper is based on the CDS spread of some companies use CAR(1), CAR(2) and CARMA(2,1). However, there are several limitations in the model, besides estimation of the CARMA model, the results are better and it can be better if we set the real plausible amount of recovery rate in our model. Also, by changing the structure of the stochastic recovery rate we can improve the efficiency of the model.

References

- [1] E. Altman (2006) Default Recovery Rates and Log in Credit Risk Modeling and Practice: an Updated Review of the Literature and Empirical Evidence, The oxford handbook of credit derivation.

- [2] M.J.P. Anson, F.J. Fabozzi, M. Choudhry, and Ren-Raw Chen (2004) Credit Derivatives: Instruments, Applications, and Pricing, WILEY.

- [3] G. Bakshi, D. Madan, F. Zhang (2001) Understanding the Role of Recovery in Default Risk Models: Empricial Comparisons and Implied Recovery Rates, SSRN Electronic Journal, DOI: 10.2139/ssrn.285940.

- [4] T.R. Bielechi, M. Rutkowski (2002) Credit Risk: Modeling, Valuation and Hedging , Springer, Berlin.

- [5] T. Bjork (2009) Arbitrage Theory in Continuous-Time, Oxford University Press.

- [6] P.J. Brockwell, R.A. Davis (2000) Introuduction of Time Series and Forecasting , Springer.

- [7] P.J. Brockwell, R.A. Davis, Y. Yang (2011) Estimation for Non-negative Lévy-driven CARMA Processes, J. Business snd Economic statistics, 29, 250-259.

- [8] P.J. Brockwell, V. Ferrazzano, C. Kluppelberg (2013) High-frequency Sampling and Kernel Estimation for Continuous-time Moving Average Processes, Journal of Time Series Analysis, 34, DOI: 10.1111/jtsa.12022.

- [9] D. Duffie (2005) Credit Risk Modeling with Affine Process, Journal of Banking Finance, 29, 2751-2802.

- [10] M. Eifert (2015) Time Series Models For Credit Default Swap Premiums , Journal of Credit Risk, 3, 21-44.

- [11] J. Hull, and A. White (2003) The Valuation of Credit Default Swap Options , Journal of derivations, 10, 40 -50.

- [12] M. Jakovelev (2007) Determinats of Credit Default Swap Spread:Evidence from European Credit Drivatives Market, Lappenranta University of Technology, Thesis.

- [13] M. Jaskowaki, M. McAleer (2011) Estimation of Implied Recovary Rates.A Case Study of the CDS Spread Market, Vienna University of Ecoomics and Business.

- [14] R.A. Jarrow, D. Lando, S. Turnbull (1997) A Markove Chain Model for the Term Structure of Credit Risk Spread, Rev. Financ. Stud., 10,2, 481-523.

- [15] CH. Kitwiwattanachai (2012) The Stochastic Recovery Rate in CDS: Empirical Test and Model, Working paper.

- [16] S. M. Iacus, L. Mercuri (2015) Implementation of Levy CARMA Model in Yuima Package, Computational Statistics, 30,4, 1111-1141.

- [17] E. Schlemm, R. Stelzer (2012) Quasi Maximum Likelihood Estimation for Strongly Mixing State Space Models and Multivariate Lévy-driven CARMA Processes, Electron J stat, 6, 2185-2234.

- [18] H. Tomasson (2015) Some Computationall Aspects of Gaussian CARMA Modelling, Journal stochastic comptational, 25, 375 -387.

- [19] Ph.D. Tuan (1997) Estimation of Parameters of Continuous-time Gausian Stationary Process with Rational Spectral Density Function., Biometrika, 64, 385-399.

- [20] D. Wemanhove (2009) Credit Default Swap Spread Model: Descriptive, Insight in the Determinants if CDS Spread, University of Twente, Thesis.

- [21] S.M Iacus, N. Yoshida (2017) Simulation and Inference for Stochastic Processes with YUIMA, Springer, https://cran.r-project.org/web/packages/yuima/index.html.