Parametric Inference for Discretely Observed Subordinate Diffusions111This research was supported by Hong Kong Research Grant Council GRF Grant No. 14205816.

Abstract

Subordinate diffusions are constructed by time changing diffusion processes with an independent Lévy subordinator. This is a rich family of Markovian jump processes which exhibit a variety of jump behavior and have found many applications. This paper studies parametric inference of discretely observed ergodic subordinate diffusions. We solve the identifiability problem for these processes using spectral theory and propose a two-step estimation procedure based on estimating functions. In the first step, we use an estimating function that only involves diffusion parameters. In the second step, a martingale estimating function based on eigenvalues and eigenfunctions of the subordinate diffusion is used to estimate the parameters of the Lévy subordinator and the problem of how to choose the weighting matrix is solved. When the eigenpairs do not have analytical expressions, we apply the constant perturbation method with high order corrections to calculate them numerically and the martingale estimating function can be computed efficiently. Consistency and asymptotic normality of our estimator are established considering the effect of numerical approximation. Through numerical examples, we show that our method is both computationally and statistically efficient. A subordinate diffusion model for VIX (CBOE volatility index) is developed which provides good fit to the data.

Keywords: diffusions, time change, subordinate diffusions, estimating functions,

eigenfunctions.

1 Introduction

Diffusion processes have been widely used in applications, and statistical inference for them have been extensively studied. We refer readers to, for example, Kutoyants (2004), Sørensen (2004), Aït-Sahalia et al. (2010), Bibby et al. (2010a) and Kessler et al. (2012) for survey of various techniques in the literature. However, there are also many applications, especially in finance and economics, in which diffusion models are not adequate to describe the data due to the presence of jumps. See for example, Aït-Sahalia and Jacod (2009b), Aït-Sahalia and Jacod (2009a), Aït-Sahalia and Jacod (2011), Aït-Sahalia et al. (2012), Todorov and Tauchen (2010), Todorov and Tauchen (2011) for various non-parametric methods to test existence of jumps and evidence for jumps in important applications.

A useful way to construct Markovian jump processes is to apply Bochner’s subordination to diffusion processes. This classical technique, originally introduced in Bochner (1949) in the semigroup context, corresponds to a stochastic time change using an independent nonnegative Lévy process (a.k.a., Lévy subordinator) as the random clock (a detailed account of Bochner’s subordination can be found in Schilling et al. (2012), Chapter 13). Let be a time-homogeneous diffusion, and be a Lévy subordinator, independent of . The time changed process is called subordinate diffusion, and it is Markovian and time-homogeneous due to the the independent increment and stationary increment property of the Lévy subordinator, respectively. Since generally jumps, jumps are created in . Depending on whether has drift or not, is a jump-diffusion or a pure jump process. Jumps of are in general state-dependent and could exhibit a variety of interesting behavior, making the time-changed process an appropriate model in many applications. For example, if is a mean-reverting diffusion, then jumps of are mean-reverting as well (see Li and Linetsky (2014)), and if moves in a finite interval, then does not jump outside the same interval. In addition, jumps of could have finite or infinite activity and finite or infinite variation. Some recent high-frequency non-parametric statistical analysis shows that some financial variables follow a pure jump process with infinite jump activity and infinite jump variation (see e.g., Todorov and Tauchen (2011)) and subordinate diffusions provide natural parametric candidates for modeling them. Successful applications of subordinate diffusions have already been found in finance. See for example, Mendoza-Arriaga et al. (2010); Li and Linetsky (2014); Li et al. (2017) and the discussions in Li et al. (2016); Li and Linetsky (2013, 2015). But these references focus on option pricing. In the special case where is a Brownian motion, is a Lévy process (Cont and Tankov (2004), Section 4.4) and hence one can view subordinate diffusions as a natural generalization of many Lévy processes by time changing more general diffusions.

This paper considers parametric inference for discretely observed ergodic subordinate diffusions, which has not been studied in the literature. Here only the value of the time-changed process is observed at a discrete set of times, and both the diffusion and the Lévy subordinator cannot be observed. This setting fits the applications we have in mind. For example, in Li and Linetsky (2014), the subordinate Ornstein-Uhlenbeck process is used to model the commodity spot price, which is the only quantity that can be observed in practice. Our aim is to develop an estimation method that is both computationally and statistically efficient, and it is applicable for a general class of and . We develop a two-step estimation procedure based on estimating functions that meets all these requirements. As an application, we show that a subordinate diffusion provides good fit to the historical data of VIX (CBOE Volatility Index). VIX is commonly regarded as the market’s fear gauge and there are many actively traded derivatives written on VIX, which are very important investment and hedging tools (see the review in Li et al. (2017)). To fit the VIX data, diffusion models are proposed in Goard and Mazur (2013). We show that our subordinate diffusion model which contains jumps performs significantly better. In the rest of the introduction, we provide key background information for subordinate diffusions and discuss issues involved and related literature.

1.1 Subordinate Diffusions

Consider a diffusion process living on an interval with end-point and (). We denote its drift and diffusion coefficient by and , respectively, and its infinitesimal generator by , which is an operator defined on a dense subset of , where is the stationary density of (see (1.1)). The following assumption on is made in this paper.

Assumption 1.

(1) is ergodic with stationary density

| (1.1) |

Here is the speed density of .

(2) The spectrum of is purely discrete.

(3) and are twice continuously differentiable and on any interval .

Sufficient conditions for a diffusion to satisfy Assumption 1 (1) can be found in Kessler and Sørensen (1999), Condition 4.1. The purely discrete spectrum assumption holds for many ergodic diffusions used in applications, with well-known examples including the Ornstein-Uhlenbeck process, Feller’s square-root process and the Jacobi process. Linetsky (2008), Theorem 3.2 provide conditions that imply purely discrete spectrum for diffusions (see also Hansen et al. (1998)). Assumption 1 (3) is a technical condition that is needed in solving the identification problem for subordinate diffusions. Under Assumption 1, if , then must be a reflecting boundary, otherwise it is inaccessible. The same conclusion holds for .

Next consider a Lévy subordinator , which is a nonnegative Lévy process and assume that it is independent of . Its Laplace transform is given by the well-known Lévy-Khintchine formula (e.g., Cont and Tankov (2004), Eq.(4.5))

| (1.2) |

where is the drift of and is called the Lévy measure with . The function is known as the Laplace exponent in the literature. A commonly used class of Lévy subordinators is the tempered stable family, in which

| (1.3) |

When , the subordinator is the inverse Gaussian process (Barndorff-Nielsen ), a popular choice in finance. For tempered stable subordinators,

| (1.4) |

where is the gamma function.

A subordinate diffusion is defined as . In general, is a jump-diffusion or a pure jump process depending on whether is positive or zero. Denote the infinitesimal generator of the subordinate diffusion by . Then using the Phillips theorem (Schilling et al. (2012), Theorem 13.6), one can show that , and for (a fully rigorous proof is given in Li et al. (2016), Theorem 4.2),

| (1.5) |

where for and ,

| (1.6) | |||

| (1.7) | |||

| (1.8) |

Here is the transition density of diffusion and we extend the definition of to by defining . It can be proved that is a Lévy-type measure, i.e., . The jump intensity is clearly state dependent in general and could exhibit a variety of interesting behavior, making subordinate diffusions good candidates for jump modeling.

Let be the -th eigenvalue of the diffusion generator and is the associated eigenfunction, i.e., . Under Assumption 1, purely discreteness of the spectrum also implies that all eigenvalues are simple (Linetsky (2008), Theorem 3.2), so we have . Let be the transition operator of , i.e., and is defined on . Then the spectrum of is also discrete and ( and share the same set of eigenfunctions). We normalize such that , where is the diffusion stationary density defined in (1.1). We also have for , that is, different eigenfunctions are orthogonal w.r.t. . The set of eigenfunctions forms an orthonormal basis of .

A key observation that will be used in developing the estimation method is that for , the spectrum of its generator (defined on a dense subset of ) and its transition operator (defined on ) are also purely discrete, and

| (1.9) |

This equation shows that subordination preserves the set of eigenfunctions and only changes the eigenvalues using the Laplace exponent of the subordinator. The proof of this fact can be found in Linetsky (2008), p.283. Let be the transition density of . Li and Linetsky (2015), Proposition 2.4 shows that, under the condition , if either or when , is bounded on any compact set of for all and , then admits the following bilinear eigenfunction expansion which converges uniformly on compacts for and :

| (1.10) |

Lemma 2.1 in Section 2 shows that under Assumption 1, is ergodic and converges to as . As for , , we have as . Subsequently, we must also have

| (1.11) |

for to converge to .

1.2 Issues and Related Literature

The first issue we need to address is identifiability of subordinate diffusions. In general, one cannot hope to identify and uniquely given only the data of (an example is given in Section 2). Using spectral theory, we show that the characteristics of the diffusion and the subordinator can be identified up to scale. This implies that to estimate the parameters of , the scale needs to be fixed first, but the law of does not change when the scale varies.

The transition density is given by (1.10). In general, and are unknown so the method of maximum likelihood estimation cannot be applied. Even when explicit expressions are available for them, computing the expansion for can be demanding especially when the time step between two observations is small. For example, when is the subordinate Ornstein-Uhlenbeck process (Li and Linetsky (2014)), and are known, but in our numerical experiment it could take several thousand or even over 10,000 terms for the partial sum in (1.10) to converge to an acceptable level of accuracy when is one day. In financial applications, typically daily or even higher frequency data is used.

We propose an estimation method for subordinate diffusions based on estimating functions. An overview of the estimating function approach for diffusions can be found in Sørensen (1997), Bibby et al. (2010b). It is shown that this is a statistically efficient method for diffusions if the estimating functions are appropriately chosen. In particular, when analytical expressions for and are available, Kessler and Sørensen (1999) (hereafter KS) propose to construct martingale estimating functions based on the eigenfunctions and they work well in applications (see Larsen and Sørensen (2007) for the application of this method to estimate the dynamics of exchange rates in a target zone). For subordinate diffusions, if we have analytical formulas for and , we can directly apply the KS idea to construct martingale estimating functions based on (1.9), but compared to estimating , has more parameters so computation takes longer time. When and do not have analytical expressions, since there exist numerical algorithms for the Sturm-Liouville problem that can achieve high level of accuracy, we can compute and numerically. If the KS approach were followed, numerical computation of and is needed in every iteration (note that the estimator is found by solving an equation through iterations), which is time-consuming.

This observation leads us to propose a two-step procedure that is computationally much more efficient. In Step 1, we use estimating functions proposed in Conley et al. (1997) to estimate diffusion parameters (up to scale). Conley et al. (1997) considers how to estimate the parameters of a diffusion under random sampling (but they do not estimate the parameters associated with the random sampling scheme). They propose estimating functions that only involve diffusion parameters using the randomly sampled data. Since deterministically sampled data of a subordinate diffusion can be viewed as randomly sampled data of the background diffusion, we can apply their estimating functions, and the estimator can be computed fast. In Step 2, we estimate the subordinator parameters using the eigenfunction-based estimating function , where is the data for , is the vector of subordinator parameters and is a column vector with the same length as . Since the diffusion parameters have been estimated in Step 1, all and are determined and do not change in iterations to find the estimator . How to choose is important for the method’s statistical efficiency. We can set according to the “optimal weight” formula in Kessler and Sørensen (1999) (hereafter KS weight). If the diffusion parameters estimated in Step 1 are the true values, the KS weight is optimal in the sense that the covariance matrix for is minimized. Since diffusion parameters are estimated and thus contain errors, the KS weight is not optimal. In this paper we obtain the formula for the optimal weight, which is nevertheless difficult to compute. In our simulation study, we numerically compare the standard error for under the optimal weight and the KS weight. We find that the results are very close. Given the ease of calculating the KS weight, we use it in our method instead of the optimal one. The idea of combining different types of estimating functions is also used in Bibby and Sørensen (2001) for estimating a discretely observed diffusion with a high-dimensional parameter. There, simple estimating functions proposed by Kessler (2000) and martingale estimating functions developed in Bibby and Sørensen (1995) are combined to simplify the estimation procedure.

Methodologically, our paper improves Kessler and Sørensen (1999) and Bibby and Sørensen (2001) in the following aspects.

-

(1)

Kessler and Sørensen (1999) only considers the situation where eigenvalues and eigenfunctions are analytically known. We deal with the general case with unknown eigenvalues and eigenfunctions, and show how to calculate the eigenfunction-based martingale estimating function numerically in an efficient way. We also develop consistency and asymptotic normality results considering the effect of numerical approximation. These results are not directly implied by the existing asymptotic theory for estimating functions which assumes that they can be computed exactly.

-

(2)

Bibby and Sørensen (2001) did not address the issue of obtaining the optimal weighting matrix for the martingale estimating function when it is combined with other estimating functions. We solved this problem in our context.

The present work is related to a growing literature on estimating time-changed Lévy processes, which are also constructed by time change and are very popular in modeling asset prices (see Carr and Wu (2004)). A time-changed Lévy process is constructed as , where is a Lévy process with Lévy measure and . Such time change is absolutely continuous, and the process is often called the activity rate process, which is used to introduce stochastic volatility into the Lévy model. We do not attempt to survey the rather extensive literature on the estimation of time-changed Lévy processes, but instead mention a few works. See, e.g., Figueroa-López (2009, 2011), Belomestny (2011) for non-parametric estimation of , and Bull (2014) for inference of , among other works. Subordinate diffusions and time-changed Lévy processes are constructed using different background processes (diffusions for the former and Lévy processes for the latter) and different time changes (Lévy subordinators are used as the time change for the former, which are not absolutely continuous). Thus, subordinate diffusions generally do not belong to the class of time-changed Lévy processes. In addition, subordinate diffusions exhibit richer jump behavior than time-changed Lévy processes because they could have state-dependent jumps (the compensator of the random jump measure of is ; see the expression for in (1.8)), while jumps in time-changed Lévy processes are state-independent (the compensator of the random jump measure of is , which is independent of ). Unlike time-changed Lévy processes, which have stochastic volatility and can generate the volatility clustering phenomenon, subordinate diffusions do not possess such a feature. To incorporate it, one can further time change a subordinate diffusion by an absolutely continuous process in the form of (see Li and Linetsky (2014)). How to estimate these time-changed subordinate diffusions is an interesting problem for future research.

1.3 Organization of the Paper

The rest of the paper is organized as follows. Section 2 solves the identification problem for subordinate diffusions. In Section 3, we present the two-step procedure to estimate subordinate diffusions by first assuming that and are known and derive the optimal weight for the eigenfunction-based martingale estimating function. We then consider the general situation in which and are unknown and we show how to obtain the estimator using the numerical approximation of and . In Section 4, we develop asymptotic analysis of our estimators considering the effect of numerical approximations. Under regularity conditions, we show that our estimator is consistent and asymptotically normal. Section 5 contains various numerical examples and an application to VIX data. Proofs are collected in the appendix except those in Section 4. Section 6 provides a summary and discusses future research.

To conclude the introduction, we fix some notations. ′ denotes the transpose of a vector or a matrix. For a vector function and a parameter , is a matrix with element . In particular, when is a scalar function, is a row vector.

2 Identifiability of Subordinate Diffusions

Since we are only given the data of , it is expected that and cannot be uniquely identified. Below we present an example.

Example 1.

Let be an Ornstein-Uhlenbeck (OU) diffusion, i.e.,

| (2.1) |

with . Its stationary density is given by

| (2.2) |

It is well known that for the OU process (Karlin and Taylor (1981)),

| (2.3) |

where is the Hermite polynomial of order , and satisfies .

Let be an inverse Gaussian subordinator with drift . Its Lévy measure is given by with , , and . We call an IG-SubOU process for short.

Let . For the Lévy measure of , define

| (2.4) |

We call the characteristics triplet of . Example 1 already shows that in the case of IG-SubOU process, given a characteristics triplet, appropriate scaling does not alter the law of the process. This observation holds more generally provided that we have the bilinear eigenfunction expansion for . Furthermore, using spectral theory, we show that given two characteristics triplets, that they yield the same transition probability density implies that they are related by appropriate scaling. We need the following lemma on the ergodicity of subordinate diffusions, which will also be used in proving consistency of our estimator.

Lemma 2.1.

Theorem 2.1.

Consider two characteristics triplet () and denote the corresponding transition probability density by . Under Assumption 1, and are identical implies that there exists a constant such that

| (2.5) |

where is the -th eigenvalue of the generator of the diffusion with characteristic . Now, suppose that (2.5) holds for some constant . Under Assumption 1 and the condition , if either or when , is bounded on any compact set of for all and , then and are identical.

For a given subordinator, using the explicit form of its Lévy measure, we can simplify the condition to obtain explicit conditions on the parameters of the subordinator. Below we consider the important class of tempered stable subordinators.

Corollary 2.1.

The result in Example 1 for the IG-SubOU process becomes a special case of Corollary 2.1 with . Theorem 2.1 implies that, to estimate the parameters of a subordinate diffusion, a scale needs to be fixed first. In Example 1, we can, for example, fix and estimate the remaining parameters of the IG-SubOU process.

3 A Two-Step Estimation Procedure for Subordinate Diffusions

Let be a vector for the parameters of the diffusion and be a vector for the parameters of the subordinator . Put , which is a vector for the parameters of . The data of is given by with . In our estimation procedure, we use two estimating functions

| (3.1) |

where is a vector function, and

| (3.2) |

where is a vector function. We choose based on moment conditions developed in Conley et al. (1997) and is a martingale estimating function based on eigenfunctions. The estimation consists of two steps. In the first step, , the estimator of , is obtained by solving . Then, in the second step, we find , the estimator of , by solving . To simplify the notation, we will also write as below.

3.1 The Choice of Moment Conditions

Conley et al. (1997) estimates the parameters of a diffusion under random sampling. They assume that the random sampling process is increasing and independent of the underlying diffusion and has stationary increments. Under this assumption, two types of moment conditions are proposed. A deterministic sample of the subordinate diffusion can be viewed as a random sample of the diffusion . Furthermore, in our set-up, the random sampling process clearly satisfies the assumption in Conley et al. (1997). Hence we can adopt the following two types of moment conditions proposed there ( is the stationary distribution of with density and denotes taking expectation with initial distribution equal to )

| (3.3) |

and

| (3.4) |

where

| (3.5) |

The function satisfies that (1) for each , is bounded and continuous and for each , is bounded and continuous; (2) is bounded and continuous for all and is bounded and continuous for all . An efficient choice of test function in (3.3) is given by (see Hansen and Scheinkman (1995), Conley et al. (1997), Kessler (2000))

| (3.6) |

To construct the vector function in the estimating function (3.1), we select its components from the moment conditions (3.3) and (3.4).

We use () to construct . Recall that for each , , and using the tower law, , which holds for any initial distribution for process . We can combine these moment conditions together. Let be a vector function (), then

| (3.7) |

Note that we do not use in the moment condition due to (1.11). Let be a vector function with each element

| (3.8) |

and is a matrix. We put (recall that is the transpose of ). Then,

| (3.9) |

It is also easy to see that is a martingale. Such martingale estimating function based on eigenfunctions is first proposed by Kessler and Sørensen (1999) to estimate a discretely sampled diffusion with analytical expressions for the eigenvalues and the eigenfunctions. The choice of the weighting matrix is crucial for this method’s efficiency, which we discuss next.

3.2 The Choice of the Weighting Matrix

Let’s first assume that the diffusion parameter is known. Then, to determine the optimal weighting matrix in (3.9) in the sense of Godambe and Heyde (1987), we can follow Kessler and Sørensen (1999). Adapting Eq.(3.3) in Kessler and Sørensen (1999) to our setting, we obtain a weighting matrix which solves the following linear system (we denote the solution by and refer to it as the KS weight hereafter)

| (3.10) |

where is a matrix and is a matrix with

| (3.11) | ||||

| (3.12) | ||||

| (3.13) |

Since the diffusion parameters also need to be estimated, computed by (3.10) is not the true optimal weighting matrix.

Now we derive the optimal weighting matrix. We will make precise the meaning of being “optimal” below. First, we define one vector and two matrices. Let

| (3.16) | |||

| (3.21) | |||

| (3.26) |

To simplify the notation, we suppress the dependence on and in and . Assuming that and are invertible, can be represented as

| (3.27) |

In Section 4, under certain regularity conditions, we will prove that

| (3.28) |

where is the estimator for and is its true value, and

| (3.29) | ||||

| (3.34) |

with in evaluating all the matrices involved. From the asymptotic normality result, for fixed large sample size , we can approximate the covariance matrix of by . Note that the estimating function for the diffusion parameter is fixed, so the upper left block matrix in , which can be seen as the approximate covariance matrix for , is fixed. Our aim is to find the weighting matrix that minimizes the lower right block matrix in , the approximate covariance matrix for . The precise definition is given below. is the estimating function constructed using the weighting matrix in (3.2).

Definition 3.1.

Let be the collection of all possible weighting matrix. Define , , and . is optimal within if the lower right sub-matrix of is minimized, that is,

| (3.40) | |||

| (3.46) |

is positive semi-definite for all . Here all quantities without * correspond to using weighting matrix . We assume that is invertible for all .

Remark 3.1.

Our definition of the optimal weighting matrix is only concerned with the covariance matrix of . The true definition of optimality would be to look at the full covariance matrix. We have tried to derive the true optimal weighting matrix, but it is very difficult to obtain an expression for it. This is why we adopted the modified definition of optimality given in Definition 3.1. Such modification will not cause significant loss of statistical efficiency provided that the estimator is close to , the true value of . This is because the optimal weighting matrix derived under the modified definition would be asymptotically close to the true one.

While we can also apply weighting to all the moment conditions, including those for estimating , the derivation of the optimal weighting matrix would be even harder, and it will certainly require more computations to calculate it. For these reasons, we only consider weighting the eigenfunction-based estimating functions. The numerical examples in Section 5 show that our approach delivers good results.

We next provide an equivalent characterization of optimality.

Proposition 3.1.

is optimal if and only if

| (3.47) |

is a constant matrix for any where

In the following, refers to taking expectation with the stationary distribution as the initial distribution (for notational simplicity, we dropped in the subscript). Using (3.1) and (3.9), it is straightforward to obtain that

and

Now we simplify . refers to the information generated by the process up to time . First, note that for ,

| (3.48) | |||

| (3.49) |

Then,

| (3.50) |

Define

| (3.51) |

Then . The optimality condition for our problem is that

| (3.57) | ||||

| (3.58) |

is a constant matrix. (3.57) can be rewritten as , where

| (3.59) | ||||

| (3.60) | ||||

| (3.61) | ||||

| (3.62) |

Since (3.57) is a constant for all , we have where is a constant matrix. Since is arbitrary, we can set where is a constant matrix with each entry equal to 1 and is an arbitrary constant in . Then, we have

Differentiating with respect to on both sides of the above equation, we get for any . Thus, from (3.62),

| (3.63) |

Since and involve , the above equation is not an explicit expression for . However, since and do not depend on , is of the following form

| (3.64) | ||||

| (3.65) | ||||

| (3.66) |

where and are constant matrices. Note that the optimal weighting matrix is not unique because is still optimal for any . Here, we will try to find the general form of an optimal weighting matrix.

Proposition 3.2.

of form (3.64) is an optimal weight when and solve the following linear system.

| (3.67) |

where

| (3.68) | |||

| (3.69) | |||

| (3.70) | |||

| (3.71) | |||

| (3.72) |

In general, to compute to in closed-form is very difficult, even when analytical expressions for the eigenvalues and the eigenfunctions are available. To calculate them numerically also requires extensive computations. In Section 5, we numerically compute them in the problem of estimating the SubOU process. We then compare the standard error for each subordinator parameter using the optimal weighting matrix and the KS weighting matrix. The comparison reveals little difference between these two choices. Since the KS weighting matrix is much easier to compute, we will use it instead of the optimal one in our method.

3.3 Numerical Approximations

For estimating diffusions using eigenfunction based estimating functions, Kessler and Sørensen (1999) only considers the case in which explicit expressions for the eigenvalues and the eigenfunctions are available. In general, they are not known in closed-form.

In this paper, we apply an efficient numerical method to compute the eigenvalues and the eigenfunctions accurately for the Sturm-Liouville (SL) problem associated with the given diffusion. A particularly attractive class of methods for solving the SL problem numerically is the coefficient approximation method (see Pryce (1993)). Here, we use a particular type of coefficient approximation, known as constant perturbation method (CPM) with high-order corrections to achieve high-level of accuracy (see Ledoux et al. (2004); Ledoux and Van Daele (2010)). This method can handle a large class of SL problems even with discontinuity in the coefficients. It is implemented in a Matlab package called MATSLISE, which we directly use in our implementation. In general, the accuracy of eigenvalues and eigenfunctions deteriorates as their order increases. Fortunately, we do not need to use a large number of eigenpairs in the estimating function (3.9). Our numerical experiment in Section 5 shows that using only the first several eigenpairs suffices for statistical efficiency, which is in line with the finding of Kessler and Sørensen (1999) for estimating diffusions.

In our estimation procedure, we first estimate the diffusion parameters using estimating function (3.1). After they are obtained, we only need to run the CPM once to numerically calculate for from to , because they only depend on the diffusion parameters. By separating the estimation of diffusion and subordinator parameters, we avoid running the CPM multiple times and thus making the estimation procedure computationally more efficient.

To run the CPM, we specify a finite grid that covers a large enough region. The MATSLISE program returns approximations for the eigenvalues and for the eigenfunctions on the grid. To obtain an approximate value for an eigenfunction at a non-grid point, we use linear interpolation. Denote the -th approximated eigenpair as . Then, we approximate the original estimating function in (3.9) by the following

| (3.73) |

where and is the approximated KS weighting matrix which solves

Here,

which can be calculated analytically as we know the Laplace exponent in closed-form. is defined as in (3.12) by using the approximated eigenvalues and eigenfunctions. To evaluate , we need to calculate the integral

| (3.74) |

which is equivalent to pricing an European option with payoff function in a subordinate diffusion model. Recently, Li and Zhang (2016) developed an efficient algorithm for pricing European options in general subordinate diffusion models. Their method requires specifying a grid to discretize the state space. In our implementation, we use a uniform grid with step size , although non-uniform grids can be used in Li and Zhang’s method. We denote the approximation to using their method by and the resulting weighting matrix and the estimating function by and . In general, and can be different. Inaccuracy in the eigenpairs can cause significant loss of precision in the estimator. Therefore, in our implementation, we choose a fine for the CPM, which guarantees high level of accuracy in the eigenvalues and the eigenfunctions. does not need to be as fine as and we choose it to be a sub-grid of . The error of using to approximate the exact is dominated by the error in calculating the integral (3.74), which is by Li and Zhang (2017) (the approximation error for the eigenvalues and the eigenfunctions is at much higher order than because the CPM is used with high-order corrections). The error order for approximating (3.74) can be further improved using extrapolation as pointed out in Li and Zhang (2017). Using two rather coarse grids and , one can extrapolate the results from these two grids to reduce the error to . We first calculate and for on the grid . To obtain at non-grid points, we apply linear interpolation.

4 Consistency and Asymptotic Normality

The subordinate diffusion parameter space is denoted by , which is assumed to be an open subset of . is the true value of . Let , which is the joint density of under the true parameter value if the initial density is the stationary one. denotes taking expectation under the true parameter value . Recall the vector functions and in (3.1) and (3.2). Let , and . In our analysis, we consider an arbitrary weighting matrix for . The following assumption is imposed (similar assumptions are also made in Kessler and Sørensen (1999) and Sørensen (1999)).

Assumption 2.

and a neighbourhood B of in exists such that the following conditions hold.

(a) is continuously differentiable w.r.t. on B for all . is continuously differentiable w.r.t. and on B for all and .

(b) Each element of the first partial derivatives of w.r.t. , as well as each element of the first partial derivatives of w.r.t. are dominated for all by a function which is integrable w.r.t. .

(c) Each element of and is integrable w.r.t. for all , and square-integrable w.r.t. for .

(d) Let and . and are non-singular.

A function is locally dominated integrable w.r.t. if for each , there exists a neighborhood and a non-negative integrable function such that for all ; see Kessler et al. (2012), p.5.

Assumption 3.

(a) for all .

(b) Each element of and each element of are locally dominated integrable w.r.t. .

Remark 4.1.

When the weighting matrix is given by the KS one, it can be shown that is positive definite and hence non-singular as long as .

We next develop the Central Limit Theorem (CLT) for our estimating function. Since is not a martingale, to develop its CLT, we need the following property.

Proposition 4.1.

Under Assumption 1, the diffusion transition operator is a strong contraction for any , that is, there exists some such that for any such that ( denotes the norm). is also a strong contraction for any .

Proof.

For any , admits an eigenfunction expansion

| (4.1) |

From (1.11), , . So for such that , . Using the orthonormality of and that for , we obtain

| (4.2) |

Thus is a strong contraction. For , using the definition of subordination, for such that ,

| (4.3) | ||||

| (4.4) |

Here, is the distribution of . Since , is also a strong contraction. ∎

Now we can investigate the convergence of .

Proof.

Based on Proposition 4.2, we have the following consistency and asymptotic normality result by applying Theorem 1.2.2 of Sørensen (2012).

Theorem 4.1.

Under Assumption 1 and 2, an estimator exists with a probability tending to one as . Moreover,

and

where and (the invertibility of is guaranteed by Assumption 2 (d)). Moreover, under Assumption 3, the estimator is the unique -estimator on any bounded subset of containing with probability tending to 1 as .

Theorem 4.1 does not consider that generally cannot be computed exactly. Next, we take into consideration the effect of numerical approximations that are used in Section 3.3 to compute the weighting matrix in the KS way. In the following, is the Euclidean norm of vector , and for matrix , . Recall that is the step size of the grid . The computation of does not require discretization. For the estimator of , we write it as because it depends on the grid that is used. We put and let . Suppose that

| (4.11) | |||

| (4.12) |

for some , and , are continuous with respect to . In (4.11), without extrapolation and with extrapolation in view of the discussions in Section 3.3. As for , (4.11) implies that

| (4.13) |

In general, the step size depends on the number of observations , so we will write it as below whenever necessary. Our main result is that previous conclusions about consistency and asymptotic normality hold under suitable assumptions on the convergence of . We need the next two lemmas.

Lemma 4.1.

Proof.

Note that

| (4.14) | |||

| (4.15) | |||

| (4.16) |

Since is a compact set, the first term converges to almost surely by Lemma 1.2.3 in Sørensen (2012). As , the second term also converges to 0. ∎

Lemma 4.2.

Proof.

For any compact subset of , there exists a finite number such that for since is continuous. Then,

| (4.19) | |||

| (4.20) | |||

| (4.21) | |||

| (4.22) |

By the finite covering property of a compact set, the dominated integrability condition of Lemma 1.2.3 in Sørensen (2012) follows from the local dominated integrability of (Assumption 3 (b)) and the continuity of (Assumption 2 (a)). Applying this lemma shows the convergence of the first term. Obviously, the second term converges to . The second claim can be proved similarly. ∎

Theorem 4.2.

Under Assumption 1 and 2, and (4.11), (4.12), suppose that is continuously differentiable in a neighbourhood of in and . Then, an estimator exists with probability tending to 1 as and

on the set where they exist. Under Assumption 3, the estimator is the unique -estimator on any bounded subset of containing with probability tending to 1 as . Moreover, for large enough, almost surely on the set where they exist.

Proof.

We check the three conditions required for Theorem 1.10.2 in Sørensen (2012). Condition (i) follows from (4.17). Let be a compact subset of . (4.18) implies condition (ii). Condition (iii) is equivalent to Assumption 2 (d). Thus, applying this theorem shows the existence of a consistent estimator .

Now we prove the second statement. Let denote the closed ball with radius centered at . By Assumption 3 (a), for any bounded subset of containing , we have

| (4.23) |

for all . This, together with Lemma 4.2, implies that the conditions of Theorem 1.10.3 in Sørensen (2012) are satisfied. Thus, for any sequence of -estimator,

| (4.24) |

as for all . Let be an -estimator. Let where is a known consistent -estimator. Thus, is a consistent estimator by (4.24). Then, by Theorem 1.10.2 in Sørensen (2012), as which means is eventually unique on .

For the last part, due to the consistency of and , there exists a sequence satisfying and , where

| (4.25) |

Applying the mean value theorem to each element of (the -th element is denoted by ) on , we have

| (4.26) | ||||

| (4.27) |

where for some , and for ,

Theorem 4.3.

5 Numerical Examples

In this section, we consider the IG-SubOU process discussed in Example 1 with (the subordinator has no drift and hence is a pure jump process), which we will use to evaluate several important questions numerically in Section 5.1 to 5.4. This is a non-trivial process for which many quantities can be computed analytically. As an application of our method, we will construct a subordinate diffusion model to fit VIX data in Section 5.5.

For the IG-SubOU process, let and be the mean rate and variance rate of the inverse Gaussian subordinator, i.e., and . We use and instead of and to reparameterize the Lévy density of , because are easy to interpret. Under the new parametrization, . The parameters of the pure jump IG-SubOU process are . The eigenpairs of the OU process are given in (2.3), which have explicit expressions. The computation of is particularly simple and can be done via the following recursion

| (5.1) |

The true parameter values for are given by , , , and (the time unit is day). To estimate the parameters, we generate 2000 daily data by simulation (i.e., day).

From the scaling invariance pointed out in Corollary 2.1, we fix and only estimate . To estimate the diffusion parameter , we use the test function (3.6) in (3.3) (the stationary density of the OU process is given in (2.2)), and obtain two moment conditions

| (5.2) |

Using these moment conditions to construct estimating functions, we obtain the estimator for as follows (note that the value of is fixed in advance)

| (5.3) |

5.1 Comparison of the KS Weight and the Optimal Weight

We use estimating function based on eigenfunctions to estimate . To get the KS weight, we solve (3.10). For the IG-SubOU process, and can be obtained in closed-form. We have

| (5.4) | |||

| (5.5) |

Using

we obtain that

| (5.12) | ||||

| (5.13) |

To calculate the optimal weight, we need to solve the linear system in Proposition 3.2 to get and . We calculate to by Monte Carlo simulation with 20,000 replications. Note that the inner expectations in the expressions for to , , , and can all be computed in closed-form for the SubOU process (we do not show the formulas here to save space).

We next discuss how to calculate the standard error for the subordinator parameters and . If the KS weight is used, the covariance matrix for the estimator is approximately equal to (see Definition 3.1)

| (5.14) |

For the SubOU process, the formula for each matrix above except is shown on page 9. The expression inside each expectation is analytically known. The expectations are computed by Monte Carlo simulation with 200,000 replications. , where is defined in (3.51). For the SubOU process, each term inside the expectation for is known and the expectation is again computed by Monte Carlo simulation with 200,000 replications.

If the optimal weight is used, the covariance matrix for the estimator is approximately equal to (see Definition 3.1)

| (5.20) | |||

| (5.21) | |||

| (5.22) | |||

| (5.23) |

For the SubOU process, the above inner expectations can be computed in closed-form and the outer expectation is computed by Monte Carlo simulation with 200,000 replications.

We compare using the KS weight and the optimal weight in terms of the standard error for and when different numbers of eigenfunctions are used. The results are shown in Table 1. We clearly see that the standard errors are very close. Since the KS weight is much easier to compute, we recommend using the KS weight in our method, and it is used in all the following examples and applications.

| Number of eigenfunctions | SE for the KS weight | SE for the optimal weight | |

|---|---|---|---|

| 2 | 0.0546609 | 0.0546591 | |

| 3 | 0.0437687 | 0.0437683 | |

| 4 | 0.0434508 | 0.0434503 | |

| 5 | 0.0433678 | 0.0433673 | |

| 6 | 0.0432791 | 0.0432786 | |

| 2 | 1.7195609 | 1.7195110 | |

| 3 | 0.3333475 | 0.3333454 | |

| 4 | 0.1813183 | 0.1813178 | |

| 5 | 0.1682431 | 0.1682428 | |

| 6 | 0.1531301 | 0.1531295 |

5.2 How Many Eigenfunctions to Use

We examine the impact of the number of eigenfunctions used in the estimating function on the standard error of the subordinator parameter and . We also calculate the standard error under maximum likelihood estimation which is known to achieve the best statistical efficiency. Theorem 2.2 of Billingsley (1961b) shows that , where . To calculate , we use the bilinear eigenfunction expansion (1.10) for , which can be computed by truncating the infinite series when the relative accuracy level of is reached. To calculate the expectation for , we use Monte Carlo simulation with 200,000 replications.

Table 2 displays the standard error of for MLE and various number of eigenfunctions. As expected, MLE gives the smallest standard error, and as the number of eigenfunctions increases, the standard error for both and decrease to those under MLE. However, the marginal decrease in the standard error is quite small when the number of eigenfunctions is already at . In general, increasing the number of eigenfunctions reduces standard error but requires more computations to obtain the estimator. Using 4 eigenfunctions seems to best balance computational efficiency and statistical efficiency for the IG-SubOU process. Our finding is in line with those in Kessler and Sørensen (1999) and Larsen and Sørensen (2007), who estimate diffusions using eigenfunction-based estimating functions. For the diffusion models considered there, using a few number of eigenfunctions is already good enough.

| SE for | SE for | |

|---|---|---|

| MLE | 0.0430 | 0.1276 |

| 2 eigenfunctions | 0.0547 | 1.7196 |

| 3 eigenfunctions | 0.0438 | 0.3333 |

| 4 eigenfunctions | 0.0435 | 0.1813 |

| 5 eigenfunctions | 0.0434 | 0.1682 |

| 6 eigenfunctions | 0.0433 | 0.1531 |

| 7 eigenfunctions | 0.0432 | 0.1479 |

| 8 eigenfunctions | 0.0432 | 0.1430 |

5.3 The Effect of Numerical Approximation

In general, the eigenvalues and the eigenfunctions are not known explicitly, and numerical approximations are needed as discussed in Section 3.3. For the IG-SubOU, since we have explicit expressions for the eigenvalues and the eigenfunctions, we can check the error of using MATSLISE to numerically calculate them. We choose . The region is large enough for the OU process under the assumed parameter values. The absolute and relative error for the first four nonzero eigenvalues, as well as the maximum absolute error and maximum relative error for the first four nonconstant eigenfunctions on the grid are shown in Table 3. In general, as the order of the eigenpair increases, the CPM becomes less accurate, but if the order of the eigenpairs is not too high, we still attain very high level of accuracy.

| Eigenpair | Abs Error of Eigenvalue | Rel Error of Eigenvalue | Max Abs Error of Eigenfunction | Max Rel Error of Eigenfunction |

|---|---|---|---|---|

| 1 | 4.1284e-12 | 1.0321e-10 | 3.7068e-10 | 5.6797e-9 |

| 2 | 2.1349e-12 | 2.6687e-11 | 6.3483e-10 | 4.3054e-9 |

| 3 | 3.3295e-12 | 2.7746e-11 | 3.5525e-9 | 4.6452e-9 |

| 4 | 3.6774e-12 | 2.2984e-11 | 1.3555e-8 | 5.3099e-8 |

We also need to numerically calculate the integral (3.74) to get the KS weight. To do this, we specify two grids, and . For each grid, we run the Li and Zhang algorithm (Li and Zhang (2016)) to approximate (3.74) and then we extrapolate the results under the two grids to obtain a more accurate approximation. The estimation results for the two methods are listed in Table 4. Here to estimate the standard error, we simulate 100 trajectories with each containing 2000 daily observations to get 100 realizations for the estimator and calculate its sample standard deviation. From the table, we can see that both methods give almost identical results. Therefore, the numerical approximation proposed in Section 5 works very well.

| Exact Eigenpair ( (SE)) | Approx Eigenpair ( (SE)) | |

|---|---|---|

| 0.0426(0.0071) | 0.0426(0.0071) | |

| -0.0027(0.0336) | -0.0027(0.0336) | |

| 1.0033(0.0429) | 1.0034(0.0429) | |

| 0.5253(0.1840) | 0.5254(0.1840) |

5.4 The Impact of Data Frequency

We examine the impact of data frequency on the standard error of the estimator. Now we set the sampling time interval days but keep the same sampling period. Thus, there are 200,000 observations in the sampling period of 2000 days. The standard error of the estimator, which is again estimated from 100 simulated trajectories, is shown in Table 5. Increasing data frequency in the same sampling period has little impact on estimating , the long-run mean of the OU process. To reduce its standard error, the sampling period should be increased. Higher frequency of data does reduce the standard error of (the mean-reversion speed of the OU process), (mean rate of the subordinator) and (variance rate of the subordinator). In particular, by sampling 100 times faster, we achieve a reduction by around 50% in the standard error of . For and , the reduction ratio is much smaller but still significant.

| Estimate | 0.0423 | -0.0003 | 1.0020 | 0.5063 |

| SE | 0.0065 | 0.0336 | 0.0283 | 0.0928 |

5.5 A Subordinate Diffusion Model for Fitting VIX Data

The CBOE volatility index, known as VIX, is a well-known fear gauge with large volume of futures and options contracts written on it. Using high-frequency data of VIX and applying non-parametric statistical tools developed in Todorov and Tauchen (2010), Todorov and Tauchen (2011) shows that VIX follows a pure jump process with infinite jump activity and infinite jump variation. Here, we develop a parametric pure jump model with these features based on subordinate diffusions for fitting VIX data.

Goard and Mazur (2013) analyzed the fit of a class of diffusion models to VIX and concluded that the 3/2 diffusion, which is the solution to the SDE , achieves the best fit. Here, we consider a more general class of diffusions than Goard and Mazur (2013). We assume that follows

| (5.24) |

The volatility of VIX is positively correlated with VIX itself, so it is reasonable to assume . We then construct a subordinate diffusion by time changing with an independent inverse Gaussian subordinator without drift. We choose this subordinator because it can be shown that using it makes the time changed process a pure jump process with infinite jump activity and infinite jump variation, capturing the features found in Todorov and Tauchen (2011) (the proof is similar to the proof of Proposition 2 in Li et al. (2017)). Due to the scaling invariance result in Corollary 2.1, we fix and estimate the other parameters.

For to satisfy Assumption 1, we need to impose some restrictions on the parameters. The sufficient condition for to have purely discrete spectrum can be derived by applying Theorem 3.3 of Linetsky (2008), which requires or . The sufficient condition that guarantees ergodicity for diffusions of form (5.24) can be found in Conley et al. (1997). Together, we have the following restrictions: , , , or , , if , , ; if , , ; if , and no restrictions on ; if , is replaced by in the previous statements. In our estimation, we set .

To estimate the diffusion parameters, we first apply (3.3) with (this denotes the column vector of partial derivative w.r.t. ) and obtain the following moment condition

where

We add another moment condition to estimate , which is

| (5.25) |

with . Following Conley et al. (1997), we set and to be the quantile of the empirical distribution of , which is 0.0056 in our case. To estimate and which are the mean rate and variance rate of the inverse Gaussian subordinator, we use the estimating function (3.9) with . The eigenvalues and eigenfunctions are first numerically calculated by the CPM, and then we run Li and Zhang algorithm with extrapolation to calculate (3.74) to obtain the KS weight.

We also estimate the diffusion model (5.24) as a benchmark. It is not difficult to see that the general diffusion model can be expressed as the diffusion in (5.24) with time changed with a deterministic clock . This model is again estimated using the two-step procedure above by first estimating the diffusion parameters and then .

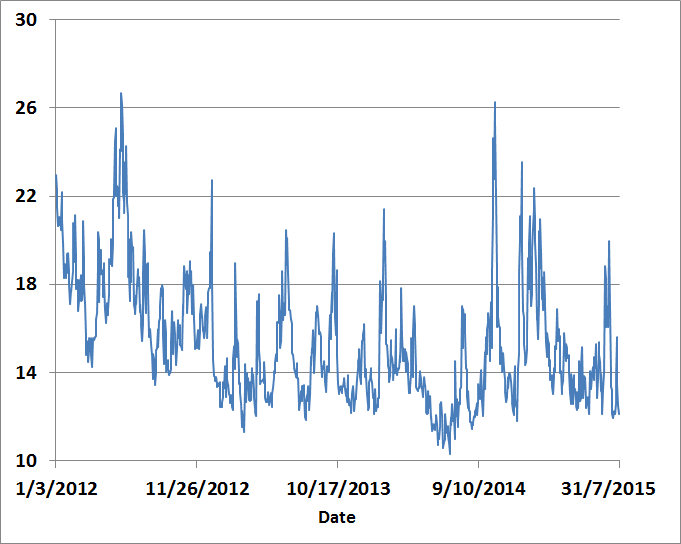

The data we use is daily VIX data in the period 03/01/2012 to 31/07/2014 with a total of 900 days downloaded from CBOE. Figure 1(a) plots the sample path of VIX, which is strongly mean-reverting with large moves. The estimation results for the diffusion model and the subordinate diffusion model are listed in Table 6. Here, the time unit is year and years.

| para () | |||||||

|---|---|---|---|---|---|---|---|

| diffusion | 0.0053 | 0.0177 | -0.3273 | 2.3695 | N.A. | N.A. | 225.3732 |

| jump | 0.0053 | 0.0177 | -0.3273 | 2.3695 | 222.2240 | 212.2837 | N.A. |

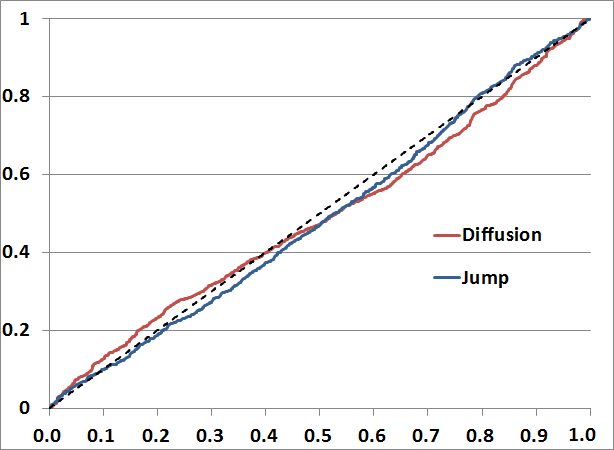

We employ the hypothesis test used in Larsen and Sørensen (2007) to test the goodness of fit. This test evaluates whether are i.i.d. uniform random variables over ( is the conditional distribution function for the parametric model). To do this, we first calculate s for the model under consideration using the estimated parameter values. Then, we apply the Kolmogorov-Smirnov test and the test. The test statistics and -value are shown in Table 7, which shows that the diffusion model is rejected at all practical significance levels while the subordinate diffusion model fits the data well. The superiority of the subordinate diffusion model over the diffusion counterpart is also evidenced from the QQ plot in Figure 1(b).

| K-S test | test (20 bins) | test (100 bins) | |||

|---|---|---|---|---|---|

| SubDiff(Jump) | statistic | 0.0374 | 20.0444 | 88.8889 | |

| p-value | 15.63% | 12.88% | 62.97% | ||

| Diffusion | statistic | 0.0599 | 45.7333 | 150.0000 | |

| p-value | 0.3% | 0.0059% | 0.0277% |

6 Conclusions

This paper considers parametric inference for a discretely observed ergodic subordinate diffusion. In general, we can only identify the characteristics of a subordinate diffusion up to scale and a two-step estimation procedure based on estimating functions is proposed, which is computationally and statistically efficient. The estimating function in the first step is based on the moment conditions that only involve diffusion parameters. In the second step, a martingale estimating function constructed using eigenvalues and eigenfunctions of the subordinate diffusion is used to estimate the parameters of the Lévy subordinator. Our method does not require the eigenpairs to be known analytically. For the general case, we develop an efficient numerical procedure to calculate the martingale estimating function. Under regularity conditions, consistency and asymptotic normality of our estimator are established considering the effect of numerical approximation. In future research, we will apply our method to estimate subordinate diffusion models in other applications, such as fitting commodity price data. We also plan to develop efficient methods to estimate other types of time-changed diffusions, for which the time change is not a Lévy subordinator but a more complicated process (see Li and Linetsky (2014) and Mendoza-Arriaga et al. (2010)). These models exhibit stochastic volatility and are very useful in financial applications.

Appendix A Proofs

Lemma 2.1: From Proposition 6 in Hansen and Scheinkman (1995), is ergodic if and only if for implies that . Here is the domain of and . We verify this equivalent condition. For such that , suppose that is not identically zero. Since , . Then shows that is an eigenfunction of with eigenvalue equal to . Since and have the same set of eigenfunctions, we must also have for some . However, by (1.9). Therefore , which further implies by (1.2), and hence for some nonzero . This contradicts that is ergodic (which we assume in Assumption 1 (1)), because applying Hansen and Scheinkman (1995), Proposition 6 again shows that when is ergodic, for implies that . So now we can conclude that for implies that and is ergodic.

To show that is ergodic, we can verify the equivalent condition in Proposition 7 of Hansen and Scheinkman (1995). The arguments are similar to the above and are omitted here to save space.

To show that is the stationary density for , let be the transition density of and be the distribution of . Then ’s transition density . We have

| (A.1) | ||||

| (A.2) |

This shows the claim. ∎

Theorem 2.1: “”: We first prove the implications of . Let be the law of with transition density and initial distribution (). Then implies for any . Since is ergodic by Lemma 2.1, we have for any initial distribution and any such that () is finite (note that is the stationary density for under by Lemma 2.1),

| (A.3) |

Since , we must have . Taking for arbitrary shows for . If a boundary point is finite and included in the state space, using the continuity of shows that at the boundary point. To sum up, for . In the following, we will denote the common stationary density by and all common quantities will be denoted without subscript . The rest of the proof consists of two steps.

Step 1: We will compare and . Two cases are considered below.

Case 1. Suppose lives on a compact interval with two reflecting boundaries. In this case, the spectrum of is discrete and so is the spectrum of . Note that implies that for any , so they share the same orthonormal set of eigenfunctions, and so do and (because a function is an eigenfunction of if and only if it is an eigenfunction of ). Take one eigenfunction . We have

| (A.4) |

Note that . Multiplying both sides of the equation by and noting that , we get

or

Integrating on both sides from to and using , we obtain

| (A.5) |

Similarly, we have

| (A.6) |

Combining (A.5) and (A.6), it is clear that and are proportional on . Since has a finite number of points in light of Theorem 4.1 of Hansen et al. (1998) and for all , there are finite number of such that . Hence, except on a finite number of points, and are proportional. However, from the continuity of and (Assumption 1 (3)), they must be proportional on the entire , i.e., there exists such that for all . Because , we have for all . Together, we have for all .

Case 2. We now consider with general state space . For any finite , we consider a diffusion living on with the same drift and diffusion coefficient as on this interval, and is reflected at . Denote the generators of associated with and by and . Note that the stationary density of is proportional to the stationary density of on , so it is the same under and . We will show that and have the same set of eigenfunctions.

Suppose is an eigenfunction of with corresponding eigenvalue . Then

From the discussions on p.788 of Hansen and Scheinkman (1995), has derivatives up to the fourth order on and all of them have finite limits when approaches and . Find small enough such that . Define a new function on such that on , for and , , for , and has derivatives up to the fourth order on . Note that has compact support and it belongs to and . Moreover, and are twice continuously differentiable and with compact support, thus is in . It is easy to see that . Thus, we have

This shows that is an eigenfunction of with eigenvalue , which further implies that for some constant , and hence is also an eigenfunction of . Conversely, using similar arguments, one can show that if is an eigenfunction of , then it is also an eigenfunction of . This shows that and have the same set of eigenfunctions.

Now we can repeat the procedure used in Case 1 and conclude that for any finite , there exists such that for all . Due to the continuity of and , does not depend on and since is arbitrary, holds for all .

Step 2: We now show the implications on the characteristics of the subordinator. We have proved that for for some constant . Then for . We have already explained in the proof of Case 1 that share the same orthonormal set of eigenfunctions which we denote by . Let be the eigenvalue of for , then is the eigenvalue of for . For each , we have

implies that

| (A.7) |

From Bertoin (1999), p.7

and

By (A.7), we have

Thus From Bertoin (1999), Section 1.2, we have

| (A.8) |

Since , we have for all .

“” We now prove that the conditions in (2.5) implies . From (A.8), we see that (2.5) gives us that . Our assumption implies that both and are given by the bilinear eigenfunction expansion (1.10). Using the given conditions and the expansion, it is straightforward verify that . ∎

Proof of Corollary 2.1: For tempered stable subordinators, using (1.3), we obtain that

| (A.9) |

The condition for all eigenvalues becomes that the equation

| (A.10) |

has infinitely many solutions on . It is not difficult to show that this is equivalent to , and .∎

Proof of Proposition 3.1: Denote

| (A.11) |

is defined similarly with by replacing with . Since is optimal,

| (A.12) |

is positive semi-definite for all possible . Note that

is positive semi-definite. Now let and is still defined in the same way as (A.11) by replacing and of with those of . Then

| (A.18) | |||

| (A.24) |

This is of form , where is positive semi-definite since is optimal. is positive semi-definite only when . The equation that can be rewritten as where is the expression in the parenthesis of (A.24). Now, replace by where is an arbitrary diagonal matrix with constant diagonal entries. Then, we have or for every . Since is arbitrary, we must have , and hence

| (A.25) |

for every possible . This shows the only if part of the statement.

Now suppose that (A.25) holds. We want to prove , which is given in (A.12), is positive semi-definite for all . Denote by

Using the definition of and ((A.11)), one can show that , , and (A.25) can be reformulated as . Now we have

| (A.26) | |||

| (A.27) | |||

| (A.28) | |||

| (A.29) |

which implies that is positive semi-definite.∎

Proof of Proposition 3.2: Inserting (3.64) into the definition of , we obtain

and

Substituting (3.64) into (3.62) for , we have

Using and (3.59) for , we obtain that the coefficient of and are equal to 0, and . Since the optimal weighting matrix is only unique up to scale, we can normalize to , and we have

Some simplifications give us the desired result. ∎

References

- Aït-Sahalia et al. (2010) Aït-Sahalia, Y., L. P. Hansen, and J. A. Scheinkeman (2010). Operator methods for continuosu time Markov processes. In Y. Aït-Sahalia and L. P. Hansen (Eds.), Handbook of Financial Econometrics: Tools and Techniques, Chapter 1, pp. 1–62. Amsterdam: North-Holland.

- Aït-Sahalia and Jacod (2009a) Aït-Sahalia, Y. and J. Jacod (2009a). Estimating the degree of activity of jumps in high frequency data. The Annals of Statistics 37(5A), 2202–2244.

- Aït-Sahalia and Jacod (2009b) Aït-Sahalia, Y. and J. Jacod (2009b). Testing for jumps in a discretely observed process. The Annals of Statistics 37(1), 184–222.

- Aït-Sahalia and Jacod (2011) Aït-Sahalia, Y. and J. Jacod (2011). Testing whether jumps have finite or infinite activity. The Annals of Statistics 39(3), 1689–1719.

- Aït-Sahalia et al. (2012) Aït-Sahalia, Y., J. Jacod, and J. Li (2012). Testing for jumps in noisy high frequency data. Journal of Econometrics 168(2), 207–222.

- (6) Barndorff-Nielsen, O. E. Processes of Normal Inverse Gaussian type. Finance and Stochastics 2(1), 41–68.

- Belomestny (2011) Belomestny, D. (2011). Statistical inference for time-changed Lévy processes via composite characteristic function estimation. The Annals of Statistics 39(4), 2205–2242.

- Bertoin (1999) Bertoin, J. (1999). Subordinators: examples and applications. In Lectures on probability theory and statistics, pp. 1–91. Berlin: Springer.

- Bibby et al. (2010a) Bibby, B. M., M. Jacobsen, and M. Sørensen (2010a). Estimating functions for discretely sampled diffusion-type models. In Y. Aïtsahalia and L. P. Hansen (Eds.), Handbook of Financial Econometrics, Volume 1, Chapter 4, pp. 203–262. Amsterdam: North-Holland.

- Bibby et al. (2010b) Bibby, B. M., M. Jacobsen, and M. Sørensen (2010b). Estimating functions for discretely sampled diffusion-type models. In Y. Aït-Sahalia and L. P. Hansen (Eds.), Handbook of Financial Econometrics: Tools and Techniques, Chapter 4, pp. 203–268. Amsterdam: North-Holland.

- Bibby and Sørensen (1995) Bibby, B. M. and M. Sørensen (1995). Martingale estimation functions for discretely observed diffusion processes. Bernoulli 1(1), 17–39.

- Bibby and Sørensen (2001) Bibby, B. M. and M. Sørensen (2001). Simplified estimating functions for diffusion models with a high-dimensional parameter. Scandinavian Journal of Statistics 28(1), 99–112.

- Billingsley (1961a) Billingsley, P. (1961a). The Lindeberg-Lévy theorem for martingales. Proceedings of the American Mathematical Society 12(5), 788–792.

- Billingsley (1961b) Billingsley, P. (1961b). Statistical inference for Markov processes, Volume 2. University of Chicago Press.

- Bochner (1949) Bochner, S. (1949). Diffusion equations and stochastic processes. Proceedings of the National Academy of Sciences of the United States of America 35(7), 368–370.

- Bull (2014) Bull, A. D. (2014). Estimating time-changes in noisy Lévy models. The Annals of Statistics 42(5), 2026–2057.

- Carr and Wu (2004) Carr, P. and L. Wu (2004). Time-changed Lévy processes and option pricing. Journal of Financial economics 71(1), 113–141.

- Conley et al. (1997) Conley, T. G., L. P. Hansen, E. G. Luttmer, and J. A. Scheinkman (1997). Short-term interest rates as subordinated diffusions. Review of Financial Studies 10(3), 525–577.

- Cont and Tankov (2004) Cont, R. and P. Tankov (2004). Financial Modeling with Jump Processes. Cambridge: Chapman & Hall.

- Figueroa-López (2009) Figueroa-López, J. E. (2009). Nonparametric estimation of time-changed Lévy models under high-frequency data. Advances in Applied Probability 41(04), 1161–1188.

- Figueroa-López (2011) Figueroa-López, J. E. (2011). Central limit theorems for the non-parametric estimation of time-changed Lévy models. Scandinavian Journal of Statistics 38(4), 748–765.

- Goard and Mazur (2013) Goard, J. and M. Mazur (2013). Stochastic volatility models and the pricing of VIX options. Mathematical Finance 23(3), 439–458.

- Godambe and Heyde (1987) Godambe, V. and C. Heyde (1987). Quasi-likelihood and optimal estimation, correspondent paper. International Statistical Review/Revue Internationale de Statistique 55(3), 231–244.

- Hansen and Scheinkman (1995) Hansen, L. P. and J. A. Scheinkman (1995). Back to the future: generating moment implications for continuous-time Markov processes. Econometrica 63(4), 767–804.

- Hansen et al. (1998) Hansen, L. P., J. A. Scheinkman, and N. Touzi (1998). Spectral methods for identifying scalar diffusions. Journal of Econometrics 86(1), 1–32.

- Karlin and Taylor (1981) Karlin, S. and H. M. Taylor (1981). A second course in stochastic processes, Volume 2. New York: Academic Press.

- Kessler (2000) Kessler, M. (2000). Simple and explicit estimating functions for a discretely observed diffusion process. Scandinavian Journal of Statistics 27(1), 65–82.

- Kessler et al. (2012) Kessler, M., A. Lindner, and M. Sørensen (2012). Statistical methods for stochastic differential equations. Boca Raton: CRC Press.

- Kessler and Sørensen (1999) Kessler, M. and M. Sørensen (1999). Estimating equations based on eigenfunctions for a discretely observed diffusion process. Bernoulli 5(2), 299–314.

- Kutoyants (2004) Kutoyants, Y. A. (2004). Statistical inference for ergodic diffusion processes. London: Springer.

- Larsen and Sørensen (2007) Larsen, K. S. and M. Sørensen (2007). Diffusion models for exchange rates in a target zone. Mathematical Finance 17(2), 285–306.

- Ledoux and Van Daele (2010) Ledoux, V. and M. Van Daele (2010). Solving Sturm–Liouville problems by piecewise perturbation methods, revisited. Computer Physics Communications 181(8), 1335–1345.

- Ledoux et al. (2004) Ledoux, V., M. Van Daele, and G. V. Berghe (2004). CP methods of higher order for Sturm–Liouville and Schrödinger equations. Computer Physics Communications 162(3), 151–165.

- Li et al. (2016) Li, J., L. Li, and R. Mendoza-Arriaga (2016). Additive subordination and its applications in finance. Finance and Stochastics 20(3), 589–634.

- Li et al. (2017) Li, J., L. Li, and G. Zhang (2017). Pure jump models for pricing and hedging VIX derivatives. Journal of Economic Dynamics and Control 74(1), 28–55.

- Li and Linetsky (2013) Li, L. and V. Linetsky (2013). Optimal stopping and early exercise: an eigenfunction expansion approach. Operations Research 61(3), 625–643.

- Li and Linetsky (2014) Li, L. and V. Linetsky (2014). Time-changed Ornstein-Uhlenbeck processes and their applications in commodity derivative models. Mathematical Finance 24(2), 289–330.

- Li and Linetsky (2015) Li, L. and V. Linetsky (2015). Discretely monitored first passage problems and barrier options: an eigenfunction expansion approach. Finance and Stochastics 19(4), 941–977.

- Li and Zhang (2016) Li, L. and G. Zhang (2016). Option pricing in some non-Lévy jump models. SIAM Journal on Scientific Computing 38(4), B539–B569.

- Li and Zhang (2017) Li, L. and G. Zhang (2017). Error analysis of finite difference and Markov chain approximations for option pricing. Mathematical Finance. Forthcoming.

- Linetsky (2008) Linetsky, V. (2008). Spectral methods in derivatives pricing. In J. Birge and V. Linetsky (Eds.), Handbook of Financial Engineering, Handbooks in Operations Research and Management, Chapter 6. Amsterdam: Elsevier.

- Mendoza-Arriaga et al. (2010) Mendoza-Arriaga, R., P. Carr, and V. Linetsky (2010). Time changed Markov processes in unified credit-equity modeling. Mathematical Finance 20(4), 527–569.

- Pryce (1993) Pryce, J. D. (1993). Numerical solution of Sturm-Liouville problems. Oxford University Press.

- Schilling et al. (2012) Schilling, R. L., R. Song, and Z. Vondracek (2012). Bernstein functions: theory and applications, Volume 37. Berlin/Boston: Walter de Gruyter.

- Sørensen (2004) Sørensen, H. (2004). Parametric inference for diffusion processes observed at discrete points in time: a survey. International Statistical Review 72(3), 337–354.

- Sørensen (1997) Sørensen, M. (1997). Estimating functions for discretely observed diffusions: A review. Lecture Notes-Monograph Series, 305–325.

- Sørensen (1999) Sørensen, M. (1999). On asymptotics of estimating functions. Brazilian Journal of Probability and Statistics 13(2), 111–136.

- Sørensen (2012) Sørensen, M. (2012). Estimating functions for diffusion-type processes. In Statistical Methods for Stochastic Differential Equations. Boca Raton: CRC Press.

- Todorov and Tauchen (2010) Todorov, V. and G. Tauchen (2010). Activity signature functions for high-frequency data analysis. Journal of Econometrics 154(2), 125–138.

- Todorov and Tauchen (2011) Todorov, V. and G. Tauchen (2011). Volatility jumps. Journal of Business & Economic Statistics 29(3), 356–371.