Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations

Abstract

We propose a new algorithm for solving parabolic partial differential equations (PDEs) and backward stochastic differential equations (BSDEs) in high dimension, by making an analogy between the BSDE and reinforcement learning with the gradient of the solution playing the role of the policy function, and the loss function given by the error between the prescribed terminal condition and the solution of the BSDE. The policy function is then approximated by a neural network, as is done in deep reinforcement learning. Numerical results using TensorFlow illustrate the efficiency and accuracy of the proposed algorithms for several -dimensional nonlinear PDEs from physics and finance such as the Allen-Cahn equation, the Hamilton-Jacobi-Bellman equation, and a nonlinear pricing model for financial derivatives.

1 Introduction

Developing efficient numerical algorithms for high dimensional (say, hundreds of dimensions) partial differential equations (PDEs) has been one of the most challenging tasks in applied mathematics. As is well-known, the difficulty lies in the “curse of dimensionality” [1], namely, as the dimensionality grows, the complexity of the algorithms grows exponentially. For this reason, there are only a limited number of cases where practical high dimensional algorithms have been developed. For linear parabolic PDEs, one can use the Feynman-Kac formula and Monte Carlo methods to develop efficient algorithms to evaluate solutions at any given space-time locations. For a class of inviscid Hamilton-Jacobi equations, Darbon & Osher have recently developed an algorithm which performs numerically well in the case of such high dimensional inviscid Hamilton-Jacobi equations; see [9]. Darbon & Osher’s algorithm is based on results from compressed sensing and on the Hopf formulas for the Hamilton-Jacobi equations. A general algorithm for (nonlinear) parabolic PDEs based on the Feynman-Kac and Bismut-Elworthy-Li formula and a multi-level decomposition of Picard iteration was developed in [11] and has been shown to be quite efficient on a number examples in finance and physics. The complexity of the algorithm is shown to be for semilinear heat equations, where is the dimensionality of the problem and is the required accuracy.

In recent years, a new class of techniques, called deep learning, have emerged in machine learning and have proven to be very effective in dealing with a large class of high dimensional problems in computer vision (cf., e.g., [23]), natural language processing (cf., e.g., [20]), time series analysis, etc. (cf., e.g., [15, 24]). This success fuels in speculations that deep learning might hold the key to solve the curse of dimensionality problem. It should be emphasized that at the present time, there are no theoretical results that support such claims although the practical success of deep learning has been astonishing. However, this should not prevent us from trying to apply deep learning to other problems where the curse of dimensionality has been the issue.

In this paper, we explore the use of deep learning for solving general high dimensional PDEs. To this end, it is necessary to formulate the PDEs as a learning problem. Motivated by ideas in [16] where deep learning-based algorithms were developed for high dimensional stochastic control problems, we explore a connection between (nonlinear) parabolic PDEs and backward stochastic differential equations (BSDEs) (see [26, 28, 25]) since BSDEs share a lot of common features with stochastic control problems.

2 Main ideas of the algorithm

We will consider a fairly general class of nonlinear parabolic PDEs (see (30) in Subsection 4.1 below). The proposed algorithm is based on the following set of ideas:

-

(i)

Through the so-called nonlinear Feynman-Kac formula, we can formulate the PDEs equivalently as BSDEs.

-

(ii)

One can view the BSDE as a stochastic control problem with the gradient of the solution being the policy function. These stochastic control problems can then be viewed as model-based reinforcement learning problems.

-

(iii)

The (high dimensional) policy function can then be approximated by a deep neural network, as has been done in deep reinforcement learning.

Instead of formulating initial value problems, as is commonly done in the PDE literature, we consider the set up with terminal conditions since this facilitates making connections with BSDEs. Terminal value problems can obviously be transformed to initial value problems and vice versa.

In the remainder of this section we present a rough sketch of the derivation of the proposed algorithm, which we refer to as deep BSDE solver. In this derivation we restrict ourself to a specific class of nonlinear PDEs, that is, we restrict ourself to semilinear heat equations (see (PDE) below) and refer to Subsections 3.2 and 4.1 below for the general introduction of the deep BSDE solver.

2.1 An example: a semilinear heat partial differential equation (PDE)

Let , , , let and be continuous functions, and let satisfy for all , that and

| (PDE) |

A key idea of this work is to reformulate the PDE (PDE) as an appropriate stochastic control problem.

2.2 Formulation of the PDE as a suitable stochastic control problem

More specifically, let be a probability space, let be a -dimensional standard Brownian motion on , let be the normal filtration on generated by , let be the set of all -adapted -valued stochastic processes with continuous sample paths, and for every and every let be an -adapted stochastic process with continuous sample paths which satisfies that for all it holds -a.s. that

| (1) |

We now view the solution of (PDE) and its spatial derivative as the solution of a stochastic control problem associated to (1). More formally, under suitable regularity hypotheses on the nonlinearity it holds that the pair consisting of and is the (up to indistinguishability) unique global minimum of the function

| (2) |

One can also view the stochastic control problem (1)–(2) (with being the control) as a model-based reinforcement learning problem. In that analogy, we view as the policy and we approximate using feedforward neural networks (see (11) and Section 4 below for further details). The process , , corresponds to the value function associated to the stochastic control problem and can be computed approximatively by employing the policy (see (9) below for details). The connection between the PDE (PDE) and the stochastic control problem (1)–(2) is based on the nonlinear Feynman-Kac formula which links PDEs and BSDEs (see (BSDE) and (3) below).

2.3 The nonlinear Feynman-Kac formula

Let and be -adapted stochastic processes with continuous sample paths which satisfy that for all it holds -a.s. that

| (BSDE) |

Under suitable additional regularity assumptions on the nonlinearity we have that the nonlinear parabolic PDE (PDE) is related to the BSDE (BSDE) in the sense that for all it holds -a.s. that

| (3) |

(cf., e.g., [25, Section 3] and [27]). The first identity in (3) is sometimes referred to as nonlinear Feynman-Kac formula in the literature.

2.4 Forward discretization of the backward stochastic differential equation (BSDE)

To derive the deep BSDE solver, we first plug the second identity in (3) into (BSDE) to obtain that for all it holds -a.s. that

| (4) |

In particular, we obtain that for all with it holds -a.s. that

| (5) |

Next we apply a time discretization to (5). More specifically, let and let be real numbers which satisfy

| (6) |

and observe that (5) suggests for sufficiently large that

| (7) | ||||

2.5 Deep learning-based approximations

In the next step we employ a deep learning approximation for

| (8) |

but not for , , . Approximations for , , , in turn, can be computed recursively by using (7) together with deep learning approximations for (8). More specifically, let , let , , be real numbers, let , , , be continuous functions, and let , , be stochastic processes which satisfy for all , that and

| (9) |

We think of as the number of parameters in the neural network, for all appropriate we think of as suitable approximations

| (10) |

of , and for all appropriate , , we think of as suitable approximations

| (11) |

of .

2.6 Stochastic optimization algorithms

The “appropriate” can be obtained by minimizing the expected loss function through stochastic gradient descent-type algorithms. For the loss function we pick the squared approximation error associated to the terminal condition of the BSDE (BSDE). More precisely, assume that the function has a unique global minimum and let be the real vector for which the function

| (12) |

is minimal. Minimizing the function (12) is inspired by the fact that

| (13) |

according to (BSDE) above (cf. (2) above). Under suitable regularity assumptions, we approximate the vector through stochastic gradient descent-type approximation methods and thereby we obtain random approximations of . For sufficiently large we then employ the random variable as a suitable implementable approximation

| (14) |

of (cf. (10) above) and for sufficiently large and all , we use the random variable as a suitable implementable approximation

| (15) |

of (cf. (11) above). In the next section the proposed approximation method is described in more detail.

3 Details of the algorithm

3.1 Formulation of the proposed algorithm in the case of semilinear heat equations

In this subsection we describe the algorithm proposed in this article in the specific situation where (PDE) is the PDE under consideration, where batch normalization (see Ioffe & Szegedy [21]) is not employed, and where the plain-vanilla stochastic gradient descent approximation method with a constant learning rate and without mini-batches is the employed stochastic algorithm. The general framework, which includes the setting in this subsection as a special case, can be found in Subsection 3.2 below.

Framework 3.1 (Specific case).

Let , , , let and be functions, let be a probability space, let , , be independent -dimensional standard Brownian motions on , let be real numbers with

| (16) |

for every let , for every , let be a function, for every , let be the stochastic process which satisfies for all that and

| (17) |

for every let be the function which satisfies for all , that

| (18) |

for every let be a function which satisfies for all , that

| (19) |

and let be a stochastic process which satisfy for all that

| (20) |

3.2 Formulation of the proposed algorithm in the general case

Framework 3.2 (General case).

Let , , , let , , and be functions, let be a probability space, let , , be independent -dimensional standard Brownian motions on , let be real numbers with

| (23) |

for every let , for every , , , let be a function, for every let and , , , be stochastic processes which satisfy for all , , that

| (24) |

| (25) |

for every , let be the function which satisfies for all , that

| (26) |

for every , let be a function which satisfies for all , that

| (27) |

let be a function, for every let and be functions, and let , , and be stochastic processes which satisfy for all that

| (28) |

| (29) |

3.3 Comments on the proposed algorithm

The dynamics in (24) associated to the stochastic processes for allows us to incorporate different algorithms for the discretization of the considered forward stochastic differential equation (SDE) into the deep BSDE solver in Subsection 3.2. The dynamics in (29) associated to the stochastic processes , , and , , allows us to incorporate different stochastic approximation algorithms such as

-

•

stochastic gradient descent with or without mini-batches (see Subsection 5.1 below) as well as

- •

The dynamics in (28) associated to the stochastic process , , allows us to incorporate the standardization procedure in batch normalization (see Ioffe & Szegedy [21] and also Section 4 below) into the deep BSDE solver in Subsection 3.2. In that case we think of , , as approximatively calculated means and standard deviations.

4 Examples for nonlinear partial differential equations (PDEs) and nonlinear backward stochastic differential equations (BSDEs)

In this section we illustrate the algorithm proposed in Subsection 3.2 using several concrete example PDEs. In the examples below we will employ the general approximation method in Subsection 3.2 in conjunction with the Adam optimizer (cf. Example 5.2 below and Kingma & Ba [22]) with mini-batches with samples in each iteration step (see Subsection 4.1 for a detailed description).

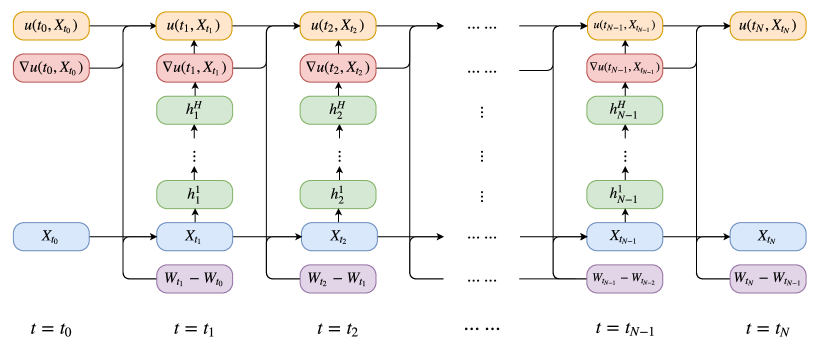

In our implementation we employ fully-connected feedforward neural networks to represent for , , (cf. also Figure 1 below for a rough sketch of the architecture of the deep BSDE solver). Each of the neural networks consists of layers ( input layer [-dimensional], hidden layers [both -dimensional], and output layer [-dimensional]). The number of hidden units in each hidden layer is equal to . We also adopt batch normalization (BN) (see Ioffe & Szegedy [21]) right after each matrix multiplication and before activation. We employ the rectifier function as our activation function for the hidden variables. All the weights in the network are initialized using a normal or a uniform distribution without any pre-training. Each of the numerical experiments presented below is performed in Python using TensorFlow on a Macbook Pro with a Gigahertz (GHz) Intel Core i5 micro processor and 16 gigabytes (GB) of 1867 Megahertz (MHz) double data rate type three synchronous dynamic random-access memory (DDR3-SDRAM). We also refer to the Python code 1 in Subsection 6.1 below for an implementation of the deep BSDE solver in the case of the -dimensional Allen-Cahn PDE (35).

4.1 Setting

Assume the setting in Subsection 3.2, assume for all that , , , , , let and be functions, let be a continuous and at most polynomially growing function which satisfies for all that , , and

| (30) |

let , , , , , let , , be the functions which satisfy for all , that

| (31) |

and assume for all , , that

| (32) |

and

| (33) |

Remark 4.1.

In this remark we illustrate the specific choice of the dimension of in the framework in Subsection 4.1 above.

-

(i)

The first component of is employed for approximating the real number .

-

(ii)

The next -components of are employed for approximating the components of the -matrix .

-

(iii)

In each of the employed neural networks we use components of to describe the linear transformation from the -dimensional first layer (input layer) to the -dimensional second layer (first hidden layer) (to uniquely describe a real -matrix).

-

(iv)

In each of the employed neural networks we use components of to uniquely describe the linear transformation from the -dimensional second layer (first hidden layer) to the -dimensional third layer (second hidden layer) (to uniquely describe a real -matrix).

-

(v)

In each of the employed neural networks we use components of to describe the linear transformation from the -dimensional third layer (second hidden layer) to the -dimensional fourth layer (output layer) (to uniquely describe a real -matrix).

-

(vi)

After each of the linear transformations in items (iii)–(v) above we employ a componentwise affine linear transformation (multiplication with a diagonal matrix and addition of a vector) within the batch normalization procedure, i.e., in each of the employed neural networks, we use components of for the componentwise affine linear transformation between the first linear transformation (see item (iii)) and the first application of the activation function, we use components of for the componentwise affine linear transformation between the second linear transformation (see item (iv)) and the second application of the activation function, and we use components of for the componentwise affine linear transformation after the third linear transformation (see item (v)).

| (34) |

4.2 Allen-Cahn equation

In this section we test the deep BSDE solver in the case of an -dimensional Allen-Cahn PDE with a cubic nonlinearity (see (35) below).

More specifically, assume the setting in the Subsection 4.1 and assume for all , , , , that , , , , , , , , , and . Note that the solution of the PDE (30) then satisfies for all , that and

| (35) |

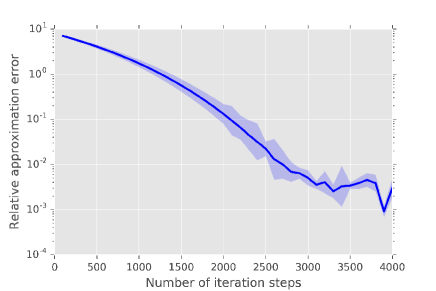

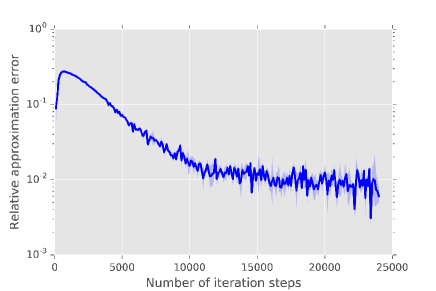

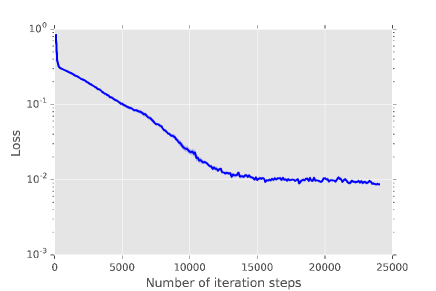

In Table 1 we approximatively calculate the mean of , the standard deviation of , the relative -approximatin error associated to , the standard deviation of the relative -approximatin error associated to , and the runtime in seconds needed to calculate one realization of against based on independent realizations ( independent runs) (see also the Python code 1 below). Table 1 also depicts the mean of the loss function associated to and the standard deviation of the loss function associated to against based on Monte Carlo samples and independent realizations ( independent runs). In addition, the relative -approximation error associated to against is pictured on the left hand side of Figure 2 based on independent realizations ( independent runs) and the mean of the loss function associated to against is pictured on the right hand side of Figure 2 based on Monte Carlo samples and independent realizations ( independent runs). In the approximative computations of the relative -approximation errors in Table 1 and Figure 2 the value of the exact solution of the PDE (35) is replaced by the value which, in turn, is calculated by means of the Branching diffusion method (see the Matlab code 2 below and see, e.g., [17, 19, 18] for analytical and numerical results for the Branching diffusion method in the literature).

| Number | Mean | Standard | Relative | Standard | Mean | Standard | Runtime |

| of | of | deviation | -appr. | deviation | of the | deviation | in sec. |

| iteration | of | error | of the | loss | of the | for one | |

| steps | relative | function | loss | realization | |||

| -appr. | function | of | |||||

| error | |||||||

| 0 | 0.4740 | 0.0514 | 7.9775 | 0.9734 | 0.11630 | 0.02953 | |

| 1000 | 0.1446 | 0.0340 | 1.7384 | 0.6436 | 0.00550 | 0.00344 | 201 |

| 2000 | 0.0598 | 0.0058 | 0.1318 | 0.1103 | 0.00029 | 0.00006 | 348 |

| 3000 | 0.0530 | 0.0002 | 0.0050 | 0.0041 | 0.00023 | 0.00001 | 500 |

| 4000 | 0.0528 | 0.0002 | 0.0030 | 0.0022 | 0.00020 | 0.00001 | 647 |

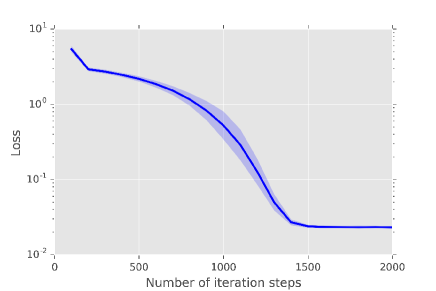

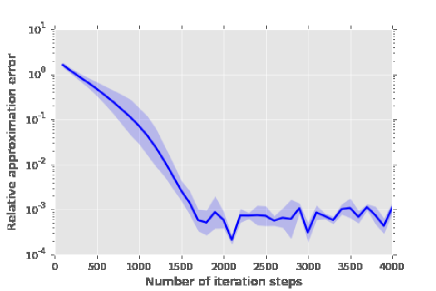

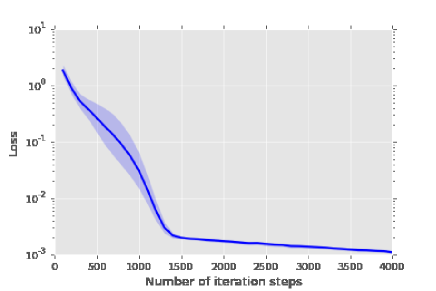

4.3 A Hamilton-Jacobi-Bellman (HJB) equation

In this subsection we apply the deep BSDE solver in Subsection 3.2 to a Hamilton-Jacobi-Bellman (HJB) equation which admits an explicit solution that can be obtained through the Cole-Hopf transformation (cf., e.g., Chassagneux & Richou [7, Section 4.2] and Debnath [10, Section 8.4]).

Assume the setting in the Subsection 4.1 and assume for all , , , , that , , , , , , , , , and . Note that the solution of the PDE (30) then satisfies for all , that and

| (36) |

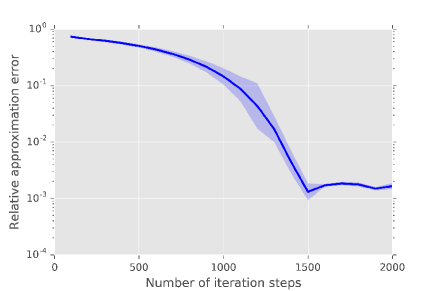

In Table 2 we approximatively calculate the mean of , the standard deviation of , the relative -approximatin error associated to , the standard deviation of the relative -approximatin error associated to , and the runtime in seconds needed to calculate one realization of against based on independent realizations ( independent runs). Table 2 also depicts the mean of the loss function associated to and the standard deviation of the loss function associated to against based on Monte Carlo samples and independent realizations ( independent runs). In addition, the relative -approximation error associated to against is pictured on the left hand side of Figure 3 based on independent realizations ( independent runs) and the mean of the loss function associated to against is pictured on the right hand side of Figure 3 based on Monte Carlo samples and independent realizations ( independent runs). In the approximative computations of the relative -approximation errors in Table 2 and Figure 3 the value of the exact solution of the PDE (35) is replaced by the value which, in turn, is calculated by means of Lemma 4.2 below (with , , , , in the notation of Lemma 4.2) and a classical Monte Carlo method (see the Matlab code 3 below).

| Number | Mean | Standard | Relative | Standard | Mean | Standard | Runtime |

| of | of | deviation | -appr. | deviation | of the | deviation | in sec. |

| iteration | of | error | of the | loss | of the | for one | |

| steps | relative | function | loss | realization | |||

| -appr. | function | of | |||||

| error | |||||||

| 0 | 0.3167 | 0.3059 | 0.9310 | 0.0666 | 18.4052 | 2.5090 | |

| 500 | 2.2785 | 0.3521 | 0.5036 | 0.0767 | 2.1789 | 0.3848 | 116 |

| 1000 | 3.9229 | 0.3183 | 0.1454 | 0.0693 | 0.5226 | 0.2859 | 182 |

| 1500 | 4.5921 | 0.0063 | 0.0013 | 0.006 | 0.0239 | 0.0024 | 248 |

| 2000 | 4.5977 | 0.0019 | 0.0017 | 0.0004 | 0.0231 | 0.0026 | 330 |

Lemma 4.2 (Cf., e.g., Section 4.2 in [7] and Section 8.4 in [10]).

Let , , , let be a probability space, let be a -dimensional standard Brownian motion, let be a function which satisfies , let be the function which satisfies for all , , that

| (37) |

and let be the function which satisfies for all that

| (38) |

Then

-

(i)

it holds that is a continuous function,

-

(ii)

it holds that , and

-

(iii)

it holds for all that and

(39)

Proof of Lemma 4.2.

Throughout this proof let and let and be the functions which satisfy for all , that

| (40) |

Observe that the hypothesis that ensures that for all it holds that

| (41) |

Combining this with Lebesgue’s theorem of dominated convergence ensures that is a continuous function. This and the fact that

| (42) |

establish Item (i). Next note that the Feynman-Kac formula ensures that for all , it holds that and

| (43) |

This and (42) demonstrate Item (ii). It thus remains to prove Item (iii). For this note that the chain rule and (42) imply that for all , , it holds that

| (44) |

Again the chain rule and (42) hence ensure that for all , , it holds that

| (45) |

This assures that for all , , it holds that

| (46) |

Combining this with (44) demonstrates that for all , it holds that

| (47) |

Equation (43) hence shows that for all , it holds that

| (48) |

This and (44) demonstrate that for all , it holds that

| (49) |

This and the fact that

| (50) |

establish Item (iii). The proof of Lemma 4.2 is thus completed. ∎

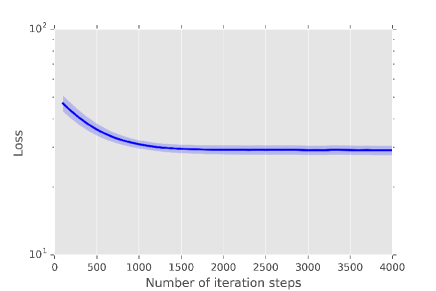

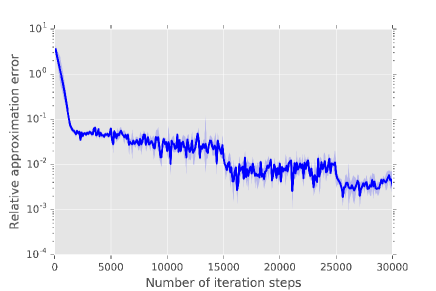

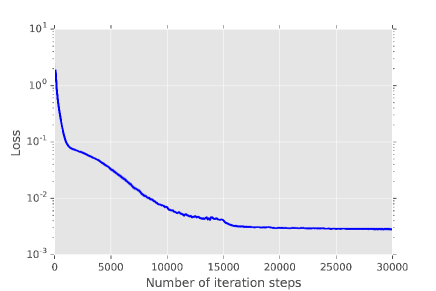

4.4 Pricing of European financial derivatives with different interest rates for borrowing and lending

In this subsection we apply the deep BSDE solver to a pricing problem of an European financial derivative in a financial market where the risk free bank account used for the hedging of the financial derivative has different interest rates for borrowing and lending (see Bergman [4] and, e.g., [12, 2, 3, 5, 8, 11] where this example has been used as a test example for numerical methods for BSDEs).

Assume the setting in Subsection 4.1, let , , , , and assume for all , , , , that , , , , , , , and

| (51) |

| (52) |

| (53) |

Note that the solution of the PDE (30) then satisfies for all , that and

| (54) |

Hence, we obtain for all , that and

| (55) |

This shows that for all , it holds that and

| (56) |

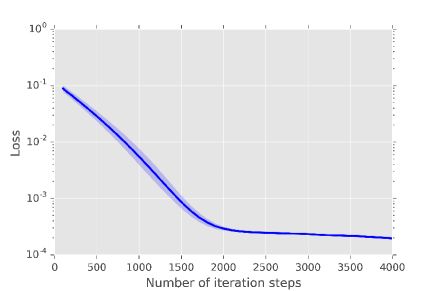

In Table 3 we approximatively calculate the mean of , the standard deviation of , the relative -approximatin error associated to , the standard deviation of the relative -approximatin error associated to , and the runtime in seconds needed to calculate one realization of against based on independent realizations ( independent runs). Table 3 also depicts the mean of the loss function associated to and the standard deviation of the loss function associated to against based on Monte Carlo samples and independent realizations ( independent runs). In addition, the relative -approximation error associated to against is pictured on the left hand side of Figure 4 based on independent realizations ( independent runs) and the mean of the loss function associated to against is pictured on the right hand side of Figure 4 based on Monte Carlo samples and independent realizations ( independent runs). In the approximative computations of the relative -approximation errors in Table 3 and Figure 4 the value of the exact solution of the PDE (56) is replaced by the value which, in turn, is calculated by means of the multilevel-Picard approximation method in E et al. [11] (see [11, in Table 6 in Section 4.3]).

| Number | Mean | Standard | Relative | Standard | Mean | Standard | Runtime |

| of | of | deviation | -appr. | deviation | of the | deviation | in sec. |

| iteration | of | error | of the | loss | of the | for one | |

| steps | relative | function | loss | realization | |||

| -appr. | function | of | |||||

| error | |||||||

| 0 | 16.964 | 0.882 | 0.204 | 0.041 | 53.666 | 8.957 | |

| 1000 | 20.309 | 0.524 | 0.046 | 0.025 | 30.886 | 3.076 | 194 |

| 2000 | 21.150 | 0.098 | 0.007 | 0.005 | 29.197 | 3.160 | 331 |

| 3000 | 21.229 | 0.034 | 0.003 | 0.002 | 29.070 | 3.246 | 470 |

| 4000 | 21.217 | 0.043 | 0.004 | 0.002 | 29.029 | 3.236 | 617 |

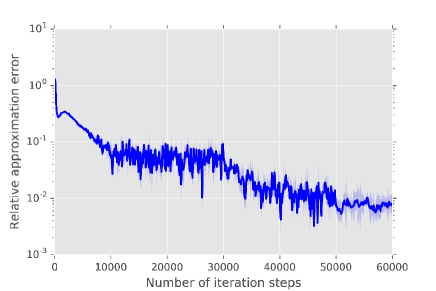

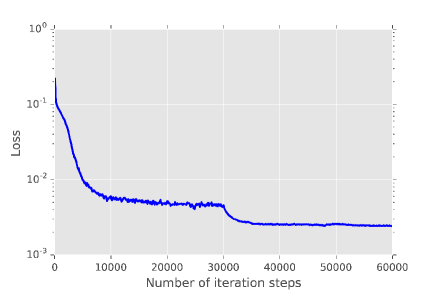

4.5 Multidimensional Burgers-type PDEs with explicit solutions

In this subsection we consider a high-dimensional version of the example analyzed numerically in Chassagneux [6, Example 4.6 in Subsection 4.2].

More specifically, assume the setting in Subsection 4.1, and assume for all , , , that , , , , and

| (57) |

Note that the solution of the PDE (30) then satisfies for all , that and

| (58) |

(cf. Lemma 4.3 below [with , in the notation of Lemma 4.3 below]). On the left hand side of Figure 5 we present approximatively the relative -approximatin error associated to against based on independent realizations ( independent runs) in the case

| (59) |

On the right hand side of Figure 5 we present approximatively the mean of the loss function associated to against based on Monte Carlo samples and independent realizations ( independent runs) in the case (59). On the left hand side of Figure 6 we present approximatively the relative -approximatin error associated to against based on independent realizations ( independent runs) in the case

| (60) |

On the right hand side of Figure 6 we present approximatively the mean of the loss function associated to against based on Monte Carlo samples and independent realizations ( independent runs) in the case (60).

Lemma 4.3 (Cf. Example 4.6 in Subsection 4.2 in [6]).

Let , , let be the function which satisfies for all , that

| (61) |

and let be the function which satisfies for all , , , that

| (62) |

Then it holds for all , that

| (63) |

Proof of Lemma 4.3.

Throughout this proof let be the real numbers given by

| (64) |

and let be the function which satisfies for all , that

| (65) |

Observe that for all , , it holds that

| (66) |

| (67) |

and

| (68) |

Note that (66), (67), and (68) ensure that for all , it holds that

| (69) |

Moreover, observe that (68) demonstrates that for all , it holds that

| (70) |

Hence, we obtain that for all , it holds that

| (71) |

Combining this with (69) implies that for all , it holds that

| (72) |

The fact that hence demonstrates that for all , it holds that

| (73) |

This and the fact that show that for all , it holds that

| (74) |

The proof of Lemma 4.3 is thus completed. ∎

4.6 An example PDE with quadratically growing derivatives and an explicit solution

In this subsection we consider a high-dimensional version of the example analyzed numerically in Gobet & Turkedjiev [13, Section 5]. More specifically, Gobet & Turkedjiev [13, Section 5] employ the PDE in (76) below as a numerical test example but with the time horizont instead of in this article and with the dimension instead of in this article.

Assume the setting in Subsection 4.1, let , let be the function which satisfies for all that , and assume for all , , , , , that , , , , , , , , , and

| (75) |

Note that the solution of the PDE (30) then satisfies for all , that and

| (76) |

On the left hand side of Figure 7 we present approximatively the relative -approximatin error associated to against based on independent realizations ( independent runs). On the right hand side of Figure 7 we present approximatively the mean of the loss function associated to against based on Monte Carlo samples and independent realizations ( independent runs).

4.7 Time-dependent reaction-diffusion-type example PDEs with oscillating explicit solutions

In this subsection we consider a high-dimensional version of the example PDE analyzed numerically in Gobet & Turkedjiev [14, Subsection 6.1]. More specifically, Gobet & Turkedjiev [14, Subsection 6.1] employ the PDE in (78) below as a numerical test example but in two space-dimensions () instead of in hundred space-dimensions () as in this article.

Assume the setting in Subsection 4.1, let , , assume for all , , , , that , , , , , , , , , and

| (77) |

Note that the solution of the PDE (30) then satisfies for all , that and

| (78) |

(cf. Lemma 4.4 below). On the left hand side of Figure 7 we present approximatively the relative -approximatin error associated to against based on independent realizations ( independent runs). On the right hand side of Figure 7 we present approximatively the mean of the loss function associated to against based on Monte Carlo samples and independent realizations ( independent runs).

Lemma 4.4 (Cf. Subsection 6.1 in [14]).

Let , and let be the function which satisfies for all , that

| (79) |

Then it holds for all , that , , and

| (80) |

Proof of Lemma 4.4.

Note that for all , it holds that

| (81) |

In addition, observe that for all , , it holds that

| (82) |

Hence, we obtain that for all , , it holds that

| (83) |

This ensures that for all , it holds that

| (84) |

Combining this with (81) proves that for all , it holds that

| (85) |

This demonstrates that for all , it holds that

| (86) |

The proof of Lemma 4.4 is thus completed. ∎

5 Appendix A: Special cases of the proposed algorithm

In this subsection we illustrate the general algorithm in Subsection 3.2 in several special cases. More specifically, in Subsections 5.1 and 5.2 we provide special choices for the functions , , and , , employed in (29) and in Subsections 5.3 and 5.4 we provide special choices for the function in (24).

5.1 Stochastic gradient descent (SGD)

Example 5.1.

Assume the setting in Subsection 3.2, let , and assume for all , , that

| (87) |

Then it holds for all that

| (88) |

5.2 Adaptive Moment Estimation (Adam) with mini-batches

In this subsection we illustrate how the so-called Adam optimizer (see [22]) can be employed in conjunction with the deep BSDE solver in Subsection 3.2 (cf. also Subsection 4.1 above).

Example 5.2.

Assume the setting in Subsection 3.2, assume that , let , , be the functions which satisfy for all , that

| (89) |

let , , , , let be the stochastic processes which satisfy for all that , and assume for all , , that

| (90) |

and

| (91) |

Then it holds for all that

| (92) |

5.3 Geometric Brownian motion

Example 5.3.

Assume the setting in Section 3.2, let , and assume for all , , that

| (93) |

Then it holds for all , that

| (94) |

5.4 Euler-Maruyama scheme

Example 5.4.

Assume the setting in Section 3.2, let and be functions, and assume for all , that

| (96) |

Then it holds for all , that

| (97) |

6 Appendix B: Python and Matlab source codes

6.1 Python source code for an implementation of the deep BSDE solver in the case of the Allen-Cahn PDE (35) in Subsection 4.2

6.2 Matlab source code for the Branching diffusion method used in Subsection 4.2

6.3 Matlab source code for the classical Monte Carlo method used in Subsection 4.3

Acknowledgements

Christian Beck and Sebastian Becker are gratefully acknowledged for useful suggestions regarding the implementation of the deep BSDE solver. This project has been partially supported through the Major Program of NNSFC under grant 91130005, the research grant ONR N00014-13-1-0338, and the research grant DOE DE-SC0009248.

References

- [1] Bellman, R. Dynamic programming. Princeton Landmarks in Mathematics. Princeton University Press, Princeton, NJ, 2010. Reprint of the 1957 edition, With a new introduction by Stuart Dreyfus.

- [2] Bender, C., and Denk, R. A forward scheme for backward SDEs. Stochastic Processes and their Applications 117, 12 (2007), 1793–1812.

- [3] Bender, C., Schweizer, N., and Zhuo, J. A primal-dual algorithm for BSDEs. arXiv:1310.3694 (2014), 36 pages.

- [4] Bergman, Y. Z. Option pricing with differential interest rates. Review of Financial Studies 8, 2 (1995), 475–500.

- [5] Briand, P., and Labart, C. Simulation of BSDEs by Wiener chaos expansion. Ann. Appl. Probab. 24, 3 (06 2014), 1129–1171.

- [6] Chassagneux, J.-F. Linear multistep schemes for BSDEs. SIAM J. Numer. Anal. 52, 6 (2014), 2815–2836.

- [7] Chassagneux, J.-F., and Richou, A. Numerical simulation of quadratic BSDEs. Ann. Appl. Probab. 26, 1 (2016), 262–304.

- [8] Crisan, D., and Manolarakis, K. Solving backward stochastic differential equations using the cubature method: Application to nonlinear pricing. SIAM Journal on Financial Mathematics 3, 1 (2012), 534–571.

- [9] Darbon, J., and Osher, S. Algorithms for overcoming the curse of dimensionality for certain Hamilton-Jacobi equations arising in control theory and elsewhere. Res. Math. Sci. 3 (2016), Paper No. 19, 26.

- [10] Debnath, L. Nonlinear partial differential equations for scientists and engineers, third ed. Birkhäuser/Springer, New York, 2012.

- [11] E, W., Hutzenthaler, M., Jentzen, A., and Kruse, T. On full history recursive multilevel Picard approximations and numerical approximations for high-dimensional nonlinear parabolic partial differential equations and high-dimensional nonlinear backward stochastic differential equations. arXiv:1607.03295 (2017), 46 pages.

- [12] Gobet, E., Lemor, J.-P., and Warin, X. A regression-based Monte Carlo method to solve backward stochastic differential equations. Ann. Appl. Probab. 15, 3 (2005), 2172–2202.

- [13] Gobet, E., and Turkedjiev, P. Linear regression MDP scheme for discrete backward stochastic differential equations under general conditions. Math. Comp. 85, 299 (2016), 1359–1391.

- [14] Gobet, E., and Turkedjiev, P. Adaptive importance sampling in least-squares Monte Carlo algorithms for backward stochastic differential equations. Stochastic Process. Appl. 127, 4 (2017), 1171–1203.

- [15] Goodfellow, I., Bengio, Y., and Courville, A. Deep Learning. MIT Press, 2016. http://www.deeplearningbook.org.

- [16] Han, J., and E, W. Deep Learning Approximation for Stochastic Control Problems. arXiv:1611.07422 (2016), 9 pages.

- [17] Henry-Labordère, P. Counterparty risk valuation: a marked branching diffusion approach. arXiv:1203.2369 (2012), 17 pages.

- [18] Henry-Labordère, P., Oudjane, N., Tan, X., Touzi, N., and Warin, X. Branching diffusion representation of semilinear PDEs and Monte Carlo approximation. arXiv:1603.01727 (2016), 30 pages.

- [19] Henry-Labordère, P., Tan, X., and Touzi, N. A numerical algorithm for a class of BSDEs via the branching process. Stochastic Process. Appl. 124, 2 (2014), 1112–1140.

- [20] Hinton, G. E., Deng, L., Yu, D., Dahl, G., Mohamed, A., Jaitly, N., Senior, A., Vanhoucke, V., Nguyen, P., Sainath, T., and Kingsbury, B. Deep neural networks for acoustic modeling in speech recognition. Signal Processing Magazine 29 (2012), 82–97.

- [21] Ioffe, S., and Szegedy, C. Batch normalization: accelerating deep network training by reducing internal covariate shift. Proceedings of The 32nd International Conference on Machine Learning (ICML), June 2015.

- [22] Kingma, D., and Ba, J. Adam: a method for stochastic optimization. Proceedings of the International Conference on Learning Representations (ICLR), May 2015.

- [23] Krizhevsky, A., Sutskever, I., and Hinton, G. E. Imagenet classification with deep convolutional neural networks. Advances in Neural Information Processing Systems 25 (2012), 1097–1105.

- [24] LeCun, Y., Bengio, Y., and Hinton, G. Deep learning. Nature 521 (2015), 436–444.

- [25] Pardoux, É., and Peng, S. Backward stochastic differential equations and quasilinear parabolic partial differential equations. In Stochastic partial differential equations and their applications (Charlotte, NC, 1991), vol. 176 of Lecture Notes in Control and Inform. Sci. Springer, Berlin, 1992, pp. 200–217.

- [26] Pardoux, É., and Peng, S. G. Adapted solution of a backward stochastic differential equation. Systems Control Lett. 14, 1 (1990), 55–61.

- [27] Pardoux, E., and Tang, S. Forward-backward stochastic differential equations and quasilinear parabolic PDEs. Probab. Theory Related Fields 114, 2 (1999), 123–150.

- [28] Peng, S. G. Probabilistic interpretation for systems of quasilinear parabolic partial differential equations. Stochastics Stochastics Rep. 37, 1-2 (1991), 61–74.