Efficient Rare-Event Simulation for Multiple Jump Events in Regularly Varying Random Walks and Compound Poisson Processes

Abstract

We propose a class of strongly efficient rare event simulation estimators for random walks and compound Poisson processes with a regularly varying increment/jump-size distribution in a general large deviations regime. Our estimator is based on an importance sampling strategy that hinges on the heavy-tailed sample path large deviations result recently established in [23]. The new estimators are straightforward to implement and can be used to systematically evaluate the probability of a wide range of rare events with bounded relative error. They are “universal” in the sense that a single importance sampling scheme applies to a very general class of rare events that arise in heavy-tailed systems. In particular, our estimators can deal with rare events that are caused by multiple big jumps (therefore, beyond the usual principle of a single big jump) as well as multidimensional processes such as the buffer content process of a queueing network. We illustrate the versatility of our approach with several applications that arise in the context of mathematical finance, actuarial science, and queueing theory.

1 Introduction

In this paper, we develop a strongly efficient importance sampling scheme for computing rare-event probabilities involving path functionals of heavy-tailed random walks and compound Poisson processes in a general large deviations regime. Heavy-tailed distributions play an important role in many man-made stochastic systems. For example, they accurately model inputs to computer and communications networks (see e.g. [17]), and they are an essential component of the description of many financial risk processes (see e.g. [14]).

We focus on stochastic processes with a regularly varying increment/jump-size distribution. The estimators produced with our sampling scheme are straightforward to implement and can be used to estimate the likelihood of a wide range of rare events with bounded relative error. In particular, such a single sampling scheme applies to a very general class of rare events whose occurrence is caused by one or several components in the system which exhibit extreme behavior, while the rest of the system is operating in “normal” circumstances (therefore, beyond the usual principle of a single big jump). In particular, our results apply to a large class of continuous functionals of multiple random walks and compound Poisson processes.

Our estimators are based on importance sampling, a Monte Carlo technique which consists in biasing the nominal distribution of the underlying process in order to induce the rare event of interest. The estimator is obtained by weighting each sample by the corresponding likelihood ratio in order to obtain unbiased estimators. Our goal is to find biasing techniques leading to estimators which have bounded coefficient of variation uniformly as the probability of the event of interest tends to zero in a suitable large deviations regime. A brief review of importance sampling and the notion of strong efficiency will be given later in this paper; for a more in-depth discussion, see [1].

The construction of our sampling scheme is driven by recently developed sample path large deviations results in [23] for regularly varying Lévy processes and random walks. Specifically, let , be a one-dimensional compensated compound Poisson process with unit arrival rate and a positive jump distribution that is regularly varying at infinity. Define , with . For a measurable set satisfying a specific topological property, the large deviations results derived in [23] establish that

where precise details can be found in Section 2 below. In practice, exact estimates are often demanded. Hence, we design a sampling scheme for rare events that take the form . We illustrate our approach with several applications that arise in the context of mathematical finance, actuarial science, and queueing theory.

In order to contextualize our contribution, let us provide a review of the theory and methods which are standard in rare event simulation settings similar to those studied in this paper.

In the context of stochastic processes with light-tailed characteristics, such as random walks with increments possessing a finite moment generating function in a neighborhood of the origin, large deviations theory can be used to bias the process of interest in order to induce the occurrence of the rare event in question. In fact, it is well known that a conventional type of proof of the asymptotic lower bound in large deviations analysis one can extract an exponential change of measure which can sometimes be proved to be efficient (for counterexamples see e.g. [18] and [19]). By connecting the design of efficient importance sampling estimators with a game theoretic formulation, [10], [11] and [12] provide the foundations for the use of large deviations theory in the construction and analysis of provably efficient rare event simulation estimators. Moreover, a weakly efficient “universal” sampler has been proposed by [13] for a general class of hitting sets in arbitrary Jackson network topologies.

The setting of stochastic processes with heavy-tailed increments brings up additional challenges compared to its light-tailed counterpart discussed in the previous paragraph. These challenges were exposed in [2]. First of all, typically, the asymptotic conditional distribution of any particular increment given the rare event of interest converges to the underlying nominal distribution. Intuitively, if a rare event is caused by a large jump that may occur in a single “unlucky” increment out of many possible alternatives, then the chance that any specific increment is precisely the unlucky one is, naturally, small. So, any particular increment is likely to behave “normally” and therefore, in contrast to the light-tailed setting, there is no direct way in which one might attempt to bias a particular increment in order to stir the process towards the rare event of interest.

Moreover, as pointed out in [2], the asymptotic description of the most likely way in which a rare event may occur, for example due to the presence of a single large jump, does not lead to a valid change of measure for importance sampling because it is possible that several large jumps (or no large jump at all) might actually produce the event of interest under the nominal dynamics of the system. In other words, the natural biasing mechanism induced by directly approximating the zero-variance importance sampling distribution in the heavy-tailed setting assigns zero probability to events which are possible under the nominal dynamics leading to an ill-defined likelihood ratio.

The use of state-dependent importance sampling provides a way to deal with these difficulties. In [4], the authors explain how approximating Doob’s -transform can lead to a feasible change of measure which produces a strongly efficient importance sampling estimator in the setting of first passage time probabilities for one dimensional random walks. A Lyapunov technique was introduced for the analysis of state-dependent importance sampling estimators. But the direct approximation of Doob’s -transform might be difficult to implement in higher dimensions both because of sampling implementation challenges and the evaluation of normalizing constants.

In the setting of one-dimensional compound sums of independent and identically distributed (i.i.d.) regularly varying random variables, [9] produced a state-dependent change of measure whose normalizing constant is straightforward to implement. Their idea can be described as follows: each increment is sampled by either the original measure or—with small probability, which is a design parameter—a different measure, which is essentially the original measure conditional on exhibiting a large jump. The advantage of the mixture samplers is that sampling implementation challenges and the evaluation of normalizing constants can often be addressed by choosing a suitable set of parameters.

Under the setting where the time horizon is growing in large and moderate deviation schemes, Blanchet and Liu show in [6] how to use Lyapunov inequalities to address both the parameter selection while enforcing a bounded relative error. A key step in the methodology is the construction of a suitable Lyapunov function (for an illustration of the technique in multidimensional settings, see [7]). Blanchet and Liu suggest using the type of fluid analysis which is prevalent in the large deviations literature of heavy-tailed stochastic processes (see e.g. [15] and [16]). However, the construction of the Lyapunov function and the verification of the Lyapunov inequality becomes highly non-trivial in settings involving multiple jumps and the presence of boundaries which are common in queueing systems, for an example of the types of complications which arise in queueing settings, see [5].

The idea of using mixtures, suggested in [9], is also used here. But, while [9] treats a particular one-dimensional setting involving a rare event that is caused by a single big jump during a bounded time horizon, our setting is more general. We allow for a wide range of events, which might be caused by multiple jumps during a growing time horizon in a large deviations scaling.

Recall that we are interested in estimating the probability . The concept behind our sampling scheme can be described as follows. Based on the large deviations results derived in [23], we construct first an auxiliary set that is closely related to the optimization problem given by (2.1) below. Then, given a fixed mixture probability parameter , we generate the sample path of under the nominal measure. And, with probability we generate the sample path of under the measure . Finally, as a consequence of applying the importance sampling technique, we scale our samplers with a suitable likelihood ratio given as in (3.3) below. It should be noted that the set can be as general as in the setting of [23]. Therefore, our methodological contribution in this paper addresses precisely those types of difficulties mentioned in the previous paragraphs, such as, multiple jumps, growing time horizon, avoiding the evaluation of normalizing constants, and by-passing the verification of Lyapunov inequalities. The advantages of our sampling scheme are that the new estimators are strongly efficient and straightforward to implement. Moreover, they are “universal” in the sense that a single importance sampling scheme applies to a very general class of rare events involving multiple jumps that arise in heavy-tailed systems. As a final remark, it should be mentioned that constructing the auxiliary set requires choosing a set of suitable parameters whose existence is guaranteed by the topological property we impose on . Hence, one of the main challenges is to select the set of parameters specifically for each application.

Our mathematical contributions in this paper can be summarized as follows.

-

•

We propose a simulation algorithm for estimating the rare-event probability of , together with a sampling scheme for given , which is based on a rejection sampling with an unconditional acceptance probability bounded away from zero as .

-

•

By showing the existence of the parameter , we prove the strong efficiency of our sampling scheme under a very general setting (see Assumption 2 below).

-

•

We showcase the versatility of the algorithm by illustrating the implementation of the proposed sampling scheme to the rare-events that arise in finance, actuarial science, and queueing theory.

-

•

Especially, in the application to queueing networks (see Section 6 below), we show that the tail index of the rare-event probability—which usually exhibit a complex boundary behavior due to the nonlinear nature of the associated Skorokhod mapping—can be determined by solving knapsack problem with nonlinear constraints.

The rest of the paper is organized as follows. Section 2 deals with basic background and notations required to state our contributions. Section 3 introduces our estimators and describes the main result. Applications and numerical implementations are discussed in Section 4, Section 5, and Section 6. All the proofs of results presented in this paper are given in Section 7.

2 Notations and preliminaries

2.1 Notations

We start with a summary of notations that will be employed in this paper. Let denote the set of non-negative integers, and let denote the set of non-negative real numbers. Let and denote the interior and the closure of , respectively. Let be the metric space of real-valued RCLL functions on , denoted by , equipped with the Skorokhod metric on that is defined by

where denotes the identity mapping, denotes the uniform metric, i.e., , and denotes the set of all strictly increasing, continuous bijections from to itself. Let denote the -fold product space of . Let denote the subset of functions in that are non-negative and nondecreasing in each coordinate. When it comes to the tail indices of a regularly varying distribution, we use (or in the multidimensional case) for the right tail and for the left tail. Let denote the subspace of consisting of non-decreasing step functions vanishing at time zero with jumps, and let denote the subspace of consisting of non-decreasing step functions vanishing at with at most jumps, i.e. . Define

where

and . Define a partial order on such that if and only if , where . Define

Let denote the subspace of the Skorokhod space consisting of step functions vanishing at the origin with exactly downward jumps and upward jumps. Define

where .

Given non-negative sequences of real numbers and , we write , and , if , and , respectively. Given two -valued functions and , we write , if there exists such that . For , , we write , if , for all . Let the cardinality of be denoted by or . Finally, let and denote the set of all -combinations and -permutations of a set , respectively. Note that and

To describe the efficiency of a rare-event simulation algorithm, we adopt a widely applied criterion, which requires that the relative mean squared error of the associated estimator is appropriately controlled. To be more precise, suppose that we are interested in a sequence of rare events , which becomes more and more rare as . For each , let be an unbiased estimator of the rare-event probability . is said to be strongly efficient if . In particular, strong efficiency implies that the number of simulation runs required to estimate the target probability to a given relative accuracy is bounded with respect to (w.r.t.) .

2.2 Preliminaries

As we will see, the simulation algorithm that we propose in this paper is constructed based on the asymptotic behavior of rare-event probabilities, therefore we review some well known large deviations results for scaled Lévy processes with heavy-tailed Lévy measures, introduced in [23]. To begin with, let be a Lévy process with Lévy measure , where is spectrally positive and regularly varying (at infinity) with index . Let denote the associated scaled process. Let denote the restriction of -fold product measure of to , where . For , define a (Borel) measure

where , are i.i.d. uniformly distributed on . Note that is concentrated on , i.e., . Moreover, we make the convention that is the Dirac measure concentrated on the zero function. The following result is useful in designing an efficient algorithm for rare events involving one-dimensional scaled processes. Throughout the rest of this paper, all measurable sets are understood to be Borel measurable.

Result 2.1 (Theorem 3.1 of [23]).

Suppose that is a measurable set. If is bounded away from , where , then we have that

As one can see in Section 5 and Section 6 below, plenty of applications can be interpreted as sample-path rare events in a multidimensional setting. Therefore, it is particularly interesting to consider large deviations results for multidimensional processes. Let be independent centered one-dimensional Lévy processes with spectrally positive Lévy measures , respectively, where each is regularly varying with index at infinity. Moreover, for the finite product of metric spaces, we use the maximum metric; i.e., we use for the product of metric spaces . Finally, for , we define (which is concentrated on ) as the product measure of

Result 2.2 states a large deviations result for dimensional process for .

Result 2.2 (Theorem 3.6 of [23]).

Suppose that is measurable. If is bounded away from , where

| (2.1) |

then we have that

Note that the assumption that is bounded away from guarantees the uniqueness of . Finally, we conclude this section with an extension of Result 2.2, which will be useful in constructing an efficient simulation algorithm for heavy-tailed random walks. Let , , be a random walk, set , , and define , . Let be as defined above. Similarly, let denote the restriction of -fold product measure of to , where . Let be the Dirac measure concentrated on the zero function. For each , define a measure (which is concentrated on )

where ’s and ’s are i.i.d. uniform on .

Result 2.3.

Suppose that is regularly varying with index and is regularly varying with index . Let be a measurable set bounded away from , where

| (2.2) |

Then

3 Main results

In this section we present our main results. Although the large deviations results reviewed in Section 2 are stated for Lévy processes, we focus on compensated compound Poisson process for simulation purposes. Let denote a -dimensional compensated compound Poisson process, and recall that is the scaled process with , . For a measurable set , we are interested in estimating the probability of the event , when is large. Note that, in view of the law of large numbers, one can expect that for ’s that are bounded away from the zero function, and hence, ’s are rare events for large ’s. In Section 3.1, we first illustrate the idea of our algorithm in the special case for , where the notations are simpler. In Section 3.2 we extend this result to general .

3.1 The one-dimensional case

Let be a one-dimensional compensated compound Poisson process with jump sizes . That is,

where is a Poisson process with arrival rate , and let denote the associated scaled process. Moreover, let be regularly varying of index . The following assumption is essential for analyzing the asymptotic behavior of the rare-event probability, and hence, deriving the strong efficiency of our estimator.

Assumption 1.

Let be a measurable set in . We assume that is bounded away from , where denotes the minimal number of upward jumps of a step function in . Moreover, assume that .

Remark 1.

As one can see in Section 4, 5, and 6, one of the typical settings that arises in applications is that the set can be written as a finite combination of unions and intersections of , where each is a continuous function, and all sets are subsets of a general topological space . If we denote this operation of taking unions and intersections by (i.e., ), then it holds that

Hence, holds if has positive Lebesque measure, where is defined by for , and

Analogously, one can derive a sufficient condition for (see Assumption 2 below). More details about this discussion can be found in Section 3.1 of [23].

We design a rare-event simulation algorithm that estimates the probability of efficiently, based on an importance sampling strategy. To construct an importance distribution, we introduce a constant and define , where is given by

In the construction of our rare-event simulation algorithm, we will take advantage of the fact that one can always choose so that is sufficiently “close” to . The specific choice of will be further discussed later in Section 4, 5, and 6 for concrete examples. Let denote the conditional distribution given . One should notice that . Moreover, by the Fubini-Tonelli’s theorem, a closed-form expression for is given by

| (3.1) |

From (3.1) one should recognize that can be interpreted as the event of a Poisson distributed random variable with rate crossing the level . Now, let be arbitrary but fixed. We propose an importance distribution that is absolutely continuous w.r.t. and is given by

| (3.2) |

We give here an algorithm for generating the sample path of under the probability measure . Since , we observe that

where satisfies . Note that can be computed, since

Hence, it remains to discuss sampling from . It turns out that we can proceed a rejection sampling, where drawing from the proposal distribution can be achieved as follows.

-

1.

Sample uniformly from ;

-

2.

sample each , , conditional on ;

-

3.

sample , , , under the nominal measure.

Note that the target density , defined by

can be bounded by , where

and hence,

Now, it is natural to accept with probability

Finally, we are able to formulate the pseudocode for generating the sample path of under in Algorithm 1. Moreover, we show in Proposition 3.1 that the expected running time of Algorithm 1 is uniformly bounded from above w.r.t. .

Proposition 3.1.

Let denote the expected running time of Algorithm 1. Under the assumption that is regularly varying of index , we have that is uniformly bounded from above w.r.t. , i.e. .

Proof.

See Section 7. ∎

In view of the observations we made so far, we propose an estimator for that is given by

| (3.3) |

Intuitively, an importance sampling technique is used to get more samples from the interesting region, by sampling from a distribution that overweights the important region. Based on this, the choice of can be “justified”, since is mimicking the asymptotic behavior of the probability of interest. However, as one can see in the proof of strong efficiency (see Theorem 3.6 below), we should analyze the second moment of our estimator to avoid “backfire”, yielding an estimator with larger or even infinite variance. It turns out that this intuition can be made rigorous by applying Result 2.1. We end this section with a theorem regarding to the strong efficiency of our estimator.

Theorem 3.2.

Proof.

Analogous to the proof of the more general Theorem 3.6 presented below, where the existence of is also discussed. ∎

3.2 Extension to general

In this section we extend the results in Section 3.1 to the case with arbitrary . To be precise, let be a superposition of independent compensated compound Poisson processes with upward jumps, where is a Poisson process with arrival rate , and

Moreover, let be regularly varying of index at infinity. Finally, let denote the corresponding scaled process. As we can see in Result 2.2, the large deviations results for depend heavily on the value of , where is as defined in (2.1). However, for , the grid satisfying is not unique in general. Therefore assuming being bounded away from is not sufficient for our purposes. The following assumption, which is slightly different from the one we made in Section 3.1, corresponds to the extension of Result 2.1 to Result 2.2.

Assumption 2.

Let be a measurable set. Assume that is bounded away from , where is the unique solution of the minimization problem given by (2.1). Moreover, assume that .

If the solution to (2.1) is not unique, we may partition . As in Section 3.1, we focus now on constructing the auxiliary set for the importance distribution. Define and . As one can see in the proof of Theorem 3.6, controlling the probability of should be taken into account in choosing the auxiliary set . In the one-dimensional case, letting mimic the optimal path leading to the rare event makes us capable of controlling the relative error of our estimator. However, the same strategy will fail in the multidimensional case, since the rare event can be reached through other feasible but not necessarily optimal paths. Thus, we require a more complicated construction of .

Definition 1.

Let be a measurable set in , and let denote the unique solution to (2.1). Let with for all , and define

| (3.4) |

where is the set of càdlàg functions on that have greater or equal to than number of jumps with size larger than in its -th coordinate, i.e.,

Remark 2.

Note that the cardinality of is finite. To design a strongly efficient simulation algorithm for estimating , we will take advantages of an important property of . That is, for all with being bounded away from , there exists an index , such that the path of in its -th coordinate is bounded away from , for every . An illustration of can be found in Figure 1.

Let and let be as defined in (3.2), following the same strategy as in Section 3.1 we propose an estimator that takes the same form as in (3.3). Before turning to the efficiency analysis of our estimator, we summarize the findings above in Algorithm 2.

Remark 3.

In order to complete our algorithm, we need to discuss the computation of , as well as the strategy of sampling from the conditional distribution . Since constructed in Definition 1 is the union of with , by the inclusion-exclusion principle, it is sufficient to discuss computing the probability of sets of the form , where is a finite collection of elements in . It turns out that the probability of such a set can be computed similarly as in Section 3.1. Based on this observation, we give the following proposition.

Proposition 3.3.

The probability of is equal to

where .

Proof.

See Section 7. ∎

Remark 4.

As in Section 3.1, we now discuss generating the sample path of under in the next step. To begin with, we need the following lemma, which shows that can be decomposed into finitely many disjoint sets.

Lemma 3.4.

Let . Let the elements in , denoted by , be ordered such that . Define

| (3.5) |

Then, we have that

Proof.

See Section 7. ∎

Lemma 3.4 shows that can be decomposed into finitely many disjoint sets. This implies that

where

and satisfies that

Hence, it remains to design a sampling scheme for generating the sample path of under (for details about generating multi-dimensional discrete random numbers, see e.g. [21]). Due to the special structure of , we are able to generate independently under . To see this, first note that sampling is trivial due to the discussion in Section 3.1. Define

and

for . By (3.5), we have that

where satisfies . Note that

Therefore, it suffices to consider sampling under . Again, we can proceed a similar approach as in Section 3.1:

-

1.

Sample uniformly from ;

-

2.

sample each , , conditional on ;

-

3.

sample , , , under the nominal measure.

-

4.

accept with probability

Finally, we are able to give the pseudocode of this sampling scheme in Algorithm 3 below. For its expected running time, an analogous result to Proposition 3.1 is formulated in Proposition 3.5.

Proposition 3.5.

Let denote the expected running time of Algorithm 3. Under the assumption that is regularly varying of index , for all , we have that is uniformly bounded from above w.r.t. , i.e. .

Proof.

Analogous to the proof Proposition 3.1. ∎

The discussion above shows that sampling from the conditional distribution is tractable. As we mentioned in the introduction, our estimator is straightforward to implement. Moreover, its strong efficiency, which is formulated in Theorem 3.6, can be proved based on Lemma 3.7. Without introducing any new notations, we formulate a corollary to address a special case, where it is sufficient to consider a smaller (in the sense of cardinality) set than as in Definition 1.

Theorem 3.6.

Proof.

See Section 7. ∎

Lemma 3.7.

Proof.

See Section 7. ∎

Corollary 3.8.

Along with Assumption 2, we assume additionally that there exists an index set and such that: for every , there exists satisfying . Set , where if and only if

-

•

satisfies that ; and

-

•

for every , we have that .

Setting with

there exists such that the estimator given by

is strongly efficient for estimating .

Remark 5.

Even though our simulation algorithm is constructed in the context of Poisson processes with positive jump distributions, it can be easily generalized to the case, where the jump distributions are regularly varying at both and (for details see the proof of Theorem 3.5 in [23] and the references therein).

3.3 Extension to random walks

Let , be a centered random walk with increments . Let be regularly varying with index and let be regularly varying with index . Define , , where

| (3.6) |

In this subsection, we want to design an efficient simulation algorithm for estimating the probability of . As in Section 3.1 and Section 3.2, we make the following assumption for the set .

Assumption 3.

Let be a measurable set. Assume that is bounded away from , where is the unique solution of the minimization problem given by (2.2). Moreover, assume that .

Then, we construct the auxiliary set as follows.

Definition 2.

Defining and , we propose an estimator for that is given by (3.3). Note that, computing , as well as generating the sample path under can be achieved by following similar strategies as in Section 3.1 and Section 3.2. Hence, the details are omitted (for examples, see Section 4 and Section 5 below). We state the strong efficiency of our estimator in the following theorem.

Theorem 3.9.

With the results presented in this section at hand, we are able to apply our general simulation algorithm to three examples in the next sections. These examples can be found in the applications of mathematical finance, actuarial science and queueing networks.

4 An application to finite-time ruin probabilities

Problem settings

Let , , be a centered random walk with increments . Moreover, let be regularly varying at with index . For , define

Additionally, we make a technical assumption that is not a multiple of . We are interested in computing . This probability is particularly interesting, since it is related to, for example, insurance, where huge claims may be reinsured and therefore are irrelevant in the sense of estimating the finite time ruin probability of an insurance company.

Large deviations results

The rare-event probability can be estimated efficiently using the technique introduced in Section 3. To see this, define

and , where for . Note that . Set . Intuitively, should be the key parameter, as it takes at least jumps of size to cross level . This intuition has been made rigorous by Rhee et al. in [23, Section 5.1], where the authors show that is bounded away from , and hence, .

Construction of

Since is bounded away from , we can set

and

where is the parameter that needs to be tuned. For the completeness of our algorithm, we give a closed-form expression for . Let denote the probability of , then we have that

| (4.1) |

where the latter representation in (4.1) is for numerical purposes.

Choice of

As we mentioned in Remark 3, a strategy of choosing the parameters needs to be discussed in the next step. From the proof of Theorem 3.6, it is sufficient to select such that . We propose to select such that , and that

| (4.2) |

In view of Theorem 3.9, it is sufficient to show that is bounded away from with satisfying (4.2). To see this, choose with . This implies that there exists satisfying and . In particular, there exists a homeomorphism satisfying

| (4.3) |

For , using (4.3) and the identity , we conclude that the following holds:

-

1.

, for every ; and

-

2.

there exists such that

This implies that

Moreover, for , every jump of should be bounded by after having jumps with size bigger than . Due to the fact that satisfies (4.2) and that is not a multiple of , we obtain the result by choosing sufficiently small.

Sampling from

Summarizing the discussion from previous paragraphs, we are able to propose a strongly efficient estimator for that is given by (3.3). As the last ingredient of our simulation algorithm, a strategy of sampling from () needs to be discussed. We use a similar strategy as in Algorithm 3 and formulate the pseudocode in Algorithm 4.

Numerical results

Finally, we investigate our algorithm numerically based on a concrete example. Let , where , i.e. follows a Pareto distribution with scale parameter and shape parameter . Let , and . In Table 1 we select , , and summarize the estimated probability and the level of precision (ratio between the radius of the 95% confidence interval and the estimated value) for different combinations of and (based on samples). We observe that, for different values of , the precision stays roughly constant as grows. This confirms our theoretical results.

|

||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|

|

|||||||||||||

|

||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

|

||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

|

||||||||||||||||||

|

|

|

|

|

|

|

5 An application in barrier option pricing

In this section we consider an application that arises in the context of financial mathematics; in particular we consider a down-in barrier option (see Section 11.3 in [26]).

Problem settings

Let , , be a centered random walk with increments . Let be regularly varying with index and let be regularly varying with index . Let , and be positive real numbers. We provide a strongly efficient estimator for the probability of

which can be interpreted as the chance of exercising a down-in barrier option. This application is interesting, since, as we will see, the large deviations behavior of is caused by two large jumps.

Large deviations results

To begin with, define

Obviously, we have that , where denotes the solution to (2.2). To verify the topological property of , we define by , and . Note that , and are continuous, therefore

is a closed set. By adapting the results in [23, Section 5.2], it can be shown that, for any arbitrary , and are bounded away from and , respectively. Hence, is bounded away from . Applying Result 2.3, we obtain that .

Construction of

Now we are in the framework of Theorem 3.9. Note that, by Definition 2, we have that , where

However, adapting the idea behind Corollary 3.8 together with the fact that is bounded away from both and , it is sufficient to consider . Hence, we can set

As we mentioned in the introduction, it is possible that estimators may be crafted specifically for the events of interest, in order to obtain (up to constant factors) better performance. Due to the fact that at least one downward jump should happen before upward jumps, without introducing new notations, we can modify such that

This implies that . By a straightforward computation, we obatin that

where and .

Choice of and

We discuss here the strategy of choosing the parameters and . From the proof of Theorem 3.6, it is sufficient to select , such that . Hence, we propose to choose and such that , and that

| (5.1) |

W.l.o.g. we assume that is the unique minimum of (5.1). It suffices to prove that is bounded away from . To show that with is bounded away from , choose with . This implies that there exists satisfying , where . In particular, there exists homeomorphism satisfying

| (5.2) |

Using (5.2) and the identity , we conclude that, for and , at least one of the following holds:

-

•

, for every ; or

-

•

, for every .

For , by (5.2) there exists such that

| (5.3) |

Moreover, we can assume that for satisfying . Otherwise is bounded by for satisfying . By choosing sufficiently small, this leads to a contradiction of that and is the minimum of (5.1). Hence, (5.3) implies that

Since , choosing sufficiently small we obtain the result. Similarly, it can be can shown that is bounded away from for .

Sampling from

Summarizing the discussion in the previous paragraphs, we are able to propose a strongly efficient estimator for that is given by (3.3). As in Section 4, a strategy of sampling from needs to be discussed. Even though is modified to obtain smaller relative error, a similar strategy as in Algorithm 3 can be used here. We formulate the pseudocode in Algorithm 5.

Numerical results

We end this section with a numerical investigation (based on samples). Let , where is a random variable with density function that is given by

where and . In the following example we choose , , and . In Table 2 we compare the estimated rare-event probability and precision w.r.t. different values of , and . We observe that the precision stays roughly constant as increases for different combinations of and , which suggests the strong efficiency of our estimator.

|

||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

6 An application to queueing networks

In this section, an application to queueing networks is considered. More specifically, the probability of the number of customers in a subset of the system crossing a high level is estimated. Although some particular cases exist that allow for an explicit analysis (see e.g. Section 13 in [8]), it is hard to come up with exact results for the distribution of the workload process in general. Hence, implementing our algorithm in such a context is particularly interesting.

6.1 Model description and preliminaries

To be specific, we consider a -dimensional stochastic fluid model. Suppose that jobs arrive to the -th station in the network according to a Poisson process with unit rate, which is denoted by and independent of for . Moreover, the -th arrival of the -th station brings a job of size . We are assuming that is a sequence of i.i.d. positive random vectors and that is independent of . Therefore, the total amount of external work that arrives to the -th station up to time is given by . Now, assume that the workload at the -th station is processed as a fluid by the server at a rate and that a proportion of the fluid processed by the -th station is routed to the -th server. Moreover, we assume that is a substochastic matrix with and that as . The dynamics of the model are expressed formally by the so-called Skorokhod map (for details see e.g. [24], [25], [20] etc.), that is defined in terms of a pair of processes satisfying a stochastic differential equation that we shall describe now. Let , , and denote the workload of the -th station at time , for given , we have that

| (6.1) |

where encodes the minimal amount of pushing required to keep non-negative. In order to describe how to characterize the solution to (6.1), we need to introduce some notations. Let with

i.e.,

and with . The following results summarize useful properties and characterizations of the Skorokhod mappings , , as well as the workload process .

Result 6.1 (Theorem 14.2.1, Theorem 14.2.5 and Theorem 14.2.7 of [27]).

For all , the mappings and are well-defined. Moreover, and are Lipschitz continuous w.r.t. both the uniform metric and the Skorokhod metric. If and , then solve the Skorokhod problem given by (6.1).

Result 6.2 (Lemma 14.3.3, Corollary 14.3.4 and Corollary 14.3.5 of [27]).

Let . For the discontinuity points of (denoted by ) and , we have that . Moreover, if has only positive jumps, then is continuous and .

Result 6.3 (Theorem 14.2.2 of [27]).

The regulator map can be characterized as the unique fixed point of the map , which is defined by

Result 6.4 (Consequence of Theorem 4.1 of [22]).

Let be a non-decreasing function such that . Then, for , we have that

and

for any .

Finally, we assume that the right tail of is regularly varying with index and that the stability condition holds, i.e. , where . Let and . Let be a binary vector, and let denote the index set encoded by , i.e., if . Set and . Define by and by . Moreover, let . We are interested in estimating the probability of . By Theorem 14.2.6 (iii) of [27], we have that , and hence it holds that

| (6.2) |

where and .

6.2 Large deviations results

To obtain the large deviations asymptotics for the rare-event probability as in (6.2), we proceed the following.

- •

- •

-

•

Finally, we derive a large deviations result for by applying Result 2.2.

We start with the optimization problem given by (2.1). Due to the fact that is in general not a compensated compound Poisson process but one with certain drift, it is convenient to consider a slightly different problem, which is given by

| (6.3) |

where , due to the stability condition, and . Define and , where denotes the unit vector with entries except for the -th coordinate. By Result 6.2, instead of (6.3) we can solve two separate problems that are given by

| (6.4) |

and

| (6.5) |

Note that the optimization problem given by (6.5) can be solved easily by considering , therefore we focus on the optimization problem given by (6.4). Let be a subset of . Moreover, let and let be such that

| (6.6) |

A necessary and sufficient condition for the existence of is given in the following Proposition.

Proposition 6.1.

Let . Moreover, let be such that

| (6.7) |

Define

| (6.8) |

If , then there exists satisfying (6.6) and , if and only if . Additionally, if , then we have that .

Proof.

We give here a sketch of the proof, where a detailed one can be found in Section 7. Note that given by (6.8) is the increasing rate of the subset of the workload process, whose associated input process does not have any jumps but starts with sufficiently large initial value. Based on this observation, a can be constructed for the “if”-part of the first statement. For the “only if”-part, suppose that there exists a satisfying . By Result 6.4, enlarging the size of jumps in will preserve the fact that . Hence, we can construct a new , such that

-

•

the associated workload process is piecewise linear between two neighboring discontinuity points; and

-

•

the increasing rate of is always smaller or equal than given by (6.8).

∎

Remark 6.

Note that (6.7) can be written in a matrix notation that is given by

where and denote the vector and matrix respectively with its -th row and column being removed for all . Using the Banach fixed-point theorem, we obtain that , where and .

Define and

where is as defined in (6.8) with denoting the index set encoded by . By Proposition 6.1, we conclude that the optimization problem formulated in (6.4) is equivalent to

| (6.9) |

Thanks to the last statement of Proposition 6.1, it is unnecessary to check every for solving (6.9). Although, the optimization problem formulated in (6.9) is a nonstandard knapsack problem with nonlinear constraints. In the following example, we consider a specific fluid network and illustrate how to solve the optimization problem given by (6.9) using Proposition 6.1.

Example 1.

Consider the fluid network given by , and

We are interested in the probability of the rare event that the third station crosses the level at time for large , i.e. . It is easy to check that the stability condition holds. By an easy computation, we obtain that and . For , the optimal solution to (6.9) is given by .

Suppose that we have solved the optimization problem given by (6.9). To obtain the large deviations results, the following technical assumption needs to be made.

Assumption 4.

By Result 2.2, Assumption 4 c) implies that the rare event is caused by multiple large jumps. Throughout the rest of this section, we assume that Assumption 4 holds. We end this subsection with a large deviations result for , which is formulated in the following proposition.

Proposition 6.2.

Proof.

See Section 7. ∎

6.3 Simulation

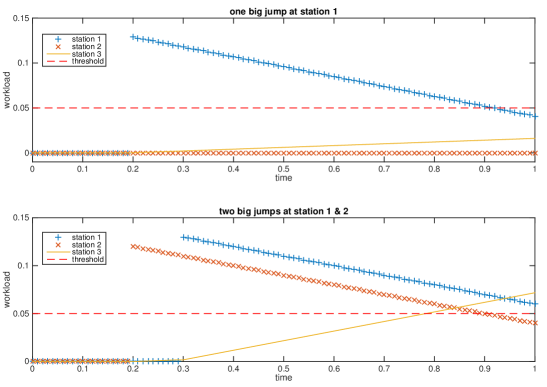

Again, we are in the setting of Theorem 3.6. To be able to discuss the choice of and the parameter in a more precise context, let us consider the stochastic fluid network introduced in Example 1.

Example 1 (continued).

Recall that, for , the optimal solution of (6.3) is given by , if we assume that . Moreover, it can be easily shown that is bounded away from both and . Combining this with , as well as Corollary 3.8, it is sufficient to take . This implies that

and hence

We choose such that . To begin with, we assume w.l.o.g. that , otherwise we can simply set , since . Now the parameter can be chosen such that

For the choice of , we observe that the job arriving at the second station can have arbitrarily large size. Hence, it is sufficient to consider the inequality , where and . Solving the inequality we obtain that . This simply means that the workload process of the third station cannot exceed the level at time if we keep both of the first and the second stations overloaded less than of the time. Since the workload process of the first station decays at rate , one can choose such that

Analogously, it is sufficient to set such that

We give a closed-form expression for . By assumption are mutually independent, therefore we have that

Conditional on , we obtain that

Summarizing the findings from above, we are able to propose a strongly efficient estimator for that is given by

Moreover, Algorithm 3 can be used to sample from . To see this, we decompose into two disjoint sets and that are given by

and

respectively. Using Algorithm 3, the sample path of can be simulated independently on both and . We present the numerical results based on samples in Table 3. We choose such that and , for . As one can see, the numerical results suggest again what our theory predicts.

|

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

|||||||||

|

||||||||||||

|

|

|

|

|

|||||||||

|

||||||||||||

|

|

|

|

|

7 Proofs

In this section we provide proofs of the results presented in this paper.

Proof of Proposition 3.1.

Proof of Proposition 3.3.

Let be as defined in (3.4). For , define

By the inclusion-exclusion principle, we have that

| (7.1) |

Moreover, for any finite collection of elements in with , we have that

| (7.2) |

where . Since are independent processes, we obtain that

∎

Proof of Lemma 3.4.

Recall that

Hence, we have that

| (7.3) |

By definition

Therefore, we have that

| (7.4) |

Plugging (7.4) into (7.3), we obtain that

Applying the same procedure to , we obtain that

Iterating the same procedure times, we obtain that

| (7.5) |

Since are ordered such that , we obtain that

| (7.6) |

Plugging (7.6) into (7.5), we obtain that

∎

Proof of Theorem 3.6.

For the second moment of (under the change of measure) we have that

Combining this with Lemma 3.7 we obtain the strong efficiency of our estimator.

∎

Proof of Lemma 3.7.

First, note that follows immediately from Result 2.2.

We need to show the existence of such that . Since is bounded away from by assumption, there exists such that . On the one hand, from [23] we have that

| (7.7) |

On the other hand, we have that

| (7.8) |

Let be a step function in the set . By (7.7), there exists , such that , and for all with . Combining with the fact that , we conclude that

| (7.9) |

or in other words, the sum of smallest jump is bounded from below by for each of satisfying . Combining (7.8) with (7.9), as well as choosing sufficiently small, there exists at least one such that the smallest jump of is bounded from below by for arbitrary but fixed . Repeating the same procedure as described above, we can construct for every , such that the optimization problem, given by

| (7.10) |

has a unique solution satisfying . We denote this specific choice of for every by . It should be noted that the existence and the uniqueness of can be guaranteed by enlarging the set (since we are looking for an upper bound for ), together with choosing the corresponding sufficiently small. Therefore, it remains to show that, under the chosen , the set is bounded away from . Select satisfying , and hence, there exists such that . On the one hand, combining with (7.7), there exists such that , for all . Hence, we have that , , satisfying

| (7.11) |

for all with . On the other hand, there exist homeomorphisms such that

| (7.12) |

for . Combining (7.12) with (7.8), we conclude the existence of at least one such that

| (7.13) |

Since , we have that

| (7.14) |

for all with . Finally, by (7.11), (7.13) and the choice of , we conclude that choosing sufficiently small leads to contradiction of (7.14). ∎

Proof of Proposition 6.1.

We derive a necessary and sufficient condition for with (6.6).

For the “only if”-part, suppose that . Let , and be such that

Obviously satisfies (6.6). For , by Result 6.3, the regulator process should satisfy the fixed point equation that is given by

Using the fact that , we obtain that , for . For , again by Result 6.3, it holds that

| (7.15) |

and

| (7.16) |

Since are non-negative, by Result 6.2, we conclude that , as well as are continuous in on . Using the Bolzano-Weierstrass theorem, there exists a set of sufficiently large (depending on ), such that for . Plugging this into (7.16) along with setting for , , we obtain that

| (7.17) |

Note that (7.17) is solved by satisfying (6.7). Moreover, by a straightforward computation, for the workload process , we obtain that . Since by assumption , we can choose such that .

For the other direction of the proof, suppose that for some satisfying (6.6). Let the jump sizes and the associated jump times of be denoted by and , respectively. First we should mention that, by Result 6.4, enlarging will preserve the fact that . Moreover, let denote the discontinuity points of with and define , for every . Now observe that , . Hence, we have that , for . For , , we can easily check that

by taking sufficiently large , where

Since , by Result 6.4 and (6.7), we conclude that , for . Defining , we consider for . Following a similar argument as above, we claim that

for sufficiently large , where

Consider the fixed point equation that is given by

| (7.18) |

Since , by Result 6.4, we obtain that , for every . By making the convention that for , we claim that , for . Since , by Result 6.4, (7.18) and (6.7), we conclude that , for . Iterating the same procedure more times, we can construct a (by taking sufficiently large) such that is piecewise linear between neighboring discontinuity points. Moreover, the increasing rate of is less than , i.e. , for . Therefore, we obtain that .

Proof of Proposition 6.2.

Let the unique optimal solution of (6.9) be denoted by . To prove that is bounded away from

it is sufficient to show that is bounded away from for all . To begin with, let . Under Assumption 4 we have that , where if and only if . Applying a similar approach as in the proof of Proposition 6.1, it can be shown that . This implies that there exists satisfying

| (7.19) |

Moreover, by Result 6.1 we conclude that the mapping as composition of Lipschitz continuous mappings (for continuity of see e.g. Theorem 12.5 in [3]) is again Lipschitz continuous. Let denote the Lipschitz constant of . Combining this with (7.19) we conclude that , hence the second statement is obtained by applying Result 2.2. ∎

References

- [1] S. Asmussen and P. Glynn. Stochastic simulation: Algorithms and analysis, volume 57 of Stochastic Modelling and Applied Probability. Springer-Verlag New York, 1st edition, 2007.

- [2] S. Asmussen, H. Schmidli, and V. Schmidt. Tail probabilities for non-standard risk and queueing processes with subexponential jumps. Advances in Applied Probability, 31(2):422–447, 1999.

- [3] P. Billingsley. Convergence of probability measures. John Wiley & Sons, 2013.

- [4] J. Blanchet and P. Glynn. Efficient rare-event simulation for the maximum of heavy-tailed random walks. The Annals of Applied Probability, 18(4):1351–1378, August 2008.

- [5] J. Blanchet, P. Glynn, and J. Liu. Efficient rare event simulation for heavy-tailed multiserver queues. Technical report, 2007.

- [6] J. Blanchet and J. Liu. State-dependent importance sampling for regularly varying random walks. Advances in Applied Probability, 40(4):1104–1128, Dezember 2008.

- [7] J. Blanchet and J. Liu. Efficient importance sampling in ruin problems for multidimensional regularly varying random walks. Journal of Applied Probability, 47(2):301–322, June 2010.

- [8] K. Debicki and M. Mandjes. Queues and Lévy Fluctuation Theory. Universitext. Springer International Publishing, 1st edition, 2015.

- [9] P. Dupuis, K. Leder, and H. Wang. Importance sampling for sums of random variables with regularly varying tails. ACM Transitions on Modeling and Computer Simulation, 17(3), July 2007.

- [10] P. Dupuis, A. D. Sezer, and H. Wang. Dynamic importance sampling for queueing networks. The Annals of Applied Probability, 17(4):1306–1346, August 2007.

- [11] P. Dupuis and H. Wang. Importance sampling, large deviations, and differential games. Stochastics and Stochastic Reports, 76(6):481–508, 2004.

- [12] P. Dupuis and H. Wang. On the convergence from discrete to continuous time in an optimal stopping problem. The Annals of Applied Probability, 15(2):1339–1366, 2005.

- [13] P. Dupuis and H. Wang. Importance sampling for Jackson networks. Queueing Systems, 62(1):113–157, 2009.

- [14] P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling extremal events for insurance and finance, volume 33 of Stochastic Modelling and Applied Probability. Springer-Verlag Berlin Heidelberg, 1st edition, 1997.

- [15] S. Foss and D. Korshunov. Heavy tails in multi-server queue. Queueing Systems: Theory and Applications, 52(1):31–48, January 2006.

- [16] S. Foss and D. Korshunov. On large delays in multi-server queues with heavy tails. Mathematics of Operations Research, 37(2):201–218, 2012.

- [17] S. Foss, D. Korshunov, and S. Zachary. An introduction to heavy-tailed and subexponential distributions, volume 38 of Springer Series in Operations Research and Financial Engineering. Springer-Verlag New York, 2nd edition, 2013.

- [18] P. Glasserman and S.-G. Kou. Analysis of an importance sampling estimator for tandem queues. ACM Transactions on Modeling and Computer Simulation, 5(1):22–42, January 1995.

- [19] P. Glasserman and Y. Wang. Counterexamples in importance sampling for large deviations probabilities. The Annals of Applied Probability, 7(3):731–746, August 1997.

- [20] J. M. Harrison and M. I. Reiman. Reflected Brownian motion on an orthant. The Annals of Probability, 9(2):302–308, April 1981.

- [21] X. Hu and H. Cui. Generating multi-dimensional discrete distribution random number. In 2010 Sixth International Conference on Natural Computation, volume 3, pages 1102–1104, August 2010.

- [22] S. Ramasubramanian. A subsidy-surplus model and the skorokhod problem in an orthant. Mathematics of Operations Research, 25(3):509–538, 2000.

- [23] C.-H. Rhee, J. Blanchet, and B. Zwart. Sample path large deviations for heavy-tailed Lévy processes and random walks. eprint arXiv:1606.02795, 2016.

- [24] A. V. Skorokhod. Stochastic equations for diffusion processes in a bounded region. Theory of Probability & Its Applications, 6(3):264–274, 1961.

- [25] A. V. Skorokhod. Stochastic equations for diffusion processes in a bounded region. II. Theory of Probability & Its Applications, 7(1):3–23, 1962.

- [26] P. Tankov and R. Cont. Financial Modelling with Jump Processes, Second Edition. Chapman and Hall/CRC Financial Mathematics Series. Taylor & Francis, 2nd edition, 2015.

- [27] W. Whitt. Stochastic-Process Limits. Springer Series in Operations Research and Financial Engineering. Springer-Verlag New York, 1st edition, 2002.