Credit card fraud detection through parenclitic network analysis

Abstract

The detection of frauds in credit card transactions is a major topic in financial research, of profound economic implications. While this has hitherto been tackled through data analysis techniques, the resemblances between this and other problems, like the design of recommendation systems and of diagnostic / prognostic medical tools, suggest that a complex network approach may yield important benefits. In this contribution we present a first hybrid data mining / complex network classification algorithm, able to detect illegal instances in a real card transaction data set. It is based on a recently proposed network reconstruction algorithm that allows creating representations of the deviation of one instance from a reference group. We show how the inclusion of features extracted from the network data representation improves the score obtained by a standard, neural network-based classification algorithm; and additionally how this combined approach can outperform a commercial fraud detection system in specific operation niches. Beyond these specific results, this contribution represents a new example on how complex networks and data mining can be integrated as complementary tools, with the former providing a view to data beyond the capabilities of the latter.

I Introduction

Credit card frauds, a concept included in the wider notion of financial frauds Ngai et al. (2011); West and Bhattacharya (2016), is a topic attracting an increasing attention from the scientific community. This is due, on the one hand, to the raising costs that they generate for the system, reaching billions of dollars in yearly losses and a percentage loss of revenues equal to the of online payments Bhatla et al. (2003). On the other hand, credit card frauds have important social consequences and ramifications, as they support organised crime, terrorism funding and international narcotics trafficking - see Rollins and Wilson (2006) for a complete review.

Detecting unauthorised credit card transactions is an extremely complex problem, as features are seldom useful if taken individually. To illustrate, a large transaction is not prima facie suspicious, unless it is performed at usual times (e.g. at night) or in an unusual store (i.e. a store never visited before by the card owner, located in a different city, etc.). When different features have to be combined in non-trivial ways, the customary solution is to resort to data mining, a sub-field of computer science dealing with the automatic discovery of patterns in data sets Friedman et al. (2001); Han et al. (2011); Witten et al. (2016). Most of the data mining models to detect credit card frauds are based on artificial neural networks (ANN), a model inspired on the structural aspects of biological neural networks, and in which a set of nodes process the input signal by interacting between them Zurada (1992); Hagan et al. (1996). This does not come as a surprise, as ANN are able to extract complex non-linear patterns from data, with almost no hypotheses on the underlying structure. ANN yielded good results in credit card classification tasks, as for instance in Ghosh and Reilly (1994); Aleskerov et al. (1997); Brause et al. (1999); Maes et al. (2002); Syeda et al. (2002); Carneiro et al. (2015) - see Bhattacharyya et al. (2011); Sethi and Gera (2014); Zojaji et al. (2016) for reviews.

While data mining algorithms are able to detect hidden patterns in data, they usually lack the capacity of synthesising metrics describing the global structure created by the interactions between the different features. In recent years, the use of complex networks theory has been proposed as a way of overcoming this limitation. Complex networks are a statistical-mechanics understanding of the classical graph theory, aimed at describing and characterising the structure of complex systems Strogatz (2001); Albert and Barabási (2002); Boccaletti et al. (2006). The interaction between network theory and data mining is bidirectional: the former can be used to synthesise high-level features to be fed into a classification problem; while the latter can endow networks with an objective way of validating results - see Zanin et al. (2016a) for a complete review.

More specifically, complex networks and data mining can be integrated as complementary tools in order to extract, synthesise and create new representations of a data source, with the aim of, for instance, discover new hidden patterns in a complex structure. The appropriate integration of complex network metrics can result in improved classification rates with respect to classical data mining algorithms and, reciprocally, there are many situations in which data mining can be used to solve important issues in complex network theory and applications Zanin et al. (2016a).

In this contribution we explore the possibility of using complex networks as a way of improving credit card fraud detection. Specifically, networks are used to synthesise complex features representing card transactions, relying on the recently proposed approach of parenclitic networks (Section II). Afterwards, their relevance is evaluated by means of a large dataset of real transactions, by comparing the yielded increase in the classification score when compared to the use of a standard ANN algorithm (Section III). We additionally show that the combined data mining / complex networks approach is able to outperform a commercial system in some specific situations.

II Methods

In this section we present the main tools that are going to be used for the classification of credit card transactions between licit and illicit. Given a credit card transaction with features , the problem entails detecting if it is illicit or not from its features and the knowledge obtained from an historical training dataset - what is known as a supervised learning problem. From a mathematical point of view, we have to model a function and find such that if , then is not illicit. Note that, while there are multiple types of illicit patterns, such aspect is here not considered, in that any suspicious transaction is considered as a potential fraudulent one.

We firstly introduce the concept of parenclitic networks in Section II.1, a network reconstruction technique that allows highlighting the differences between one instance and a set of standard (i.e. baseline, or in this case licit) instances Zanin and Boccaletti (2011); Zanin et al. (2014a). We subsequently describe the real data set used for validation (Section II.2), including the available raw features (Table 2); and the global classification model (Section II.3).

II.1 Parenclitic networks reconstruction

As initially proposed in Zanin and Boccaletti (2011), one may hypothesise that the right classification of an observation does not only come from its features, but also from the structure of correlations between them. Following the mathematica formalism introduced before, if we consider the set

then is a manifold in such that if we take a (new) transaction with features such that , then is considered as an illicit transaction. In general it is computationally impossible to obtain the set directly from the training dataset, since it is a high dimensional problem. As an alternative, the parenclitic approach analyses the family of projections of into 2-dimensional spaces corresponding to couples of features with . Hence, if we consider a training dataset with transactions, each of them described by (numeric) features, we can analyse up to two-dimensional projections of pairs of different features, each of them with up to points in . In order to quantify the correlation between pairs of features, the parenclitic approach proposes associating a network to each transaction with nodes (as many as features considered) and the links measure the correlation between features Zanin et al. (2014a). Hence the following pre-processing must be completed: for every two-dimensional projection of given by a couple of features with , the correlation for the licit transactions in the training dataset is measured (by means of, for instance, a linear regression or other curve fitting techniques). For the shake of simplicity, we have here considered a linear regression, such that every pair of features with yields a linear fitting between and for the licit transactions in the training dataset. Mathematically, this is represented by a linear equation of the form:

Once these linear regression lines are computed, a threshold is fixed. Given a new (i.e. not included in the training set) transaction with features , a network is associated to as follows:

-

•

has nodes ,

-

•

For every pair of nodes we compute as the (euclidian) distance from to the line in , i.e.

As an alternative, the euclidian distance could be replaced by any pseudo-distance function in . For the shake of simplicity, the euclidian distance will be used in this paper, but similar results can be obtained for other pseudo-distance functions.

-

•

For every pair of nodes , the (undirected) link is in graph if and only if .

Note that the parenclitic network summarises the couples of features whose correlation strongly differs from a typical licit transaction; the structure of this network thus contains valuable information about the (abnormal) correlation of features in the credit card transaction. Once this parenclitic network is computed, it is necessary to transform it in a set of features compatible with a data mining algorithm. Towards this end, several structural measures have been extracted, and will be considered as new features associated with the transaction (see next section for details). Among all possible structural measures that could be computed (see, for example, Ref. Costa et al. (2007) and references therein), those here selected are summarised in Table 1.

| Name | Description |

|---|---|

| Maximum node degree Costa et al. (2007) | Maximum degree of all nodes in the network. It is calculated as , being the degree of nodes |

| Entropy of the degree distribution Wang et al. (2006) | Shannon entropy of the distribution of nodes degrees. It is given by , being the probability of finding a node of degree . |

| Assortativity Costa et al. (2007) | Pearson’s correlation coefficient between the degree of connected nodes. |

| Clustering coefficient Costa et al. (2007) | Measure of the presence of triangles in the network. It is defined as the number of triangles (groups of three fully-connected nodes) over the number of connected triplets (groups of three nodes connected by at least two links). |

| Geodesic distance Costa et al. (2007) | Average length of the shortest path connecting pairs of nodes. |

| Efficiency Latora and Marchiori (2001) | Inverse of the harmonic mean of the length of all shortest distances. |

| Information Content Zanin et al. (2014b) | Metric assessing the presence of meso-scale structures in the network. |

II.2 Data set description

The data set here considered includes all credit and debit card transactions of clients of the Spanish bank BBVA, from January 2011 to December 2012. Each month, an average of million operations were realized by million cards, for a total of GB of information.

Transactions are automatically screened by an algorithm designed to detect suspected transactions, and returning a score from (no suspect) to (potentially illegal). Afterwards, transactions are classified in two categories, i.e. legal and illegal, as the result of a manual classification performed by the bank’s legal personnel - using both information of the automatic algorithm, and customers’ complaints. This allows us to detect which transactions were positively detected as frauds by the automatic algorithm, and which were false negatives.

Available fields included a time stamp of the operation, the quantity (both in Euro and in the original currency, if different), and the origin (the card) and destination (the store) of the operation; the two latter fields were anonymised, so that the exact card number and the name of the store could not be recovered. Some additional features have been synthesised from the previous ones, e.g. the average transaction size of a given user. A full list of the available fields is reported in Tab 2. Additionally, a full statistical characterisation of the features can be found in Ref. Zanin et al. (2016b), including the temporal evolution of the structure of the transactions network.

| Name | Type | Description |

| Transaction size | Integer | Size, in Euro, of the transaction under analysis. |

| Time since last transaction | Integer | Time, in seconds, since the last transaction of the same card. |

| Last transaction size | Integer | Size, in Euro, of the previous transaction executed by the same card. |

| Average transaction size | Float | Average size, in Euro, of the transactions executed by the card in the last month. |

| Average time between transactions | Float | Average time, in seconds, between consecutive transactions of the same card. |

| Same shop | Boolean | is the shop corresponds to the one of the last transaction of the same card, otherwise. |

| Hour of the day | Integer | Hour (from to ) at which the operation was realised. |

| Fraud rate | Float | Average rate of illegal operations, for all cards, in the last transactions. |

| Fraud suspectness | Integer | Number representing the likelihood for the transaction to be illicit, according to the bank automatic fraud detection algorithm. Values range between (no fraud suspected) to (certain fraud). |

| Fraud | Boolean | if the transaction has been recognised as a fraud, otherwise. |

II.3 Classification models

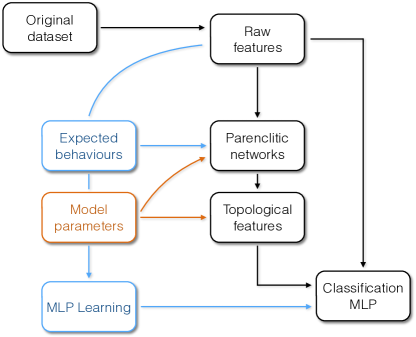

As previously introduced, in this contribution we are going to explore two different ways of detecting illicit credit card transactions: a classical data mining approach, and the introduction of features extracted from a network representation. In both cases, the process must follow some common steps: it is first necessary to extract the expected behavior, i.e. a set of features representing the typical legal and illegal transaction; for then building a model that learns from those features, and yields an expected classification for a new transaction not yet studied.

Fig. 1 depicts an overview of the whole process. It starts from the original data set, from which a set of raw features are extracted - as described in Section II.2 and listed in Tab. 2. The features corresponding to the licit transactions are then used to recover the normal relations, as described in Section II.1, and to reconstruct the parenclitic networks of all transactions. These networks are then binarised, i.e. links with weight below a given threshold are deleted, and a set of topological metrics are extracted - see Table 1 for a complete list. Note that, at the end of this analysis, all transactions are described by features: coming from the raw data, and from the network analysis.

Artificial Neural Networks (ANNs), and specifically Muti-Layer Perceptrons (MLP) have been chosen as the final model for classifying new transactions. They are inspired by the structural aspects of biological neural networks, and are represented by a set of connected nodes in which each connection has a weight associated with it, and the network learns the classification function adjusting the node weights Rosenblatt (1958); Hagan et al. (1996). The output of each artificial neuron is defined by:

| (1) |

being the vector of weights, and the sigmoid activation function:

| (2) |

Following the standard configuration, neurons were organized in three layers: an input one, with a number of neurons equal to the input features; an intermediate, or hidden one, with ten neurons; and a final output layer comprising just one computational element. The training has been performed with the standard back-propagation algorithm Werbos (1974). Finally, the reconstruction of the MLP models has been performed using the KNIME software Berthold et al. (2009).

The evaluation of the classification efficiency has been performed using both sensitivity (also known as True Positive Rate - TPR) and Receiver Operating Characteristic (ROC) curves Hanley and McNeil (1982). These curves are created by plotting the True Positive Rate (TPR) against the False Positive Rate (FPR) at various threshold settings. ROC plots present the important advantage of showing the performance of the classification model for different sensitivity values. This is relevant for the problem at hand, as false positives are extremely expensive, e.g. in terms of the negative commercial image of the bank; conservative solutions are therefore usually preferred.

III Results

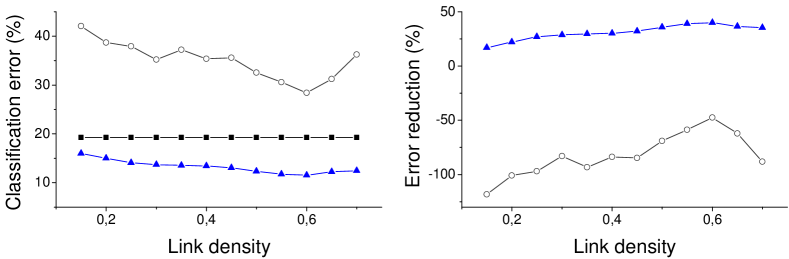

As explained in Section II.1, the parenclitic approach usually requires the definition of a threshold , which is used to binarise the (initially weighted) networks. Instead of using an a priori approach, i.e. the definition of using expert judgement, we here tackle the problem indirectly, by following the procedure proposed in Ref. Zanin et al. (2012). Specifically, we optimise the network reconstruction by finding the link density (and hence the value of ) that optimises the efficacy of the classification model.

Fig. 2 Left presents the evolution of the classification error (sensitivity or TPR) as a function of the considered link density, for three different scenarios: the use of only the raw features, as described in Tab. 2 (solid black squares); the use of the features extracted from the parenclitic representation alone (hollow black circles); and the use of the combined sets of features (solid blue triangles). Note that, in the former case, the result is constant, as the original features are not affected by the binarisation process. In order to avoid overfitting, this classification has been performed on a balanced sub data set, composed of an equal number of legal and illegal transactions.

Several conclusions can be drawn from Fig. 2. First of all, the features extracted from the parenclitic networks are not enough, alone, to reach a low classification error. This has to be expected: while important information can be codified in the interaction between raw features, some important clues may be hidden in the latter, e.g. abnormal transaction sizes or timings. At the same time, the addition of parenclitic features to the raw data set enhance the obtained results, with the error dropping from a to a . This is further illustrated in Fig. 2 Right, depicting the reduction in the classification error (in percentage) when considering only parenclitic features and the whole data set - note that, in the first case, the reduction is negative as the error increases. Finally, the best classification suggests that the optimal link density that should be considered is of a - meaning that the of links with less weight should be deleted.

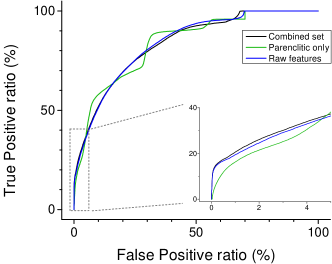

If Fig. 2 is useful to detect the best link density for the analysis, it does not convey information about the real performance of the classification algorithm in an operational environment. For that, Fig. 3 Left presents three ROC curves, corresponding to the use of raw (blue line), parenclitic (green line), and combined features (black line) as before. Note that results here presented correspond to the optimal link density of , as previously estimated. As previously discussed, the most interesting operational configuration is the one minimising the number of false positives, as this minimises the commercial costs of the organisation. The inset of Fig. 3 thus shows the bottom left part of the curves. It can be appreciated that, after an initial part in which results are comparable, the addition of the parenclitic features slightly increases the number of true positives - note how the black line is above the blue one. Even though this may seem a negligible difference, it is worth noting that any improvement, however small, has a significant impact due to the large number of transactions managed by the system. Increasing the fraud detection rate by would allow identify new illicit transactions per year, or M€ in saved costs.

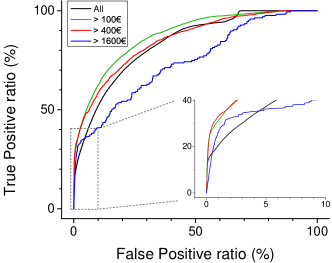

Fig. 3 Right further presents four ROC curves calculated for different transaction sizes: all transactions (black line), and transactions above € (green line), € (red line) and € (blue line). Deleting small transactions results in an improvement of the detection efficiency - note how the green and red lines lay above the black one. Additionally, the proposed algorithm fails for large transactions; this does not come as a surprise, as the larger the size, the fewer the available instances, making training more challenging.

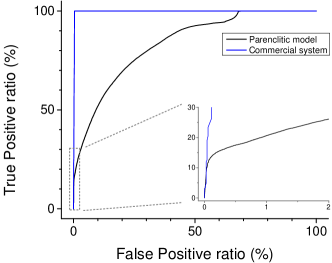

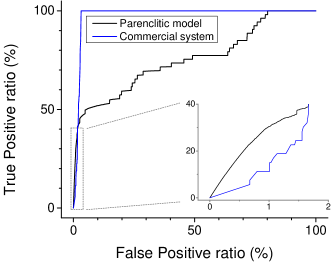

If what previously presented illustrates that the use of a network representation can improve a fraud detection algorithm, it does not clarify how it ranks against a commercial system. As may be expected, the proposed algorithm is less efficient than the fraud score included in the original data set - see Fig. 4 Left111Due to confidentiality issues, the name and characteristics of the commercial fraud detection system cannot be included in this publication.. Nevertheless, there are niches in which the opposite happens, the most important being the analysis of on-line transactions. Fig. 4 Right depicts two ROC curves, respectively for the algorithm based on parenclitic networks (black line) and the commercial system (blue line), when only transactions realised through Internet are considered. While the commercial system clearly outperforms the proposed algorithm, with an Area Under the Curve (AUC) close to , the latter is slightly better for a low ratio of False Positive - as previously explained, the plane region most interesting for real operations.

IV Conclusions

Complex networks and data mining models share more characteristics that what may prima facie appear, most notably having similar objectives: both aim at extracting information from (potentially complex) systems to ultimately generate new compact quantifiable representations. At the same time, they approach this common problem from two different approaches: the former by extracting and quantitatively evaluating the underlying structure, the latter by creating predictive models based on historical data Zanin et al. (2016a). In this contribution we test the hypothesis that complex networks can be used as a way to improve data mining models, framed within the problem of detecting fraud instances in credit card transactions, providing a new example about how complex networks and data mining may be integrated as complementary tools in a synergistic manner in order to improve the classification rates obtained by classical data mining algorithms.

Results confirm that features extracted from a network-based representation of data, leveraging on a recently proposed parenclitic approach Zanin and Boccaletti (2011); Zanin et al. (2014a), can play an important role: while not effective in themselves, such features can improve the score obtained by a standard ANN classification model. We further show how the resulting model is especially efficient in detecting frauds in some niches of operations, like medium-sized and on-line transactions. Finally, we illustrate as, in the latter case, the network-based model is able to yield better results than a commercial fraud detection system. All results have been obtained with a unique data set, comprising all transactions managed during two years by a major Spanish bank, and including more than million operations.

References

- Ngai et al. (2011) E. Ngai, Y. Hu, Y. Wong, Y. Chen, and X. Sun, Decision Support Systems 50, 559 (2011).

- West and Bhattacharya (2016) J. West and M. Bhattacharya, Computers & Security 57, 47 (2016).

- Bhatla et al. (2003) T. P. Bhatla, V. Prabhu, and A. Dua, Cards business review 1 (2003).

- Rollins and Wilson (2006) J. Rollins and C. Wilson, “Terrorist capabilities for cyberattack: Overview and policy issues,” (2006).

- Friedman et al. (2001) J. Friedman, T. Hastie, and R. Tibshirani, The elements of statistical learning, Vol. 1 (Springer series in statistics Springer, Berlin, 2001).

- Han et al. (2011) J. Han, J. Pei, and M. Kamber, Data mining: concepts and techniques (Elsevier, 2011).

- Witten et al. (2016) I. H. Witten, E. Frank, M. A. Hall, and C. J. Pal, Data Mining: Practical machine learning tools and techniques (Morgan Kaufmann, 2016).

- Zurada (1992) J. M. Zurada, Introduction to artificial neural systems, Vol. 8 (West St. Paul, 1992).

- Hagan et al. (1996) M. T. Hagan, H. B. Demuth, and M. H. Beale, Neural network design (Pws Pub. Boston, 1996).

- Ghosh and Reilly (1994) S. Ghosh and D. L. Reilly, in System Sciences, 1994. Proceedings of the Twenty-Seventh Hawaii International Conference on, Vol. 3 (IEEE, 1994) pp. 621–630.

- Aleskerov et al. (1997) E. Aleskerov, B. Freisleben, and B. Rao, in Computational Intelligence for Financial Engineering (CIFEr), 1997., Proceedings of the IEEE/IAFE 1997 (IEEE, 1997) pp. 220–226.

- Brause et al. (1999) R. Brause, T. Langsdorf, and M. Hepp, in Tools with Artificial Intelligence, 1999. Proceedings. 11th IEEE International Conference on (IEEE, 1999) pp. 103–106.

- Maes et al. (2002) S. Maes, K. Tuyls, B. Vanschoenwinkel, and B. Manderick, in Proceedings of the 1st international naiso congress on neuro fuzzy technologies (2002) pp. 261–270.

- Syeda et al. (2002) M. Syeda, Y.-Q. Zhang, and Y. Pan, in Fuzzy Systems, 2002. FUZZ-IEEE’02. Proceedings of the 2002 IEEE International Conference on, Vol. 1 (IEEE, 2002) pp. 572–577.

- Carneiro et al. (2015) E. M. Carneiro, L. A. V. Dias, A. M. da Cunha, and L. F. S. Mialaret, in Information Technology-New Generations (ITNG), 2015 12th International Conference on (IEEE, 2015) pp. 122–126.

- Bhattacharyya et al. (2011) S. Bhattacharyya, S. Jha, K. Tharakunnel, and J. C. Westland, Decision Support Systems 50, 602 (2011).

- Sethi and Gera (2014) N. Sethi and A. Gera, International Journal of Computer Science and Mobile Computing 3, 780 (2014).

- Zojaji et al. (2016) Z. Zojaji, R. E. Atani, A. H. Monadjemi, et al., arXiv preprint arXiv:1611.06439 (2016).

- Strogatz (2001) S. H. Strogatz, Nature 410, 268 (2001).

- Albert and Barabási (2002) R. Albert and A.-L. Barabási, Reviews of modern physics 74, 47 (2002).

- Boccaletti et al. (2006) S. Boccaletti, V. Latora, Y. Moreno, M. Chavez, and D.-U. Hwang, Physics reports 424, 175 (2006).

- Zanin et al. (2016a) M. Zanin, D. Papo, P. A. Sousa, E. Menasalvas, A. Nicchi, E. Kubik, and S. Boccaletti, Physics Reports 635, 1 (2016a).

- Zanin and Boccaletti (2011) M. Zanin and S. Boccaletti, Chaos: An Interdisciplinary Journal of Nonlinear Science 21, 033103 (2011).

- Zanin et al. (2014a) M. Zanin, J. M. Alcazar, J. V. Carbajosa, M. G. Paez, D. Papo, P. Sousa, E. Menasalvas, and S. Boccaletti, Scientific reports 4 (2014a).

- Costa et al. (2007) L. d. F. Costa, F. A. Rodrigues, G. Travieso, and P. R. Villas Boas, Advances in Physics 56, 167 (2007).

- Wang et al. (2006) B. Wang, H. Tang, C. Guo, and Z. Xiu, Physica A: Statistical Mechanics and its Applications 363, 591 (2006).

- Latora and Marchiori (2001) V. Latora and M. Marchiori, Physical review letters 87, 198701 (2001).

- Zanin et al. (2014b) M. Zanin, P. A. Sousa, and E. Menasalvas, EPL (Europhysics Letters) 106, 30001 (2014b).

- Zanin et al. (2016b) M. Zanin, D. Papo, M. Romance, R. Criado, and S. Moral, Physica A 462, 134 (2016b).

- Rosenblatt (1958) F. Rosenblatt, Psychological Review 65, 386 (1958).

- Werbos (1974) P. Werbos, Beyond Regression: New Tools for Prediction and Analysis in the Behavioral Sciences, Ph.D. thesis, Harvard University (1974).

- Berthold et al. (2009) M. R. Berthold, N. Cebron, F. Dill, T. R. Gabriel, T. Kötter, T. Meinl, P. Ohl, K. Thiel, and B. Wiswedel, AcM SIGKDD explorations Newsletter 11, 26 (2009).

- Hanley and McNeil (1982) J. A. Hanley and B. J. McNeil, Radiology 143, 29 (1982).

- Zanin et al. (2012) M. Zanin, P. Sousa, D. Papo, R. Bajo, J. García-Prieto, F. del Pozo, E. Menasalvas, and S. Boccaletti, Scientific reports 2, 630 (2012).

- Note (1) Due to confidentiality issues, the name and characteristics of the commercial fraud detection system cannot be included in this publication.