Moral hazard in welfare economics: on the advantage of Planner’s advices to manage employees’ actions.111This work is supported by the ANR project Pacman, ANR-16-CE05-0027 and the Chair Financial Risks (Risk Foundation, sponsored by Soci t G n rale).

Abstract: In this paper, we study moral hazard problems in contract theory by adding an exogenous Planner to manage the actions of many Agents hired by a Principal. We provide conditions ensuring that Pareto optima exist for the Agents using the scalarization method associated with the multi-objective optimization problem and we solve the problem of the Principal by finding optimal remunerations given to the Agents. We illustrate our study with a linear-quadratic model by comparing the results obtained when we add a Planner in the Principal/multi-Agents problem with the results obtained in the classical second-best case. More particularly in this example, we give necessary and sufficient conditions ensuring that Pareto optima are Nash equilibria and we prove that the Principal takes the benefit of the action of the Planner in some cases.

Key words: Moral hazard, Nash equilibrium, Pareto efficiency, multi-objective optimization problems, BSDEs.

AMS 2000 subject classifications: Primary: 91A06, 91B40. Secondary: 91B15, 91B10, 91B69, 93E20.

JEL subject classifications: C61, C73, D60, D82, D86, J33, O21.

1 Introduction

In 1992, Maastricht treaty, considered as the key stage in the European Union construction, proposed the establishment of a single currency for its members to ensure a stability of prices inside the EU. This date marks the birth of the euro, as the common currency of the eurozone, with the creation of the European Institut Monetary to ensure the introduction of it, which has operated until the creation in 1998 of a central bank for Europe, the European Central Bank. The ECB is the decision-making center of the Eurosystem, which is one of the main component of the EU (see for instance [38, Chapter 5, Section 2.5] for a description of its general role inside the EU) to ensure the economical smooth functioning of the eurozone, and Maastricht Treaty contains some criteria that member states are supposed to respect. For instance, the Article 104-C stipulates that "Member States shall avoid excessive government deficits" and some criteria to respect it concern the Government budget balance, which does not have to exceed 3% of the GDP and the debt-to-GDP ratio, which does not have to exceed 60%. If these benchmarks are exceeded, through the Stability and Growth Pact, members of eurozone have accepted to follow a precise procedure each year to reduce their debt. Even before the financial crisis of 2007-2008, these rules have been discussed (see [33]), and since the Greek government-debt crisis this controversy has been amplified.333See for instance (see [13, 12, 20, 24]). The fact is that the eurozone is very heterogeneous in the respect of Maastricht criteria as showed in Table 1.

| EU members | gov. deficit/surplus in % of GDP | debt-to-GDP ratio in % |

|---|---|---|

| Estonia | +0.1 | 10.1 |

| Finland | -2.8 | 63.6 |

| France | -3.5 | 96.2 |

| Germany | +0.7 | 71.2 |

| Greece | -7.5 | 177.4 |

| Ireland | -1.9 | 78.6 |

| Italie | -2.6 | 132.3 |

| Lithuania | -0.2 | 38.7 |

| Spain | -5.1 | 99.8 |

| Euro area (19 countries) | -2.1 | 90.4 |

The natural questions arising are the following:

-

a.

How the ECB can provide incentives to EU members to respect the rules induced by Maastricht treaty? Which kind of procedure is the more efficient?

-

b.

How EU members have to interact for the welfare of the European Union?

The Greek government crisis has impacted all the eurozone and showed that members are strongly correlated each others. Through this example we see that one difficulty of both the ECB and eurozone members is to reach an optimal decision and equilibria to succeed in the global european construction.

The example above, and more specially the problem a., describes the kind of investigations made in the incentives theory starting in the 70’s (see among others [28, 29]) and is an illustration of a Principal/Agent problem. More exactly, the classical framework considered is the following: a Principal (she) aims at proposing to an Agent (he) a contract. The Agent can accept or reject the contract proposed by the Principal and under acceptance conditions, he will provide a work to manage the wealth of the Principal. However, the Principal is potentially imperfectly informed about the actions of the Agent, by observing only the result of his work without any direct access on it. The Principal thus designs a contract which maximizes her own utility by considering this asymmetry of information, given that the utility of the Agent is held to a given level (his reservation utility). From a game theory point of view, this class of problems can be identified with a Stackelberg game between the Principal and the Agents, i.e. the Principal anticipates the best-reaction effort of the Agent and takes it into account to maximize her utility. Moral hazard in contracting theory, i.e the Principal has no access on the work of her Agent, has been developed during the 80’s and was investigated in a particular continuous time framework by Holmström and Milgrom in [17]. We refer to the monographies of Laffont and Martimort [23], Laffont and Tirole [22], Sung [40] and Cvitanic and Zhang [8] for nice reviews of the literature in this topic and different situations studied dealing with moral hazard in Principal/Agent problems. More recently, the noticeable work of Sannikov [37] investigates a stopping time problem in contract theory by emphasizing the fundamental impact of the value function of the Agent’s problem to solve the problem of the Principal. This was then mathematically formalized with the works of Cvitanic, Possamaï and Touzi in [6, 7] by proposing a nice handleable procedure to solve a large panel of problems in moral hazard. More exactly, they have showed that the Stackelberg equilibrium between the Agent and the Principal may be reduced to two steps in the studying of general problems in contracts theory. First, given a fixed contract proposes by the Principal, the Agent aims at maximizing his utility by finding the best reaction effort associated with the proposed contract. It is well-known, since the works of Rouge and El Karoui [36] and Hu, Imkeller and Müller [18] that a utility maximization problem can be reduced to solve Backward Stochastic Differential Equations (BSDE for short, we refer to the works of Pardoux and Peng [31, 32] and El Karoui, Peng and Quenez [9] for general results related to this theory), and Cvitanic, Possamaï and Touzi have proved that more generally, when the Agent can control the volatility, the problem can be reduced to solve a second order BSDE (see for instance the seminal work [39] and the extension of it with more general conditions [34]). Then, it is proved in [6, 7] that the problem of the Principal can be reduced to solve a stochastic control problem with state variables of the problem the output and the value function of the Agent, by using the HJB equations associated with it and verification theorems.

An extension of moral hazard with a Principal and an Agent, which echoes the example of the ECB as the Principal and the EU members as the Agents presented above, consists in considering a Principal dealing with many Agents. Principal/Multi-Agents problems have been investigated in a one period framework by Hölmstrom [16] (among others) and then extended in the continuous time model by Koo, Shim and Sung in [21] and more recently by Elie and Possamaï in [11]. In the latter, Elie and Possamaï consider exponential utility functions for the Agents and the Principal and they assume that the Agents are rational so that the first step of the procedure to solve the Agents’ problems remains to find Nash equilibria, which can be reduced to solve a multi-dimensional quadratic BSDE, as explained in [11]. Nevertheless, by recalling the example of the ECB and EU members above with question b., we can also consider an other type of interactions between the Agents.

In microeconomics, we can distinguish two type of interactions between connected agents. Agents can be considered as rational economical entities and aim at finding their best reaction functions to maximize their wealths/minimize their costs, in view of the actions of the others. This investigation consists in finding a Nash equilibrium and fits with a situation in which the (non-cooperative) agents cannot deviate from this equilibrium. However, as explained with the so-called prisoner’s dilemma (see Table 2 for more explanation), the configuration obtained is not necessarily an optimal choice for the welfare of the system.

| keep silent | denounce | |

|---|---|---|

| keep silent | ||

| denounce |

Welfare economics is a part of microeconomics which aims at determining the degree of well-being of a situation and Pareto optima are considered as one criterion to measure it. Indeed, a Pareto optimum consists in finding a configuration in which all the considered entities cannot deviate without harming the state of an other entity. Unlike a Nash equilibrium, a Pareto optimum is not reached using dominant strategies but has to be imposed in a general situation, since rational entities will reasonably converge to a Nash equilibrium. Finding Pareto optima gives a lot of information in terms of general equilibrium inside a system of markets and supply/demand systems, as showed by (among others) Walras in [42] to explain price-setting mechanisms, and mathematically formulated by Arrow and Debreu in [3] with the celebrated two fundamental theorems of welfare economics. Roughly speaking, the first fundamental theorem of welfare economics states that any general equilibrium in a competitive market is (weakly) Pareto optimal. The second states that any Pareto optimum can lead to a general equilibrium by reallocating initial appropriations. We refer to [28, 2] and the monography [25] for more details on it. It is however444We for instance refer to [1] for an investigation of this kind of issues. not clear that with information asymmetry this equivalence is always true (specially the second fundamental theorem does not hold), but studying the existence of Pareto optima seems to be interesting to have relevant information related to general equilibrium in view of the first theorem. Moral hazard problems dealing with Pareto optimality was studied in a one-period model in [35] and in a two-period model in [30]. As far as we know, it does not have been investigated in continuous time models and the present paper is the first who considers it. Before going further, let us explain how we have to understand the Principal/multi-Agents problem studied in this work. Since the actions of Agents lead naturally to a Nash equilibrium (which does not coincides a priori with a Pareto optimum), we have to assume that the Agents cannot manage their work themselves or are forced to follow a precise strategy. This induces to introduce a third player in the Principal/multi-Agents game, namely the Planner, who imposes an effort to the Agents for their well-being. More specifically, the Planner can be seen as a mediator inside a firm who managed the actions of agents or a regulator who forces the Agents to act for the global interest. The Planer can be for instance a Government who imposes some Labour laws, by thinking about the global interest of the employees or any other entity who manages actions of Agents hired by a Principal. In this paper, we will distinguish the case where no Planner impacts the Stackelberg equilibrium, which coincides with the second best case in contract theory and where rational Agents reach to Nash equilibria, to the case in which a Planner manages the work of the Agents. The structure of the paper is the following:

After having described the Economy studied in Section 2, we extend the result of [11] to general separable utilities for the Agents, and general utilities for the Principal in Section 3 for the classical second-best case, named the no-Planner model. We provide conditions on the data ensuring that the multi-dimensional BSDE associated with Nash equilibria for the Agents is well-posed as an application of the recent results in [15] (see Appendix B and Remark 3.1). Then, in Section 4 we turn to the model in which a Planner manages the action of Agents. Using the fact that finding Pareto optima can be reduced to solve a Multi-Objective Optimization Problem (MOOP for short), we give general forms of some Pareto optima through the solutions of BSDEs and we solve the problem of the Principal using the HJB equation associated with it. Finally, in Section 5, we apply our results to a linear-quadratic model similar to the applied model studied in [11] with two Agents having appetence coefficients and we give some interpretations on the relevant results. We compare the no-Planner model with models in which a Planner intervenes in the Principal/multi-Agents problem by providing sufficient and necessary conditions such that a Nash equilibrium is Pareto efficient, and by comparing the value functions of the Principal.

2 The Economy

We consider a finite number of Agents hired by one Principal. Each Agent receives from the Principal a salary at a fixed horizon to manage the project of the Principal described by an valued process with volatility an valued map denoted by depending on the output , given by

| (2.1) |

where is an dimensional Brownian motion defined on some probability space filtred with the natural filtration of the Brownian motion . We assume in this paper that the volatility is uniformly bounded, the map is progressively measurable, invertible and such that (2.1) has a unique strong solution with exponential moments.

Remark 2.1.

The boundedness of is here for the sake of simplicity, while the invertibility is fundamental to define properly the weak formulation of the problem as explained in [11].

2.1 Impact of the actions of interacting agent

Let be a subset of . We assume that any agent can impact, with his effort, both the value of his assigned project and the values of the other projects. More explicitly, any th Agent has an impact on the th component on and on the other components managed by the other Agents. We represent the general action of the Agents by a matrix where is the action of the th Agent on the project . Thus, is the valued column vector of the th Agent’s actions. This matrix impacts555See Appendix A for mathematical details. the dynamic (2.1) of by adding a drift defined as a map from such that for any time , any space variable and any effort of the Agents, we have

For technical reasons, we have to focus on admissible actions of the Agents as a subspace of valued process for which the model is well-posed. We refer to Appendix A for a mathematical definition of it. Thus, under technical conditions given in the appendix, the dynamic of , impacted by any admissible actions of Agents, is given by

| (2.2) |

where

is a Brownian motion under some probability measure equivalent to . We thus work under the weak formulation of the problem (see [11, Sections 2.1 and 2.2] for more details on it).

Interpretation of (2.2).

We first focus on the dependance with respect to in both the volatility and the drift of the project. This classical phenomenon expresses some friction effects between the different projects managed by the Agents so that each component of the general outcome can depend on the values of the others. Turn now to the dependance with respect to the effort of the Agents. The dynamic of the project depends on all the efforts provided by the Agents and assuming that the th Agent has preferences depending on the th component of , this model emphasizes exactly an interacting effect between Agents since each Agent can impact positively or negatively the project managed by an other.

2.2 Stackelberg equilibrium, Nash equilibrium and Pareto optimality

It is well known that a moral hazard problem can be identified with a Stackelberg equilibrium between the Principal and the Agents. In the considered system, the first step consists in finding a best respond effort provided by the Agents given a sequence of salaries proposed by the Principal. In the second step, taking into account the reactions of the Agents, the Principal aims at maximizing her own utility.

We assume that each Agent is penalized through a cost function depending on his effort. More precisely, we denote by the cost function associated with the th Agent.

For any , we set the utility of the th Agent. We will consider in this paper separable utilities given a sequence of salaries given by the Principal and an admissible action chosen by the -Agents, such that

where is a concave and increasing map so that its inverse is well-defined and increasing, is the appetence function of Agent to manage project which satisfies a technical, but not too restrictive, assumption (see Assumption (G) in Appendix A). For instance, , where is the appetence of Agent toward the project compared to the other projects.

We recall that any Agent can accept or reject the contract proposed by the Principal through a reservation utility constrain. More exactly, we denote by a general set of admissible666See Appendix A for mathematical details with the definition of . contracts proposed by the Principal to the Agents, which remains to put technical assumptions ensuring that all the mathematical objects used in this paper are well-defined and such that for any panel of contracts the following reservation utility constrains are satisfied

| (2.3) |

with a reservation utility for the th Agent. We denote the vector of reservation utilities.

An interesting problem concerns the intrinsic type of best reaction efforts provided by the Agents. Two different approaches can be investigated.

One can assume that each Agent provides an optimal effort in view of the actions of the others. In this case, each Agent aims at finding a best reaction effort given both a salary proposed by the Principal and other Agents efforts. This situation typically fits with a non-cooperative game between Agents which reach to find stable equilibria of type Nash equilibria. This problem was well investigated in [11] by proving that Agents play an equilibrium in view of performance of others players. Mathematically777See paragraphs Notations and General model and definitions in Appendix A for the definitions of the operator and the space of admissible best reaction with (A.3)., we define a Nash equilibrium for the Agents by the following

Definition 2.1 (Nash equilibrium).

Given an admissible contract , a Nash equilibrium for the Agents is an admissible effort such that for any

| (2.4) |

The main problem of Nash equilibrium is that it is not optimal in general, from a welfare economics point of view, of interacting entities (see the prisoner’s dilema in Table 2). It is why in this paper we will mainly focus on Pareto optima, mathematically defined by

Definition 2.2 (Pareto optimum).

An admissible action is Pareto optimal if it does not exist such that for any and for at least one index .

The studied model coincides with a Principal/multi-Agents problem in which an exogenous entity, called the Planner, forces the Agents to act for the global interest. Given an optimal remuneration, the Planner aims at maximizing the global utility of the -Agents by finding a Pareto equilibrium. Then, taking the best reaction effort of the Agents into account, the Principal chooses among the set of contracts those who maximize her utility.

3 Some reminders on the no-Planner model

We assume that no Planner intervenes in the Stackelberg games between Agents and the Principal and we extend merely the main results in [11] to the case of separable utilities and we omit the proof since they follow exactly the same lines that [11]. In that case, we consider rational Agents reaching a Nash equilibrium given an admissible sequence of contracts , which corresponds to the classical second-best case. Intuitively, we begin to set the paradigm of any th Agent. Given a salary given by the Principal and an effort provided by the others, Agent aims at solving

| (3.1) |

Following the same computations than those in [11], by using martingale representation theorems, Problem (3.1) remains to solve

| (3.2) |

and by denoting the maximizer of the generator of this BSDE, we deduce that the -valued process is the best reaction effort of Agent given a salary and effort of the other players , where is the unique solution to BSDE (3.2), under technical assumption stated in Appendix A.

3.1 Nash equilibrium and multidimensional BSDE

Now, each Agent computes his best reaction effort at the same time. We thus have to assume that for any there exists a fixed point inspiring by the best reaction effort of Agent made before. We consider that the following assumption holds in the following

Assumption 3.1.

For any , there exists such that

We denote by the set of fixed point .

As emphasized by [11], finding a Nash equilibrium for any sequence of salaries is strongly linked to find a solution to the following multidimensional BSDE

Similarly to Theorem 4.1 in [11], we can now state that there is a one to one correspondance between a Nash equilibrium and a solution to BSDE (3.3). The proof of this result follows exactly the same lines that the proof of Theorem 4.1 in [11].

Theorem 3.1.

Remark 3.1.

The previous theorem emphasizes that the existence of a Nash equilibrium is connected to the existence of a unique solution in the sense of Definition 3.1. As explained in [14], for instance, the problem is mathematically ill-posed in general and [11] circumvents this problem by imposing the existence of a solution to BSDE (3.1) in the definition of admissible contracts. However, as soon as the class of admissible contracts is sufficiently regular, recent results [43, 15] can be applied to ensure that the multidimensional BSDE (3.3) is well-posed. We refer to Appendix B for more details on this class of admissible contracts and Proposition B.1 which gives conditions ensuring that their exists a unique solution in the sense of Definition 3.1 of this BSDE.

3.2 The problem of the Principal and multidimensional HJB equation

As previously, this section is very informal to allege the reading since it is a mere extension of [11] to separable and general utilities. The results are again completely similar to those in [11] and can be proved by following exactly the same lines. For the sake of readability, we prefer to omit it to focus on the proofs of Section 4 below, which is the real contribution of this paper.

Assume that BSDE (3.3) admits a unique solution for some . Let be a Nash equilibrium selected by the Agents (see [11, Section 4.1.4] for some selection criterion) or the Principal888In fact, if the Agents cannot select a Nash equilibrium, then the problem of the Principal is where is the restriction of with selection criterion for the Agents, and the results below are completely similar. It is why for the sake of simplicity, we assume that only one Nash equilibrium is selected here, to allege the reading. if the Agents cannot select it. Recall that the Principal aims at solving

| (3.4) |

As explained in [37, 6, 7], by mimicking [11, Section 4.2] and in view of the decomposition (3.3) of admissible contracts, one can show999See Section 4.2 which provides a path to do it or [11] for exponential utilities. that solving this problem remains to solve a stochastic control problem with two state variables: the value of the firm and the value function of the th Agent for any . This suggests to introduce the following Hamiltonian by

Thus, the HJB equation associated with (3.4) is

As usual, using a classical verification theorem (see for instance [41]) we get the following result

Theorem 3.2.

Assume that PDE (HJB-Na) admits a unique solution continuously differentiable with respect to and twice continuously differentiable with respect to its spaces variables and that for any , the supremum in is attained for (at least) one . Moreover, for any , we assume that the following coupled SDE

admits a unique solution where

If moreover and for any , then

is an optimal contract which solves the Principal problem (3.4) with

4 Multi Objective Optimization Problem with separable preferences

Assume now that the Agent does not manage their efforts which are chosen by an exogenous Planner who acts for the welfare of the Agents. We fix a sequence of admissible contracts . As before, in all this section, we work under technical assumptions on the coefficients given in Appendix A (see Assumption A.1).

4.1 Solving the multi objective problem using scalarization

Let be a sequence of nonnegative reals such that and consider the multi-objective optimization problem

| (4.1) |

The following proposition gives sufficient conditions to find Pareto optima through solutions to the MOOP.

Proposition 4.1 (Theorem 3.1.2 in [27]).

If their exists for any with such that the multi-objective optimization problem (4.1) has a solution denoted by , then is Pareto optimal.

The coefficient can be seen as the part chosen by the Planner of the utility of Agent to maximize the general weighted utility of the Agents.101010See [25, Proposition 16.F.1], can also be seen as the inverse of the marginal utility of Agent . Fix a sequence with . We set for any

Problem (4.1) thus becomes

| (4.2) |

with

We consider the following BSDE for any

| (4.3) |

We thus have the following Lemma, whose the proof is postponed to Appendix C

Lemma 4.1.

BSDE (4.3) admits a unique solution such that

Let be defined for any by

We define for any

We consider the following BSDE

| (4.4) |

The following result solves the problem of the Planner and we refer to Appendix C for its proof.

Theorem 4.1.

BSDE (4.4) admits a (unique) solution denoted by such that

and any in is Pareto optimal for any such that .

Remark 4.1.

Concerning the choice of the parameter by the Planner, one can assume that the Planner is penalized by a bad choice of Pareto optima given some external criteria. For instance, the Planner could be forced to choose a class of depending on the performance of any Agents relatively to the others, e.g. for some with the underlying cost of the Agent to manage project . Mathematically, the Planner aims at solving for instance

for some cost function depending on the characteristics of the Agents. An other section criterion could be to take any parameter and the corresponding Pareto optima which are Nash equilibria. Thus, we deal in the following with a parameter chosen by the Planner due to some selection criterions. If this is not unique, we assume that the Principal have the final say on this choice and maximizes her utility over all the selected Pareto optima. We also assume that in this case that is reduced to a singleton for the sake of simplicity (if not and as usual, the Principal also maximizes her utility on any Pareto optima with parameter ).

4.2 Characterization of the set of admissible contracts

Let be the (unique) solution to BSDE (4.4). We fix and the Pareto optimum in (reduced to a singleton for the sake of simplicity as explained in Remark 4.1). We consider the following BSDE

| (4.5) |

We thus have the fundamental following Proposition and we refer to Appendix C for its proof

Proposition 4.2.

In view of Proposition 4.2 above, we have

This suggests to introduce a set of contracts as the set of random variables with defined by

for any controls , where denotes the set of controls -predictable processes such that .

We set an -predictable process with values in such that its coefficient is the th element of the vector process . In this case we define the -valued process

by setting (with an abuse of notation but justified by Proposition 4.2)

| (4.7) |

with and

In this case, from Proposition 4.2, we get111111The inclusion is in the definition of . The inclusion comes from (4.2) by using martingale representation.

| (4.8) |

In the following we will denote the set of -predictable process with values in such that for any .

4.3 The general problem of the Principal with an exogenous Planner

Using the notation (4.7), we recall that the Principal solves

| (4.9) |

From Proposition 4.2 and Characterization (4.8), Problem (4.9) becomes

| (4.10) |

Since and are increasing, one can explicitly get the optimal for any by saturating the reservation utility constrains of the Agents, i.e., . Thus, Problem (4.10) becomes

| (4.11) |

As emphasized above and as an extension of [37, 6, 7], solving (4.11) remains to solve a stochastic control problem with

-

•

control variable: ,

-

•

two state variables: the value of the firm and the value function of the th Agent for any .

We define by

We thus consider the following HJB equation associated with (4.11)

As usual, using a classical verification theorem (see for instance [41]) we get the following result

Theorem 4.2.

Assume that PDE (HJB-Par) admits a unique solution continuously differentiable with respect to and twice continuously differentiable with respect to its spaces variables and that for any , the supremum in is attained for (at least) one . Moreover, for any , we assume that the following coupled SDE

admits a unique solution where

If moreover then

is an optimal contract which solves the Principal problem (4.9), with

5 Application to a bidimensional linear-quadratic model

We compare the case where a Planner intervenes in the Stackelberg equilibrium between the Principal and the Agent with the case in which no-Planner acts in the linear-quadratic model developed in [11].

5.1 The model and characterization of Pareto optima

Let , and .

action of Agent on the project with

We also assume that their exists such that for any

with

Then, for any parameter with , we have for any

5.2 Problem of the Principal under the action of a general Planner

We get

where and and with, by setting

One can show after tedious but easy computations that is coercive in and and convexe. The first order conditions are then given by

This implies to distinguish or not.

5.2.1 Pareto optima and Optimal contracts with an exogenous Planner

For any fixed by an exogenous Planner, (FOC) gives

By maximizing the function , we get the following general Pareto optima conditions

Thus, given a Pareto optimum of parameter chosen by the Planner, the optimal contracts given to Agent 1 and Agent 2 are respectively

and

Notice that admits a maximum in . We can deduce that the case coincides with a cooperative Planner with the Principal.

Remark 5.1.

In fact, notice that has a continuous extension when or , which corresponds to weak Pareto optima (see [27, Theorem 3.1.1]). In this case, we set

5.2.2 Pareto optimum with a cooperative Planner

It remains to the case where the Planner and the Principal cooperate by choosing .

The first order conditions (FOC) induces the following Pareto optima conditions

with

We thus have the following optimal contracts for Agent 1 and Agent 2 respectively

and

Interpretations.

-

We find the first-best effort cf [11, Theorem 3.3.] which is both a Nash equilibrium in the first best model and a Pareto optimum with a cooperative Planner.

-

We get in the case of a cooperative Planner infinitely number of optimal contracts which differs clearly form the classical case and results in [11].

-

If and , i.e. Agent is more efficient that Agent to manage his project and to help Agent to manage his project. Take each Agent strictly will receive the value of his own project. Fixed part is greater for Agent than for Agent .

-

If , i.e. Agent is more efficient with project than Agent , the part of the project given to Agent is greater than the part of this project given to Agent and depend of the relative performance of this Agent compared to the others. We get similar results with project .

-

Notice that for any Pareto coefficients, the optimal effort of each Agent is always a booster of each project. At the equilibrium, each Agent does not penalize the project of the others. This phenomenon indeed appears as soon as the appetence coefficients are different for Agent 1 and Agent 2 as emphazised in [11].

-

Finally, notice that at the optimum, the appetence parameter does not impact the value function of the Principal and optimal efforts. More exactly, in this model the Principal proposes optimal contracts to the Agents which cancelled their ambitious in their works and such that ambitions of the Agents have no impact on the value of the Principal. Besides, we recover the suppression of the appetence for competitions of the Agent by the Principal since she penalizes each th Agent with the amount , , as in [11].

5.2.3 Comparison with the no-Planner model

We now turn to a comparison between a model in which a Planner manages the effort of the Agents and a model in which Agents are rational entities who aim at finding a Nash equilibrium. Using [11] and results of Section 3, the Nash equilibrium is given for any by

The problem of the Principal is then to solve

We get

with

Noticing that is coercive and convexe, one get from the first order conditions the following solutions

In this case, optimal contracts are given by

and

The result below gives necessary and sufficient conditions for which the Nash equilibrium coincides with a Pareto equilibrium.

Proposition 5.1 (Suffisant and necessary conditions).

Assume that is convex. The Nash equilibrium is a Pareto optimum if and only if there exists such that

In this case coincides with Pareto optimum with parameter .

Proof.

Since is convex, we notice that is concave since is linear and is convex with respect to and by using comparison of BSDEs (see [5] for instance). Thus, finding a Pareto equilibrium is equivalent to find such that their exists a solution of the multi-objective problem from [27, Theorem 3.1.7].

Now, a Nash equilibrium is Pareto optimal if and only if there exists such that

By rewriting these conditions, we get the result. ∎

Toy models in which Nash equilibrium are Pareto optimal.

-

•

The Nash equilibrium is Pareto efficient with if and only if (the Principal is risk-neutral).

-

•

Assume that and , i.e. the cost of the effort of the Agent is the same towards the project or the project . In this case, we necessarily have

Then, the Nash equilibrium coincides with a Pareto optimum with parameter if and only if

We now turn to a last interesting results remaining to say that the Principal can benefit from the action of a Planner to broke the Stackelberg game between her and her Agents.

Proposition 5.2 (Advantage of adding a Planner).

There exists a (non-empty) set of parameters such that for any , i.e. adding a Planner can improve the value of the Principal.

Moreover, and . In other words, a Planner choosing weak Pareto optima does not improve the value function of the Principal compared to a no-Planner model.

Proof.

For any , notice that . Thus,

Thus, by using the continuity with respect to of , we deduce that there exists a set such that and for any .

A tedious computation shows that is decreasing, and

Thus, by using Remark 5.1, easy computations directly give and ∎

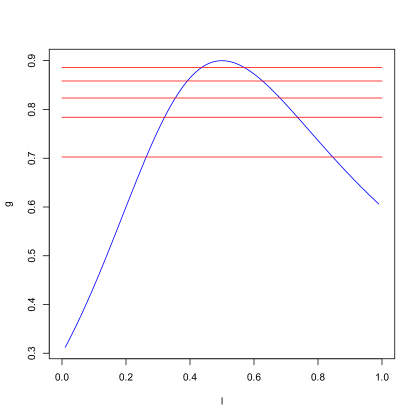

We illustrate this proposition with the Figure 1 below. Notice that has the same monotonicity than . Thus comparing with is enough to compare the value functions of the Principal with and without a Planner. We notice in particular that the length of the set is decreasing with the risk aversion of the Principal.

6 Conclusion

In this paper, we have proved that in a linear-quadratic model there exists configurations such that Nash equilibria are Pareto efficient (see Proposition 5.1). We also have seen that it is sometimes advantageous from the Principal point of view, to add a Planner in the model who imposes Pareto optimal actions to the Agents, compared to the case in which the Agents are rational, non-cooperative, and compute themselves their best-reaction effort (see Proposition 5.2). On the contrary, if the Planner chooses a weak Pareto optimum, then the value of the Principal is always worse than a no-Planner model. We would like to propose some extensions to this work for the path of future researches which might also be worth investigating.

First extension will consist in the studying of classical exponential utilities for the Agents. The main issue of this work is indeed that we assume that Agents are risk neutral in the application in order to make all the computations. In this case, we do not fit with separable utilities and the scalarization method proposed to solve the problem does not work. An other approach which could be considered should be to use other methods to find Pareto optima, see for instance [27], more tractable for exponential utilities.

The second extension is directly linked to Remark 4.1 since the natural question which is not considered in the present work is to wonder what is happening if the Planner is not exogenous in the sense that he is also hired by the Principal. In this case, the Planner has to be seen as a consulting mediator which aims at finding Pareto optima and which is remunerated by the Principal. This required to modify the classical Stackelberg-type approach by adding this third player in the game.

7 Acknowlegments

The author is very grateful to François Delarue for having suggested to do this study during a discussion and for his advices together with Dylan Possamaï for his general advices in the writing of this paper. The author also thanks Miquel Oliu-Barton and Patrick Beißner for discussions on welfare economics and Pareto efficiency.

References

- [1] D. Acemoglu and A. Simsek. Moral hazard and efficiency in general equilibrium with anonymous trading MIT Department of Economics Working Paper No. 10-8, 2010.

- [2] R. Arnott and J. Stiglitz. The welfare economics of moral hazard. In Risk, information and insurance, pages 91–121. Springer, 1991.

- [3] K. J Arrow and G. Debreu. Existence of an equilibrium for a competitive economy. Econometrica: Journal of the Econometric Society, pages 265–290, 1954.

- [4] P. Briand and Y. Hu. BSDE with quadratic growth and unbounded terminal value. Probability Theory and Related Fields, 136(4):604–618, 2006.

- [5] P. Briand and Y. Hu. Quadratic BSDEs with convex generators and unbounded terminal conditions. Probability Theory and Related Fields, 141(3-4):543–567, 2008.

- [6] J. Cvitanić, D. Possamaï, and N. Touzi. Moral hazard in dynamic risk management. Management Science, to appear, 2014.

- [7] J. Cvitanić, D. Possamaï, and N. Touzi. Dynamic programming approach to principal–agent problems. arXiv preprint arXiv:1510.07111v3, 2017.

- [8] J. Cvitanić and J. Zhang. Contract theory in continuous–time models. Springer, 2012.

- [9] N. El Karoui, S. Peng, and M.-C. Quenez. Backward stochastic differential equations in finance. Mathematical Finance, 7(1):1–71, 1997.

- [10] R. Élie, T. Mastrolia, and D. Possamaï. A tale of a principal and many many agents. arXiv preprint arXiv:1608.05226, 2016.

- [11] R. Élie and D. Possamaï. Contracting theory with competitive interacting agents. arXiv preprint arXiv:1605.08099, 2016.

- [12] A. Feertchak and G. Poingt. Présidentielle : faut-il remettre en cause les 3% de déficit public? Le Figaro, March 2017.

- [13] B. Fofana. La règle des 3% de déficit des états est-elle un "non-sens"? Libération, February, 2017.

- [14] C. Frei and G. Dos Reis. A financial market with interacting investors: does an equilibrium exist? Mathematics and financial economics, 4(3):161–182, 2011.

- [15] J. Harter and A. Richou. A stability approach for solving multidimensional quadratic BSDEs. arXiv preprint arXiv:1606.08627, 2016.

- [16] B. Holmström. Moral hazard in teams. The Bell Journal of Economics, 13(2):324–340, 1982.

- [17] B. Holmström and P. Milgrom. Aggregation and linearity in the provision of intertemporal incentives. Econometrica, 55(2):303–328, 1987.

- [18] Y. Hu, P. Imkeller, M. Müller. Utility maximization in incomplete markets. The Annals of Applied Probability, 15(3):1691–1712, 2005.

- [19] N. Kazamaki. Continuous exponential martingales and BMO. Springer, 2006.

- [20] M. Khan. How the european central bank became the real villain of greece’s debt drama. The Telegraph, May 2015.

- [21] H.K. Koo, G. Shim, and J. Sung. Optimal multi–agent performance measures for team contracts. Mathematical Finance, 18(4):649–667, 2008.

- [22] J.J. Laffont, and J. Tirole. A Theory of Incentives in Procurement and Regulation. MIT press, 1993.

- [23] J.J. Laffont, and D. Martimort. The theory of incentives: the principal-agent model. Princeton University Press, Princeton, 2001.

- [24] N. KA Läufer. Die maastricht-kriterien: Fug oder unfug. Im Internet unter: http://www. uni-konstanz. de/FuF/wiwi/laufer/lecture2/kriterien-text. html, 2008.

- [25] A. Mas-Colell, M. Dennis Whinston, J. R Green, et al. Microeconomic theory, volume 1. Oxford university press New York, 1995.

- [26] T. Mastrolia, D. Possamaï, and A. Réveillac. On the Malliavin differentiability of BSDEs. Annales de l’institut Henri Poincaré, Probabilités et Statistiques B, to appear, 2014.

- [27] K. Miettinen. Nonlinear multiobjective optimization, volume 12. Springer Science & Business Media, 2012.

- [28] J.A. Mirrlees. Notes on welfare economics, information and uncertainty. In M.S. Balch, D.L. McFadden, and S.Y. Wu, editors, Essays on economic behavior under uncertainty, pages 243–261. Amsterdam: North Holland, 1974.

- [29] J.A. Mirrlees. The optimal structure of incentives and authority within an organization. The Bell Journal of Economics, 7(1):105–131, 1976.

- [30] L. Panaccione et al. Pareto optima and competitive equilibria with moral hazard and financial markets. The BE Journal of Theoretical Economics, 7(1):1–21, 2007.

- [31] É. Pardoux and S. Peng. Adapted solution of a backward stochastic differential equation. Systems & Control Letters, 14(1):55–61, 1990.

- [32] É. Pardoux and S. Peng. Backward stochastic differential equations and quasilinear parabolic partial differential equations. In B.L. Rozovskii and R.B. Sowers, editors, Stochastic partial differential equations and their applications. Proceedings of IFIP WG 7/1 international conference University of North Carolina at Charlotte, NC June 6–8, 1991, volume 176 of Lecture notes in control and information sciences, pages 200–217. Springer, 1992.

- [33] J. Peet. Maastricht follies. Economist, 347(8063), 1998.

- [34] D. Possamaï, X. Tan, and C. Zhou. Stochastic control for a class of nonlinear kernels and applications. arXiv preprint arXiv:1510.08439, 2015.

- [35] E. C Prescott and R. M Townsend. Pareto optima and competitive equilibria with adverse selection and moral hazard. Econometrica: Journal of the Econometric Society, pages 21–45, 1984.

- [36] R. Rouge and N. El Karoui. Pricing via utility maximization and entropy. Mathematical Finance, 10(2):259–276, 2000.

- [37] Y. Sannikov. A continuous–time version of the principal–agent problem. The Review of Economic Studies, 75(3):957–984, 2008.

- [38] H K Scheller. The european central bank. History, Role and Functions. ECB, 2004.

- [39] H. Mete Soner, N. Touzi, and J. Zhang. Wellposedness of second order backward sdes. Probability Theory and Related Fields, 153(1-2):149–190, 2012.

- [40] J. Sung. Lectures on the theory of contracts in corporate finance: from discrete–time to continuous–time models. Com2Mac Lecture Note Series, 4, 2001.

- [41] N. Touzi. Optimal stochastic control, stochastic target problems, and backward SDE, volume 29. Springer Science & Business Media, 2012.

- [42] L. Walras. Éléments d’économie politique pure; ou, Théorie de la richesse sociale. F. Rouge, 1896.

- [43] H. Xing and G. Žitković. A class of globally solvable Markovian quadratic BSDE systems and applications. arXiv preprint arXiv:1603.00217, 2016.

Appendix A The mathematical model and general notations

In this section we set all the notations and spaces used in this paper in the paragraphs "General notations" and "Spaces" respectively. We also defined mathematically the considered model in Paragraph "General model and definitions" and we put the general assumptions which are supposed to be satisfied in all the paper.

General notations. Let be the set of reals. Let and be two positive integers. We denote by the set of matrices with rows and columns, and simplify the notations when , by using . We denote by the identity matrix of order and the zero-valued coefficients matrix. For any , we define as the usual transpose of the matrix . We will always identify with . For any matrix and for any we denote by its th column and similarly we denote by its th row. Besides, for any , we denote its coordinates by . We denote by the Euclidian norm on , when there is no ambiguity on the dimension. The associated inner product between and is denoted by . We also denote by the dimensional vector . Similarly, for any , we define for any as the vector without its th component, that is to say . For any , and any , we define the following dimensional vector

For any , and any , we define the following dimensional matrix

For any Banach space , let be a map from into . For any , we denote by the gradient of and we denote by the Hessian matrix of and similarly we denote by the gradient of and we denote by the Hessian matrix of . Finally, we denote by the inverse function of any if it exists.

Spaces. For any finite dimensional normed space , (resp. ) will denote the set of valued, adapted processes (resp. predictable processes) and for any we set

is the so-called set of predictable processes such that the stochastic integral is a BMO-martingale. We refer to [19] for more details on this space and properties related to this theory. We also denote the classical Doleans-Dade exponential of any local -martingale .

General model and definitions. We assume that the following technical assumptions hold in this paper

Assumption A.1.

For any and any , the map is continuously differentiable, the map is progressive and measurable for any and we assume that their exists a positive constant such that for any

| (A.1) |

For any the map is progressive and measurable. Moreover, the map is increasing, convex and continuously differentiable for any . Assume also that there exists such that

| (A.2) |

and for any

Remark A.1.

Assumption (G).

For any and for any ,

In order to define a probability equivalent to such that is a Brownian motion under , we need to introduce the set of admissible effort. An -adapted and -valued process is said admissible if is an -martingale and if for the same appearing in Assumption A.1 we have for any and any

We also define for any -valued and -adapted process the set by

| (A.3) |

Now, in order to use the theory of quadratic BSDE and apply the result of for instance [4, 5], we must define the set of admissible contracts as the set of -measurable and -valued random variable satisfying the constrain (2.3) and such that

Appendix B Multidimensional quadratic growth BSDEs: application of the results in [15]

The aim of this section is to provide conditions ensuring that Theorem 3.1 holds, by giving a set of admissible contracts for which there exists a solution to the multi-dimensional BSDE (3.3). We consider the set of admissible contract

where is the classical of random variables which are Malliavin differentiable.

Recall that under Assumption A.1, from [10, Lemma 4.1], for any there exists

satisfying

We assume that

-

The map is continuously differentiable such that there exists with

-

The map is continuously differentiable such that there exists with

and moreover

-

The map is continuously differentiable such that there exists with

Thus, for any

Lemma B.1.

Proof.

We compute directly

∎

We now introduce a localisation of defined by where satisfies projection properties on a ball centred on with radius . We denote by the unique solution of BSDE (3.3) with generator , which fits the classical Lipschitz BSDE framework. For all we set the following assumption

(BMO,p) There exists a positive contant such that121212The positive constant comes from Burkholder-Davis-Gundy inequality, see Section 1.1 paragraph Inequalities-BDG in [15] for more details.

-

-

.

As a direct131313After having discussed with Jonathan Harter, assumption (Df,b), (iii) in [15] is not a canonical assumption for the proof of [15, Theorem 3.1]. Indeed, in this paper, the authors needs this assumption only to ensure that the BSDE with projector admits Malliavin differentiable solution as an application of [9]. However, as explained in [26, Section 5 and Section 6] this assumption can be removed in the Markovian case. The author thanks Jonathan Harter for this clarification. consequence of [15, Theorem 3.1] and Lemma B.1 we have the following proposition

Appendix C Technical proofs of Section 4

First recall that under Assumption A.1, from [10, Lemma 4.1], for any there exists

satisfying

| (C.1) |

We now turn to the proofs of the main results in Section 4

Proof of Lemma 4.1.

Proof of Theorem 4.1.

Using (C.1) together with Condition (A.2), the definition of and Assumptions A.1 and (G), we obtain from (for instance) [5] the existence and uniqueness of a solution of BSDE (4.4). Now, by using a comparison theorem for BSDE (4.3) (see for instance [5, Theorem 5]), we deduce that and that any in is Pareto optimal from Proposition 4.1. ∎

Proof of Proposition 4.2.

Let be the solution of BSDE (4.4) from Theorem 4.1. The fact that BSDE (4.2) admits a unique solution in is a direct consequence of the definitions of and . Changing the probability by using Girsanov’s theorem, we directly get

Denote by and , we notice that the pair of process is solution of

Using the uniqueness of the solution of BSDE (4.4), we deduce that and ∎