Strategic Dynamic Pricing with Network Effects

Abstract

We study the optimal pricing strategy of a monopolist selling homogeneous goods to buyers over multiple periods. The customers choose their time of purchase to maximize their payoff that depends on their valuation of the product, the purchase price, and the utility they derive from past purchases of others, termed the network effect. We first show that the optimal price sequence is non-decreasing. Therefore, by postponing purchase to future rounds, customers trade-off a higher utility from the network effects with a higher price. We then show that a customer’s equilibrium strategy can be characterized by a threshold rule in which at each round a customer purchases the product if and only if her valuation exceeds a certain threshold. This implies that customers face an inference problem regarding the valuations of others, i.e., observing that a customer has not yet purchased the product, signals that her valuation is below a threshold. We consider a block model of network interactions, where there are blocks of buyers (with size equal to constant fraction of total number of buyers) subject to the same network effect. A natural benchmark, this model allows us to provide an explicit characterization of the optimal price sequence asymptotically as the number of agents goes to infinity, which notably is linearly increasing in time with a slope that depends on the network effect through a scalar given by the sum of entries of the inverse of the network weight matrix. Our characterization shows that increasing the “imbalance” in the network defined as the difference between the in and out degree of the nodes increases the revenue of the monopolist. We further study the effects of price discrimination and show that in earlier periods monopolist offers lower prices to blocks with higher Bonacich centrality to encourage them to purchase, which in turn further incentivizes other customers to buy in subsequent periods.

1 Introduction

The benefits that users derive from various products such as digital products (e.g., computer software and smartphone apps) and electronics (e.g., smartphones, hardware devices, and computers) depend, among other things, on the other users who have purchased the product before and thus have contributed to improvements of various aspects of the product. User’s purchase decisions in settings with such externalities, termed network effects, will focus on not just whether but when to make a purchase. This implies that a seller will choose a dynamic price path for the product that aims to build the central early user population to increase the network effects and the purchase possibility of the product in later periods. Despite the ubiquity of these issues, there is little work on dynamic pricing with network effects.

In this paper, we study the problem of dynamic pricing in the presence of network effects. We consider a dynamic game between a monopolist seller and a set of buyers. All buyers and seller are forward-looking. The seller announces and commits to a price sequence and buyers decide whether and when to buy a single item. The utility of each buyer depends on her valuation of the product, the price sequence, and the (weighted) number of other customers who have already bought the product. We first show that in this setting the optimal price sequence is non-decreasing. We then show that the equilibrium purchase decision of buyers (in Perfect Bayesian Equilibrium) can be characterized by a threshold rule in which buyers purchase at different rounds if and only if their valuations exceed a certain threshold. This characterization implies that customers face a learning problem regarding the valuations of others since if a round has reached and a customer has not yet purchased the item, her valuation must be below the threshold. Therefore, at any round the belief of a customer regarding the valuations of the remaining customers gets updated using Bayes’ rule. As the optimal price sequence is non-decreasing, by postponing purchase to future rounds each buyer faces the following trade-off: on one hand, she has to pay a higher price, and on the other hand, her utility from the network effects becomes larger.

Building on this characterization, we find the optimal pricing strategy in a block model setting. In particular, we consider a block model with blocks such that each block has a constant fraction of the total number of buyers. The networks effects are captured by a matrix , where denotes the network effect of a buyer in block on a buyer in block . This model provides a natural benchmark in which there are blocks of users subject to the same network effect while still allowing diverse interactions among these blocks. Different blocks may for example represent communities with different characteristics (see Tirole (1988, Chapter 7) and Talluri and Van Ryzin (2006, Chapter 8)). Most importantly, this model allows us to write the seller’s expected revenue as a multivariate Bernstein polynomial which enables us to use asymptotic convergence theory of these polynomials and explicitly characterize the optimal price sequence (see Lorentz (2012)).

Interestingly, for any distribution of buyers’ valuations (under some regularity conditions) we find the closed-form solution of the optimal price sequence asymptotically as the number of users goes to infinity. The optimal price sequence is linearly increasing, and our characterization shows that the properties of both optimal price sequence and the optimal revenue depend on the quantity which we term the network effect. In particular, the extent of the price difference at two consecutive rounds (slope of the price path) is greater for higher network effect and the optimal revenue is increasing and convex in network effect. The network effect (and hence the optimal revenue) is higher for “imbalance” networks.111A directed network is called balance if for each node the out-degree and in-degree are equal. More precisely, for a given sum of network effects (i.e., sum of the entries of ), by decreasing sum of the multiplication of out-degree and in-degree of blocks the revenue increases.

Moreover, we consider a setting with price discrimination, where monopolist offers different prices to different blocks, and characterize the optimal price sequence. We establish that the optimal price sequence is linearly increasing with a slope which is in the form of a “weighted Bonacich centrality”. Our results indicate that in earlier periods monopolist offers lower prices to blocks with higher centrality to encourage them to purchase, which in turn further incentivizes other customers to buy at higher prices in the subsequent periods. We also consider a variation of our model with utility from all purchases and characterize the optimal price sequence and revenue.

1.1 Related Literature

Our paper relates to two sets of works: (i) the study of markets with network effects and (ii) the study of markets with forward-looking strategic buyers.

1.1.1 Network Externalities

Markets for products with network effects has been first studied in Rohlfs (1974), Katz and Shapiro (1985), and Farrell and Saloner (1985). Given the importance of network effects in markets, empirical investigations have examined its implications in a variety of industries. In particular, Au and Kauffman (2001) examine the adoption of electronic bill and payment technology and show the existence of network effects and its implications, Gallaugher and Wang (2002) empirically study the market for Web server software and establish the presence of network effects, and Brynjolfsson and Kemerer (1996) empirically study the network effects in software product market and confirm that the network effects significantly has increased the price of products.

Moreover, on the theory side, a line of research has examined the strategic and welfare implications of network effects. In particular, Candogan et al. (2012), Cohen and Harsha (2013), and Bloch and Quérou (2013) study the optimal static price sequence of a seller selling a divisible good (service) to consumers with network effects. They consider a two-stage game in which a seller decides on the prices, and then buyers decide their consumption in an equilibrium. Given a set of prices, their model takes the form of a network game among agents that interact locally, which relates to a series of papers such as Ballester et al. (2006); Bramoullé and Kranton (2007); Galeotti and Goyal (2009), and Bramoullé et al. (2014). Related models are more recently investigated in Fainmesser and Galeotti (2016), Alizamir et al. (2017), and Belloni et al. (2017). In particular, Alizamir et al. (2017) consider promotion planning of network products and study the effect of network structure.

1.1.2 Strategic Buyers

A number of papers in the literature consider strategic forward-looking buyers who make inter-temporal purchasing decisions with the goal of maximizing their utility. Many empirical works confirm that assuming myopic customer behavior is no longer a tenable assumption (see e.g. Li et al. (2014)). The importance of forward-looking customer behavior in shaping firms’ pricing decision has been broadly identified by practitioners and a recent literature has theoretically studied its implications (see Liu and Van Ryzin (2008); Hörner and Samuelson (2011), Board and Skrzypacz (2016); Pai and Vohra (2013); Borgs et al. (2014); Cachon and Feldman (2015); Chen and Farias (2015); Yang and Zhang (2015); Lobel et al. (2015); Dilme and Li (2016); Bernstein and Martínez-de Albéniz (2016)). In particular, Besbes and Lobel (2015) study the optimal price sequence of a committed seller that faces customers arriving over time with heterogeneous willingness to wait before making a purchase. They show that cyclic pricing policies are optimal for this setting. Ajorlou et al. (2016) consider a setting in which customers know about the existence of a product through the word-of-mouth communication and study the pricing strategy of the seller. Papanastasiou and Savva (2016) consider a setting in which forward-looking customers learn the quality (unknown and fixed) of a product from the reviews of their peers and study the pricing strategy of the seller. Lingenbrink and Iyer (2018) consider a setting with strategic customers and uncertain inventory and find the revenue-optimal signaling mechanism (i.e., the signaling that “persuades” customers to purchase at higher price).222Our paper also relates to the literature on the “Coase conjecture” Coase (1972); Gul et al. (1986). “Coasian dynamics” (Hart and Tirole (1988)) consist of two properties: (i) higher valuation buyers make their purchase no later than lower valuation buyers (skimming property) and (ii) equilibrium price sequence is non-increasing over time (price monotonicity property). In this paper, we show that the second property does not hold when network effects are present.

1.2 Notation

For any matrix , we use both and to denote the entry at th row and th column. We show vectors with bold face letters. For a matrix , and denote the spectral radius and infinity norm of , defined as , and , respectively. The vector of all ones is shown by , where the dimension of vector is clear from the context. For any event , if holds and , otherwise. For any integer , we let . We denote the transpose of vector and matrix by and , respectively. For two vectors , means entry-wise inequality, i.e. , for all . For two matrices , means entry-wise inequality, i.e. , for all . We show a weighted directed network by where represents the set of nodes and represents the weight of the edge from to . In-degree and out-degree of node are denoted by and . A network is called symmetric iff for all and is called balance iff for all . We let denote the projection operator onto the interval .

1.3 Outline

The rest of the paper is organized as follows. In Sections 2, 3, and 4 we describe the model and provide preliminary characterizations of buyers and seller strategy. In Section 5 we characterize the optimal price sequence. In Section 6, we study the effects of network structure on the optimal price sequence and optimal revenue. Finally, in Section 7 we characterize optimal price sequence with price discrimination, leading to concluding remarks in Section 8. All of the omitted proofs as well as a variation of our model and analysis are presented in the Appendix.

2 Model Description

We consider a dynamic game between a monopolist with infinitely many homogeneous items and buyers in rounds. For our analysis, we find it more convenient to index the rounds in decreasing order, i.e., round refers to period (there are remaining periods until the end of selling horizon). The monopolist announces a price sequence where is the price offered for the item at round . At each round, buyers decide whether to buy the item or postpone it to future rounds. We let denote the set of buyers that buy the item at round at price . The history available to buyers at round is given by (we also let ). Each buyer has a valuation in drawn independently from a known continuous distribution . The utility of each buyer depends on her valuation, the price sequence, and a network effect term. More specifically, we assume that buyer interactions are captured by a directed weighted graph , where is the set of buyers and is a weight matrix with representing the utility gain derives from ’s purchase (note that can be different from ). Thus, the utility of buyer with valuation , if she buys the item at round with price is given by

| (2.1) |

where . The third term is the weighted sum of other buyers who have bought the item before round and represents the “network effect” on buyer ’s utility. This utility model captures situations in which other buyers purchase decisions affect a buyer’s utility by improving the product through their use. Hence, at the time a buyer makes her purchase decision and utilizes the product, what matters is past users that determine how improved the product is. Note that consistent with this interpretation and full rationality (in perfect Bayesian equilibrium), even though buyers derive utility from purchases in the past, they are forward-looking, i.e., they take into account all future behavior and decide to postpone the purchase if it is optimal. In Appendix 8.1, we consider a variation of our model with utility from all purchases (i.e., not only the previous purchases). For this alternative model, we find the optimal price sequence and the optimal revenue of the monopolist.

We next describe the buyers’ strategies. A given price sequence induces a dynamic incomplete information game among buyers. A (pure) strategy for buyer is a sequence , where is a mapping from into , mapping buyer ’s valuation, the history of the game, and the price sequence into a purchase decision. A perfect Bayesian equilibrium is a collection of strategies , for such that buyer maximizes her expected utility given her belief (updated in a Bayesian manner) and strategies of other buyers. In particular, in a perfect Bayesian equilibrium a buyer buys the item at round with price if and only if

where the left hand side is the utility of buyer if she purchases at round and the right hand side is the maximum of expected utility from purchasing in any of the future rounds (i.e., ). The expectation is taken over the belief of buyer regarding the other buyers’ valuations.

For a given price sequence , the expected revenue of the monopolist is333We use the terms monopolist and seller interchangeably. We also use the terms user, customer, and buyer interchangeably.

| (2.2) |

where we normalized the marginal cost of the monopolist to zero. We refer to the price sequence that maximizes Eq. (2.2) as the optimal price sequence and the corresponding revenue as the optimal revenue (we also use the term optimal normalized revenue which is equal to the optimal revenue divided by the number of buyers). The ability of the seller to commit to a price sequence is important for our results. Without such commitment, a Coase conjecture-type reasoning would create a downward pressure on prices and would tend to reduce seller’s revenue (Coase (1972)). Though such commitment is not possible in some settings, many sellers can build a reputation for such commitment, for instance, by creating explicit early discounts which will be lifted later on (see Talluri and Van Ryzin (2006, Chapter 8) for a discussion of committed pricing).

3 Preliminary Characterizations

In this section, we show the optimal price sequence is non-decreasing and characterize the purchase decision of customers in equilibrium. Each buyer faces an optimal stopping problem, choosing the round (if any) along a sequence of prices at which to accept the offered price and exit the game given the strategy of other buyers. We next show that the optimal price sequence is non-decreasing and buyer chooses to purchase the item only if her valuation exceeds a time and history dependent threshold denoted by that satisfies for all . In the rest of the paper, we use and interchangeably and refer to them as critical thresholds.

Proposition 1

-

(a)

The seller’s optimal price sequence is non-decreasing, i.e., any optimal price sequence has a corresponding non-decreasing price sequence in which the equilibrium path (the purchase decision of buyers) remains the same.

-

(b)

Given a non-decreasing price sequence, the purchase decision of buyer in any equilibrium is a thresholding decision, i.e., for each there exists a sequence , such that for and buyer purchases at round if and only if .

Proposition 1 is a crucial observation on which much of the rest of our analysis builds. Technically, it is simple and relates to previous results in dynamic settings with preferences satisfying single crossing. Its implications in our model are far-reaching, however. Without network effects, increasing (non-decreasing) price sequence would be impossible to sustain. Because with increasing prices, high-valuation buyers will tend to be the first ones to purchase, and if lower-valuation buyers prefer not to purchase early on (with low prices), they would also prefer not to purchase later on with higher prices (as there is no benefit from network effects). This phenomenon is transformed in the presence of network effects. Now because the increase in the number of users over time raises the network effect term (regardless of the exact form of network interactions), lower-valuation buyers might prefer to buy later and at higher prices. In fact, it is not optimal for the seller to have a strictly decreasing price sequence, because this would induce all buyers to delay, while an increasing price sequence would induce high-valuation buyers to purchase early, while lower-valuation ones wait and purchase once the network effect is higher.

In the next lemma we provide a relation for the critical thresholds describing the buyers’ purchase decision.

Lemma 1

Given a non-decreasing price sequence , for the critical thresholds satisfy the following indifference condition

| (3.1) |

with for all . Moreover, if ’s are in , then we have

This relation is defined by noting that a buyer with valuation equal to must be indifferent between buying at round and waiting until round .

The sequence , depends on the history of the game and Lemma 1 provides an indifference condition for it, with boundary conditions , . This is because in the first period, the seller and buyers have not yet learned anything about buyer ’s valuation. Note that each buyer faces an inference problem regarding the valuation of the other buyers. In particular, if round with history is reached and a buyer has not purchased the item, then all buyers know that belongs to with cumulative density function

which is obtained via Bayes’ rule.

In the next example, we illustrate two main challenges in analyzing the equilibrium of this game. First, we illustrate that finding the optimal price sequence is a complicated task because the monopolist needs to take into account all possible histories (i.e., histories for a game with buyers in rounds). Second, we illustrate the possibility of having multiple equilibria.

Example 1

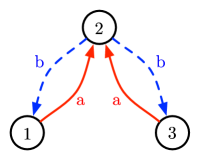

We consider a game with buyers in periods ( and ) where the network effects are represented by

for and (see Figure 1). We also let the valuations to be uniform, i.e., , for all . Given a non-decreasing price sequence , if the critical thresholds are in , using Lemma 1 for the first period (i.e., ) leads to

where we used , . This set of equations have multiple solutions, leading to multiple strategies for the first period of the game. In particular, the critical thresholds satisfy

| (3.2) |

Using Lemma 1 for the second period (i.e., ), we have

| (3.3) |

Given any set of critical thresholds, the expected revenue becomes

| (3.4) |

where the expectation is taken over all histories for ( possible histories). The first term is the revenue in the first period and the second term is the expected revenue in the second period, given . Maximizing the expected revenue subject to Eqs. (3.2) and (1), leads to the following pairs (among many others) of price sequence and buyers’ strategies:

-

•

Symmetric equilibrium: in this equilibrium the buyers’ decision depend on their valuation, price, and the network effects, and not on their identity. Therefore, the strategies of buyers and are the same, i.e., and which leads to price sequence and with expected revenue . The corresponding buyers’ strategies in the first period are determined by critical thresholds , , and in the second period by critical thresholds given in Eq. (1). Note that all these critical thresholds are in .

-

•

Asymmetric equilibrium: suppose the buyers’ strategies in the first period are determined by critical thresholds , , . The optimal price sequence becomes and with expected revenue . The buyers’ strategies in the second period are determined by critical thresholds given in Eq. (1). Note that again all these critical thresholds are in .

To overcome the challenges illustrated in Example 1 and to obtain a tractable expected revenue, we will consider a block model as described in the next section and focus on the symmetric equilibrium concept. Intuitively, with this setting the sample equilibrium path is close to its expectation which enables us to use techniques from probability theory (namely, Bernstein polynomial convergence; see Lorentz (2012)) to find a closed-form characterization for the expected revenue as well as the optimal price sequence.

4 The Block Model and Buyers’ Equilibrium

We consider a “block model” (first introduced in White et al. (1976); Holland et al. (1983)) in which the buyers are partitioned into blocks. Block denoted by has many buyers for some . We let be a diagonal matrix with . The utility gains of buyers in block from purchase decision of buyers in block are equal and denoted by . Hence we can capture all the gains by a network matrix . Formally, we let

where the normalization by is to guarantee that the network effects term in buyers’ utilities does not grow with and is comparable to valuations which are in . For instance, if many buyers from block purchase the product, then the network effects of a buyer in is . This model provides a natural benchmark in which there are blocks of users subject to the same network effect while still allowing diverse interactions among these blocks. These blocks may for example represent communities with dense linkages within themselves. Most importantly, this model allows us to write the monopolist’s expected revenue as a multivariate Bernstein polynomial which enables us to use convergence results of these polynomials and explicitly characterize the optimal price sequence.

The following provides the definition and convergence of multivariate Bernstein polynomial (see Lorentz (2012, Chapter 2.9)).

Definition 1 (Multivariate Bernstein Polynomial)

For any function , where is -dimensional simplex, multivariate Bernstein polynomial is defined as

where

Theorem 1 (Lorentz (2012))

If is continuous, then we have uniformly.

As shown in Example 1 there exist multiple equilibria for buyers’ purchase decisions; however, there exists a unique symmetric equilibrium in which a buyer’s strategy depends on her valuation and her network effects, not on her identity. In the rest of the paper, we use the symmetric equilibrium concept and refer to it as buyers’ equilibrium.444Symmetric equilibrium is used as a selection device among multiple equilibria which is widely used in the literature. See Gul et al. (1986), Chen (2012), Hörner and Samuelson (2011) for dynamic pricing settings, Krishna (2009, Chapter 4) for auction setting, and (Talluri and Van Ryzin, 2006, Chapter 8) for pricing games. Using Lemma 1, the buyers’ equilibrium is characterized by critical thresholds defined for blocks described in the next corollary.

Corollary 1 (Buyers’ Equilibrium)

Given a non-decreasing price sequence , for the critical thresholds satisfy the following indifference condition

| (4.1) |

with for all . Moreover, in the buyers’ equilibrium any remaining buyer in block purchases at price if and only if her valuation exceeds .

5 Optimal Price Sequence

In this section, we characterize the optimal price sequence for any valuation distribution and network effects under the following regularity conditions.

Assumption 1

Matrix is invertible and the distribution is such that

is non-decreasing. Also, the matrix is such that .

The assumption on is the analogous of the regularity condition (i.e., is non-decreasing) and is used to guarantee the uniqueness of the optimal price sequence. Indeed, without network effect (i.e., with ) this assumption reduces to the regularity condition which is used in optimal auction design (see Myerson (1981)). The assumptions on the network matrix guarantee that the critical thresholds are interior (i.e., in ) and therefore enable their explicit characterization. As an example, we next show that for uniform valuations and a weakly-tied block model, i.e., , for small , Assumption 1 holds. This network matrix captures situations in which inter block interactions are weak.

Lemma 2

Suppose with . If , then Assumption 1 holds for uniform valuations and , for .

Our key result presented next provides an explicit characterization of optimal prices and optimal revenue as a function of the network effects.

Theorem 2

Suppose Assumption 1 holds. The optimal price sequence in the limit (as ) is given by

| (5.1) |

where is the solution of

In addition, the optimal normalized revenue is

| (5.2) |

Proof We provide the main steps of the proof for and uniform valuations. The complete proof is presented in the Appendix.

We first characterize the buyers’ equilibrium given a price sequence as a function of network matrix and then find the optimal price sequence. Using Corollary 1, the indifference condition for any block in the first period becomes

where we used uniform distribution for valuations in the last equality. By letting and using the definition of and , we can write this equation in compact form as

| (5.3) |

In the second period, any remaining buyer in block buys the item if and only if

which for uniform valuations happens with probability

Therefore, the monopolist’s expected revenue can be written as

| (5.4) |

where the first term of each summand is the probability of a multivariate Binomial random variable capturing the probability of the event that in the first period for each block , out of many buyers purchase the item. The second term of each summand is the expected revenue of the monopolist given this event. In particular, for each block , buyers purchase the product at price and each of the remaining buyers purchase the product at price with probability .

To obtain a closed-form expression for the optimal expected revenue, we consider the limiting normalized revenue as and then use Bernstein polynomial convergence presented in Theorem 1. Letting

the normalized expected revenue given in Eq. (5.4) becomes

Therefore, using Theorem 1 the limiting normalized revenue becomes

| (5.5) |

where the second equality follows from Assumption 1 and Eq. (5.3), as we will show at the end of this proof. Combining Eqs. (5.3) and (5), the normalized limiting revenue denoted by becomes

We next find that maximizes . The first order conditions of are

which leads to

| (5.6) |

The solution of the first order conditions indeed lead to the maximum of . We can see this by taking second order derivative of and showing that the Hessian is negative semidefinite. In particular, taking second order derivative of leads to the following Hessian

which is negative definite. This can be seen by noting that and , which holds because Assumption 1 for uniform distributions guarantees .555A symmetric matrix is negative definite if and . Therefore, the maximum of is attained at the solution of the first order conditions. Plugging and from Eq. (5.6) in , the optimal revenue becomes

Finally, we show that the prices and and their corresponding guarantee for all , showing that the projection operators used in Eq. (5) are identity. This is equivalent to

| (5.7) |

Using Eq. (5.3), we can rewrite Eq. (5.7) in vector form as . The lower bound evidently holds as . The upper bound after plugging in and in Eq. (5.3) and finding , becomes

which holds because of Assumption 1 and in particular . This completes the proof for the special case of and uniform valuations.

Theorem 2 shows that the optimal price sequence is linearly increasing. Moreover, the impact of the network matrix on the optimal price sequence and the optimal revenue is captured by a single network measure .

Definition 2

We refer to the term as network effect and denote it by .

We next show the properties of the optimal normalized revenue as well as the optimal price sequence as a function of the network effect and the number of rounds.

Proposition 2

Suppose Assumption 1 holds. The optimal normalized revenue is increasing in and increasing and convex in network effect . Moreover, the slope of the optimal price sequence (i.e., the difference of the optimal prices in two consecutive rounds) is increasing in .

-

•

Proposition 2 shows that the optimal normalized revenue is an increasing convex function in network effect. Intuitively, this holds because increasing increases the utility of buyers in two different ways: (i) direct effect: as increases, keeping purchase probability of other buyers the same, each buyer enjoys a higher network effect, and (ii) indirect effect: as increases, the purchase probability of other buyers in previous rounds increases (i.e., the critical thresholds decrease), leading to higher utility.

-

•

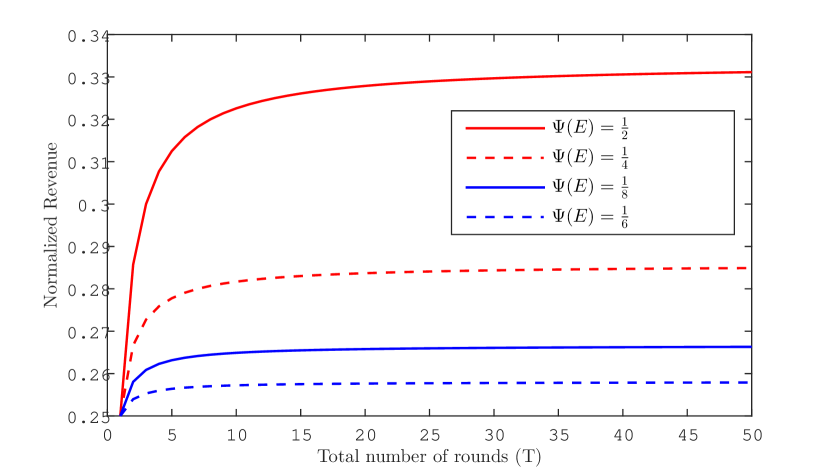

Figure 2(a) shows the optimal normalized revenue as a function of the number of rounds, illustrating that the optimal revenue is increasing in . The optimal revenue approaches the limiting normalized revenue as relatively fast. For instance, for uniform valuations if we want to obtain of the optimal revenue (i.e., revenue of infinitely many rounds), then for , rounds suffice and for , rounds suffice.

-

•

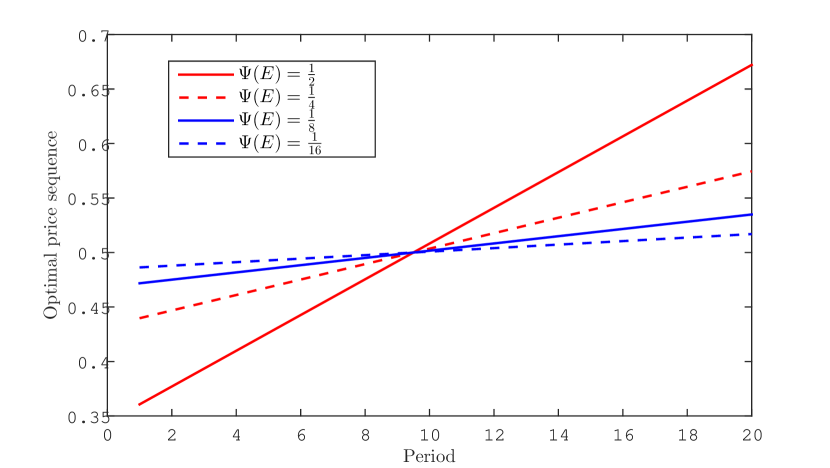

Figure 2(b) shows the optimal price sequence for various network effects, illustrating that the slope of the optimal price sequence is increasing in . Proposition 2 shows the slope of the optimal price sequence is increasing in the network effect. Intuitively, this holds because as increases, the past purchases contribute more to the utility of buyers, incentivizing them to purchase at a higher price.

-

•

Buyers with valuations below the critical threshold of the last period do not buy the item. This threshold is decreasing in and . Therefore, increasing or increases the number of users who purchase the item.

6 Aggregate Network Effect

In Theorem 2 we characterized the optimal price sequence as a function of the network effect . We now study in more detail the effect of network properties on and the optimal price sequence and revenue. In this regard, we consider a weakly-tied block model, where for and some sufficiently small . This network matrix represents a natural setting in which the utility gain of buyers within each block is larger than the ones across blocks. Also, note that for this network matrix, using Lemma 2, for uniform valuations and , Assumption 1 and therefore Theorem 2 holds. In particular, a second order Taylor approximation of leads to

| (6.1) |

Proposition 2 together with Eq. (6.1) leads to the following implications.

-

•

The second term shows that higher sum of inter blocks utility gains, i.e, , leads to higher and therefore higher revenue.

-

•

The third term shows that for a given , the highest revenue is obtained for a network with the minimum where

Here and correspond to the out-degree and in-degree in the network matrix , respectively. This shows that the highest revenue is obtained for a network with minimum . With a small , the influential blocks (i.e., with high out-degrees) are less influenced by other blocks (i.e., have low in-degrees). Therefore, the influential blocks have little incentive to postpone their purchase and prefer to purchase earlier (i.e., they have a low critical threshold). This in turn incentivizes users from other blocks to purchase at higher prices in subsequent periods (because of the higher network effect term), increasing the revenues of the monopolist. As an example, for (i.e., if there exists an edge from to ), a bipartite directed graph has the highest revenue ( for all ).

We next show that the minimum (for a given in-degree sequence or fixed ) is obtained for a network with the most degree sequence “imbalance”, where the imbalance sequence is defined as (see Mubayi et al. (2001)).

Proposition 3

Consider two network matrices and with the same in-degree sequence and different out-degree sequences denoted by and , respectively. If the imbalance sequence of majorizes the imbalance sequence of , then .666We say a sequence majorizes if and only if for any we have .

The next example illustrates the effect of imbalance sequence on revenue by comparing the revenues of a directed chain, a directed ring, and a directed star network.

Example 2

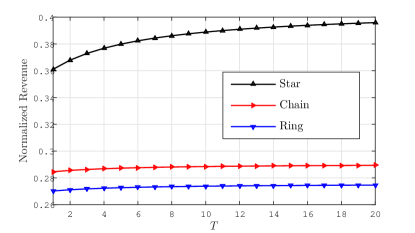

We consider a directed chain, a directed ring, and a directed star network (where the edges are from the periphery nodes to the center node) with blocks. For all of these networks we let the network matrix be , , , and the weight of different edges in each network be the same. The first and second terms of Eq. (6.1) are the same for these three networks, but the third terms are different. In particular, the term for directed ring, directed chain, and directed star are , , and , respectively. Therefore, the network effect and the revenue of directed star is higher than directed chain, which is higher than directed ring. Figure 3 illustrates the revenues of these three networks as a function of the number of periods.

Figure 3: The normalized revenue as function of the number of periods for the networks of Example 2: directed chain, directed ring, and directed star networks. -

•

For a given , among balanced networks for which , for all (note that a symmetric network, i.e., is balanced) the highest revenue is obtained by a regular network, i.e., a network with for all . This follows because we have

where we used the balancedness in the last equality and Cauchy-Schwarz in the inequality. The inequality becomes an equality if and only if for any , we have , showing that a regular network has the highest revenue. Here, because of the balancedness, each block is equally influential and influenced by others. Now suppose the network is not regular and consider the block with the highest out-degree (which is equal to its in-degree). The customers in this block have a high in-degree and therefore prefer to postpone their purchase to future rounds (because they will obtain a large utility gain from other purchases). Thus, the monopolist cannot fully utilize the network effect of this block on other blocks to increase the revenue.

7 Price Discrimination

In this section, we study price discrimination and characterize the optimal price sequence. With price discrimination, at each round the price offered to different blocks can be different. Throughout this section we assume that the valuations are uniform, but, the results can be generalized to any valuation distribution under proper regularity assumptions.

Proposition 4

Suppose the valuations are uniform and is positive semidefinite. The optimal price sequence in the limit (as ) is given by

| (7.1) |

where is the solution of

| (7.2) |

Note that for a symmetric weakly-tied block model, i.e., , similar to Lemma 2, for small enough , Assumption 1 holds.

We can rewrite the optimal price sequence as

where is the Bonacich centrality with parameter in network defined as (see Bonacich (1987)). Proposition 4 establishes that the optimal price sequence is linear and the slope of this linear price sequence is given by a “weighted Bonacich centrality”. This implies that in the early periods the monopolist offers a lower price to more central blocks and rapidly increases the price offered to them in subsequent periods. This is to encourage more central buyers to purchase in the early periods which in turn incentivizes more buyers (due to larger centrality) to purchase in subsequent periods.

We next compare the optimal price sequence in this setting with that of the static pricing studied in Candogan et al. (2012). The buyer’s strategies in a setting with one round of pricing is given by a threshold rule where buyers in block purchase the item if their valuation exceed . These thresholds satisfy the indifference condition

where . This leads to .777For any the expected normalized number of customers in block who purchase the item is . Therefore, our model becomes identical to the consumption model of Candogan et al. (2012) by letting the “consumption level” of block be equal to . Therefore, the normalized revenue becomes

| (7.3) |

Maximizing Eq. (7.3) over leads to

| (7.4) |

which is the same as the optimal prices obtained for static pricing in Candogan et al. (2012, Theorem 2) with . Comparing our result in Proposition 4 and Eq. (7.4), we note that the optimal price given in Eq. (7.4) for symmetric networks (i.e., ) is (see also Candogan et al. (2012, Corollary 1)). However, in our setting with more than one period, even for symmetric networks, the optimal price sequence depends on the network structure (see Eqs. (7.1) and (7.2)) and the monopolist obtains revenue gains from the network effects which is in sharp contrast with Candogan et al. (2012, Section 5).

Acknowledgment

We thank participants at several seminars and conferences for useful suggestions and comments. We specially thank Daron Acemoglu, Kimon Drakopolous, Saeed Alaei, and Ozan Candogan for very helpful discussions and suggestions.

8 Conclusion

We study the problem of finding the optimal price sequence for a product given a set of customers with heterogeneous valuations that strategically decide their purchase time (if any). The product features network effects, i.e., the utility of each customer depends on the price sequence, her valuation, as well as a weighted number of other buyers who have purchased the item. We establish that the problem of finding the optimal price sequence is a tractable one and explicitly characterize the optimal price sequence as a function of the network structure. Our main result identifies a novel dependence on the network structure: sum of the entries of the inverse of network matrix, termed network effect. From a structural perspective, the optimal price sequence is always linearly increasing with a slope that is increasing in the network effect. We establish that increasing network imbalance increases the network effect which, in turn, increases the revenue. The framework and results we present in this paper lay the ground for a potential new approach to the class of dynamic pricing problems with strategic customers and combinatorial structures. Avenues for future research include the expansion of the set of problems that may be tackled through the present approach. For example, the question of dynamic strategic pricing with limited inventory and strategic buyers and seller is a natural extension.

Appendix

Proof of Proposition 1

Proof of part (a): if for some , then none of the buyers will buy the item at round (note that the period with price is after the period with price ). This is because if they wait until the next round, the price decreases and the network effect term of their utility weakly increases (it either remains the same or increases). Therefore, the equilibrium path (the purchase decision of buyers) in the continuation game (i.e., in rounds ) is the same as a game in which we have . Staring from the last period (i.e., ) and repeatedly applying this argument shows the existence of a non-decreasing price sequence with the same equilibrium path as the optimal price sequence.

Proof of part (b): for a given equilibrium, suppose that buyer with valuation finds it optimal to purchase at price in round . Then it must be the case that her utility from purchasing in round is not smaller than her expected utility from postponing the purchase to future rounds (i.e., not purchasing at round ). Therefore, we must have

Since (there is a probability with which does not buy at all), the derivative in of the left hand side of this inequality is at least as large as that of the right hand side. Therefore, buyer with valuations finds it strictly optimal to also purchase at round with price . This shows that if buyer at time does not purchase, then her valuation is larger than a certain threshold denoted by . Finally, note that each buyer that purchases the item leaves the game, leading to , for .

Proof of Lemma 1

Using Proposition 1, for a given price sequence and history , the decision of buyer at time is to buy if and only if her valuation exceeds . Buyer with valuation must be indifferent between accepting price and waiting until the subsequent round (in a continuation game with periods to go). If buyer with valuation purchases at price , her utility (conditional on period having been reached) is

| (8.1) |

By waiting one more period instead, buyer with valuation obtains utility

| (8.2) |

Buyer with threshold at round must be indifferent between buying at round and buying at the next round, i.e., round . Subtracting Eq. (8.1) and Eq. (8.2) leads to

where

Finally, note that if , then buyer has purchased the item in round and if , then using Bayes’ rule we have

which completes the proof.

Proof of Lemma 2

Proof of : we will show that . First note that since , we have which guarantees is invertible. Since , we also have

where the last two inequalities follow from .

Proof of :

using Taylor series expansion of (which converges because ), leads to

| (8.3) |

We also have

| (8.4) |

where inequality (1) follows from and inequality (2) follows from . This inequality holds because for any we have

Putting Eqs. (8.3) and (Proof of Lemma 2) together leads to

where we used in the last inequality that follows from .

Proof of non-decreasing: for uniform distribution this condition is equivalent to having . Finally, note that this holds because from (8.3) we obtain .

Proof of Theorem 2

Throughput this proof we use the following notation for probability mass function of a multinomial random variable:

for all and such that and .

For a given price sequence and a general distribution, using Corollary 1, the critical thresholds defining Buyers’ equilibrium satisfy

| (8.5) |

with the convention that where . We will next find the limiting normalized revenue for a given price sequence. The normalized revenue is

| (8.6) |

where by convention and the multinomial distribution captures the number of possibilities for selecting a partition of into subsets of size , and . Note that for , shows the number of buyers in block who buy at price and the remaining number of buyers in block (i.e., many) decide not to buy the product. We rewrite Eq. (Proof of Theorem 2) and take the limit as , resulting in

where we used Theorem 1 for . Again using Theorem 1, times for as , the normalized expected revenue becomes

| (8.7) |

where we used the fact that which guarantees for all . At the end of this proof, we will show that Assumption 1 guarantees . Taking summation of Eq. (Proof of Theorem 2) for leads to

Using this equation in Eq. (Proof of Theorem 2) for leads to . Therefore, the normalized revenue can be written as

| (8.8) |

where (1) follows from Eq. (Proof of Theorem 2). Therefore, the monopolist’s problem is to choose that maximizes

The first order conditions, results in

We will first find the solution of this set of equations and then show that with Assumption 1, the solution of first order conditions maximizes the revenue. Starting from the last equation, we obtain

Plugging this into the equation corresponding to , leads to

Repeating this argument leads to

| (8.9) |

Using Eq. (8.9) for and the equation corresponding to yields

| (8.10) |

Moreover, using Eq. (8.9) for in the equation corresponding to , gives

| (8.11) |

Combining Eq. (8.10) and Eq. (Proof of Theorem 2), we find the price in the first and last periods as

| (8.12) |

Invoking Eq. (Proof of Theorem 2) in Eq. (8.9) results in the optimal price sequence

| (8.13) |

Therefore, the price sequence starts from in the first periods and linearly increases. Also, note that the price given by the solution of Eq. (Proof of Theorem 2) is unique. We show this by establishing that

is increasing. Taking derivative of this equation leads to

where we used Assumption 1 in the last inequality.

We next show that the first order condition gives the optimal price sequence. The Hessian of is given by a symmetric matrix where for , , , for , and . We next show that the Hessian is negative semidefinite. For any , we show that . We have

| (8.14) |

where (1) follows from and (2) follows from Eq. (Proof of Theorem 2). In order to show Eq. (Proof of Theorem 2) is non-positive it suffices to show that the matrix

is negative semidefinite. Since , in order to show is negative semidefinite, it suffices to show the determinant is non-negative. The determinant is

where we used Assumption 1 to obtain the inequality.

To complete the proof, it remains to verify . This holds because using Eq. (Proof of Theorem 2), we obtain

| (8.15) |

where the inequality holds because and from Assumption 1, we have . Therefore, we have . We will next show that . Inequality evidently holds as we have . Also, is equivalent to

| (8.16) |

This holds because we have

where (1) follows from , (2) follows from , and (3) follows from Assumption 1 and in particular . We next find the corresponding optimal normalized revenue. Plugging price sequence Eq. (8.13) in Eq. (Proof of Theorem 2) leads to the optimal normalized revenue

Proof of Proposition 2

Using Theorem 2, the optimal normalized revenue is

| (8.17) |

where

| (8.18) |

We next take the derivative of Eq. 8.17 with respect to and show that it is positive, implying that the optimal normalized revenue is increasing in both and . Taking derivative of Eq. 8.17 with respect to leads to

| (8.19) |

Also, taking derivative of Eq. (8.18) with respect to yields

| (8.20) |

Plugging Eq. (8.20) into Eq. (Proof of Proposition 2) gives

Therefore, the optimal normalized revenue in increasing in . Since is increasing in both and , the optimal normalized revenue is increasing in both and .

The second derivative of the optimal normalized revenue with respect to is

where we used Assumption 1 in the inequality. Since is linear in (i.e., ), the optimal normalized revenue is convex in .

The slope of the optimal price sequence is . We next take the derivative of the slope with respect to and show it is non-negative. We have

where we used Assumption 1 in the inequality. Therefore, the slope of the optimal price sequence is increasing in .

Proof of Proposition 3

First note that given the in-degree sequence, we have . We next compare the terms and . Since the imbalance sequence of majorizes the imbalance sequence of , we have

| (8.21) |

Using Eq. (8.21) for , yields

Again, using Eq. (8.21) for and the previous inequality we obtain

where we used and . Repeating this argument, leads to

which completes the proof.

Proof of Proposition 4

Similar to the proof of Theorem 2 the critical thresholds defining the buyers’ equilibrium satisfy

| (8.22) |

and the normalized revenue becomes

| (8.23) |

Taking derivative of the revenue and multiplying by leads to

Similar to the argument used in the proof of Theorem 2, the optimal price sequence becomes

| (8.24) |

Plugging this into the equation corresponding to , we obtain

| (8.25) |

Finally, using (8.25) in the equation corresponding to , leads to given by

This equation simplifies to

| (8.26) |

Plugging Eq. (8.26) in Eq. (8.25) leads to

which gives the optimal price sequence given in the statement of Theorem 4. We next show that the first order condition provides the optimal solution. To this end, we show that the Hessian is negative semidefinite. The Hessian is given by

We need to show that for any we have

This follows by taking summation of the following inequalities:

where the first and last set of inequalities evidently hold and the second inequality follows from the assumption that is positive semidefinite. Finally, note that since is positive semidefinite, is invertible.

We will next show that the critical thresholds are interior. By Assumption we have , showing for . Therefore, using Eq. (Proof of Proposition 4), we obtain . We will next show . Since and , we obtain . We next show that . Using Eq. (Proof of Proposition 4), we have

where the first inequality evidently holds and the second inequality follows from Eqs. (8.24) and (8.25). Finally, using the Sherman-Morrison-Woodbury formula Horn and Johnson (2012, Section 0.7.4) stated at the end of this proof, we can simplify Eq. 8.26 as follows

Lemma 3 (Sherman-Morrison-Woodbury)

Suppose that a nonsingular matrix has a known inverse and consider ,in which is -by-, is -by-, and is -by- and nonsingular. If is nonsingular, then

8.1 Model with Utility from all Purchases

In this subsection, we consider a variation of our model in which the utility of a buyer depends on the entire set of buyers who buy the product over periods. More specifically, the utility of buyer is

where is the valuation of buyer and is the posted price at round . We assume that customers are individually rational, i.e., if a customer purchases at round , her utility considering only the purchases already happened, should be non-negative. This assumption is crucial as without this assumption given any price sequence all customers purchase the item at the round with minimum price. We next show via an example that in this setting the optimal price sequence can either be increasing or decreasing.

Example 3

Let the valuations be uniform over , , and . We first find the optimal non-decreasing price sequence and then find the optimal non-increasing price sequence.

-

•

Non-decreasing price sequence (i.e. ): the optimal prices are with revenue . The seller’s problem becomes

where the first term of the objective captures the case when both valuations are above which happens with probability with corresponding revenue . The second term captures the case when only one of the valuations is above whose probability is . In this case, the monopolist obtains revenue from the buyer with valuation above . The other buyer purchases if its valuation is above whose probability is (i.e., ) and its revenue is . Also, note that if both valuations are below , then none of the buyers purchases the product in the first period. Therefore, they generate no network effect and none of them will purchase in the second period with price which is higher than . The solution to this optimization problem is .

-

•

Non-increasing price sequence (i.e., ): note that in this case customers may postpone the purchase even if their utility is non-negative in order to pay the lower price offered in the subsequent period. If a buyer with valuation buys in the first period her expected utility becomes

(8.27) where the term is the probability of the other customer purchasing in one of the periods. On the other hand, if a buyer with valuation buys in the second period her expected utility becomes

(8.28) where the term is the probability of the other customer purchasing in one of the periods. Comparing Eqs. (8.27) and (8.28), a buyer with valuation purchases in the first period if and only if

which leads to . If the prices does not satisfy this inequality, then both buyers purchase in the second period with price (i.e., lower price) and the optimal expected revenue becomes . We next consider a price sequence that satisfies and show the optimal expected revenue is always higher than . In this case, the seller’s problem becomes

s.t. where the first term of the objective captures the case when both valuations are above which happens with probability with corresponding revenue . The second term captures the case when only one of the valuations is above whose probability is . In this case, the monopolist obtains revenue from the buyer with valuation above . The other buyer purchases if its valuation is above whose probability is (i.e., ) and its revenue is . The third terms of the objective captures the case when both valuations are below . In this case, each player purchase in the second period with probability and obtains revenue from each purchase. The solution of this problem is:

-

1.

If , the optimal price sequence is , with the optimal revenue .

-

2.

If , the optimal price sequence is , , with the optimal revenue .

-

3.

If , the optimal price sequence is , , with the optimal revenue .

-

4.

If , , the optimal price sequence is , , with the optimal revenue .

-

1.

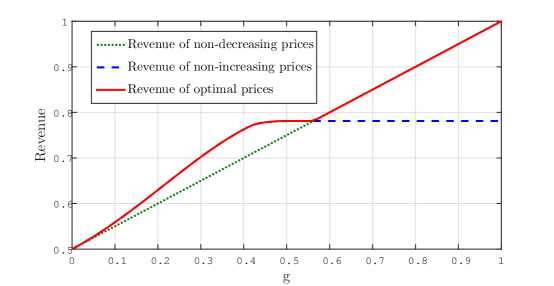

Putting these two cases together the optimal revenue becomes the one plotted in Figure 4.

In Example 3, the optimal price sequence can be decreasing because a buyer who observes a lower price in the second period might be willing to purchase in the first period (with higher price) in order to incentivize the other buyer to purchase in the second period. This effect goes away once we consider a large number of buyers for which a similar argument to that of Proposition 1 shows that the optimal price sequence is non-decreasing. In the next proposition we characterize the optimal price sequence (which is non-decreasing).

Proposition 5

Suppose the valuations are uniform and . The optimal price sequence in the limit (as ) is , with the optimal normalized revenue

Note that similar to Lemma 2 for a weakly-tied block model and small enough , the Assumption of Proposition 5 holds, i.e., .

Proposition 5 implies the following:

-

•

The optimal revenue increases as the entries of the weighted network effects increases.

-

•

Since , the limiting revenue as becomes (see Horn and Johnson (2012, Chapter 5))

-

•

For a weakly-tied block model and small enough , we have and the first order Taylor series of leads to

This shows that revenue becomes higher as the weighted summation of network externalities increases, where the weights are given by . This establishes that revenue is higher when we have higher externality among blocks with higher sizes.

Proof of Proposition 5

The critical thresholds defining the buyers’ equilibrium satisfy

| (8.29) |

with the convention that . Eq. (8.29) leads to

| (8.30) |

with the convention . The normalized revenue can be written as

| (8.31) |

which we need to maximize over non-decreasing price sequences, i.e., . We show that the optimal solution is , . We establish this by using the sufficient KKT conditions for optimality (Bertsekas (1999, Proposition 3.3.2)). Following the notations used in Bertsekas (1999), we let

With this notation, the optimization problem can be rewritten as

Letting and

we have

| (8.32) | |||

| (8.33) | |||

| (8.34) | |||

| (8.35) | |||

| (8.36) |

In particular, Eq. (8.32) and Eq. (8.33) are straightforward to verify, Eq. (8.34) holds as all inequalities are active and Eq. (8.35) holds because we have

where we used in the last inequality. Finally, Eq. (8.36) holds because all that satisfy the conditions are of the form for some non-zero for which

Therefore, using Bertsekas (1999, Proposition 3.3.2), , is the optimal price sequence which results in revenue

Finally, note that with price sequence for , Eq. (Proof of Proposition 5) results in , showing that the critical thresholds are in .

References

- Ajorlou et al. (2016) Amir Ajorlou, Ali Jadbabaie, and Ali Kakhbod. Dynamic pricing in social networks: The word-of-mouth effect. Management Science, 2016.

- Alizamir et al. (2017) Saed Alizamir, Ningyuan Chen, and Vahideh Manshadi. Promotion planning of network goods. 2017.

- Au and Kauffman (2001) Yoris A Au and Robert J Kauffman. Should we wait? network externalities, compatibility, and electronic billing adoption. Journal of Management Information Systems, 18(2):47–63, 2001.

- Ballester et al. (2006) Coralio Ballester, Antoni Calvó-Armengol, and Yves Zenou. Who’s who in networks. wanted: the key player. Econometrica, 74(5):1403–1417, 2006.

- Belloni et al. (2017) Alexandre Belloni, Changrong Deng, and Saša Pekeč. Mechanism and network design with private negative externalities. Operations Research, 65(3):577–594, 2017.

- Bernstein and Martínez-de Albéniz (2016) Fernando Bernstein and Victor Martínez-de Albéniz. Dynamic product rotation in the presence of strategic customers. Management Science, 2016.

- Bertsekas (1999) Dimitri P Bertsekas. Nonlinear programming. Athena scientific Belmont, 1999.

- Besbes and Lobel (2015) Omar Besbes and Ilan Lobel. Intertemporal price discrimination: Structure and computation of optimal policies. Management Science, 61(1):92–110, 2015.

- Bloch and Quérou (2013) Francis Bloch and Nicolas Quérou. Pricing in social networks. Games and economic behavior, 80:243–261, 2013.

- Board and Skrzypacz (2016) Simon Board and Andrzej Skrzypacz. Revenue management with forward-looking buyers. Journal of Political Economy, 124(4):1046–1087, 2016.

- Bonacich (1987) Phillip Bonacich. Power and centrality: A family of measures. American journal of sociology, 92(5):1170–1182, 1987.

- Borgs et al. (2014) Christian Borgs, Ozan Candogan, Jennifer Chayes, Ilan Lobel, and Hamid Nazerzadeh. Optimal multiperiod pricing with service guarantees. Management Science, 60(7):1792–1811, 2014.

- Bramoullé and Kranton (2007) Yann Bramoullé and Rachel Kranton. Public goods in networks. Journal of Economic Theory, 135(1):478–494, 2007.

- Bramoullé et al. (2014) Yann Bramoullé, Rachel Kranton, and Martin D’amours. Strategic interaction and networks. The American Economic Review, 104(3):898–930, 2014.

- Brynjolfsson and Kemerer (1996) Erik Brynjolfsson and Chris F Kemerer. Network externalities in microcomputer software: An econometric analysis of the spreadsheet market. Management Science, 42(12):1627–1647, 1996.

- Cachon and Feldman (2015) Gérard P Cachon and Pnina Feldman. Price commitments with strategic consumers: Why it can be optimal to discount more frequently… than optimal. Manufacturing & Service Operations Management, 17(3):399–410, 2015.

- Candogan et al. (2012) Ozan Candogan, Kostas Bimpikis, and Asuman Ozdaglar. Optimal pricing in networks with externalities. Operations Research, 60(4):883–905, 2012.

- Chen (2012) Chia-Hui Chen. Name your own price at priceline. com: Strategic bidding and lockout periods. Review of Economic Studies, 79(4):1341–1369, 2012.

- Chen and Farias (2015) Yiwei Chen and Vivek F Farias. Robust dynamic pricing with strategic customers. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, pages 777–777. ACM, 2015.

- Coase (1972) Ronald H Coase. Durability and monopoly. The Journal of Law and Economics, 15(1):143–149, 1972.

- Cohen and Harsha (2013) Maxime Cohen and Pavithra Harsha. Designing price incentives in a network with social interactions. 2013.

- Dilme and Li (2016) Francesc Dilme and Fei Li. Revenue management without commitment: dynamic pricing and periodic fire sales. Available at SSRN 2435982, 2016.

- Fainmesser and Galeotti (2016) Itay P Fainmesser and Andrea Galeotti. Pricing network effects: Competition. 2016.

- Farrell and Saloner (1985) Joseph Farrell and Garth Saloner. Standardization, compatibility, and innovation. The RAND Journal of Economics, pages 70–83, 1985.

- Galeotti and Goyal (2009) Andrea Galeotti and Sanjeev Goyal. Influencing the influencers: a theory of strategic diffusion. The RAND Journal of Economics, 40(3):509–532, 2009.

- Gallaugher and Wang (2002) John M Gallaugher and Yu-Ming Wang. Understanding network effects in software markets: evidence from web server pricing. Mis Quarterly, pages 303–327, 2002.

- Gul et al. (1986) Faruk Gul, Hugo Sonnenschein, and Robert Wilson. Foundations of dynamic monopoly and the coase conjecture. Journal of Economic Theory, 39(1):155–190, 1986.

- Hart and Tirole (1988) Oliver D Hart and Jean Tirole. Contract renegotiation and coasian dynamics. The Review of Economic Studies, 55(4):509–540, 1988.

- Holland et al. (1983) Paul W Holland, Kathryn Blackmond Laskey, and Samuel Leinhardt. Stochastic blockmodels: First steps. Social networks, 5(2):109–137, 1983.

- Horn and Johnson (2012) Roger A Horn and Charles R Johnson. Matrix analysis. Cambridge university press, 2012.

- Hörner and Samuelson (2011) Johannes Hörner and Larry Samuelson. Managing strategic buyers. Journal of Political Economy, 119(3):379–425, 2011.

- Katz and Shapiro (1985) Michael L Katz and Carl Shapiro. Network externalities, competition, and compatibility. The American economic review, 75(3):424–440, 1985.

- Krishna (2009) Vijay Krishna. Auction theory. Academic press, 2009.

- Li et al. (2014) Jun Li, Nelson Granados, and Serguei Netessine. Are consumers strategic? structural estimation from the air-travel industry. Management Science, 60(9):2114–2137, 2014.

- Lingenbrink and Iyer (2018) David Lingenbrink and Krishnamurthy Iyer. Signaling in online retail: Efficacy of public signals. 2018.

- Liu and Van Ryzin (2008) Qian Liu and Garrett J Van Ryzin. Strategic capacity rationing to induce early purchases. Management Science, 54(6):1115–1131, 2008.

- Lobel et al. (2015) Ilan Lobel, Jigar Patel, Gustavo Vulcano, and Jiawei Zhang. Optimizing product launches in the presence of strategic consumers. Management Science, 62(6):1778–1799, 2015.

- Lorentz (2012) George G Lorentz. Bernstein polynomials. American Mathematical Soc., 2012.

- Mubayi et al. (2001) Dhruv Mubayi, Todd G Will, and Douglas B West. Realizing degree imbalances in directed graphs. Discrete Mathematics, 239(1-3):147–153, 2001.

- Myerson (1981) Roger B Myerson. Optimal auction design. Mathematics of operations research, 6(1):58–73, 1981.

- Pai and Vohra (2013) Mallesh M Pai and Rakesh Vohra. Optimal dynamic auctions and simple index rules. Mathematics of Operations Research, 38(4):682–697, 2013.

- Papanastasiou and Savva (2016) Yiangos Papanastasiou and Nicos Savva. Dynamic pricing in the presence of social learning and strategic consumers. Management Science, 2016.

- Rohlfs (1974) Jeffrey Rohlfs. A theory of interdependent demand for a communications service. The Bell Journal of Economics and Management Science, pages 16–37, 1974.

- Talluri and Van Ryzin (2006) Kalyan T Talluri and Garrett J Van Ryzin. The theory and practice of revenue management, volume 68. Springer Science & Business Media, 2006.

- Tirole (1988) Jean Tirole. The theory of industrial organization. MIT press, 1988.

- White et al. (1976) Harrison C White, Scott A Boorman, and Ronald L Breiger. Social structure from multiple networks. i. blockmodels of roles and positions. American journal of sociology, 81(4):730–780, 1976.

- Yang and Zhang (2015) Nan Yang and Philip Renyu Zhang. Dynamic pricing and inventory management under network externality. Available at SSRN 2571705, 2015.