Convergence analysis of quasi-Monte Carlo sampling for quantile and expected shortfall

Abstract.

Quantiles and expected shortfalls are usually used to measure risks of stochastic systems, which are often estimated by Monte Carlo methods. This paper focuses on the use of quasi-Monte Carlo (QMC) method, whose convergence rate is asymptotically better than Monte Carlo in the numerical integration. We first prove the convergence of QMC-based quantile estimates under very mild conditions, and then establish a deterministic error bound of for the quantile estimates, where is the dimension of the QMC point sets used in the simulation and is the sample size. Under certain conditions, we show that the mean squared error (MSE) of the randomized QMC estimate for expected shortfall is . Moreover, under stronger conditions the MSE can be improved to for arbitrarily small .

Key words and phrases:

quasi-Monte Carlo method, quantile, value-at-risk, expected shortfall, conditional value-at-risk2010 Mathematics Subject Classification:

Primary 65D30, 65C051. Introduction

Many application areas use quantiles or expected shortfalls to measure risks of stochastic systems. For instance, in the financial industry, a quantile (known as value-at-risk) plays an important role for quantifying and managing portfolio risk. On the other hand, expected shortfall (known as conditional value-at-risk) may provide incentives for risk managers to take into account tail risks beyond quantile. We refer to [8] for a review on the two measures. This paper focuses on estimating quantiles and expected shortfalls via simulation-based methods. Monte Carlo (MC) is a natural method to estimate them. However, the MC approach is often criticized for time-consuming, since value-at-risk estimation is often relevant to rare events simulation. That usually calls for a large number of runs to get accurate estimation. To address this issue, various variance reduction techniques are employed to increase the accuracy of MC. Importance sampling (IS) is a promising variance reduction technique for value-at-risk estimation (see, e.g., [5, 6]).

Beyond the use of MC, Avramidis and Wilson [1] proposed correlation-induction techniques to improve quantile estimation based on Latin hypercube sampling (LHS). They showed that the correlation-inducted LHS estimator is asymptotically normal and unbiased with smaller variance than that of the crude MC. Subsequently, Jin et al. [9] modified the correlation-inducted LHS estimator of [1] and proposed a new quantile estimator based on an indirect means of realizing full stratification of [16] that reuses samples. They showed that the error probability for the stratified quantile estimator is zero for sufficiently large, but finite sample size . Moreover, in some special cases, the convergence rate is , as opposed to the crude MC rate . However, the stratified quantile estimator requires sample sizes that grow exponentially with the dimension of the problem.

Quasi-Monte Carlo (QMC) methods are deterministic versions of the MC methods, and have an asymptotically faster convergence rate than MC as shown in the field of numerical integration. It is straightforward to use QMC methods for estimating quantiles and expected shortfalls. Particularly, Papageorgiou and Paskov [18] observed from empirical studies that QMC methods provide a highly efficient alternative to MC for quantile calculation. Jin and Zhang [10] aimed at smoothing QMC estimators via Fourier transformation so that the faster convergence rate of QMC methods can be reclaimed. To the best of our knowledge, the convergence and the rates of convergence for plain QMC in estimating quantile and expected shortfall are still unclear.

In this paper, we focus on the use of QMC and randomized QMC (RQMC) for estimating quantile and expected shortfall. We first prove the convergence of QMC-based quantile estimates, and establish some useful error bounds for assessing the error rate. We then provide an error bound for the expected shortfall estimate, and find that the efficiency of the expected shortfall estimate is strongly tied to the efficiency of (R)QMC quadrature for a specific discontinuous function and a specific function with kinks. Under mild conditions, we show that the mean squared error (MSE) of the RQMC-based expected shortfall estimate is , which is asymptotically better than plain MC and LHS. Moreover, under stronger conditions the MSE can be improved to for arbitrarily small , where is the dimension of the problem.

The rest of this paper is organized as follows. In Section 2, we introduce some background on quantile estimation and some preliminary results on QMC methods. In Section 3, we study the convergence and the convergence rate of QMC-based quantile estimate. In Section 4, we study the MSE of QMC-based expected shortfall estimate. In Section 5, we perform a numerical study for stochastic network models for which our theoretical results can be applied. Section 6 concludes this paper.

2. Preliminaries

Let be a real-valued random variable of interest with a cumulative distribution function (CDF) . For instance, is the loss or profit of a portfolio over a given holding period. We are interested in the left tail of the distribution of . For a fixed , the quantity

| (2.1) |

is called the ’th quantile of (or the value-at-risk of in the context of risk management). The expected shortfall of is defined as

| (2.2) |

where . The expected shortfall is also known as the tail conditional expectation or conditional value-at-risk. Assume that the variable can be simulated easily. Our goal is to estimate the quantile and the expected shortfall by means of simulation.

In the MC setting, the CDF of can be estimated by the empirical CDF

| (2.3) |

where ’s are independent and identically distributed random replications of . The quantile is then estimated by

| (2.4) |

Let be the th-order statistic of . It is easy to see that , where denotes the smallest integer no less than . The corresponding estimate of the expected shortfall is given by

| (2.5) |

Serfling [20] showed that with probability 1 (w.p.1) as under very mild assumptions. If has a continuous density in a neighborhood of and , Serfling [20] further showed that is asymptotically normally distributed. For the expected shortfall estimate (2.5), Trindade et al. [22] found that under certain conditions, w.p.1 as , and is asymptotically normally distributed.

MC is often criticized for its slow convergence. QMC has the potential to improve the convergence rate. We now turn to the regime of QMC in estimating quantiles and expected shortfalls. To start with, let’s consider the problem of estimating an integral over the unit cube

QMC quadrature rule takes the average

| (2.6) |

where are carefully chosen points in . The Koksma-Hlawka inequality gives a deterministic error bound for the quadrature rule (2.6)

| (2.7) |

where , is the variation of in the sense of Hardy and Krause, and is the star-discrepancy of points in ; see [13] for details. There are many ways to construct point sets such that . As a result, the QMC error is for integrands with bounded variation in the sense of Hardy and Krause (BVHK). In this paper, we restrict our attention to -sequences or -nets in base (see the definitions below).

Definition 2.1.

An elementary interval in base is a subset of of the form

| (2.8) |

where , with for .

The elementary interval (2.8) is a hyperrectangle of volume . For given , the unit cube is partitioned into elementary intervals of the form (2.8).

Definition 2.2.

Let and be nonnegative integers with . A point set of points is a -net in base if every elementary interval in base of volume contains exactly points of the point set.

Definition 2.3.

Let be a nonnegative integer. An infinite sequence is a -sequence in base if the finite point set is a -net in base for all and .

For QMC, it is important to obtain an estimate of the quadrature error . But both the variation and the star discrepancy in the upper bound (2.7) are very hard to compute, and the upper bound is restricted to functions of finite variation. Instead, one can randomize the points and treat the random version of the quadrature in (2.6) as an RQMC quadrature rule. Usually, the randomized points are uniformly distributed over , and the low discrepancy property of the points is preserved under the randomization (see [11] and Chapter 13 of the monograph [3] for a survey of various RQMC methods). In this paper, we focus on the scrambling technique proposed by [14] to randomize -sequences or -nets.

QMC methods are designed to sample -dimensional vectors that are uniformly distributed on the unit cube . To fit into the setting of quantile estimation, one needs to know the mechanism of sampling the target variable via standard uniform distributed variables. In what follows, we assume that the target variable can be generated by

| (2.9) |

where the function is easily computed. For practical problems, it may be easy to obtain the mapping by using the multivariate inverse transformation proposed by Rosenblatt [19]. In the QMC setting, we shall rewrite the empirical CDF (2.3) as

| (2.10) |

where are QMC or RQMC points. The QMC estimate of the quantile is then obtained by the formula (2.4). The expected shortfall estimate (2.5) is then replaced by

3. Convergence analysis for QMC quantile estimation

In this section, we first show the convergence of QMC estimates for quantile estimation under very mild conditions. Then we give a deterministic error bound for QMC estimates under some relatively stronger conditions.

Theorem 3.1.

Let be a random variable with CDF . The empirical CDF given by (2.10) is based on QMC points. Assume that

-

(i)

is the unique solution of , and

-

(ii)

for all .

Then as .

Proof.

By the definition of in (2.4), we have

for all . By the uniqueness condition (i) and the definition of in (2.1), we find that for any ,

| (3.1) |

Assume that does not converge to . Then there exists an and an infinite sequence of positive integers with such that for all . If , then By condition (ii),

This leads to a contradiction because by using (3.1).

On the other hand, if , then . By condition (2),

That also leads to a contradiction because . As a result, converges to as goes to infinity. ∎

The uniqueness condition (i) is also the minimal requirement for establishing the strong consistency of the associated MC estimate [20, p. 75]. Condition (ii) implies that the empirical CDF converges to the true CDF for all in the QMC setting. Recall that the random variable can be generated via the mapping (2.9). This calls for the Jordan measurability of the set

for all .

Corollary 3.2.

Suppose that the point set used in (2.10) is the first points of a -net in base . If is the unique solution of and is Jordan measurable for all , then as .

Proof.

Note that Riemann integrability of may not lead to Riemann integrability of the indicator function . Chen et al. [2] gave such an example by using Thomae’s function. By Lebesgue’s theorem (see [12]), is Riemann integrable (or equivalently, is Jordan measurable) iff , where is the Lebesgue measure in .

Definition 3.3.

For a set , the outer parallel body of at distance is defined as

where denotes the Euclidean norm. When , we use a convention that for any .

Let a positive nondecreasing function defined for all and satisfying . Then we let be the family of all Lebesgue-measurable for which

Every is actually Jordan measurable. Conversely, every Jordan measurable subset of belongs to for a suitable function (see [13, pp. 168-169]). To establish an error bound of quantile estimate, we need a stronger condition that has a common upper bound for in a neighborhood of . For , denote as a -neighborhood of .

Assumption 3.4.

Assume that has a density in a neighborhood of and is positive and continuous at .

Assumption 3.5.

Assume that there exist a positive nondecreasing function satisfying and such that

for any .

Theorem 3.6.

Proof.

By Definition 2.2, there exist disjoint elementary intervals with volume such that all contain exactly points of the -net in base . Let , and denote as the number of the points of the -net contained in the set . By the fairness of the elementary intervals, we have

Similarly to the proof of Lemma 4.1 in [7], one can choose with length as small as possible. By doing so, the length of is no larger than

Let’s assume that by taking large enough . By Assumption 3.5,

Therefore, we have

| (3.2) |

If the set is convex for all , then with for small enough. This is because the volume for any convex set is bounded by that of the case , which is no larger than for small enough (see the proof of Lemma 3.7). By Theorem 3.6, the deterministic error bound for the QMC-based quantile estimate becomes

The result may be extended to pseudo-convex sets (see [23]). However, the convex conditions on may be restrictive for practical problems. We next show that under the Lipschitz continuity condition on , for some constant . The same rate also applies for this case.

Lemma 3.7.

Suppose that is Lipschitz continuous over with modulus . If Assumption 3.4 is satisfied, there exist such that

for any .

Proof.

Let be the boundary of the unit cube , and let . Note that . As a result,

Note that . So there exists such that for any . For any , there exists such that . Since is Lipschitz, . Therefore,

By Assumption 3.4, there exists such that for all . Let . Assume that and . By the mean value theorem, for some . Using gives for all and all .

∎

Theorem 3.8.

4. Convergence analysis for RQMC expected shortfall estimation

In this section, we study the MSE of the expected shortfall estimate when using RQMC. Define , which is estimated by

| (4.1) |

where are given in (2.10). Note that can be viewed as a QMC quadrature rule and for the kink function . Also, and . The following lemma gives a relationship between the quantile estimation error and the expected shortfall estimation error.

Lemma 4.1.

Proof.

Theorem 4.2.

Suppose that the point set used in (2.10) and (2.11) is a scrambled -net in base , where . Suppose additionally that Assumptions 3.4 and 3.5 are satisfied and . Then for large enough,

| (4.2) |

where

and is given in Assumption 3.5. Particularly, . If is of BVHK and for some constant , then

for arbitrarily small .

Proof.

It is known that a scrambled -net is a -net w.p.1 (see [14]). By combining Theorem 3.6 and Lemma 4.1, we have

For any square-integrable integrands, as shown in [15], the scrambled net variance with sample size is . This implies and , leading to .

Since for some constant , it is easy to see that admits ()-dimensional Minkowski content (see [7]). By Theorem 3.5 in [7], we have for arbitrarily small . By Theorem 4.4 in [7], we have . Consequently, .

∎

Remark 4.3.

The deterministic error bound for the quantile estimate established in Theorem 3.6 plays an important role in studying the MSE of the expected shortfall estimate. The convergence result in Theorem 3.1 does not help to bound the MSE. Observed from (4.2), the accuracy of the expected shortfall estimate depends strongly on the RQMC integration of the kink function . This implies that if the RQMC quadrature rule yields a faster rate of convergence for the kink function, one can expect a better performance of the expected shortfall estimate. However, if is not of BVHK, it may be hard to predict the MSE rate for the function unless using the worst-case rate .

5. Numerical Examples

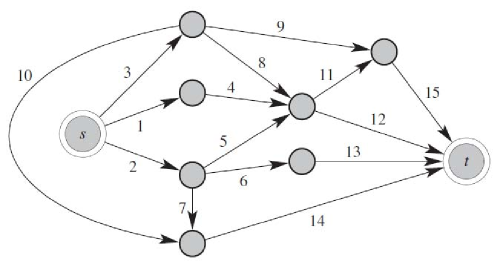

A stochastic activity network (SAN) models the time to compute a project having activities with random durations and precedence constraints. Figure 1 shows an instance of SAN with activities, which correspond to the edges in the network. Dong and Nakayama [4] studied this model with LHS. Let denote the time to complete the activity . Assume that the activity durations are independent exponential random variables , i.e., the density of is given by , where . The network in Figure 1 has paths form nodes to , denoted by . Specially, , , , , , , , . The time to complete the project can be modeled by the random variable

We are interested in estimating the quantile of . To simulate the model using QMC, we generate for . As a result, can be expressed a function of , denoted by . It should be noted that is not Lipschitz continuous. So Theorem 3.8 cannot be applied directly. To circumvent this, we rewrite the set as , where

Let , and let . Then . It is easy to see that is Lipschitz continuous over because for all . So by Lemma 3.7 and using , the conditions in Theorem 3.6 are satisfied with for some constant . The QMC error for the quantile estimation is .

We now study the MSE of the expected shortfall estimate when using RQMC. By Theorem 4.4 in [7], we have since . Using (4.2) gives

However, since is not of BVHK, the rate established in Theorem 3.5 of [7] cannot be applied for the integrand . Instead, using the worst-case rate arrives at . This confirms that RQMC performs asymptotically better than MC and LHS for expected shortfall estimation. The MSE rate may be too conservative when is small.

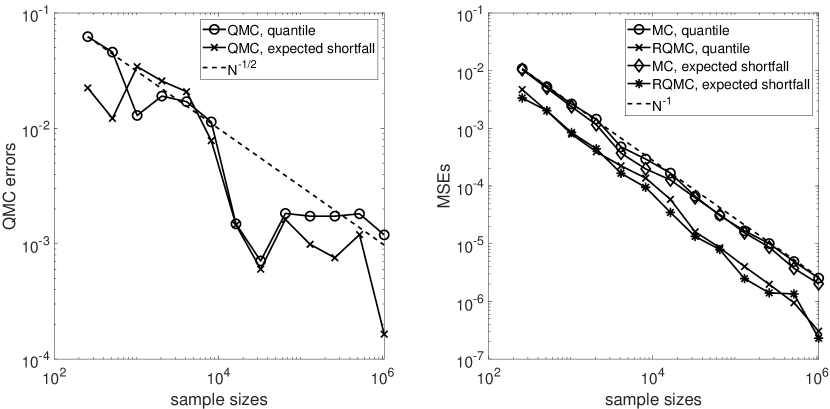

Figure 2 shows the numerical results for the SAN model in Figure 1 with for and for . In the numerical experiments, we use Sobol’ points as inputs for QMC-based estimates and scrambled Sobol’ points for RQMC-based estimates. The MSEs in right panel of Figure 2 are computed based on 100 independent repetitions. Estimation of the errors requires knowing the true value of the quantity being estimated. Here we use the MC method with a very large sample size (say, ) to obtain accurate estimates of and and treat them as the true values. We consider the case for which the true values are The empirical evidence shows convergence rates of (R)QMC beyond the crude MC rate of . Particularly, RQMC yields lower MSEs than MC for both the quantile and the expected shortfall estimations.

6. Conclusion

In this paper, we proved the convergence of QMC-based quantile estimates under very mild assumptions. More importantly, we proved that the QMC error is bounded from above by . The error rate is worse than the usual MC rate for . But this error rate is critical to establish considerable MSE rates of RQMC for expected shortfall estimation. It is possible to obtain a faster error rate for RQMC-based quantile estimates as suggested by the numerical study. Owen [15] showed that scrambled net quadrature rules can yield an MSE of for square-integrable functions. We conjecture that RQMC-based quantile estimation can also lead to an MSE of under some technical conditions. We leave this problem open for future research.

References

- [1] A. N. Avramidis and J. R. Wilson, Correlation-induction techniques for estimating quantiles in simulation experiments, Oper. Res. 46 (1998), no. 4, 574–591.

- [2] S. Chen, J. Dick, and A. B. Owen, Consistency of Markov chain quasi-Monte Carlo on continuous state spaces, Ann. Stat. 39 (2011), no. 2, 673–701.

- [3] J. Dick and F. Pillichshammer, Digital nets and sequences: Discrepancy theory and quasi-monte carlo integration, Cambridge University Press, 2010.

- [4] H. Dong and M. K. Nakayama, Quantile estimation with Latin hypercube sampling, Oper. Res. 65 (2017), no. 6, 1678–1695.

- [5] P. Glasserman, P. Heidelberger, and P. Shahabuddin, Variance reduction techniques for estimating value-at-risk, Management Sci. 46 (2000), no. 10, 1349–1364.

- [6] P. W. Glynn, Importance sampling for Monte Carlo estimation of quantiles, Mathematical Methods in Stochastic Simulation and Experimental Design: Proceedings of the 2nd St. Petersburg Workshop on Simulation, 1996, pp. 180–185.

- [7] Z. He and X. Wang, On the convergence rate of randomized quasi-Monte Carlo for discontinuous functions, SIAM J. Numer. Anal. 53 (2015), no. 5, 2488–2503.

- [8] L. J. Hong, Z. Hu, and G. Liu, Monte Carlo methods for value-at-risk and conditional value-at-risk: A review, ACM Trans. Model. Comput. Simulation 24 (2014), no. 4, 22.

- [9] X. Jin, M. C. Fu, and X. Xiong, Probabilistic error bounds for simulation quantile estimators, Management Sci. 49 (2003), no. 2, 230–246.

- [10] X. Jin and A. X. Zhang, Reclaiming quasi-Monte Carlo efficiency in portfolio value-at-risk simulation through Fourier transform, Management Sci. 52 (2006), no. 6, 925–938.

- [11] P. L’Ecuyer and C. Lemieux, Recent advances in randomized quasi-Monte Carlo methods, Modeling Uncertainty: An Examination of Stochastic Theory, Methods, and Applications (Moshe Dror, Pierre L’Ecuyer, and Ferenc Szidarovszky, eds.), Kluwer Academic Publishers, 2005, pp. 419–474.

- [12] J. E. Marsden and M. J. Hoffman, Elementary classical analysis, Macmillan, 1993.

- [13] H. Niederreiter, Random Number Generation and Quasi-Monte Carlo Methods, SIAM, Philadelphia, 1992.

- [14] A. B. Owen, Randomly permuted -nets and -sequences, Monte Carlo and Quasi-Monte Carlo Methods in Scientific Computing (H. Niederreiter and P. J.-S. Shiue, eds.), Springer, 1995, pp. 299–317.

- [15] by same author, Monte Carlo variance of scrambled net quadrature, SIAM J. Numer. Anal. 34 (1997), no. 5, 1884–1910.

- [16] by same author, Latin supercube sampling for very high-dimensional simulations, ACM Trans. Model. Comput. Simul. 8 (1998), no. 1, 71–102.

- [17] by same author, Multidimensional variation for quasi-Monte Carlo, International Conference on Statistics in honour of Professor K.-T. Fang’s 65th birthday (J. Fan and G. Li, eds.), 2005.

- [18] A. Papageorgiou and S. H. Paskov, Deterministic simulation for risk management, J. Portfolio Management 25 (1999), no. 5, 122–127.

- [19] M. Rosenblatt, Remarks on a multivariate transformation, Ann. Math. Stat. 23 (1952), no. 3, 470–472.

- [20] R. J. Serfling, Approximation theorems of mathematical statistics, Wiley, New York, 1980.

- [21] L. Sun and L. J. Hong, Asymptotic representations for importance-sampling estimators of value-at-risk and conditional value-at-risk, Oper. Res. Lett. 38 (2010), no. 4, 246–251.

- [22] A. A. Trindade, S. Uryasev, A. Shapiro, and G. Zrazhevsky, Financial prediction with constrained tail risk, J. Banking Finance 31 (2007), no. 11, 3524–3538.

- [23] H. Zhu and J. Dick, Discrepancy bounds for deterministic acceptance-rejection samplers, Electron. J. Stat. 8 (2014), no. 1, 678–707.