Mini-Flash Crashes, Model Risk, and Optimal Execution

Abstract.

Oft-cited causes of mini-flash crashes include human errors, endogenous feedback loops, the nature of modern liquidity provision. We develop a mathematical model which captures aspects of these explanations. Empirical features of recent mini-flash crashes are present in our framework. For example, there are periods when no such events will occur. If they do, even just before their onset, market participants may not know with certainty that a disruption will unfold. Our mini-flash crashes can materialize in both low and high trading volume environments and may be accompanied by a partial synchronization in order submission.

Instead of adopting a classically-inspired equilibrium approach, we borrow ideas from the optimal execution literature. Each of our agents begins with beliefs about how his own trades impact prices and how prices would move in his absence. They, along with other market participants, then submit orders which are executed at a common venue. Naturally, this leads us to explicitly distinguish between how prices actually evolve and our agents’ opinions. In particular, every agent’s beliefs will be expressly incorrect.

Key words and phrases:

Flash crash, model error, optimal execution.2010 Mathematics Subject Classification:

Primary 91G80; Secondary 60H30, 60H10, 34M351. Overview

Amidst the violent market disruption on May 6, 2010, the infamous Flash Crash,

“Over 20,000 trades across more than 300 securities were executed at prices more than 60% away from their values just moments before. Moreover, many of these trades were executed at prices of a penny or less, or as high as $100,000, before prices of those securities returned to their ‘pre-crash’ levels” ([2]).

Today, this particular event remains so memorable due to its remarkable scale.

In fact, lesser versions of the Flash Crash, or mini-flash crashes, happen quite often. Anecdotal evidence suggests that there may be over a dozen every day ([22]). A rigorous empirical analysis uncovered “18,520 crashes and spikes with durations less than 1,500 ms” in stock prices from 2006 through 2011 ([31]). The exhaustive documentation on Nanex LLC’s “NxResearch” site offers further corroboration as well ([4]).

Why do such phenomena occur? Several answers have been proposed. Roughly, most point to human errors, endogenous feedback loops, the nature of modern liquidity provision. These ideas can be viewed as different ways to rationalize how an extreme (local or global) dislocation in supply and demand can arise in modern markets. Our contribution is the development of a model which captures this. Our model also appears to exhibit features of historical mini-flash crashes. For instance, there are periods in which extreme price moves will not manifest. If they do, accompanying trade volumes can be high or low. Some market participants may partially synchronize their trading during a mini-flash crash. Our agents may not know that a mini-flash crash is about to begin even just before its onset.

Our results seem to be aligned with intuitive expectations as well. For example, our mini-flash crashes can begin if some of our agents are too uncertain about their initial beliefs, inaccurate in their understanding of price dynamics, slow to update their models and objectives, or willing to take on risk.

We construct our model beginning with a finite population of agents trading in a single risky asset, each of whom must decide how to act based upon his own preferences, beliefs, and observations. Our specifications are drawn from ideas in the price impact and optimal execution literature and are given in Sections 3.1 - 3.2.

We imagine that our agents’ orders are submitted to a single venue, where they are executed together with trades from other (unmodeled) market participants. This naturally compels us to make an explicit distinction between how the risky asset price actually evolves and our agents’ beliefs about its future evolution (see Section 3.3).

Since we view our agents as simultaneously solving their own optimal execution problems, we avoid certain strong assumptions that would have been implicitly needed, if we had used a classical equilibrium-based approach. We use a similar framework to [12, 15] in that our players’ interaction with the rest of the world (in addition to each other) is given by a price impact model. An additional consequence is that we precisely describe the errors in our agents’ beliefs. Potentially, each agent could be wrong both about how his trades affect prices and how prices would move in his absence.

To the best of our knowledge, this general setup appears to be a new paradigm for modeling heterogeneous agent systems in the contexts of optimal execution and mini-flash crashes.

We are ready to begin presenting our work in detail. We highlight key background material and our paper’s contributions in relation to it in Section 2. Our agents and their beliefs are described in Section 3. We describe the correct dynamics of the risky asset’s price in Section 3.3. General analysis of the dynamical system when our agents act as prescribed by Section 3 but prices actually move as in Section 3.3 are given in Section 4. Using the material in Section 4, we obtain explicit characterization of mini-flash crashes when uncertain agents are semi-symmetric in 5. Numerical examples illustrating our main results are given in Section 6. Our longer proofs are contained in Appendices A - C.

2. Background & Contributions

In this section, we clarify our contributions and explain how they fit into the current literature. We already mentioned that existing theories on the causes of mini-flash crashes could be viewed as falling into one of five categories (see Section 1). Here are further details.

-

i)

Human errors (and, relatedly, improper risk management) are among the most commonly cited causes of mini-flash crashes ([29], [35], [5]). The SEC claims that the majority of mini-flash crashes originate from such sources, in fact ([35]). When we read about fat finger trades, rogue algorithms, or glitches in the media, typically human errors are indirectly responsible. For example, due to a bug in the systems at the Tokyo Stock Exchange and a typo in a trade submitted by Mizuho Securities, the share price of the recruitment agency J-Com fell in minutes from 672,000 to 572,000 on December 8, 2005 ([1]).

-

ii)

Mini-flash crashes may be caused by the rapid, endogenous formation of positive feedback loops ([3], [31], [23], [29], [28], [30]). As Johnson et al. put it,

“Crowds of agents frequently converge on the same strategy and hence simultaneously flood the market with the same type of order, thereby generating the frequent extreme price-change events” ([31]).

A separate empirical study on the Flash Crash of May 6, 2010, specifically, determined that at its peak, “95% of the trading was due to endogenous triggering effects” ([23]).

-

iii)

The nature of liquidity provision in modern markets is thought to cause some mini-flash crashes ([33], [20], [18], [27], [32], [26], [19]). Today, the majority of liquidity is provided by participants that are free from formal market-making obligations ([18]). In particular, they can instantly vanish, effectively taking one or both sides of the order book at some venue with them. A mini-flash crash can arise either directly as bid-ask spreads blow out or indirectly when a market order (of any size) tears through a nearly empty collection of limit orders. Such a phenomenon has been called fleeting liquidity and may have contributed to the occurrence of 38% of mini-flash crashes from 2006 - 2011 ([27]).

This proposed explanation is deeply intertwined with a crucial empirical observation: Mini-flash crashes occur in both high and low trading volume regimes. For instance, the trading volume during the 30s mini-flash crash of “WisdomTree LargeCap” Growth Fund on November 27, 2012 was nearly eight times the average daily trading volume for this security ([5]). The empirical study by Florescu et al. offers extensive evidence that mini-flash crashes often occur during low trading volume periods as well.

Aspects of (i), (ii), and (iii) are reflected in our work. For example, the human error theory arises in each of the following ways:

- a)

- b)

-

c)

Every agent’s trades may also indirectly impact prices by inducing others to make different decisions than they would otherwise (see Section 3.2 and Section 3.3). This potential effect is not modeled by our agents (see Section 3.1). More generally, even if we have a single agent in our setup trading with other unspecified market participants, the parameters in his fundamental value model might be inaccurate (see Section 3.1 and Section 3.3).

- d)

- e)

- f)

-

g)

Every agent has a model for how prices are affected by the temporary impact of trades (see Section 3.1). In some cases, there will be a mini-flash crash if our agents sufficiently underestimate the role of aggregate temporary impact. No such disturbance will occur otherwise. Our agents may be more prone to induce mini-flash crashes in this way when there are many of them (see Lemmas 4.2 and 5.1).

Notice that some of our agents’ human errors directly cause mini-flash crashes, though not all (see Proposition 4.2). We highlight this observation in Figures 1 - 3. Implicitly, the occasional absence of mini-flash crashes also agrees with (i). Despite the regularity of these disruptions on a market-wide basis, individual securities may rarely experience such an event. Similarly, traders’ models and strategies do roughly achieve their intended goals much of the time, which we observe as well (see Proposition 4.2).

Several key ideas from the endogenous feedback loop theory are present in our paper. For example, if a mini-flash crash does occur, it almost surely does so because of “endogenous triggering effects.” Specifically, our mini-flash crashes arise when some of our agents buy or sell at faster and faster rates, which they only do because they started trading more rapidly in the first place (see Section 3.3 and Lemma 4.1). As predicted by this theory, some of our agents also “converge on the same strategy” during mini-flash crashes: In certain cases, the agents driving these events all buy or sell together with the same (exploding) growth rate (see Theorems 5.1 and 5.2). Figures 5, 8, and 11 graphically illustrate this partial synchronization.

We do not explicitly model liquidity providers in our framework, as we view our agents as submitting market orders to a single venue (see Section 3.3). We still view our paper as reflecting (iii), at least in some sense, since our mini-flash crashes can be accompanied by both high and low trading volumes (see Corollary 3.1 and Theorems 5.1 and 5.2). Visualizations of this point are provided in Figures 4, 6, 7, 9, 10, and 12.

3. Agents and the Execution Price

In this section we describe our agents and their individual optimal execution problems. We end this section by introducing the “true” execution price.

3.1. Agents’ Models

Our agents trade continuously by optimally selecting a trading rate from a particular class of admissible strategies. To motivate our specifications of their choices and objectives, we first define their models and beliefs.

All trades submitted at time are executed immediately at the price . At each time , every agent observes the correct value of . No agent knows the true dynamics of the stochastic process , though.

In our framework, Agent ’s models the the risky asset without his own trading by

| (3.1) |

where is a Wiener process and is a normally distributed with mean and variance which is independent of the Wiener process. (In what follows we will write down for the probability measure of agent .) This drift term represents the price pressure that Agent believes will arise due to the trades of (other) institutional investors. Agent approximates the average behavior of uninformed or noise traders using the Brownian term.111 Almgren & Lorenz provide further details regarding the interpretation of (3.1) ([8]). A possible extension of our work could replace (3.1) with one of the more recent models considered in the literature on optimal trading problems with a learning aspect ([8], [21], [14], [25], [36], [24], [17]). If , then we call Agent an uncertain agent. If , then we call Agent a certain agent. Regardless of whether he is certain or uncertain in this sense, we will soon see that Agent can always be viewed as certain about many things, e.g, he will not change the form of his models, objectives, or admissible strategies on . From this perspective, one might partially connect our work on mini-flash crashes to explanations of longer term financial bubbles based on overconfident investors ([37]).

Intuitively, Agent ’s selection of (3.1) makes the most sense when is large and is short. Notice that Agent makes no attempt to precisely estimate the number of other market participants, nor their individual goals or beliefs. That he believes he cannot improve the predictive accuracy of (3.1) by doing so appears to suggest that the population of traders is of sufficient size. Together with the fact that real drifts and volatilities are non-constant, (3.1) only seems even potentially plausible over short periods.

Let be the space of -adapted processes of trading speeds such that is continuous on for -almost surely,

| (3.2) |

and

| (3.3) |

For any , we denote by

| (3.4) |

the agent’s inventory.

The agent models the execution price as , which is given by

| (3.5) |

Agent has chosen the deterministic positive constants and in (3.5) prior to time . Agent could be viewed as taking into account his own effects on the execution price via an Almgren-Chriss reduced-form model ([7], [6], [9]). would denote Agent ’s estimate for his permanent price impact parameter, while he would approximate his temporary price impact parameter with .

3.2. Each Agent’s Optimization Problem

Agent ’s objective is to maximize the following objective function:

| (3.6) |

This frequently used criteria balances his realized trading revenue and risks associated with delayed liquidation. Agent selects the deterministic risk aversion parameter based upon his appetite.

Let us denote

| (3.7) |

Lemma 3.1.

(3.6) has a unique optimizer almost surely. When is chosen such that is continuous on , satisfies the linear ODE

| (3.8) |

Proof.

See Appendix A.1. ∎

Remark 3.1.

The first term in (3.1) arises from our constraint that Agent must liquidate by the terminal time (see (3.3)). In fact, the weighting factor

tends to as . Intuitively, the reason that Agent believes that and remain finite as is that tends very rapidly to zero.

Agent thinks that he learns about ’s realized value over time, which is captured by the second term in (3.1) since

| (3.9) |

([34]). The factor

is bounded by and tends to zero as .

The second term may either dampen or amplify the effects of the first. Agent believes that the weighting factors reflect that his need to liquidate must eventually overwhelm his desire to profit by trading in the direction of the risky asset’s drift.

An immediate observation from Lemma 3.1 is the following observation for certain agents, which we record as a corollary for ease of referencing.

Corollary 3.1.

If , then does not depend on . In particular, it is deterministic and satisfies the linear ODE

| (3.10) |

3.3. Execution Price

We now specify how actually evolves. While each agent observes the same realized path of this process, in general, no agent knows the correct dynamics.222 There is a single trivial case where this is not true. If , , , , and , our lone agent’s model would be exactly right. An agent’s trading decisions are entirely determined by his beliefs, preferences, and observations of a single realized path of .

Let be a filtered probability space satisfying the usual conditions. The space is equipped with an -Wiener process under , which we denote by . We also have the following deterministic real constants:

can be arbitrary; however, the remaining constants are strictly positive.

The true execution price under is the -adapted process

| (3.11) |

Equation (3.11) can be viewed as a multi-agent extension of the Almgren-Chriss model ([7], [6], [9]). Models of this form, particularly when the ’s (’s) are all identical, have been applied in the context of predatory trading ([13]). On the other hand, [12, 15] consider a mean-field game model where the interactions between the players are through the price as it is here. Although both of these papers address latency and learning in their models misspecification of agents’s models is an important element in our framework. Moreover, our agents do not observe each other or know each other’s parameters. In fact, in our finite player set-up they do not even know the number of players .

In what follows we will say that a mini-flash crash occurs, if the tends to either or on our time horizon.

The parameters and are the correct values of Agent ’s permanent and temporary price impact parameters, respectively. We allow these quantities to have arbitrary relationships to Agent ’s corresponding estimates and . For instance, Agent might underestimate his permanent impact () but perfectly estimate his temporary impact (). Similarly, Agent ’s prior for the correct drift may be accurate or severely mistaken. Comparing our descriptions of in (3.5) and in (3.11), we see that Agent proxies each term in (3.11) as follows:

4. Analysis of the Dynamical System

When our agents implement the strategies that they believe are optimal (see Lemma 3.1) but has the dynamics in (3.11), what happens? The goal of Section 4 is to offer some general answers to this question.

To simplify our presentation, we begin by introducing and analyzing additional notation (see Definition 4.1 and Lemma B.1). We find that our agents’ inventories and trading rates evolve according to a particular ODE system with stochastic coefficients (see Lemma 4.1). Under certain conditions, the system can have a singular point (see Lemma 4.2). For convenience, we study what unfolds when this singular point is of the first kind (see Proposition 4.1). We also examine the case in which there is no singular point (Proposition 4.2).

We will have an even mix of deterministic and stochastic maps. In what follows, we always explicitly indicate -dependence to distinguish between the two. Our equations are solved pathwise, so we do not encounter probabilistic concerns. We will fix such that has a continuous path.

Definition 4.1.

Define the maps

by

Here, are the uncertain agents, whose behavior we are set out to characterize. The behavior of the certain agents are already described. They are not influenced by the execution price but they do have an influence on it.

Definition 4.2.

When has a root on , we let denote the smallest one (see Lemma B.1).

Lemma 4.1.

Suppose that has a root on . If , then , the ’s and the ’s are all uniquely defined and continuous on . Moreover, the uncertain agents’ strategies are characterized by

| (4.1) |

where denotes the first -entries of . When does not have a root on , the same statements hold after replacing with .

Proof.

See Appendix B.1. ∎

Lemma 4.1 does not address the behavior of our uncertain agents’ inventories and trading rates as or . The difficulties are that is non-invertible at , while ’s entries explode at (see Lemma B.1).

The approach for resolving these issues is well-established (see Chapter 6 of [16]). We sketch the key points when has a root on and . Analyzing the effects of ’s explosion at is similar (see Proposition 4.2).

We begin by considering the homogeneous equation corresponding to (4.1):

| (4.2) |

We change notation to emphasize that (4) no longer describes the uncertain agents’ optimal strategies. We next write (4) in a more convenient form.

Lemma 4.2.

Proof.

See Appendix B.2. ∎

Definition 4.3.

Let us denote the unique non-zero eigenvalue of in the above lemma by .

Proposition 4.1.

Suppose that has a root on , , and . If , then for some small ,

| (4.4) |

for . Here,

-

is an eigenbasis for ( corresponds to );

-

is a (non-singular-)matrix-valued analytic function on such that (see (B.6));

-

are constants (see (B.3));

-

and are continuous real-valued functions on (see (B.3)).

We get and on by differentiating (4.1) and by substituting and into (3.11), respectively.

Proof.

See Appendix B.3. ∎

Proposition 4.2.

Suppose that does not have a root on . Then , the ’s and the ’s are all uniquely defined and continuous on . Moreover,

| (4.5) |

Remark 4.1.

Proof.

See Appendix B.4. ∎

5. Explicit Characterizations of Flash Crashes for Semi-Symmetric Uncertain Agents

In this section we thoroughly analyze a broad but tractable class of scenarios. This will enable us to both theoretically and numerically investigate the occurrence of mini-flash crashes. We specify that our uncertain agents’ parameters are identical, except for their initial inventories , means of their initial drift priors , and their initial estimates for the fundamental price . Such agents are nearly symmetric, so we call them semi-symmetric.

Definition 5.1.

We say that our uncertain agents are semi-symmetric when there are positive constants

such that for each

Since ’s and the ’s are the same for (see Definitions 3.7, 4.1, and 5.1). We denote these functions by and , respectively.

Definition 5.1 implies that the diagonal entries of are identical, as are the off-diagonal entries. The same is true for (see Definition 4.1). Such a simplification considerably reduces the difficulties in computing , , and an eigenbasis for (see (C.5) and Lemma 5.2). The ’s, ’s, and ’s only enter in , which also has a nice structure (see (C.23)).

5.1. Results

Lemma 5.1.

Suppose that the uncertain agents are semi-symmetric. Then has a root on and if and only if

| (5.1) |

In this case, the zero of at is of multiplicity 1.

Remark 5.1.

By varying our parameters in (5.1) one at a time we can obtain the following interpretations discussed in Section 2:

- i)

-

ii)

(5.1) holds when is high. A given uncertain agent believes that his own temporary impact parameter is , while the actual collective temporary impact parameter induced by the uncertain agents is . Then is large whenever each uncertain agent severely underestimates his own temporary impact or there are many uncertain agents, giving (g) in Section 2.

- iii)

-

iv)

(5.1) holds when is low. We conclude (e) in Section 2, as measures our uncertain agents’ aversion to volatility risks (see Section 3.2). Observe that both the numerator and the denominator of the LHS in (C.1) roughly look like for small ; however, when is large, the whole LHS looks like since is bounded by 1 on .

Proof.

See Appendix C.1. ∎

Remark 5.2.

Lemma 5.2.

Suppose that the uncertain agents are semi-symmetric and (5.1) holds. Then

| (5.3) |

and the corresponding eigenvector is . By slightly perturbing and/or , if necessary, we can ensure that . In this case, is diagonalizable and the remaining vectors in an eigenbasis for (all with the eigenvalue zero) are

Remark 5.3.

With the exceptions of and , all parameters in (5.3) determine whether or not has a root on (see Lemma 5.1). They also fix the value of (see Remark 5.2). Hence, to interpret (5.3), we only consider the roles of and . These parameters enter (5.3) via

| (5.4) |

Intuitively, (5.4) can be viewed as the ratio of two terms: The numerator measures how far a given uncertain agent’s estimate of his own permanent impact is from the uncertain agents’ actual collective permanent impact. The denominator, which must be positive due to Lemma 5.1, is the corresponding measure for the temporary impact. One might call (5.4) a mistake ratio.

Since by Lemma B.1, is positive only when (5.4) is high enough. We have when the uncertain agents’ total permanent impact and a single uncertain agent’s’ estimate of his own permanent impact are too close or when his estimate exceeds the cumulative permanent impact. More precisely,

| (5.5) |

Whether a mini-flash crash is accompanied by high or low trading volumes is effectively determined by which inequality in (5.3) holds (see Theorems 5.1 and 5.2 and Sections 2, 6.2, and 6.3).

Proof.

See Appendix C.2. ∎

Theorem 5.1.

Remark 5.4.

Since (see Proposition 4.1), (B.3) and Lemma 5.2 imply that will be large and positive when the uncertain agents hold significant, similar long positions. will be of high magnitude but negative, if the uncertain agents carry substantial, similarly-sized short positions. Hence, a spike in is more likely when the uncertain agents are synchronized aggressive buyers, while the odds of a collapse improve when they are synchronized heavy sellers. These effects play the deciding role as , as the integral limits in (5.6) and (5.7) are finite.

Proof.

See Appendix C.3. ∎

Theorem 5.2.

Remark 5.5.

We make no rigorous statement regarding the case. Most of Theorem 5.2’s proof would still be valid (see Appendix C.3); however, the final estimates are especially convenient when (see (C.3) - (C.3)). The over-arching purpose of Theorem 5.2 is only to illustrate that mini-flash crashes can occur in low trading volume environments (see Section 2). Nevertheless, we suspect that mini-flash crashes might unfold when , e.g., see Section 6.2 and (C.3) - (C.3).

Proof.

See Appendix C.3. ∎

6. Numerical illustrations

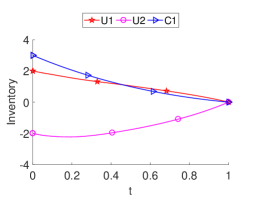

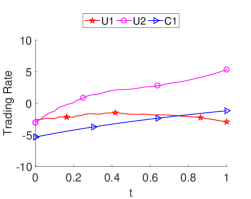

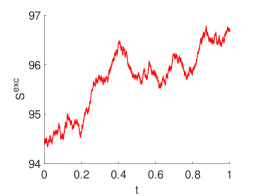

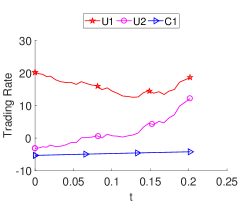

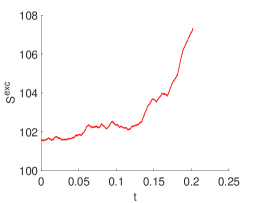

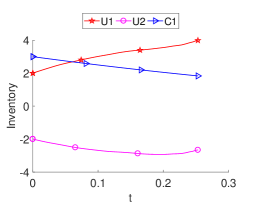

6.1. Example 1: No mini-flash crash

Our mini-flash crashes do not always occur (see Lemmas 4.2 and 5.1). In Section 6.1, we illustrate this by numerically simulating a scenario in which has no root on .

By Lemma 5.1 and (C.5), we know that is non-vanishing on if and only if

| (6.1) |

One selection of parameters for which (6.1) is satisfied is

| (6.8) |

In fact, the LHS of (6.1) then equals 1.1095. Observe that there is no need to specify and as they are irrelevant (see Corollary 3.1, Definition 4.1, and Lemma 4.1). Again, our purposes are only illustrative here, and we leave the reproduction of a specific practically meaningful scenario for a future work.

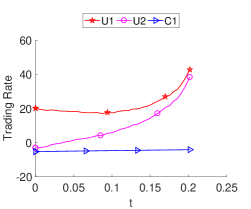

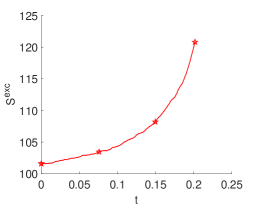

Since and , we have two uncertain agents and one certain agent in the coming plots. We label the corresponding curves with , , and . For example, the label will signify a quantity for Agent 1, the first uncertain agent. In Figures 1 and 2, we plot inventories and trading rates. The execution price is depicted in Figure 3.

The diagrams exhibit all of the important qualities that we expect based upon our theoretical results. Here are a few key features:

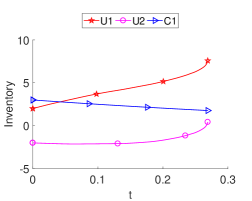

6.2. Example 2: A mini-flash crash with low trading volume

Our mini-flash crashes can be accompanied by low trading volumes (see Theorem 5.2). In Section 6.2, we visualize this by studying a concrete scenario in which has a root on ; ; the zero of at is of multiplicity 1; ; and . The behavior of the ’s is then characterized by Corollary 3.1 and Theorem 5.2. Theorem 5.2 would rigorously describe and the ’s as , if . To improve the quality of our plots, we consider a situation where instead (see Remark 5.5).

By Lemmas 5.1 and 5.2, we must select parameters such that (5.1) is satisfied and

| (6.9) |

is a positive non-integer. We can keep most of our choices in (6.8) the same and only make a few revisions:

| (6.12) |

As in Section 6.1, we do not seek to replicate a particular historical situation. We immediately get (5.1), as its LHS is 4.3302. Using Remark 5.2 and (6.9), we can show that

Again, we have two uncertain agents and one certain agent. We retain the - labeling system from Section 6.1. The inventories, trading rates, and execution price are plotted in Figures 4 - 6. To aid our illustration, we truncate the time domains in Figures 5 - 6 to

for the left and right plots, respectively.

The qualities that we expect based upon Theorem 5.2, and Remark 5.5 are all present. We offered some applicable comments in Section 6.1, so we only add a few new observations here.

- i)

- ii)

- iii)

- iv)

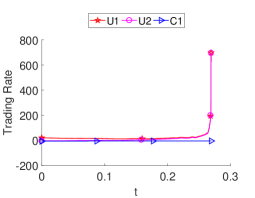

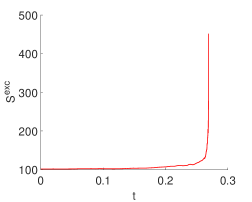

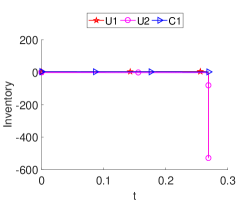

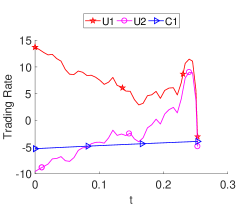

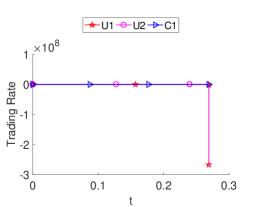

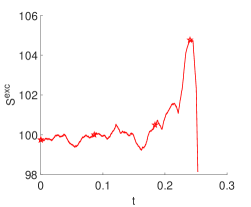

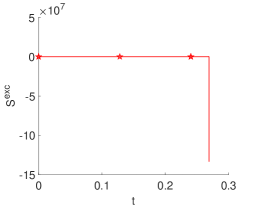

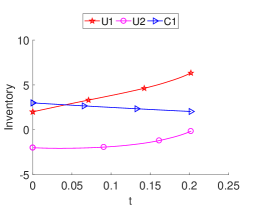

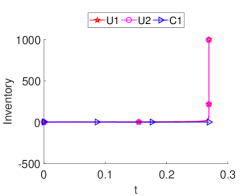

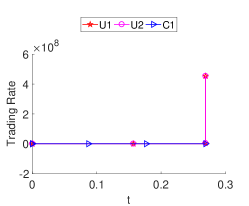

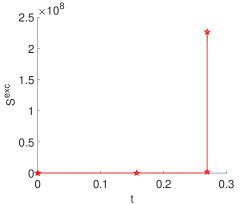

6.3. Example 3: A mini-flash crash with high trading volume

Our mini-flash crashes can also be accompanied by high trading volumes (see Theorem 5.1). We illustrate this in Section 6.3 by simulating a case in which has a root on ; ; the zero of at is of multiplicity 1; ; and . The behaviors of , the ’s, and the ’s are then described by Corollary 3.1 and Theorem 5.1.

We especially wish to emphasize the stochastic explosion direction and do this in two ways.

First, we choose the same deterministic parameters to create Figures 7 - 12. The difference is that one realization of is used in Figures 7 - 9, while another is used in Figures 10 - 12. We denote the corresponding ’s by and , since there are spikes and crashes in the former and latter plots, respectively.

Second, Figures 7 - 9 themselves suggest that the explosion direction is random. This is particularly true in Figures 8 - 9, since we initially notice that the price rapidly rises as the uncertain agents’ buying rates synchronize. Only moments before the mini-flash crash do we see the price collapsing and the uncertain agents’ aggressively selling together.

Now, we need to choose parameters such that (5.1) is satisfied and

is a negative non-integer due to Lemmas 5.1 and 5.1. Compared to Section 6.2, we set

and keep every other parameter the same. As in Sections 6.1 - 6.2, we do not have in mind a special historical example here. Since we have only changed and , the values of and do not differ from Section 6.2; however, is now negative:

The numbers of uncertain and certain agents are still two and one, respectively. We also retain the -labeling system from Sections 6.1 - 6.2. Figures 7 and 10 depict the agents’ inventories. We plot the agents’ trading rates in Figures 8 and 11. The execution price appears in Figures 9 and 12. To help with our visualization, the time domains in the left plots in Figures 7 - 9 and Figures 10 - 12 are truncated to and , respectively.

Our observations regarding Figures 7 - 12 are in agreement with Corollary 3.1 and Theorem 5.1. We have already made note of many important aspects in Sections 6.1 - 6.2 and only remark upon the new details.

- i)

- ii)

- iii)

- iv)

-

v)

The explosion rates in the price and uncertain agents’ trading rates in Section 6.2 are slower than in Section 6.3 (see Figures 5 - 6, Figures 8 - 9, and Figures 11 - 12). We did not explicitly state this previously; however, this is to be expected since trading rates are integrable in Section 6.2 but not in Section 6.3.

7. conclusion

In this paper we show how mini-flash crashes might occur when agents learn and make their decisions based upon misspecified models. We give a necessary and sufficient condition for a mini-flash crash to occur and observe that if the agents

-

i)

are too uncertain about their prior information

-

ii)

sufficiently underestimate the aggregate temporary impact

-

iii)

have long trading periods

-

iv)

have low risk aversion

then mini flash crashes occur.

Our numerical section has three main examples illustrating our three main results. In the first example, we see that not all human errors directly cause mini-flash crashes illustrating Proposition 4.2. Despite the regularity of the human errors on a market-wide basis, individual securities may rarely experience such an event. Similarly, traders’ models and strategies do roughly achieve their intended goals much of the time, as it is observed in the real markets.

The two other examples are about the nature of the mini-flash crashes. If a mini-flash crash does occur, it almost surely does so because of “endogenous triggering effects.” As predicted by Theorems 5.1 and 5.2), some of our agents also “converge on the same strategy” during mini-flash crashes: In certain cases, the agents driving these events all buy or sell together with the same (exploding) growth rate. The two theorems and the examples illustrating them are to demonstrate that mini-flash crashes can be accompanied by both high and low trading volumes.

Appendix A Section 3 Proofs

A.1. Proof of Lemma 3.1

Step 1: Denote the usual -augmentation of by . Let be the space of -progressively measurable processes such that (3.2) and (3.3) hold. We, again, define the process by (3.4) for any strategy . Agent ’s auxiliary problem is to maximize

| (A.1) |

over . It is not difficult to show that

| (A.2) |

for . Section 7.4 of [34] and (3.1) imply that the process with

is an -Wiener process under and

| (A.3) |

After integrating by parts and recalling (3.4) and (A.3), we get

We also have

Now -a.s. by the definition of in Step A.1. Since , and do not depend on Agent ’s choice of , (A.2) implies that maximizes (A.1) over if and only if it maximizes

| (A.4) |

Clearly, maximizes (A.4) over if and only if it minimizes

| (A.5) |

Step 3: Recall the definition of from (3.7) and let

| (A.11) |

We see from Theorem 3.2 of [10] that (A.5) has a unique solution . Moreover, the corresponding optimal inventory process satisfies the linear ODE

| (A.12) |

-a.s. on .

Using Fubini’s theorem and (A.2), we get that

| (A.13) |

The half-angle formula together with (3.9) and (A.11) imply that (A.1) can be re-written as

| (A.14) |

Step 4: We know that satisfies (3.2) and (3.3), as all strategies in have these properties. Now is continuous on for -almost every . When such an is chosen, (A.1) becomes (3.1). The latter is a first order linear ODE with continuous coefficients, so is continuous on (e.g., by Chapter 1.2 of [38]).

Since our terminal inventory constraint is deterministic, we observe that

exists and is finite from (28) and (29) in the proof of Theorem 3.2 in [10], as well as (A.13) in Step A.1. In particular, we can view the paths of on as -a.s. continuous.333Alternatively, we could give an argument using singular point theory as in Section 4. We conclude by noting that is also -adapted by (28) and (29) in the proof of Theorem 3.2 in [10], (3.9), and (A.13) in Step A.1.

∎

Appendix B Section 4 Proofs

We frequently reference various easy properties of the functions in Definition 4.1. We collect these below for convenience. We will leave the proof to the reader.

Lemma B.1.

Fix . We have the following:

-

i)

is a strictly decreasing nonnegative function on with .

-

ii)

The entries of are analytic on and .

-

iii)

If has a root on , we can find the smallest one which we denote by . In this case, and the zero of at is of finite multiplicity.

-

iv)

The entries of are analytic on but

-

v)

’s entries are continuous on .

B.1. Proof of Lemma 4.1

Let . At each time , Agent observes the correct value of , interprets this value as the realized value of , and computes .444By abuse of notation, we evaluate and are evaluated at ; however, Agent would evaluate these quantities at some . We adopt similar conventions in the sequel without further comment. By (3.5), it follows that

| (B.1) |

After substituting (3.11) into (B.1), we have

| (B.2) |

The quantity on the LHS of (B.1) plays a role in determining Agent ’s strategy (see Lemma 3.1). Substituting (B.1) into (3.1) and applying the half-angle formula for , we get

It follows that the uncertain agents’ strategies are characterized by the ODE system

| (B.3) |

Corollary 3.1, Lemma B.1 and a standard existence and uniqueness theorem (see Sections 1.1 and 3.1 of [11]) finish the argument. ∎

B.2. Proof of Lemma 4.2

As ,

Here, adj denotes the usual adjugate operator.

We can find a non-negative integer such that the multiplicity of the zero of at is by Lemma B.1. Hence, there is a unique non-vanishing analytic function such that

| (B.4) |

on a small neighborhood of . Note that is non-vanishing, as the zeroes of are isolated and (see Lemma B.1). We then define the analytic (see Lemma B.1) map by

| (B.5) |

and arrive at (4.3).

Since has a root at , the rank of is no more than . We conclude by observing that adj has rank 1 when has rank ; otherwise, adj must be the zero matrix. The comments about the rank of immediately follow. ∎

B.3. Proof of Proposition 4.1

since . Then (4) has a singular point of the first kind at (see our discussion above). by hypothesis, so Theorem 6.5 of [16] implies that a fundamental solution of (4) on for some is given by

| (B.6) |

In (B.6), is an analytic -valued function with . Moreover, is invertible for all and555Any fundamental solution of (4.3) is invertible everywhere, as are matrix exponentials.

| (B.7) |

The solution of (4.1) satisfies

near (argue as in Lemma 4.2). Since

is also a fundamental solution of (4.3) on 666See Theorem 2.5 of Coddington & Carlson ([16]). and equals at , we can apply variation of parameters777See Theorem 2.8 of Coddington & Carlson ([16]). to obtain

| (B.8) |

We can find an eigenbasis for such that corresponds to . We then define the continuous real-valued functions on and the constants as certain eigenbasis coordinates:

| (B.9) |

Taken with (B.3), these definitions immediately give (4.1) after recalling that for any matrix with eigenvalue and corresponding eigenvector , we have

∎

B.4. Proof of Proposition 4.2

We know that , the ’s and the ’s are all uniquely defined and continuous on (see Lemma 4.1). Corollary 3.1 implies that and are continuous at for (the certain agents). It also gives us

for . It remains to show that

| (B.10) |

As discussed above, one difficulty is that the diagonal entries of in (4.1) explode at (see Lemma B.1); however, the approach for resolving this issue is similar to that used to analyze solution behavior near .

First, we show that (4) (after replacing with ) has a singular point of the first kind at . Now has a zero of multiplicity 1 at since

Hence, there is a unique non-vanishing analytic function such that

| (B.11) |

on a small neighborhood of . Near , it follows that the entries of are given by

| (B.16) |

(see Definition 4.1). On this region, the solution of (4) satisfies

| (B.17) |

By (B.16) and Lemma B.1, (B.17) has a singular point of the first kind at .

Second, we find a fundamental solution of (B.17) near . We know that

by (B.11), (B.16), and Lemma B.1. Theorem 6.5 of [16] implies that a fundamental solution of (B.17) on for some is given by

| (B.18) |

In (B.18), is an analytic -valued function with . Also, is invertible for all .888Any fundamental solution of (B.17) is invertible everywhere.

Finally, we use our fundamental solution to solve (4.1) and conclude the proof. Notice that also has a zero of multiplicity 1 at since

There is a unique non-vanishing analytic function such that

| (B.19) |

on a neighborhood of . In particular, the entries of near are given by

| (B.20) |

Since

is also a fundamental solution of (4.3) on 999See Theorem 2.5 of Coddington & Carlson ([16]). and equals at , we can apply variation of parameters101010See Theorem 2.8 of Coddington & Carlson ([16]). to obtain

| (B.21) |

Appendix C Section 5 Proofs

C.1. Proof of Lemma 5.1

First observe that (5.1) is equivalent to

| (C.1) |

by Definitions 3.7 and 4.1. By Definitions 4.1 and 5.1, we see that is now given by

| (C.4) |

A short calculation shows that

| (C.5) |

The first term in (C.5) is always at least 1. The second term is non-zero at 0 but does have a root on if and only if (C.1) holds.111111In fact, is the unique root of in this case. Both of these observations come from Lemma B.1.

C.2. Proof of Lemma 5.2

C.3. Proof of Theorems 5.1 and 5.2

Since our uncertain agents are semi-symmetric,

| (C.17) |

for by Definition 4.1. For convenience, we introduce the following deterministic function121212 The function is deterministic by Corollary 3.1. and the constants :

| (C.21) |

Using (C.3), we get that

| (C.22) |

By (C.2), is an eigenbasis for . Moreover,

| (C.23) |

is the eigenvalue corresponding to each of , while

| (C.24) |

corresponds to .

By (B.3), it follows that

| (C.25) |

It follows that we can find analytic deterministic functions and such that

| (C.26) |

for each .131313 Note that is continuously differentiable on by Corollary 3.1. Since (see Proposition 4.1), (C.2) and Remark 5.2 further imply that

| (C.27) |

and

| (C.28) |

While , determining the sign of is difficult, in general, as it depends upon the sign of (see (C.3)).

We see from (C.26) and (C.27) that the expression

| (C.29) |

is bounded near for each and almost every . In particular, the coordinates of both

and its time derivative are bounded near for such as well.

Since , the -coordinate of tends to 1 . For , the -coordinate of tends to 0 as . In each situation, we can also obtain Lipschitz bounds on the convergence. Due to (4.1) and (C.26), potential explosions in the coordinates of are characterized by

| (C.30) |

Specifically,

| (C.31) |

To finish the proof, we separately consider the and cases.

Case.

Assume that . It follows that

Clearly,

meaning that

| (C.32) | ||||

and

| (C.33) | ||||

Arguing as in our discussion of (C.29), we see that the hypotheses in (C.32) and (C.33) also imply that

respectively.141414 In particular, the coordinates of will asymptotically explode at the rate . Conditional on , the RHS of the inequality in (C.32) (and C.33) is deterministic. Since (see (C.28)), we finish our proof of Theorem 5.1.

Case.

Assume that . We can find a constant such that

| (C.34) |

Hence, (C.30) is bounded as and

exists in by our previous comments.

By our discussion surrounding (C.29), we see that explosions in the coordinates of are characterized by

| (C.35) |

More precisely,

| (C.36) |

Suggestively, we first rewrite the expression in (C.3) as

| (C.37) |

Let and be the deterministic Lipschitz coefficients for and . The first two lines of (C.3) are deterministic, and we can obtain the following bounds:

In (C.3), the third line is deterministic conditional on . Lines 4 - 6 of (C.3) are stochastic conditional on . Letting be the maximum of on , we notice that

References

- [1] BBC News: probe into Japan share sale error. http://news.bbc.co.uk/2/hi/business/4512962.stm. Accessed: 2017-04-15.

- [2] Commodity Futures Trading Commission and the Securities & Exchange Commission: findings regarding the market events of May 6, 2010. https://www.sec.gov/news/studies/2010/marketevents-report.pdf. Accessed: 2017-04-15.

- [3] Nanex LLC.: flash crash summary report. http://www.nanex.net/FlashCrashFinal/FlashCrashSummary.html. Accessed: 2017-04-15.

- [4] Nanex LLC.: NxResearch. http://www.nanex.net/NxResearch/. Accessed: 2017-04-15.

- [5] Securities and Exchange Commission: Merrill Lynch charged with trading control failures that led to mini flash crashes. https://www.sec.gov/news/pressrelease/2016-192.html. Accessed: 2017-04-15.

- [6] R. Almgren and N. Chriss, Value under liquidation, Risk, 12 (1999), pp. 61–63.

- [7] , Optimal execution of portfolio transactions, J. Risk, 3 (2001), pp. 5–40.

- [8] R. Almgren and J. Lorenz, Adaptive arrival price, Trading, 2007 (2007), pp. 59–66.

- [9] R. F. Almgren, Optimal execution with nonlinear impact functions and trading-enhanced risk, Appl. Math. Finance, 10 (2003), pp. 1–18.

- [10] P. Bank, H. M. Soner, and M. Voß, Hedging with temporary price impact, Math. Financ. Econ., 11 (2017), pp. 215–239.

- [11] V. Barbu, Differential equations, Springer Undergraduate Mathematics Series, Springer, Cham, 2016. Translated from the 1985 Romanian original by Liviu Nicolaescu.

- [12] P. Cardaliaguet and C.-A. Lehalle, Mean field game of controls and an application to trade crowding, Mathematics and Financial Economics, 12 (2018), pp. 335–363.

- [13] B. I. Carlin, M. S. Lobo, and S. Viswanathan, Episodic liquidity crises: cooperative and predatory trading, J. Finance, 62 (2007), pp. 2235–2274.

- [14] Á. Cartea, S. Jaimungal, and D. Kinzebulatov, Algorithmic trading with learning, Int. J. Theoretical Appl. Finance, 19 (2016), p. 1650028.

- [15] P. Casgrain and S. Jaimungal, Algorithmic Trading with Partial Information: A Mean Field Game Approach, ArXiv e-prints, (2018).

- [16] E. A. Coddington and R. Carlson, Linear ordinary differential equations, Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 1997.

- [17] K. Colaneri, Z. Eksi, R. Frey, and M. Szölgyenyi, Shall I sell or shall I wait? Optimal liquidation under partial information with price impact, ArXiv e-prints, (2016).

- [18] D. Dick, Erroneous combustion, CFA Institute Magazine, 24 (2013), pp. 20–21.

- [19] D. Easley, M. M. López de Prado, and M. O‘Hara, Flow toxicity and liquidity in a high-frequency world, Rev. Financ. Stud., 25 (2012), p. 1457.

- [20] D. Easley, M. M. López de Prado, and M. O’Hara, The microstructure of the “flash crash”: flow toxicity, liquidity crashes, and the probability of informed trading, J. Portfolio Manage., 37 (2011), pp. 118–128.

- [21] E. Ekström and J. Vaicenavicius, Optimal liquidation of an asset under drift uncertainty, SIAM J. Financial Math., 7 (2016), pp. 357–381.

- [22] M. Farrell, Mini flash crashes: a dozen a day. http://money.cnn.com/2013/03/20/investing/mini-flash-crash/. Accessed: 2017-04-15.

- [23] V. Filimonov and D. Sornette, Quantifying reflexivity in financial markets: Toward a prediction of flash crashes, Phys. Rev. E., 85 (2012), p. 056108.

- [24] R. Frey, A. Gabih, and R. Wunderlich, Portfolio optimization under partial information with expert opinions, Int. J. Theor. Appl. Finance, 15 (2012), p. 1250009.

- [25] N. Gârleanu and L. H. Pedersen, Dynamic trading with predictable returns and transaction costs, J. Finance, 68 (2013), pp. 2309–2340.

- [26] R. Gayduk and S. Nadtochiy, Liquidity Effects of Trading Frequency, Math. Finance, (forthcoming).

- [27] A. Golub, J. Keane, and S.-H. Poon, High frequency trading and mini flash crashes, ArXiv e-prints, (2012).

- [28] J. Huang and J. Wang, Liquidity and market crashes, Rev. Financ. Stud, 22 (2009), pp. 2607–2643.

- [29] N. I. Ismail and L. Mnyanda, Flash crash of the pound baffles traders with algorithms being blamed. https://www.bloomberg.com/news/articles/2016-10-06/pound-plunges-6-1-percent-in-biggest-drop-since-brexit-result. Accessed: 2017-04-15.

- [30] S. J. Leal, M. Napoletano, A. Roventini, and G. Fagiolo, Rock around the clock: An agent-based model of low- and high-frequency trading, J. Evol. Econ., 26 (2016), pp. 49–76.

- [31] N. Johnson, G. Zhao, E. Hunsader, H. Qi, N. Johnson, J. Meng, and B. Tivnan, Abrupt rise of new machine ecology beyond human response time, Sci. Rep., 3 (2013), pp. 1–7.

- [32] A. Joulin, A. Lefevre, D. Grunberg, and J.-P. Bouchaud, Stock price jumps: news and volume play a minor role, Wilmott Magazine, Sep/Oct (2008), pp. 1–7.

- [33] A. A. Kirilenko, A. S. Kyle, M. Samadi, and T. Tuzun, The flash crash: high frequency trading in an electronic market, J. Finance, (forthcoming).

- [34] R. S. Liptser and A. N. Shiryaev, Statistics of random processes. I, vol. 5 of Applications of Mathematics (New York), Springer-Verlag, Berlin, expanded ed., 2001. General theory, Translated from the 1974 Russian original by A. B. Aries, Stochastic Modelling and Applied Probability.

- [35] S. Mamudi, Sudden stock crashes usually caused by human error, SEC says. https://www.bloomberg.com/news/articles/2013-06-18/sudden-stock-crashes-mostly-show-human-error-sec-s-berman-says. Accessed: 2017-04-15.

- [36] F. Passerini and S. E. Vazquez, Optimal trading with alpha predictors, ArXiv e-prints, (2015).

- [37] J. A. Scheinkman and W. Xiong, Overconfidence and speculative bubbles, J. Polit. Econ., 111 (2003), pp. 1183–1220.

- [38] W. Walter, Ordinary differential equations, vol. 182 of Graduate Texts in Mathematics, Springer-Verlag, New York, 1998. Translated from the sixth German (1996) edition by Russell Thompson, Readings in Mathematics.