On the validity of parametric block correlation matrices with constant within and between group correlations

Abstract

We consider the set of parametric block correlation matrices with blocks of various (and possibly different) sizes,

whose diagonal blocks are compound symmetry (CS) correlation matrices and off-diagonal blocks are constant matrices.

Such matrices appear in probabilistic models on categorical data, when the levels are partitioned in groups,

assuming a constant correlation within a group and a constant correlation for each pair of groups.

We obtain two necessary and sufficient conditions for positive definiteness of elements of .

Firstly we consider the block average map , consisting in replacing a block by its mean value.

We prove that for any , if and only if .

Hence it is equivalent to check the validity of the covariance matrix of group means,

which only depends on the number of groups and not on their sizes.

This theorem can be extended to a wider set of block matrices.

Secondly, we consider the subset of

for which the between group correlation is the same for all pairs of groups.

Positive definiteness then comes down to find the positive definite interval of a matrix pencil on .

We obtain a simple characterization by localizing the roots of the determinant with within group correlation values.

1 Introduction

We consider the set of real parametric block correlation matrices

where diagonal blocs are compound symmetry matrices of size () and off-diagonal blocks are constant matrices of size :

All parameters are assumed to be in .

When we set by convention ,

and denote by the set of such that .

Such matrices appear in probabilistic models on categorical data, when the levels are partitioned in groups of sizes , assuming a constant correlation within the group and a constant correlation for each pair of groups . Without loss of generality, we assume that corresponds to the first levels, to the next ones, and so on. This results in a parameterization of the correlation matrix (see e.g. [6]) involving a small number of parameters. In order to further reduce the number of parameters, one may often consider the subset

such that the between group correlation has a common value over pairs of groups.

Even more parsimonious models are obtained when a common value is also assumed for within group correlations.

There are some common points with statistical models involving groups of variables,

such as linear mixed effects models or hierarchical models.

When , is simply the CS correlation matrix used in random intercept model.

When the blocks have the same size, a common within group correlation and a common between group correlations,

is a block CS matrix met in equicorrelated models. In that case, it is also connected to linear models with doubly exchangeable distributed errors [9].

We aim at answering the question: For which values of ()

is the matrix positive definite?

In the simple case where has a block CS structure, as cited in the previous paragraph,

the necessary and sufficient condition for positive definiteness is known

(see e.g. [8], Lemma 4.3.).

There is also a connection to matrix pencils, corresponding to matrices parameterized linearly by a single parameter.

However, in general, the result seems not to be known.

2 Preliminaries

2.1 Additional notations and basics

-

•

Positive definiteness. If , recall that is positive semidefinite (p.s.d.), or simply positive, if for all . We denote: . Similarly is positive definite (p.d.) if for all non-zero . We denote: .

-

•

Matrix of ones. denotes the matrix of ones. More generally, .

-

•

Compound symmetry (CS) matrices. is the CS covariance matrix. The CS correlation matrix is , and for , It is well-known that

(1) For instance denoting , one can see that the eigenvalues of are with multiplicity (eigenvector ) and with multiplicity (eigenspace: ).

2.2 The block average map

We denote by the block average map on , consisting in replacing a block by its mean value:

is an example of positive linear map in the sense that if then . Indeed, where is the matrix defined by

and we retrieve one of the typical cases presented in [1] (Example 2.2.1.(vi)).

This also can be viewed with a probabilistic interpretation.

If , it is a covariance matrix of some random vector .

Then is the covariance matrix of the group means

where .

Finally, we give the explicit form of when .

Define for :

| (2) |

Notice that . Then:

2.3 The block filling map

We call block filling map from to , the linear map

This transformation fills each block by a constant value, given by . Notice that is a positive linear map, since where is the matrix

Clearly the filling and averaging operations cancel each other when they are done in this order, corresponding to and to the relation

On the other hand, is generally not equal to , and is an orthogonal projection of rank .

2.4 A wider class of block matrices

The results of the next section are valid on a wider class of block matrices, that we now introduce. This is the set of symmetric block matrices

where off-diagonal blocks are constant matrices of size ,

and diagonal blocks are of size and verify .

To see that , notice that if then

and

which is p.d. for because the symmetric matrix

is an orthogonal projection: .

2.5 Matrix pencil and positive definite interval

When a parametric matrix of depends linearly on a single parameter , it can be written as a matrix pencil,

where . The problem of finding such that is positive definite was investigated in several studies ([3], [4]). A main result is that the admissible values form an open interval, called positive definite interval (PD interval). Indeed it is the intersection of a straight line with the open convex cone of positive definite matrices ([3]). Now denote . When is p.d., is a continuous function such that . Furthermore, is null on the boundary of : if is p.s.d. but not p.d., there exists such that implying that is an eigenvalue of . The PD interval is then obtained by computing the negative and positive roots of which are closest to 0. Equivalently, the PD interval is related to the largest and smallest eigenvalues of the symmetric matrix ([4]). Indeed if and only if

i.e. is an eigenvalue of , which has the same eigenvalues than .

3 Main results

3.1 Positive definiteness of elements of

Positive definiteness of a block matrix (of size ) in – and thus in – can be simply checked on the block average matrix (of size ):

Theorem 1.

Let . Then,

-

1.

and .

-

2.

and .

The text of the theorem can be simplified on , for which diagonal blocks are CS correlation matrices. Indeed, p.d. of is then equivalent to the two conditions and (Eq. 1). The former is contained in the definition of . The latter is a consequence of p.d. of by looking at the signs of its diagonal elements (Eq. 2). Hence, we have:

Theorem 2.

Let . Then,

For completeness, we provide a description of , via a representation of its block diagonal elements.

It is shown that is in general much wider than :

the -th diagonal block of is represented by parameters,

whereas the -th diagonal block of is a CS correlation matrix described by parameter.

Proposition 1.

Let be a matrix whose columns form a basis of . Then all symmetric matrices of size such that are written in a unique way as

where is a p.s.d.matrix of size and is a real number.

3.2 Positive definiteness of elements of

We now focus on the subclass , for which the positive definiteness condition of Theorem 2 can be further simplified. Let and denote :

where the ’s are given by Eq. 2 and lie in . We can further restrict the search of a necessary and sufficient condition to vectors

such that ().

Indeed this condition is necessary as all diagonal minors must be strictly positive.

Notice that “” is the condition for positive definiteness of

the block diagonals terms in .

When is fixed, the map is a matrix pencil

with and . As recalled in Section 2, the values of such that is positive definite form an open interval, called positive definite interval (PD interval). It is obtained by computing the negative and positive roots of which are closest to 0.

In this context, our main contribution is to provide a localization of the roots of as well as an analytical expression. They both simplify the computation of the PD interval.

Lemma 1.

Let ,

and denote by the values of rearranged in ascending order.

Denote and more generally let be the leading minor of ().

Then is a polynomial of order given by

| (3) |

Let us further assume that all are . Then the roots of are all real and interlaced with the ’s:

Furthermore,

Theorem 3.

Notice that the interval on given in Theorem 3 can be easily found numerically. Indeed, from Lemma 1, and are roots of that are perfectly localized, and can be found by a zero search algorithm such as Brent’s algorithm ([2]). More precisely is the unique root in the interval , and the unique root in .

4 Corollaries

We first give a direct consequence of Theorem 2 for two groups, and a sufficient condition for elements of obtained by comparison to a compound symmetry matrix. They are expressed with the ’s of Eq. 2.

Corollary 1 (Case of 2 groups).

Let . Then,

Corollary 2 (A sufficient condition on ).

Let and . If () and , then .

For completeness, we give a specific result when all groups have the same size, a common between group correlation, and a common within group correlation. There is nothing new here, as it is a special case of block CS matrices for which the result is known, but this gives another view of it.

Corollary 3.

Assume that and for all , . Define . Then,

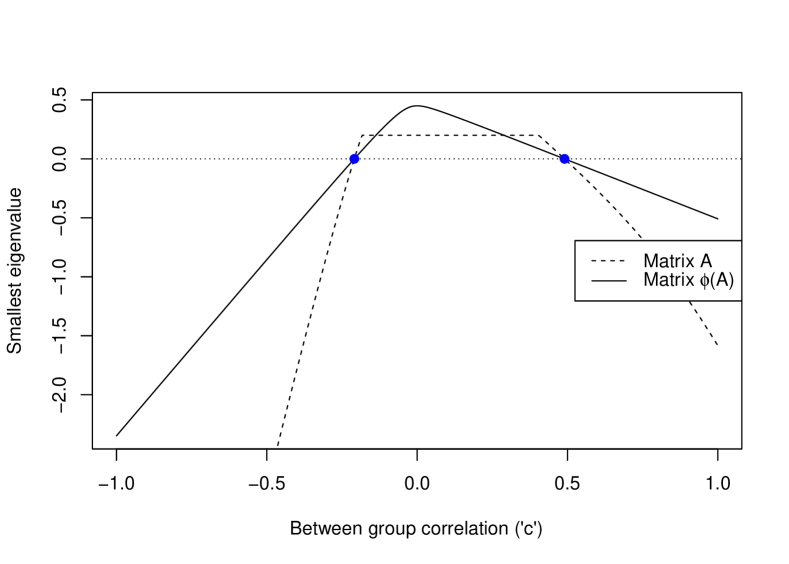

5 A numerical application

Consider the parametric matrix corresponding to 4 groups of size with a common between group correlation. The condition means that:

Now choose . The sufficient condition of Corollary 2 gives the following interval for the between group parameter (printing is limited to the first 2 digits) :

Theorem 3 gives the optimal interval, which is a bit larger:

| (4) |

This interval was obtained by using the Brent’s algorithm, implemented in R (function uniroot of package stats, [7]), thanks to the localization given in Theorem 3. The result is illustrated on Figure 1. For a pedagogical purpose, we represented the smallest eigenvalue of and as a function of , denoted respectively . These eigenvalues have been computed numerically using the eigen function in R. This confirms the results of Theorem 2 and Theorem 3: the values of such that the smallest eigenvalue is positive is the same in both cases, and correspond to the theoretical interval (4). Notice that the size of is much smaller than . Finally, the plateau on the graph is explained by the fact that is equal to , which does not depend on , which remains true on an open interval containing by continuity of the determinant.

6 Proofs

6.1 Proof of Theorem 1 and related material.

Proof of Proposition 1.

First of all, notice that finding a symmetric matrix of size such that

is equivalent to finding a p.s.d. matrix of size such that .

The link between and is given by , where is a real number equal to .

Hence, the proposition will be proved if we show that all p.s.d. matrices such that

are of the form

| (5) |

where is a p.s.d. matrix of size ,

and is a matrix whose columns form a basis of .

Notice that all p.s.d. matrix of the form 5 satisfy, by definition of ,

Conversely, let be a p.s.d. matrix such that . Thus is the covariance matrix of a random vector . Without loss of generality, we can assume that is centered: . Then, is also centered and

Hence, with probability 1.

Thus and is spanned by the columns of :

there exists a random variable such that .

As a consequence, , with .

To see that and are uniquely determined, assume that holds for another p.s.d. matrix of size and another real . Then . Thus, . By multiplying this relation at left side by and by at right side, we get because the Gram matrix has rank and is thus invertible. ∎

We then give a technical lemma.

Lemma 2.

Let be a symmetric matrix such that is positive. If is p.d. and if for some vector , then has constant elements, i.e. .

Proof of Lemma 2.

Since has rang and has rank , the matrix must have rank . Thus, by Prop. 1, where is p.d. of size , and is a matrix whose columns form an orthonormal basis of . Now, . Since is p.d. it implies . By definition of , we have . ∎

Proof of Theorem 1.

Statement 1.

If is positive then the diagonal blocks are also positive,

and is positive since is a positive linear map.

Conversely, if is positive then is positive,

as is a positive linear map.

Now, since has constant off-diagonal blocks,

is a block diagonal matrix with diagonal blocks

, which are assumed to be positive.

Hence is positive as a sum of two positive matrices.

Statement 2. If is p.d. then

so are the . Moreover is p.d.

since the matrix has rank .

Now assume that and all the ’s are p.d.

Denote ,

and let be a vector of length with component vectors .

Then,

By Statement 1, both matrices and are positive. Hence, the left hand side is equal to zero iff both terms at the right hand side vanish. Now is block-diagonal, and each diagonal block is the difference between a block and its average element. By lemma 2, we have iff each vector is constant (). The second term is a quadratic form in the vector of group sums , namely . So vanishes iff each average does. Thus if , each block is constant and has zero mean, which is only possible when . ∎

6.2 Proof of Theorem 3

Proof of Lemma 1.

For the sake of simplicity, and without restriction,

we can assume that the have been sorted in increasing order:

(.

Indeed the reordering does not change the determinant.

Now for , define:

where is the matrix extracted from by keeping the first rows and first columns.

In particular , and .

Let us now derive the analytical expression of . We first prove a recurrence formula. By expanding with respect to the last column, we have:

The first term is equal to . For the second one, subtracting the last column to the other ones gives:

Finally we obtain a relation linking to , valid for :

| (6) |

The explicit formula of (written in Eq. 3 for ) is then proved recursively on . Indeed, one can easily check it for , and if it is true for , then with Eq. 6, it holds:

We also deduce of Eq.6 that is a polynomial of order whose leading term is . In particular, when .

From now on, assume that . The interlacing of the roots of with the ’s is obtained by evaluating at (). Indeed, subtracting column , whose components are all equal to , one directly obtains:

Thus the sign of depends on the rank of in . Those signs alternate when one read the sequence starting by at . Since the limit in is , and as the number of zeros of is less than , we deduce by the intermediate value theorem that there is exactly 1 zero in each interval . Furthermore , resulting in the interlacing

We are now able to locate the roots of relatively to those of . From Eq 6, it holds:

In particular , showing that since is negative on and positive on . Similarly, one deduce from Eq. 6 that so that since is positive on and negative on . Finally, we obtain by recursion that

More generally, Eq. 6 implies that

the positive roots of are interlaced with the positive roots of .

Finally one can check that the previous results remain valid in case of equality of several ,

where the corresponding strict inequalities are replaced by large inequalities.

For completeness, we give an alternative proof of this last statement, using algebraic arguments. Consider the pencil matrix . Recall that is a root of if and only if

i.e. is an eigenvalue of , or equivalently of the symmetric matrix . Similarly, is the root of if and only if is an eigenvalue of

where we use the fact that is diagonal for the last equality. Hence the roots of are the negative inverse of the eigenvalues of the principal submatrix of . Furthermore, by Sylvester’s law, has the same inertia as . It is easy to see that has two eigenvalues: with multiplicity (eigenvector ) and with multiplicity (eigenspace: ). Thus has positive eigenvalue, and negative ones. Consequently, has negative root and positive ones. Now by Cauchy interlacing theorem ([5], §4.3.), the eigenvalues of consecutive principal submatrices are interlaced. As is increasing on and , it results in two separate interlacings for the roots of consecutive ’s: one for negative roots, one for positive roots. We finally get the announced inequalities:

∎

Proof of Theorem 3.

The result is straightforward from Lemma 1,

implying that the PD interval on is given by .

An alternative proof is given by applying the Sylvester conditions and using Lemma 1.

Indeed the intersection of sets when

is the interval .

Furthermore, let , and .

Denote by the diagonal matrix obtained by replacing by in .

Then , which shows that the PD interval is increasing with .

∎

6.3 Proof of corollaries

Proof of Corollary 3.

Here which gives the announced necessary and sufficient condition

by Theorem 2.

Alternatively the result can be obtained directly on ,

which is here a block compound symmetry covariance matrix

with and . It is known (see e.g. [8], Lemma 4.3.) that if and only if . Now, is p.d. if and only if leading to . Similarly, is p.d. if and only if leading to . ∎

Acknowledgements

Part of this research was conducted within the frame of the Chair in Applied Mathematics OQUAIDO, gathering partners in technological research (BRGM, CEA, IFPEN, IRSN, Safran, Storengy) and academia (CNRS, Ecole Centrale de Lyon, Mines Saint-Etienne, University of Grenoble, University of Nice, University of Toulouse) around advanced methods for Computer Experiments.

References

- [1] Rajendra Bhatia. Positive Definite Matrices. Princeton University Press, 2007.

- [2] R. Brent. Algorithms for Minimization without Derivatives. Englewood Cliffs, NJ: Prentice-Hall, 1973.

- [3] R.J. Caron and N.I.M. Gould. Finding a positive semidefinite interval for a parametric matrix. Linear Algebra and its Applications, 76:19 – 29, 1986.

- [4] R.J. Caron, T. Traynor, and S. Jibrin. Feasibility and constraint analysis of sets of linear matrix inequalities. INFORMS Journal on Computing, 22(1):144–153, 2010.

- [5] R. A. Horn and C. R. Johnson. Matrix Analysis. Cambridge University Press, New York, NY, USA, 2nd edition, 2012.

- [6] Peter Z. G. Qian, Huaiqing Wu, and C. F. Jeff Wu. Gaussian process models for computer experiments with qualitative and quantitative factors. Technometrics, 50(3):383–396, 2008.

- [7] R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2016.

- [8] G. Ritter and M. T. Gallegos. Bayesian object identification: Variants. Journal of Multivariate Analysis, 81(2):301 – 334, 2002.

- [9] A. Roy and M. Fonseca. Linear models with doubly exchangeable distributed errors. Communications in Statistics - Theory and Methods, 41(13-14):2545–2569, 2012.