Selection of Sparse Vine Copulas in High Dimensions with the Lasso

Abstract

We propose a novel structure selection method for high dimensional () sparse vine copulas. Current sequential greedy approaches for structure selection require calculating spanning trees in hundreds of dimensions and fitting the pair copulas and their parameters iteratively throughout the structure selection process. Our method uses a connection between the vine and structural equation models (SEMs). The later can be estimated very fast using the Lasso, also in very high dimensions, to obtain sparse models. Thus, we obtain a structure estimate independently of the chosen pair copulas and parameters. Additionally, we define the novel concept of regularization paths for R-vine matrices. It relates sparsity of the vine copula model in terms of independence copulas to a penalization coefficient in the structural equation models. We illustrate our approach and provide many numerical examples. These include simulations and data applications in high dimensions, showing the superiority of our approach to other existing methods.

Keywords: Dependence Modeling, Vine Copula, Lasso, Sparsity

1 Introduction

Modeling dependence in high dimensional systems has become an increasingly important topic nowadays. This is mainly because data is more available but also computation capacities increase permanently. Hence, modeling joint distributions in arbitrary dimensions is key to understand and predict multivariate phenomena. Since analytically tractable multivariate distributions for arbitrary dimensions are hard to find and impose the same distributions on both marginals and dependency, copula models have become popular in recent decades. Based on the theorem of Sklar (1959), they enable modeling marginal distributions and dependency behaviour separately. This however only translates the problem of complex -dimensional distributions to -dimensional copulas. To overcome this, the pair copula construction (PCC) of Aas

et al. (2009) allows for more flexible dimensional models. They consist of the marginal distributions and (conditional) bivariate copulas as building blocks, all of which can be chosen independently from each other. The resulting models, called regular vines or R-vines Kurowicka and

Joe (2011) are specified by a sequence of linked trees, the R-vine structure, where the edges of the trees identify bivariate copulas. This method has been very popular in the last years in the financial context, see Aas (2016) for an overview of applications. When it comes to determining a suitable R-vine structure, most often the algorithm of Dissmann Dißmann et al. (2013) is used. This locally greedy approach works well in lower dimensional setups. However, for high dimensional data it can not be ensured that its solutions are close to the optimum solution of this high dimensional combinatorial optimization problem. Our goal is to contribute another entirely different method for looking at the R-vine structure, scaling to hundreds of dimensions. This is necessary since e. g. the current Bayesian approaches Gruber and

Czado (2015a), Gruber and

Czado (2015b) are computationally highly intensive and can not be used for more than dimensions. Also, the Pair-Copula Bayesian Networks of Bauer and

Czado (2016) are not applicable in dimensions which exceed . Even though they exploit conditional independences given by a graphical model, they may ultimately involve high dimensional numerical integration. This is clearly a drawback to the pair-copula construction, which does not require integration at all. The work of Müller and

Czado (2016) proved to be several times faster than Dissmann’s algorithm in moderately high dimensions, e. g. by exploiting sparsity induced by DAGs modelled with a multivariate Gaussian distribution. As our approach, they also split the estimation of the R-vine structure from the pair copula estimates. Their approach to fit several DAGs with different degrees of sparsity has the drawback that each DAG generates a different R-vine structure. Thus, the fitting procedure has to be redone for each degree of sparsity, as with Dissmann’s algorithm. Additionally, it still relies on maximum spanning trees.

The goal of this paper is to develop a novel approach exploiting in particular sparse structures. For this, we utilize the Lasso Tibshirani (1994) which heavily influenced statistics in recent years by performing parameter estimation and model selection simultaneously. Introduced in the regression domain, it found widespread applications in other areas, such as the graphical Lasso for graphical models, see Friedman

et al. (2008) and others. A very favourable property of the Lasso is the regularization path, linking the Lasso-solutions to a tuning parameter , describing the degree of penalization for the respective solution.

Our approach relates vine copula models to structural equation models (SEMs) as introduced by Brechmann and

Joe (2014). This allows us to tap into the Lasso world by introducing a penalized regression on the structural equations which reflects the necessary properties for vine copula models, the so called proximity condition. We show that Lasso-solutions to these structural equations, i. e. the regularization path, can be related to specific entries in the R-vine structure. By virtue of these concepts, we are able to introduce a regularization path concept for the R-vine itself. Thus, we obtain a high dimensional vine copula with a sparsity pattern reflecting the chosen degree of penalization.

The structure of the paper is as follows. First, we briefly introduce dependence modeling with R-vines in Section 2. We sketch the connection to structural equation models, which enables us to use the Lasso in Section 3 and the Lasso will be reviewed in Section 4. In Section 5, we introduce our novel approach by first considering the first R-vine tree and all subsequently estimated higher trees. We will define the R-vine regularization path and discuss the choice of the tuning parameter , which controls the strength of penalization. In Section 6, we compare our approach to Dissmann’s algorithm in a simulation study to show that our method deals better with sparse situations, especially present in high dimensional setups. After that, an example and outlook in dimensions follows. We conclude the paper with a discussion in Section 7.

2 Dependence Modeling with R-vines

We use the following conventions. Upper case letters denote random variables, and lower case letters their realizations. Bold lower case letters denote vectors and bold upper case letters denote matrices. Referring to sub-vectors, we denote by the -th entry of the vector and the first entries of the vector . When considering matrices, we denote the -th entry in the -th row of the matrix . For rows or columns of a matrix , we write for the -th column and

for the -th row of , respectively. Additionally, we have the following three data scales when working with copulas.

-

(i)

x-scale: the original scale of , i.i.d., with density ,

-

(ii)

u-scale or copula-scale: , the cdf of and , ,

-

(iii)

z-scale: , the cdf of thus , .

We assume a random vector with joint density function and joint distribution function . By Sklar (1959), we can separate the univariate marginal distribution functions from the dependency structure such that , where is an appropriate -dimensional copula. If are continuous, is unique. The corresponding joint density function is given by

| (2.1) |

where is a -dimensional copula density. This expression incorporates a, possibly complex, -dimensional copula density. As shown by Aas et al. (2009), -dimensional copula densities may be decomposed into bivariate (conditional) copula densities. Its elements, the pair copulas can be chosen completely independent from each other and display e. g. positive or negative tail dependence or asymmetric dependence. For a pair-copula-construction (PCC) in dimensions, there exist many possible decompositions. These may be organized to represent a valid joint density by regular vines (R-vines), see Bedford and Cooke (2001, 2002). A vine tree sequence stores which bivariate (conditional) copula densities occur in the factorization of a -dimensional copula density. Such a sequence in dimensions is given by such that

-

(i)

is a tree with nodes and edges ,

-

(ii)

for , is a tree with nodes and edges ,

-

(iii)

if two nodes in are joined by an edge, the corresponding edges in must share a common node (proximity condition (pc)).

To formalize this, define the complete union of an edge by

where the conditioning set of an edge is defined as and

is the conditioned set. Since and are singletons, is a doubleton for each , see (Kurowicka and

Cooke, 2006, p. 96). For edges , we define the set of bivariate copula densities corresponding to by with the conditioned set and the conditioning set . Denote sub vectors of by . With the PCC, Equation (2.1) yields

| (2.2) |

When we speak of bivariate conditional copulas, we take into account the simplifying assumption, which is imposing that the two-dimensional conditional copula density is independent of the conditioning value (Stöber et al., 2013). The parameters of the bivariate copula densities are given by . This determines the R-vine copula . A representation of such a R-vine copula is most easily given by lower triangular matrices, see Dißmann et al. (2013). Such an R-vine matrix has to satisfy three properties.

-

(i)

for ,

-

(ii)

for ,

-

(iii)

for all , , there exist with and such that

(2.3)

The last property is reflecting the proximity condition. Conditions on can be checked very quickly algorithmically.

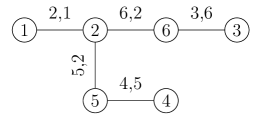

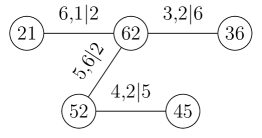

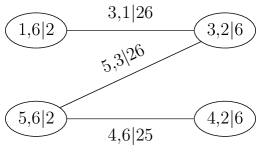

Example 2.1 (R-vine in 6 dimensions).

The R-vine matrix describes the R-vine in Figure 1 as follows. Edges in are pairs of the main diagonal and the lowest row, e. g. , , , etc. is given by the main diagonal and the second last row conditioned on the last row, e. g. ; , etc. Higher order trees are encoded similarly.

The associated R-vine matrix is given by

With for conditioning vector , , , the density becomes

The corresponding pair copula families and their parameters can also be stored in lower triangular family and parameter matrices and . Thus, the family and parameters of the pair copula described by are given by and . When two-parametric pair copulas are considered, an additional parameter matrix is used similarly.

Since we are interested in high dimensional applications, model reduction plays an essential role. Overall, there are edges, thus, model complexity increases quadratically in . This can be simplified by only modeling the first trees and assuming (conditional) independence for the remaining higher trees, see Brechmann et al. (2012) for a discussion. If , then a -truncated R-vine is an R-vine where each pair copula density assigned to an edge is represented by the independence copula density . In a -truncated R-vine, the second outer product in (2.2) has instead of factors. For an R-vine model with the parameter set , consider replications of dimensional data with for . We neglect the marginal distributions , the log-Likelihood on the u-scale is

Since the log-Likelihood always increases whenever more parameters enter the model, it is not advisable to use it for especially sparse structures since models will contain too many parameters of which a large portion do not contribute significantly to the model fit. Thus, there exist penalized goodness-of-fit measures which require that the log-Likelihood increases significantly to prefer a larger model. Such measures are the Akaike information criterion (AIC) Akaike (1973) and the Bayesian information criterion (BIC) Schwarz (1978). Abbreviate and define

where equals the number of parameters in the model . For , BIC will penalize more than AIC. If the number of possible parameters in an R-vine is greater or equal than the sample size and the model is comparably small, BIC is no longer consistent and will penalize too little. For high dimensional data, this assumption is reasonable and we use a modified version of BIC (mBIC) as in Frommlet et al. (2011),

| (2.4) |

3 Structural equation models (SEMs)

Our approach connects the R-vine structure to structural equation models (SEMs). For this, we utilize the approach of Brechmann and Joe (2014), who give a representation of -truncated Gaussian R-vines in terms of structural equation models (SEMs). SEMs are often used to model the influence of unobservable latent variables, see e. g. Kaplan (2009), Hoyle (1995) or Bollen (1989). We want to stress that we are not considering latent variables in this paper and are thus only dealing with actual observations. Given a Gaussian R-vine with structure , we define a SEM corresponding to denoted by . Let be an R-vine tree sequence and assume without loss of generality . For denote the edges in by using an assignment function , . For higher trees, we generalize for . Thus, the trees contain edges for . Based on the R-vine structure , define by

| (3.1) | ||||

with i.i.d. and such that for . Brechmann and Joe (2014) assume a -truncated R-vine and restate the SEM in (3.1) with

Thus, we have for each edge that for :

| (3.2) |

The first step to generalize this implication is that we not only allow for a specific truncation level . Furthermore, we want to set specific regression coefficients to zero, also for . Additionally, we generalize the ordering of the equations from first to last using an ordering function . Thus, is on the left hand side of the -th equation and has at most right hand summands, including the error term, i. e. we obtain a triangular structure. We rewrite (3.1) as

| (3.3) | ||||

We define some additional terminology to deal with zero regression coefficients.

Definition 3.1 (SEM regressor sets).

Consider a SEM as in (3.3) with ordering function . Then, has at most potential regressors for . We define the set of potential regressors of by , i. e. the left hand side indices of the previous structural equations. Define the set , the set of actual regressors of . is the set of unused regressors.

We visualize the concepts in the following example. Recall that refers to the -th row in the SEM and to the corresponding left hand side index of the -th row.

Example 3.2 (Example 2.1 cont.).

Following our previous example, the R-vine matrix gives rise to the following values of the ordering function and the assignment function . Considering , we have the main diagonal , see also Table 1, left two columns. Since R-vine matrices are most often denoted as lower-diagonal matrices in the literature, we have . The values of the assignment function can be read column-wise from . For example, consider , the -th column of with . Then, and . Generally, we obtain for :

The values of can also be written in tabular form, see Table 1. The -th row of this table corresponds to column of the R-vine matrix . For example, consider the first column of , i. e. with , according to Table 1. Correspondingly , see also Table 1.

| 1 | 1 | - | - | - | - | - |

|---|---|---|---|---|---|---|

| 2 | 2 | - | - | - | - | |

| 3 | 6 | - | - | - | ||

| 4 | 3 | - | - | |||

| 5 | 5 | - | ||||

| 6 | 4 |

The R-vine Matrix is given by

We now want to evaluate the correspondence between independence copulas in the R-vine and zero coefficients in the SEM. Assume the following lower triangular family matrix with representing independence and indicating a Gaussian copula.

The zeros in the family matrix , i. e. independence copulas, are reflected by zero coefficients in the SEM. For and we have

We emphasize that only the parameter value is set to zero. The assignment function is unchanged since it is necessary to determine a valid R-vine structure. This way, we impose independence, i. e. sparsity in the R-vine which is reflected by the corresponding SEM. We now illustrate how this choice affects , and .

| (3.4) | ||||

In other words, the non-zero coefficients in the SEM (3.4) are drawn from the corresponding columns of the R-vine structure matrix where the family matrix is non-zero. Consider an arbitrary column in the matrix . The non-zero entries correspond to . For example, if we consider again the first column of , for and . Using this vector to obtain the non-zero entries from the R-vine structure matrix , we have the first column and thus the non-zero entries as in (3.4) and Table 2 for .

Having characterized the connection between R-vines and SEMs, our goal is now to find an inverse transformation. More precisely, given high dimensional data, we want estimate a SEM where many of the coefficients are zero. For simplicity, assume for . For each structural equation, we obtain a set with . This leaves us with a sparse SEM as in (3.1),

| (3.5) | ||||

Under additional assumptions, this SEM can also be written as an R-vine with structure matrix and family matrix . Because of the zero-coefficients in , entries in the family matrix can be set to , i. e. representing the independence copula. This means, we want to generalize the implication (3.2) in such a way that we have for each edge and :

| (3.6) |

Thus, we obtain a sparse R-vine model. This model is not restricted to a joint Gaussian probability distribution as our SEM is. We can estimate the marginal distributions entirely independent of the dependence behaviour and use vast numbers of parametric and non-parametric pair copulas to describe the joint distribution. To describe more precisely what is motivated by (3.6), we now introduce an R-vine representation of SEM.

Definition 3.3 (R-vine representation of a SEM).

Consider a SEM in dimensions, where we assume without loss of generality for .

| (3.7) | ||||

The SEM (3.7) has an R-vine representation if there exists an R-vine tree sequence such that for and we have

To put it in a nutshell, the -row of the SEM corresponds to column of the R-vine matrix for . This definition connects SEMs and R-vines. Based on this, we can consider setting specific regressors in the SEM to zero to obtain a sparse R-vine model. We note two caveats of this approach. First, of all, not every SEM with specific coefficients set to zero reflects a R-vine structure, since the proximity condition has to hold for the R-vine structure. Second, a SEM does not necessarily determine the R-vine structure uniquely. We give examples for these assertions and move on to sketch the general approach.

Example 3.4 (SEM without R-vine representation).

Consider the following SEM in dimensions.

If we now want to find a representing R-vine structure, the R-vine trees and must have edges in terms of the assignment function as we saw from definition 3.3. Since we have at most two right hand side summands, we need to find values for for and such that the following holds:

Assume without loss of generality the following edges are chosen in the first tree : . Now, we can not set to obtain as required. This is since , but . Note additionally that we can not have more than four edges in , since otherwise, it would not be a tree.

Next, we show an example of that two R-vines with identical SEM representations.

Example 3.5 (Different -truncated R-vines with identical SEM representation in dimensions).

Consider the following two -truncated R-vines and their SEM representations.

Both have identical SEM representations, i. e. only looking at the corresponding equations without knowing exactly the assignment function and thus, which regressor belongs to which R-vine tree, we are not able to distinguish between those two SEMs.

| (3.8) | ||||

| (3.9) | ||||

We will develop an approach which overcomes the restrictions sketched in the Examples 3.5 and 3.4. First, we will need to determine the R-vine structure based on the assignment function before we consider the sets of zero-coefficients. The method we are going to use for this is the Lasso, which we will recapture briefly.

4 The Lasso in linear regression

In the most general case, consider a sample of observations , , where . We want to approximate given a set of linear predictors

with unknown regression coefficients and . This is most often solved by minimizing the quadratic error with respect to and :

| (4.1) |

The solution to this optimization problem often contains many coefficients . Thus, for large, the model becomes overly parametrized and hard to interpret. Yet, solving (4.1) under the additional constraint

| (4.2) |

yields a parsimonious model. This regularization technique is called the Lasso and since its invention, see Tibshirani (1994), proved very useful in many applications. By shrinking coefficients exactly to zero, it combines both parameter estimation and model selection in one step. It also works in cases where , which are hard to solve otherwise. The Lasso is hence the method of choice when dealing with many possible predictors, of which only some contribute significantly to the model fit. For convenience, we will consider the following Lagrangian form of the optimization problem (4.3), which is equivalent to (4.1) under the constraint (4.2):

| (4.3) |

for some . One can show that a solution of (4.3) minimizes the problem in (4.1) under the condition (4.2) with , see Hastie et al. (2015). We do not include an intercept in our considerations and thus set for the remainder of the paper. If we consider the problem (4.3) and set , all coefficients , will be set to zero because of the penalization. Decreasing , more and more coefficients become non-zero. This relationship between and is called the regularization path. We formalize it by a set such that

Thus, for each we are given the non-zero regression coefficients. How to choose is not obvious. Most often, k-fold cross-validation is employed. Since it is not vital for the remainder of the paper, we describe it in Appendix A and conclude with a brief example, introducing the concept of regularization paths.

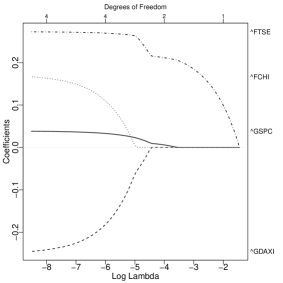

Example 4.1 (Lasso, regularization path, cross validation).

We use the worldindices dataset, included in the CDVine package, see Brechmann and

Schepsmeier (2013) comprising variables with observations on the u-scale. More precisely, these are the stocks indices ^GSPC, ^N225, ^SSEC, ^GDAXI, ^FCHI, ^FTSE of the US, Japanese, Chinese, German, French and British stock markets. We transform our observations to the z-scale using the normal quantile function, see page 2 and denote them by , where , , and so on. Let us assume that we want to model the index by the regressors ^GSPC, ^GDAXI, ^FCHI, ^FTSE, , respectively. We write the regression equation

with unknown regression coefficients and . We set and want to solve the regression problem with the Lasso. Thus we obtain the optimization problem

| (4.4) |

The solution to this optimization problem is a regularization path, either along or , i. e. the norm of the regression vector. We use the R-package glmnet (Friedman

et al., 2010) to calculate the regularization paths with respect to the norm, see Figure 4 and ..

We see that is the first non-zero coefficient along the regularization path. Additionally, we obtain that coefficients can of course also be negative and the regularization paths of different regressors may intersect. We denote the path by . Note that must not necessarily be the case as in this example. Above the plot, the corresponding number of non-zero parameters is indicated.

5 Vine Copula structure selection with the Lasso

To use SEMs and the Lasso to calculate a vine copula structure, we proceed in three steps. First, we calculate an ordering function for for the SEM ordering. Secondly, we identify the assignment function . Finally, we use the Lasso to identify the non-zero coefficient sets for . Before we calculate the ordering function , recall the three different scales, x-scale, u-scale and z-scale. Normally, data with is obtained on the x-scale. The transformation to the u-scale is important for copula modeling as the marginal effects have then been removed from the data. The transformation to the z-scale again is important for performing explorative data analysis. For example, considering contour shapes of bivariate data on the u-scale is hard. However, on the z-scale, deviations from normal dependence can be seen quite easily. Another advantage of the z-scale over the x-scale is that almost all data points will lie in an interval . Thus, performing regressions on such data will have standardized coefficients which eases the interpretation.

5.1 Calculation of the ordering function

Assume for the moment we already have found an ordering and that it coincides with the ordering of the variables, i. e. for . In a SEM in the form of (3.1), can have regressors for , based on our model assumption. Thus, if we compute solutions for the equations

we end up with a list of regression coefficients for each . Moreover, if we solve these equations with the Lasso and some suitably chosen , specific regression coefficients are set to zero. Considering all equations, some will occur more often with non-zero coefficients than others. Based on the SEM structure we have, it is beneficial to assign the regressors which occur often a low value of the ordering function . In a SEM with such a structure, these which occurred often as regressors can then be chosen as regressors by the assignment function .

Definition 5.1 (Lasso Ordering).

Consider samples from and let with columns , such that are the Lasso solutions to the minimization problems

For each possible regressor , calculate the number of over all and assign the ones with highest occurrence the lowest number in the ordering function . More precisely,

The corresponding are calculated via -fold cross-validation. In case of ties, i. e. two or more variables are occurring equally often as regressors for the remaining variables, we choose the ordering of these variables randomly.

The intuition is similar to a method proposed by Meinshausen and Bühlmann (2006) to find undirected graphical models. They use the Lasso to find neighbourhoods of nodes which are exactly the non-zero coefficient regressors calculated by the Lasso. We give a brief numerical example.

Example 5.2 (Calculation of ordering function ).

We consider the worldindices dataset, included in the CDVine package, see Brechmann and Schepsmeier (2013) comprising variables with observations on the u-scale. We transform our observations to the z-scale using the normal quantile function. We calculate Lasso regression coefficients of on for . Of course, the number of non-zero regression coefficients depends on the choice of the penalization coefficient for each regression on . Our experiments showed that it is feasible to choose according to -fold cross-validation.

| variable | id | # occurrence | ||

|---|---|---|---|---|

^GSPC

|

1 | 2 | 4 | 0.170 |

^N225

|

2 | 2 | 5 | 0.129 |

^SSEC

|

3 | 1 | 6 | 0.171 |

^GDAXI

|

4 | 3 | 3 | 0.065 |

^FCHI

|

5 | 4 | 1 | 0.049 |

^FTSE

|

6 | 4 | 2 | 0.053 |

If two or more variables have the same number of occurrences as regressors for other variables, we choose randomly to determine a unique ordering. If one or more variables do not occur as regressors at all, we assign them the last ranks and break ties by choosing randomly.

5.2 Sparse R-vine structure selection with the Lasso

Knowing the ordering function , we can write a SEM as in (3.1). Assume for notational convenience that the ordering already reflects the ordering as chosen in Section 5.1, i. e. . The first two equations of the SEM are trivially described. However, we can not directly use the Lasso to solve the later SEM equations stepwise or simultaneously. If we do, we might end up with non zero coefficients, which cannot be translated into a valid R-vine matrix as in Example 3.2. It is much more likely that we obtain a sparse SEM as in Example 3.4, which does not have a representation as R-vine in the sense of Definition 3.3 because of the restrictions imposed by the proximity condition. Additionally, we have to keep in mind that the solution to our SEM is also dependent on the choice of the penalization parameter . Thus, for different values of , different R-vine representations with different levels of sparsity result. We will now present an approach which computes an R-vine structure matrix together with a coefficient matrix , flexibly parametrizing the non-independence copulas in the R-vine in terms of . We consider the first R-vine tree and all higher order trees separately.

Selection of the first R-vine tree

Let be a matrix with . To obtain a valid R-vine matrix, we trivially set the entry and we are left to determine Lasso regularization paths for the remaining columns of . Thus, we have the regression problems for :

| (5.1) |

and denote the solutions as . To formalize how we process these solutions, recall the definition of the regularization path by the set returning the non-zero coefficients in the regression of for each value of :

Clearly, for . If and but and for , we say . This terminology is necessary to obtain an ordering on the set . It is motivated by the fact that we want to obtain the coefficients which are non-zero for the largest penalization values of . Thus, assume we have two coefficients for the problem (5.1), for some . Now, letting , both coefficients will become non-zero in the end, as the penalization shrinks to zero. However, if there exists a such that (5.1) is solved with and we obtain but , we consider the more important coefficient and denote . The set contains all non-zero regressors for the penalization value of the regression problem (5.1), ordered according to their first non-zero occurrence, i. e. the regularization path. In the case of two or more which are simultaneously non-zero on the regularization path, we take the one with the highest absolute value of the coefficient once they occur. This means, is the -th non-zero regressor on the regularization path of the regression problem (5.1). For the first R-vine tree , let be the -th entry in according to the ordering . Then, is chosen such that

| (5.2) |

Setting means we obtain the entire regularization path for each stored in . Together with the trivially set pair , each pair , corresponds to an edge in . These are pairs and no pair can occur more than once since each left hand side of the equations is different. Thus, we set . The R-vine matrix has the following form.

Thus, also the sets for are updated. As mentioned, in this step we calculate the entire regularization path for each , with respect to (5.1). However, we can not be sure if in one path subsequent values adhere to the proximity condition, see Example 3.4. We keep the paths stored as they may be compatible with the proximity condition which we will check later on and which may save computation time. Recall that the regularization paths also include the corresponding for which the coefficients on the regularization path become non zero. This finishes the selection of .

Selection of the higher order trees

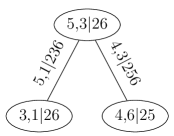

In the first tree, it was not necessary to take into account the proximity condition to compute a valid R-vine matrix . However, for the sequential steps, this will be the case. We consider again the -dimensional data from Example 5.2.

Example 5.3 (Example 5.2 cont.).

We use the ordering function to obtain . We set the value as it is the only allowed entry. Computing the regularization paths for the variables , i. e. solutions to (5.1), we obtain:

Note here that we consider as we want to obtain the entire path without any shrinkage. We take the first coefficients according to the ordering to determine the first R-vine tree , encoded by the -th row of the partial R-vine matrix .

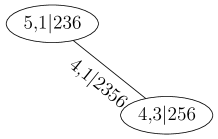

We need to determine the second tree, i. e. . First, we note that is the only valid choice. For the general case, consider the missing entry , marked by . First, we check whether the second entry in the regularization path, is valid. By checking the proximity condition (2.3), this is not the case as and are not connected in . Thus, we recompute the regularization path such that and adheres to the proximity condition. The set of possible regressors are the entries on the main diagonal to the right of the first column , where is already occurring. This leaves us with . From these, only is a possible entry according to the proximity condition. Thus, the remaining are set on a blacklist set for the entry by . Next, we re-run the penalized regression to find a new regularization path reflecting the blacklist. However, we also have to include that there are regressors we want to include on the regularization path before the second regressor, i. e. . We will call it the whitelist set . Since we can set individual penalties for each variable, we set . The optimization problem for the entry is given by:

Thus, we obtain a new sequence such that and adheres to the proximity condition. Whenever we have to start a new regression since the next regressor on the regularization path does not adhere to the proximity condition as described previously, we denote this as a proximity condition failure (pcf). In the end, we obtain the complete R-vine matrix . Additionally, we yield the corresponding entries for each entry, based either on an already computed regularization path or a new computation. We store it together with the R-vine matrix.

Using this approach, we complete a partial R-vine matrix column-wise from right to left in steps. However, since each lower order tree put restrictions on higher order trees by the proximity condition, we have iterations in the -th column for . From a computational point of view, it is more favourable to complete the matrix row-by-row, i. e. tree by tree. Thus, the structure estimation, i. e. computation of regularization paths, can be done in parallel. Because of the particular importance, we restate the optimization leading to the higher order tree estimates in the general form.

Definition 5.4 (Higher order tree selection).

Let be a partial R-vine matrix and assume without loss of generality the main diagonal . For each matrix entry with , define the set of potential regressors

, the whitelist and the blacklist

. We solve for the optimization problem:

| (5.3) |

to obtain a regularization path such that

-

•

for ,

-

•

adheres to the proximity condition.

To check whether a specific regressors is in the blacklist or not, we can use the partial R-vine matrix to see if (2.3) holds for this value. This concludes the part where we deal with the structure selection of the R-vine. We continue with considering the sparsity, i. e. how to use the Lasso to not only calculate a feasible structure but also perform model selection. Thus, we aim to make our R-vine model sparser by setting independence copulas.

5.3 Calculating R-vine regularization paths

From the previous calculations, we obtain an R-vine structure together with a regularization path, i. e. a functional relationship between and the non-zero regression coefficients. Now, we use this information to define the entire regularization path of the regression of onto , where denotes the R-vine structure matrix. This path will be called column regularization path. For notational convenience, we reverse the order of the rows of the matrix to obtain a new matrix . By this convention, the corresponding -th entry in column corresponds to the -th R-vine tree and we have for . For example, the first column of the R-vine Matrix from Example 5.3 is . Thus, . Finally note that the -th column in and has exactly non-zero entries.

Definition 5.5 (Column regularization path).

Let be an R-vine structure matrix in dimensions. A column regularization path of the reversed -th column is a vector for such that

for some .

Thus, each column of the R-vine matrix is assigned a vector which contains threshold values. These values are a by-product of the penalized regressions we ran and specify for which threshold of penalization, the corresponding SEM coefficients are set to zero, and hence, pair copulas are set to independence copulas. Thus, only by comparing component-wise for some , the column regularization path helps to set pair copulas to the independence copula to reflect a specific degree of sparsity associated to . For the column where we only have one value, we perform a single regression, so called soft thresholding to calculate the corresponding value of .

The advantage of this path is now that we are able to regularize each column of the R-vine matrix independently based on a solid theoretical reasoning, i. e. the Lasso. In practice, we consider the R-vine family matrix and fix a specific threshold of .

We consider the column regularization path and calculate component-wise the -th column of the R-vine family matrix as

Note that we reverse the ordering to work solely with lower triangular matrices, i. e. corresponds to for . Thus, all coefficients which are on the regularization path associated to a value of , are set to zero, and hence, the corresponding pair copula is set to the independence copula. The remaining pair copulas are then subject to further estimation. We can not only calculate single column regularization paths, but the entire regularization path of the R-vine.

Definition 5.6 (Regularization path of an R-vine).

Let be an R-vine structure matrix in dimensions. The regularization path of the R-vine is a matrix such that its columns are column regularization paths of the corresponding R-vine matrix columns , .

Summarizing, we obtain an R-vine structure which is not only entirely independent of pseudo-observations of lower level trees as compared to Dissmann’s algorithm. It is also independent of a specific penalization level since it is built stepwise by considering the non-zero regressors along the entire regularization paths for the R-vine tree sequence. This allows us to calculate one specific R-vine structure and then consider it under arbitrary many penalization levels , obtaining different levels of sparsity for one generally valid R-vine structure. We consider the regularization path matrix of the dimensional example R-vine from Example 5.7 before proposing methods for choosing .

Example 5.7 (Example 5.3 cont.).

Consider the R-vine matrix from Example 5.3. For comparison, we also display the R-vine matrix generated from Dissmann’s algorithm, calculated with VineCopula R-package, see Schepsmeier et al. (2016).

We compute the following regularization path matrix for the R-vine structure .

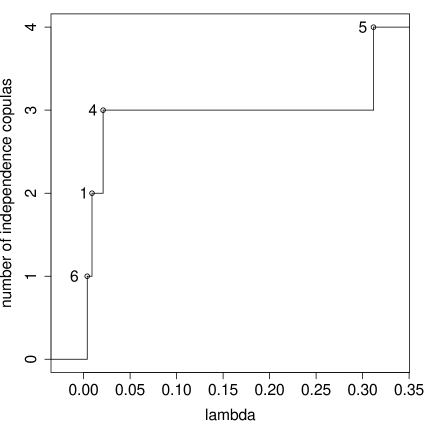

We observe that the values are column-wise monotonically decreasing if there is no proximity condition failure (pcf). For example, in the first column, the original regularization path did not meet the proximity condition and was recalculated. Thus, the values of are not necessarily decreasing. We visualize the column regularization path of column with a step function, indicating the corresponding entries in the R-vine matrix.

As , more and more pair copulas are set to the independence copula, starting from higher order trees to lower order tres. The matrix can now be used to regulate the sparsity, i. e. the number of independence copulas in our R-vine model.

5.4 Selection of the tuning parameter

We propose two approaches how we can utilize the regularization path matrices to obtain sparse R-vine models. A high value in these matrices means a significant contribution to the model fit, where a low values means the opposite. Introducing now a threshold value and checking whether or not entries in are below or above this value, the corresponding entries in are set to the independence copula or left for estimation of the pair copula type and parameter. Denote the regularization path of the R-vine by with family matrix .

Single threshold approach

The first approach is to specify some threshold and calculate the family matrix entries according to

| (5.4) |

Pair copulas corresponding to unit entries in the family matrix are then subject to, e. g. maximum likelihood estimation. Such an approach can easily be evaluated using a grid of . Recall that we only need to compute the structure and regularization matrix once upfront and then evaluate the corresponding threshold. In the data example, we consider a grid of threshold parameters.

Adaptive threshold approach

A second approach is to specify not a threshold value itself, but to calculate the threshold such that a specified share of the entries in fall below the threshold. Recall that has entries as lower diagonal matrix. Our intention is to grab the highest of the values in . Thus, we solve the following equation for a threshold :

| (5.5) |

This threshold can easily be found by sorting all entries of decreasingly and stop once entries have been found.

6 Numerical examples

6.1 Simulation study

We demonstrate the overall feasibility of our proposed approach, and superiority compared to the current standard algorithm for selection of R-vines. We show that the Lasso outperforms Dissmann’s method in terms of the modified BIC, see (2.4), when the data is sparse. Additionally, our approach is much faster and allows to separate the structure selection from the actual pair copula estimation. Thus, one structure matrix together with its R-vine regularization path matrix can be used to infer arbitrarily many different sparse R-vine models.

We gathered data from the S&P100 constituents from January 01, 2013 to December 31, 2016. Removing incomplete data because stocks entering or leaving the index, we obtain dimensions on observations. We calculated daily log-returns of the adjusted closing prices, incorporating dividends and stock splits. We fitted ARMA-GARCH models with and residuals distributed according to a normal, Student-t or skew Student-t distribution onto each of the time series, obtaining candidate models for each time series. We chose the time series model with highest log-Likelihood and calculated the corresponding standardized residuals. These residuals are transformed to the u-scale using their empirical cumulative distribution function. We use Dissmann’s algorithm to fit different models with several degrees of sparsity by imposing -truncations in the model fit. All pair copula families implemented in the R-package VineCopula were allowed and a level independence test was performed. Thus, we obtain three scenarios from which we draw replications of samples each. In all these scenarios, there is clearly non-Gaussian dependence, as we have e. g. Student -copulas and Frank copulas out of non independence copulas total. The proportions are very similar in the – and – truncated scenarios. For these replicated data sets, we fit Dissmann’s approach using the VineCopula R-package. Additionally, we use our novel Lasso approach and use the single threshold approach with , and adaptive threshold approach with and . We additionally test for independence copulas using a significance level after applying the threshold.

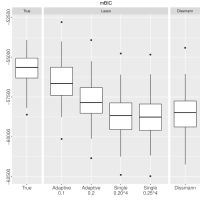

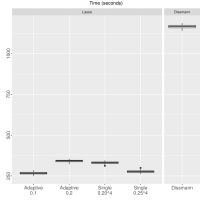

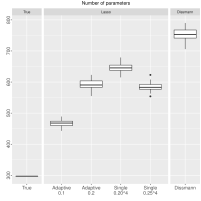

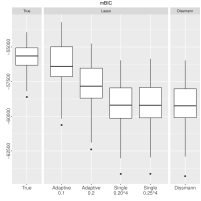

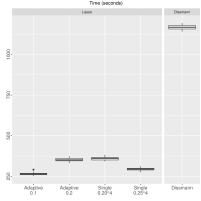

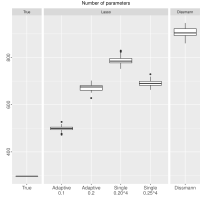

To draw conclusions, we consider boxplots where we compare the true values with both our Lasso approaches and Dissmann’s algorithm.

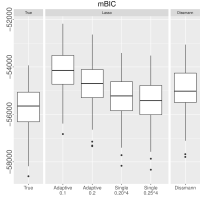

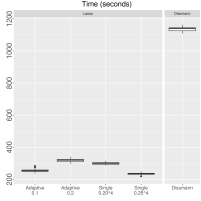

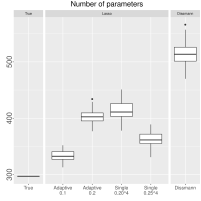

The boxplots in Figure 6 show mBIC, computation time and number of parameters for scenario . The remaining plots for the other scenarios are similar and hence deferred to Appendix B. We see that our approach attains mBIC closer to the true model than Dissmann in all the scenarios. Our novel approaches require much less parameter, where the single threshold approach is superior to the adaptive threshold approach. In terms of computation time, the single threshold approach is also advantageous to its competitors. This is particularly surprising since the single threshold is the same for all scenarios and works for different degrees of sparsity. We stress again that once a Lasso structure and regularization path is found, multiple models can be considered by varying the thresholding parameter .

6.2 Data example

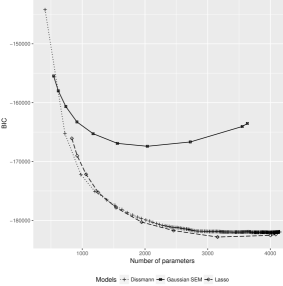

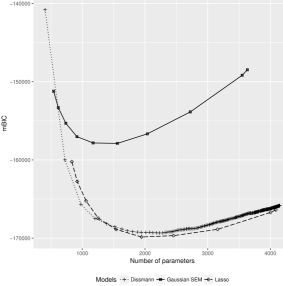

We scale our approach to even higher dimensions. Because of the availability of data, we again consider a financial dataset. Thus, we obtain data from the S&P500 constituents, also from January 1, 2013 to December 31, 2016. We isolate stocks which fall into the sectors Financial Services , Health Care , Industrials , Information Technology and Telecommunication Services . We apply the same procedure as to our data prepared for the simulation study and use suitable ARMA-GARCH models to remove trends and seasonality from the time series. The residuals are then transformed using the empirical cumulative distribution function to the u-scale. To obtain models, we use Dissmann’s algorithm with a level independence test and -truncation, i. e. we fit a full model and the split it into the first trees for to obtain submodels. We consider only one-parametric pair copula families and the -copula. The same pair copula selection also applies for our approach where we calculated models along a grid of single threshold values . We additionally also test for independence using a significance level . As a comparison, we also include the merely Gaussian SEM. We plot the corresponding BIC and mBIC values of both models, see Figure 7.

For the Lasso approach, the BIC and mBIC of the models is decreasing with decreasing as less pair copulas get penalized and we obtain more and more parameters. We see that BIC and mBIC attain a minimum for both Lasso and Dissmann approach different from the full models, where and for Dissmann. Both our Lasso approach and Dissmann’s algorithm outperform the Gaussian SEM significantly which indicates non-Gaussian dependence. Additionally, we see that the Lasso outperforms the Dissmann method in both criteria as it attains smaller values. For computation times, we report that one fit of the Lasso approach took approximately 30 minutes. The entire Dissmann fit for the full model took over 5,5 hours, all times on a Linux Cluster with 32 cores. Thus, all of the Lasso models on the grid were fitted before the full Dissmann fit was complete. The Gaussian-SEM is much faster compared to both non-Gaussian approaches. We see that in terms of mBIC, the optimal models have around parameters out of total parameters. We observe most often Student (386) and Frank copulas (810). Our expectation is that for higher dimensional models, the ratio of significant parameters to total number of parameters becomes even smaller, making sparse model selection key for high dimensional setups.

7 Discussion

We presented an entirely novel structure selection method for high dimensional vine copulas. Our proposal is based on application of the well known Lasso in the context of dependence modeling. We described the theoretical connection via structural equation models and how we can adapt the Lasso to reflect the proximity condition, a key ingredient for vine models. We transferred the concept of regularization paths to vine copulas and proposed methods for finding thresholds for models. In our numerical examples, we demonstrated the feasibility and superiority of our approach over existing methods when non-Gaussian dependence is present. We observed superior fit with respect to stronger penalizing goodness-of-fit measures and for computation time. We believe that in especially high dimensional settings, it is of paramount interest to first rule out the majority of the unnecessary information to only obtain the most significant contributions, which is clearly a characterizing feature of the Lasso. However, this also depends on the choice of the tuning parameter . More elaborate selection strategies for and other penalty functions, e. g. the elastic net by Zou and Hastie (2005), are also part of current and future research.

Acknowledgement

The first author is thankful for support from Allianz Deutschland AG. The second author is supported by the German Research foundation (DFG grant GZ 86/4-1). Numerical computations were performed on a Linux cluster supported by DFG grant INST 95/919-1 FUGG.

References

- Aas (2016) Aas, K. (2016). Pair-copula constructions for financial applications: A review. Econometrics 4(4).

- Aas et al. (2009) Aas, K., C. Czado, A. Frigessi, and H. Bakken (2009). Pair-copula constructions of multiple dependence. Insurance, Mathematics and Economics 44, 182–198.

- Akaike (1973) Akaike, H. (1973). Information theory and an extension of the maximum likelihood principle. In B. N. Petrov and F. Csaki (Eds.), Proceedings of the Second International Symposium on Information Theory Budapest, Akademiai Kiado, pp. 267–281.

- Bauer and Czado (2016) Bauer, A. and C. Czado (2016). Pair-Copula Bayesian networks. Journal of Computational and Graphical Statistics 25(4), 1248–1271.

- Bedford and Cooke (2001) Bedford, T. and R. Cooke (2001). Probability density decomposition for conditionally dependent random variables modeled by vines. Annals of Mathematics and Artificial Intelligence 32, 245–268.

- Bedford and Cooke (2002) Bedford, T. and R. Cooke (2002). Vines - a new graphical model for dependent random variables. Annals of Statistics 30(4), 1031–1068.

- Bollen (1989) Bollen, K. A. (1989). Structural Equations with Latent Variables (1st ed.). John Wiley and Sons, Chicester.

- Brechmann et al. (2012) Brechmann, E., C. Czado, and K. Aas (2012). Truncated regular vines in high dimensions with application to financial data. Canadian Journal of Statistics 40, 68–85.

- Brechmann and Joe (2014) Brechmann, E. C. and H. Joe (2014). Parsimonious parameterization of correlation matrices using truncated vines and factor analysis. Computational Statistics & Data Analysis 77, 233–251.

- Brechmann and Schepsmeier (2013) Brechmann, E. C. and U. Schepsmeier (2013). Modeling Dependence with C- and D-Vine Copulas: The R package CDVine. Journal of Statistical Software 52(3), 1–27.

- Dißmann et al. (2013) Dißmann, J., E. Brechmann, C. Czado, and D. Kurowicka (2013). Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics and Data Analysis 52(1), 52–59.

- Friedman et al. (2008) Friedman, J., T. Hastie, and R. Tibshirani (2008). Sparse inverse covariance estimation with the graphical lasso. Biostatistics 9(3), 432.

- Friedman et al. (2010) Friedman, J., T. Hastie, and R. Tibshirani (2010). Regularization Paths for Generalized Linear Models via Coordinate Descent. Journal of Statistical Software 33(1), 1–22.

- Frommlet et al. (2011) Frommlet, F., A. Chakrabarti, M. Murawska, and M. Bogdan (2011). Asymptotic Bayes optimality under sparsity for generally distributed effect sizes under the alternative. Technical report.

- Gruber and Czado (2015a) Gruber, L. and C. Czado (2015a). Bayesian model selection of regular vine copulas. Preprint.

- Gruber and Czado (2015b) Gruber, L. and C. Czado (2015b). Sequential bayesian model selection of regular vine copulas. Bayesian Analysis 10, 937–963.

- Hastie et al. (2015) Hastie, T., R. Tibshirani, and M. Wainwright (2015). Statistical Learning with Sparsity The Lasso and Generalizations. Boca Raton: CRC Press.

- Hoyle (1995) Hoyle, R. H. (1995). Structural Equation Modeling (1st ed.). SAGE Publications, Thousand Oaks.

- Kaplan (2009) Kaplan, D. (2009). Structural Equation Modeling: Foundations and Extensions (2nd ed.). SAGE Publications, Thousand Oaks.

- Kurowicka and Cooke (2006) Kurowicka, D. and R. Cooke (2006). Uncertainty Analysis and High Dimensional Dependence Modelling (1st ed.). John Wiley & Sons, Ltd, Chicester.

- Kurowicka and Joe (2011) Kurowicka, D. and H. Joe (2011). Dependence Modeling - Handbook on Vine Copulae. Singapore: World Scientific Publishing Co.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and P. Bühlmann (2006, 06). High-dimensional graphs and variable selection with the Lasso. Ann. Statist. 34(3), 1436–1462.

- Müller and Czado (2016) Müller, D. and C. Czado (2016). Representing Sparse Gaussian DAGs as Sparse R-vines Allowing for Non-Gaussian Dependence. arXiv preprint arXiv:1604.04202.

- Schepsmeier et al. (2016) Schepsmeier, U., J. Stöber, E. C. Brechmann, B. Graeler, T. Nagler, and T. Erhardt (2016). VineCopula: Statistical Inference of Vine Copulas. R package version 2.0.6.

- Schwarz (1978) Schwarz, G. (1978). Estimating the dimension of a model. The Annals of Statistics 6(2), 461–464.

- Sklar (1959) Sklar, A. (1959). Fonctions dé repartition á n dimensions et leurs marges. Publ. Inst. Stat. Univ. Paris 8, 229–231.

- Stöber et al. (2013) Stöber, J., H. Joe, and C. Czado (2013). Simplified pair copula constructions-limitations and extensions. Journal of Multivariate Analysis 119(0), 101 – 118.

- Tibshirani (1994) Tibshirani, R. (1994). Regression Shrinkage and Selection Via the Lasso. Journal of the Royal Statistical Society, Series B 58, 267–288.

- Zou and Hastie (2005) Zou, H. and T. Hastie (2005). Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 67(2), 301–320.

Appendix A Cross validation for the Lasso

Assume a setup as introduced in the section 4. We divide the total data set of observations into randomly chosen subsets such that . We obtain training data sets and corresponding test data sets , . Then, the coefficient vector is estimated for various on each of the training sets. Now we use these coefficient vectors to predict for each test data set the values

For these values, we also know the true values , , . Thus, we can calculate the mean squared prediction error for this pair of training and test data:

Since we have pairs of training and test data, we obtain an estimate for the prediction error for each of the values of by averaging:

Next, consider the dependence between and the corresponding error . A natural choice is to select such that is minimal in , we denote this by . Alternatively, we choose such that it is at least in within one-standard error of the minimum, denote . For both types of cross validation methods, see Friedman et al. (2010) or Hastie et al. (2015, p. 13).

Appendix B Additional results of the simulation study