Minimum Rényi Entropy Portfolios

Abstract

Accounting for the non-normality of asset returns remains challenging in robust portfolio optimization. In this article, we tackle this problem by assessing the risk of the portfolio through the “amount of randomness” conveyed by its returns. We achieve this by using an objective function that relies on the exponential of Rényi entropy, an information-theoretic criterion that precisely quantifies the uncertainty embedded in a distribution, accounting for higher-order moments. Compared to Shannon entropy, Rényi entropy features a parameter that can be tuned to play around the notion of uncertainty. A Gram-Charlier expansion shows that it controls the relative contributions of the central (variance) and tail (kurtosis) parts of the distribution in the measure. We further rely on a non-parametric estimator of the exponential Rényi entropy that extends a robust sample-spacings estimator initially designed for Shannon entropy. A portfolio selection application illustrates that minimizing Rényi entropy yields portfolios that outperform state-of-the-art minimum variance portfolios in terms of risk-return-turnover trade-off.

Keywords: Portfolio selection; Shannon entropy; Rényi entropy; Risk measure; Information theory.

Introduction

In portfolio optimization, it is well-known that a high sensitivity of the optimal portfolio weights to estimation errors in the parameter inputs can render otherwise sound investment strategies largely sub-optimal out-of-sample (see Kolm et al. 2014 and references therein). This is in particular the case of the mean-variance portfolio of Markowitz (1952): the optimal weights are very sensitive to estimation errors in the assets’ expected return. To tackle this robustness issue, one can simply disregard the portfolio’s expected return constraint, leading to the risk-based allocation framework (see e.g. Ardia et al. 2017). Minimum risk portfolios have in particular attracted investors’ attention as “the minimum-variance portfolio usually performs better out of sample than any other mean-variance portfolio - even when the Sharpe ratio or other performance measures related to both the mean and variance are used for the comparison” (DeMiguel and Nogales 2009 p.560).

Minimum risk portfolios are commonly built using the variance as risk measure. As the sample-based minimum variance portfolio is still quite vulnerable to estimation errors, various robust alternatives have been developed (see Fabozzi et al. 2010 and Scutellà and Recchia 2013 for reviews). Shrinkage estimation as introduced by Ledoit and Wolf (2003, 2004a,b) has proved particularly appealing. Still, the problem remains that the variance is an adequate risk measure only for Gaussian distributions and is largely unaffected by increasing tail concentration (Vermorken et al. 2012). As a result, the minimum variance portfolio does not account for the non-normality of asset returns. Two main alternative approaches can be employed to deal with non-normality. First, one can minimize a downside risk measure, e.g. the minimum VaR and CVaR portfolios. However, such portfolios coincide with a mean-risk approach (Fabozzi et al. 2010), producing robustness issues as for the mean-variance portfolio. Second, one can extend the Taylor expansion of the utility function to include the portfolio return’s third and/or fourth moments (see e.g. Adcock 2014). However, robustifying such higher-order portfolios is very challenging due to increased dimensionality and large sensitivity to outliers.

In this article, we propose a new (albeit natural) way of designing robust minimum risk portfolios that account for the non-normality of asset returns. We do so by minimizing the portfolio return’s uncertainty measured via the exponential of Rényi entropy, estimated within a robust -spacings framework. The optimal portfolios so obtained are called minimum Rényi entropy portfolios. Entropy is a well-known concept coming from information theory. It precisely aims at quantifying the uncertainty/amount of randomness conveyed by a distribution, embedding all higher-order moments (Cover and Thomas 2006). As a result, it is not surprising to notice that Shannon entropy (the most standard definition of entropy) has been recognized as an appealing measure in finance (Sbuelz and Trojani 2008, Zhou et al. 2013, Ormos and Zibriczky 2014) portfolio management (Philippatos and Wilson 1972, Dionisio et al. 2006, Vermorken et al. 2012, Flores et al. 2017) and utility theory (Yang and Qiu 2005, Abbas 2006, Jose et al. 2008). However, when using entropy to construct optimal portfolios, the literature is so far limited to employing entropy as a penalty term besides a more standard cost function: one considers the weights as discrete probabilities, and uses their entropy as a penalty term to shrink them towards the equally-weighted solution (see Bera and Park 2008, Zhou et al. 2013). Instead, we use the entropy of the portfolio return’s distribution (not that of the weights) as the risk-based cost function. Searching for the weights minimizing the latter amounts to minimize the returns’ uncertainty and thus provides the minimum risk portfolio in the sense of information theory.

In addition, we rely on Rényi entropy, an extension of Shannon entropy. It features a parameter that allows one to trade off the minimization of central and tail uncertainty. We argue in particular in favor of setting as, then, Rényi entropy has natural connections with measures of spread (as shown by the extended Chebyshev’s inequality of Campbell 1966) and with a minimum variance-kurtosis objective (as shown by a novel Gram-Charlier expansion of the measure). The empirical results support that choice as well.

Our contribution is organized as follows. Section 2 explores the theoretical properties of the exponential Rényi entropy and makes the link with the notion of risk. Section 3 follows with the minimum Rényi entropy portfolio and its connections with higher-order moments. Section 4 derives a robust -spacings estimator of the measure and studies its consistency and robustness. We design and perform an empirical out-of-sample performance study of the proposed method in Section 5. Minimum Rényi entropy portfolios are shown to outperform standard minimum risk portfolios in terms of risk-adjusted performance, while achieving a reasonable level of turnover for values of close to zero. Section 6 concludes.

For conciseness, the proofs of the different propositions are reported in the Online Resources.

Exponential Rényi entropy and risk measurement

We start this section by introducing the Rényi entropy, a flexible measure that quantifies the uncertainty of a random variable from its distribution. It encompasses the well-known Shannon entropy which is recovered as a special case. We then show how its exponential transform can be thought of as a deviation risk measure. A discussion of the impact of Rényi’s parameter closes the section, arguing in particular that setting should be favored in our portfolio selection context.

In the sequel, we respectively denote and the cdf and pdf of a random variable . We are exclusively interested in continuous distributions.

Shannon and Rényi entropy

The entropy of a random variable commonly refers to its Shannon entropy, first introduced by Shannon (1948), giving birth to a new scientific discipline: information theory. It is defined as

| (2.1) |

This measure is known to quantify the amount of randomness embedded in . For instance, when is a continuous random variable with bounded support, this quantity is maximized for the uniform distribution, which is the most uncertain one. Shannon entropy embeds many important properties. We refer to Cover and Thomas (2006) for an extended treatment.

Rényi (1961) proposed a generalization of Shannon entropy in (2.1) with the help of a parameter . The idea was to consider a generalized averaging of , leading to the following definition:

| (2.2) |

whenever the expectation exists. Shannon entropy is recovered as a special case in the sense that

| (2.3) |

Just like Shannon entropy, Rényi entropy enjoys interesting properties. However, its exponential transform has more natural properties in the context of risk. The next section is dedicated to a more detailed analysis of the exponential Rényi entropy and its connection with deviation risk measures.

Exponential Rényi entropy

We denote by the exponential Rényi entropy, which, from (2.2), reads as

| (2.4) |

This quantity was first introduced by Campbell (1966) who studied its relevance as a measure of spread of a distribution for . We come back to the link between and measures of spread in Section 2.4. In this article, we apply this measure to the construction of minimum risk portfolios (see Section 3).

Properties

From the properties of Rényi entropy (see Koski and Persson 1992, Johnson and Vignat 2007, Pham et al. 2008), obeys the below properties.

Proposition 2.1.

Let be a real constant. satisfies the following properties:

-

(i)

translation-invariance:

-

(ii)

scaling property:

-

(iii)

it is non-increasing and continuous in .

Connection with deviation risk measures

Quantifying uncertainty, it is appealing to use the exponential Rényi entropy as a deviation risk measure, introduced by Rockafellar et al. (2006).

Definition 2.1.

A deviation risk measure is any functional satisfying:111 is the space of random variables defined on the support set having finite moment.

-

(i)

Positivity: for all non-constant , and for any constant ;

-

(ii)

Positive homogeneity: ;

-

(iii)

Translation-invariance: ;

-

(iv)

Sub-additivity: .

Let us show that fulfills the first three properties of deviation risk measures (sub-additivity is dealt with in next section).

Positive homogeneity and translation invariance result from the properties of in Proposition 2.1. Regarding positivity , is strictly positive if is non-constant from the positivity of the density . To see that it is null if is constant, let us compute where is a constant by computing the limit of as tends to zero for a given random variable of finite entropy:

The sub-additivity property

In this section, we begin with underlining that whereas is expected to be sub-additive for most cases encountered in portfolio selection, it is not, strictly speaking, sub-additive.

Proposition 2.2.

is, generally speaking, not a sub-additive measure.

Proof.

Appendix A gives three analytical counter-examples to sub-additivity using pairs of random variables : a pair of independent one-sided (Lévy), a pair of independent two-sided bimodal (Gaussian mixtures) based on the entropy bounds derived in Vrins et al. (2007), and eventually a pair of comonotonic random variables. ∎

We stress that this proposition contradicts some statements recently made in the portfolio management literature (see e.g. Flores et al. 2017).222We are grateful to the authors of the aforementioned paper for discussion about the provided counter-examples.

It is however worth stressing that those counter-examples are atypical in portfolio applications. The Lévy distribution for instance is extremely heavy-tailed: none of the moments are defined, and asset returns exibit much lighter tails in practice (Cont 2001). Similarly, multi-modal distributions and comonotonicity are behaviours that rarely arise in portfolio management.

In fact, just like for the Value-at-Risk (Danielsson et al. 2013), sub-additivity of the exponential Rényi entropy can be reasonably assumed to hold in the specific context of portfolio optimization. For instance, the exponential Rényi entropy of collapses to (Koski and Persson 1992). From the stability of the Gausian distribution, the sub-additivity property is equivalent to , which in turns holds from the sub-additivity of the standard deviation (Artzner et al. 1999).

However, this particular case is quite restrictive as asset returns are typically not well described by the Gaussian distribution. A more appealing candidate to model the fat tails observed in asset returns is the general class of elliptical (a.k.a. radial) distributions, that has many applications in mathematical finance and portfolio theory, see e.g. Chen et al. (2011). Elliptical distributions comprise, among others, the Gaussian, Student’s , Cauchy and Laplace distributions. As the next proposition shows, the exponential Rényi entropy is sub-additive when is distributed according to an elliptical distribution, providing a broader and more realistic sufficient condition than the Gaussian setting.

Proposition 2.3.

Let with a bivariate elliptical distribution, i.e.

where is a non-negative density generator function and is the absolute value of the determinant of , the scale matrix of . Then, is sub-additive for the pair .

Proof.

See Appendix B.1. ∎

Remark 2.1.

Proposition 2.3 can be extended to any dimension, meaning that, if , then . Combined with the positive homogeneity property, this means that is sub-additive at the portfolio level, i.e. denoting positive portfolio weights, we have .

Exponential Rényi entropy as a flexible risk measure

This section explains how allows to tune the relative contributions of the central and tail parts of the distribution, leading to different definitions of risk.

To show this, consider the two extreme cases and . As the next proposition shows, when , measures the spread of , while when , is given by the inverse of the supremum of (see Koski and Persson 1992).

Proposition 2.4.

Let be a continuous random variable, then and read as

| (2.5) | |||

| (2.6) |

where is the Lebesgue measure of the support set of , .

As one can see, changing modifies the way we measure entropy, i.e. uncertainty, and so the risk. Taking amounts to measure risk by the support of the distribution, while taking amounts to measure risk by the maximal probability. By minimizing the portfolio return’s entropy, as we propose in the next section, one can therefore minimize the density range on the -axis with or maximize the density range on the -axis with . focuses only on extreme values (low entropy = low distance between extreme values), while focuses only on the most likely outcomes (low entropy = high maximal probability), and so, in the symmetric unimodal case, on the center of the distribution.

From those two extreme cases, it results that, in portfolio selection applications, taking too large is not desirable because will barely be affected by tail events, which is the criticism that is made about the variance. Conversely, by decreasing , we assign more similar “weight” to all events, hence increasing the relative importance of tail events compared to events around the mode.

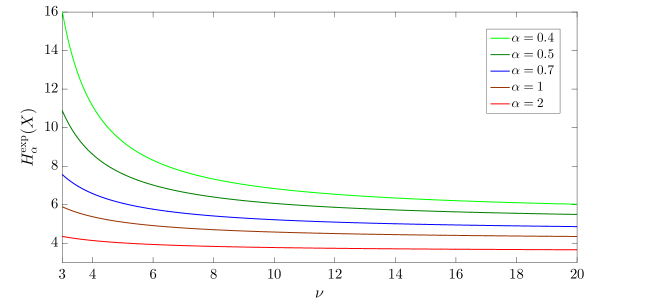

Example 2.1.

To illustrate this effect of , Figure 2.1 shows how , -Student(), evolves with for different values of . From Zografos and Nadarajah (2005), expresses as

| (2.7) |

As one can see, when going from to , the sensitivity to the increase of tail uncertainty is indeed increasingly visible.

Appeal of the case in a portfolio selection context

The previous section argued how decreasing the value of allows one to obtain a measure of entropy that is increasingly more affected by tail events. In this section, we show more specifically that investors should favor setting , in which case provides an appealing extension of the variance as a risk criterion.

First, for , has close connections with measures of spread. By minimizing the variance, investors ensure that most of the probability distribution of the portfolio return is concentrated in some small interval around the mean. This is established by Chebyshev’s inequality which, given the set , says that

Similarly, for , a small value of entails that most of the probability distribution of is concentrated on a set of small Lebesgue measure. This is determined by Campbell (1966)’s extended Chebyshev’s inequality.

Proposition 2.5.

Let be a continuous random variable whose Rényi entropy is defined for . Then, given and , the following inequality holds:

| (2.8) |

This inequality is more general than Chebyshev’s inequality as it does not only deal with the absolute deviation around the mean, but instead relates the spread in terms of the size of the set on which most of the probability density is situated. For a unimodal random variable with and as , which is common for asset returns, then there are only two values of for which (if ). Denoting them and , we have and (2.8) means that

as . In other words, if is small, the probability that is concentrated on a small interval around its mode is close to one.

A second argument in favor of setting is related to the Gram-Charlier expansion of Rényi entropy derived in Section 3.2. The expansion will show that, when , the coefficient in front of the kurtosis of is positive (and instead negative for ) and so that an increase in kurtosis decreases the Rényi entropy, as desired by investors.

Third, the empirical results presented in Section 5.2 display a largely better performance of the minimum Rényi entropy portfolio when as well.

Minimum Rényi entropy portfolio

Given the good match between the theoretical properties of and the desirable features of portfolio selection criteria, we use this measure as an objective function to design investment strategies. In particular, we propose to construct a minimum risk portfolio, called the minimum Rényi entropy (MRE) portfolio, that minimizes the exponential Rényi entropy of the portfolio return. We denote by the portfolio return such that where is the vector of portfolio weights and is the random vector of assets’ return.

Definition

The MRE portfolio over an investment set of assets for a given is defined as

| (3.1) |

where is a set of constraints on , including the full investment constraint .

Note that, being affected by higher-order moments that are non-convex functions of the weights (Jurczenko and Maillet 2006), the optimization program in (3.1) may not necessarily be convex, i.e. feature only one local optimum. Hence, in solving for the MRE portfolio, one must ideally resort to global optimization techniques rather than standard local optimizers. We come back to this matter in Section 5.1.4.

Connection with moments-based portfolios: A Gram-Charlier expansion

Traditional minimum risk portfolios are built from specific moments of the portfolio return, typically the variance, leading to the minimum variance portfolio, and possibly higher-order moments as in e.g. Martellini and Ziemann (2010), Adcock (2014) and Vanduffel and Yao (2017), that we call higher-order portfolios.

In the classical Markowitz Gaussian setting, the MRE portfolio coincides with the minimum variance portfolio as there is a one-to-one correspondence between and the variance for Gaussian random variables.

In a more general setting however, the MRE portfolio is more attractive than the minimum variance one as it accounts for the uncertainty coming from higher-order moments. To see this, it is useful to derive a truncated Gram-Charlier (GC) expansion of Rényi entropy.

Proposition 3.1.

Let and note its standardized copy. Define and . Then, the truncated GC expansion of , denoted , writes as

| (3.2) | ||||

with coefficients

| (3.3) | ||||

Proof.

See Appendix B.2. ∎

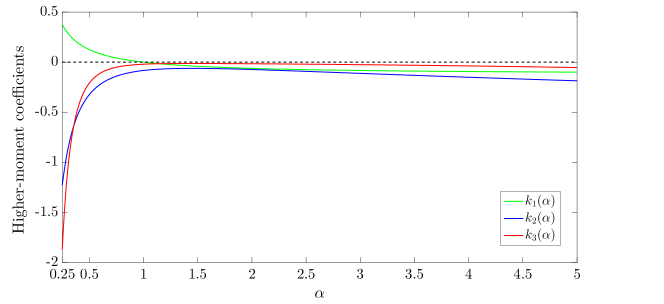

The three coefficients , and are displayed in Figure 3.1.

Setting , we get the GC expansion derived in Hyvärinen et al. (2001). Hence, the ability to control for kurtosis is a notable advantage of Rényi entropy over Shannon entropy, as in the latter case .

The connection between the MRE and higher-order portfolios is now made explicit. We have , which yields333Minimizing or is equivalent as is a monotonically increasing function.

| (3.4) | ||||

When is close to a Gaussian, the main contributing higher-order term will be . When , and so the MRE portfolio is similar to a minimum variance-kurtosis portfolio, which, as noted by Martellini and Ziemann (2010), is a well-performing higher-order portfolio as estimators for even moments are less noisy than estimators for odd moments. When however, and so the effect is reversed. In line with investors’ preferences for kurtosis, setting is thus more natural, as we noted in Section 2.4.

Hence, in line with Section 2.3, by playing with one trades off the minimization of the central (variance) and tail (kurtosis) uncertainty, i.e. of the first two even moments.

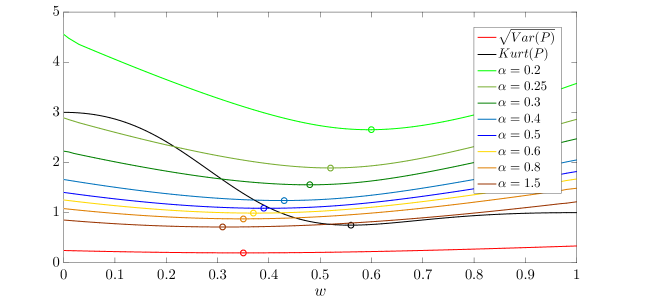

Example 3.1.

Consider assets that follow a zero-mean Student’s distribution with and . We build a portfolio and evaluate by numerical integration. On Figure 3.2, we display how , and depend on . As we can see, when is high enough, is close to the minimum variance solution because and that mostly central events matter when is high. However, the more decreases, the more important is the impact of the fatter tails of () and so the more approaches the minimum kurtosis solution.

Given that and are negative for all , the two additional terms and can be interpreted as driving the solution away from the Gaussian’s skewness and kurtosis. This is intuitive as, under a fixed mean and variance, the Shannon entropy is maximized for the Gaussian distribution (Cover and Thomas 2006).

Finally, note that the optimization program in (3.1) can accommodate an additional constraint on the portfolio expected return of the form with the vector of assets’ expected return, to account for the fact that investors do not only look at the risk, but also at the reward. In light of the GC expansion, such a framework would be linked to higher-moment efficient frontiers studied by e.g. Adcock (2014) and Qi et al. (2017). In the empirical study, we however concentrate on risk minimization due to the technical difficulties inherent in estimating the vector (see Section 1) that yield significant loss in out-of-sample performance.

Robust -spacings estimator of

In this section, we explain how, given a finite sample with , one can estimate in a robust way. In particular, we propose to use an estimator based on sample-spacings and discuss its properties in terms of consistency and robustness.

Motivation and expression for the -spacings estimator

To avoid making assumptions about the portfolio return’s distribution, we are looking for a non-parametric estimator of . There exists substantial research on non-parametric estimation of Shannon entropy, reviews of which can be found in Beirlant et al. (1997).

A natural way of estimating entropy is the plug-in estimate where a density estimator is plugged into the integral defining the entropy. One could for example choose the well-known Parzen (a.k.a. kernel) estimator. However, this estimator is known to be very sensitive to the bandwidth parameter, which can yield issues of stability for our portfolio optimization context.444When applied to our empirical data in Section 5, the Parzen estimator (with Gaussian kernel) achieves a worse risk-adjusted performance than the -spacings estimator considered here for a wide range of values of the bandwidth parameter. Instead, -spacings estimation of entropy is more reliable: Wachowiak et al. (2005) show that such estimators “are robust and accurate, compare favorably to the popular Parzen window method for estimating entropies, and, in many cases, require fewer computations than Parzen methods.” Therefore, we rely on a robust -spacings estimator of Rényi entropy that extends the Shannon entropy -spacings estimator of Learned-Miller and Fisher (1993), a “consistent, rapidly converging and computationally efficient estimator of entropy which is robust to outliers.”

Appendix C gives a detailed derivation of the estimator, of which we only report the final expression here for conciseness.

Proposition 4.1.

Let be a continuous random variable. Then, the -spacings estimator of , denoted , reads as

| (4.1) | ||||

where are the order statistics of (i.e. the observations sorted by increasing order) and is an integer parameter.

Proof.

See Appendix C. ∎

The parameter is a free parameter of great importance: increasing its value reduces the estimator’s variance by grouping more order statistics in each spacing . As a consequence, it plays a crucial role as it determines the robustness of the estimator, and in turn of the MRE portfolio. We come back to this in Section 4.2.2.

Taking the limit where , we recover the exponential of the estimator of Learned-Miller and Fisher (1993):

| (4.2) | ||||

Properties of the -spacings estimator

-spacings estimation of entropy has attracted numerous research (see Beirlant et al. 1997) and dates a while back, e.g. Vasicek (1976). However, it has been considered mainly for Shannon entropy and, even for this specific case, only asymptotic behaviour has been studied. In the general case , consistency has not been established. In this section, we first discuss the estimator’s properties in terms of consistency, arguing that the estimator’s asymptotic bias can be ignored for the sake of our portfolio application. Second, we show how the parameter determines the estimator’s robustness.

Asymptotic bias

Let us first consider the case and denote . van Es (1992) proved that is asymptotically biased but, interestingly, that the bias only depends on the fixed value of and not on the density :

| (4.3) |

where is the digamma function. Equation (4.3) means that we can simply subtract the bias to get a consistent estimator. Getting back to the exponential case, this means that

| (4.4) |

Interestingly, as readily seen from (4.4), because the asymptotic bias depends only on when , using the bias-corrected estimator in (4.4) or the biased estimator in (4.2) is equivalent when searching the weights that minimize the entropy in (3.1). Ideally, we would want the same result to hold for all , i.e. the asymptotic bias to depend only on and . While such a result is not known, Hegde et al. (2005) note that “in many practical applications, […] this bias does not affect the solution, since it is independent of the true data distribution […].” Further, as we now show, the estimator’s bias for and is the same, i.e. it does not depend on the specific location and scale of .

Proposition 4.2.

Let and , then the -spacings estimator’s bias .

Proof.

See Appendix B.3. ∎

Robustness to outliers

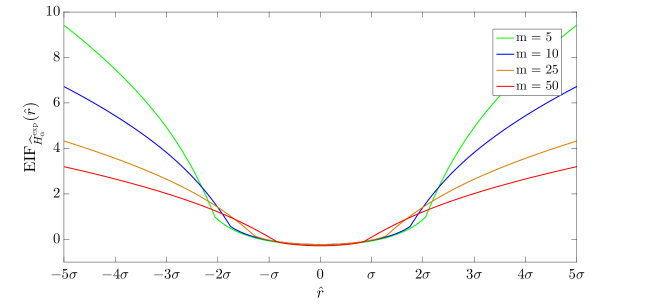

The parameter acts as a smoothing parameter that controls the estimator’s variance. This section shows that increasing makes the -spacings estimator more robust to outliers, which is crucial to ensure a solid out-of-sample performance of the MRE portfolio. Robustness conveys that a small perturbation from the true return distribution yields only a small change in the estimator’s value.

In assessing the robustness of an estimator, the Empirical Influence Function (EIF) represents a useful tool (see Hampel et al. 1986). Given an estimator of a quantity based on a sample of size , measures the sensitivity of the estimator to the addition of a supplementary observation in the sample:

| (4.5) |

Intuitively, the lower is , the more robust is the estimator . Figure 4.1 illustrates the EIF of the -spacings estimator - - for values from . Following Hampel et al. (1986), we set to eliminate the random sample variability. We consider and report the results for only as other values yield similar insights. One can indeed observe that the EIF decreases with for large enough values of , i.e. for outliers.

Out-of-sample empirical study

We finish the article with an out-of-sample performance study of the MRE portfolio that aims at showing the practical interest of the proposed portfolio policy compared to several existing strategies. The study is performed on six datasets commonly used as benchmarks in the portfolio optimization literature.

Methodology

Strategies of comparison

The reported results compare the MRE portfolio with to five different minimum variance (MV) portfolios. The first four solve the quadratic optimization program

| (5.1) |

by estimating with the sample covariance matrix and the three robust shrinkage estimators developed by Ledoit and Wolf (2003, 2004a,b):

| (5.2) | ||||

where minimizes the Frobenius norm between the shrinkage estimator and the true matrix . The three target matrices are based upon a constant correlation model (), a single-factor model () and a multiple of the identity matrix ().

The fifth MV portfolio is the one-step M-portfolio (MP) of DeMiguel and Nogales (2009):

| (5.3) |

where is the Huber’s robust loss function

| (5.4) |

We note that we have also implemented the robust Bayes-Stein mean-variance portfolio of Jorion (1986) as well as the minimum VaR portfolio using the robust estimator in Boudt et al. (2008). We do not report their results as, even though such criteria are positively affected by higher returns, they feature a lower risk-adjusted performance than the MRE portfolio due to their sensitivity to the portfolio expected return. The equally-weighted strategy has been considered as well but, while it naturally achieves the lowest turnover, it is largely outperformed by all the other strategies and so is not reported either.

Datasets

We rely upon six monthly returns datasets from the Kenneth French library that are extensively used as benchmarks in the literature to compare portfolio strategies (see e.g. DeMiguel et al. 2009a,b, Behr et al. 2013 and Ardia et al. 2017). The datasets are listed on Table 5.1.

| Datasets | Abb. | Time period | |

|---|---|---|---|

| 6 Fama-French portfolios of firms sorted by size and book-to-market | 6BTM | 6 | 07/1963 - 06/2016 |

| 25 Fama-French portfolios of firms sorted by size and book-to-market | 25BTM | 25 | 07/1963 - 06/2016 |

| 6 Fama-French portfolios of firms sorted by size and momentum | 6Mom | 6 | 07/1963 - 06/2016 |

| 25 Fama-French portfolios of firms sorted by size and momentum | 25Mom | 25 | 07/1963 - 06/2016 |

| 10 industry portfolios representing the US stock market | 10Ind | 10 | 07/1963 - 06/2016 |

| 17 industry portfolios representing the US stock market | 17Ind | 17 | 07/1963 - 06/2016 |

Dynamic rebalancing

We construct the portfolios by dynamic rebalancing. Rebalancing the weights not too frequently is important to ensure a satisfactory performance and turnover (Carroll et al. 2017), hence we set a rolling window of one year as in Behr et al. (2013). The estimation window is set to ten years, i.e. . We use as starting date 07/1963 as in DeMiguel et al. (2009b) and Behr et al. (2013), and rebalance the portfolios until 06/2016. This represents an out-of-sample period of 43 years.

Optimization

As pointed out in Section 3.1, the MRE optimization program is, generally speaking, not a convex problem. Therefore, to find the optimal weights, we rely on the global optimizer of Ugray et al. (2007) based on the Nelder-Mead algorithm. By doing so, we minimize the risk of getting stuck in a local minimum. We observe on the different datasets that recompiling the optimization several times yields essentially indistinguishable solutions, outlining that non-convexity is not a major issue.

Choice of

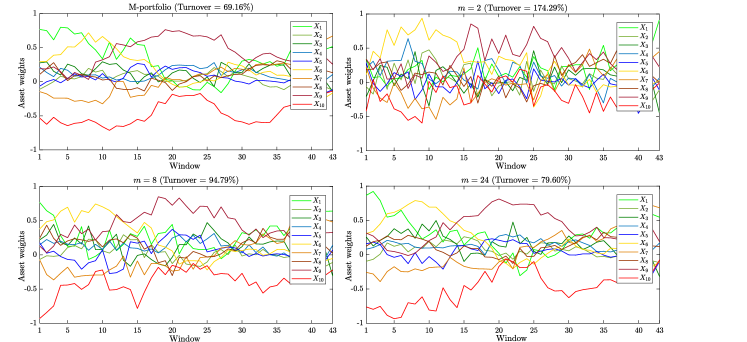

As pointed out in Section 4.2.2, the value of for the -spacings estimator is of paramount importance as it determines the robustness of the MRE portfolio. To illustrate this, Table 5.1 reports, for the 10Ind dataset, the time evolution of the MRE optimal weights for and . These are unconstrained weights, i.e. corresponding to . The weights of the M-portfolio are also reported for comparison. One can clearly observe that increasing improves the stability of the optimal weights obtained.

As a first strategy, we have considered the leave-one-out cross validation method, using as criteria maximum return, minimum variance and maximum Sharpe ratio. However, the results obtained were quite poor both in terms of performance and turnover. Allowing to change at each rolling window seems to add instability to the procedure and is not recommended.

Therefore, as a second strategy, we have used the simple rule-of-thumb which works well on the considered datasets. We observe actually that once is high enough, the results display only a very minor sensitivity to the specific value of that is chosen, so that one can set without fearing that another different but close value would yield dissimilar results.555Specifically, the results in Table 5.2 for and yield a very similar performance. The only changes are in terms of turnover, which is higher for and nearly identical for .

Weight constraints

To alleviate the estimation error, it is common in portfolio optimization to restrict the solution space . This has the effect of improving the stability of the optimal weights obtained and in turn the portfolios’ out-of-sample performance. This is easily understood from Table 5.1, in which all the portfolios feature a significant turnover in the unconstrained case, even though is relatively low in comparison to the sample size .

Therefore, we optimize the different portfolios subject to a constraint on the weights. We implement the global variance-based constraint (GVBC) devised by Levy and Levy (2014), which reads as

| (5.5) |

where and . The underlying rationale of GVBC is “to impose more stringent constraints on stocks with relatively high standard deviations, as the estimation errors for these stocks’ parameters, and hence the potential economic loss, are larger than for stocks with relatively low standard deviations” (Levy and Levy 2014 p.375). Using a U.S. industry portfolio dataset, the authors observe largely improved out-of-sample Sharpe ratios compared to several robust portfolio selection strategies for a wide range of values of . In particular, the results are stable for between 10% and 25%. In the sequel, we set at the higher hand, i.e. , as too low values make it difficult to distinguish between the different portfolios as they are too close to the equally-weighted one (corresponding to ). The conclusions of the empirical study remain the same for and , though naturally less strikingly.

Performance measures

We measure the portfolios’ out-of-sample performance and stability with three criteria:

-

1.

The Sharpe ratio, defined as

(5.6) and estimated using sample estimators, which is the most common performance measure used in the asset allocation literature. For simplicity, we assume that , as in e.g. DeMiguel et al. (2009b), i.e. we report the reciprocal of the coefficient of variation.

-

2.

Given that the appeal of the MRE portfolio compared to the minimum variance one is to account for higher-order uncertainty, using the Sharpe ratio alone is not sufficient to assess the merit of our portfolio policy. Hence, we also report the adjusted Sharpe ratio of Pézier (2004) that accounts for investors’ higher-moment preferences, defined as

(5.7) that we estimate using sample moment estimators.

-

3.

To assess the stability and associated transaction costs of the portfolios, we report the turnover, defined as usual as

(5.8) where is the number of rebalancing periods, is the desired weight of asset at time and is its weight before rebalancing at .

All three criteria are expressed in annual terms.

Out-of-sample results

| Sharpe ratio (SR) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| MRE portfolios | MV portfolios | ||||||||||

| MP | |||||||||||

| 6BTM | 0.844 | 0.845 | 0.846 | 0.841 | 0.832 | 0.815 | 0.835 | 0.821 | 0.833 | 0.836 | 0.841 |

| 25BTM | 0.985 | 0.980 | 0.973 | 0.961 | 0.937 | 0.906 | 0.953 | 0.913 | 0.951 | 0.957 | 0.956 |

| 6Mom | 0.768 | 0.763 | 0.753 | 0.750 | 0.716 | 0.700 | 0.738 | 0.741 | 0.738 | 0.737 | 0.731 |

| 25Mom | 0.936 | 0.948 | 0.957 | 0.960 | 0.954 | 0.928 | 0.902 | 0.920 | 0.904 | 0.903 | 0.916 |

| 10Ind | 0.995 | 1.001 | 1.014 | 1.013 | 0.971 | 0.936 | 0.977 | 0.970 | 0.983 | 0.973 | 0.976 |

| 17Ind | 0.938 | 0.947 | 0.936 | 0.965 | 0.905 | 0.891 | 0.936 | 0.924 | 0.935 | 0.935 | 0.918 |

| Average | 0.911 | 0.914 | 0.913 | 0.915 | 0.886 | 0.863 | 0.890 | 0.882 | 0.891 | 0.890 | 0.890 |

| Adjusted Sharpe ratio (ASR) | |||||||||||

| MRE portfolios | MV portfolios | ||||||||||

| MP | |||||||||||

| 6BTM | 0.829 | 0.830 | 0.831 | 0.826 | 0.816 | 0.800 | 0.822 | 0.809 | 0.821 | 0.824 | 0.826 |

| 25BTM | 0.969 | 0.963 | 0.956 | 0.943 | 0.919 | 0.889 | 0.940 | 0.906 | 0.939 | 0.944 | 0.940 |

| 6Mom | 0.759 | 0.753 | 0.744 | 0.741 | 0.708 | 0.694 | 0.730 | 0.733 | 0.729 | 0.729 | 0.723 |

| 25Mom | 0.921 | 0.934 | 0.943 | 0.947 | 0.943 | 0.918 | 0.889 | 0.909 | 0.892 | 0.890 | 0.902 |

| 10Ind | 0.990 | 0.995 | 1.005 | 1.004 | 0.965 | 0.927 | 0.973 | 0.966 | 0.979 | 0.968 | 0.972 |

| 17Ind | 0.950 | 0.959 | 0.945 | 0.975 | 0.911 | 0.901 | 0.950 | 0.940 | 0.950 | 0.949 | 0.929 |

| Average | 0.903 | 0.906 | 0.904 | 0.906 | 0.877 | 0.855 | 0.884 | 0.877 | 0.885 | 0.884 | 0.882 |

| Turnover | |||||||||||

| MRE portfolios | MV portfolios | ||||||||||

| MP | |||||||||||

| 6BTM | 0.184 | 0.182 | 0.183 | 0.189 | 0.218 | 0.266 | 0.171 | 0.167 | 0.170 | 0.168 | 0.168 |

| 25BTM | 0.499 | 0.535 | 0.616 | 0.966 | 1.356 | 1.502 | 0.448 | 0.464 | 0.443 | 0.445 | 0.478 |

| 6Mom | 0.167 | 0.171 | 0.180 | 0.191 | 0.247 | 0.284 | 0.168 | 0.168 | 0.167 | 0.168 | 0.178 |

| 25Mom | 0.437 | 0.444 | 0.523 | 0.635 | 0.860 | 1.200 | 0.417 | 0.413 | 0.410 | 0.416 | 0.422 |

| 10Ind | 0.348 | 0.350 | 0.378 | 0.450 | 0.600 | 0.776 | 0.283 | 0.276 | 0.274 | 0.286 | 0.321 |

| 17Ind | 0.526 | 0.568 | 0.685 | 0.825 | 1.033 | 1.246 | 0.449 | 0.422 | 0.433 | 0.452 | 0.467 |

| Average | 0.360 | 0.375 | 0.427 | 0.542 | 0.719 | 0.879 | 0.323 | 0.318 | 0.316 | 0.322 | 0.339 |

The results are reported on Table 5.2. Several interesting observations can be made.

First, comparing the six MRE portfolios, one can clearly see that and yield by far the worst performance. This is consistent with the Gram-Charlier expansion in (3.2), where setting favors solutions with more kurtosis (as in that case). Therefore, both from a theoretical and empirical perspective, it is recommended to set , as argued in Section 2.4.

Second, the turnover of the MRE portfolio systematically increases with . It does not increase too much from to but then quickly increases dramatically. This effect can be explained by the fact that the convexity of (as a function of ) decreases as increases. This is for example visible in Figure 3.2. This makes that the minimum is more bound to change largely from one rolling window to another as the objective function is flatter around the minimum the higher the .

Third, it is appealing to observe that, for , the performance of the MRE portfolio is very stable with respect to . This is easily observed by looking at the average and across the six datasets. This parameter robustness is an appealing behaviour for the decision-maker. Combined with the fact that the turnover increases with , this means that choosing quite low, in this case around , yields the best trade-off between risk, return and turnover.666For completeness, we have checked the results for as well. The turnover barely decreases compared to , and the Sharpe ratio measures remain nearly identical.

Fourth, comparing the MRE and MV portfolios, one can definitely observe that the MRE portfolios improve upon the MV portfolios both in terms of and , except naturally for and that we discard in the discussion below. Indeed, averaging across the six datasets, each MRE portfolio displays larger and than all the MV portfolios. In terms of turnover however, all the MRE portfolios display less stability than the MV portfolios. This is to be expected as the MRE portfolio is sensitive to the higher-order moments, which are more affected by outliers than the variance. That said, for and , the increase in turnover is quite modest (around 4 percentage points on average for ).

Therefore, we conclude that Rényi entropy provides a better risk criterion than the variance in an asset allocation context, especially for low values of , specifically around for the datasets considered here.

Conclusion

Many studies from the wide scientific literature suggest that minimum risk portfolios exhibit solid out-of-sample performances in spite of the fact that there is no target return constraint. Whereas variance – initially introduced by Markowitz – is a natural risk measure in a Gaussian framework, it fails to capture extreme events that arguably arise in real applications. In order to take this reality into account, various alternative risk measures have been put forward.

In this article, we have proposed a natural uncertainty measure - the exponential Rényi entropy - as a higher-moment criterion for portfolio selection. Rényi entropy generalizes Shannon entropy, yielding a set of uncertainty measures. Its parameter enables to tune the relative contributions of the central and tail parts of the distribution in the measure. Its exponential transform fulfills desirable properties as it is closely related to the class of deviation risk measures, as well as to measures of spread for .

Minimizing this measure yields the minimum Rényi entropy portfolio. A Gram-Charlier expansion shows that this portfolio represents a higher-moment extension of the minimum variance portfolio, with controlling the trade-off between variance and kurtosis minimization.

In practical settings, the empirical study has demonstrated that the minimum Rényi entropy portfolio fares better out-of-sample compared to state-of-the-art robust minimum variance portfolios in terms of trading off risk, return and turnover, especially for close to zero.

Beyond our application, this article points the appeal of Rényi entropy in various operations research problems as a powerful way of capturing higher-moment uncertainty, and of using entropy as an optimization criterion rather than just an ad hoc evaluation measure. In the particular case of portfolio selection, Rényi entropy has been shown to be a powerful alternative to existing risk criteria, opening the door to other applications. For instance, one may apply Rényi entropy to the risk parity strategy, which raises the challenge of computing the assets’ contributions to the portfolio return’s exponential Rényi entropy.

Acknowledgements

The authors are grateful to Kris Boudt and Victor DeMiguel for stimulating discussions. The authors also thank participants of the Actuarial and Financial Mathematics 2018 Conference, the 35th Annual Conference of the French Finance Association (AFFI) and the 2018 Belgian Financial Research Forum for their comments and suggestions. This work was supported by the Fonds National de la Recherche Scientifique (F.R.S.-FNRS) [grant number FC 17775].

Appendices

Counter-examples to sub-additivity of

In this section, we report the three counter-examples to sub-additivity as mentioned in Proposition 2.2.

Lévy distributions

Proposition.

is not sub-additive for a pair of independent Lévy-distributed random variables.

Proof.

The pdf of is given by and is strictly positive for . Its exponential entropy is known in closed-form (see Zografos and Nadarajah 2003): , where is the Euler-Mascheroni constant. We note the parameters of as and , respectively, with . As Lévy is a stable law, the sum is again Lévy-distributed with parameters and . Sub-additivity is thus equivalent to , which never holds when . ∎

Bimodal distributions

Proposition.

Consider a pair of independent standard Normal variables and a pair of independent Bernoulli variables of parameter , independent from both . Define with constants and . Then, is not sub-additive for the pair whenever e.g. and .

Proof.

Noting the standard Gaussian density, the marginal densities of are given by the Gaussian mixtures

| (A.1) | ||||

It is easy to show (see e.g. Pham and Vrins 2005) that the density of is

| (A.2) | ||||

Because only depends on the density of , we denote . Vrins et al. (2007) show that, for a random variable whose density can be written in the form with positive weights summing to 1 and Gaussian kernels , then can be bounded below and above. More explicitly,

| (A.3) |

with

| (A.4) | ||||

where , and . Rearranging the by increasing order and defining with , by convention, we have

| (A.5) |

with the complementary error function , where is the standard Gaussian cdf.

Using these lower and upper bounds, the operator fails to be sub-additive for the pair if

| (A.6) |

Indeed, the LHS is a lower-bound to while the RHS is an upper-bound to . Setting , the bounds in (A.4) applied to the densities in (A.1)-(A.2) read as

| (A.7) | ||||

from which we find for example that, setting , (A.6) holds as long as . ∎

Comonotonic random variables

Proposition.

is not sub-additive for a comonotonic pair , with , .

Proof.

Two random variables are comonotonic when can be written as where is a continuous strictly increasing function. Denote , which is also strictly increasing and so invertible, and denote its inverse. Then, the cdf of is given by

and its pdf reads

As a result, becomes

A change of variable and algebraic manipulations lead to

Based on a similar reasoning, we can show that

meaning that sub-additivity amounts to showing that

| (A.8) |

Let us now show instead a counter-example to (A.8) where the left-hand side is higher than the right-hand side, i.e. where is super-additive. Because has to be a positive random variable ( is strictly increasing), we consider . Define and . To have super-additivity, we have to show that

| (A.9) |

One can find the pdf of and to be given by

| (A.10) | |||

| (A.11) |

We can now compute the expectations. From (A.10), is given by the following integral:

A change of variable and integration by parts yields

where is the upper incomplete Gamma function. A similar derivation yields , i.e. minus the Euler-Mascheroni constant. Finally, we have in agreement with (A.9) that

hence providing a counter-example to sub-additivity. ∎

Proofs of Propositions

Proof of Proposition 2.3

Proof.

We set without loss of generality as is translation-invariant. The proof relies on the special convolution properties of elliptical distributions, see e.g. Fang and Zhang (1990). In particular, any linear combination of an elliptical random vector remains elliptical, meaning that we can write

where , and so . Moreover, any elliptical distribution can be written as , where and is a spherical distribution, i.e. an elliptical distribution with , the identity matrix. Applied to our case, this means that we can write , and , with . Finally, the sub-additivity of reduces to

which is true for any . ∎

Proof of Proposition 3.1

Proof.

The truncated Gram-Charlier (GC) expansion of the pdf of is given by

| (B.1) |

The proof relies on special properties of the Hermite polynomials ’s. Those are defined in relation with the derivatives of the standard Gaussian pdf :

The first four polynomials are given by , , and . They form an orthonormal system in the sense that

To find the GC expansion of , we want to have a similar system for the power of . One can check that with and that

with , , and . Hence, in relation with the original polynomials ’s, forms the system

Following algebraic manipulations, the first four coefficients ’s express as

Let us now first derive the GC expansion of . Using the results above and the second-order Taylor expansion , approximates as

Note that there is no term left because . Now, to finish, we need to get back to . We apply the Taylor expansion

where , which finally yields

where the functions , and are made explicit in (3.3). ∎

Proof of Proposition 4.2

Proof.

For notation purposes, we denote . From Royston (1982), the density of , the order statistics of , writes as

| (B.2) |

As we have and , we find from (B.2) that the density of is given by

meaning that

| (B.3) |

Replacing (B.3) in the expression of , we can write

| (B.4) |

Moreover, as , we have . Replacing this in (B.4) yields

which completes the proof. ∎

Derivation of the -spacings estimator of

This appendix derives the -spacings estimator of , whose final expression is reported in Section 4.1.

Consider i.i.d. copies of a continuous random variable . We denote the corresponding order statistics and define the associated -spacings () as the sequence of non-negative differences , for .

In a first step, we build a 1-spacing estimator of because the case has a natural relation to a sample-spacings estimator of the density .

First, recall that the order statistics of a uniform random variable follow a Beta distribution (Arnold et al. 1992). In particular,

Let us now map through to obtain i.i.d. random variables . Obviously, the sequence agrees with the order statistics , leading to:

Hence, the expected probability mass between two order statistics is

| (C.1) |

One can use this key observation to obtain an estimator of being told order statistics. Indeed, one can thus approximate between two successive order statistics by a constant such that the corresponding probability mass

agrees with the expected probability mass in (C.1). Denoting and , this yields

for . As the spacings form a partition of , one can approximate the density by

| (C.2) |

This estimator corresponds to the histogram composed of bins with bounds , , and with height such that the area of each bin is equal to .

From this density estimator, one can derive a 1-spacing plug-in estimator of as follows.

Proposition C.1.

Let the density of a continuous random variable be approximated by (C.2), then the 1-spacing plug-in estimator of is given by

| (C.3) |

Proof.

The estimator in (C.3) can not be used as such because, in general, we do not know and , i.e. the true support of . Following Learned-Miller and Fisher (1993), we therefore disregard the values below and above , and compensate this by a factor , yielding the final approximation

As detailed by Learned-Miller and Fisher (1993) in the specific case of Shannon entropy, the 1-spacing estimator suffers from high variance. To reduce the asymptotic variance, one can consider a -spacings estimator where the -spacings overlap. The counterpart of becomes

for . However, because the -spacings overlap, they do not form a partition of anymore (the same can fall in more than one -spacing), hence we lose the correspondence with the density estimator as a weighted sum of indicators in (C.2). Still, from the definition of , we can consider this extension of :

which corresponds to (4.1). Taking the limit , we recover the estimator in (4.2):

References

Abbas, A. (2006). Maximum entropy utility. Operations Research, 54(2), 277–290.

Adcock, C. (2014). Mean–variance–skewness efficient surfaces, Stein’s lemma and the multivariate extended skew-student distribution. European Journal of Operational Research, 234(2), 392–401.

Ardia, D., Bolliger, G., Boudt, K., & Gagnon-Fleury, J. (2017). The impact of covariance misspecification in risk-based portfolios. Annals of Operations Research, 254(1-2), 1–16.

Arnold, B., Balakrishnan, N., & Nagaraja, H. (1992). A first course in order statistics. New York: John Wiley & Sons.

Artzner, P., Delbaen, F., Eber, J., & Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3), 203–228.

Behr, P., Guettler, A., & Miebs, F. (2013). On portfolio optimization: Imposing the right constraints. Journal of Banking and Finance, 37, 1232–1242.

Beirlant, J., Dudewicz, E., Gyofi, L., & van der Meulen, E. (1997). Non-parametric entropy estimation: An overview. International Journal of Mathematical and Statistical Sciences, 6(1), 17–39.

Bera, A., & Park, S. (2008). Optimal portfolio diversification using the maximum entropy principle. Econometric Reviews, 27(4–6), 484–512.

Boudt, K., Peterson, B., & Croux, C. (2008). Estimation and decomposition of downside risk for portfolios with non-normal returns. Journal of Risk, 11, 79–103.

Campbell, L. (1966). Exponential entropy as a measure of extent of a distribution. Z. Wahrsch., 5, 217–225.

Carroll, R., Conlon, T., Cotter, J., & Salvador, E. (2017). Asset allocation with correlation: A composite trade-off. European Journal of Operational Research, 262(3), 1164–1180.

Chen, L., He, S., & Zhang, S. (2011). When all risk-adjusted performance measures are the same: In praise of the Sharpe ratio. Quantitative Finance, 11(10), 1439–1447.

Cont, R. (2001). Empirical properties of asset returns: Stylized facts and statistical issues. Quantitative Finance, 1, 223–236.

Cover, T., & Thomas, J. (2006). Elements of information theory (2nd ed.). New Jersey: Wiley.

Daníelsson, J., Jorgensenb, B., Samorodnitskyc, G., Sarma, M., & de Vries, C. (2013). Fat tails, VaR and subadditivity. Journal of Econometrics, 172, 283–291.

DeMiguel, V., Garlappi, L., & Uppal, R. (2009a). Optimal versus naive diversification: How inefficient is the 1/N portfolio strategy? The Review of Financial Studies, 22(5), 1915–1953.

DeMiguel, V., Garlappi, L., Nogales, F., & Uppal, R. (2009b). A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management Science, 55(5), 798–812.

DeMiguel, V., & Nogales, F. (2009). Portfolio selection with robust estimation. Operations Research, 57, 560–577.

Dionisio, A., Menezes, R., & Mendes, A. (2006). An econophysics approach to analyse uncertainty in financial markets: An application to the Portuguese stock market. The European Physical Journal B, 50, 161–164.

van Es, B. (1992). Estimating functionals related to a density by a class of statistics based on spacings. Scandinavian Journal of Statistics, 19(1), 61–72.

Fabozzi, F., Huang, D., & Zhou, G. (2010). Robust portfolios: Contributions from operations research and finance. Annals of Operations Research, 176(1), 191–220.

Fang, K., & Zhang, Y. (1990). Generalized multivariate analysis. New York: Springer.

Flores, Y., Bianchi, R., Drew, M., & Trück, S. (2017). The diversification delta: A different perspective. Journal of Portfolio Management, 43(4), 112–124.

Hampel, F., Ronchetti, E., Rousseeuw, P., & Stahel, W. (1986). Robust statistics: The approach based on influence functions. New York: Wiley.

Hegde, A., Lan, T., & Erdogmus, D. (2005). Order statistics based estimator for Rényi entropy. IEEE Workshop on Machine Learning for Signal Processing, 335–339.

Hyvärinen, A., Karhunen, J., & Oja, E. (2001). Independent component analysis. New York: John Wiley & Sons.

Johnson, O., & Vignat, C. (2007). Some results concerning maximum Rényi entropy distributions. Annales de l’Institut Henri-Poincaré (B) Probab. Statist., 43(3), 339–351.

Jorion, P. (1986). Bayes-Stein estimation for portfolio analysis. Journal of Financial and Quantitative Analysis, 21(3), 279–292.

Jose, V., Nau, R., & Winkler, R. (2008). Scoring rules, generalized entropy, and utility maximization. Operations Research, 56(5), 1146–1157.

Jurczenko, E., & Maillet, B. (2006). Multi-moment asset allocation and pricing models. West Sussex: John Wiley & Sons.

Kolm, P., Tütüncü, R., & Fabozzi, F. (2014). 60 years of portfolio optimization: Practical challenges and current trends. European Journal of Operational Research, 234(2), 356–371.

Koski, T., & Persson, L. (1992). Some properties of generalized exponential entropies with application to data compression. Information Sciences, 62, 103–132.

Learned-Miller, E., & Fisher, J. (2003). ICA using spacings estimates of entropy. Journal of Machine Learning Research, 4, 1271–1295.

Ledoit, O., & Wolf, M. (2003). Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of Empirical Finance, 10, 603–621.

Ledoit, O., & Wolf, M. (2004a). A well-conditioned estimator for large-dimensional covariance matrices. Journal of Multivariate Analysis, 88, 365–411.

Ledoit, O., & Wolf, M. (2004b). Honey, I shrunk the sample covariance matrix. Journal of Portfolio Management, 30, 110–119.

Levy, H., & Levy, M. (2014). The benefits of differential variance-based constraints in portfolio optimization. European Journal of Operational Research, 234, 372–381.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77–91.

Martellini, L., & Ziemann, V. (2010). Improved estimates of higher-order comoments and implications for portfolio selection. Review of Financial Studies, 23(4), 1467–1502.

Ormos, M., & Zibriczky D. (2014). Entropy-based financial asset pricing. Plos One, 9(12), e115742.

Pézier, J. (2004). Risk and risk aversion. In Alexander, C., & Sheedy, E. The professional risk managers’ handbook. Wilmington DE: PRMIA Publications.

Pham, D., & Vrins, F. (2005) Local minima of information-theoretic criteria in blind source separation. IEEE Signal Processing Letters, 12(11), 788–791.

Pham, D., Vrins, F., & Verleysen, M. (2008). On the risk of using Rényi’s entropy for blind source separation. IEEE Transactions on Signal Processing, 56(10), 4611–4620.

Philippatos, G., & Wilson, C. (1972). Entropy, market risk, and the selection of efficient portfolios. Applied Economics, 4(3), 209–220.

Qi, Y., Steuer, R., & Wimmer, M. (2017). An analytical derivation of the efficient surface in portfolio selection with three criteria. Annals of Operations Research, 251(1-2), 161–177.

Rényi, A. (1961). On measures of entropy and information. Fourth Berkeley Symposium on Mathematical Statistics and Probability, 547–561.

Rockafellar, R., Uryasev, S., & Zabarankin, M. (2006). Generalized deviations in risk analysis. Finance and Stochastics, 10, 51–74.

Royston, J. (1982). Expected normal order statistics (exact and approximate). Journal of the Royal Statistical Society Series C (Applied Statistics), 31(2), 161–165.

Sbuelz, A., & Trojani, F. (2008). Asset prices with locally constrained-entropy recursive multiple-priors utility. Journal of Economic Dynamics and Control, 32(11), 3695–3717.

Scutellà, M., & Recchia, R. (2013). Robust portfolio asset allocation and risk measures. Annals of Operations Research, 204(1), 145–169.

Shannon, C. (1948). A mathematical theory of communication. Bell Systems Technical Journal, 27, 379–423 and 623–656.

Ugray, Z., Lasdon, L., Plummer, J. Glover, F., Kelly, J., & Martí, R. (2007). Scatter search and local NLP solvers: A multistart framework for global optimization. INFORMS Journal on Computing, 19(3), 328–340.

Vanduffel, S., & Yao, J. (2017). A stein type lemma for the multivariate generalized hyperbolic distribution. European Journal of Operational Research, 261(2), 606–612.

Vasicek, O. (1976). A test for normality based on entropy. Journal of the Royal Statistical Society Series B (Methodological), 38(1), 54–59.

Vermorken, M., Medda, F., & Schroder, T. (2012). The diversification delta: A higher-moment measure for portfolio diversification. Journal of Portfolio Management, 39(1), 67–74.

Vrins, F., Pham, D., & Verleysen, M. (2007). Mixing and non-mixing local minima of the entropy contrast for blind source separation. IEEE Transactions on Information Theory, 53(3), 1030–1042.

Wachowiak, M., Smolikova, R., Tourassi, G., & Elmaghraby, A. (2005). Estimation of generalized entropies with sample spacing. Pattern Analysis and Applications, 8, 95–101.

Yang, J., & Qiu, W. (2005). A measure of risk and a decision-making model based on expected utility and entropy. European Journal of Operational Research, 164(3), 792–799.

Zhou, R., Cai, R., & Tong, G. (2013). Applications of entropy in finance: A review. Entropy, 15, 4909–4931.

Zografos, K., & Nadarajah, S. (2003). Formulas for Rényi information and related measures for univariate distributions. Information Sciences, 155(1-2), 119–138.

Zografos, K., & Nadarajah, S. (2005). Expressions for Rényi and Shannon entropies for multivariate distributions. Statistics & Probability Letters, 71(1), 71–84.