Two explicit Skorokhod embeddings for simple symmetric random walk††thanks: Xue Dong He thanks research funds from Columbia University and The Chinese University of Hong Kong. Jan Obłój thanks CUHK for hosting him as a visitor in March 2013 and gratefully acknowledges support from the ERC (grant no. 335421) under the EU’s FP, and from St John’s College in Oxford. The research of Xun Yu Zhou was supported by grants from Columbia University, the Oxford–Man Institute of Quantitative Finance and Oxford–Nie Financial Big Data Lab. The authors are grateful to anonymous reviewers for their comments and in particular express thanks to one reviewer who has suggested the current method of proof of Theorem 1 to replace our original one and made comments which led to our Remark 3.

Abstract

Motivated by problems in behavioural finance, we provide two explicit constructions of a randomized stopping time which embeds a given centered distribution on integers into a simple symmetric random walk in a uniformly integrable manner. Our first construction has a simple Markovian structure: at each step, we stop if an independent coin with a state-dependent bias returns tails. Our second construction is a discrete analogue of the celebrated Azéma–Yor solution and requires independent coin tosses only when excursions away from maximum breach predefined levels. Further, this construction maximizes the distribution of the stopped running maximum among all uniformly integrable embeddings of .

Keywords: Skorokhod embedding; simple symmetric random walk; randomized stopping time; Azéma-Yor stopping time.

1 Introduction

We contribute to the literature on Skorokhod embedding problem (SEP). The SEP, in general, refers to the problem of finding a stopping time , such that a given stochastic process , when stopped, has the prescribed distribution : . When such a exists we say that embeds into . This problem was first formulated and solved by Skorokhod (1965) when is a standard Brownian motion. It has remained an active field of study ever since, see Obłój (2004) for a survey, and has recently seen a revived interest thanks to an intimate connection with the Martingale Optimal Transport, see Beiglböck et al. (2016) and the references therein.

In this paper, we consider the SEP for the simple symmetric random walk. Our interest arose from a casino gambling model of Barberis (2012) in which the gambler’s cumulative gain and loss process is modeled by a random walk. The gambler has to decide when to stop gambling and her preferences are given by cumulative prospect theory (Tversky and Kahneman, 1992). Such preferences lead to dynamic inconsistency, so this optimal stopping problem cannot be solved by the classical Snell envelop and dynamic programming approaches. By applying the Skorokhod embedding result we obtain here, He et al. (2016) convert the optimal stopping problem into an infinite-dimensional optimization problem, find the (pre-committed) optimal stopping time, and study the gambler’s behavior in the casino.

To discuss our results, let us first introduce some notation. We let be a simple symmetric random walk defined on a filtered probability space , where . We work in discrete time so here, and elsewhere, denotes . We let be the set of –stopping times and say that is uniformly integrable (UI) if the stopped process is UI. Here, and more generally when considering martingale, one typically restricts the attention to UI stopping times to avoid trivialities and to obtain solutions which are of interest and use. We let denote the set of integers and the set of probability measures on which admit finite first moment and are centered. Our prime interest is in stopping times which solve the SEP:

| (1) |

Clearly if then . For embeddings in a Brownian motion, the analogue of (1) has a solution if and only if . However, in the present setup, the reverse implication depends on the filtration . If we consider the natural filtration where , then Cox and Obłój (2008) showed that the set of probability measures on for which is a fractal subset of . In contrast, Rost (1971) and Dinges (1974) showed how to solve the SEP using randomized stopping times, so that if is rich enough then for all . We note also that the introduction of external randomness is natural from the point of view of applications. In the casino model of Barberis (2012) mentioned above, He et al. (2017) and Henderson et al. (2017) showed that the gambler is strictly better off when she uses extra randomness, such as a coin toss, in her stopping strategy instead of relying on . Similarly, randomized stopping times are useful in solving optimal stopping problems, see e.g. Belomestny and Krätschmer (2016) and He et al. (2016).

Our contribution is to give two new constructions of with certain desirable optimality properties. Our first construction, in Section 2 below, has minimal (Markovian) dependence property: a decision to stop only depends on the current state of and an independent coin toss. The coins are suitably biased, with state dependent probabilities, which can be readily computed using an explicit algorithm we provide. Such a strategy is easy to compute and easy to implement, which is important for applications, e.g. to justify its use by economic agents, see He et al. (2017). We also link our construction to the embedding in Cox et al. (2011) and show that the former corresponds to a suitable projection of the latter. Our second construction, presented in Section 3, is a discrete–time analogue of the Azéma and Yor (1979) embedding. It is also explicit and its first appeal lies in the fact that it only stops when the loss, relative to the last maximum, gets too large. It also has an inherent probabilistic interest: it maximizes , simultaneously for all , among all , attaining the classical Blackwell et al. (1963) bound for . We conclude the paper with explicit examples worked out in Section 4.

2 Randomized Markovian Solution to the SEP

To formalize our first construction, consider and a family of Bernoulli random variables with , which are independent of each other and of . Each stands for the outcome of a coin toss at time when with standing for heads and standing for tails. To such we associate

| (2) |

which is a stopping time relative to where . The decision to stop at time only depends on the state and an independent coin toss. Accordingly, we refer to as a randomized Markovian stopping time. It is clear however that the distribution of is a function of and does not depend on the particular choice of the random variable . The following shows that such stopping times allow us to solve (1) for all .

Theorem 1

For any , there exists such that solves .

2.1 Proof of Theorem 1

We establish the theorem by embedding our setup into a Brownian setting and then using Theorem 5.1 in Cox et al. (2011). We reserve for the discrete time parameter and use for the continuous time parameter. We assume our probability space supports a standard Brownian motion . We let denote its natural filtration taken right-continuous and complete and denote its local time at time and level . Recall that is fixed. Cox et al. (2011) show that there exists a measure on such that, for a Poisson random measure with intensity , independent of ,

is minimal and embeds , i.e., and is uniformly integrable, the latter being equivalent to minimality of , see Obłój (2004, Sec. 8). Moreover, by the construction in Cox et al. (2011), for any interval that contains the support of . For it follows that is a measure on : ; otherwise, can possibly hit when the local time accumulates at certain non-integer level , in which case takes value . In addition, if has support bounded from above, i.e., for a certain , then and , with analogous expressions when the support is bounded from below. We note that is a Poisson process with parameter , and its first arrival time is exponentially distributed with parameter . We can now rewrite the embedding time as

Consider now consecutive hitting times of integers

and note that is a simple symmetric random walk. Recall that the measure is supported on . This implies a particularly simple structure of the stopping time . First, note that unless . Then, let us describe conditionally on . In particular, and is again exponential with parameter . happens in if and only if the local time accumulated at level is greater than this exponential variable. Clearly this event depends on the past only through the value of . More formally, considering the new Brownian motion , , and denoting its local time in zero as we see that if and only if which, conditionally on , is independent of and has probability which only depends on . Further, in this case . If we let on then it follows that is a stopping time relative to the natural filtration of enlarged with a suitable family of independent random variables, it has the precise structure of in (2), embeds and is UI. More precisely, using the space homogeneity of Brownian motion, we can define the probabilities using just the local time in zero, and it follows that if we take

then as required.

Remark 1

We note that by following the methodology in Cox et al. (2011) one could write a direct proof of Theorem 1, albeit longer and more involved than the one above. In particular, it is insightful to point out that if has a finite support – with , for some – then as constructed above can be shown to be the maximal element in the set

2.2 Algorithmic computation of the stopping probabilities

In this section, we work under the assumptions of Theorem 1 and provide an algorithmic method for computing obtained therein. We let and denote the expected number of visits of to state strictly before , i.e.:

| (3) |

Denote . It is a matter of straightforward verification to check that for any the processes

are martingales. To compute , we then apply the optional sampling theorem at and let . Using the fact that is a UI family of random variables together with monotone convergence theorem, we deduce that

| (4) | ||||

| (5) |

Writing , we now compute

Therefore, if , we must have . If and , which is the case if and only if is on the boundaries of the support, we have , i.e., we have to stop instantly. If , then and this can only happen for states outside the boundaries of the support. In this case, we set , which is consistent with the characterisation in Remark 1. Thus in Theorem 1 is given by

| (6) |

where and can be calculated from (4) and (5). This can be seen as the equation on the bottom of page S22 in Cox et al. (2011) specialised to our setup. While that equation is only argued heuristically therein, in our setup we can give it a rigorous meaning and proof.

3 Randomized Azéma-Yor solution to the SEP

Let us recall the celebrated Azéma-Yor solution to the SEP for a standard Brownian motion . As above, we reserve for the discrete time parameter and use for the continuous time parameter. To a centered probability measure on we associate its barycenter function

| (7) |

where and for such that . We let denote the right-continuous inverse of ; i.e., , . Then

| (8) |

satisfies and is UI. Furthermore, for any other such solution to the SEP, and any , we have ; hence maximizes the distribution of the maximum in the stochastic order. Here is the Hardy-Littlewood transform of and the bound is due to Blackwell et al. (1963), and has been extensively studied since; see e.g. Carraro et al. (2012) for details.

A direct transcription of the Azéma-Yor embedding to the context of a simple symmetric random walk only works for measures for which for all , which is a restrictive condition; see Cox and Obłój (2008) for details. For a general we should seek instead to emulate the structure of the stopping time: the process stops when its drawdown hits a certain level, i.e., when , or when it reaches a new maximum at which time a new maximum drawdown level is set, whichever comes first. Only in general, we expect to use an independent randomization when deciding to stop or to continue an excursion away from the maximum. Surprisingly, this can be done explicitly and the resulting stopping time maximizes stochastically the distribution of the running maximum of the stopped random walk among all solutions in (1).

Before we state the theorem we need to introduce some notation. Let and denote and the bounds of the support of . The barycentre function is piece-wise constant on with jumps in atoms of , is non-decreasing, left-continuous with for , for , and . The inverse function is right-continuous, non-decreasing with , and is integer valued on . Further, for and for ; in particular for . Moreover, for any , if and only if is in the range of ; consequently, for any that is not in the range of .

For each , is a nonempty set of finitely many integers which we rank and denote as . Similarly, we rank , which is a nonempty set of finitely many integers if and a set of countably many integers otherwise. Then, for each , . Note that we may have , in which case . For each and for when , define

| (9) | ||||

When , define

| (10) |

Then, as we will see in the proof of Theorem 2, for each and for when , is in for and we let ; when , is in for each and we set . Let be a family of mutually independent Bernoulli random variables, independent of , with . We let and define the enlarged filtration via .

We are now ready to define our Azéma–Yor embedding for . It is an –stopping time which, in analogy to (8), stops when an excursion away from the maximum breaches a given level. However, since the maximum only takes integer values, we emulate the behaviour of between hitting times of two consecutive integers in an averaged manner, using independent randomization. Specifically, if we let then after but before we may stop at each of depending on the independent coin tosses , while we stop a.s. if we hit . If we first hit then a new set of stopping levels is set. Finally, we stop upon hitting .

Theorem 2

Let and be given by

Then and for any

| (11) |

with the convention .

The optimality property in (11) is analogous to the optimality of in a Brownian setup, as described above and the bound in (11) coincides with .

Remark 2

Note that by considering our solution for we obtain a reversed Azéma–Yor solution which stops when the maximum drawup since the time of the historical minimum hits certain levels. It follows from (11) that such embedding maximizes the distribution of the running minimum in the stochastic order.

Remark 3

We do not claim that is the only embedding which achieves the upper bound in (11). Our construction inherits the main structural property of the Azéma-Yor embedding for : when a new maximum is hit, a lower threshold is set (which may depend on an independent randomisation) and we either stop when this threshold is hit or else a new maximum is set. This, in effect, averages out the behaviour of between hitting times of two consecutive integers. Instead, we could consider averaging out only the behaviour of between the first hitting time of an integer and the minimum between the hitting time of and the return of the embedded walk to . The resulting embedding would have the following structure: each time the random walk is at its maximum, a (randomized) threshold is set and the walk stops if it hits this threshold. If not, a new instance of the threshold level is drawn when the walk returns to . This is iterated until the walk is stopped at the current threshold level or when is hit which changes the distribution of the threshold level. This embedding appears less natural for us, having the casino gambling motivation in mind, however it should share the optimality property of in (11).

3.1 Proof of Theorem 2

It is straightforward to verify that all the conclusions of the theorem hold for the case in which , so we assume in the following that and thus . Throughout the proof we let and recall that . We first prove constructively that ’s are well defined and the constructed stopping time embeds into the random walk. Specifically, we argue by induction that for any the stopping time satisfies

| (12) |

For clarity of the presentation, somewhat lengthy and technical, proof of the above equalities is relegated to Section 3.2 below.

Next, we show that . If , by the construction of , we have

since , , and . Consequently, a.s. and for any , . If , by definition, a.s. Moreover, because (12) is true for , we have for any . From the definition of , we conclude that does not take any values in , so for any integer in this interval. Since , it remains to argue . This follows from (12) with :

where the fourth equality follows because for any and .

To conclude that it remains to argue that is UI, which is equivalent to , see e.g. Azéma et al. (1980). We first show that

Because never visits states outside any interval that contains the support of , we only need to prove this when , and hence , and taking .

By (15) and the construction of , we see that for , , we have

| (13) |

where the last equality is the case because

consequently,

For the function attains its maximum on in . Taking , we can bound the first term by

which goes to zero with since . Similarly, gives

and we conclude that as . It remains to argue that

This is trivial if . Otherwise and ’s are infinitely many. For , by the construction of , implies that visits before hitting 1 and is not stopped at any . Denote the and note that as . By construction, the probability that does not stop at given that reaches is , . On the other hand, the probability that visits before hitting 1 is . Therefore, the probability that visits before hitting 1 and is not stopped at any is

From (10), since has a finite first moment. Therefore,

The above concludes the proof of .

While (11) may be deduced from known bounds, as explained before, we provide a quick self–contained proof. Fix any and . When , by UI, we have and for any .

Next, by Doob’s maximal equality and the UI of , and hence, for ,

| (14) |

Considering and , and recalling (13), we obtain

3.2 Proof of (12)

First, we show the inductive step: we prove that (12) holds for given that it holds for . Because (12) is true for , we obtain

| (15) |

where is defined as in (9). Recalling that and for , we conclude that .

Consider first the case when , so that and stops if is hit between and . Consequently,

Next, we consider the case in which . A direct calculation yields

where the inequality follows from and for any . Consequently, . On the other hand, because for any that is not in the range of , we conclude that

Consequently, we have

where the last inequality holds because . It follows, since , that is strictly decreasing in with and . Consequently, is well defined and , . Recall . Set . Then, for each ,

Therefore, recalling the definition of and , for , we have . Further, and and we verify that (12) holds for .

We move on to showing the inductive base step: we prove (12) holds for . When , ’s are finitely many and the proof is exactly as above. When , by definition, because and . Recalling that for any that is not in the range of , we have

Because and for any , we conclude that . In addition, , showing that . Therefore, ’s are well defined, positive, and strictly decreasing in , and . Therefore, for each . Following the same arguments as previously, one concludes that (12) holds for .

4 Examples

We end this paper with an explicit computation of our two embeddings for two examples.

4.1 Optimal Gambling Strategy

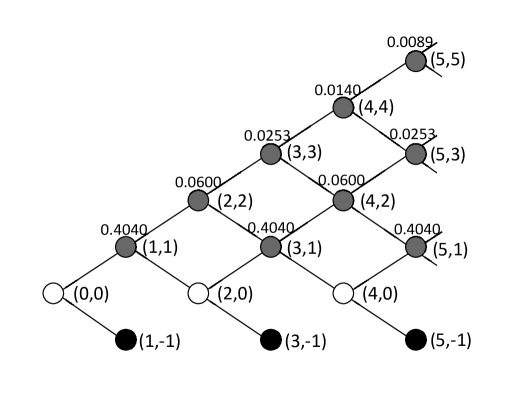

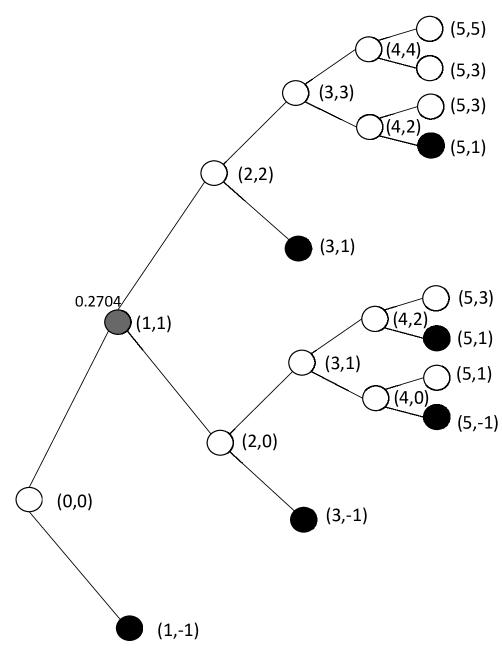

The first example is a measure arising naturally from the casino gambling model studied in He et al. (2016). Therein, a gambler whose preferences are represented by cumulative prospect theory (Tversky and Kahneman, 1992) is repeatedly offered a fair bet in a casino and decides when to stop gambling and exit the casino. The optimal distribution of the gambler’s gain and loss at the exit time is a certain , which may be characterised explicitly, see He et al. (2016, Theorem 2). With a set of reasonable model parameters111Specifically: , , , , and ., we obtain

| (16) |

We first exhibit the randomized Markovian stopping time of Theorem 1. Using the algorithm given in Section 2.2 we compute , the probabilities of a coin tossed at turning up tails, for all :

Note that and ; so one does not stop at 0 and must stop upon reaching . The stopping time is illustrated in the left pane of Figure 1: is represented by a recombining binomial tree. Black nodes stand for “stop”, white nodes stand for “continue”, and grey nodes stand for the cases in which a random coin is tossed and one stops if and only if the coin turns up tails. The probability that the random coin turns tails is shown on the top of each grey node.

Next we follow Theorem 2 to construct a randomized Azéma-Yor stopping time embedding . To this end, we compute ’s and ’s, which stand for the drawdown levels that are set after reaching maximum and the probabilities that the coins tossed at these levels turn up tails, respectively:

The stopping time is then illustrated in the right pane of Figure 1: is represented by a non-recombining binomial tree. Again, black nodes stand for “stop”, white nodes stand for “continue”, and grey nodes stand for the cases in which a random coin is tossed and one stops if and only if the coin turns up tails. The probability that the random coin turns up tails is shown on the top of each grey node.

By definition, is Markovian: at each time time , the decision to stop depends only on the current state and an independent coin toss. However, to implement the strategy, one needs to toss a coin most of the times. In contrast requires less independent coin tossing: e.g. in the first five periods at most one such a coin toss, but it is path-dependent. For instance, consider and . If one reaches this node along the path from (0,0), through (1,1) and (2,2), and to (3,1), then she stops. If one reaches this node along the path from (0,0), through (1,1) and (2,0), and to (3,1), then she continues. Therefore, compared to the randomized Markovian strategy, the randomized Azéma-Yor strategy may involve less independent coin tosses but is typically path-dependent222Indeed, He et al. (2017) showed that, theoretically, any path-dependent strategy is equivalent to a randomization of Markovian strategies. as it considers relative loss when deciding if to stop or not.

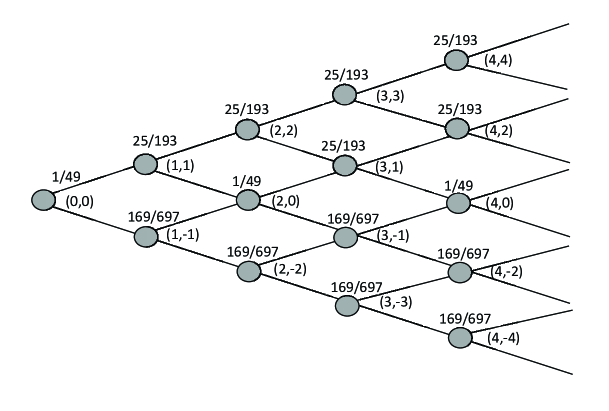

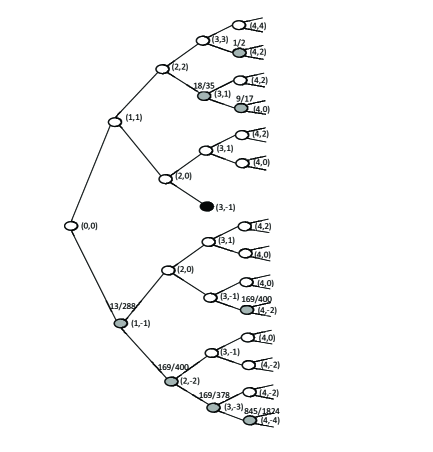

4.2 Mixed Geometric Measure

The second example is a mixed geometric measure on with

| (17) |

where , , , and so that .

The randomized Markovian stopping time that embeds given by (17) can be derived analytically. Indeed, according to the algorithm given in Section 2.2, the probability of a coin tossed at turning up tails is

The randomized Azéma-Yor stopping time that embeds given by (17) can also be derived analytically. Because the formulae for ’s and ’s are tedious, we chose not to present them here. Instead, we illustrate the two embeddings in Figure 2 by setting and . As in the previous example, the randomized Azéma-Yor stopping time involves less randomization than the randomized Markovian stopping time at the cost of being path-dependent.

References

- (1)

- Azéma et al. (1980) Azéma, J., Gundy, R. F. and Yor, M. (1980). Sur l’intégrabilité uniforme des martingales continues, Séminaire de Probabilités XIV, Vol. 784 of LNM, Springer, Berlin, pp. 53–61.

- Azéma and Yor (1979) Azéma, J. and Yor, M. (1979). Une solution simple au problème de Skorokhod, Séminaire de Probabilités XIII, Vol. 721 of LNM, Springer, Berlin, pp. 90–115.

- Barberis (2012) Barberis, N. (2012). A model of casino gambling, Management Science 58(1): 35–51.

- Beiglböck et al. (2016) Beiglböck, M., Cox, A. M. G. and Huesmann, M. (2016). Optimal transport and Skorokhod embedding, Inventiones mathematicae . (online first).

- Belomestny and Krätschmer (2016) Belomestny, D. and Krätschmer, V. (2016). Optimal stopping under model uncertainty: randomized stopping times approach, Ann. Appl. Probab. 26(2): 1260–1295.

- Blackwell et al. (1963) Blackwell, D., Dubins, L. E. et al. (1963). A converse to the dominated convergence theorem, Illinois Journal of Mathematics 7(3): 508–514.

- Carraro et al. (2012) Carraro, L., El Karoui, N. and Obłój, J. (2012). On Azéma-Yor processes, their optimal properties and the Bachelier-Drawdown equation, Ann. Probab. 40(1): 372–400.

- Cox et al. (2011) Cox, A. M. G., Hobson, D. G. and Obłój, J. (2011). Time-homogeneous diffusions with a given marginal at a random time, ESAIM: Probability and Statistics 15: S11–S24.

- Cox and Obłój (2008) Cox, A. M. G. and Obłój, J. (2008). Classes of measures which can be embedded in the simple symmetric random walk, Electronic Journal of Probability 13: 1203–1228.

- Dinges (1974) Dinges, H. (1974). Stopping sequences, Séminaire de Probabilités VIII, Vol. 381 of LNM, Springer, pp. 27–36.

- He et al. (2016) He, X. D., Hu, S., Obłój, J. and Zhou, X. Y. (2016). Optimal exit time from casino gambling: strategies of pre-committing and naive agents. SSRN 2684043.

- He et al. (2017) He, X. D., Hu, S., Obłój, J. and Zhou, X. Y. (2017). Randomized and path-dependent strategies in Barberis’ casino gambling model, Oper. Res. 65(1): 97–103.

- Henderson et al. (2017) Henderson, V., Hobson, D. and Tse, A. (2017). Randomized strategies and prospect theory in a dynamic context, Journal of Economic Theory 168: 287–300.

- Obłój (2004) Obłój, J. (2004). The skorokhod embedding problem and its offspring, Probability Surveys 1: 321–392.

- Rost (1971) Rost, H. (1971). Markoff-ketten bei sich füllenden löchern im zustandsraum, Ann. Inst. Fourier, Vol. 21, pp. 253–270.

- Skorokhod (1965) Skorokhod, A. V. (1965). Studies in the theory of random processes, Translated from the Russian by Scripta Technica, Inc, Addison-Wesley Publishing Co., Inc., Reading, Mass.

- Tversky and Kahneman (1992) Tversky, A. and Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty, Journal of Risk and Uncertainty 5(4): 297–323.