The Monotone Case Approach for the Solution of Certain Multidimensional Optimal Stopping Problems

Abstract

This paper studies explicitly solvable multidimensional optimal stopping problems of sum- and product-type in discrete and continuous time using the monotone case approach. It gives a review on monotone case stopping using the Doob decomposition, resp. Doob-Meyer decomposition in continuous time, also in its multiplicative versions. The approach via these decompositions leads to explicit solutions for a variety of examples, including multidimensional versions of the house-selling and burglar’s problem, the Poisson disorder problem, and an optimal investment problem.

Keywords: Monotone Stopping Rules; Optimal Stopping; Explicit Solutions; Multidimensional; Doob Decomposition; Doob-Meyer Decomposition; House-Selling Problem; Multiple Buying-Selling; Burglar’s Problem; Poisson Disorder Problem; Optimal Investment Problem

Mathematics Subject Classification: 60G40; 62L10; 91G80

1 Introduction

In multidimensional problems, optimal stopping theory reaches its limits when trying to find explicit solutions for problems with a finite time horizon or an underlying (Markovian) process in dimension . In the one-dimensional case with infinite time horizon, the optimal continuation set usually is an interval of the real line, bounded or unbounded, so it remains to determine the boundary of that interval, which boils down to finding equations for one or two, resp., real numbers. A wealth of techniques has been developed to achieve this, see Salminen (1985), Dayanik and Karatzas (2003) for one dimensional diffusions, or Mordecki and Salminen (2007) and Christensen et al. (2013) for jump processes, to name but a few.

The notion of a multidimensional stopping problem is employed in this article in the following sense. It is used for such problems where the general theory of optimal stopping prescribes that the optimal stopping time is given by the first entrance time of a stochastic process into a -dimensional optimal stopping set with (Euclidean) dimension . Some typical cases are as follows: The underlying stochastic process is a Markovian process with -dimensional state space; under certain explicit time dependencies of the pay-off, in particular for finite time horizon, the space-time process arises with . Particularly in discrete time problems multidimensional problems arise due to history dependence for the optimal stopping time, e.g. for a Markovian process of degree , or even full history dependence as in the well-known best choice problem of Robbins, see Bruss (2005). There are a few multidimensional problems, see Dubins et al. (1994), Margrabe (1978), Gerber and Shiu (1996), Shepp and Shiryaev (1995), which, by some transformation method, may be transferred to a one-dimensional problem. Let us call a multidimensional problem truly multidimensional (as a manner of speech) if such a transformation seems hardly possible, at least does not seem to be available in the current literature (as we know it). Explicit solutions for such problems seem to be rare, but, of course, many techniques have been developed to tackle such problems, either semi-explicitly using nonlinear integral equations, see the monograph Peskir and Shiryaev (2006) or the more recent article Christensen et al. (2018) for an overview, or numerically, see Chapter 8 in Detemple (2006) and Glasserman (2004).

The purpose of this note is to provide some examples of seemingly truly multidimensional problems with an explicit solution where the payoffs take the form or for stochastic processes in discrete time as well as in continuous time. Knowing the individual solutions for the -problems in general does not seem to lead to the explicit solution for the sum or product problem. Here, we present a class of examples for which this is possible, the key being the notion of monotone stopping problems. The class of monotone stopping problems has been used extensively in the solution of optimal stopping problems, in particular in the first decades starting with Chow and Robbins (1961, 1963). A long list of examples can be found in Chow et al. (1971) and, more recently, in Ferguson (2008). The extension to continuous time problems is not straightforward. This was developed in Ross (1971), Irle (1979), Irle (1983), and Jensen (1989). Although these references are not very recent, it is interesting to note that the solution to certain “modern” optimal stopping problems is directly based on the notion of monotone case problems. Here, one may look e.g. at the odds-algorithm initiated in Bruss (2000) and extended by Ferguson (2016), or at Christensen (2017) where, to solve the original problem, an auxiliary problem for a two-dimensional process consisting of the underlying Markov process and its running maximum with suitable monotonicity properties is introduced. See also Christensen and Irle (2019) for related results.

This paper aims at presenting the monotone case approach to optimal stopping by a systematic use of the Doob (in continuous time Doob-Meyer) decomposition of the pay-off process, and shows how it may be used to solve some multidimensional stopping problems. The Doob(-Meyer) decomposition is a well-known tool in the treatment of super-/sub-martingales, in particular in optimal stopping it is applied to the Snell envelope. In the theory of continuous time finance, the decomposition, applied to the Snell envelope, is used to obtain duality results for option pricing, see Jamshidian (2007) for an overview and further discussions.

Here we review monotone case problems in terms of the Doob(-Meyer) decomposition with regard to the optimality of the myopic stopping time in Section 2. Although this approach seems to be natural and is mathematically straightforward, we could not locate it in the literature in this form, so we present it in a survey style. Due to the simplicity of this approach, the very short proofs are given. Almost sure finiteness of stopping times is not needed in this approach. The multiplicative Doob(-Meyer) decomposition is included, and our treatment covers the discrete and continuous time case in a unified way such that it can be used for the application in multidimensional problems in Sections 3 and 4. In Section 3 we show that, under certain assumptions, the monotone case property of the individual stopping problems carries over to the sum- and product-type problems providing an explicit solution. For this, we use the Doob(-Meyer) decomposition. We discuss a variety of examples in Section 4. We start with multidimensional versions of the classical house-selling and burglar’s problem. Here, the original one-dimensional problems are well-known to be solvable using the theory of monotone stopping. Also the multidimensional house-selling problem with recall was already solved in Bruss and Ferguson (1997). The last two examples are multidimensional extensions of continuous-time problems: the Poisson disorder problem and the optimal investment problem, which in one dimension are usually solved using other argument. The more involved arguments concerning the Doob-Meyer decomposition are treated there in detail.

2 Monotone Stopping Problems

2.1 Monotone stopping problems in discrete time and the Doob decomposition

Let us first stay in the realm of discrete time problems with infinite time horizon. For a sequence of integrable random variables, adapted to a given filtration , we want to find a stopping time such that

| (1) |

Here runs through all stopping times such that exists. We include a random variable , so that the stopping times may assume the value . A natural choice for our problems below is see the discussion in Subsection 2.2.3.

There is a certain class of such problems for which we can easily solve this. Call the above problem a monotone case problem iff for all it holds that

Using sets in the notation this may be written as

A particularly simple sufficient condition for the monotone case is that the differences

hence

This condition turns out to be fulfilled in many examples of interest and allows for the treatment of multidimensional problems of sum type discussed in the following section.

If we only want to consider stopping times , e.g. if stopping in is clearly suboptimal, then we may formulate the monotone case condition only for . Of course, using , this may be subsumed in the case , so we shall look at in the following and, similarly in the latter continuous time case, at .

Comparing the current gain with what to expect in the next step leads to the stopping time

It is called the one-step look ahead rule or, as we will use in this paper, the myopic rule. In general, this does not yield an optimal rule, but in monotone case problems it is the natural candidate for an optimal one. The discussion of the optimality of for the monotone case is a well-known topic, see the references mentioned in the introduction. We, however, find it enlightening to provide a short review using the Doob decomposition, which leads to a shortcut to optimality results without the usual machinery of optimal stopping theory. This approach also provides a unifying line of argument for both discrete and continuous time. For every let

so that by telescoping expectation terms we have the Doob decomposition

with a zero mean martingale . For the myopic stopping time

– valid for all if – and in the monotone case

Thus we have

and, using for ,

So, for any stopping time , not necessarily finite a.s.,

Basically these simple inequalities are the foundation for the optimality properties of the myopic stopping time. We provide sufficient conditions for this optimality, called (V1) and (V2), which are suitable for our classes of problems, in Subsection 2.2.

Remark 2.1.

It is remarkable that the myopic stopping rule immediately provides optimal stopping times for all possible time horizons in the monotone case. The same observation also holds true in the continuous time case discussed below. See also Ferguson (2008) and Irle (2017). This is in strong contrast to most Markovian-type optimal stopping problems, where infinite time problems are often easier to solve as the stopping boundary is not time dependent.

2.2 Optimality of The Myopic Rule Based on the Doob Decomposition

We continue the treatment of Subsection 2.1 and assume that we are in the monotone case.

2.2.1 Optimality for finite time horizon

Let and a bounded stopping time. Then, using the martingale property, , valid for bounded stopping times,

This implies optimality of for the finite time horizon .

2.2.2 Optimality for infinite time horizon

The extension from the finite to the infinite case uses the approximation so that on , but on we need a specific definition of Here, we use

so that . We introduce the following conditions:

| (V1) |

| (V2) |

Note for (V1) that is increasing in .

Proof.

2.2.3 Discussion of Assumptions (V1) and (V2)

The validity of (V2) is of course a well-known topic in optimal stopping, independently of the monotone case context. We only remark that, under , Fatou’s Lemma shows that for any

The same holds if we add costs of observation, e.g. , assuming .

(V1) follows from the condition which is the standard assumption in optimal stopping theory, see e.g. Theorem 4.5, 4.5’ in Chow et al. (1971). This needs a short argument.

Proposition 2.3.

(V1).

Proof.

Using Fatou’s Lemma again, we have

Due to our definition of we have to show that on . On this set, is increasing, hence exists. Furthermore, is a martingale fulfilling the boundedness condition

since We may thus invoke the martingale convergence theorem and obtain the convergence of to some a.s. finite random variable. Since on , this shows the convergence of , hence of , on this set. ∎

2.3 Monotone stopping problems in continuous time and the Doob-Meyer decomposition

To find the extension of the discrete time case to continuous time processes we may use the Doob-Meyer decomposition. Under regularity assumptions, not discussed here, we have

where is a zero mean martingale and is of locally bounded variation. Now assume that we may write

where is increasing. Then the myopic stopping time – here often called infinitesimal look ahead rule – becomes

In this situation, we say that the monotone case holds if

If is non-increasing in , then again the monotone case property is immediate. The discussion of optimality is essentially the same as in the discrete time case, so is omitted. As no confusion can occur, we keep the notations (V1) and (V2) for the continuous-time versions of the optimality conditions.

2.4 Monotone stopping problems in discrete time and the multiplicative Doob decomposition

For processes with we may also consider the multiplicative Doob decomposition

where, with ,

Optimality of the myopic stopping time may also be inferred from this multiplicative decomposition in the monotone case. As in Subsection 2.1, we have for any

The multiplicative decomposition leads, however, to different sufficient conditions for optimality. There is also a connection to a change of measure approach. Both is discussed in Subsection 2.5 below.

We furthermore observe that we have a monotone case problem in particular if

which turns out to be a basis for the treatment of product-type problems in the following section.

2.5 Optimality of The Myopic Rule based on the Multiplicative Decomposition

We assume the setting of Subsection 2.4 and work under the assumption that we are in the monotone case.

2.5.1 Optimality for finite time horizon

2.5.2 Optimality for infinite time horizon

To extend this argument to infinite time horizon, first note that, due to the positivity property of the , (V2) is valid due to the discussion in Subsection 2.2.3. Condition (V1) has to be taken care of for the specific problem at hand (and we know from Subsection 2.2.3 that is sufficient).

We now present a measure-change approach leading to another sufficient condition for optimality. We use a probability measure such that for each , invoking the Kolmogorov extension theorem for the existence of . Then for any stopping time

Proposition 2.4.

Assume that

| (W1) |

Then, is optimal, i.e.

Proof.

For any stopping time

∎

As (W1) does not seem to be very handy for applications, we now give a sufficient condition. Using

we see that we obtain optimality for if

Note the similarities to the approach of Beibel and Lerche as presented, e.g., in Beibel and Lerche (1997) and Lerche and Urusov (2007). There, in the continuous time case, the decomposition and is used for the case for some diffusion . Then, the stopping time

has on the property , as the myopic stopping time.

2.6 Monotone stopping problems in continuous time and the multiplicative Doob-Meyer decomposition

Also in continuous time, a multiplicative Doob-Meyer-type decomposition of the form

can be found in the case of a positive special semimartingale , see Jamshidian (2007). For the ease of exposition, we now concentrate on the case of continuous semimartingales to have more explicit formulas. Using ibid, Theorem 4.2, is a local martingale and if denotes the process in the additive Doob-Meyer decomposition as in Subsection 2.3, the process here is given by

The optimality may be discussed as in the discrete time case. We again remark that the problem can be identified to be monotone in particular if the process

3 Multidimensional Monotone Case Problems

We now come to the main point of this paper: Can we use the monotone case approach to find truly multidimensional stopping problems with explicit solutions? The answer is yes as shown in the following section by several non-trivial examples.

3.1 The sum problem

Already for sequences of real numbers, usually with strict inequality. For optimal stopping,

with strict inequality as a rule; this means that being able to solve the stopping problems for and does not imply that we are able to solve the stopping problem for .

3.1.1 Discrete time case

Now let us look at sequences , adapted to a common filtration , with Doob decompositions

where as in Subsection 2.1. Then, the Doob decomposition for the sum process is

Now, if for each the stopping problem for is a monotone case problem it does not necessarily follow that we have a monotone case problem for , see Example 4.2 below. But in the special case that all the are non-increasing in the monotone case property holds. We formulate this as a simple proposition:

Proposition 3.1.

Proof.

For the Doob decomposition

the sequence is non-increasing in by assumption, yielding .

now follows from using Proposition 2.2.

∎

3.1.2 Continuous time case

Now let us look at continuous time processes , adapted to a common filtration , with Doob-Meyer decompositions

where for an increasing independent of . (The typical case is .) Then, the Doob decomposition for the sum process is

so that for non-increasing the monotone case property holds. We obtain as in the discrete time case:

Proposition 3.2.

Remark 3.3.

The assumptions of the previous Propositions can obviously be relaxed by assuming that the processes are of the form

where is a non-increasing process and is a process independent of .

3.2 The product problem

3.2.1 Discrete time case

Now let us again consider positive sequences , which we now assume to be independent. We are interested in the product problem with gain In this case

So, if in the special individual monotone case problems

| (2) |

then this also holds for the product. By noting that (V2) is fulfilled automatically by the positivity, we obtain

3.2.2 Continuous time case

The same argument as in the discrete case yields

Proposition 3.5.

Assume that the processes are positive, independent semimartingales, and have multiplicative Doob-Meyer decomposition

such that is non-increasing in for . Then:

-

(i)

The product problem for is a monotone case problem with myopic rule

-

(ii)

If (V1) holds for , then the myopic rule is optimal.

4 Examples

4.1 The multidimensional house-selling problem

4.1.1 Sum problem

-

(i)

With recall: Consider independent i.i.d. integrable sequences and let for

In the terminology of the house-selling problem we have houses to sell with gain when selling it at time describing a seller’s market, the max stating that former offers may be used. It is well-known, see Chow et al. (1971), that this is a monotone case problem with

where

The filtration is, of course, the one generated by the independent sequences. Since the are non-increasing in and the are non-decreasing in , the processes are non-increasing in . Proposition 3.1 yields that the multidimensional sum problem with reward

is a monotone case problem, and the myopic stopping time

with

is optimal under the additional condition of finite variance for . The validity of (V1) and (V2) follows as in the univariate case, see Ferguson (2008), Appendix to Chapter 4, Theorem 1.

This problem was already solved by Bruss and Ferguson (1997), using the monotone case property for the sum problem in this example. Their treatment includes the validity of (V1) and (V2), and also explicit solutions for the uniform distribution where and the exponential distribution with , . Then

In the house-selling problem, the functions are decreasing and convex. In the two examples above, we assumed identical distributions, so that are independent of and the stopping sets are symmetrical. Of course, this will disappear for non-identical distributions. If the underlying distributions are discrete then the will be piecewise linear and the optimal stopping sets polyhedrons.

-

(ii)

Without recall: In the house-selling problem without recall we have

which is not a monotone case problem. But this one-dimensional problem has the same solution, i.e. optimal stopping time and optimal value as the problem with recall. This is well-known and follows from

Looking at the sum problem without recall we have

which again is not a monotone case problem. But clearly, this is not a truly multidimensional problem as it reduces to the one-dimensional problem for Using , the optimal stopping time is given by

with

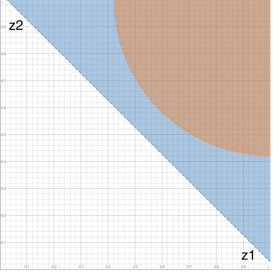

thus a different geometric structure than in the problem with recall. For the explicit computation of , an explicit expression for the distribution of is necessary. As a simple example we take two uniform distributions to arrive at

-

(iii)

Since

it follows that

see Figure 1. However, no ordering between and may be inferred, as they are entrance times for two different stochastic sequences.

Figure 1: Stopping sets (red, with recall) and (blue and red, without recall) for in the multidimensional sum house-selling problem for uniform distributions and .

4.1.2 Product problem

Another multidimensional version of the house-selling problem is the product problem with constant costs, that is, with reward

Looking at possible applications for the product structure, prices of houses do not provide an appropriate setting. We look at the selling of other assets, keeping the traditional notion of the house-selling problem, although asset-selling problem might be more appropriate. Stopping problems with product structure over various assets arise in American option pricing of financial engineers, and we sketch a possible case in the following lines. Consider (with recall) a selling problem for a commodity together with a currency conversion. Here and the first factor gives the obtainable prices for the commodity in currency , the second factor gives the obtainable exchange rates from currency to currency , and the product gives the prices in currency .

In the product problem with constant costs it can straightforwardly be checked that this does not lead to a monotone case problem. We now modify the classical problem by using a discounting factor which is also appropriate for the financial engineering setting. More precisely, for as above with a.s., let for

Then,

where

Similar as for the sum problem, the are decreasing in and the are non-decreasing in , so that the processes are non-increasing in . Therefore, the multidimensional product problem with gain

is a monotone case problem and the myopic stopping time reads as

It is not difficult to see that is optimal according to Proposition 3.4. Indeed, (V2) is clear due to the non-negativity and for (V1) it can be checked that for all integrable , see e.g. Ferguson (2008), Chapter 4, Section 4.7. We provide the short argument: Since

it is enough to consider . Then

As for the sum problem, we obtain an explicit optimal stopping rule when considering concrete distributions. For example, consider the case that all are uniformly distributed on , then

so

where

See Figure 2 for an illustration.

Remark 4.1.

In the house-selling problem, as well as in other stopping problems, one might want to also study a problem of -type, that is the problem with gain

So, this is not a truly multidimensional problem as it boils down to a one-dimensional problem for . But in general, it seems harder to work with max-type problems than with sum problems due to the nonlinearity of the max function.

4.2 The multidimensional burglar’s problem

4.2.1 Sum problem

Here, we have for independent i.i.d. sequences and , where describes the burglar’s gain and or when getting caught or not caught, resp. Then, we look at

with obvious interpretation. The sum problem corresponds to the question when a burglar gang should stop their work. It is well-known that for each we have a monotone case problem. Indeed, writing it holds that

hence iff

Let us first look at the sum problem for and constant . Then,

If , this becomes

hence

But if, e.g., the next then

and does not hold true in general. So, the sum problem is not monotone in general.

In the case that is independent of – that is the police takes away all stolen goods when catching one member of the gang – the problem for

is simply the one-dimensional case for

4.2.2 Product problem

We now consider the product version of the multidimensional burglar’s problem. Looking at possible applications we may turn to the pricing of American options in financial engineering. Here we may have asset prices together with exchange rates and default variables , a bankruptcy replacing being caught. We could directly apply Proposition 3.4, but we want to cover a slightly more general case including geometric averages of the gains:

with

so

Using it follows

so that holds iff

So under , the inequality to be considered becomes

Since is non-decreasing in , we have a monotone case problem and the myopic stopping time is the the first entrance time for the -dimensional random walk into the set

with

The optimality of the myopic stopping time follows as in the univariate case; see Proposition 3.4 and Ferguson (2008), 5.4.

4.3 The multidimensional Poisson disorder problem

The classical Poisson disorder problem is a change point-detection problem where the goal is to determine a stopping time which is as close as possible to the unobservable time when the intensity of an observed Poisson process changes its value. Early treatments include Galcuk and Rozovskiĭ (1971), Davis (1976), and a complete solution was obtained in Peskir and Shiryaev (2002). Further calculations can be found in Bayraktar et al. (2005).

Our multidimensional version of this problem is based on observing such independent processes with different change points The aim is now to find one time which is as close as possible to the unobservable times We now give a precise formulation. For each , the unobservable random time is assumed to be exponentially distributed with parameter and the corresponding observable process is a counting process whose intensity switches from a constant to at . Furthermore, all random variables are independent for different . We denote by the filtration given by

As is not observable, we have to work under the subfiltration generated by only. If we stop the process at , a measure to describe the distance of and often used in the literature is

for some constant . We also stay in this setting, although a similar line of reasoning could be applied for other gain functions also. As is not adapted to the observable information , we introduce the processes by conditioning as

The classical Poisson disorder problem for is the optimal stopping problem of over all -stopping times . Here, of course, we want to minimize (and not maximize) the expected distance, so that we have to make the obvious minor changes in the theory.

We now study the corresponding problem for the sum process

Here, denotes the number of processes without a change before plus a weighted sum of the cumulated times that have passed by since the other processes have changed their intensity.

A possible application is a technical system consisting of components. Component changes its characteristics at a random time . After these changes, the component produces additional costs of per time unit. denotes a time for maintenance. Inspecting component before produce (standardized) costs 1. Then, the optimal stopping problem corresponds to the following question: What is the best time for maintenance in this technical system?

The Doob-Meyer decomposition for can explicitly be found in Peskir and Shiryaev (2002), (2.14), and is given by

where

and denotes the posterior probability process

The process can be calculated in terms of in this case, see Peskir and Shiryaev (2002), (2.8),(2.9). Indeed,

where

In particular, it can be seen that the process is increasing in the case , and therefore so is It is furthermore easily seen that the integrability assumptions in Proposition 3.2 are fulfilled. Therefore, we obtain that the optimal stopping time in the multidimensional Poisson disorder problem is – under the assumption – given by

so that the optimal stopping time is a first entrance time into a half space

for the -dimensional posterior probability process.

Let us underline that the elementary line of argument used here breaks down for general parameter sets, where more sophisticated techniques, such as pasting conditions, have to be applied. This, however, seems to be very hard to carry out in this multidimensional formulation, and there does not seem to be hope to obtain an explicit solution in these cases. It is furthermore interesting to note that Remark 2.1 implies that our solution to the (multidimensional) Poisson disorder problem also solves the Poisson disorder problem in the finite time case, i.e. the optimal boundary is not time-dependent. This is, of course, in strong contrast to, e.g., the Wiener disorder problem, see Gapeev and Peskir (2006).

4.4 Optimal investment problem for negative subordinators

One of the most famous multidimensional optimal stopping problems is the optimal investment problem studied, e.g., in McDonald and Siegel (1986), Olsen and Stensland (1992), Hu and Øksendal (1998), Gahungu and Smeers (2011), Christensen and Irle (2011), Nishide and Rogers (2011), and Christensen and Salminen (2018). It can be described as follows: Let a fixed discounting factor, be a -dimensional Lévy process and let furthermore . The optimal stopping problem can then be formulated as

At the investment time the investor gets the fixed standardized reward 1 and has to pay the sum of the costs (with the reward as numéraire). In the notation of this paper we are faced with a sum problem for where

In the case that is a -dimensional (possibly correlated) Brownian motion with drift, it was conjectured in Hu and Øksendal (1998) that the optimal stopping time is a first entrance time into a half-space for the process . But this was disproved for all nontrivial cases, see Christensen and Irle (2011), Nishide and Rogers (2011). The structure of the optimal boundary is much more complicated in this case and can be characterized as the solution to a nonlinear integral equation, also for more general Lévy processes with only negative jumps, see Christensen and Salminen (2018). An explicit description cannot be expected to exist in general.

In a special case, however, our theory immediately leads to an explicit solution. We assume now that are negative subordinators, i.e., all (standardized) cost factors have non-increasing sample paths. This case is typically implicitly excluded in the general theory. For example, the integral equation for the optimal boundary obtained in Christensen and Salminen (2018) has no unique solution in this case.

In terms of the characteristic triple, the assumption means that the jump measure is concentrated on and the drift vector has non-positive entries . Applying Itô’s formula for jump processes yields the Doob-Meyer decomposition as

where

and

According to Remark 3.3, the sum problem is monotone and the myopic stopping time is

As each is bounded, it is immediate that (V1) and (V2) are fulfilled. We obtain that in this case a stopping rule as conjectured in Hu and Øksendal (1998) is indeed optimal.

Even more, the minimum of and is the optimal stopping time for the investment problem with time horizon by Remark 2.1. For other underlying processes, such a time-independent solution can of course not be expected.

Acknowledgments

We thank the referees for their careful reading of the manuscript and their very helpful suggestions.

References

- Bayraktar et al. (2005) E. Bayraktar, S. Dayanik, and I. Karatzas. The standard Poisson disorder problem revisited. Stochastic Process. Appl., 115(9):1437–1450, 2005.

- Beibel and Lerche (1997) M. Beibel and H. R. Lerche. A new look at optimal stopping problems related to mathematical finance. Statist. Sinica, 7(1):93–108, 1997.

- Bruss (2000) F. T. Bruss. Sum the odds to one and stop. Ann. Probab., 28(3):1384–1391, 2000.

- Bruss (2005) F. T. Bruss. What is known about Robbins’ problem? J. Appl. Probab., 42(1):108–120, 2005.

- Bruss and Ferguson (1997) F. T. Bruss and T. S. Ferguson. Multiple buying or selling with vector offers. Journal of Applied Probability, 34(4):959–973, 1997.

- Chow and Robbins (1961) Y. S. Chow and H. Robbins. A martingale system theorem and applications. In Proc. 4th Berkeley Sympos. Math. Statist. and Prob., Vol. I, pages 93–104. Univ. California Press, Berkeley, Calif., 1961.

- Chow and Robbins (1963) Y. S. Chow and H. Robbins. On optimal stopping rules. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 2:33–49, 1963.

- Chow et al. (1971) Y. S. Chow, H. Robbins, and D. Siegmund. Great expectations: the theory of optimal stopping. Houghton Mifflin Co., Boston, Mass., 1971.

- Christensen (2017) S. Christensen. An effective method for the explicit solution of sequential problems on the real line. Sequential Analysis, 36(1):2–18, 2017.

- Christensen and Irle (2011) S. Christensen and A. Irle. A harmonic function technique for the optimal stopping of diffusions. Stochastics, 83(4-6):347–363, 2011.

- Christensen and Irle (2019) S. Christensen and A. Irle. A general method for finding the optimal threshold in discrete time. Stochastics, 91(5):728–753, 2019.

- Christensen and Salminen (2018) S. Christensen and P. Salminen. Multidimensional investment problem. Mathematics and Financial Economics, 12(1):75–95, 2018.

- Christensen et al. (2013) S. Christensen, P. Salminen, and B. Q. Ta. Optimal stopping of strong markov processes. Stochastic Processes and their Applications, 123(3):1138 – 1159, 2013.

- Christensen et al. (2018) S. Christensen, F. Crocce, E. Mordecki, and P. Salminen. On optimal stopping of multidimensional diffusions. to appear in Stochastic Processes and Their Applications, 2018.

- Davis (1976) M. Davis. A note on the Poisson disorder problem. Banach Center Publications, 1(1):65–72, 1976.

- Dayanik and Karatzas (2003) S. Dayanik and I. Karatzas. On the optimal stopping problem for one-dimensional diffusions. Stochastic Process. Appl., 107(2):173–212, 2003.

- Detemple (2006) J. Detemple. American-style derivatives. Chapman & Hall/CRC Financial Mathematics Series. Chapman & Hall/CRC, Boca Raton, FL, 2006. Valuation and computation.

- Dubins et al. (1994) L. E. Dubins, L. A. Shepp, and A. N. Shiryaev. Optimal stopping rules and maximal inequalities for Bessel processes. Theory of Probability & Its Applications, 38(2):226–261, 1994.

- Ferguson (2008) T. S. Ferguson. Optimal stopping and applications. electronic text, see https://www.math.ucla.edu/ tom/Stopping/Contents.html, 2008.

- Ferguson (2016) T. S. Ferguson. The sum-the-odds theorem with application to a stopping game of Sakaguchi. Math. Appl. (Warsaw), 44(1):45–61, 2016.

- Gahungu and Smeers (2011) J. Gahungu and Y. Smeers. Optimal time to invest when the price processes are geometric Brownian motions. A tentative based on smooth fit. CORE Discussion Papers 2011034, Université catholique de Louvain, Center for Operations Research and Econometrics (CORE), 2011.

- Galcuk and Rozovskiĭ (1971) L. I. Galcuk and B. L. Rozovskiĭ. The problem of “disorder” for a Poisson process. Teor. Verojatnost. i Primenen., 16:729–734, 1971.

- Gapeev and Peskir (2006) P. V. Gapeev and G. Peskir. The Wiener disorder problem with finite horizon. Stochastic processes and their applications, 116(12):1770–1791, 2006.

- Gerber and Shiu (1996) H. U. Gerber and E. S. Shiu. Martingale approach to pricing perpetual American options on two stocks. Mathematical finance, 6(3):303–322, 1996.

- Glasserman (2004) P. Glasserman. Monte Carlo methods in financial engineering, volume 53 of Applications of Mathematics (New York). Springer-Verlag, New York, 2004. Stochastic Modelling and Applied Probability.

- Hu and Øksendal (1998) Y. Hu and B. Øksendal. Optimal time to invest when the price processes are geometric Brownian motions. Finance Stoch., 2(3):295–310, 1998.

- Irle (1979) A. Irle. Monotone stopping problems and continuous time processes. Z. Wahrsch. Verw. Gebiete, 48(1):49–56, 1979.

- Irle (1983) A. Irle. On the infinitesimal characterization of monotone stopping problems in continuous time. In Mathematical learning models—theory and algorithms (Bad Honnef, 1982), volume 20 of Lect. Notes Stat., pages 93–100. Springer, New York, 1983.

- Irle (2017) A. Irle. Discussion on “An effective method for the explicit solution of sequential problems on the real line” by Sören Christensen. Sequential Analysis, 36(1):27–29, 2017.

- Jamshidian (2007) F. Jamshidian. The duality of optimal exercise and domineering claims: A doob–meyer decomposition approach to the snell envelope. Stochastics, 79(1-2):27–60, 2007.

- Jensen (1989) U. Jensen. Monotone stopping rules for stochastic processes in a semimartingale representation with applications. Optimization, 20(6):837–852, 1989.

- Lerche and Urusov (2007) H. R. Lerche and M. Urusov. Optimal stopping via measure transformation: the Beibel-Lerche approach. Stochastics, 79(3-4):275–291, 2007.

- Margrabe (1978) W. Margrabe. The value of an option to exchange one asset for another. The journal of finance, 33(1):177–186, 1978.

- McDonald and Siegel (1986) R. McDonald and D. Siegel. The value of waiting to invest. The Quarterly Journal of Economics, 101(4):707–27, November 1986.

- Mordecki and Salminen (2007) E. Mordecki and P. Salminen. Optimal stopping of Hunt and Lévy processes. Stochastics, 79(3-4):233–251, 2007.

- Nishide and Rogers (2011) K. Nishide and L. C. G. Rogers. Optimal time to exchange two baskets. J. Appl. Probab., 48(1):21–30, 2011.

- Olsen and Stensland (1992) T. Olsen and G. Stensland. On optimal timing of investment when cost components are additive and follows geometric diffusions. Journal of Economic Dynamics and Control, 16:39–51, 1992.

- Peskir and Shiryaev (2002) G. Peskir and A. N. Shiryaev. Solving the Poisson disorder problem. In Advances in finance and stochastics, pages 295–312. Springer, Berlin, 2002.

- Peskir and Shiryaev (2006) G. Peskir and A. N. Shiryaev. Optimal stopping and free-boundary problems. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel, 2006.

- Ross (1971) S. M. Ross. Infinitesimal look-ahead stopping rules. The Annals of Mathematical Statistics, 42(1):297–303, 1971.

- Salminen (1985) P. Salminen. Optimal stopping of one-dimensional diffusions. Math. Nachr., 124:85–101, 1985.

- Shepp and Shiryaev (1995) L. A. Shepp and A. N. Shiryaev. A new look at pricing of the Russian option. Theory of Probability & Its Applications, 39(1):103–119, 1995.