Mass Volume Curves and Anomaly Ranking

Abstract

This paper aims at formulating the issue of ranking multivariate unlabeled observations depending on their degree of abnormality as an unsupervised statistical learning task. In the 1-d situation, this problem is usually tackled by means of tail estimation techniques: univariate observations are viewed as all the more ‘abnormal’ as they are located far in the tail(s) of the underlying probability distribution. It would be desirable as well to dispose of a scalar valued ‘scoring’ function allowing for comparing the degree of abnormality of multivariate observations. Here we formulate the issue of scoring anomalies as a M-estimation problem by means of a novel functional performance criterion, referred to as the Mass Volume curve (MV curve in short), whose optimal elements are strictly increasing transforms of the density almost everywhere on the support of the density. We first study the statistical estimation of the MV curve of a given scoring function and we provide a strategy to build confidence regions using a smoothed bootstrap approach. Optimization of this functional criterion over the set of piecewise constant scoring functions is next tackled. This boils down to estimating a sequence of empirical minimum volume sets whose levels are chosen adaptively from the data, so as to adjust to the variations of the optimal MV curve, while controling the bias of its approximation by a stepwise curve. Generalization bounds are then established for the difference in sup norm between the MV curve of the empirical scoring function thus obtained and the optimal MV curve.

Keywords. Anomaly ranking, Unsupervised learning, Bootstrap, M-estimation.

1 Introduction

In a wide variety of applications, ranging from the monitoring of aircraft engines in aeronautics to non destructive control quality in the industry through fraud detection, network intrusion surveillance or system management in data centers (see for instance (Viswanathan et al., 2012)), anomaly detection is of crucial importance. In most common situations, anomalies correspond to ‘rare’ observations and must be automatically detected based on an unlabeled dataset. In practice, the very purpose of anomaly detection techniques is to rank observations by degree of abnormality/novelty, rather than simply assigning them a binary label, ‘abnormal’ vs ‘normal’. In the case of univariate observations, abnormal values are generally those which are extremes, i.e. ‘too large’ or ‘too small’ in regard to central quantities such as the mean or the median, and anomaly detection may then derive from standard tail distribution analysis: the farther in the tail the observation lies, the more ‘abnormal’ it is considered. In contrast, it is far from easy to formulate the issue in a multivariate context. In the present paper, motivated by applications such as those aforementioned, we place ourselves in the situation where (unlabeled) observations take their values in a possibly very high-dimensional space, with say, making approaches based on nonparametric density estimation or multivariate (heavy-) tail modeling hardly feasible, if not unfeasible, due to the curse of dimensionality. In this framework, a variety of statistical techniques, relying on the concept of minimum volume set investigated in the seminal contributions of Einmahl and Mason (1992) and Polonik (1997) (see Section 2), have been developed in order to split the feature space into two halves and decide whether observations should be considered as ‘normal’ (namely when lying in the minimum volume set estimated on the basis of the dataset available) or not (when lying in the complementary set ) with a given confidence level . One may also refer to (Scott and Nowak, 2006) and to (Koltchinskii, 1997) for closely related notions. The problem considered here is of different nature, the goal pursued is not to assign to all possible observations a label ‘normal’ vs ‘abnormal’, but to rank them according to their level of ‘abnormality’. The most natural way to define a preorder on the feature space is to transport the natural order on the real line through some (measurable) scoring function : the ‘smaller’ the score , the more likely the observation is viewed as ‘abnormal’. This problem shall be here referred to as anomaly scoring. It can be somehow related to the literature dedicated to statistical depth functions in nonparametric statistics and operations research, see (Zuo and Serfling, 2000) and the references therein. Such parametric functions are generally proposed ad hoc in order to define a ‘center’ for the probability distribution of interest and a notion of distance to the latter, e.g. the concept of ‘center-outward ordering’ induced by halfspace depth in (Tukey, 1975) or (Donoho and Gasko, 1992). The angle embraced in this paper is quite different, its objective is indeed twofold: 1) propose a performance criterion for the anomaly scoring problem so as to formulate it in terms of -estimation 2) investigate the accuracy of scoring rules which optimize empirical estimates of the criterion thus tailored.

Due to the global nature of the ranking problem, the criterion we promote is functional, just like the Receiver Operating Characteristic (ROC) and Precision-Recall curves in the supervised ranking setup (i.e. when a binary label, e.g. ‘normal’ vs ‘abnormal’, is assigned to the sampling data), and shall be referred to as the Mass Volume curve (MV curve in abbreviated form). The latter induces a partial preorder on the set of scoring functions: the collection of optimal elements is defined as the set of scoring functions whose MV curve is minimum everywhere. Such optimal scoring functions are proved to coincide to strictly increasing transforms of the underlying probability density almost everywhere on the support of this underlying probability density (see Section 3 for the exact definition). In the unsupervised setting, curve analysis is shown to play a role quite comparable to that of curve analysis for supervised anomaly detection. The issue of estimating the curve of a given scoring function based on sampling data is then tackled and a smooth bootstrap method for constructing confidence regions is analyzed. A statistical methodology to build a nearly optimal scoring function is next described, which works as follows: first, a piecewise constant approximant of the optimal curve is estimated by solving a few minimum volume set estimation problems where confidence levels are chosen adaptively from the data to adjust to the variations of the optimal curve; second, a piecewise constant scoring function is built based on the sequence of estimated minimum volume sets. The curve of the scoring rule thus produced can be related to a stepwise approximant of the (unknown) optimal curve, which permits to establish the generalization ability of the algorithm through rate bounds in terms of norm in the space.

The rest of the article is structured as follows. Section 2 describes the mathematical framework, sets out the main notations and recalls the crucial notions related to anomaly/novelty detection on which the analysis carried out in the paper relies. Section 3 first provides an informal description of the anomaly scoring problem and then introduces the curve criterion, dedicated to evaluate the performance of any scoring function. The set of optimal elements is described and statistical results related to the estimation of the curve of a given scoring function are stated in Section 4. Statistical learning of an anomaly scoring function is then formulated as a functional -estimation problem in Section 5, while Section 6 is devoted to the study of a specific algorithm for the design of nearly optimal anomaly scoring functions. Technical proofs are deferred to the Appendix section.

We finally point out that a very preliminary version of this work has been presented in the conference AISTATS 2013 (see (Clémençon and Jakubowicz, 2013)). The present article gives a better characterization of the optimal scoring functions and investigates much deeper the statistical assessment of the performance of a given scoring function. In particular, it shows how to construct confidence regions for the curve of a scoring function in a computationally feasible fashion, using the (smooth) bootstrap methodology for which we state a consistency result. This consistency result gives a rate of convergence which promotes the use of a smooth bootstrap approach, rather than a naive bootstrap technique. Additionally, in Section 6, the confidence levels of the minimum volume sets to be estimated are chosen in a data-driven way (instead of considering a regular subdivision of the interval fixed in advance), giving to the statistical estimation and learning procedures proposed in this paper crucial adaptivity properties, with respect to the (unknown) shape of the optimal curve. Eventually, we give an example showing that the nature of the problem tackled here is very different than that of density estimation and we also give a simpler formula of the derivative of the optimal curve (that of the underlying density) compared to the one originally given in (Clémençon and Jakubowicz, 2013).

2 Background and Preliminaries

As a first go, we start off with describing the mathematical setup and recalling key concepts in anomaly detection involved in the subsequent analysis.

2.1 Framework and Notations

Here and throughout, we suppose that we observe independent and identically distributed realizations of an unknown continuous probability distribution , copies of a generic random variable , taking their values in a (possibly very high dimensional) feature space , with . The density of the random variable with respect to , the Lebesgue measure on , is denoted by , its support by and the indicator function of any event by . For any set , its complementary is denoted by . The sup norm of any real valued function is denoted by and the Dirac mass at any point by . The notation is used to mean boundedness in probability. The quantile function of any real valued random variable with cumulative distribution function is defined by for all . For any real valued random variable , the generalized inverse of the decreasing function is defined by for all . For any function , denotes the cumulative distribution function of the random variable . In addition, for any , denotes the quantile at level of the distribution of . We also set for all . Finally, constants in inequalities are denoted by either or and may vary at each occurrence.

A natural way of defining preorders on is to map its elements onto and use the natural order on the real half-line.

Definition 1.

(Scoring function) A scoring function is any measurable function that is integrable with respect to the Lebesgue measure.

The set of all scoring functions is denoted by and we denote the level sets of any scoring function by:

Observe that the family is decreasing (for the inclusion, as increases from to ):

and that and 111Recall that a sequence of subsets of an ensemble is said to converge if and only if . In such a case, one defines its limit, denoted by as ..

The following quantities shall also be used in the sequel. For any scoring function and threshold level , define:

The quantity is referred to as the mass of the level set , while is generally termed the volume (with respect to the Lebesgue measure).

Remark 1.

The integrability of a scoring function (see Definition 1) implies that the volumes are finite on : for any ,

Incidentally, we point out that, in the specific case , the set is the density contour cluster of the density function at level , see (Polonik, 1995) for instance. Such a set is also referred to as a density level set. Observe in addition that, using the terminology introduced in (Liu et al., 1999), is the region enclosed by the contour of depth when is a depth function.

2.2 Minimum Volume Sets

The notion of minimum volume sets has been introduced and investigated in the seminal contributions of Einmahl and Mason (1992) and Polonik (1997) in order to describe regions where a multivariate random variable takes its values with highest/smallest probability. Let , a minimum volume set of mass at least is any solution of the constrained minimization problem

| (1) |

where the minimum is taken over all measurable subsets of . Application of this concept includes in particular novelty/anomaly detection: for large values of , abnormal observations (outliers) are those which belong to the complementary set . In the continuous setting, it can be shown that there exists a threshold value equal to such that the level set is a solution of the constrained optimization problem above. The (generalized) quantile function is then defined by:

The definition of can be extended to the interval by setting and . The following assumptions shall be used in the subsequent analysis.

-

(A1)

The density is bounded: .

-

(A2)

The density has no flat parts, i.e. for any ,

Under the assumptions above, for any , there exists a unique minimum volume set (equal to up to subsets of null -measure), whose mass is equal to exactly. Additionally, the mapping is continuous on and uniformly continuous on for all (when the support of is compact, uniform continuity holds on the whole interval ).

From a statistical perspective, estimates of minimum volume sets are built by replacing the unknown probability distribution by its empirical version and restricting optimization to a collection of borelian subsets of , supposed rich enough to include all density level sets (or reasonable approximations of the latter). In (Polonik, 1997), functional limit results are derived for the generalized empirical quantile process under certain assumptions for the class (stipulating in particular that is a Glivenko-Cantelli class for ). In (Scott and Nowak, 2006), it is proposed to replace the level by where plays the role of tolerance parameter. The latter should be chosen of the same order as the supremum roughly, complexity of the class being controlled by the VC dimension or by means of the concept of Rademacher averages, so as to establish rate bounds at fixed.

Alternatively, so-termed plug-in techniques, consisting in computing first an estimate of the density and considering next level sets of the resulting estimator have been investigated in several papers, among which (Cavalier, 1997; Tsybakov, 1997; Rigollet and Vert, 2009; Cadre, 2006; Cadre et al., 2013). Such an approach however yields significant computational issues even for moderate values of the dimension, inherent to the curse of dimensionality phenomenon.

3 Ranking Anomalies

In this section, the issue of scoring observations depending on their level of novelty/abnormality is first described in an informal manner and next formulated quantitatively, as a functional optimization problem, by means of a novel concept, termed the Mass Volume curve.

3.1 Overall Objective

The problem considered in this article is to learn a scoring function , based on training data , so as to describe the extremal behavior of the (high-dimensional) random vector by that of the univariate variable , which can be summarized by its tail behavior near : hopefully, the smaller the score , the more abnormal/rare the observation should be considered. Hence, an optimal scoring function should naturally permit to rank observations by increasing order of magnitude of (see Section 3.2 for the precise definition of the set of optimal scoring functions). The preorder on induced by such an optimal scoring function could then be used to rank observations by their degree of abnormality: for any optimal scoring function , an observation is more abnormal than an observation if and only if .

3.2 A Functional Criterion: the Mass Volume Curve

We now introduce the concept of Mass Volume curve and shows that it is a natural criterion to evaluate the accuracy of decision rules in regard to anomaly scoring.

Definition 2.

(True Mass Volume curve) Let . Its Mass Volume curve ( curve in abbreviated form) with respect to the probability distribution of the random variable is the plot of the function

If the scoring function is upper bounded, exists and is defined on .

Remark 2.

(Parametric Mass Volume Curve) If is invertible, and therefore is the ordinary inverse of , the Mass Volume curve of the scoring function can also be defined as the parametric curve:

Remark 3.

(Connections to ROC/concentration analysis) We point out that the curve resembles a receiver operating characteristic (ROC) curve of the test/diagnostic function (see (Egan, 1975)), except that the distribution under the alternative hypothesis is not a probability measure but the image of Lebesgue measure on by the function , while the distribution under the null hypothesis is the probability distribution of the random variable . Hence, the curvature of the graph somehow measures the extent to which the spread of the distribution of differs from that of a uniform distribution. Observe also that, in the case where the support of coincides with the unit square , the curve of any scoring function corresponds to the concentration function introduced in (Polonik, 1999), where is the uniform probability distribution on and , to compare the concentration of with that of with respect to the class of sublevel sets of the function . Notice finally that, when is a depth function, is a scale curve, as defined in (Liu et al., 1999).

This functional criterion induces a partial order over the set of all scoring functions. Let and be two scoring functions on , the ordering provided by is better than that induced by when

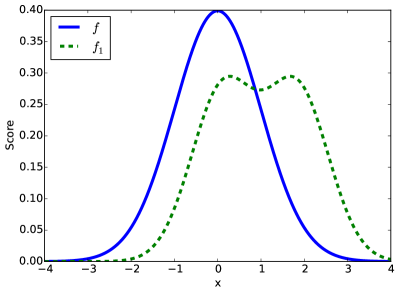

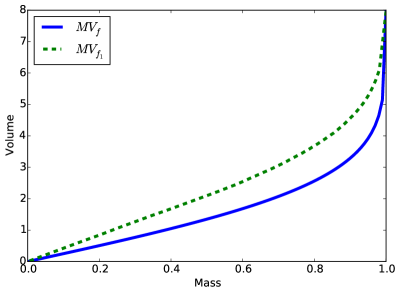

Typical curves are illustrated in Fig. 1. A desirable curve increases slowly and rises near , just like the lowest curve of Fig. 1. This corresponds to the situation where the distribution of the random variable is much concentrated around its modes and the highest values (respectively, the lowest values) taken by are located near the modes of (respectively, in the tail region of ). The curve of the scoring function is then close to the right lower corner of the Mass Volume space. We point out that, in certain situations, some parts of the MV curve may be of interest solely, corresponding to large values of when focus is on extremal observations (the tail region of the random variable ) and to small values of when modes of the underlying distribution are investigated.

We define the set of optimal scoring functions as follows. We recall here that for any set , its complementary is denoted by .

Definition 3.

The set of optimal scoring functions is the set of scoring functions such that there exist and a function such that

-

(i)

,

-

(ii)

For all , ,

-

(iii)

is strictly increasing,

-

(iv)

For -almost all , .

One can note that, as expected, the density and strictly increasing transforms of the density belong to . More generally and roughly speaking, an optimal scoring function is a strictly increasing transform of the density -almost everywhere on the support of the density. Note also that on the one hand, if , thanks to , and , we have for almost all (because up to subsets of null measure as shown in Lemma 1). Therefore -almost everywhere on . On the other hand, thanks to , for almost all and therefore -almost everywhere on . Thus the values of on are -almost everywhere lower than the values of on , where is almost everywhere a strictly increasing transform of the density .

The result below shows that optimal scoring functions are those whose curves are minimum everywhere.

Proposition 1.

From now on we will thus use to denote the curve of elements of . The proof of Proposition 1 can be found in Appendix A. Incidentally, notice that, equipped with the notations introduced in 2.2, we have for all . We also point out that bound (3) reveals that the pointwise difference between the optimal curve and that of a scoring function candidate is controlled by the error made in recovering the specific minimum volume set through .

Remark 4.

In the framework we develop, anomaly scoring boils down to recovering the decreasing collection of all level sets of the density function , , without necessarily disposing of the corresponding levels. Indeed, one may check that any scoring function of the form

| (4) |

where is an arbitrary finite positive measure dominating the Lebesgue measure on , belongs to . Observe that corresponds to the case where is chosen to be the Lebesgue measure on in Eq. (4). The anomaly scoring problem can be thus cast as an overlaid collection of minimum volume set estimation problems. This observation shall turn out to be very useful when designing practical statistical learning strategies in Section 6.

We point out that the optimal curve provides a measure of the mass concentration of the random variable : the lower the curve , the more concentrated the distribution . Indeed, the excess mass functional introduced in (Muller and Sawitzki, 1991) can be expressed as . Hence, we have for all . One may refer to (Polonik, 1995) for results related to the statistical estimation of density contour clusters and applications to multimodality testing using the excess mass functional.

Example 1.

(Univariate Gaussian distribution) Let be random variable with Gaussian distribution , we have , where is the cumulative distribution function of .

Example 2.

(Multivariate Gaussian distribution) Let be a multivariate random variable with Gaussian distribution . We assume that is a diagonal matrix and we denote by its diagonal coefficients. The density level set is exactly the set with . It is well known that , the distribution with degrees of freedom. Thus , denoting the quantile of order of the distribution. The set is exactly the ellipsoid with semi-principal axes of length . The formula of the volume of an ellipsoid gives where is the gamma function.

The following result reveals that the optimal curve is convex and provides a closed analytical form for its derivative. The proof is given in Appendix A.

Proposition 2.

The convexity of might be explained as follows: when considering density level sets with increasing probabilities , their volumes increase as well, but they increase more and more quickly since the mass of the distribution becomes less and less concentrated.

Elementary properties of curves are summarized in the following proposition.

Proposition 3.

(Properties of curves) For any , the following assertions hold true.

-

(i)

Invariance. For any strictly increasing function , we have .

-

(ii)

Monotonicity. The mapping is increasing.

Assertion may be proved using the following property of the quantile function (see e.g. Property 2.3 in (Embrechts and Hofert, 2013)): for any cumulative distribution function , any and any , if and only if . Assertion derives from the fact that the quantile function is increasing. Details are left to the reader.

4 Statistical Estimation

In practice, curves are unknown, just like the probability distribution of the random variable , and must be estimated based on the observed sample . Replacing the mass of each level set by its statistical counterpart in Definition 2 leads to define the notion of empirical curve. We set, for all ,

| (5) |

where denotes the empirical distribution of the . Notice that takes its values in the set .

Definition 4.

(Empirical curve) Let . By definition, the empirical curve of is the graph of the (piecewise constant) function

Remark 5.

(On volume estimation). Except for very specific choices of the scoring function (e.g. when is piecewise constant and the volumes of the subsets of on which is constant can be explicitly computed), no closed analytic form for the volume is available in general and Monte-Carlo procedures should be used to estimate it (which may be practically challenging in a high-dimensional setting). Computation of volumes in high dimensions is an active topic of research (Lovász and Vempala, 2006) and for simplicity, this is not taken into account in the subsequent analysis.

In order to obtain a smoothed version , a typical strategy consists in replacing the empirical distribution estimate involved in (5) by the continuous distribution with density , with where is a regularizing Parzen-Rosenblatt kernel (i.e. a bounded square integrable function such that ) and is the smoothing bandwidth (see for instance (Wand and Jones, 1994)).

4.1 Consistency and Asymptotic Normality

The theorem below reveals that, under mild assumptions, the empirical curve is a consistent and asymptotically Gaussian estimate of the curve, uniformly over any subinterval of . It involves the assumptions listed below.

-

(A3)

The scoring function is bounded: .

-

(A4)

The random variable has a continuous cumulative distribution function . Let and . The distribution function is twice differentiable on and

(6) -

(A5)

There exists such that

-

(A6)

has a limit when tends towards from the left:

-

(A7)

The mapping is of class .

Assumption (A3) implies that exists and . Note also that if is not bounded, one can always consider . Indeed takes its values in and as is strictly increasing thanks to Proposition 3. Assumptions (A4) and (A5) are common assumptions for the strong approximation of the quantile process (see for instance (Csörgő and Révész, 1978)). Condition (6) and assumption (A5) are respectively equivalent to for all and

Eventually, assumption (A6) is equivalent to: has a limit when tends towards . The density can therefore be extended by continuity to the interval . As , (6) can then be replaced by for all which also gives for all . One can also note that is thus invertible on with inverse .

In order to state part of the following theorem, we assume that the probability space is rich enough in the sense that an infinite sequence of Brownian bridges can be defined on it.

Theorem 1.

Let and . Assume that assumptions (A3)-(A7) are fulfilled. The following assertions hold true.

-

(i)

(Consistency) With probability one, we have uniformly over :

-

(ii)

(Strong approximation) There exists a sequence of Brownian bridges such that we almost surely have, uniformly over the compact interval : as ,

where

The technical proof is given in Appendix A. One can note from the proof of assertion that this assertion does not require assumption (A5) to be satisfied. The proof of assertion relies on standard strong approximation results for the quantile process (Csörgő and Révész, 1978, 1981; Csörgő, 1983). Assertion means that the fluctuation process converges in the space of càd-làg functions on equipped with the sup norm, to the law of a Gaussian stochastic process .

Remark 6.

Assumption (A6) is required in order to state the results of assertions and on the interval . However this assumption is restrictive as it implies that is discontinuous at since whereas for all . Instead of assumption (A6), if one assumes that is decreasing on an interval to the left of , then the result of assertion can be obtained on the interval with the same rate of convergence if and with the same rate of convergence up to and factors if . In this case, assertion also holds on (see for instance (Csörgő and Révész, 1978)).

4.2 Confidence Regions in the Mass Volume Space

The true curve of a given scoring function is unknown in practice and its performance must be statistically assessed based on a data sample. Beyond consistency of the empirical curve in sup norm and the asymptotic normality of the fluctuation process, we now tackle the question of constructing confidence bands in the space.

Definition 5.

Based on a sample , a (random) confidence region for the curve of a given scoring function at confidence level is any borelian set of the space (possibly depending on ) that covers the curve with probability larger than :

In practice, confidence regions shall be of the form of balls in the Skorohod’s space of càd-làg functions on with respect to the norm and with the estimate introduced in Definition 4 as center for some fixed :

Constructing confidence regions based on the approximation stated in Theorem 1 would require to know the density . Hence a bootstrap approach (Efron, 1979) should be preferred. Following in the footsteps of Silverman and Young (1987), it is recommended to implement a smoothed bootstrap procedure. The asymptotic validity of such a resampling method derives from a strong approximation result similar to the one of Theorem 1. Let be the fluctuation process defined for all by

The bootstrap approach suggests to consider, as an estimate of the law of the fluctuation process , the conditional law given the original sample of the naive bootstrapped fluctuation process

| (7) |

where, given , is the empirical curve of the scoring function based on a sample of i.i.d. random variables with distribution . The difficulty is twofold. First, the target is a distribution on a path space, namely a subspace of the Skorohod’s space equipped with the norm. Second, is a functional of the quantile process . The naive bootstrap, which consists in resampling from the raw empirical distribution , generally provides bad approximations of the distribution of empirical quantiles: the rate of convergence for a given quantile is indeed of order (Falk and Reiss, 1989) whereas the rate of the Gaussian approximation is (see (25) in Appendix A). The same phenomenon may be naturally observed for curves. In a similar manner to what is usually recommended for empirical quantiles, a smoothed version of the bootstrap algorithm shall be implemented in order to improve the approximation rate of the distribution of , namely, to resample the data from a smoothed version of the empirical distribution . We thus consider the smooth boostrapped fluctuation process

| (8) |

where, given , is the empirical curve of the scoring function based on a sample of i.i.d. random variables with distribution and where is the smooth version of the empirical curve, being the generalized inverse of . The algorithm for building a confidence band at level in the space from sampling data is described in Algorithm 1.

Before turning to the theoretical analysis of this algorithm, its description calls a few comments. From a computational perspective, the smoothed bootstrap distribution must be approximated in its turn, by means of a Monte-Carlo approximation scheme. Based on the bootstrap fluctuation processes obtained, with , the radius then coincides with the empirical quantile at level of the statistical population . Concerning the number of bootstrap replications, picking does not modify the rate of convergence. However, choosing of magnitude comparable to so that is an integer may be more appropriate: the -quantile of the approximate bootstrap distribution is then uniquely defined and this does not impact the rate of convergence neither (Hall, 1986).

4.2.1 Bootstrap consistency

The next theorem reveals the asymptotic validity of the bootstrap estimate proposed above where we assume that the smoothed version of the distribution function is computed at step 1 of Algorithm 1 using a kernel . It requires the following assumptions.

-

(B1)

The density is bounded and of class .

-

(B2)

The bandwidth decreases towards as in a way that , and .

-

(B3)

The kernel has finite support and satisfies the following conditions: , and .

-

(B4)

The kernel is such that and is of the form , being a polynomial and a bounded real function of bounded variation.

-

(B5)

The kernel is differentiable with derivative such that and of the form , being a polynomial and a bounded real function of bounded variation.

-

(B6)

The bandwidth is such that tends to 0 as .

Assumptions (B1) and (B3) are needed to control the biases and . Assumption (B2) on the bandwidth and assumption (B4) (respectively assumption (B5)) are needed to control (respectively ) thanks to the result of Giné and Guillou (2002). Assumption (B6) ensures that tends to almost surely as . Assumptions (B3)-(B5) are fulfilled, for instance, by the biweight kernel defined for all by:

| (9) |

Theorem 2.

The proof is given in Appendix A. Note that under assumption (B2) tends to as . The primary tuning parameters of Algorithm 1 concern the bandwidth . The optimal bandwidth is obtained by minimizing the term with respect to . This leads to and an approximation error of order for the bootstrap estimate (see (Stute, 1982) for details on the derivation of the optimal bandwidth). Notice that assumptions (B2) and (B6) are fulfilled by such a bandwidth.

Although the rate of the bootstrap estimate is slower than that of the Gaussian approximation, the smoothed bootstrap method remains very appealing from a computational perspective: it is indeed very difficult to build confidence bands from simulated Brownian bridges in practice. Finally, as said above, it should be noticed that a non smoothed bootstrap of the curve would lead to worse approximation rates, of the order namely, see (Falk and Reiss, 1989).

Remark 8.

In the result of Theorem 2 we consider the supremum over instead of the supremum over for several reasons. One of the reasons is that to obtain a rate of convergence for the bootstrap approximation we need to have the boundedness of the density of the supremum of the absolute value of the Gaussian process . This is almost immediate from the result of Pitt and Tran (1979) if the supremum is over (see the proof of Theorem 2 in Appendix A for more details). This is more complicated if the supremum is over . Using the result of Lifshits (1987), a closer look at the Gaussian process might lead to the boundedness of the density of the supremum of over . Another reason is that several arguments in the proof also use the fact that . However we do not have as under the assumptions of Theorem 2 is continuous on and therefore .

4.2.2 Illustrative Numerical Experiments

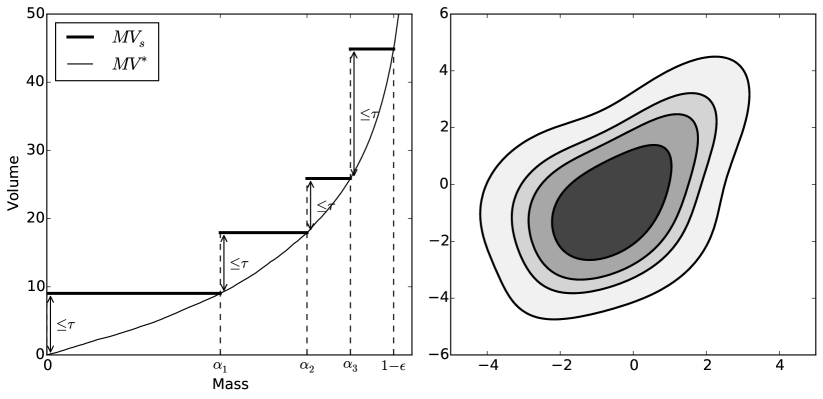

Let denote the density of a Gaussian distribution with mean and covariance . We consider a two-dimensional Gaussian mixture whose density is given by:

| (10) |

where , ,

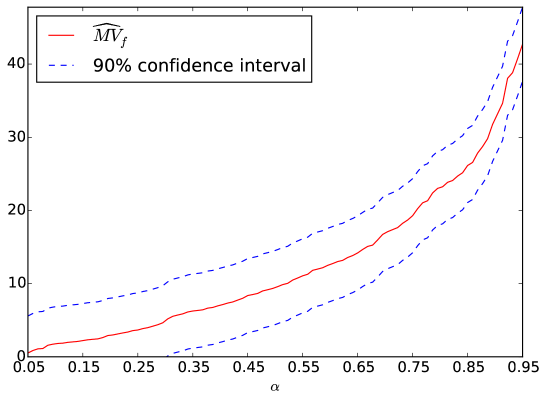

Density level sets of such a distribution are shown in Fig. 3(a). We draw a sample of size from this two-dimensional Gaussian mixture and compute . We then apply Algorithm 1 using the biweight kernel defined in (9) with a bandwidth to obtain a % confidence band. We take and bootstrap replications to approximate . All the volumes required to compute the curves are estimated using Monte-Carlo integration, drawing uniformly samples in the hypercube enclosing the data. Fig. 2 shows the % confidence curves.

In this section, statistical estimation of the true curve of a given scoring function has been investigated, as well as the problem of building confidence regions in the Mass Volume space. In all the rest of the paper, focus is on statistical learning of a nearly optimal scoring function based on a training sample with respect to the curve criterion.

5 A M-estimation Approach to Anomaly Scoring

Now we are are equipped with the concept of Mass Volume curve, the anomaly scoring task can be formulated as the building of a scoring function , based on the training set , such that is as close as possible to the optimum . Due to the functional nature of the criterion performance, there are many ways of measuring how close the curve of a scoring function candidate and the optimal one are. The -distances, for , provide a relevant collection of risk measures. Let be fixed (take if ) and consider the losses related to the -distance and that related to the sup norm:

Observe that, by virtue of Proposition 1, the ‘excess-risk’ decomposition applies in the case and the learning problem can be directly tackled through standard -estimation arguments:

Hence, possible learning techniques could be based on the minimization, over a set of candidates, of empirical counterparts of the area under the curve, such as . In contrast, the approach cannot be straightforwardly extended to the sup norm situation. A possible strategy is to combine -estimation with approximation methods so as to ‘discretize’ the functional optimization task. This strategy can be implemented as follows. First, we replace the unknown target curve by an approximation that can be described by a finite number of scalar parameters, by a piecewise constant approximant whose breakpoints are given by a subdivision precisely, and that is itself a curve, namely the curve of the piecewise constant scoring function

| (11) |

which is indeed a piecewise constant approximant of related to the meshgrid (see (12)). Then, the -risk can be decomposed as the sum of two terms

the second term on the right-hand side being viewed as the bias of the statistical method. Restricting optimization to the first term on the right-hand side of the -risk decomposition, the problem thus boils down to recovering the bilevel sets for as we obviously have

This simple observation paves the way for designing scoring strategies relying on the estimation of a finite number of minimum volume sets.

In the next section, we describe a learning algorithm for anomaly ranking, that can be viewed to a certain extent as a statistical version of an adaptive approximation method by piecewise constants introduced in (DeVore, 1987) (see also Section 3.3 in (DeVore, 1998)), to build a piecewise constant estimate of the optimal curve and a nearly optimal piecewise constant scoring function, mimicking . The subdivision is entirely learnt from the data, in order to produce accurate estimates of in an adaptive fashion: looking at Fig. 1, an ideal meshgrid should be loose where is nearly flat or grows very slowly (‘near’ ) and refined when it exhibits high degrees of variability (as one gets closer to ).

Before describing and analyzing a prototypal approach to curve optimization, a few remarks are in order.

Remark 9.

(Connections with supervised ranking) Based on the observation made in Remark 3, one may see that, in the specific case where the support of coincides with the unit square , the curve of any scoring function corresponds to the reflection about the first diagonal of the curve of when the ‘negative distribution’ is the uniform distribution on and the ‘positive distribution’ is . As shown in (Clémençon and Robbiano, 2014), this permits to turn unsupervised ranking into supervised ranking in the compact support situation and to exploit supervised ranking algorithms combined with random sampling to solve the curve minimization problem. A similar idea had been proposed in (Steinwart et al., 2005) to turn anomaly detection into supervised binary classification.

Remark 10.

(Plug-in) As the density is an optimal scoring function, a natural strategy would be to estimate first the unknown density function by means of (non-) parametric techniques and next use the resulting estimator as a scoring function. Beyond the computational difficulties one would be confronted to for large or even moderate values of the dimension, we point out that the goal pursued in this paper is by nature very different from density estimation: the local properties of the density function are useless here, only the ordering of the possible observations it induces is of importance (see Proposition 1). One may also show that a candidate can be a better approximation of the density than a candidate for the loss say, but a worse approximation for the curve criterion (see Example 3).

Example 3.

Let be the density of the truncated normal distribution with support , mean equal to 0.5 and variance equal to . Let’s consider and defined for all as

We thus have . Hence is a better approximation of with respect to the distance. However and is a better scoring function than with respect to the curve criterion. Indeed one can first show that . This thus gives . Now let , is of the form with and . The set is of the form with and . If , i.e., , then on the one hand and on the other hand almost everywhere by the uniqueness of the solution of which is impossible. Eventually, . One can also observe that in contrary to , preserves the order induced by .

6 The A-Rank Algorithm

Now that the anomaly scoring problem has been rigorously formulated, we propose a statistical method to solve it and establish learning rates for the sup norm loss.

6.1 Piecewise Constant Scoring Functions

We focus on scoring functions of the simplest form, piecewise constant functions. Let and consider a partition of the feature space in pairwise disjoint subsets of finite Lebesgue measure: and the subset . When is finite, one may suppose of finite Lebesgue measure. Then, define the piecewise constant scoring function given by:

Its piecewise constant curve is given by:

| (12) |

where , and for all . If is finite, can be defined on the whole interval .

6.2 Adaptive Approximation of the Optimal MV Curve

Using ideas developed in (DeVore, 1987) (see also Section 3.3 in (DeVore, 1998)), we propose to design an adaptive approximation scheme instead of a subdivision fixed in advance. In such a procedure, the subdivision is progressively refined by adding new breakpoints, as further information about the local variation of the target is gained: the subdivision will be coarse where the optimal is almost flat and fine where it grows rapidly.

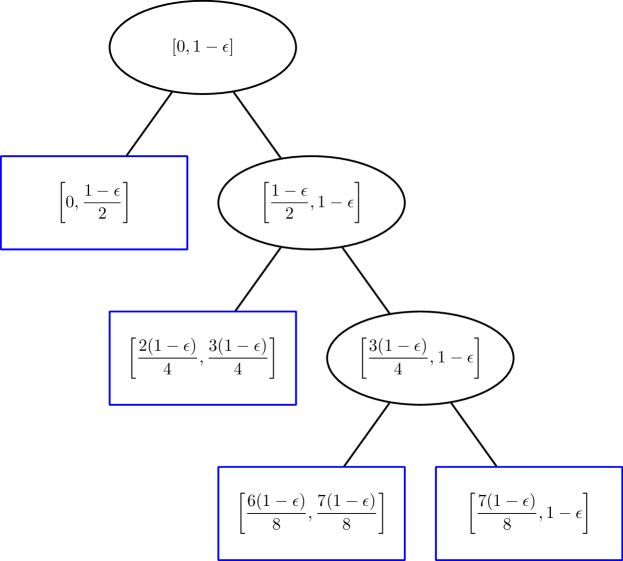

We restrict ourselves only to dyadic subdivisions with breakpoints , with and and to partitions of the interval produced by recursive dyadic partitioning: any dyadic subinterval is possibly split into two halves, producing two siblings and , depending on the local properties of the target . This adaptive estimation algorithm can be viewed as a top-down search strategy through a binary tree structure.

A binary tree is a tree where all internal nodes have exactly two children. The root of the tree represents the interval and each node of depth a subinterval . The two children resulting of a split of the node are the nodes and . A terminal node or a leaf is a node without children. In the sequel, will denote interchangeably the interval and the related node. Equipped with this flexible tree structure, define a possibly very heterogeneous subdivision of

The approximant associated with the the binary tree is given by: ,

where the sum is over all the such that is a leaf. In order to decide whether a subinterval should be split or not, we use the local error on the subinterval defined by

The local error provides a simple way of estimating the variability of the nondecreasing function on the interval . This measure is nonnegative and additive: for any siblings and of the same subinterval ,

From (DeVore, 1987), we know that controls the approximation rate of by a constant on any interval in the sense that:

where for any function , denotes the sup norm over the interval .

Given a tolerance , the general concept of the algorithm generating a binary tree and leading to its associated approximant is as follows: if , the interval is split in two siblings, otherwise is not split and becomes a leaf. If the algorithm ends we thus have:

An illustration is given in Fig. 3: Fig. 3(a) shows the piecewise constant approximant of as well as the corresponding piecewise scoring function and Fig. 3(b) shows the related binary tree.

6.3 Empirical Adaptive Estimation of the Optimal MV Curve

The adaptive approximation procedure described above can be turned itself into an adaptive estimation technique. As the optimal curve is unknown, the local error on a subinterval is estimated by its empirical counterpart

where is an estimation of the minimum volume set . Let be a class of measurable subsets of the feature space of finite Lebesgue measure and . The empirical minimum volume set related to the class and level is the solution of the optimization problem:

| (13) |

where is a penalty term related to the complexity of the class, referred to as the penalty parameter. The accuracy of the solution depends on the choices for the class and for the penalty parameter (see (Scott and Nowak, 2006)). In this paper, we do not address the issue of designing algorithms for empirical minimum volume set estimation, we refer to Section 7 of (Scott and Nowak, 2006) for a description of off-the-shelf methods documented in the literature, including partition-based techniques.

As , the empirical local error is nonnegative and additive:

for any siblings and of the same subinterval.

Splitting criterion.

The empirical local error will serve as a splitting criterion. Given a tolerance , if , the interval is split in two subintervals and . If , the interval is not split and is a leaf of the tree .

Stopping criterion.

One can observe that the estimation algorithm does not necessarily terminate for any given tolerance . Indeed, as for any , the function is a piecewise constant function with breakpoints . This follows by observing that, for any , , the solution of the empirical optimization problem (13) is . Therefore if is strictly lower than the minimum of the amplitude of the jumps of the piecewise constant function , the algorithm does not stop.

However, the fact that the function is a piecewise constant function tells us that the estimation algorithm should stop when the level is reached, where denotes the floor part function. Indeed if , the interval is such that . This either means that and belong to the same interval or that and . In the former case and . In the latter case, is equal to the amplitude of the jump of at . If this amplitude is lower than , is a leaf. If this amplitude is strictly greater than , we should normally split . However this split will not improve the error as cannot be lower than the amplitude of the jump of . We therefore add a condition to the algorithm. This ensures that the algorithm terminates while not changing the output when is greater that the maximum of the amplitudes of the jumps of . Note however that we do not necessarily have for all such that is a leaf.

The adaptive estimation method is summarized in Algorithm 2. We denote by the subdivision output by the algorithm such that the empirical piecewise constant estimator of (and of ) is given by

Its bias incorporates in particular that caused by the approximation/discretization stage inherent to the method.

6.4 The Anomaly Ranking algorithm A-Rank

The goal pursued is actually to build a scoring function whose curve is asymptotically close to the empirical estimate . In this respect, one should pay attention to the fact that is not a curve in general. Indeed, the sequence of estimated minimum volume sets sorted by increasing order of their mass , is not necessarily increasing (for the inclusion), in contrast to the true minimum level sets . This explains the monotonicity step of the following algorithm.

The A-Rank algorithm is implemented in two stages. Stage 1 consists in running Algorithm 2 to find the breakpoints and the corresponding empirical minimum volume sets . Stage 2 consists in the monotonicity step before overlaying the estimated sets. The statistical learning method is described at length in Algorithm 3.

Before analyzing the statistical performance of the A-rank algorithm, a few remarks are in order.

Notice first that we could alternatively build a monotone sequence of subsets , recursively through: and for . The results established in the sequel straightforwardly extend to this construction.

One obtains as a byproduct of the algorithm a rough piecewise constant estimator of the (optimal scoring) function , namely , the Riemann sum approximating the integral (4) when is the Lebesgue measure.

6.5 Performance Bounds for the A-Rank Algorithm

We now prove a result describing the performance of the scoring function produced by the algorithm proposed in the previous section to solve the anomaly scoring problem, as formulated in Section 5. The following assumptions are required.

-

(C1)

, .

-

(C2)

Let be a Rademacher chaos independent from the ’s. The Rademacher average given by

(14) where the expectation is over all the random variables, is such that for all , , where is a constant.

Assumption (C2) is very general, it is satisfied in particular when the class is of finite VC dimension, see (Koltchinskii, 2006). We recall here that for we have (Scott and Nowak, 2006):

| (15) |

with ,

| (16) |

Therefore assumption (C2) says that the rate of uniform convergence of true to empirical probabilities is of the order . Assumption (C1) is in contrast very restrictive, it could be however relaxed at the price of a much more technical analysis, involving the study of the bias in empirical minimum volume set estimation under adequate assumptions on the smoothness of the boundaries of the ’s, like in Tsybakov (1997) for instance (see Remark 11 below).

We state a rate of convergence for Algorithm 2. The following assumption shall be required.

-

(C3)

The function is differentiable on with derivative for all . Futhermore the derivative belongs to the space of Borel functions such that:

As explained in (DeVore, 1987), the space contains all spaces , but is strictly contained in .

Theorem 3.

The proof of this result can be found in Appendix A. Its argument essentially combines the analysis of the approximation scheme described in Section 6.2 and the generalization bounds for empirical minimum volume sets established in in (Scott and Nowak, 2006), see Theorem 3 and Lemma 19 therein. Here, the rate obtained is not proved to be optimal in the minimax sense, lower bounds will be investigated in a future work.

Corollary 1.

To derive the rate of convergence of the curve of the estimated scoring function towards we need the following assumption on the density :

-

(C4)

There exist constants and such that for all sufficiently small

This condition (stated with instead of ) was first introduced in (Polonik, 1995) and used in (Polonik, 1997) to derive rates of convergence of . It is also used in (Rigollet and Vert, 2009) to obtain fast rates for plug-in estimators of density level sets. The exponent controls the slope of the function around any level . It is related to Tsybakov’s margin assumption stated for the binary classification framework. The relation between Tsybakov’s margin assumption and the -exponent assumption is given in (Steinwart et al., 2005).

Theorem 4.

Notice that the convergence rate is always slower than . Furthermore, because of assumption (C1), the convergence rate only depends on the dimension through the parameter (refer to (Polonik, 1995) for examples of this parameter). However, assumption (C1), made here for simplicity’s sake, is very restrictive and relaxing this assumption is discussed in Remark 11.

Remark 11.

(Bias analysis) Whereas the bias resulting from the discretization of the anomaly ranking problem discussed in Section 6.2 is taken into account in the present rate bound analysis, that related to the approximation of the minimum volume sets has been neglected here for simplicity’s sake (assumption (C1)). We point out that, under smoothness assumptions on the density sublevel sets, it is possible to control such a bias term. Indeed, consider for instance the case where the boundary is of finite perimeter (note that this is the case as soon as is of bounded variation, the boundary being then by virtue of ’s continuity). In this case, if is the collection of all subsets of obtained by binding together an arbitrary number of hypercubes of side length , cartesian products of intervals of the form for , the bias term inherent to the estimation of the minimum volume set is bounded by , up to a multiplicative constant (see Proposition 9.7 in (Mallat, 1990)). Smaller bounds can be naturally established under more restrictive assumptions involving a regularity parameter of , such as its box dimension. Although the optimal choice for would then depend on , a standard fashion of nearly achieving the optimal rate of convergence is to perform model selection (see Section 4 in (Scott and Nowak, 2006)).

The general approach described above can be extended in various ways. The class over which minimum volume set estimation is performed (and the penalty parameter as well) could vary depending on the mass target . Additionally assumption (C1) could be relaxed as discussed in Remark 11. In such a case, if denotes the solution of the minimum volume set optimization problem (1) over the class , the error term could be decomposed into the sum of a stochastic error and an approximation error:

The choice of the class should then balanced the two errors. On the one hand, if the class is small, e.g. of finite VC dimension, then the stochastic error can be controlled thanks to assumption (C2) but the approximation error may be very large for some distributions. On the other hand, if the class is large, e.g. of infinite VC dimension, then the stochastic error will be very large for some distributions. A model selection approach could thus be incorporated, so as to select an adequate class (refer to Section 4 in (Scott and Nowak, 2006)).

In the present analysis, we have restricted our attention to a truncated part of the space, corresponding to mass levels in the interval and avoiding thus out-of-sample tail regions (in the case where is of infinite Lebesgue measure). An interesting direction for further research could consist in investigating the accuracy of anomaly scoring algorithms when letting slowly decay to zero as , under adequate assumptions on the asymptotic behavior of .

Finally, we emphasize that the A-Rank algorithm is prototypal, the essential objective of its description/analysis in this paper is to provide an insight into the nature of the anomaly scoring issue, viewed here as a continuum of minimum volume set estimation problems. Beyond the possible improvements mentioned above (e.g. target mass level dependent classes ), the main limitation for the practical implementation of such an approach arises from the apparent lack of minimum volume set estimation techniques that can be scaled to high-dimensional settings documented in the literature (except the dyadic recursive partitioning method considered in (Scott and Nowak, 2006), see Section 6.3 therein). However, as observed in (Steinwart et al., 2005) (see also (Clémençon and Robbiano, 2014)), supervised methods combined with sampling procedures can be used for this purpose in moderate dimensions. Refer also to Remark 9.

7 Conclusion

Motivated by a wide variety of applications including health monitoring of complex infrastructures or fraud detection for instance, we have formulated the issue of learning how to rank observations in the same order as that induced by the density function, which we called anomaly scoring here. For this problem, much less ambitious than estimation of the local values taken by the density, a functional performance criterion, the Mass Volume curve namely, is proposed. What curve analysis achieves for unsupervised anomaly detection is quite akin to what ROC curve analysis accomplishes in the supervised setting.

The statistical estimation of curves has been investigated from an asymptotic perspective and we have provided a strategy, where the feature space is overlaid with a few well-chosen empirical minimum volume sets, to build a scoring function with statistical guarantees in terms of rate of convergence for the norm in the space.

Acknowledgements

We are grateful to François Portier and Prof. Patrice Bertail for very helpful discussions. We also thank an anomymous reviewer for raising an important question which led to an improvement of Proposition 1.

Appendix A Proofs

A.1 Properties of the MV Curve

To prove Proposition 1 we need the following lemma.

Lemma 1.

The support of the density is equal to the set up to subsets of null measure, i.e.

The proof is deferred to Appendix B.

Proof of Proposition 1.

We start by proving that all elements of have the same curve equal to . One can first show that for all and all , . Let and let ,

where the second equality holds because for any and any , if and only if (see e.g. Property 2.3 in (Embrechts and Hofert, 2013)). Thanks to assertion in the definition of , for , and as , the term of the last line of the previous equation is equal to . Using the notations introduced in the definition of , the term can be decomposed as follows:

The first term is lower than (thanks to assertion in the definition of ) and is therefore equal to . We deal with the second term as follows. Let ,

The second term is lower than and is therefore equal to 0. Thanks again to assertion , the first term is equal to

where we also used assertions and . As done above for , this last term can be shown to be equal to . Therefore,

and as done above for , this can be shown to be equal to .

We now show (3) and in (2). Let , . We have,

Now let . As shown above, we have . Furthermore, and one can show that . We therefore have . As minimizes over all sets with mass at least , we have .

Finally we prove in (2). On the one hand, for we have . On the other hand, as , thanks to in (2) (which has been proven above), for all scoring function , . Therefore . We thus have on . From now on, we replace by for the sake of clarity. We thus want to prove that on implies . The proof is decomposed in three steps.

First step.

We first show that for -almost all ,

and

Let be fixed. We have . Since , by uniqueness of the solution of the minimum volume set optimization problem up to subsets of null measure, we have which is equivalent to: for -almost all

i.e. there exists such that and for all , . Note that depends on and we cannot consider to take the union over all of the because this union would not necessarily be of null measure (as we have uncountably many ). However considering the union over the rationals of is sufficient. Indeed, let denote such a union:

As it is a union over a countable set of , and for all and all ,

Let and let . We know that there exists a decreasing sequence of elements of such that converges towards when tends to infinity. Now, thanks to a property of the quantile function (see e.g. assertion (5) of Property 2.3 in (Embrechts, 2013)), we have, for all ,

Thus the sequence is decreasing (with respect to set inclusion) and

as one can show that

Similarly,

For all , (because ) and thus the two limits are equal. Hence the first result.

Now this also implies that for ,

If denotes a random variable with uniform distribution on , the left-hand side can be rewritten as

Similarly, the right-hand side is equal to and therefore for all , .

Second step.

We can now prove assertions , , and . We will first show that for almost all , there exists such that .

One may first observe that where . Indeed, (if then ) and therefore which is equal to 0 since, thanks to Lemma 1, .

Let . If is continuous at then . Now, since is increasing, has at most countably many discontinuities and each discontinuity corresponds to a jump of between two values and . We also know that this jump of corresponds to a flat part of between and . However if has a flat part between and then (recall that is continuous as has no flat parts). This gives

Thus -almost everywhere on . This implies that . Let be the union of such sets over :

and let . We have and for all , there exists such that because is continuous at (otherwise this would imply that belongs to a region corresponding to a flat part of , i.e. one of the sets ).

Similarly, we can show that there exists a set such that and for all , there exists such that . The only difference with is that we here have to consider so that .

Let . We have . Let such that and let . There exists such that . Let’s first consider the case where . We have

| (17) |

As , and . Analogously, as , and . Thus . Let’s now consider the case . We do not know that (17) still holds. However we can always assume without loss of generality that is bounded. Indeed, if is not bounded, consider the function . As is strictly increasing, thanks to Proposition 3, . Besides, as takes its values in , takes its values in and is bounded. Finally, if we show that with strictly increasing then we also have that is a strictly increasing transform of . Then as is bounded, is defined at and we can replace on by on in the proposition. We can then show that holds for .

Similarly, implies . Therefore for all ,

and hence the existence of . One can for instance take .

Third step.

Finally, assertion derives from the fact that for we have . ∎

Proof of Proposition 2.

To prove the convexity of we show that the slopes are increasing. Let be in ,

where the third equality holds because for any and any , if and only if (see e.g. Property 2.3 in (Embrechts and Hofert, 2013)). Now as , we obtain

because the distribution of is the uniform distribution on (as is continuous since has no flat parts). Similarly, one can show that . Hence, we finally have

We now prove the differentiability of and the formula of its derivative. First as is invertible on , is the ordinary inverse of on . Let and . Proceeding similarly as above we can show that

Therefore as is continuous (because is the ordinary inverse of ),

Analogously, we also have

which implies that . For , we have and proceeding as for , if ,

and

Therefore . Thus, as for all we obtain the formula of the derivative of . ∎

A.2 Statistical Estimation of the MV curve

A.2.1 Strong approximation: proof of Theorem 1

To prove Theorem 1 we need the following lemma.

Lemma 2.

Proof of Lemma 2.

Let for all . As is continuous, the random variables are i.i.d. with uniform distribution on . Their empirical cumulative distribution function is given by for all . Furthermore we have for all , . We also define . Let denote the uniform empirical process defined for all by and denote the uniform empirical quantile process defined for all by . Applying the Dvoretzky-Kiefer-Wolfowitz (DKW) inequality (Massart, 1990) gives for all and all ,

| (18) |

As for all in the sample space (see equation (1.4.5) in (Csörgő, 1983)), the DKW inequality (18) holds when replacing by . Taking , we obtain for all ,

| (19) |

As , by the Borel-Cantelli lemma, we almost surely have for large enough,

| (20) |

Using the mean value theorem we can write for ,

where is between and . As is increasing we have for all , . From (20) we know that there exists a constant such that we almost surely have for large enough, . Therefore, almost surely and for large enough,

Note that the last infimum is strictly positive because as is continuous, the infimum is reached at a point and as on (assumptions (A4) and (A6)), .

This eventually leads to: almost surely and for large enough,

∎

Proof of assertion of Theorem 1.

Proof.

Assume that assumptions (A3)-(A4) and (A6)-(A7) are fulfilled. Using the mean value theorem we can write for all

where is between and . Therefore,

Now for all , and belong to the support of , i.e., . This is true for because it is equal to one of the , . Thus . As is continuous, we have

and

From Lemma 2 we know that there exists a constant such that we almost surely have for large enough,

Therefore converges almost surely to and so is . ∎

Proof of assertion of Theorem 1.

Proof.

For all , let . Assume that assumptions (A3)-(A7) are fulfilled. By virtue of Theorem 3.1.2 in (Csörgő, 1983), there exists a sequence of Brownian bridges such that, we almost surely have:

| (21) |

where is the uniform quantile process as defined in the proof of Lemma 2. From (3.3) of Theorem 3 in (Csörgő and Révész, 1978), we also have almost surely, for large enough,

where and . Hence for large enough we have and therefore we almost surely have

| (22) |

Now from the proof of theorem 3.2.1 in (Csörgő, 1983), we also almost surely have,

| (23) |

Combining (21), (22) and (23), we almost surely have:

As one can show that and for all we almost surely have

With the change of variable this leads to

where is the sequence of stochastic processes defined by . Notice that for all , is a Brownian Bridge as it has the same distribution as . Thus there exists a constant independent of such that almost surely for large enough and for all ,

Hence, dividing by which is strictly positive for all (assumptions (A4) and (A6)), we almost surely have, for large enough and for all ,

| (24) |

where is strictly positive by the same argument as the one given in the proof of Lemma 2. Now using a Taylor expansion of which is of class (assumption (A7)) we can write for all :

where is the remainder of the Taylor expansion, being between and . We thus have

For the first term we almost surely have, for all and for large enough,

For all , . As is continuous, is bounded by .

We treat the second term as follows. For all , and are in . Therefore and as is continuous, is bounded by . Thus,

where the last inequality holds almost surely and for large enough and where is the constant of Lemma 2.

Eventually, combining the bounds on and we almost surely have

This concludes the proof. ∎

A.2.2 Bootstrap consistency: Proof of Theorem 2

Recall that for all , and . Let and be respectively defined for all as and .

Sketch of proof.

The argument is based on a strong approximation type inequality for (see Lemma 3) and (see Lemma 4). These inequalities can then be used to obtain a result on the rate of convergence of the cumulative distribution function of (respectively, the conditional cumulative distribution function of ) towards the supremum of a Gaussian process which depends on (respectively the smoothed empirical version of ). We finally obtain the result using the rate of the strong uniform convergence of towards on (see Lemma 5). The technical proofs of Lemma 3, Lemma 4 and Lemma 5 are deferred to Appendix B for the sake of clarity of the proof of the main result.

We first need the following strong approximation result.

Lemma 3.

Let . There exists a positive constant such that

We also need the counterpart of Lemma 3 conditionally on the data set .

Lemma 4.

Eventually, to control the distance between the distribution of and the conditional distribution of we need the following lemma.

Lemma 5.

We can now proof the main result.

Proof of Theorem 2.

Therefore using a result of Sargan and Mikhail (1971), we have for all ,

and

where denotes the density of and where for the first equality we use the fact that for all the random variable is equal in distribution to and for the last inequality the result from (Pitt and Tran, 1979) stating that has a density bounded by a constant as the supremum of a Gaussian process such that for all , and . Indeed, as is a Brownian bridge it is almost surely continuous on and as is continuous on , is almost surely continuous on and therefore almost surely . Furthermore, is continuous and thanks to Lemma 10, for all , . Therefore is attained and is strictly positive.

Therefore,

| (25) |

Reasoning similarly as above, thanks to the result of Lemma 4, there exists a constant such that, -almost surely, as ,

Therefore using the result of (Sargan and Mikhail, 1971), we -almost surely have, for all ,

We now need the following result.

Lemma 6.

The exists a constant such that we -almost surely have for large enough,

Proof of Lemma 6.

Let . If both probabilities are equal to 0 as the two random variables involved are positive. Hence we have (for all in the sample space)

| (26) |

Let . Thanks to Lemma 5 there exists a constant independent of such that we almost surely have for large enough:

| (27) |

Furthermore, we can assume, given large enough, that there exists a constant such that as tends towards . Observe that

and decompose the last term as follows

| (28) | ||||

where the event is defined as

and its complementary is given by

The first term of (28) is lower than

where the last equality stands from the fact that the law of conditionally on is equal to the law of . The second term of (28) is lower than

which is -almost surely equal to thanks to (27). Note that the fact that this holds -almost surely is independent of . Therefore we -almost surely have: for all ,

where we use a Taylor expansion and where is between and .

For large enough, we have . On the one hand this gives and, as , . Therefore, as is between and , we have in fact, . Thus . On the other hand, we also have . This eventually gives -almost surely, for all ,

| (29) |

A lower bound can be obtained in a similar fashion: -almost surely, for all ,

| (30) |

Combining the two inequalities (29) and (30) we obtain that there exists a constant such that we -almost surely have

Let be the density of the Gaussian distribution . Using a remark in the paper of (Tsirel’son, 1976, p. 854), there exists such that for all ,

| (31) |

where is such that , is arbitrary and only depends on , and the cumulative distribution function of the Gaussian distribution . Now the function is bounded on as it is continuous and tends towards when tends to . Therefore from (31) we have that . And as from (Pitt and Tran, 1979) is bounded on , so is on . Eventually, and there exists a constant such that -almost surely,

| (32) |

From Lemma 6, we -almost surely have

and thus

Finally combining this last inequality with (25) we obtain the result of the theorem.

∎

A.3 A-Rank Algorithm

A.3.1 Proof of Theorem 3

The proof follows closely the one of theorem 2 in (Clémençon and Vayatis, 2009). For clarity, we start off with recalling the following result.

Proposition 4.

The major part of this result is given by Theorem 3 and Lemma 19 in (Scott and Nowak, 2006). Although they prove the result for a given , it can be extended to all . The upper bound on can be obtained with the following reasoning. Suppose that we have , then and because minimizes over all measurable sets such that . The upper bound on the volume gives , thus . Hence also minimizes over all measurable sets such that and by uniqueness of the solution under assumptions (A1) and (A2), we have which contradicts .

We now prove the following lemma quantifying the uniform deviation of the empirical local error from the true local error over all dyadic scales.

Lemma 7.

Proof.

Let , ,

From proposition 4, with probability at least we have: for all ,

therefore with probability at least , for all , ,

and the result follows. ∎

From Lemma 7, with probability at least , for all , ,

| (34) |

Let be the piecewise constant approximant of the optimal curve built from the same recursive strategy as the one implemented in Algorithm 2 but based on the true local error and without the condition , denoting the associated meshgrid. We thus have, for every :

We also use the notation to denote the function defined for all as

where we recall that is the meshgrid obtained in Algorithm 2 implemented with the empirical error estimate .

Choosing , we obtain that with probability at least , the meshgrid is finer than where , and coarser than where . Indeed, thanks to (34), implies that with probability , . It also implies that . Indeed, if , then is such that which gives, using the mean value theorem, which contradicts . Therefore with probability at least , splitting for the true local error and a tolerance implies splitting in Algorithm 2. Analogously, implies, thanks to (34), that with probability at least , . Therefore with probability at least , splitting in Algorithm 2 implies splitting for the true local error and a tolerance .

We now use the following bound

The second term is bounded by with probability at least because with probability at least the meshgrid is finer than and therefore

On the same event, for the first term we have,

Thus we finally have

For the second part of the theorem on the cardinality of the meshgrid obtained with Algorithm 2 we use the following lemma (DeVore, 1998).

Lemma 8.

Applying this lemma to we obtain that the number of terminal nodes of is such that

As is coarser than with probability at least , the number of terminal nodes of the former is bounded by the number of terminal nodes of the latter with probability at least .

A.3.2 Proof of Theorem 4

We use the following notation: . We first prove a lemma quantifying the loss coming from the monotonicity step of Algorithm 3.

Lemma 9.

Proof.

First, from proposition 4, we have with probability at least , ,

| (37) |

For , we have and thus and the inequalities of the Lemma are trivially satisfied. For , we have and with (37) the inequalities of the Lemma are satisfied. For all ,

and . The same argument gives

We show how to obtain the upper bound for the case . We have and

Now,

where the last inclusion comes from the fact that . Hence,

and thus

Using assumption (C4), for any , if denotes the solution of the optimization problem (13), we can as in Polonik (1997) (see proof of Lemma 3.2) bound : with probability at least ,

Minimizing the right-hand side with respect to gives

where is a constant depending only on , and . We thus finally have, with probability at least ,

and therefore,

For , we can obtain in a similar fashion,

and derive the following result: with probability at least , for all ,

For (36), first note that for all , where depends only on and . Therefore the same procedure leads to: with probability , for all ,

∎

We can now prove Theorem 4. We first write

Taking , and using the same argument as in the proof of Theorem 3, the second term of the right-hand side is bounded by . We now deal with the first term. Let ,

But one can observe that

to obtain

Now is increasing, therefore on , and

We thus have

The first term is equal to and thanks to Lemma 9 we have with probability at least

| (38) |

For the second term we write

where is such that . We bound by

We bound the first term as follows. Let . If the depth has been reached, . Therefore the mean value theorem gives:

Otherwise, this means that and we decompose into

Using Lemma 9, the right-hand side is bounded by . Eventually,

Using the mean value theorem and Lemma 9, the second term can be bounded by

As and as is increasing, the third term is bounded by which is also bounded as the first term by . We thus obtain

and combining this inequality with (38), we have

Eventually, with probability at least ,

| (39) | ||||

Using the same argument as in the proof of Theorem 3, on the same event, which holds with probability at least , is coarser than where and therefore is of the order of . Using assumption (C2), for large enough, . Therefore the right-hand side of (39) is of the order of:

Choosing to balance the two terms of this expression, we finally obtain that with probability at least ,

Appendix B Technical results

This section contains the proofs of technical results that have been postponed for the sake of clarity.

B.1 Proof of Lemma 1

Proof.

We recall here that and . If then thus and . Therefore we have to prove . Let’s assume and let . The intersection is not empty. Otherwise we would have . Therefore there exists and we have as . We also have . Indeed, is in the closure of and therefore there exists a sequence of elements of which converges towards as tends to infinity. Thus for all and as is continuous, , i.e.

This implies that is equal to 0 -almost everywhere on . However, if then, by definition of , . Therefore and as and on , contains a subset of non null -measure on which . This is a contradiction with the fact that is equal to 0 -almost everywhere on and thus , which is equivalent to . ∎

B.2 Proof of Lemma 3

Proof of Lemma 3.

The proof is based on Remark 3.2.4 in (Csörgő, 1983). Let denote the quantile process defined for all by

Using the mean value theorem we can write for all ,

where is between and and where is defined as in the proof of Lemma 2. Let be the uniform quantile process defined in Lemma 2. For all , .

Now we know from Theorem 1 in (Csörgő and Révész, 1978) that for all and for all ,

| (40) |

where and are positive absolute constants and where is the same sequence of Brownian Bridges as the one of the proof of assertion of Theorem 1. For all , we can write

| (41) |

Using a Taylor expansion of as in the proof of part of Theorem 1 we have for all ,

where is between and . With the change of variable , we obtain for all that is between and and that

and therefore

| (42) |

To bound the right-hand side of the previous inequality we need the following results. From the DKW inequality (see proof of Lemma 2) we have for all and for all ,

| (43) |

From Theorem 1.5.1 in (Csörgő, 1983) we have for all and for all ,

| (44) | ||||

where for all , and where denotes the floor part function. Finally from the proof of Theorem 1.4.3 in (Csörgő, 1983) we have for all and for all ,

| (45) | ||||

Let and be positive and let . We consider the four following events:

Let where denotes the complement of a set . We first deal with the first term of the right-hand side of (42). From (41) we have for all ,

where the second inequality holds because . Now for all , . As is continuous . Furthermore, for all , where the infimum is strictly positive. Therefore for all ,

We now deal with the second term of the right-hand side of (42). For all , and are in . Therefore and as is continuous, . Now, as in the proof of Lemma 2, using the mean value theorem we can write for ,

where is the one of (41). As and bounding by as previously we obtain

We eventually have