A Semismooth Newton Method for Fast, Generic Convex Programming

Abstract

We introduce Newton-ADMM, a method for fast conic optimization. The basic idea is to view the residuals of consecutive iterates generated by the alternating direction method of multipliers (ADMM) as a set of fixed point equations, and then use a nonsmooth Newton method to find a solution; we apply the basic idea to the Splitting Cone Solver (SCS), a state-of-the-art method for solving generic conic optimization problems. We demonstrate theoretically, by extending the theory of semismooth operators, that Newton-ADMM converges rapidly (i.e., quadratically) to a solution; empirically, Newton-ADMM is significantly faster than SCS on a number of problems. The method also has essentially no tuning parameters, generates certificates of primal or dual infeasibility, when appropriate, and can be specialized to solve specific convex problems.

1 Introduction and related work

Conic optimization problems (or cone programs) are convex optimization problems of the form

| (1) |

where are problem data, specified by the user, and is a proper cone (Nesterov and Nemirovskii, 1994; Ben-Tal and Nemirovski, 2001; Boyd and Vandenberghe, 2004); we give a formal treatment of proper cones in Section 2, but a simple example of a proper cone, for now, is the nonnegative orthant, i.e., the set of all points in with nonnegative components. These problems are quite general, encapsulating a number of standard problem classes: e.g., taking as the nonnegative orthant yields a linear program; taking as the positive semidefinite cone, i.e., the space of positive semidefinite matrices , yields a semidefinite program; and taking as the second-order (or Lorentz) cone yields a second-order cone program (a quadratic program is a special case).

Due, in part, to their generality, cone programs have been the focus of much recent work, and additionally form the basis of many convex optimization modeling frameworks, e.g., sdpsol (Wu and Boyd, 2000), YALMIP (Lofberg, 2005), and the CVX family of frameworks (Grant, 2004; Diamond and Boyd, 2016; Udell et al., 2014). These frameworks generally make it easy to quickly solve small and medium-sized convex optimization problems to high accuracy; they work by allowing the user to specify a generic convex optimization problem in a way that resembles its mathematical representation, then convert the problem into a form similar to (1), and finally solve the problem. Primal-dual interior point methods, e.g., SeDuMi (Sturm, 2002), SDPT3 (Toh et al., 2012), and CVXOPT (Andersen et al., 2011), are common for solving these cone programs. These methods are useful, as they generally converge to high accuracy in just tens of iterations, but they solve a Newton system on each iteration, and so have difficulty scaling to high-dimensional (i.e., large-) problems.

In recent work, O’Donoghue et al. (2016) use the alternating direction method of multipliers (ADMM) (Boyd et al., 2011) to solve generic cone programs; operator splitting methods (e.g., ADMM, Peaceman-Rachford splitting (Peaceman and Rachford, 1955), Douglas-Rachford splitting (Douglas and Rachford, 1956), and dual decomposition) generally converge to modest accuracy in just a few iterations, so the approach (called the splitting conic solver, or SCS) is scalable, and also has a number of other benefits, e.g., provding certificates of primal or dual infeasibility.

In this paper, we introduce a new method (called “Newton-ADMM”) for solving large-scale, generic cone programs rapidly to high accuracy. The basic idea is to view the usual ADMM recurrence relation as a fixed point iteration, and then use a truncated, nonsmooth Newton method to find a fixed point; to justify the approach, we extend the theory of semismooth operators, coming out of the applied mathematics literature over the last two decades (Mifflin, 1977; Qi and Sun, 1993; Martínez and Qi, 1995; Facchinei et al., 1996), although it has received little attention from the machine learning community (Ferris and Munson, 2004). We apply the approach to the fixed point iteration associated with SCS, to obtain a general purpose conic optimizer. We show, under regularity conditions, that Newton-ADMM is quadratically convergent; empirically, Newton-ADMM is significantly faster than SCS, on a number of problems. Also, Newton-ADMM has essentially no tuning parameters, and generates certificates of infeasibility, helpful in diagnosing problem misspecification.

The rest of the paper is organized as follows. In Section 2, we give the background on cone programs, SCS, and semismooth operators, required to derive our method for solving generic cone programs, Newton-ADMM. . In Section 3, we present Newton-ADMM, and establish some of its basic properties. In Section 4, we give various convergence guarantees. In Section 5, we empirically evaluate Newton-ADMM, and describe an extension as a specialized solver. We conclude with a discussion in Section 6.

2 Background

We first give some background on cones. Using this background, we go on to describe SCS, the cone program solver of O’Donoghue et al. (2016), in more detail. Finally, we give an overview of semismoothness (Mifflin, 1977), a generalization of smoothness, central to our Newton method.

2.1 Cone programming

We say that a set is a cone if, for all , and , we get that . The dual cone , associated with the cone , is defined as the set . Additionally, a cone is a convex cone if, for all , and , we get that . A cone is a proper cone if it is (i) convex; (ii) closed; (iii) solid, i.e., its interior is nonempty; and (iv) pointed, i.e., if both , then we get that .

The nonnegative orthant, second-order cone, and positive semidefinite cone are all proper cones (Boyd and Vandenberghe, 2004, Section 2.4.1); these cones, along with the exponential cone (defined below), can be used to represent most convex optimization problems encountered in practice. The exponential cone (see, e.g., Serrano (2015)), , is a three-dimensional proper cone, defined as the closure of the epigraph of the perspective of , with :

Cone programs resembling (1) were first described by Nesterov and Nemirovskii (1994, page 67), although special cases were, of course, considered earlier. Standard references include Ben-Tal and Nemirovski (2001) and Boyd and Vandenberghe (2004, Section 4.6.1).

2.2 SCS

Roughly speaking, SCS is an application of ADMM to a particular feasibility problem arising from the Karush-Kuhn-Tucker (KKT) optimality conditions associated with a cone program. To see this, consider a reformulation of the cone program (1), with slack variable :

| (2) |

The KKT conditions can be seen, after introducing dual variables , for the implicit constraint and the explicit constraints, respectively, to be

| (stationarity) | |||

| (primal feasibility) | |||

| (dual feasibility) | |||

where is the dual cone of ; thus, we can obtain a solution to (2), by solving the KKT system

| (14) |

Self-dual homogeneous embedding.

When the cone program (2) is primal/dual infeasible, there is no solution to the KKT system (14); so, consider embedding the system (14) in a larger system, with new variables , and solving

| (24) |

which is always solvable. The embedding (24), due to Ye et al. (1994), has a number of other nice properties. Observe that when are solutions to the embedding (24), we recover the KKT system (14); it turns out that the solutions characterize the primal or dual (in)feasibility of the cone program (2). In particular, if , then the cone program (2) is feasible, with a primal-dual solution ; on the other hand, if , then (2) is primal or dual infeasible (or both), depending on the exact values of (O’Donoghue et al., 2016, Section 2.3). The embedding (24) can also be seen as first-order homogeneous, in the sense that being a solution to (24) implies that , for , is also a solution. Finally, viewing the embedding (24) as a feasibility problem, the dual of the feasibility problem turns out to be the original feasibility problem, i.e., the embedding is self-dual.

ADMM-based algorithm.

As mentioned, the embedding (24) can be viewed as the feasibility problem

where we write ,

| (34) |

Introducing new variables , where , and rewriting so that we may apply ADMM, we get:

where and are the indicator functions of the product space , and the affine space of solutions to , respectively; after simplifying (see O’Donoghue et al. (2016, Section 3)), the ADMM recurrences are just

| (35) | ||||

| (36) | ||||

| (37) |

where denotes the projection onto . For the update (35), is a skew-symmetric matrix, hence is nonsingular, so the update can be done efficiently via the Schur complement, matrix inversion lemma, and factorization.

Projections onto dual cones.

For the update (36), the projection onto boils down to separate projections onto the “free” cone , the dual cone of , and the nonnegative orthant . These projections, for many , are well-known:

-

•

Free cone. Here, , for .

-

•

Nonnegative orthant, . The projection onto is simply given by applying the positive part operator:

(38) -

•

Second-order cone, . Write . Then the projection is

(39) -

•

Positive semidefinite cone, . The projection is

(40) where is the eigenvalue decomposition of .

-

•

Exponential cone, . If , then . If , then . If , i.e., the first two components of are negative, then . Otherwise, the projection is given by

(41) which can be computed using a Newton method (Parikh and Boyd, 2014, Section 6.3.4).

The nonnegative orthant, second-order cone, and positive semidefinite cone are all self-dual, so projecting onto these cones is equivalent to projecting onto their dual cones; to project onto the dual of the exponential cone, we use the Moreau decomposition to get

| (42) |

2.3 Semismooth operators

Here, we give an overview of semismoothness; good references include Ulbrich (2011) and Izmailov and Solodov (2014). We consider maps that are locally Lipschitz, i.e., for all , and , where is a ball centered at with radius , there exists some , such that . By a result known as Rademacher’s theorem (Evans and Gariepy, 2015, Section 3.1.2, Theorem 2), we get that is differentiable almost everywhere; we let denote the points at which is differentiable, so that is a set of measure zero.

The generalized Jacobian.

Clarke (1990) suggested the generalized Jacobian as a way to define the derivative of a locally Lipschitz map , at all points. The generalized Jacobian is related to the subgradient, as well as the directional derivative, as we discuss later on; the generalized Jacobian, though, turns out to be quite useful for defining effective nonsmooth Newton methods. The generalized Jacobian at a point of a map , is defined as ( denotes convex hull)

| (43) |

where is the usual Jacobian of at . Two useful properties of the generalized Jacobian (Clarke, 1990, Proposition 1.2): (i) , at any , is always nonempty; and (ii) if each component is convex, then the th row of any element of is just a subgradient of at .

(Strong) semismoothness and consequences.

We say that a map is semismooth if it is locally Lipschitz, and if, for all , the limit

| (44) |

exists (see, e.g., Mifflin (1977, Definition 1) and Qi and Sun (1993, Section 2)). The above definition is somewhat opaque, so various works have provided an alternative characterization of semismoothness: is semismooth if and only if it is (i) locally Lipschitz; (ii) directionally differentiable, in every direction; and (iii) we get

i.e., (see, e.g., Qi and Sun (1993, Theorem 2.3), Hintermüller (2010, Theorem 2.9), Qi and Sun (1999, page 2), and Martínez and Qi (1995, Proposition 2)). Examples of semismooth functions include , all convex functions, and all smooth functions (Mifflin, 1977; Śmietański, 2007); on the other hand, is not semismooth. A linear combination of semismooth functions is semismooth (Izmailov and Solodov, 2014, Proposition 1.75). Finally, we say that a map is strongly semismooth if, under the same conditions as above, we can replace (44) with

i.e., (see Facchinei et al. (1996, Proposition 2.3) and Facchinei and Kanzow (1997, Definition 1)).

3 Newton-ADMM and its basic properties

Next, we describe Newton-ADMM, our nonsmooth Newton method for generic convex programming; again, the basic idea is to view the ADMM recurrences (35) – (37), used by SCS, as a fixed point iteration, and then use a nonsmooth Newton method to find a fixed point. Accordingly, we let

which are just the residuals of the consecutive ADMM iterates given by (35) – (37), and ; multiplying by to change coordinates gives

| (48) |

Now, we would like to apply a Newton method to , but projections onto proper cones are not differentiable, in general. However, for many cones of interest, they are (strongly) semismooth; the following lemma summarizes.

Lemma 3.1.

Additionally, we give the following new result, for the exponential cone, which may be of independent interest.

Lemma 3.2.

The projection onto the exponential cone is semismooth.

We defer all proofs to the supplement.

Putting the pieces together, the following lemma establishes that , defined in (48), is (strongly) semismooth.

Lemma 3.3.

The preceding results lay the groundwork for us to use a semismooth Newton method (Qi and Sun, 1993), applied to , where we replace the usual Jacobian with any element of the generalized Jacobian (43); however, as many have observed (Khan and Barton, 2017), it is not always straightforward to compute an element of the generalized Jacobian. Fortunately, for us, we can just compute a subgradient of each row of , as the following lemma establishes.

Lemma 3.4.

The th row of each element of the generalized Jacobian at of the map is just a subgradient of , at .

Using the lemma, an element of the generalized Jacobian of the map is then just

| (49) |

where

| (50) |

is a -dimensional matrix forming the second row of ; equals 1 if and 0 otherwise; and is the Jacobian of the projection onto the dual cone . Here and below, we use subscripts to select components, e.g., selects the -component of from (34), and we write to mean , where .

3.1 Final algorithm

Later, we discuss computing , the Jacobian of the projection onto the dual cone , for various cones ; these pieces let us compute an element , given in (49) – (50), of the generalized Jacobian of the map , defined in (48), which we use instead of the usual Jacobian, in a semismooth Newton method; below, we describe a way to scale the method to larger problems (i.e., values of ).

Truncated, semismooth Newton method.

The conjugate gradient method is, seemingly, an appropriate choice here, as it only approximately solves the Newton system

| (51) |

with variable ; unfortunately, in our case, is nonsymmetric, so we appeal instead to the generalized minimum residual method (GMRES) (Saad and Schultz, 1986). We run GMRES until

| (52) |

where is the approximate solution from a particular iteration of GMRES, and is a user-defined tolerance; i.e., we run GMRES until the approximation error is acceptable. After GMRES computes an approximate Newton step, we use backtracking line search to compute a step size.

Now recall, from Section 2, that is always a trivial solution to the Newton system (51), due to homogeneity; so, we initialize the -components of to 1, which avoids converging to the trivial solution. Finally, we mention that when , in the cone program (1), is the direct product of several proper cones, then , in (50), simply consists of multiple such matrices, just stacked vertically.

We describe the entire method in Algorithm 1. The method has essentially no tuning parameters, since, for all the experiments, we just fix the maximum number of Newton iterations ; the backtracking line search parameters ; and the GMRES tolerances , for each Newton iteration . The cost of each Newton iteration is the number of backtracking line search iterations times the sum of two costs: the cost of projecting onto a dual cone and the cost of GMRES, i.e., , assuming GMRES returns early. Similarly, the cost of each ADMM iteration of SCS is the cost of projecting onto a dual cone plus .

3.2 Jacobians of projections onto dual cones

Here, we derive the Jacobians of projections onto the dual cones of the nonnegative orthant, second-order cone, positive semidefinite cone, and the exponential cone; here, we write to mean , where .

Nonnegative orthant.

Since the nonnegative orthant is self-dual, we can simply find a subgradient of each component in (38), to get that is diagonal with, say, set to 1 if and 0 otherwise, for .

Second-order cone.

Write . The second-order cone is self-dual, as well, so we can find subgradients of (39), to get that

| (53) |

where is a low-rank matrix (details in the supplement).

Positive semidefinite cone.

The projection map onto the (self-dual) positive semidefinite cone is matrix-valued, so computing the Jacobian is more involved. We leverage the fact that most implementations of GMRES need only the product , provided by the below lemma using matrix differentials (Magnus and Neudecker, 1995); here, is the vectorization of a real, symmetric matrix .

Lemma 3.5.

Let be the eigenvalue decomposition of , and let be a real, symmetric matrix. Then

where, here, the is interpreted diagonally;

denotes the pseudo-inverse of ; and is the indicator function of the nonnegative orthant.

Exponential cone.

Recall, from (41), that the projection onto the exponential cone is not analytic, so computing the Jacobian is much more involved, as well. The following lemma provides a Newton method for computing the Jacobian, using the KKT conditions for (41) and differentials.

Lemma 3.6.

Let . Then , where

otherwise, is a particular 3x3 matrix given in the supplement, due to space constraints.

4 Convergence guarantees

Here, we give some convergence results for Newton-ADMM, the method presented in Algorithm 1.

First, we show that, under standard regularity assumptions, the iterates generated by Algorithm 1 are globally convergent, i.e., given some initial point, the iterates converge to a solution of , where is a Newton iteration counter. We break the statement (and proof) of the result up into two cases. Theorem 4.1 establishes the result, when the sequence of step sizes converges to some number bounded away from zero and one. Theorem 4.2 establishes the result when the step sizes converge zero.

Below, we state our regularity conditions, which are similar to those given in Han et al. (1992); Martínez and Qi (1995); Facchinei et al. (1996); we elaborate in the supplement.

-

A1.

For Theorem 4.1, we assume .

-

A2.

For Theorem 4.2, we assume .

-

A3.

For Theorem 4.2, we assume (i) that the GMRES approximation tolerances are uniformly bounded by as in , (ii) that , and (iii) that .

-

A4.

For Theorem 4.2, we assume, for every convergent sequence , satisfying assumption (A2) above, and , that

where, for notational convenience, we write

-

A5.

For Theorem 4.2, we assume, for all and , and for some , that

-

A6.

For Theorem 4.3, we assume, for all , (i) that , for some constant ; and (ii) that every element of is invertible.

The two global convergence results are given below; the proofs are based on arguments in Martínez and Qi (1995, Theorem 5a), but we use fewer user-defined parameters, and a different line search method.

Theorem 4.1 (Global convergence, with , for some ).

Assume condition (A1) stated above. Then .

Theorem 4.2 (Global convergence, with ).

Assume conditions (A2), (A3), (A4), and (A5) stated above. Suppose the sequence converges to some . Then .

Next, we show, in Theorem 4.3, that when is strongly semismooth, i.e., is the nonnegative orthant, second-order cone, or positive semidefinite cone, the iterates generated by Algorithm 1 are locally quadratically convergent; the proof is similar to that of Facchinei et al. (1996, Theorem 3.2b), for semismooth maps.

Theorem 4.3 (Local quadratic convergence).

Assume condition (A6) stated above. Then the sequence of iterates generated by Algorithm 1 converges quadratically, with , for large enough .

5 Numerical examples

Next, we present an empirical evaluation of Newton-ADMM, on several problems; in these, we directly compare to SCS, which Newton-ADMM builds on, as it is the most relevant benchmark for us (O’Donoghue et al. (2016) observe that, with an optimized implementation, SCS outperforms SeDuMi, as well as SDPT3). We evaluate, for both methods, the time taken to reach the solution as well as the optimal objective value; we obtained these by running an interior point method (Andersen et al., 2011) to high accuracy. Table 1 describes the problem sizes, for both the cone form of (1), as well as the familiar form that the problem is usually written in. Later, we also describe extending Newton-ADMM to accelerate any ADMM-based algorithm, applied to any convex problem; here, we compare to state-of-the-art baselines for specific problems.

| Problem | Cones | ||||

|---|---|---|---|---|---|

| Linear prog. | 600 | 1,200 | 600 | 300 | |

| Portfolio opt. | 2,501 | 2,504 | 2,500 | – | |

| Logistic reg. | 3,200 | 7,200 | 100 | 1,000 | |

| Robust PCA | 4,376 | 8,103 | 25 | 25 |

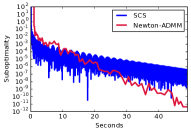

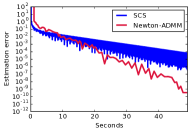

5.1 Random linear programs (LPs)

We compare Newton-ADMM and SCS on a linear program

where are problem data, and the inequality is interpreted elementwise. To ensure primal feasibility, we generated a solution by sampling its entries from a normal distribution, then projecting onto the nonnegative orthant; we generated (with , so is wide) by sampling entries from a normal distribution, then taking . To ensure dual feasibility, we generated dual solutions , associated with the equality and inequality constraints, by sampling their entries from a normal and distribution, respectively; to ensure complementary slackness, we set . Finally, to put the linear program into the cone form of (1), and hence (2), we just take

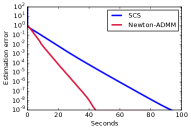

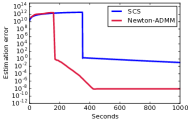

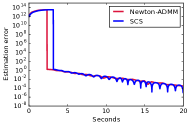

The first column of Figure 1 presents the time taken, by both Newton-ADMM and SCS, to reach the optimal objective value, as well as to reach the solution; we see that Newton-ADMM outperforms SCS in both metrics.

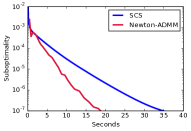

5.2 Minimum variance portfolio optimization

We consider a minimum variance portfolio optimization problem (see, e.g., Khare et al. (2015); Ali et al. (2016)),

| (54) |

where, here, the problem data is the covariance matrix associated with the prices of assets; we generated by sampling a positive definite matrix. The goal of the problem is to allocate wealth across assets such that the overall risk is minimized; shorting is allowed. Putting the above problem into the cone form of (1) yields, for , the direct product of the second-order cone and the nonnegative orthant (details in the supplement). The second column of Figure 1 shows the results; we again see that Newton-ADMM outperforms SCS.

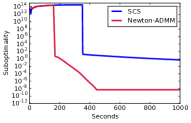

5.3 -penalized logistic regression

We consider -penalized logistic regression, i.e.,

| (55) |

where, here, here is a response vector; is a data matrix, with denoting the th row of ; and is a tuning parameter. We generated sparse underlying coefficients , by sampling entries from a normal distribution, then setting of the entries to zero; we generated (with ) by sampling its entries from a normal distribution, then set , where is (additive) Gaussian noise. For simplicity, we set the tuning parameter . Putting the above problem into the cone form of (1) yields, for , the direct product of the exponential cone and the nonnegative orthant (details in the supplement); the problem size in cone form ends up being large (see Table 1). In the third column of Figure 1, we see that Newton-ADMM outperforms SCS.

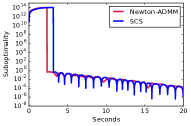

5.4 Robust principal components analysis (PCA)

Finally, we consider robust PCA,

| (56) |

where and are the nuclear and elementwise -norms, respectively, and (Candès et al., 2011, Equation 1.1). We generated a low-rank matrix , with rank ; a sparse matrix , by sampling entries from , then setting of the entries to zero; and finally set . We set . The goal is to decompose the obsevations into low-rank and sparse components. Putting the above problem into the cone form of (1) yields, for , the direct product of the positive semidefinite cone and nonnegative orthant (details in the supplement). We see that Newton-ADMM and SCS are comparable, in the fourth column of Figure 1.

5.5 Extension as a specialized solver

Finally, we observe that the basic idea of treating the residuals of consecutive ADMM iterates as a fixed point iteration, and then finding a fixed point using a Newton method, is completely general, i.e., the same idea can be used to accelerate (virtually) any ADMM-based algorithm, for a convex problem. To illustrate, consider the lasso problem,

| (57) |

where ; the ADMM recurrences (Parikh and Boyd, 2014, Section 6.4) are

| (58) | ||||

| (59) | ||||

| (60) |

where are the tuning parameter and auxiliary variables, introduced by ADMM, respectively, and is the soft-thresholding operator. The map , from (48), with components set to the residuals of the ADMM iterates given in (58) – (60), is then

where , and we also changed coordinates, similar to before. An element of the generalized Jacobian of is then

where is diagonal with set to 1 if and 0 otherwise, for .

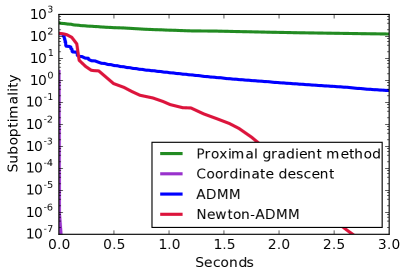

In the left panel of Figure 2, we compare a specialized Newton-ADMM applied directly to the lasso problem (57), with the ADMM algorithm for (58) – (60), a proximal gradient method (Beck and Teboulle, 2009), and a heavily-optimized implementation of coordinate descent (Friedman et al., 2007); we set . Here, the specialized Newton-ADMM is quite competitive with these strong baselines; the specialized Newton-ADMM outperforms Newton-ADMM applied to the cone program (2), so we omit the latter from the comparison. Stella et al. (2016) recently described a related approach.

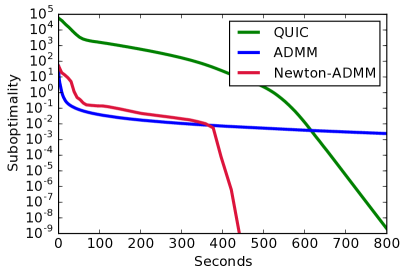

In the right panel of Figure 2, we present a similar comparison, for sparse inverse covariance estimation, with the QUIC method of Hsieh et al. (2014); Newton-ADMM clearly performs best (, details in the supplement).

6 Discussion

We introduced Newton-ADMM, a new method for generic convex programming. The basic idea is use a nonsmooth Newton method to find a fixed point of the residuals of the consecutive ADMM iterates generated by SCS, a state-of-the-art solver for cone programs; we showed that the basic idea is fairly general, and can be applied to accelerate (virtually) any ADMM-based algorithm. We presented theoretical and empirical support that Newton-ADMM converges rapidly (i.e., quadratically) to a solution, outperforming SCS across several problems.

Acknowledgements.

AA was supported by the DoE Computational Science Graduate Fellowship DE-FG02-97ER25308. EW was supported by DARPA, under award number FA8750-17-2-0027. We thank Po-Wei Wang and the referees for a careful proof-reading.

References

- Ali et al. (2016) Alnur Ali, Kshitij Khare, Sang-Yun Oh, and Bala Rajaratnam. Generalized pseudolikelihood methods for inverse covariance estimation. Technical report, 2016. Available at http://arxiv.org/pdf/1606.00033.pdf.

- Andersen et al. (2011) Martin Andersen, Joachim Dahl, Zhang Liu, and Lieven Vandenberghe. Interior point methods for large-scale cone programming. Optimization for machine learning, pages 55–83, 2011.

- Beck and Teboulle (2009) Amir Beck and Marc Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences, 2(1):183–202, 2009.

- Ben-Tal and Nemirovski (2001) Aharon Ben-Tal and Arkadi Nemirovski. Lectures on Modern Convex Optimization: Analysis, Algorithms, and Engineering Applications. SIAM, 2001.

- Boyd and Vandenberghe (2004) Stephen Boyd and Lieven Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- Boyd et al. (2011) Stephen Boyd, Neal Parikh, Eric Chu, Borja Peleato, and Jonathan Eckstein. Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends in Machine Learning, 3(1):1–122, 2011.

- Candès et al. (2011) Emmanuel Candès, Xiaodong Li, Yi Ma, and John Wright. Robust principal component analysis? Journal of the ACM, 58(3):11, 2011.

- Clarke (1990) Frank Clarke. Optimization and Nonsmooth Analysis. SIAM, 1990.

- Diamond and Boyd (2016) Steven Diamond and Stephen Boyd. CVXPY: A Python-embedded modeling language for convex optimization. Journal of Machine Learning Research, 17(83):1–5, 2016.

- Douglas and Rachford (1956) Jim Douglas and Henry Rachford. On the numerical solution of heat conduction problems in two and three space variables. Transactions of the American Mathematical Society, 82(2):421–439, 1956.

- Evans and Gariepy (2015) Lawrence Evans and Ronald Gariepy. Measure Theory and Fine Properties of Functions. CRC Press, 2015.

- Facchinei and Kanzow (1997) Francisco Facchinei and Christian Kanzow. A nonsmooth inexact Newton method for the solution of large-scale nonlinear complementarity problems. Mathematical Programming, 76(3):493–512, 1997.

- Facchinei and Pang (2007) Francisco Facchinei and Jong-Shi Pang. Finite-Dimensional Variational Inequalities and Complementarity Problems. Springer, 2007.

- Facchinei et al. (1996) Francisco Facchinei, Andreas Fischer, and Christian Kanzow. Inexact Newton methods for semismooth equations with applications to variational inequality problems, 1996.

- Fazel et al. (2001) Maryam Fazel, Haitham Hindi, and Stephen Boyd. A rank minimization heuristic with application to minimum order system approximation. In American Control Conference, 2001. Proceedings of the 2001, volume 6, pages 4734–4739. IEEE, 2001.

- Ferris and Munson (2004) Michael Ferris and Todd Munson. Semismooth support vector machines. Mathematical Programming, 101(1):185–204, 2004.

- Friedman et al. (2007) Jerome Friedman, Trevor Hastie, Holger Höfling, and Robert Tibshirani. Pathwise coordinate optimization. The Annals of Applied Statistics, 1(2):302–332, 2007.

- Grant (2004) Michael Grant. Disciplined Convex Programming. PhD thesis, Stanford University, 2004.

- Han et al. (1992) Shih-Ping Han, Jong-Shi Pang, and Narayan Rangaraj. Globally convergent Newton methods for nonsmooth equations. Mathematics of Operations Research, 17(3):586–607, 1992.

- Hintermüller (2010) Michael Hintermüller. Semismooth Newton methods and applications. Technical report, 2010. Available at http://www.math.uni-hamburg.de/home/hinze/Psfiles/Hintermueller_OWNotes.pdf.

- Hsieh et al. (2014) Cho-Jui Hsieh, Mátyás Sustik, Inderjit Dhillon, and Pradeep Ravikumar. QUIC: Quadratic approximation for sparse inverse covariance estimation. Journal of Machine Learning Research, 15(1):2911–2947, 2014.

- Izmailov and Solodov (2014) Alexey Izmailov and Mikhail Solodov. Newton-Type Methods for Optimization and Variational Problems. Springer, 2014.

- Kanzow and Fukushima (2006) Christian Kanzow and Masao Fukushima. Semismooth methods for linear and nonlinear second-order cone programs. Technical report, 2006.

- Khan and Barton (2017) Kamil A Khan and Paul Barton. Generalized derivatives for hybrid systems. IEEE Transactions on Automatic Control, 2017.

- Khare et al. (2015) Kshitij Khare, Sang-Yun Oh, and Bala Rajaratnam. A convex pseudolikelihood framework for high dimensional partial correlation estimation with convergence guarantees. Journal of the Royal Statistical Society: Series B, 77(4):803–825, 2015.

- Kong et al. (2009) Lingchen Kong, Levent Tunçel, and Naihua Xiu. Clarke generalized Jacobian of the projection onto symmetric cones. Set-Valued and Variational Analysis, 17(2):135–151, 2009.

- Lobo et al. (1998) Miguel Sousa Lobo, Lieven Vandenberghe, Stephen Boyd, and Hervé Lebret. Applications of second-order cone programming. Linear algebra and its applications, 284(1):193–228, 1998.

- Lofberg (2005) Johan Lofberg. YALMIP: A toolbox for modeling and optimization in MATLAB. In 2004 IEEE International Symposium on Computer Aided Control Systems Design, pages 284–289. IEEE, 2005.

- Magnus and Neudecker (1995) Jan Magnus and Heinz Neudecker. Matrix Differential Calculus with Applications in Statistics and Econometrics. John Wiley & Sons, 1995.

- Martínez and Qi (1995) José Martínez and Liqun Qi. Inexact Newton methods for solving nonsmooth equations. Journal of Computational and Applied Mathematics, 60(1):127–145, 1995.

- Mifflin (1977) Robert Mifflin. Semismooth and semiconvex functions in constrained optimization. SIAM Journal on Control and Optimization, 15(6):959–972, 1977.

- Nesterov and Nemirovskii (1994) Yurii Nesterov and Arkadii Nemirovskii. Interior Point Polynomial Algorithms in Convex Programming. SIAM, 1994.

- O’Donoghue et al. (2016) Brendan O’Donoghue, Eric Chu, Neal Parikh, and Stephen Boyd. Conic optimization via operator splitting and homogeneous self-dual embedding. Journal of Optimization Theory and Applications, pages 1–27, 2016.

- Parikh and Boyd (2014) Neal Parikh and Stephen Boyd. Proximal algorithms. Foundations and Trends in Optimization, 1(3):127–239, 2014.

- Peaceman and Rachford (1955) Donald Peaceman and Henry Rachford. The numerical solution of parabolic and elliptic differential equations. Journal of the Society for Industrial and Applied Mathematics, 3(1):28–41, 1955.

- Qi and Sun (1999) Liqun Qi and Defeng Sun. A survey of some nonsmooth equations and smoothing Newton methods, 1999.

- Qi and Sun (1993) Liqun Qi and Jie Sun. A nonsmooth version of Newton’s method. Mathematical Programming, 58(1-3):353–367, 1993.

- Recht et al. (2010) Benjamin Recht, Maryam Fazel, and Pablo A Parrilo. Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization. SIAM review, 52(3):471–501, 2010.

- Saad and Schultz (1986) Youcef Saad and Martin Schultz. GMRES: A generalized minimal residual algorithm for solving nonsymmetric linear systems. SIAM Journal on Scientific and Statistical Computing, 7(3):856–869, 1986.

- Serrano (2015) Santiago Serrano. Algorithms for Unsymmetric Cone Optimization and an Implementation for Problems with the Exponential Cone. PhD thesis, Stanford University, 2015.

- Śmietański (2007) Marek Śmietański. A generalized Jacobian based Newton method for semismooth block triangular system of equations. Journal of Computational and Applied Mathematics, 205(1):305–313, 2007.

- Stella et al. (2016) Lorenzo Stella, Andreas Themelis, and Panagiotis Patrinos. Forward-backward quasi-Newton methods for nonsmooth optimization problems. Technical report, 2016. Available at https://arxiv.org/pdf/1604.08096.pdf.

- Sturm (2002) Jos Sturm. Implementation of interior point methods for mixed semidefinite and second order cone optimization problems. Optimization Methods and Software, 17(6):1105–1154, 2002.

- Sun and Sun (2002) Defeng Sun and Jie Sun. Semismooth matrix-valued functions. Mathematics of Operations Research, 27(1):150–169, 2002.

- Toh et al. (2012) Kim-Chuan Toh, Michael Todd, and Reha Tütüncü. On the implementation and usage of SDPT3 — a MATLAB software package for semidefinite/quadratic/linear programming, version 4.0. In Handbook on Semidefinite, Conic, and Polynomial Optimization, pages 715–754. Springer, 2012.

- Udell et al. (2014) Madeleine Udell, Karanveer Mohan, David Zeng, Jenny Hong, Steven Diamond, and Stephen Boyd. Convex optimization in Julia. In Proceedings of the 1st First Workshop for High Performance Technical Computing in Dynamic Languages, pages 18–28. IEEE, 2014.

- Ulbrich (2011) Michael Ulbrich. Semismooth Newton Methods for Variational Inequalities and Constrained Optimization Problems in Function Spaces. SIAM, 2011.

- Wu and Boyd (2000) Shao-Po Wu and Stephen Boyd. sdpsol: A parser/solver for semidefinite programs with matrix structure. Advances in Linear Matrix Inequality Methods in Control, pages 79–91, 2000.

- Ye et al. (1994) Yinyu Ye, Michael Todd, and Shinji Mizuno. An -iteration homogeneous and self-dual linear programming algorithm. Mathematics of Operations Research, 19(1):53–67, 1994.

Supplement to “A Semismooth Newton Method for Fast, Generic Convex Programming”

S.1 Proof of Lemma 3.2

The proof relies on the proof of Lemma 3.6, below. Let , and let . Suppose converges to a point that falls into one of the first three cases given in Section 2. Then, from the statement and proof of Lemma 3.6, an element of the generalized Jacobian of the projection onto the dual of the exponential cone at , is just a matrix with fixed entries, since projections onto convex sets are continuous. If converges to a point that falls into the fourth case, then brute force, e.g., using symbolic manipulation software, reveals that an element of the generalized Jacobian (i.e., the inverse of the specific 4x4 matrix given in (S.18), below) is also a constant matrix, even as ; for completeness, we give in (S.38), at the end of the supplement. Thus in all the cases, the Jacobian is a constant matrix, which is enough to establish that the limit in (44) exists. ∎

S.2 Proof of Lemma 3.3

First, we give a useful result; its proof is elementary.

Lemma S.2.1.

The affine transformation, , of a (strongly) semismooth map , with , is (strongly) semismooth.

Proof.

First of all, we have that a map is (strongly) semismooth if and only if its components , for , are (strongly) semismooth (Qi and Sun, 1993, Corollary 2.4). Additionally, we have that (strongly) semismooth maps are closed under linear combinations (Izmailov and Solodov, 2014, Proposition 1.75). Putting the two pieces together gives the claim. ∎

Now, from Lemma 3.1, we have that the projections onto the nonnegative orthant, second-order cone, positive semidefinite cone, as well as the free cone (an affine map, hence strongly semismooth (Facchinei and Pang, 2007, Proposition 7.4.7)), are all strongly semismooth. The map , defined in (48), is just an affine transformation of these projections; thus, by (S.2.1), it is strongly semismooth.

S.3 Proof of Lemma 3.4

Proof.

We have that (i) the projection onto a convex set (e.g., the nonnegative orthant, second-order cone, positive semidefinite cone, exponential cone, and free cone), naturally, yields a convex set; (ii) the affine image of a convex set is a convex set; and (iii) retaining only some of the coordinates of a convex set is a convex set (Boyd and Vandenberghe, 2004, page 38). Hence, the components , for , of the map , defined in (48), are convex functions. Thus, by Clarke (1990, Proposition 1.2), the th row of any element of the generalized Jacobian is just a subgradient of . Now observe that the element of the generalized Jacobian, given in (49), is given by finding subgradients of the . ∎

S.4 Jacobian of the projection onto the second-order cone

In Section 3.2, we stated that, in one case, the Jacobian of the projection onto the second-order cone at some point , with , is a low-rank matrix ; the matrix is given by

| (S.1) |

which can be seen as the sum of diagonal and low-rank matrices. Here, denotes the th component of .

S.5 Proof of Lemma 3.5

Rewrite the projection onto the positive semidefinite cone as (40) as , where is the eigenvalue decomposition of some real, symmetric matrix , and the here is interpreted diagonally. Then, using the chain rule (Magnus and Neudecker, 1995), we get that

so, what remains is computing (each column of) and , i.e., the differential of (each column of) the matrix of eigenvectors, and the differential of , respectively. From Magnus and Neudecker (1995, Chapter 8), we get that

where denotes the pseudo-inverse of the matrix , and that

by applying the chain rule; here, is the indicator function of the nonnegative orthant, i.e., it equals 1 if its argument is nonnegative and 0 otherwise. Replacing with some real, symmetric matrix yields the claim. ∎

S.6 Further details on the per-iteration costs of SCS, Newton-ADMM, and CVXOPT

Here, we elaborate on the costs of a single iteration of SCS, Newton-ADMM, and CVXOPT. For simplicity, we consider the case where the cone , in the cone program (1), is just a single cone (handling the case where is the direct product of multiple cones is not hard); also, we are mostly interested in the high-dimensional case, where .

During a single iteration of SCS, described in (35) – (37), we must carry out the computations outlined below:

-

•

We must update the variable, which costs (see Section 4.1 of O’Donoghue et al. (2016)).

-

•

We must update the variable, the cost of which is dominated by the cost of projecting an -vector onto the dual cone ; for the case of projecting onto the positive semidefinite cone, we equivalently consider a matrix with dimensions . These costs are as follows:

-

–

For the nonnegative orthant, , the cost is .

-

–

For the second-order cone, , the cost is .

-

–

For the positive semidefinite cone, , the cost is .

-

–

For the exponential cone, , the cost is roughly .

-

–

-

•

We must update the variable, which has negligible cost.

Summing up, the cost of a single iteration of SCS is plus the cost of projecting onto the dual cone , as claimed in the main paper.

For Newton-ADMM, we must compute the ingredients on both sides of (51), and , as well as run GMRES and the backtracking line search. Computing both and can be seen as essentially costing the same as a single iteration of SCS, i.e., the cost of projecting onto the dual cone plus ; the backtracking line search, then, costs the number of backtracking iterations times the aforementioned cost. Furthermore, running GMRES costs , assuming it returns early. Hence the cost of a single iteration of Newton-ADMM is (as claimed in the main paper) the number of backtracking iterations times the sum of two costs: the cost of projecting onto the dual cone plus .

Finally, turning to the interior-point method CVXOPT, it can be seen that the per-iteration cost here is dominated by solving the Newton system (1.11) in Andersen et al. (2011), essentially costing .

We mention that the above per-iteration costs can, of course, be improved by taking advantage of sparsity.

S.7 Proof of Lemma 3.6

First, from the Moreau decomposition given in (42), we get that

so, what remains is to compute , for some . Looking back at the first three cases given in Section 2, we get that

where , is the indicator function of the nonnegative orthant, i.e., it equals 1 if and 0 otherwise. For the fourth case, the projection is the solution to the optimization problem given in (41). Now observe that (i) the optimization problem (41) is, in fact, convex, since the constraint is really just implied by the domain of the function ; (ii) the optimization problem (41) is feasible, since satisfies the constraint; and (iii) we can obtain a solution to the optimization problem (41), by using a Newton method (Parikh and Boyd, 2014, Section 6.3.4).

The rest of the proof relies on the KKT conditions for the optimization problem (41), as well as differentials (see, e.g., Magnus and Neudecker (1995)). The Lagrangian of the optimization problem (41) is given by

where is the dual variable. Thus, we get that the KKT conditions for the optimization problem (41), at a solution , are

| (S.2) | ||||

| (S.3) | ||||

| (S.4) | ||||

| (S.5) |

S.8 Intuition behind some of the regularity conditions for Theorem 4.1, Theorem 4.2, and Theorem 4.3

Here, we elaborate on a couple of the regularity assumptions stated in the main paper.

S.8.1 Regularity condition (A4)

Roughly speaking, the condition (A4) can be seen as requiring that the directional derivative of be bounded by .

We list some (useful) functions satisfying (A4):

-

•

The function , for . To show that the function satisfies (A4), we proceed by computing the required ingredients on both sides of (A4). Here, and for the rest of the section, we write to mean the directional derivative of the function squared, in the direction , evaluated at .

We compute, for and the Newton direction , the left-hand side of (A4),

and the right-hand side of (A4),

So, satisfying (A4) means

which is certainly true. Repeating the argument for and yields a similar result. (When , it is a solution.) Hence, satisfies (A4).

-

•

The function , with and some .

We have, for the left-hand side of (A4):

We have, for the right-hand side of (A4):

So, satisfying (A4) means

In words, functions that satisfy (A4) cannot have too small.

-

•

An argument similar the one used above for can be used to show that the function also satisfies (A4).

We also establish, by using the condition (A4), that the backtracking line search, used in Algorithm 1, terminates. Suppose, for contradiction, that the backtracking line search never terminates. Then, from the backtracking line search iteration described in Algorithm 1, we have, for all backtracking iterations ,

Taking the limit as , we get

| (S.19) |

On the other hand, expanding the right-hand side of (A4) gives

| (S.20) | ||||

| (S.21) | ||||

| (S.22) | ||||

| (S.23) | ||||

| (S.24) |

Putting (A4) and (S.24) above together immediately gives

| (S.25) |

S.8.2 Regularity condition (A5)

Roughly speaking, the condition (A5) says that the Newton step on each iteration cannot be too large.

S.9 Proof of Theorem 4.1

Proof.

We begin by recalling the condition under which backtracking line search continues, for a particular iteration of Newton’s method; this happens as long as (see Algorithm 1)

| (S.26) |

This means that when backtracking line search terminates, we get that

| (S.27) |

(To be clear, in order to get the second inequality here, we used the fact that backtracking line search terminates after (S.26) in Algorithm 1 no longer holds.) In order to get the third inequality here, we used the simple fact that , since and . So, we have shown that the sequence is both bounded below and decreasing. Note that this is just a sequence in R, and thus, by the monotone convergence theorem, it converges. Furthermore, since every convergent sequence in R is Cauchy, we get that

| (S.28) |

On the other hand, by rearranging the second inequality in (S.27), we get that

| (S.29) |

So, (S.28) along with taking the on both sides of (S.29) yields that . But assumption (A1) says that , and since , we get that , for some , and so , which implies that , as claimed. ∎

S.10 Proof of Theorem 4.2

Proof.

First of all, by the assumption that is convergent and assumption (A5), we must have that

| (S.30) |

where the second inequality here follows by rearranging (A5), and the third inequality follows from (52), as well as the triangle inequality: after computing on Newton iteration , we are assured that

Hence, since

and because the right-hand side here is bounded (as per (S.30), as well as the fact that is decreasing), we can conclude that the sequence is bounded. (We used the Euclidean distance here.)

By the Bolzano-Weierstrass theorem (for Euclidean spaces), this sequence contains a convergent subsequence; let , for some countable set , be this subsequence. Define , i.e., is the last for which (S.26) was actually true (i.e., when checked at the start of the th Newton iteration). Then we get

dividing through by and taking limits gives (observe that, from assumption (A2), )

| (S.31) | ||||

| (S.32) |

with the second line here following by assumption (A4). Expanding the right-hand side of (S.32), we get

with the second line following from the Cauchy-Schwarz inequality, and the third from (52). So, we obtain for the right-hand side of (S.32) that

| (S.33) |

Now, by assumption (A3), we require that ; thus, we must have that , as claimed. ∎

S.11 Proof of Theorem 4.3

Proof.

The theorem establishes that the iterates generated by Algorithm 1 are locally quadratically convergent, i.e., we get, for large enough and some , that

Let , for convenience. We begin by making two useful observations.

First, using the second part of assumption (A6), we get that

| (S.34) |

On the other hand, using the triangle inequality as well as (52), we get that

| (S.35) |

So, putting together (S.34) and (S.35), we get that

for some constant , since . Squaring both sides, it follows that

| (S.36) |

where is some constant, and the third line follows because (52) and assumption (A3) tell us that for some constant . Finally, Facchinei and Kanzow (1997, Theorem 2.5) and the second part of assumption (A6) tell us that the sequence of iterates converges quadratically, with , as claimed. ∎

S.12 Further details on the minimum variance portfolio optimization example

Here, we elaborate on putting the minimum variance portfolio optimization problem (54) into the cone form of (1).

S.13 Further details on the -penalized logistic regression example

Here, we elaborate on putting the -penalized logistic regression problem (55) into the cone form of (1). To keep the notation light, we write

Now, for , we use the simple fact (Serrano, 2015, Section 9.4.1) that

for , in order to conclude that

| (S.37) |

where the are some variables that we will introduce, later on. Next, we “split” the right-hand side of (S.37) into the following set of constraints:

where are more new variables. Thus, we can write the -penalized logistic regression problem (55) as

Finally, to get the cone form of (1), we use

here, denotes the th standard basis vector in , and denotes the -dimensional nonnegative orthant.

S.14 Further details on the robust PCA example

First, we observe that, using duality arguments (see, e.g., Fazel et al. (2001, Section 3) or Recht et al. (2010, Proposition 2.1)), we can rewrite the robust PCA problem (56) as

To get the cone form of (1), we use

| where is except with the th entry of its upper right block | |||

Here, denotes the -dimensional positive semidefinite cone. Also, observe that the last row of above encodes the constraint

which we can write as a linear matrix inequality (Andersen et al., 2011, Equation 1.7):