Bootstrap confidence bands for spectral estimation of Lévy densities under high-frequency observations

Abstract.

This paper develops bootstrap methods to construct uniform confidence bands for nonparametric spectral estimation of Lévy densities under high-frequency observations. We assume that we observe discrete observations at frequency , and work with the high-frequency setup where and as . We employ a spectral (or Fourier-based) estimator of the Lévy density, and develop novel implementations of Gaussian multiplier (or wild) and empirical (or Efron’s) bootstraps to construct confidence bands for the spectral estimator on a compact set that does not intersect the origin. We provide conditions under which the proposed confidence bands are asymptotically valid. Our confidence bands are shown to be asymptotically valid for a wide class of Lévy processes. We also develop a practical method for bandwidth selection, and conduct simulation studies to investigate the finite sample performance of the proposed confidence bands.

Key words and phrases:

empirical bootstrap, high-frequency data, Lévy process, multiplier bootstrap, spectral estimation1. Introduction

In the financial economics literature, it has been argued that the presence of jumps plays an important role in the dynamics of financial data such as asset returns, interest rates, currencies, and so on (cf. Cont and Tankov, 2004; Aït-Sahalia, 2004; Johannes, 2004; Aït-Sahalia and Jacod, 2014). For example, Johannes (2004) studies the dynamics of interest rate movements and argues that the presence of jumps contributes to capturing non-normalities of increment distributions that are consistent with empirical data but diffusion models can not capture. A Lévy process is a fundamental class of continuous-time stochastic processes allowing for jumps; we refer to Sato (1999) and Bertoin (1996) as standard references on Lévy processes. From the Lévy-Itô decomposition (Sato, 1999, Theorem 19.2), a Lévy process is decomposed into the sum of drift, Brownian, and jump components, and the distribution of the Lévy process is completely determined by the three parameters, namely, the drift, the diffusion coefficient, and the Lévy measure. The Lévy measure controls the jump dynamics of the Lévy process, and therefore, inference on the Lévy measure is of particular interest. In this paper, we assume that the Lévy density has a Lebesgue density (Lévy density), and study inference on the Lévy density from high-frequency observations. High-frequency data – data collected for every minute, second, or even microsecond – have become available due to the advancement of information technologies, and the analysis of high-frequency financial data has attracted a great deal of attentions in the financial econometrics literature; see, e.g., Aït-Sahalia and Jacod (2014).

To be precise, we work with the following setting. Let be a Lévy process, i.e., is a stochastic process starting at with stationary independent increments and càdlàg sample paths. From the Lévy-Khinchin representation (Sato, 1999, Theorem 8.1), has characteristic function , where , and

The triplet , called the Lévy triplet, completely characterizes the distribution of the Lévy process (cf. Sato, 1999, Theorem 7.10). Specifically, is the diffusion coefficient, is the drift, and is the Lévy measure, i.e., a Borel measure on such that

For any (Borel) set , coincides with the expected number of jumps falling in in the unit time:

where (recall that has at most countably many jumps on for any ). In this paper, we assume that the Lévy measure has Lebesgue density , called the Lévy density, i.e., . Furthermore, we assume that we observe discrete observations at frequency , and work with the high-frequency setup where and as . Since we are interested in estimation of the Lévy measure (or more precisely its Lebesgue density), we require . Heuristically, this can be understood from the observation that, within any fixed time interval, say the unit time, the Lévy process has only finitely many jumps that fall in a local neighborhood not containing the origin, so that even if the whole path could be observed, there are only finitely many data that can be used to estimate the Lévy measure at the local neighborhood. Concretely, we have in mind that the unit time is one day, and if we have 6.5 trading hours in a day and take 5 minutes as a time span, then ; each year has around 252 business days, and so we have observations per a year.

Under this setup, the goal of this paper is to develop bootstrap methods to construct confidence bands for the Lévy density. Since the Lévy density can blow up around the origin, we focus on confidence bands on a compact set that does not intersect the origin. We employ a spectral (or Fourier-based) estimator of the Lévy density, and develop novel implementations of Gaussian multiplier and empirical bootstraps to construct confidence bands for the spectral estimator. We provide conditions under which the proposed confidence bands are asymptotically valid. Notably, our confidence bands are shown to be asymptotically valid for a wide class of Lévy processes, including compound Poisson processes, (Variance-) Gamma processes, Inverse Gaussian processes, tempered stable processes, and Normal Inverse Gaussian processes with or without Brownian components.111For tempered stable processes, however, the stability index has is at most for a technical reason. Confidence bands provide a simple graphical description of the accuracy of a nonparametric curve estimator, thereby quantifying uncertainties of the estimator simultaneously over (in most cases continuum of) designs points, which is of practical importance in statistical analysis. Despite extensive studies on consistent estimation of the Lévy density, however, research on confidence intervals or bands for the Lévy density is relatively scarce – see a literature review below. In particular, to the best of our knowledge, this is the first paper to derive bootstrap-based confidence bands for the Lévy density. In addition to the theoretical results, we also develop a practical method for bandwidth selection, inspired by Bissantz et al. (2007), and conduct simulation studies to investigate the finite sample performance of the proposed confidence bands.

The literature on nonparametric estimation of Lévy measures or densities is broad. Recent contributions include Shimizu (2006), Figueroa-López (2009), Comte and Genon-Catalot (2009, 2010, 2015), Kappus and Reiß (2010), Duval (2013), and Bec and Lacour (2015) under the high-frequency setup (i.e., as ), and van Es et al. (2007), Neumann and Reiß (2009), Gugushvili (2009), Chen et al. (2010), Comte and Genon-Catalot (2010), Kappus and Reiß (2010), Belomestny (2011), Gugushvili (2012), Kappus (2014), Trabs (2015), and Belomestny and Reiß (2015) under the low-frequency setup (i.e., is fixed). Jongbload et al. (2005) study nonparametric estimation of the Lévy measure for a Lévy driven Ornstein-Uhlenbeck process under high and low frequency observations. Nickl and Reiß (2012) and Nickl et al. (2016) study estimation of distribution functions such as , and prove Donsker-type functional limit theorems for distributional function estimators under low- and high-frequency setups, respectively. We also refer to Bücher and Vetter (2013), Vetter (2014), Bücher et al. (2017), and Hoffmann and Vetter (2017) for inference on Lévy measures. However, none of these papers studies confidence bands for Lévy densities.

To the best of our knowledge, Figueroa-López (2011b) and its follow-up paper Konakov and Panov (2016) are the only references that derive uniform confidence bands for Lévy densities. They work with the high-frequency setup, but employ sieve (or projection) estimators based on the observation that for (see also Figueroa-López, 2009), which are substantially different from our spectral estimator. So, first of all, their results do not cover ours. Similarly to Smirnov (1950) and Bickel and Rosenblatt (1973), Figueroa-López (2011b) proves that the supremum deviation of the sieve estimator, suitably normalized, converges in distribution to a Gumbel distribution, by using the Komlós-Major-Tusnády (KMT) approximation of the empirical distribution function by Brownian bridges (Komlós et al., 1975), combined with extreme value theory. Figueroa-López (2011b) uses the Gumbel approximation to construct analytic confidence bands for the Lévy density, but does not study bootstrap-based confidence bands. However, since the convergence of normal extremes is known to be slow (Hall, 1991), in standard nonparametric density and regression function estimation, it is often recommended to use versions of bootstraps to construct confidence bands, instead of relying on Gumbel approximations (cf. Neumann and Polzeh;, 1998; Claeskens and Van Keilegom, 2003; Chernozhukov et al., 2014a).222For the trigonometric basis, Konakov and Panov (2016) develop an analytical method based on higher oder expansions to improve on the Gumbel approximation; see their Theorem 3.7. This paper contributes to the literature on nonparametric inference for Lévy processes by developing bootstrap confidence bands for the first time in the Lévy density estimation case. Furthermore, spectral-type estimators are among the most commonly used methods for estimation of the Lévy density (cf. Comte and Genon-Catalot, 2015; Belomestny and Reiß, 2015), and developing inference methods for them is practically important.

From a technical point of view, the proofs of the main theorems build on non-trivial applications of the intermediate Gaussian and bootstrap approximation theorems developed in Chernozhukov et al. (2014a, b, 2016). The analysis of the present paper has some connections to those of Kato and Sasaki (2016, 2017) that study confidence bands for deconvolution and nonparametric errors-in-variables regression, respectively. However, the high-frequency setup in Lévy process estimation has different probabilistic structures than the i.i.d. setup in standard nonparametric estimation. For example, the increment distribution (i.e., the distribution of ) need not be continuous and may have a discrete component (which is in contrast to the standard density estimation case); is indexed by with as , and degenerates to the point mass at the origin; and the interplay between and has to be taken care of. In particular, providing low-level regularity conditions for validity of bootstrap confidence bands in the Lévy density estimation case is far from trivial and requires substantial work. See the discussion after Assumption 4.1 and Section 4.2.

In this paper, we assume that data do not contain microstructure noises. We have in mind that the time span is small but not too small – say 5 minutes if the unit time is one day. For such cases, Aït-Sahalia and Xiu (2017) argue that the effect of microstructure noise is small.

The rest of the paper is organized as follows. In Section 2, we define a spectral estimator for the Lévy density, and in Section 3 we describe our bootstrap methods to construct confidence bands for the spectral estimator. We consider two bootstrap methods, namely, Gaussian multiplier and empirical bootstraps. In Section 4, we present theorems that establish asymptotic validity of the proposed confidence bands. In Section 5, we provide concrete examples of Lévy processes that satisfy our regularity conditions. In Section 6, we propose a practical method for bandwidth selection, and study its finite sample performance via numerical simulations. Section 7 concludes. All the proofs are deferred to Appendix.

1.1. Notation

We will obey the following notation. For any non-empty set and any (complex-valued) function on , let . Let denote the (real) Banach space of all bounded real-valued functions on equipped with the sup-norm . The Fourier transform of an integrable function on is defined as

For any , let denote the Dirac measure at . For any , let and . For and , we use the shorthand notation . For any non-empty set in and any , let where . For any positive sequences , we write if there is a positive constant independent of such that for all , if and , and if as .

2. Spectral estimation of Lévy density

We first describe a spectral estimation method for Lévy densities. Let be increments of discrete observations of the Lévy process , and observe that are i.i.d. whose common characteristic function is . In this paper, we assume that

| (2.1) |

which is equivalent to assuming that (and for all ; see Sato (1999), Corollary 25.8). Condition (2.1) ensures that the integral is well-defined, so that the characteristic exponent admits an alternative representation:

where . Furthermore, under Condition (2.1), differentiating twice, we arrive at the key identity

Therefore, applying the Fourier inversion, we conclude that

| (2.2) |

where the Fourier inversion should be interpreted in the distributional sense if the integral is not well-defined. This expression leads to a method to estimate .

First, we estimate by , where

is the empirical characteristic function ( denotes the -th derivative of with ). Let be an integrable function (kernel) such that and its Fourier transform is supported in (i.e., for all ). Then the spectral estimator of is defined by

| (2.3) |

for , where is a sequence of positive numbers (bandwidths) such that as , and is a pilot estimator of .

Some comments on the spectral estimator are in order. First, as long as , , so that for is well-defined with probability approaching one (see Lemmas A.2 and A.4). Second, the function is real-valued. Third, noting that is well-defined on (with probability approaching one) as the distinguished logarithm (Chung, 2001, Theorem 7.6.2), we see that the spectral estimator can be alternatively expressed as

for . Finally, in this paper, we are interested in estimating on a compact set away from the origin (e.g. for ), and therefore, as long as decays sufficiently fast as , we may take in theory. See the discussion after Assumption 4.1 below. However, in our simulation studies, we found that, in case of , using a proper estimator for improves on the empirical performance of the estimator and the inference methods, especially if the set is close to the origin. Therefore, we recommend to plug-in a proper estimator of . There are several existing estimators for ; see Example 2.1 below.

Our spectral estimator (2.3) is considered and studied in Belomestny (2011) and Gugushvili (2012) under the low-frequency setup. Nickl et al. (2016) use the spectral estimator (2.3) to construct estimators for distribution functions such as , and prove Donsker-type functional limit theorems for distribution function estimators under the high-frequency setup. There are versions of spectral-type estimators of similar to but different from ours (2.3). For example, in case of , Comte and Genon-Catalot (2011) consider simplified versions of the estimator (2.3) by replacing with 1 and/or with . Such simplifications produce additional biases that depend on (but not on smoothness of ); since the problem of bias is already delicate in construction of confidence bands in standard nonparametric estimation (cf. Wasserman, 2006, Section 5.7), producing additional biases is not favorable to our goal from both theoretical and practical view points. Hence, in this paper, we focus on the current spectral estimator (2.3). It is worth pointing out that the identification (2.2) of the Lévy density holds without relying on the assumption that , and therefore the deterministic bias of our spectral estimator does not depend on ; see the discussion after Assumption 4.1 below.

Furthermore, under relatively mild conditions, our spectral estimator (2.3) is consistent under the weighted sup-norm on , (see Appendix C), and thereby is able to capture the shape of globally (i.e., uniformly over ), which we believe is an attractive feature of the spectral estimator .

Example 2.1 (Examples of estimators for ).

There are several consistent estimators for available in the literature on high-frequency data analysis for continuous-time stochastic processes. We provide a couple of examples here. The first example is the truncated realized volatility (TRV) estimator proposed in Mancini (2001) :

| (2.4) |

where and . The second example is the power variation (PV) estimator proposed in Barndorff-Nielsen and Shephard (2004):

where and is the -th absolute moment of . Jacod and Reiß (2014) study the optimal rate of convergence for estimating in the minimax sense and propose the following estimator (modified to our setup):

where is a deterministic sequence. In our simulation studies, we use as an estimator of .

Strictly speaking, the references cited above study the asymptotic properties of the estimators under a different high-frequency setup that as but is fixed. For the asymptotic properties of the PV and JR estimators under our setup, we refer to Comte and Genon-Catalot (2011, Proposition 5.3) (see also Aït-Sahalia and Jacod, 2007) and Nickl et al. (2016, Proposition 13), respectively. For the sake of completeness, we summarize the asymptotic properties of the TRV estimator in the following lemma. See Appendix B.1 for the proof.

Lemma 2.1.

Suppose that the Lévy measure satisfies for some , and if , then assume in addition that . Then .

2.1. Comparison with direct kernel estimation: preliminary simulations

Alternatively to spectral-type estimation methods, exploiting the assumption that as , we can estimate the Lévy density for by applying directly kernel density estimation to increments , i.e.,

| (2.5) |

where is a compactly supported smooth kernel function. In fact, for a given fixed , if is Lipschitz continuous in a neighborhood of , then from Lemma B.1 and Proposition 2.1 in Figueroa-López (2011b), we can show that

so that is consistent for at under appropriate regularity conditions. Actually, the direct kernel estimator (2.5) is mentioned in Figueroa-Löpez (2011a, Section 4.1), although the detailed properties of (2.5) are not studied there. From a theoretical point of view, it is rather easier to develop inference methods for than the spectral estimator (2.3) under the high-frequency setup, since the former is of simpler form than the latter. So, one might be tempted to wonder why we bother to use a more complicated estimator .

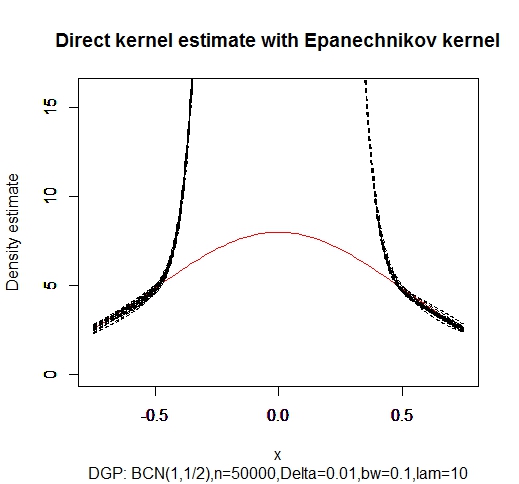

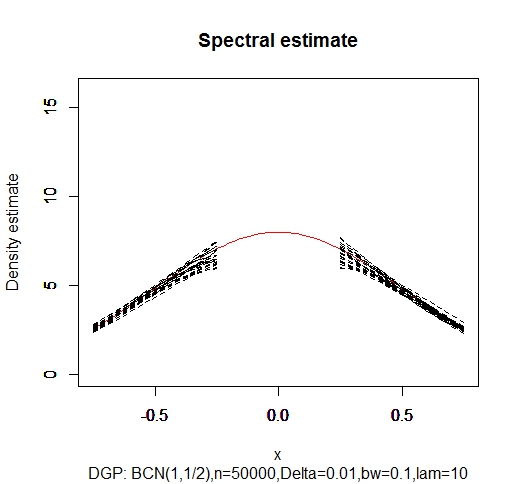

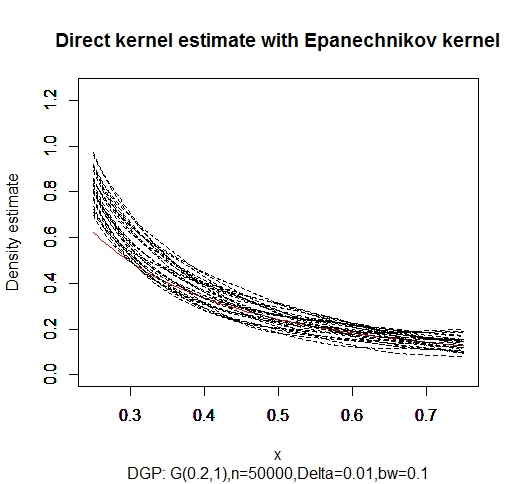

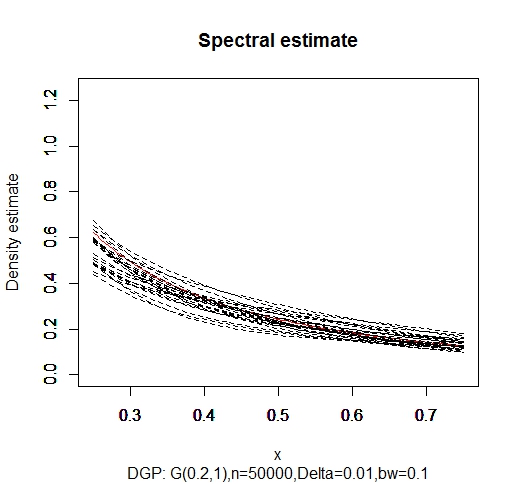

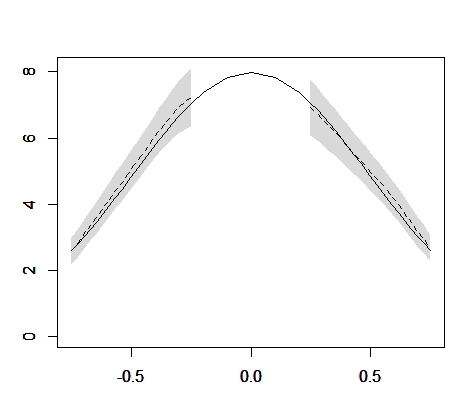

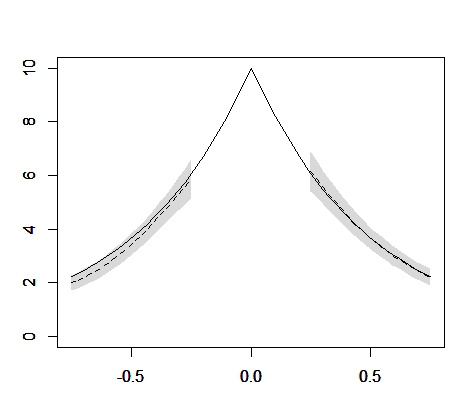

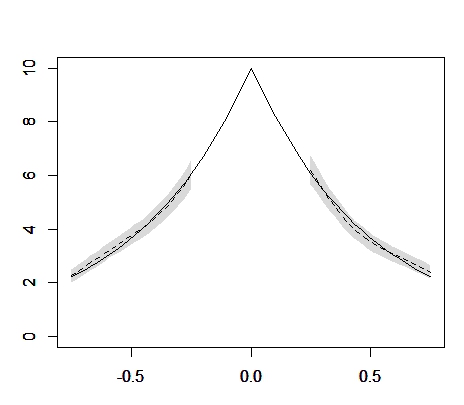

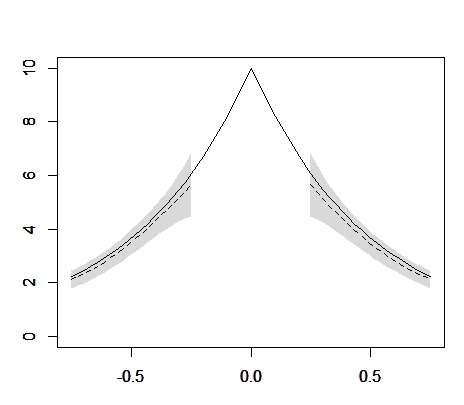

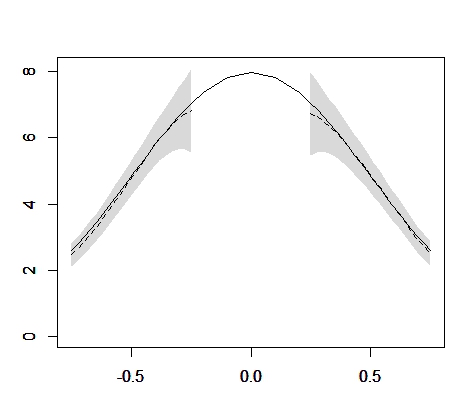

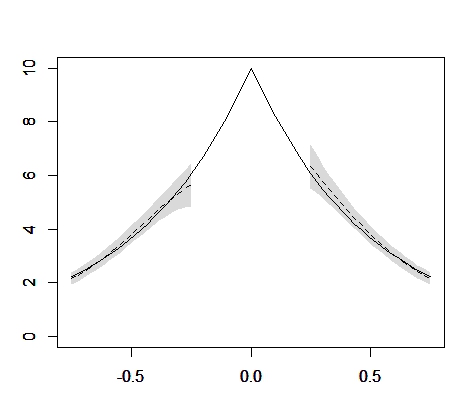

It turns out that, however, in the finite sample, the direct kernel estimate (2.5) tends to have (much) larger biases, especially near the origin, than the spectral estimate (2.3). Figures 1 and 2 compare realizations of direct kernel estimates with Epanechnikov kernel and spectral estimates with a flap-top kernel for a jump-diffusion process where is a standard Brownian motion and is a compound Poisson process (independent of ) with intensity and jump size distribution (), and for a Gamma process with parameter (i.e, has Gamma distribution with shape parameter and scale parameter ). Here we set . Preliminary calibrations show that works well for for both estimates, and we set this bandwidth value to generate these figures. The flap-top kernel used for the spectral estimate is defined by the inverse Fourier transform of equation (4.4) ahead with and . Furthermore, for the spectral estimate, we plug-in the TRV estimate with and for the jump-diffusion case, and set for the Gamma process case (using the TRV estimate for the Gamma process case produced almost same simulation results).

|

|

These figures show that the direct kernel estimate has large biases especially near the origin, whereas the spectral estimate performs reasonably well on the entire set for each case ( for the jump-diffusion case, and for the Gamma process case). In particular, the direct kernel estimate exhibits unreasonable behaviors for in the jump-diffusion case. Intuitively, such unreasonable behaviors can be understood from the observation that the increment distribution (i.e., the distribution of ) of the jump-diffusion process is the convolution of with the compound Poisson distribution that has a point mass at the origin, and therefore, the density of has a sharp peak around the origin. Since the direct kernel estimate is estimating the density of scaled by , it tends to return unreasonably large values near the origin (we also note that, since for , the interval is not a “small” neighborhood of the origin). These preliminary simulation results motivate us to study inference methods for the spectral estimator (2.3) rather than the direct kernel estimator (2.5).

3. Construction of confidence bands

We consider to construct confidence bands for on a compact set in . For example, for ; or for . The set may be a singleton, i.e., for , although we are primarily interested in the above two cases.

Under the regularity conditions stated below, we will show that can be approximated by

| (3.1) |

uniformly in . By a change of variables, we may rewrite the term (3.1) as

| (3.2) |

where is the function defined by

Note that is well-defined and real-valued. Define

and consider the process

Under the regularity conditions stated below, for sufficiently large . Furthermore, we will show that there exists a tight Gaussian random variable in with mean zero and the same covariance function as , and such that the distribution of asymptotically approximates that of in the sense that

as , which in turn yields that

| (3.3) |

Hence, construction of confidence bands for on reduces to approximating or estimating quantiles of . In fact, let

for , and consider a confidence band of the form

Since , it is seen that

so that will be a valid confidence band for on with level approximately , provided that (3.3) holds.

Now, we shall estimate the quantile , in addition to the variance function . The latter can be estimated from

where is the function defined by

Note that as long as , , so that is well-defined with probability approaching one. To estimate the quantile , we consider two bootstrap methods. The one is the Gaussian multiplier (or wild) bootstrap, and the other is the empirical (or Efron’s) bootstrap.

Gaussian multiplier bootstrap

Generate i.i.d., independent of the data , and construct the multiplier process

where . Note that under the regularity conditions stated below, , so that is well-defined with probability approaching one. Conditionally on the data , is a Gaussian process whose covariance function “estimates” that of . Hence, we estimate by

which can be computed via simulations. The resulting confidence band is

Empirical bootstrap

Next, we consider the empirical bootstrap. Let denote the empirical distribution. Conditionally on the data, generate i.i.d., and construct the bootstrap process

We estimate by

The resulting confidence band is

Remark 3.1 (Scaling by ).

One might think that, because of the scaling by , our confidence bands would be too wide if is close to the origin. However, heuristically, the standard deviation function would scale like for , so the scaling factor would be canceled out and would scale like . To see this, assuming that has finite fourth moment (which ensures that has finite fourth moment), observe that since weakly as finite measures333To see this, observe that, for each , , so that which implies that weakly., we have that, heuristically,

Of course, these approximations are only heuristic, but the discussion so far at least provides a partial explanation for that the scaling factor would not too much inflate the width of our bands. See also figures in Section 6.

4. Main results

4.1. Validity of bootstrap confidence bands

In this section, we prove validity of the proposed confidence bands and . To this end, we make the following assumption. Recall that a function is said to be -Hölder continuous for if

Let denote the distribution of , and for any , let denote the distribution of . Let be a compact set in .

Assumption 4.1.

We assume the following conditions.

-

(i)

.

-

(ii)

There exists such that the measure has Lebesgue density such that . Furthermore, for some sufficiently small such that .

-

(iii)

Let , and let be the integer such that . The function is -times differentiable, and is -Hölder continuous.

-

(iv)

Let be an integrable function (kernel) such that

(4.1) where is the Fourier transform of .

-

(v)

for some , and .

-

(vi)

Let be an estimator of such that .

Condition (i) is a moment condition and is equivalent to finiteness of the fourth moment of (and for all ; see Sato (1999), Corollary 25.8). Condition (i) excludes, e.g., -stable processes for , but it allows for not to be integrable (i.e., is allowed). Condition (ii) is a high-level condition and will be discussed in detail in the next subsection. However, at this point, we would like to remark that Condition (ii) is satisfied by a wide class of Lévy processes. Importantly, Condition (ii) allows the distribution to have a discrete component. For example, if where is a compound Poisson process (with absolutely continuous jump size distribution), then has a point mass at and where is absolutely continuous. In this case, itself is not absolutely continuous, but is absolutely continuous.

Condition (iii) is concerned with smoothness of the scaled Lévy density . Condition (iii) allows the Lévy density to have a “cusp” at the origin. For example, a Gamma process has Lévy density for some ; in this case, the Lévy density itself is discontinuous (at the origin), but the scaled version is globally Lipschitz continuous. Condition (iv) is concerned with the kernel function . We assume that is a -th order kernel, but allow for the possibility that . We will provide examples of kernel functions satisfying Condition (iv) in Remark 4.2 below. It is worth mentioning that since the Fourier transform of has compact support, the support of the kernel function itself is necessarily unbounded (which is a consequence of the Paley-Wiener theorem; see Stein and Weiss (1971), Theorem 4.1), and we will use global regularity of the scaled Lévy density to suitably bound the deterministic bias, despite that we focus on constructing confidence bands on a compact set that does not intersect the origin. It could be possible to replace Condition (iii) by a “local” smoothness condition on , but we shall keep current Condition (iii) for the simplicity of the exposition.

Condition (v) is concerned with the bandwidth and the time span . The condition ensures that (see Lemma A.2). The condition is an “undersmoothing” condition. Inspection of the proof of Theorem 4.1 shows that, without the condition , we have that

where the term comes from the deterministic bias. The right hand side is optimized by choosing , and the optimal rate for is . For our confidence bands to be valid, however, we have to choose bandwidths of smaller order (by factors) than the optimal one for estimation under the sup-norm, so that the bias term is negligible relative to the “variance” or stochastic term. Undersmoothing bandwidths are commonly used in construction of confidence bands. See Section 5.7 in Wasserman (2006) for related discussions. For example, if we choose , then Condition (v) reduces to

| (4.2) |

where the condition ensures that .

Condition (vi) is concerned with the pilot estimator of . Since the set is away from the origin, if as , then , so that the pilot estimator need not be even consistent (e.g. we may take ). Note that as long as , the Fourier transform is -times continuously differentiable, so that as (however, as noted before, in our simulations studies, we found that, when , using a proper estimator for improves upon the empirical performance of the estimator and the confidence bands).

The following theorem derives a Gaussian approximation result. Recall that a Gaussian process is a tight random variable in if and only if is totally bounded for the intrinsic pseudo-metric for , and has sample paths almost surely uniformly -continuous (cf. van der Vaart and Wellner, 1996, p.41). In that case, we say that is a tight Gaussian random variable in .

Theorem 4.1 (Gaussian approximation).

Under Assumption 4.1, for each sufficiently large , there exists a tight Gaussian random variable in with mean zero and covariance function

for , and such that as ,

The distribution of the Gaussian process that appears in Theorem 4.1 changes with , and so the approximation is only an “intermediate” one. However, such an intermediate Gaussian approximation is sufficient to prove validity of bootstraps (cf. Chernozhukov et al., 2014b). Building on Theorem 4.1, the following theorem formally establishes asymptotic validity of the two bootstrap confidence bands.

Theorem 4.2 (Validity of bootstrap confidence bands).

Remark 4.1.

For example, if we choose , then provided that (4.2) is satisfied, the supremum width of the band is .

The proofs of Theorems 4.1 and 4.2 build on non-trivial applications of the intermediate Gaussian and bootstrap approximation theorems developed in Chernozhukov et al. (2014a, b, 2016). We would like to point out here that there are several non-trivial steps in proving Theorems 4.1 and 4.2. For example, we will require to show that , but since the increment distribution may have a discrete component and degenerates to as , and changes with and has unbounded support, lower bounding the variance function is non-trivial. Second, a crucial fact in the proofs of Theorems 4.1 and 4.2 is that the function class

| (4.3) |

is a Vapnik-Chervonenkis (VC) type class. In view of Lemma 1 in Kato and Sasaki (2016), it is not difficult to verify that the function class (4.3) is VC type for an envelope function of the form ; however, using this envelope function will require more restrictive moment conditions on (we will require at least finite eighth moment of ) and additional conditions on the smoothness level depending on the moments conditions on . In fact, although it is not apparent, it turns out that, under our assumption, the function is bounded uniformly in and . So, we will verify that the function class (4.3) is VC type for a constant envelope function, which requires a different and non-trivial idea; cf. Lemma A.7.

Remark 4.2 (Examples of kernel functions).

Construction of a kernel function satisfying Condition (iv) is typically done by specifying its Fourier transform . Let be a function that is even (i.e., ), supported in , and -times continuously differentiable, and such that

Then the function is real-valued, as (which follows from changes of variables), so that is integrable, and

Here, since is even, if is even, we also have . Examples of include: for , and

| (4.4) |

for and . For the latter case, is infinitely differentiable with for all , so that its inverse Fourier transform , called a flap-top kernel, is of infinite order, i.e., for all integers (cf. McMurry and Politis, 2004).

4.2. Discussions on Condition (ii) in Assumption 4.1

In this subsection, we provide primitive regularity conditions that guarantee Condition (ii) in Assumption 4.1. We make the following assumption.

Assumption 4.2.

Assume that is continuous; ; and is positive on for some sufficiently small such that . Furthermore, there exists such that the signed measure has a Lebesgue density bounded (in absolute value) by for all sufficiently small for some constant .

Assumption 4.2 ensures Condition (ii) in Assumption 4.1 to hold.

Remark 4.3.

The first part of Assumption 4.2 is not restrictive. Recall that we are assuming finiteness of the fourth moment of in Assumption 4.1, so that the requirement that appears to be innocuous. Proposition 16 in Nickl et al. (2016) provides primitive regularity conditions that ensure that has a density bounded uniformly in ; see Assumption 15 in Nickl et al. (2016) (we allow for the density of to grow like to cover cases where and the Lévy density behaves like near the origin; see below). In particular, Assumption 15 in Nickl et al. (2016) covers many of basic examples of Lévy processes.

For example, consider the following two simple cases:

(a) ; or (b) and .

( together with the assumption that ensure that .)

For Case (a), in view of together with the fact that is integrable, a Lebesgue density of exists and is given by

Since , we see that

which shows that the density of is bounded uniformly in .

For Case (b), observe that with , and

Applying the Fourier inversion, we see that has a Lebesgue density

which is bounded (in absolute value) by . Hence, in these two cases, has a Lebesgue density bounded uniformly in for some . For other more complicated cases, we refer to Proposition 16 in Nickl et al. (2016).

For the symmetric tempered stable process with stability index and the Normal Inverse Gaussian process discussed in the next section, whose Lévy densities behave like near the origin, Proposition 16 in Nickl et al. (2016) appears not to be directly applicable. To cover those cases, we present the following lemma.

Lemma 4.1.

Suppose that and the Lévy density satisfies that for some constants ,

for all . Then the signed measure has a Lebesgue density bounded (in absolute value) by for all sufficiently small for some constant .

5. Examples

In this section, we provide some examples of Lévy processes that satisfy Conditions (i)-(iii) in Assumption 4.1. For detailed properties of Lévy processes discussed below, we refer to Cont and Tankov (2004). The first four examples are purely non-Gaussian Lévy processes (i.e., ), and we allow them to have drift terms.

Example 5.1 (Compound Poisson process).

A compound Poisson process with drift is a stochastic process of the form , where is a Poisson process with constant intensity and is a sequence of i.i.d. random variables with common distribution (jump size distribution) independent of . We assume that has Lebesgue density . In this case, the characteristic exponent is , and so the Lévy density is . Conditions (i) and (iii) can be directly translated to conditions on . From Proposition 4.1 and Remark 4.3, Condition (ii) is satisfied if is continuous, , and is positive on for some such that .

For example, the jump-part of the Merton model (Merton, 1976) is a compound Poisson process with jump size distribution for some and , for which it is not difficult to verify that Conditions (i)-(iii) are satisfied with arbitrary large , and any compact set in . The jump-part of the Kou model (Kou, 2002) is a compound Poisson process with jump size density

for some and . Let be any compact set in , , and if , and , respectively. Then, it is not difficult to verify that Conditions (i)-(iii) are satisfied with if and , and otherwise.

A compound Poisson process is a process of finite activity, i.e., has only finitely many jumps on any bounded time interval.

Example 5.2 (Tempered stable process).

A tempered stable process with index is a Lévy process with Lévy density

where , and . We assume that the stability index is restricted to . Let be any compact set in , , and if , , and , respectively. It is clear that Conditions (i) and (iii) are satisfied with if , and , and otherwise. For example, to see that is -Hölder continuous in the latter case, it suffices to verify that is -Hölder continuous on , which can be verified as follows: for any ,

where we have used that .

If , then since is bounded, in view of Remark 4.3, with has a Lebesgue density bounded uniformly in . If , then Assumption 15 Case (iii) in Nickl et al. (2016) is satisfied for with , and hence Proposition 16 in Nickl et al. (2016) yields that has a Lebesgue density bounded uniformly in . Therefore, by Proposition 4.1, Condition (ii) is satisfied in either case.

The tempered stable process includes Gamma, Inverse Gaussian, and Variance Gamma processes as special cases. A Gamma process corresponds to the case with and ; an Inverse Gaussian process corresponds to the case with and ; and a Variance Gamma process corresponds to the case with and .

The tempered stable process is a process of infinite activity, i.e., has infinitely many jumps on any bounded time interval.

The Lévy density in each of Examples of 5.1 and 5.2 has finite first moment, and therefore sample paths of the process have finite variation on any bounded time interval (Sato, 1999, Theorem 21.9). On the other hand, the following two examples have infinite variation on any bounded time interval.

Example 5.3 (Symmetric tempered stable process with ).

In the previous example, consider the case where , and , i.e.,

In this case, Condition (i) is trivially satisfied, and since extends to a Lipschitz continuous function on as , Condition (iii) is satisfied with . It is not difficult to verify that the assumption in Lemma 4.1 is satisfied, and therefore, by Proposition 4.1, Condition (ii) is satisfied for any compact set in .

Example 5.4 (Normal Inverse Gaussian process).

A Normal Inverse Gaussian (NIG) process is a purely non-Gaussian Lévy process with Lévy density

where is the modified Bessel function of the second kind with order , and has integral representation

The parameters are restricted such that and . Since decays like as , Condition (i) is satisfied. By a change of variables, we have that

Since the integral on the right hand side is well-defined for , extends to a continuous function on as

| (5.1) |

Furthermore, it is not difficult to verify that the assumption in Lemma 4.1 is satisfied, and therefore, by Proposition 4.1, Condition (ii) is satisfied for any compact set in .

Finally, it appears to be difficult to directly verify Condition (iii) to the NIG process, but inspection of the proofs of Theorems 4.1 and 4.2 shows that Condition (iii) is used only to bound the deterministic bias . Fortunately, for the NIG process, it is possible to directly bound the deterministic bias for any ; see below. Therefore, the conclusions of Theorems 4.1 and 4.2 hold true for the NIG process with any , provided that other technical conditions (Conditions (iv)-(vi)) are satisfied.

Lemma 5.1.

Let be as in (5.1), and let be an integrable function such that and . Then for any and any nonempty compact set in , we have that , where denotes the convolution.

Example 5.5 (Brownian motion + purely non-Gaussian Lévy process).

Let , where , is a standard Brownian motion, and is a purely non-Gaussian Lévy process independent of (with drift). We assume that is one of purely non-Gaussian Lévy processes in Examples 5.1–5.4. For the compound Poisson process case, we assume that , and Conditions (i) and (iii) are satisfied for . In view of Remark 4.3, it is clear that Conditions (i)-(iii) are satisfied with given in Examples 5.1–5.4, as long as is properly chosen.

6. Simulation results

6.1. Simulation framework

In this section, we present simulation results to evaluate the finite-sample performance of the proposed confidence bands. We consider the following data generating processes.

-

(1)

Brownian motion + compound Poisson process. Let , where is a standard Brownian motion, and is a compound Poisson process (see Example 5.1). The Poisson process has intensity . We set or . We consider two types of jump size distributions. For the first case, is the density of the normal distribution and the Lévy density is . We denote this case by BCN(). For the second case, is the density of the Laplace distribution with location and scale , and the Lévy density is . We denote the latter case by BCL(). For BCN() and BCL(), we take .

If , then reduces to the compound Poisson process , for which we set . In case of , we estimate by the TRV estimator with and (see Example 2.1). We also examined the performance of the confidence bands with estimated in case of , but the simulation results are almost identical to those under . Hence, we only report the simulation results with in case of . The same comment applies to the Gamma process case.

-

(2)

Gamma process. A Gamma process is a pure jump Lévy process with Lévy density (see Example 5.2). We denote this case by G(). The increment distribution is the Gamma distribution with shape parameter and scale parameter . For the Gamma process case, we take .

We use the kernel function whose Fourier transform is specified by (4.4), where we choose and . We consider the following configurations for the sample size and the time span : or , and or . Here ranges from to .

Remark 6.1.

From a theoretical point of view, we do not have to estimate even when (see the discussion on Condition (vi) in Assumption 4.1). However, in case of , we found that the estimate with tends to be less precise near the origin than that with . So, from a practical point of view, we recommend to estimate when implementing our methods.

6.2. Bandwidth selection

Now, we discuss bandwidth selection. We adapt an idea of Bissantz et al. (2007) on bandwidth selection in density deconvolution. From a theoretical point of view, for our confidence bands to work, we have to choose bandwidths that are of smaller order than the optimal rate for estimation under the the sup-norm loss. At the same time, choosing a too small bandwidth results in a too wide confidence band. Therefore, heuristically, we should choose a bandwidth “slightly” smaller than the optimal one that minimizes the -distance .

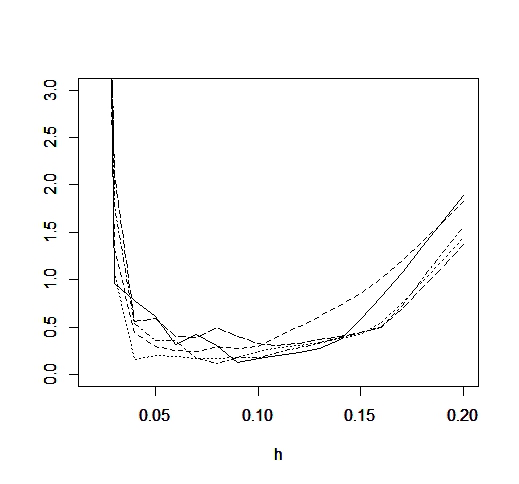

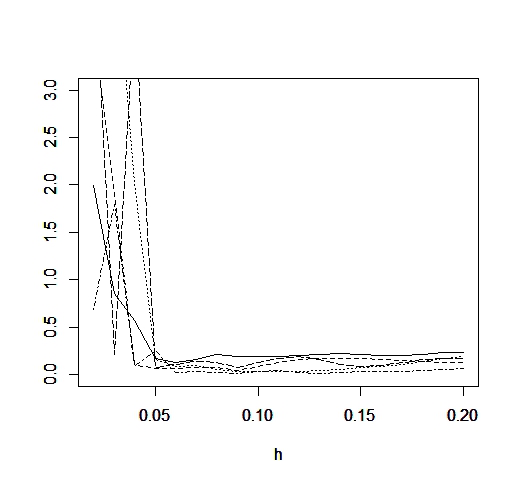

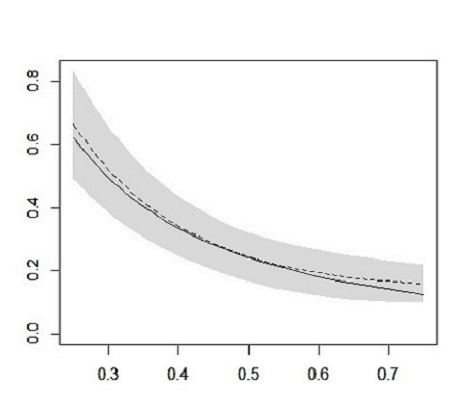

Let denote the spectral estimate with bandwidth . Figure 3 depicts five realizations of the -distance with different bandwidth values for BCN(0,1/2) with and G(0.2,1), both with . It is observed that as increases, is sharply decreasing for (say), and for , is slowly increasing. We aim to choose a bandwidth slightly smaller than . Of course, the problem is that the value of is unknown to us. Now, Figure 4 depicts five realizations of the -distance between the estimates of with adjacent bandwidth values. To be precise, we prepare grids of bandwidths , and compute the -distance ; Figure 4 depicts those values with . It is observed that shape of partly “mimics” that of ; in fact, is sharply decreasing for , but for , is almost flat. Our idea of bandwidth selection is as follows: starting from , choose the first such that is below for some ; our choice of the bandwidth is . Heuristically, this rule would choose a bandwidth “slightly” smaller than (as long as the threshold value is reasonably chosen). Formally, we employ the following rule for bandwidth selection.

-

(1)

Set a pilot bandwidth for some , and make a list of candidate bandwidths for .

-

(2)

Choose the smallest bandwidth such that the adjacent -distance is smaller than for some

In this simulation study, we choose , and . In practice, it is also recommended to make use of visual information on how behaves as increases when determining the bandwidth.

Remark 6.2.

We have also examined a version of the bandwidth selection rule with replaced by , but found that the rule described above shows better performances in terms of coverage probabilities. So, we present simulation results with the above rule.

|

|

6.3. Simulation results

In this simulation study, we focus on the multiplier bootstrap (MB) confidence band . We present simulated coverage probabilities of the MB confidence band together with simulated values of the expected mean width of the band , where denotes the Lebesgue measure for a measurable set . The number of Monte Carlo repetitions is . To compute the critical value , we generate multiplier bootstrap replications for each run of the simulations.

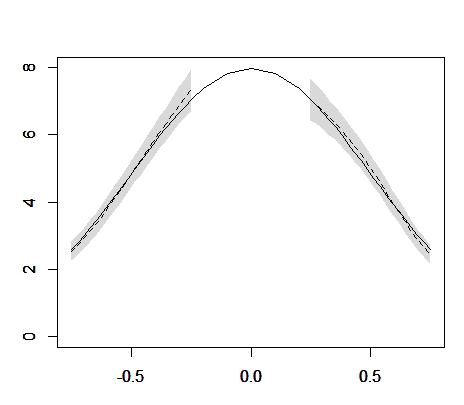

Tables 1 and 2 present simulation results for models BCN() and BCL() with , and G() under , and . Comparing BCN() with BCL() and G(0.2,1), we find that BCN() is apt to give more accurate coverage probabilities. This is partly due to the smoothness of Lévy densities. Since the normal density is smoother around the origin than those of Laplace and Gamma-Lévy densities, the estimate for BCN tends to be less biased than that for other cases. Figure 5 depicts MB confidence bands for BCN() (left), BCL() (center), both with , and G(0.2,1) (right) with (top row) and (bottom row), based on one realization for each model. Figure 6 depicts MB confidence bands for BCN() and BCL(), both with . As seen from Figures 5 and 6, the width of the MB confidence band tends to increase near the origin when the Brownian component is present (i.e., ). This partly comes from the difficulty of distinguishing small jumps from fluctuations due to the Brownian component.

Overall, the simulated coverage probabilities are reasonably close to the nominal coverage probabilities, although in some cases there are rooms for improvement. We also find that for every case, the expected mean width tends to decrease as increases, which is consistent with our theory. Notably, for BCN and BCL, the MB confidence bands exhibit similar performance for either case where the Brownian component is absent () or present ().

| Model | |||||||

|---|---|---|---|---|---|---|---|

| Cov. Prob. | BCN(0,1/2) | BCN(0,1/2) | BCL(0,1/2) | BCL(0,1/2) | G(0.2,1) | ||

| 0.90 | 0.005 | 0.816 | 0.824 | 0.812 | 0.824 | 0.812 | |

| (1.150) | (1.867) | (0.818) | (1.294) | (0.317) | |||

| 0.828 | 0.836 | 0.820 | 0.808 | 0.812 | |||

| (0.816) | (1.311) | (0.573) | (0.908) | (0.213) | |||

| 0.01 | 0.824 | 0.840 | 0.820 | 0.816 | 0.820 | ||

| (0.787) | (1.285) | (0.560) | (0.922) | (0.195) | |||

| 0.868 | 0.856 | 0.824 | 0.796 | 0.816 | |||

| (0.545) | (0.905) | (0.399) | (0.659) | (0.131) | |||

| 0.95 | 0.005 | 0.908 | 0.912 | 0.908 | 0.916 | 0.908 | |

| (1.276) | (2.071) | (0.919) | (1.453) | (0.364) | |||

| 0.912 | 0.924 | 0.908 | 0.904 | 0.920 | |||

| (0.908) | (1.455) | (0.643) | (1.019) | (0.245) | |||

| 0.01 | 0.916 | 0.928 | 0.912 | 0.916 | 0.912 | ||

| (0.876) | (1.428) | (0.631) | (1.037) | (0.226) | |||

| 0.932 | 0.936 | 0.920 | 0.876 | 0.904 | |||

| (0.607) | (1.004) | (0.449) | (0.740) | (0.153) | |||

| 0.99 | 0.005 | 0.972 | 0.976 | 0.968 | 0.984 | 0.964 | |

| (1.532) | (2.441) | (1.110) | (1.742) | (0.454) | |||

| 0.988 | 0.984 | 0.980 | 0.976 | 0.984 | |||

| (1.090) | (1.712) | (0.771) | (1.235) | (0.301) | |||

| 0.01 | 0.972 | 0.988 | 0.984 | 0.988 | 0.980 | ||

| (1.044) | (1.695) | (0.767) | (1.265) | (0.285) | |||

| 0.984 | 0.992 | 0.992 | 0.964 | 0.988 | |||

| (0.742) | (1.184) | (0.540) | (0.892) | (0.193) | |||

| Model | ||||||

|---|---|---|---|---|---|---|

| Cov. Prob. | BCN(1,1/2) | BCN(1,1/2) | BCL(1,1/2) | BCL(1,1/2) | ||

| 0.90 | 0.005 | 0.804 | 0.804 | 0.832 | 0.828 | |

| (1.447) | (2.425) | (1.002) | (1.536) | |||

| 0.808 | 0.796 | 0.820 | 0.816 | |||

| (1.050) | (1.756) | (0.699) | (1.070) | |||

| 0.01 | 0.812 | 0.808 | 0.824 | 0.804 | ||

| (1.113) | (1.900) | (0.870) | (1.303) | |||

| 0.824 | 0.804 | 0.816 | 0.792 | |||

| (0.811) | (1.409) | (0.590) | (0.946) | |||

| 0.95 | 0.005 | 0904 | 0.904 | 0.912 | 0.908 | |

| (1.606) | (2.692) | (1.119) | (1.720) | |||

| 0.908 | 0.892 | 0.916 | 0.916 | |||

| (1.165) | (1.945) | (0.784) | (1.199) | |||

| 0.01 | 0.912 | 0.908 | 0.920 | 0.904 | ||

| (1.241) | (2.116) | (0.975) | (1.460) | |||

| 0.916 | 0.896 | 0.916 | 0.896 | |||

| (0.901) | (1.568) | (0.661) | (1.056) | |||

| 0.99 | 0.005 | 0.956 | 0.968 | 0.956 | 0.988 | |

| (1.840) | (3.113) | (1.367) | (2.067) | |||

| 0.960 | 0.972 | 0.972 | 0.980 | |||

| (1.392) | (2.301) | (0.947) | (1.460) | |||

| 0.01 | 0.972 | 0.976 | 0.984 | 0.976 | ||

| (1.478) | (2.465) | (1.149) | (1.743) | |||

| 0.976 | 0.964 | 0.964 | 0.968 | |||

| (1.059) | (1.812) | (0.798) | (1.273) | |||

|

|

|

|

7. Conclusion

In this paper, we have developed bootstrap methods to construct uniform confidence bands for spectral estimators of Lévy densities from high-frequency observations. We have studied two bootstrap methods, namely, Gaussian multiplier and empirical bootstraps, and established asymptotic validity of the proposed confidence bands. Notably, the proposed confidence bands are shown to be valid for a wide class of Lévy processes. We have also developed a practical method to choose a bandwidth.

Appendix A Proofs of Theorems 4.1 and 4.2

In what follows, we always assume Assumption 4.1. The proofs rely on modern empirical process theory. For a probability measure on a measurable space and a class of measurable functions on such that , let denote the -covering number for with respect to the -seminorm . See Section 2.1 in van der Vaart and Wellner (1996) for details. Let denote the equality in distribution.

A.1. Auxiliary lemmas

We begin with proving some auxiliary lemmas that will be used to prove Theorems 4.1 and 4.2. We will freely use the following moment estimates for .

Lemma A.1.

We have

Proof.

This follows from the observations that and . ∎

Lemma A.2.

We have .

Proof.

Recall that . From Taylor’s theorem, for any , so that uniformly in . Therefore, we conclude that

This completes the proof. ∎

Lemma A.3.

We have .

Proof.

From the previous lemma, it is not difficult to verify that and . By changes of variables, observe that

Since is supported in , to show that , it suffices to verify that

To see this, observe that

This yields that

where we have used that . Next, observe the following identities

The second identity follows from the following (straightforward but tedious) calculations:

Now, noting that for , we conclude that

Likewise, we have that . This completes the proof. ∎

Lemma A.4.

For , we have that .

Proof.

This follows from Theorem 1 in Kappus and Reiß (2010), which shows that for the weight function ,

for under our assumption. Since

we conclude that

The desired result follows from Markov’s inequality. ∎

so that with probability approaching one, . Hence, with probability approaching one, is well-defined on as the distinguished logarithm (Chung, 2001, Theorem 7.6.2).

Lemma A.5.

We have

Proof.

The lemma essentially follows from the proof of Proposition 7 in Nickl et al. (2016). For the sake of completeness, we provide a proof of the lemma. Rewrite as . Let , and observe that for any ,

for some . Since is bounded in a neighborhood of the origin and (which follows from Lemmas A.2 and A.4), we have that

Next, we shall bound for . Since and , we have that

| (A.1) | |||

| (A.2) |

In view of the identities

we conclude from Lemma A.4 that for , which yields that

Finally, observe that

From the bounds (A.1) and (A.2), together with Lemma A.4, we have that

Taking these together, we conclude that

| (A.3) |

We shall verify that the right hand side is . Observe that

Since , we have that . On the other hand, as , . Since , we have that , which implies that . This completes the proof. ∎

Lemma A.6.

Recall that . Then for sufficiently large .

Proof.

Since , we have that . Next, observe that for any . Using this inequality and recalling that has distribution with , we have that

Since , it suffices to verify that

for sufficiently large . Since and by Plancherel’s theorem, we have that

From Lemma A.3, we have that , so that for ,

up to a constant independent of . The right hand side is approaching zero as , so that by taking sufficiently large, we have that

for all . Hence, for sufficiently large such that ,

by Condition (ii) in Assumption 4.1. This completes the proof. ∎

Consider the function class

Observe that

Since by Lemma A.3 and is compact, each of the three terms on the right hand side is bounded (as a function of ) uniformly in and . Choose constants independent of such that and (cf. Lemma A.6). Without loss of generality, we may assume that . Then functions in are bounded by

The next lemma provides a bound on the uniform covering number for the function class .

Lemma A.7.

There exist constants independent of such that

| (A.4) |

where is taken over all finitely discrete distributions on .

The proof of this lemma relies on the following lemma.

Lemma A.8 (Giné and Nickl (2016), Lemma 3.2.16).

Let be a function of bounded variation, i.e.,

and consider the function class . Then there exist universal constants such that

where is taken over all finitely discrete distributions on .

Proof of Lemma A.7.

Consider the auxiliary function classes

Since , is compact, and , the desired conclusion follows by verifying that there exist constants independent of such that

for . To this end, in view of Lemma A.8, it suffices to verify that, for , the total variations of are bounded in , i.e.,

This follows from observations that , and by Lemma A.3. ∎

Lemma A.9.

Let . Then , where denotes the convolution.

Proof.

Observe that by a change of variables, . If , then by Taylor’s theorem, for any ,

for some , where by convention. Since is -Hölder continuous, we have that . Now, since for , we have that for any ,

where by convention. This completes the proof. ∎

A.2. Proof of Theorem 4.1

Observe that

| (A.5) |

For the first and third terms, we have that (by Lemma A.9) and under our assumption. For the second term , Lemma A.5 yields that

uniformly in , and observe that the first term on the right hand side can be expressed as

Therefore, since , we have that

| (A.6) |

uniformly in .

Now, we approximate by the supremum in absolute value of a tight Gaussian random variable in with mean zero and the same covariance function as . To this end, we shall employ Theorem 2.1 in Chernozhukov et al. (2016). Consider the empirical process

The covering number bound (A.4) ensures the existence of a tight Gaussian random variable in with mean zero and the same covariance function as . Extend linearly to , and observe that . Note that from Theorem 3.7.28 in Giné and Nickl (2016), extends to the linear hull of in such a way that has linear sample paths, so that , and in addition has uniformly continuous paths on the symmetric convex hull of . It is not difficult to verify that the covering number of is at most twice that of . In particular, is a tight Gaussian random variable in with mean zero and the same covariance function as .

Next, since has distribution such that and , we have that

| (A.7) |

so that . On the other hand, since ,

Therefore, applying Theorem 2.1 in Chernozhukov et al. (2016) to with , and sufficiently large (in the notation used in the cited theorem), yields that there exists a random variable with such that

| (A.8) |

Now, for , define

and observe that is a tight Gaussian random variable in with mean zero and the same covariance function as . We will derive the conclusion of the theorem from (A.8). To this end, the following anti-concentration inequality will play a crucial role: for any ,

| (A.9) |

See Corollary 2.1 in Chernozhukov et al. (2014b); see also Theorem 3 in Chernozhukov et al. (2015). From the result (A.8), there exits a sequence of constants such that . Since and , we have that

for any . Likewise, we have

for any . Now, from the covering number bound (A.4) together with the fact that for all , Dudley’s entropy integral bound (cf. van der Vaart and Wellner, 1996, Corollary 2.2.8) yields that

This completes the proof.

∎

A.3. Proof of Theorem 4.2

We first prove the following technical lemma.

Lemma A.10.

.

Proof.

From Lemma A.4, we have that , so that it is not difficult to verify that and . Hence

| (A.10) |

and likewise

Since , we have that

uniformly in . Furthermore, since and

it remains to prove that . To this end, since , it suffices to prove that

| (A.11) | |||

| (A.12) |

To prove (A.11), we make use of Corollary 5.1 in Chernozhukov et al. (2014a). Let . Observe that , and . From the covering number bound (A.4) together with Corollary A.1 in Chernozhukov et al. (2014a), there exist constants independent of such that

where is taken over all finitely discrete distributions on . Therefore, from Corollary 5.1 in Chernozhukov et al. (2014a), the expectation of the left hand side on (A.11) is bounded by

For (A.12), from the covering number bound (A.4), Theorem 2.14.1 in van der Vaart and Wellner (1996) shows that the expectation of the left hand side on (A.12) is bounded by

This completes the proof. ∎

Proof of Theorem 4.2.

We separately prove the theorem for the multiplier and empirical bootstraps.

Multiplier bootstrap case: We first verify that

| (A.13) |

uniformly in . From (A.10),

Next, observe that

which yields that

Therefore, we have proved (A.13).

Now, since by Lemma A.10, we have that

| (A.14) |

uniformly in . We wish to show that

| (A.15) |

To this end, we shall apply Theorem 2.2 in Chernozhukov et al. (2016) to . Let

Applying Theorem 2.2 in Chernozhukov et al. (2016) to with , and sufficiently large (in the notation used in the cited theorem), yields that there exists a random variable whose conditional distribution given is identical to the distribution of , i.e., for all almost surely, and such that

which implies that there exists a sequence of constants such that

Since , we have that

uniformly in . From the anti-concentration inequality (A.9) together with the bound , we conclude that

uniformly in . Likewise, we have uniformly in . Hence, we have proved (A.15).

From (A.15) together with the bound , we see that . So, from (A.14), we have that

uniformly in . In view of the proof of (A.15), we conclude that

| (A.16) |

Now, we wish to show that . We begin with noting that

Recall that from the conclusion of Theorem 4.1 together with the bound , we have that . Observe that

uniformly in . Hence, using the conclusion of Theorem 4.1 together with the anti-concentration inequality (A.9), we have that

| (A.17) |

From the result (A.16), using an argument similar to Step 3 in the proof of Theorem 2 in Kato and Sasaki (2016), we can find a sequence of constants such that

| (A.18) |

with probability approaching one. Therefore,

Note that from the anti-concentration inequality, the distribution function of is continuous, so that the equality holds. Likewise, we have .

Finally, the Borell-Sudakov-Tsirelson inequality (van der Vaart and Wellner, 1996, Lemma A.2.2) yields that

which implies that from (A.18). Therefore, the supremum width of the band is

where the bound follows from (A.7). This completes the proof for the multiplier bootstrap case.

Empirical bootstrap case: Note that the bootstrap process can be expressed as

where each is the number of times that is “redrawn” in the bootstrap sample, and the vector is multinomially distributed with parameters and (probabilities) independent of the data (cf. van der Vaart and Wellner, 1996, Section 3.6). Given this expression, the proof for the empirical bootstrap case is almost identical to that for the multiplier bootstrap case, where we use Theorem 2.3 in Chernozhukov et al. (2016) instead of their Theorem 2.2. We omit the detail for brevity. ∎

Appendix B Additional proofs

B.1. Proof of Lemma 2.1

The Lévy process has the following decomposition (Lévy-Itô decomposition)

where is a standard Brownian motion and is a Poisson random measure on , independent of , with intensity measure . Depending on the value of , we set

Let . Consider the following decomposition for :

We shall evaluate for . Since with

we have that

which yields that

Furthermore, for any , we have that , which yields that

Taking , we have that . Finally, applying Lemma 13.2.6 in Jacod and Protter (2012) with , and in the notation used in the lemma, we conclude that . These estimates yield the desired result. ∎

B.2. Proof of Proposition 4.1

Since is a also Lévy process with the same Lévy density as , without loss of generality, we may assume , and we shall verify Condition (ii) for . In this proof, slightly abusing notation, we shall use the same symbol for a measure and its Lebesgue density if the latter exists. Let denote the -norm with respect to the Lebesgue measure. We first note that since is absolutely continuous, for any integer , is also absolutely continuous with density (this means that the density of the signed measure is given by the multiple of with the Lebesgue density of the signed measure ). Furthermore, boundedness of ensures that , which in turn ensures that has finite second moment. In what follows, we will freely use some basic results on convolutions and Fourier transforms of finite signed Borel measures on ; cf. Folland (1999, Section 8.6).

Verification of : The proof is similar to that of Proposition 14 in Nickl et al. (2016). We first note that by infinite divisibility. Using this property, we have that , i.e.,

Applying the Fourier inversion, we have that

| (B.1) |

where and denotes the convolution. Using the rule for finite signed Borel measures on such that and , we have that

Since (by assumption), , and , we have that

Now, if , then we have that (cf. Remark 4.3), so that . On the other hand, if , then from (B.1), we have that

where we have used that . In either case, we have that .

For , we have that

Verification of for some . We divide the proof into two steps.

Step 1. We first consider the case where , and ( ensures that ). In this case, the characteristic exponent is

Observe that , and applying the Fourier inversion to , we have that , so that . From (B.1),

and . Since for any by Markov’s inequality, we have that . So,

which shows that . This leads to the desired result with .

Step 2. Next, we consider the general case. Decompose the Lévy measure into , and observe that is a finite, non-zero measure with . Then the characteristic exponent can be decomposed as

where . From this decomposition, we have

where is a Lévy process with Lévy measure , and is a compound Poisson process with jump intensity and jump size distribution independent of . Let denote the distributions of , respectively, so that . Since is a compound Poisson distribution with absolutely continuous jump distribution, we obtain the decomposition where is absolutely continuous, so that . Since both and are absolutely continuous, so is , and

Now, since and from the result of Step 1, we have that and so . Furthermore, since by Markov’s inequality, we have that

which implies that . This leads to the desired result with . ∎

B.3. Proof of Lemma 4.1

The proof is a modification of that of Nickl et al. (2016), Proposition 16 Case (iv). We will obey the notational convention used in the proof of Proposition 4.1. We first note that, under the assumption of the lemma, the Lévy measure is infinite, since for ,

and taking shows that the far left hand side is infinite. Then, Theorem 27.7 in Sato (1999) yields that is absolutely continuous with respect to the Lebesgue measure, and by the Fourier inversion, we have that . Observe that

Since , we have that

Furthermore, since there exists a small constant such that for all , we have that

From these estimates, it is seen that . On the other hand, since

for , we have that

where . This completes the proof. ∎

B.4. Proof of Lemma 5.1

Without loss of generality, we may assume . Observe that

Pick any , and suppose that . Then

By symmetry, this inequality holds for any .

Now, by a change of variables, we have that . Observe that, since is integrable around the origin,

up to a constant that depends only on . Therefore, we conclude that

This completes the proof. ∎

Appendix C Convergence rates of under weighted sup-norm on

In this section, we study convergence rates of the spectral estimator under the weighted sup-norm . For this purpose, we work with conditions similar those in Assumption 4.1.

Proposition C.1.

Suppose that for some ; there exists such that the measure has Lebesgue density such that ; for some , is -times differentiable, and is -Hölder continuous, where is the integer such that ; let be an integrable function that satisfies (4.1). Furthermore, suppose that and . Then

where

If in addition and , then

Proof.

Recall from the decomposition (A.5) that

Lemma A.9 yields that . Furthermore, the expansion (A.6) holds under the assumption of the proposition, and therefore,

uniformly in . It remains to prove that

| (C.1) |

To this end, we shall apply Corollary 5.1 in Chernozhukov et al. (2014a) to the function class

Under the present assumption, we still have that , and choose a constant independent of such that . Let , which is an envelope function for . From the proof of Lemma (A.8), it is seen that is of bounded variation with , so that by Lemma A.8 together with a simple covering number calculation, we have that for some constants independent of ,

Observe that (cf. (A.7)), and

where we have used that , which follows from applying Theorem 1.1 in Figueroa-López (2008) with . Therefore, applying Corollary 5.1 in Chernozhukov et al. (2014a) to , we conclude that

which leads to (C.1).

The last assertion is trivial, and the proof is completed. ∎

References

- Aït-Sahalia (2004) Aït-Sahalia, Y. (2004). Disentangling diffusions from jumps. J. Financial Economics 74 487-528.

- Aït-Sahalia and Jacod (2007) Aït-Sahalia, Y. and Jacod, J. (2007). Volatility estimators for discretely sampled Lévy processes. Ann. Statist. 37 2202-2244.

- Aït-Sahalia and Jacod (2014) Aït-Sahalia, Y. and Jacod, J. (2014). High-Frequency Financial Econometrics. Princeton University Press.

- Aït-Sahalia and Xiu (2017) Aït-Sahalia, Y. and Xiu, D. (2017). A Hausman test for the presence of noise in high frequency data. J. Econometrics, to appear.

- Barndorff-Nielsen and Shephard (2004) Barndorff-Nielsen, O.E. and Shephard, N. (2004). Power and bipower variation with stochastic volatility and jumps. J. Financial Econometrics 2 1-48.

- Bickel and Rosenblatt (1973) Bickel, P. and Rosenblatt, M. (1973). On some global measures of the deviations of density function estimates. Ann. Statist. 1 1071-1095. Correction (1975) 3 1370.

- Bec and Lacour (2015) Bec, M. and Lacour, C. (2015). Adaptive pointwise estimation for pure jump Lévy processes. Stat. Inference Stoch. Process. 18 229-256.

- Belomestny (2011) Belomestny D. (2011). Statistical inference for time-changed Lévy processes via composite characteristic function estimation. Ann. Statist. 39 2205-2242.

- Belomestny and Reiß (2015) Belomestny, D. and Reiß, M. (2015). Estimation and calibration of Lévy models via Fourier methods. In: Lévy Matters IV (eds. D. Belomestny et al.) Springer, pp.1-76.

- Bertoin (1996) Bertoin, J. (1996). Lévy Processes. Cambridge University Press.

- Bissantz et al. (2007) Bissantz, N., Dümbgen, L., Holzmann, H., and Munk, A. (2007). Non-parametric confidence bands in deconvolution density estimation. J. Roy. Stat. Soc. Ser. B Stat. Methodol. 69 483-506.

- Bücher et al. (2017) Bücher, A., Hoffmann, M., Vetter, M., and Dette, H. (2017). Nonparametric tests for detecting breaks in the jump behaviour of a time-continuous process. Bernoulli 23 1335-1364.

- Bücher and Vetter (2013) Bücher, A. and Vetter, M. (2013). Nonparametric inference on Lévy measures and copulas. Ann. Statist. 41 1485-1515.

- Chen et al. (2010) Chen, S.X., Delaigle, A., and Hall, P. (2010). Nonparametric estimation for a class of Lévy processes. J. Econometrics 157 257-271.

- Chernozhukov et al. (2014a) Chernozhukov, V., Chetverikov, D., and Kato, K. (2014a). Gaussian approximation of suprema of empirical processes. Ann. Statist. 42 1564-1597.

- Chernozhukov et al. (2014b) Chernzhukov, V., Chetverikov, D., and Kato, K. (2014b). Anti-concentration and honest, adaptive confidence bands. Ann. Statist. 42 1787-1818.

- Chernozhukov et al. (2015) Chernozhukov, V., Chetverikov, D., and Kato, K. (2015). Comparison and anti-concentration bounds for maxima of Gaussian random vectors. Probab. Theory Related Fields 162 47-70.

- Chernozhukov et al. (2016) Chernozhukov, V., Chetverikov, D., and Kato, K. (2016). Empirical and multiplier bootstraps for suprema of empirical processes of increasing complexity, and related Gaussian couplings. Stochastic Process. Appl. 126 3632-3651.

- Chung (2001) Chung, K.-L. (2001). A Course in Probability Theory (3rd edition). Academic Press.

- Claeskens and Van Keilegom (2003) Claeskens, G. and Van Keilegom, I. (2003). Bootstrap confidence bands for regression curves and their derivatives. Ann. Statist. 31 1852-1884.

- Comte and Genon-Catalot (2009) Comte, F. and Genon-Catalot, V. (2009). Nonparametric estimation for pure jump Lévy processes based on high frequency data. Stochastic Process. Appl. 119 4088-4123.

- Comte and Genon-Catalot (2010) Comte, F. and Genon-Catalot, V. (2010). Nonparametric adaptive estimation for pure jump Lévy processes. Ann. Inst. H. Poincaré Probab. Stat. 46 595–617.

- Comte and Genon-Catalot (2011) Comte, F. and Genon-Catalot, V.(2011). Estimation for Lévy processes from high frequency data within a long time interval. Ann. Statist. 39 803-837.

- Comte and Genon-Catalot (2015) Comte, F. and Genon-Catalot, V. (2015). Adaptive estimation for Lévy processes. In: Lévy Matters IV (eds. D. Belomestny et al.) Springer, pp.77-177.

- Cont and Tankov (2004) Cont, R. and Tankov, P. (2004). Financial Modeling with Jump Processes. Chapman & Hall/CRC.

- Duval (2013) Duval, C. (2013). Density estimation for compound Poisson processes from discrete data. Stochastic Process. Appl. 123 3963-3986.

- van Es et al. (2007) van Es, B., Gugushvili, S. and Spreij, P. (2007). A kernel type nonparametric density estimator for decompounding. Bernoulli 13 672-694.

- Figueroa-López (2008) Figueroa-López J.E. (2008). Small-time moment asymptotics for Lévy processes. Statist. Probab. Lett. 78 3355-3365.

- Figueroa-López (2009) Figueroa-López, J.E. (2009). Nonparametric estimation for Lévy models based on discrete sampling. In: IMS Lecture Notes of the 3rd E.L. Lehmann Symposium 57, pp.117-146.

- Figueroa-Löpez (2011a) Figueroa-López, J.E. (2011a). Central limit theorems for the non-parametric estimation of time-changed Lévy models. Scand. J. Statist. 38 748-765.

- Figueroa-López (2011b) Figueroa-López, J.E. (2011b). Sieve-based confidence interval and bands for Lévy densities. Bernoulli 17 643-670.

- Folland (1999) Folland, G.B. (1999). Real Analysis (2nd Edition). Wiley.

- Giné and Nickl (2016) Giné, E. and Nickl, R. (2016). Mathematical Foundations of Infinite-Dimensional Statistical Models. Cambridge University Press.

- Gugushvili (2009) Gugushvili, S. (2009). Nonparametric estimation of the characteristic triplet of a discretely observed Lévy process. J. Nonparametric Statist. 21 321-343.

- Gugushvili (2012) Gugushvili, S. (2012). Nonparametric inference for discretely sampled Lévy processes. Ann. Inst. H. Poincaré Probab. Stat. 48 282-307.

- Hall (1991) Hall, P. (1991). On convergence rates of suprema. Probab. Theory Related Fields 89 447-455.

- Hoffmann and Vetter (2017) Hoffmann, M. and Vetter, M. (2017). Weak convergence of the empirical truncated distribution function of the Lévy measure of an Itô semimartingale. Stochastic Process. Appl., to appear.

- Jacod and Protter (2012) Jacod, J. and Protter, P. (2012). Discretization of Processes. Springer.

- Jacod and Reiß (2014) Jacod, J. and Reiß, M. (2014). A remark on the rates of convergence for integrated volatility estimation in the presence of jumps. Ann. Statist. 42 1131-1144.

- Johannes (2004) Johannes, M. (2004). The statistical and economic role of jumps in continuous-time interest rate models. J. Finance 59 227-260.

- Jongbload et al. (2005) Jongbloed, G., van der Meulen, F.H., and van der Vaart, A.W. (2005). Nonparametric inference for Lévy-driven Ornstein-Uhlenbeck processes. Bernoulli 11 759-791.

- Kappus (2014) Kappus, J. (2014). Adaptive nonparametric estimation for Lévy processes observed at low frequency. Stochastic Process. Appl. 124 730-758.

- Kappus and Reiß (2010) Kappus, J. and Reiß, M. (2010), Estimation of the characteristics of a Lévy process observed at arbitrary frequency. Statist. Neerlandica 64 314-328.

- Kato and Sasaki (2016) Kato, K. and Sasaki, Y. (2016). Uniform confidence bands in deconvolution with unknown error distribution. arXiv:1608.02251.

- Kato and Sasaki (2017) Kato, K. and Sasaki, Y. (2017). Uniform confidence bands for nonparametric errors-in-variables regression. arXiv:1702:03377.

- Komlós et al. (1975) Komlós, J., Major, P., and Tusnády, G. (1975). An approximation for partial sums of independent rv’s and the sample df I. Z. Warhsch. Verw. Gabiete 32 111-131.

- Konakov and Panov (2016) Konakov V. and Panov, V. (2016). Sup-norm convergence rates for Lévy density estimation. Extremes 19 371-403.

- Kou (2002) Kou, S. (2002). A jump-diffusion model for option pricing. Management Science 48 1086-1101.

- Mancini (2001) Mancini, C. (2001). Disentangling the jumps of the diffusion in a geometric jumping Brownian motion. Giornale dell’Istituto Italiano degli Attuari LXIV 19-47.

- McMurry and Politis (2004) McMurry, T.L. and Politis, D.N. (2004). Nonparametric regression with infinite order flat-top kernels. J. Nonparametric Statist. 16 549-562.

- Merton (1976) Merton, R. (1976). Option pricing when underlying stock returns are discontinuous. J. Financial Economics 3 125-144.

- Neumann and Polzeh; (1998) Neumann, M.H. and Polzehl, J. (1998). Simultaneous bootstrap confidence bands in nonparametric regression. J. Nonparametric Statist. 9 307-333.

- Neumann and Reiß (2009) Neumann, M.H. and Reiß, M. (2009). Nonparametric estimation for Lévy processes from low-frequency observation. Bernoulli 15 223-248.

- Nickl and Reiß (2012) Nickl, R. and Reiß, M. (2012). A Donsker theorem for Lévy measures. J. Functional Anal. 263 3306-3332.

- Nickl et al. (2016) Nickl, R., Reiß, M., Söhl, J., and Trabs, M. (2016). High-frequency Donsker theorems for Lévy measures. Probab. Theory Related Fields 164 61-108.

- Sato (1999) Sato, K.-I. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press.

- Shimizu (2006) Shimizu, Y. (2006). Density estimation of Lévy measures for discretely observed diffusion processes with jumps. J. Japan Statist. Soc. 36 37-62.

- Smirnov (1950) Smirnov, N.V. (1950). On the construction of confidence regions for the density of distribution of random variables. Doklady Akad. Nauk SSSR 74 189-191 (Russian).

- Stein and Weiss (1971) Stein, E.M. and Weiss, G. (1971). Introduction to Fourier Analysis on Euclidean Spaces. Princeton University Press.

- Trabs (2015) Trabs, M. (2015). Quantile estimation for Lévy measures. Stochastic Process. Appl. 125 3484-3521.

- van der Vaart and Wellner (1996) van der Vaart, A.W. and Wellner, J.A.(1996). Weak Convergence and Empirical Processes with Applications to Statistics. Springer.

- Vetter (2014) Vetter, M. (2014). Inference on the Lévy measure in case of noisy observations. Statist. Probab. Lett. 87 125-133.

- Wasserman (2006) Wasserman, L. (2006). All of Nonparametric Statistics. Springer.