Generalization Guarantees for Multi-item Profit Maximization:

Pricing, Auctions, and Randomized Mechanisms

Abstract

We study multi-item profit maximization when there is an underlying distribution over buyers’ values. In practice, a full description of the distribution is typically unavailable, so we study the setting where the mechanism designer only has samples from the distribution. If the designer uses the samples to optimize over a complex mechanism class—such as the set of all multi-item, multi-buyer mechanisms—a mechanism may have high average profit over the samples but low expected profit. This raises the central question of this paper: how many samples are sufficient to ensure that a mechanism’s average profit is close to its expected profit? To answer this question, we uncover structure shared by many pricing, auction, and lottery mechanisms: for any set of buyers’ values, profit is piecewise linear in the mechanism’s parameters. Using this structure, we prove new bounds for mechanism classes not yet studied in the sample-based mechanism design literature and match or improve over the best-known guarantees for many classes.

1 Introduction

The design of profit-maximizing mechanisms is a fundamental problem with diverse applications including Internet retailing, advertising markets, and strategic sourcing. This problem has traditionally been studied under the assumption that there is a joint distribution from which the buyers’ values are drawn and that the mechanism designer knows this distribution in advance. This assumption has led to groundbreaking theoretical results in the single-item setting [62], but transitioning from theory to practice is challenging because the true distribution over buyers’ values is typically unknown. Moreover, in the dramatically more challenging multi-item setting, the support of the distribution alone is often doubly exponential (even if there were just a single buyer with a finite type space***When each buyer’s values are independent from every other buyer’s values, the number of support points is , where is the number of buyers, is the number of discrete value levels a buyer can assign to a bundle, and is the number of items. This is because each of the bundles can take any of values. With correlated valuations, the prior has support points.), so obtaining and storing the distribution is typically impossible.

We relax this strong assumption and instead assume that the mechanism designer only has a set of independent samples from the distribution [55, 56, 69]. This type of sample-based mechanism design reflects current industry practices since many companies—such as online ad exchanges [48, 58], sponsored search platforms [37, 72], and travel companies [77]—use historical purchase data to adjust the sales mechanism.

In most multi-item settings, the form of the revenue-maximizing mechanism is still a mystery. Therefore, rather than use the samples to uncover the optimal mechanism, much of the literature on sample-based mechanism design suggests that we first fix a reasonably expressive mechanism class and then use the samples to optimize over the class. If, however, the mechanism class is complex and the number of samples is not sufficiently large, a mechanism with high average profit over the set of samples may have low expected profit on the actual unknown distribution: overfitting has occurred. This motivates an important question in sample-based mechanism design:

Given a set of samples and a mechanism class , what is the difference between the average profit over the samples and the expected profit on the unknown distribution for any mechanism in ?

If this difference is small, the mechanism in that maximizes average profit over the set of samples nearly maximizes expected profit over the distribution as well.

We present a general theory for deriving generalization guarantees in multi-item settings. A generalization guarantee for a mechanism class bounds the difference between the average profit over the samples and expected profit for any mechanism in . These bounds can be applied no matter how the mechanism designer optimizes over the class, using an automated or manual approach. Optimization algorithms for many of the mechanisms we study have been developed in prior research [69, 19, 11].

This paper is part of a line of research that studies how learning theory can be used to design and analyze mechanisms. Most of these papers have studied only single-parameter settings [6, 7, 39, 26, 49, 59, 60, 66, 31, 47, 43, 17, 1, 45]. In contrast, we focus on multi-item mechanism design, as have recent papers by Morgenstern and Roughgarden [61], Syrgkanis [71], Medina and Vassilvitskii [58], Cai and Daskalakis [19], and Gonczarowski and Weinberg [44].

1.1 Our contributions

Our contributions come in two interrelated parts.

A general theory that unifies diverse mechanism classes.

We uncover a structural property shared by a wide variety of mechanisms which allows us to prove generalization guarantees: for any fixed set of bids, profit is a piecewise linear function of the mechanism’s parameters. Our main theorem provides generalization bounds for any class exhibiting this structure. We relate the complexity of the partition splitting the parameter space into linear portions to the intrinsic complexity of the mechanism class, which we quantify using pseudo-dimension. In turn, pseudo-dimension bounds imply generalization bounds. We prove that many seemingly disparate mechanisms share this structure, and thus our main theorem yields learnability guarantees. By contrast, previous research on multi-item mechanism design focused on deriving guarantees for a few mechanism classes that are “simple” by design [61, 71].

| Category | Mechanism class | Valuations | Result |

|---|---|---|---|

| Pricing mechanisms | Item-pricing mechanisms | General, unit-demand, additive | Lemmas 3.17, 4.5, B.7, B.8 |

| Two-part tariffs | General | Lemma 3.15 | |

| Non-linear pricing mechanisms | General | Lemmas 3.16, A.8 | |

| Auctions | Second-price auctions with reserves | Additive | Lemmas 3.18, 4.4, B.9 |

| Affine maximizer auctions | General | Lemma 3.20 | |

| Virtual valuation combinatorial auctions | General | Lemma 3.20 | |

| Mixed-bundling auctions with reserves | General | Lemma 3.19 | |

| Randomized mechanisms | Lotteries | Additive, unit-demand | Lemmas 3.21, C.2 |

Table 1 summarizes some of the main mechanism classes we analyze and Tables 2, 3, and 4 summarize our bounds.

Our main theorem applies to lotteries, a general representation of randomized mechanisms which generate higher expected revenue than deterministic mechanisms in many settings [29, 33]. We also provide guarantees for item-pricing mechanisms where each item has a price and buyers buy their utility-maximizing bundles. Additionally, we study multi-part tariffs, where there is an upfront fee and a price per unit. These tariffs and other non-linear pricing mechanisms have been studied in economics for decades [63, 41, 75]. Our main theorem also applies to many auction classes, such as second price auctions and well-studied generalized VCG auctions including affine maximizer auctions (AMAs) and mixed-bundling auctions [69, 65, 53, 34, 50]. Under AMAs, revenue is not piecewise-linear in the original parameter space, but we show it is piecewise-linear in a higher-dimensional space.

A key challenge we face is the sensitivity of these mechanisms to small changes in their parameters. For example, changing the price of a good can cause a steep drop in profit if the buyer no longer wants to buy it. Meanwhile, for many well-understood function classes in machine learning, there is a close connection between the distance in parameter space between two parameter vectors and the distance in function space between the two corresponding functions. Since profit functions do not exhibit this predictable behavior, we must carefully analyze the structure of the mechanisms we study in order to derive our generalization guarantees.

Data-dependent generalization guarantees.

We strengthen our main theorem when the distribution over buyers’ values is “well-behaved,” proving generalization guarantees that are independent of the number of items for item-pricing mechanisms, second price auctions with reserves, and lottery mechanisms. Under anonymous prices, our bounds do not depend on the number of buyers either. These guarantees hold when the buyers are additive with values drawn from item-independent distributions (buyer ’s value for item is independent from her value for item , but her value for item may be arbitrarily correlated with buyer ’s value for item ). Buyers with item-independent value distributions have been studied extensively in prior research [19, 76, 21, 42, 5, 23, 46]. This could model buyers at, for example, antique auctions and art auctions (as long as there are no collections to try to assemble or the collections are sold as atomic lots).

| Valuations | Auction class | Our bounds | Prior bounds |

|---|---|---|---|

| Additive or unit-demand | Length- lottery menu | N/A | |

| Additive, item-independent11footnotemark: 1 | Length- item lottery menu | N/A |

Additive cost function

| Valuations | Mechanism class | Price class | Our bounds | Prior bounds | |

|---|---|---|---|---|---|

| General | Length- menus of two-part tariffs over units | Anonymous | N/A | ||

| Non-anonymous | N/A | ||||

|

Anonymous | 33footnotemark: 3 | N/A | ||

| Non-anonymous | 33footnotemark: 3 | N/A | |||

| Additively decomposable non-linear pricing | Anonymous | 33footnotemark: 3 | N/A | ||

| Non-anonymous | 33footnotemark: 3 | N/A | |||

| Item-pricing | Anonymous | 44footnotemark: 4 | |||

| Non-anonymous | 44footnotemark: 4 | ||||

| Unit-demand | Item-pricing | Anonymous | 44footnotemark: 4 | ||

| Non-anonymous | 44footnotemark: 4 | ||||

| Additive | Item-pricing | Anonymous | 44footnotemark: 4, 22footnotemark: 2 | ||

| Non-anonymous | 44footnotemark: 4, 22footnotemark: 2 | ||||

| Additive, item- independent11footnotemark: 1 | Item-pricing | Anonymous | 44footnotemark: 4, 22footnotemark: 2 | ||

| Non-anonymous | 44footnotemark: 4, 22footnotemark: 2 |

Additive cost function; 33footnotemark: 3 is an upper bound on the number of units available of item ; 44footnotemark: 4 Morgenstern and Roughgarden [61]; 22footnotemark: 2 Syrgkanis [71]. The probability these bounds fail to hold is . In all other bounds, appears in a log so we suppress it using big- notation.

| Valuations | Auction class | Our bounds | Prior bounds |

|---|---|---|---|

| General | AMAs and -auctions | 55footnotemark: 566footnotemark: 6 | |

| VVCAs | 55footnotemark: 566footnotemark: 6 | ||

| MBARPs | 55footnotemark: 5 | ||

| Additive | Second price item auctions with anonymous reserve prices | 44footnotemark: 4 | |

| Second price item auctions with non-anonymous reserve prices | 44footnotemark: 4 | ||

| Additive, item-independent11footnotemark: 1 | Second price item auctions with anonymous reserve prices | 44footnotemark: 4 | |

| Second price item auctions with non-anonymous reserve prices | 44footnotemark: 4 |

1.2 Related research

1.2.1 Sample-based mechanism design

Sample-based mechanism design was introduced in the context of automated mechanism design (AMD), where the goal is to design algorithms that take as input information about a set of buyers and return a mechanism that maximizes an objective such as revenue [28, 68, 30]. The input information about the buyers in early AMD was an explicit description of the distribution over their valuations. Later, sample-based mechanism design was introduced where the input is a set of samples from this distribution [55, 56, 69]. Those papers also introduced the idea of searching for a high-revenue mechanism in a parameterized space where any parameter vector yields a mechanism that satisfies the individual rationality and incentive-compatibility constraints. They did not provide generalization guarantees.

Balcan et al. [6, 7] were the first to study the connection between learning theory and revenue maximization. They showed how to use an algorithm that returns a high-revenue, manipulable mechanism in order to find a high-revenue, incentive-compatible mechanism. They study settings with unrestricted supply, whereas we primarily focus on settings with limited supply.

More recent research has provided generalization guarantees when there is limited supply, with a particular focus on single-parameter settings [1, 39, 26, 49, 59, 60, 66, 17, 25]. Devanur et al. [31], Gonczarowski and Nisan [43], Guo et al. [45], and Hartline and Taggart [47] provide computationally efficient algorithms for learning nearly-optimal single-item auctions in various settings. In contrast, we study multi-parameter settings. Our bounds do not apply to the state-of-the-art in this direction by Guo et al. [45] because their approach does not involve optimizing over a mechanism class with continuously tunable parameters.

Balcan et al. [9] drew on classic tools from learning theory to provide algorithms and generalization guarantees for the related problem of learning agents’ preferences. Their analysis made connections to the concept of generalized linear functions from the structured prediction literature [27]. Their algorithms predict the future purchases of utility-maximizing agents.

Morgenstern and Roughgarden [61] later used this concept of generalized linear functions to provide sample complexity guarantees for multi-item revenue maximization. They provide a technique for bounding a mechanism class’s pseudo-dimension that requires two steps, described at a high level here and in detail in Appendix B. First, one must show that for any mechanism in the class, its allocation function is a -dimensional linear function for some . Next, fixing a set of samples and an allocation per sample, one must bound the pseudo-dimension of the set of revenue functions across all mechanisms that induce those allocations.

The guarantees presented in this paper offer several advantages over Morgenstern and Roughgarden’s approach. First, our main theorem depends on a structural property—the piecewise-linear form of the revenue function—that is not defined in terms of any learning theory concept (such as generalized linear functions or pseudo-dimension) and thus can be more readily applied. Moreover, in several cases, Morgenstern and Roughgarden [61] proved loose guarantees using structured prediction; in their appendix, they used a first-principles approach to prove stronger guarantees. Their structured prediction proof technique requires them to bound the total number of allocations a mechanism class can induce on a set of samples. Their bound is a bit loose, and we are able to tighten it using the techniques we develop in this paper, as we detail in Appendix B. By combining our analysis techniques with tools from structured prediction, we are able to match the tighter bounds that Morgenstern and Roughgarden [61], which answer an open question they posed. Finally, we apply our guarantees to a wide variety of mechanism classes, both simple and complex, whereas Morgenstern and Roughgarden [61] applied their guarantees to three mechanism classes that are “simple” by design: item-pricing mechanisms, grand-bundle-pricing mechanisms (where the grand bundle is sold as a single unit), and second-price item auctions.

Syrgkanis [71] also suggests a general technique for providing generalization guarantees which he applies to several “simple” mechanism classes: the same three as Morgenstern and Roughgarden [61] as well as single-item -level auctions [60]. His generalization guarantees apply only to empirical revenue maximization algorithms, which return the mechanism in a class that maximizes average revenue over the samples. This is in contrast to our bounds (and those by Morgenstern and Roughgarden [61]) which apply uniformly to every mechanism in a given class. This is crucial when empirical revenue maximization is not computationally feasible. Another advantage of our bounds is that they grow logarithmically in where is the probability that the bound fails to hold (as do those by Morgenstern and Roughgarden [61]). In contrast, the bounds by Syrgkanis [71] grow linearly in .

1.2.2 Dynamic mechanism design

Dynamic pricing is a similar but distinct problem from ours where prices are adjusted over a finite time horizon and the consumer demand function is unknown [e.g., 3, 14, 16, all of whom study single-item settings]. The goal is typically to minimize regret (the difference between the cumulative profit of the best prices in hindsight and that of the chosen prices).

1.2.3 Approximation guarantees

Many mechanisms we analyze can guarantee approximately-optimal revenue.

Item-pricing mechanisms.

For a single unit-demand buyer with a bounded value distribution, item-pricing mechanisms can yield a constant fraction of optimal revenue [23]. Moreover, given multiple unit-demand buyers and constraints on which allocations are feasible, item-pricing mechanisms provide a constant-factor approximation [24].

For an additive buyer with independent values, item-pricing mechanisms provide a fraction of optimal revenue [46], later improved to [54]. The better of an item-pricing mechanism or selling the grand bundle as a single unit provides a constant-factor approximation in this setting [4] and generalizations thereof [13, 38]†††For multiple additive buyers, a VCG mechanism with bidder entries fees achieves a constant-factor approximation [76].. Similarly, for a subadditive buyer, the better of an item-pricing mechanism and a more general bundling mechanism provides a constant-factor approximation [67].

Two-part tariffs.

For buyers with additive values up to a matroid feasibility constraint, a sequential variant of two-part tariffs provides a constant-factor approximation [22].

Lotteries.

For a single additive buyer with independent values, Babaioff et al. [5] proved that a lottery menu of length is a -factor approximation. For a single unit-demand buyer with independent item values, Kothari et al. [52] introduce the notion of symmetric menu complexity, which is the number of menu entries up to permutations of the items. A quasi-polynomial symmetric menu complexity suffices to guarantee a approximation.

2 Preliminaries and notation

We study the problem of selling items to buyers. We denote a bundle of items as a quantity vector . The number of units of item in the bundle is . The bundle consisting of only one copy of the item is denoted by the standard basis vector , where and for all . Each buyer has a valuation function over bundles of items. We denote an allocation as where is the bundle that buyer receives. The cost to produce is and the cost to produce the allocation is . Suppose there are units available of item . Let . We use to denote buyer ’s values for all of the bundles and we use to denote a vector of buyer values. We use the notation to denote the set of all valuation vectors . Additive buyers have values and unit-demand buyers have values . The mechanisms we study are dominant strategy incentive compatible, so we assume that the bids equal the buyers’ valuations.

There is an unknown distribution over buyers’ values. The notation denotes the profit of a mechanism on the valuation vector . We use the notation and for a set of samples , we use the notation

We study real-valued functions parameterized by vectors in , denoted as For a fixed , we often consider as a function of its parameters, which we denote as .

3 Generalization guarantees

We provide generalization bounds for a variety of mechanism classes. These guarantees bound the difference between the expected profit and average empirical profit of any mechanism in the class.

Definition 3.1.

A generalization guarantee for a mechanism class is a function defined such that for any , any , and any distribution over buyers’ values, with probability at least over the draw of a set , for any , the difference between the average profit of over and the expected profit of over is at most :

Generalization guarantees allow the mechanism designer to relate the expected profit of a mechanism in which achieves maximum average profit over the set of samples to the expected profit of an optimal mechanism in . We summarize this connection in the following remark.

Remark 3.2.

For a set of samples , let maximize average profit over and let maximize expected profit. Then

Similar bounds also hold for mechanisms with approximately optimal average profit over the samples (see Corollaries A.1 and A.2 in Appendix A).

3.1 General structure for sample-based mechanism design

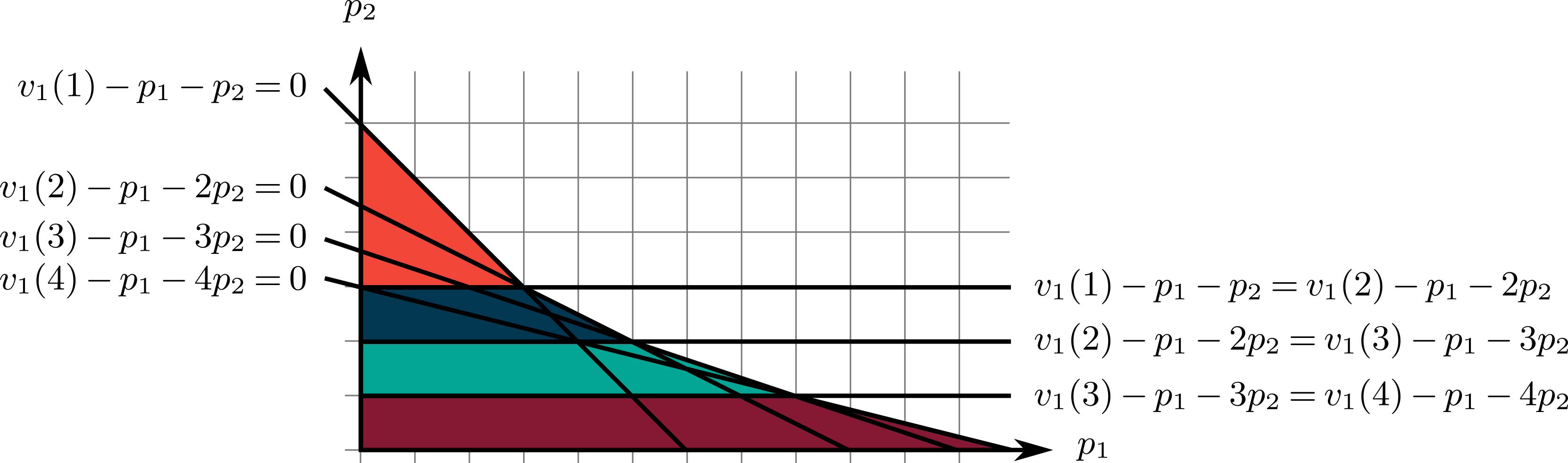

Our general theorem uses structure shared by a variety of mechanism classes to characterize the function . Our results apply broadly to parameterized sets of mechanisms where every mechanism in is defined by a vector , such as a vector of prices. Our guarantees apply to mechanism classes where for every valuation , the profit as a function of the parameters , denoted , is piecewise linear. We illustrate this property via several simple examples.

Example 3.3.

In a two-part tariff, there are multiple units (i.e., copies) of an item for sale. The seller sets an upfront fee and a price per unit . Here, we consider the simple case where there is a single buyer. If the buyer buys units, he pays . Two-part tariffs have been studied extensively [63, 41, 75] and are prevalent throughout daily life. For example, health clubs often require an upfront membership fee plus a fee per month. Amusement parks often require an entrance fee with an additional payment per ride. In many cities, purchasing a public transportation card requires an upfront fee and an additional cost per ride. Balcan et al. [11] showed how to learn two-part tariffs that maximize average revenue over a training set.

Suppose there are units of the item for sale. The buyer will buy units so long as for all and . Therefore, there are at most hyperplanes splitting into regions such that within any one region, the number of units bought is fixed, in which case profit is linear in and .

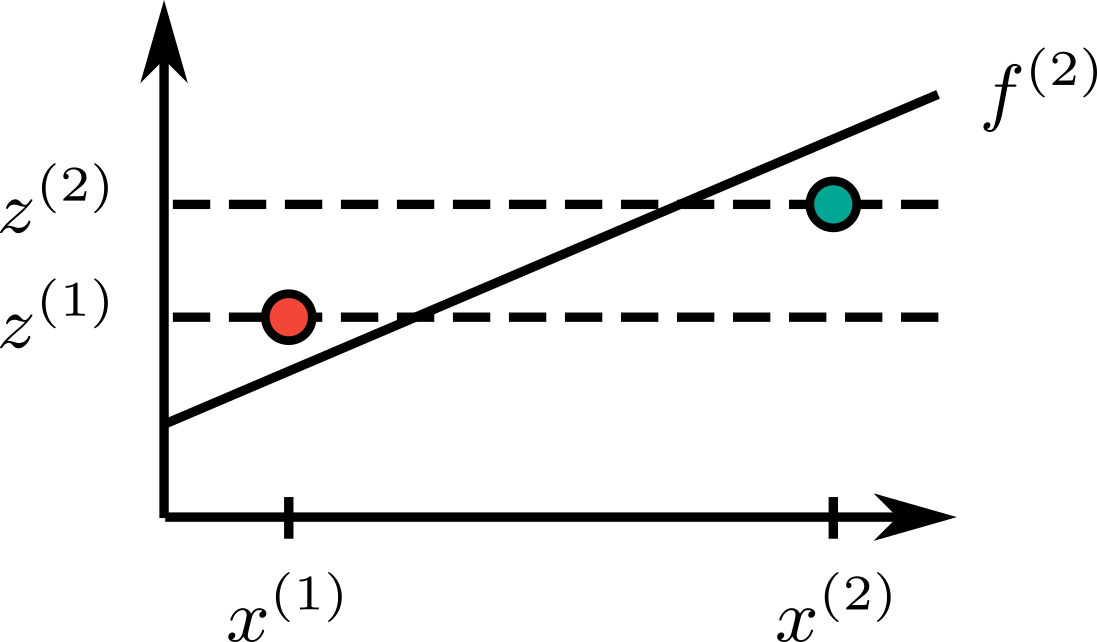

See Figure 1 for an illustration.

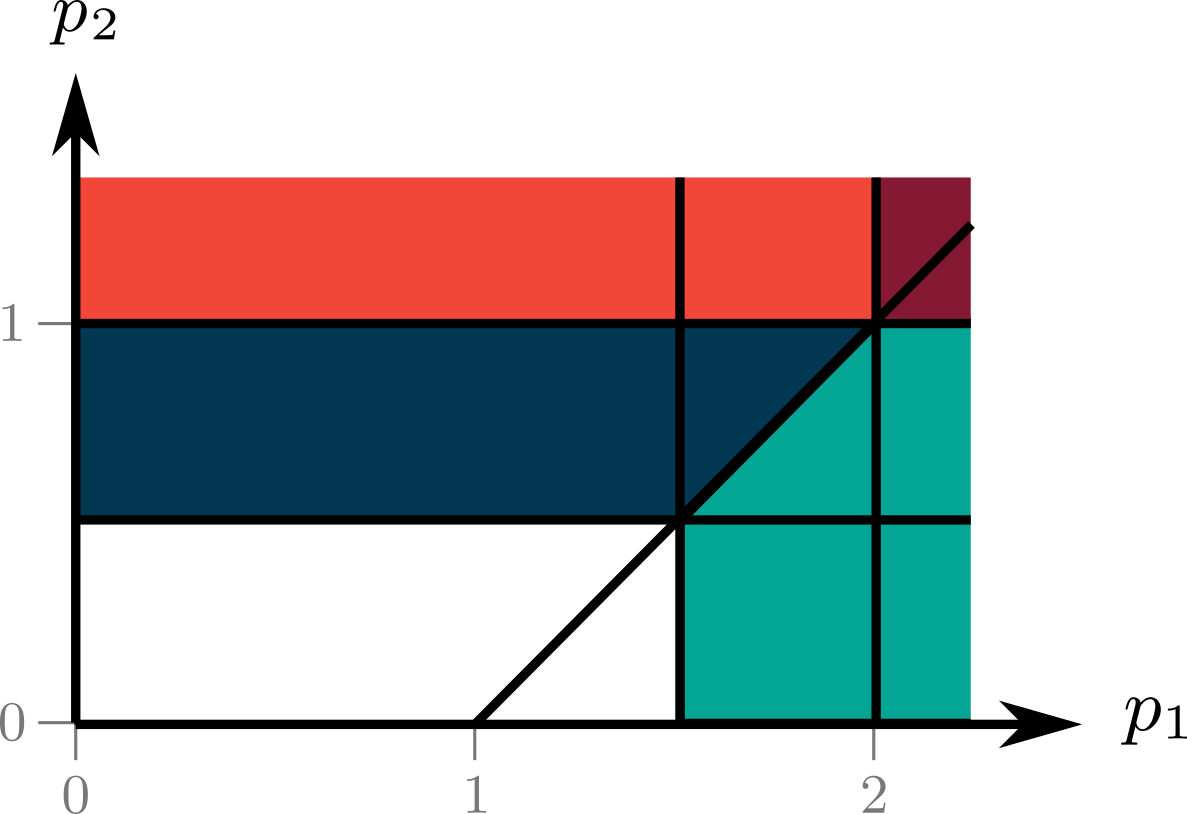

Example 3.4.

Under an item-pricing mechanism, there are multiple items, multiple buyers, and a single unit of each item for sale. Under anonymous prices, the seller sets a price per item . There is an arbitrary ordering on the buyers such that the first buyer buys the bundle that maximizes his utility, then the next buyer buys the bundle of remaining items that maximizes his utility, and so on. Buyer will prefer bundle over if , so his preference ordering over bundles is determined by these hyperplanes. Once the buyers’ preference orderings are fixed, the bundles they buy are fixed. In any region of the price space where the purchased bundles are fixed, profit is a linear in the prices.

See Figure 2 for an illustration.

We analyze the “complexity” of the partition splitting into regions where is linear.

Definition 3.5 (-delineable).

A mechanism class is -delineable if:

-

1.

The class consists of mechanisms parameterized by vectors from a set ; and

-

2.

For any valuation vector , there is a set of hyperplanes such that for any connected component of , is linear over (As is standard, indicates set removal.)

3.2 Pseudo-dimension

Pseudo-dimension is a well-studied tool used to measure the complexity of a function class. Pseudo-dimension captures the following intuition: functions in a “complex” class should be able to fit complex patterns. We first introduce the notion of shattering for general function classes.

Definition 3.6.

Let be a set of functions with an abstract domain . We say that witness the shattering of by if for all , there is a function such that for all , and for all , .

Figure 5 in Appendix A provides a visualization. The larger the set a function class can shatter, the more complex that function class is, an intuition formalized by pseudo-dimension.

Definition 3.7 (Pollard [64]).

Let be a set of functions and let be the largest set that can be shattered by . The pseudo-dimension of , denoted , is .

In the language of mechanism design, let be a subset of . We say that witness the shattering of by if for all , there is a mechanism such that for all , and for all , . The pseudo-dimension of , denoted , is the size of the largest set that is shatterable by .

Pollard [64] and Dudley [35] provide generalization guarantees in terms of pseudo-dimension, which we describe below in the language of mechanism design.

Theorem 3.8.

For any mechanism class , let be the maximum profit of any mechanism in over the support of . There is a generalization guarantee defined such that

3.3 General theorem for sample-based mechanism design

In the following theorem, which is our main theorem, we relate pseudo-dimension to delineability.

Theorem 3.9.

Let be a -delineable mechanism class. Given a distribution over buyers’ values, let be the maximum profit of any mechanism in over the support of . Then

is a generalization guarantee for .

Proof.

This theorem follows directly from the following lemma. ∎

Lemma 3.10.

If is a mechanism class that is -delineable, then .

Proof.

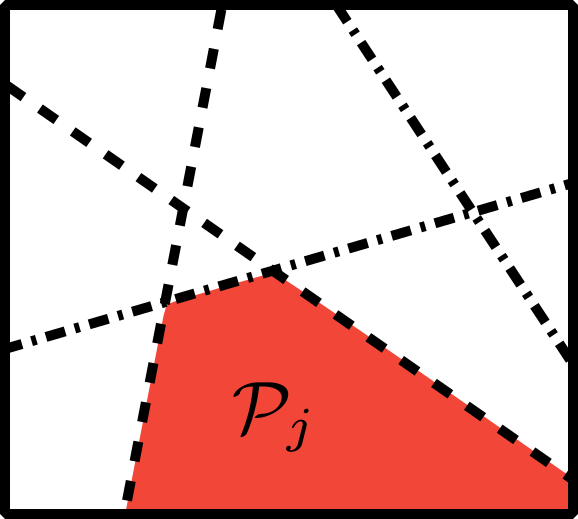

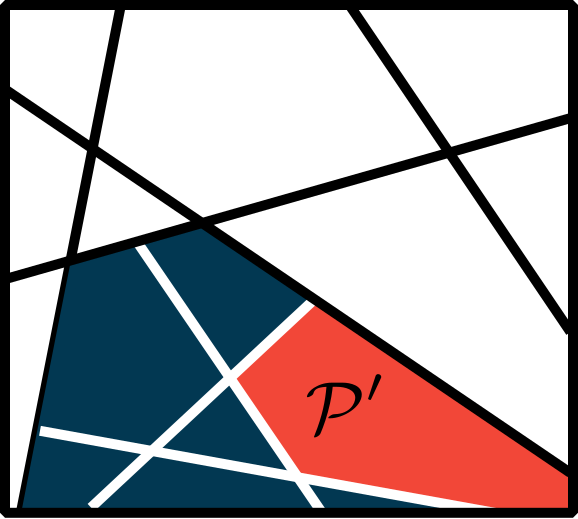

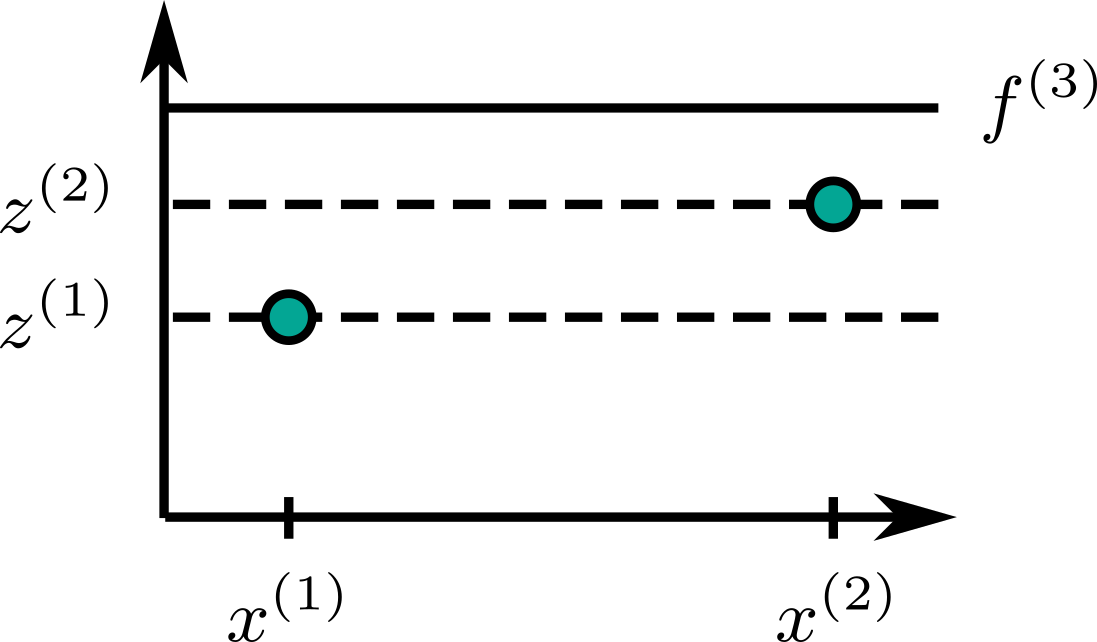

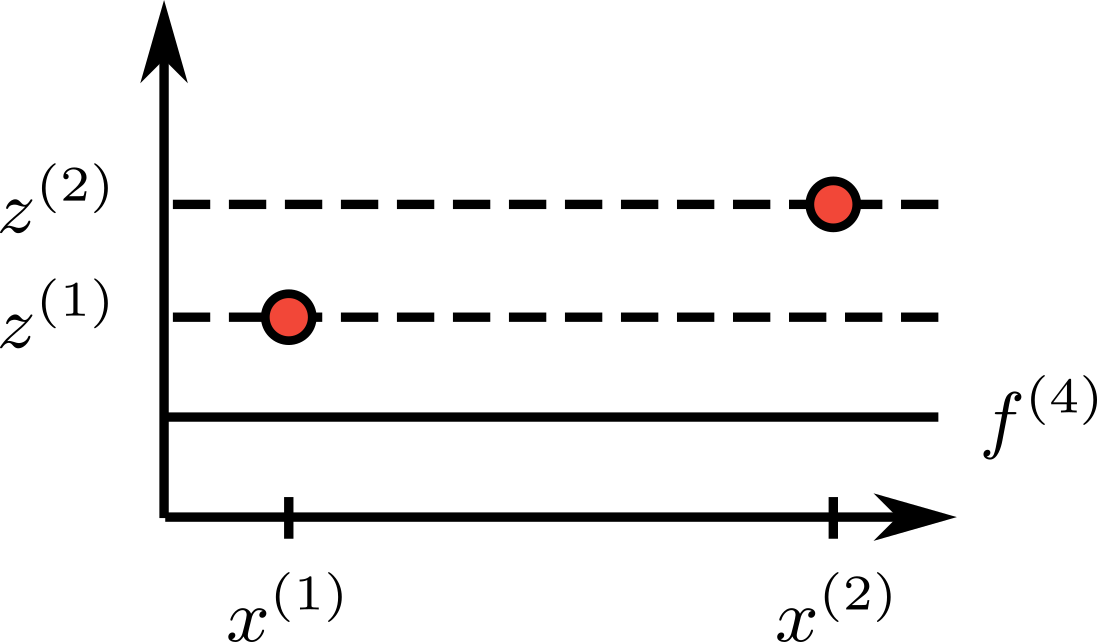

For any set of valuation vectors and real values , we show that there is a partitioning of the parameter space into at most regions such that for all in any one region and all , either or . We will then use this fact to bound . To this end, let be the set of hyperplanes such that for any connected component of , is linear over Let be the connected components of . For each set and each , is contained in a single connected component of , which means that is linear over (See Figures 3(a)-3(c) for illustrations.) Since for all , [18, Theorem 1].

For any region and , let and be defined such that for all . On one side of the hyperplane , and on the other side, . Let be all hyperplanes for all samples, i.e., In any connected component of (illustrated in Figure 3(d)), for all , is either greater than or less than for all . The number of connected components of is at most . Thus, the total number of regions where for all , is either greater than or less than is at most .

We now use this fact to bound . Suppose , so there is a set

that is shattered by with witnesses . For any , there is a parameter vector such that if and only if . Let . There are regions where for each region and each , either for all or . At most one vector in can come from any one region. This means that . The result follows from Lemma A.3. ∎

3.4 Delineable mechanism classes

We now show that a diverse array of mechanism classes are delineable, so we can apply Theorem 3.9. We warm up with Examples 3.3 and 3.4, which imply the following lemmas.

Lemma 3.11.

The class of two-part tariffs for one buyer and units of an item is -delineable.

Lemma 3.12.

The class of anonymous item-pricing mechanisms is -delineable.

3.4.1 Non-linear pricing mechanisms.

Non-linear pricing mechanisms are used to sell multiple units of a set of items. We make the following natural assumption which says that as the number of units in an allocation grows, the cost will eventually exceed the buyers’ welfare.

Assumption 3.13.

There is a cap per item such that it costs more to produce units of item than the buyers will pay. In other words, for all in the support of and all allocations , if there exists an item such that , then .

Menus of two-part tariffs.

Menus of two-part tariffs are a generalization of Example 3.3. The seller offers the buyers different two-part tariffs and each buyer chooses the tariff and number of units that maximizes his utility. For example, consumers often choose among various membership tiers—typically with a larger upfront fee and lower future payments—for health clubs, wholesale stores, amusement parks, credit cards, and cellphone plans. Under non-anonymous prices, let be the menu of two-part tariffs that the seller offers to buyer . Here, is the upfront fee of the tariff and is the price per unit. Under anonymous prices, and . Each buyer chooses the tariff and the number of units maximizing his utility, and pays . In this context, an allocation is a vector where is the number of units buyer buys.

We make the natural assumption that the seller will not choose prices that result in negative profit. In other words, he will select a profit non-negative menu of two-part tariffs, formalized below.

Definition 3.14.

For anonymous prices (respectively, non-anonymous), let (respectively, ) be the set of prices where no matter which tariff each buyer chooses and no matter how many units he buys, the seller will obtain non-negative profit. In other words, for each buyer , each tariff , and each allocation , The set of profit non-negative menus of two-part tariffs is defined by parameters in (resp., ).

Under Assumption 3.13, no matter which parameters the seller chooses in or , if all buyers simultaneously choose the tariff and the number of units that maximize their utilities, then . See Lemma A.4 for the proof. This allows us to prove the following lemma.

Lemma 3.15.

Let and be the classes of anonymous and non-anonymous profit non-negative length- menus of two-part tariffs. Under Assumption 3.13, is -delineable and is -delineable.

General non-linear pricing mechanisms.

We study general non-linear pricing mechanisms under Wilson’s bundling interpretation [75]: if the prices are anonymous, there is a price per quantity vector denoted . The buyers simultaneously choose the bundles maximizing their utilities. If the prices are non-anonymous, there is a price per vector and buyer denoted . These general non-linear pricing mechanisms include multi-part tariffs as a special case. Without assumptions, the parameter space infinite-dimensional since the seller could set prices for every bundle . In Lemma A.5, we show that under Assumption 3.13, no buyer will choose a bundle with for any if the seller chooses a profit non-negative non-linear pricing mechanism. The definition is similar to Definition 3.14 and is in Appendix A (Definition A.6).

Lemma 3.16.

Let and be the classes of anonymous and non-anonymous profit non-negative non-linear pricing mechanisms. Under Assumption 3.13, is -delineable and is -delineable.

We prove polynomial bounds when prices are additive over items (Lemma A.8).

3.4.2 Item-pricing mechanisms.

We now apply Theorem 3.9 to anonymous and non-anonymous item-pricing mechanisms. Unlike non-linear pricing, there is only one unit of each item for sale. Under anonymous prices, the seller sets a price per item. Under non-anonymous prices, there is a buyer-specific price per item. We make the common assumption [e.g., 40, 4, 21] that there is a fixed, arbitrary ordering on the buyers such that the first buyer arrives and buys the bundle that maximizes his utility, then the next buyer arrives and buys the bundle of remaining items that maximizes his utility, and so on.

Lemma 3.17.

Let (resp., ) be the class of item-pricing mechanisms with anonymous (resp., non-anonymous) prices. For additive buyers, is -delineable and is -delineable.

In Appendix B, we connect the hyperplane structure we investigate in this paper to the structured prediction literature in machine learning [27], thus strengthening our generalization bounds for item-pricing mechanisms under buyers with unit-demand and general valuations and answering an open question by Morgenstern and Roughgarden [61].

3.4.3 Auctions.

We now present applications of Lemma 3.10 to auctions in single-unit settings.

Second price item auctions with reserves.

We study additive buyers in this setting. Under non-anonymous reserves, there is a price for each item and buyer . The buyers submit bids on the items. For each item , the highest bidder wins the item if her bid is above . She pays the maximum of the second highest bid and . Under anonymous reserves, .

Lemma 3.18.

Let and be the classes of anonymous and non-anonymous second price item auctions. Then is -delineable and is -delineable.

Mixed bundling auctions with reserve prices (MBARPs).

MBARPs [50, 73] are a VCG generalization. Intuitively, the MBARP enlarges the set of agents to include the seller, whose values are defined by reserve prices. The auction boosts the social welfare of any allocation where the grand bundle is allocated and then runs the VCG over this larger set of buyers. Formally, MBARPs are defined by a parameter and reserves . Let be a function such that if some buyer receives the grand bundle under allocation and 0 otherwise. For an allocation , let be the items not allocated. The MBARP allocation is

The payments are defined as in the VCG mechanism (see Definition A.9 in Appendix A).

Lemma 3.19.

Let be the set of MBARPs. Then is -delineable.

Affine maximizer auctions (AMAs).

AMAs are the only ex post truthful mechanisms over unrestricted value domains [65] and under natural assumptions, every truthful multi-item auction is an “almost” AMA, that is, an AMA for sufficiently high values [53].‡‡‡Surprisingly, even when the buyers have additive values, AMAs can generate higher revenue than running a separate Myerson auction for each item [69]. An AMA is defined by a weight per buyer and a boost per allocation . Its allocation maximizes the weighted social welfare The payments have the same form as the VCG payments (see Definition A.10 in Appendix A). A virtual valuation combinational auction (VVCA) [55] is an AMA where each is split into terms such that where for all allocations that give buyer exactly bundle . Finally, -auctions [50] are defined such that .

Lemma 3.20.

Let , , and be the classes of AMAs, VVCAs, and -auctions, respectively. Letting , we have that is -delineable, is -delineable, and is -delineable.

3.4.4 Lotteries.

Lotteries are randomized mechanisms which typically have higher revenue than deterministic mechanisms. We analyze a single additive buyer and generalize to unit-demand buyers and multiple buyers in Appendix A.1. A length- lottery menu is a set , where and . Under the lottery , the buyer pays and receives each item with probability . For a buyer with values , let be the lottery that maximizes the his expected utility and let denote the allocation. The expected profit is The challenge in bounding the pseudo-dimension of the class of these lotteries is that is not piecewise linear in . Instead, we bound the pseudo-dimension of a related class and show that optimizing over amounts to optimizing over itself. To motivate , note that if , then , so . For , we define and . The class is delineable: for any , buyer’s chosen lottery and the bundle are determined by hyperplanes.

Lemma 3.21.

The class is -delineable.

The following lemma guarantees that optimizing over amounts to optimizing over itself.

Lemma 3.22.

With probability over for all ,

This section demonstrates that a wide variety of mechanism classes are delineable. Therefore, Theorem 3.9 immediately implies a generalization bound for a diverse array of mechanisms.

4 Distribution-dependent generalization guarantees

In this section, we provide stronger results when the buyers’ values are additive and drawn from item-independent distributions, which means that for all and , buyer ’s values for items and are independent, but her values may be correlated with buyer ’s values. We also require that the mechanism class’s profit functions decompose additively. For example, under item-pricing mechanisms, the profit decomposes into the profit obtained from selling item 1, plus the profit obtained by selling item 2, and so on. Surprisingly, our bounds do not depend on the number of items and under anonymous prices, they do not depend on the number of buyers either.

To prove distribution-dependent generalization guarantees, we use Rademacher complexity [12, 51]. In contrast, pseudo-dimension implies bounds that are worst-case over the distribution. We prove that it is impossible to obtain guarantees that are independent of the number of items using pseudo-dimension alone (Theorem 4.6).

Definition 4.1.

A distribution-dependent generalization guarantee for a mechanism class and a distribution over buyers’ values is a function defined such that for any sample size and any , with probability at least over the draw of a set , for any mechanism in , the difference between the average profit of over and the expected profit of over is at most . In other words,

The generalization guarantee is worst case in that in holds for any distribution . In contrast, the distribution-dependent bound may be much tighter when the distribution is “well-behaved”.

We now define Rademacher complexity, which measures the ability of a class of mechanism profit functions to fit random noise. Intuitively, more complex classes should fit random noise better than simple classes. The empirical Rademacher complexity of with respect to is

where . Classic learning-theoretical results [12, 51] imply the distribution-dependent generalization bound where is the maximum profit of any mechanism in over the support of . It is well-known that Rademacher complexity and pseudo-dimension are connected as follows.

We show that if the profit functions of a class decompose additively into simpler functions, then we can bound using the Rademacher complexity of those simpler functions. We use this to prove tighter bounds for several mechanism classes under additive buyers with values drawn from item-independent distributions. This includes product distributions, a setting that has been studied extensively [e.g., 46, 19, 76, 21, 5]. Formally, a mechanism class decomposes additively if for all , there are functions such that .

Corollary 4.3.

Suppose that is a set of additively decomposable mechanisms. Moreover, suppose that for all , the range of over the support of is and that the class is -delineable. For any set ,

Proof.

Lemma 4.4.

Let and be the sets of second-price auctions with anonymous and non-anonymous reserves. Suppose the buyers are additive, is item-independent, and the cost function is additive. For any set , and .

Lemma 4.5.

Let and be the sets of anonymous and non-anonymous item-pricing mechanisms. Suppose the buyers are additive, is item-independent, and the cost function is additive. For any set of samples , and .

We prove similar guarantees for menus of item lotteries (Lemma C.2). Finally, we provide lower bounds showing that one could not prove the generalization guarantees implied by Lemmas 4.4 and 4.5—which do not depend on the number of items—using pseudo-dimension alone.

Theorem 4.6.

Let and be the classes of anonymous and non-anonymous item-pricing mechanisms. Then and . The same holds if and are the classes of second-price auctions with anonymous and non-anonymous reserves.

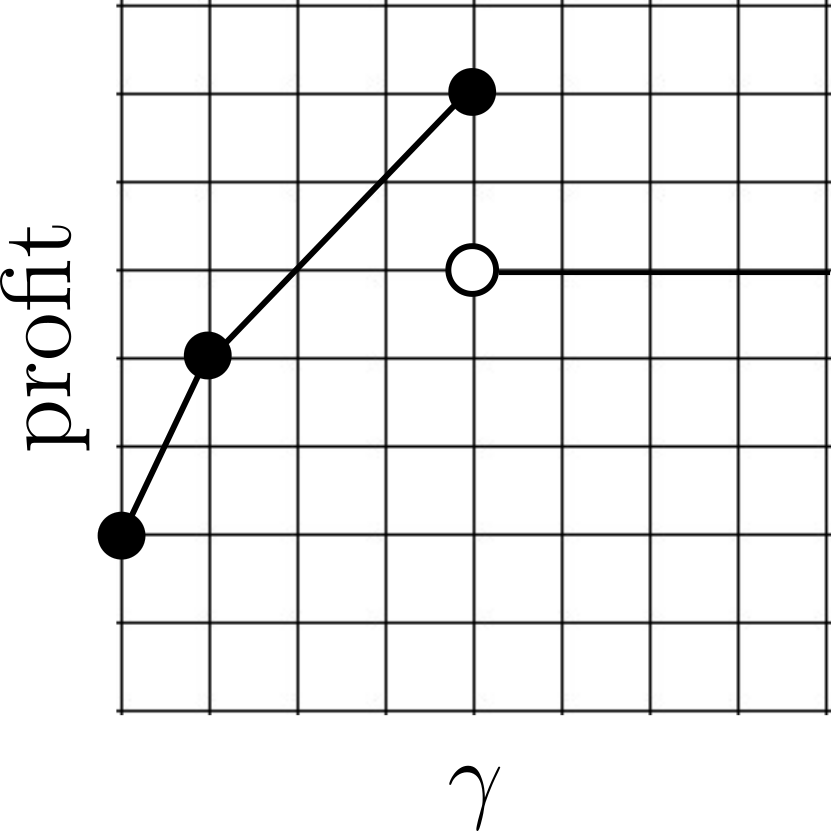

5 Optimizing the profit-generalization tradeoff

In this section, we use our results from Section 3 to provide guarantees for optimizing the profit-generalization tradeoff, drawing on classic machine learning results on structural risk minimization [74, 15].

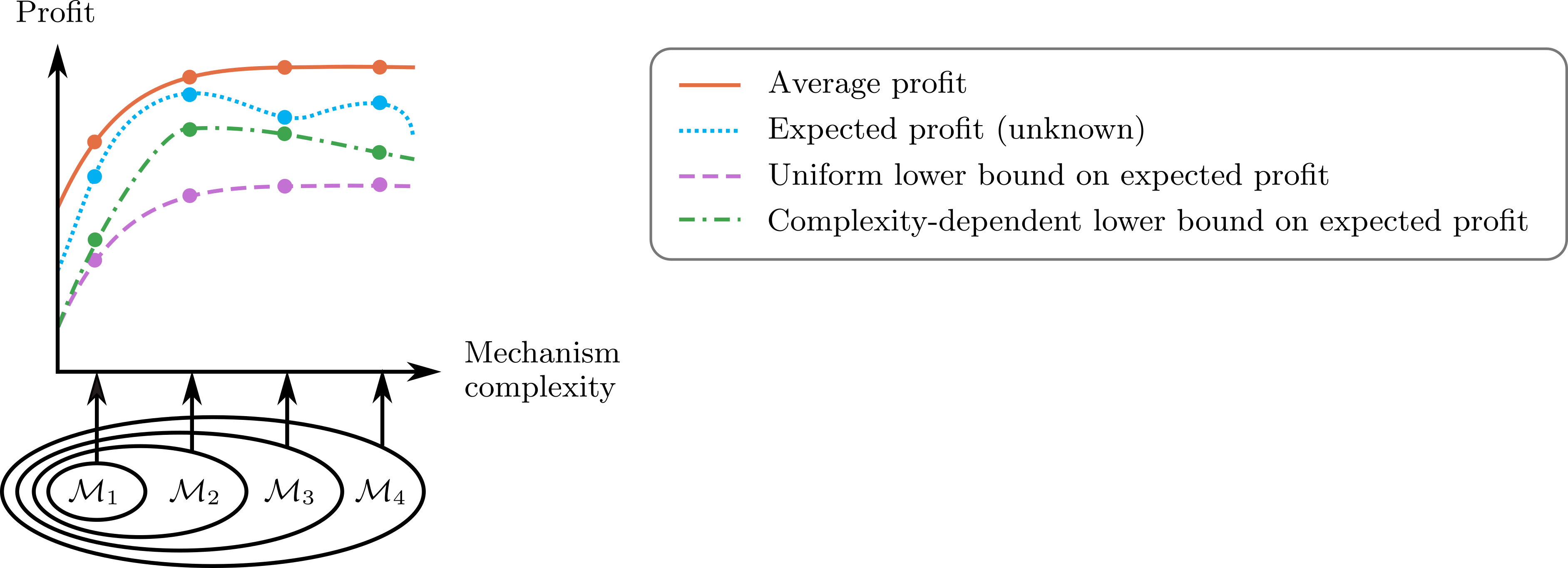

We illustrate this tradeoff§§§These figures are purely illustrative; they are not based on a simulation or real data. in Figure 4 with a mechanism class that decomposes into a nested sequence . The -axis measures the intrinsic complexity (e.g., pseudo-dimension) of the subclasses. The orange solid line illustrates the average profit over a fixed set of samples of the mechanism that maximizes average profit. In particular, the dot on the orange solid line above illustrates . Since for , . Similarly, the dot on the blue dotted line above illustrates the expected profit of . This line begins decreasing when the complexity grows to the point that overfitting occurs. The purple dashed line illustrates a uniform lower bound on the expected profit of .

Our general theorem allows us to easily derive bounds for each class . We can then “spread” across all subsets using a function such that . By a union bound, with probability , for all , . This is illustrated by the green dashed-dotted line in Figure 4, where the lower bound on the expected profit of is . By maximizing this complexity-dependent lower bound, the designer can determine that is better than .

The decomposition of into subsets and the choice of weights allow the designer to encode his prior knowledge about the market. For example, if mechanisms in are likely to be profitable, he can increase , which in turn decreases , thereby implying stronger guarantees.

We now apply this analysis to item pricing. To perform market segmentation, the seller can break the buyers into groups and charge each group a different price. For , let be the class of non-anonymous pricing mechanisms with price groups: for all mechanisms in , there is a partition of the buyers such that for all , all buyers , and all items , . We derive the following guarantee for this hierarchy.

Theorem 5.1.

Let be the class of non-anonymous item-pricing mechanisms over additive buyers. With probability over the draw , for any and any mechanism ,

We prove results for two-part tariffs, AMA, -auctions, and lottery menus in Appendix D.

6 Comparison of our results to prior research

We compare our results to prior research that provides generalization bounds for some of the mechanisms we study. Morgenstern and Roughgarden [61] studied “simple” multi-item pricing mechanisms and second-price auctions. See Tables 3 and 4 and Appendix B.1 for a comparison.

Syrgkanis [71] provided bounds specifically for the mechanism that maximizes average revenue over the samples, whereas our bounds apply to every mechanism in a given class. This is important when exactly optimizing average revenue is intractable. To illustrate their bounds, let be the anonymous item-pricing mechanism maximizing average revenue over samples. Syrgkanis [71] proved that with probability , . When is item-independent, our bound is an improvement. Otherwise, our bound is incomparable. Syrgkanis [71] proved a similar bound for non-anonymous prices (see Table 3) which is also incomparable.

Cai and Daskalakis [19] provided learning algorithms for buyers with values drawn from product distributions. For additive and unit-demand buyers with values bounded in , we match their guarantees, which are based on those of Morgenstern and Roughgarden [61]. They also study buyers with XOS, constrained additive, and subadditive values in which case our results do not provide an improvement. For example, for XOS and constrained additive buyers, Cai and Daskalakis [19] provided algorithms which return item-pricing mechanisms with entry fees. Our results would imply pessimistic bounds for this class due to the exponential number of parameters. To circumvent this, their proofs use specific structural properties exhibited by bidders with product distributions, whereas the primary focus of this paper is to provide a general theory applicable to many different mechanisms and buyer types.

Medina and Vassilvitskii [58] studied a different model than ours where items are defined by feature vectors and the seller has access to a bid predictor mapping feature vectors to bids.

Among other results, Devanur et al. [32, Section 6.1] proved that for the class of second price item auctions with non-anonymous reserves, samples are sufficient to ensure that with probability , for all , . Our Lemma 3.18 implies samples are sufficient, which is incomparable.

Gonczarowski and Weinberg [44] studied a setting where there are buyers with additive, independent values in the interval for items, as well as a generalization to Lipschitz valuations. They proved that poly samples are sufficient to learn an approximately incentive compatible mechanism with -approximately optimal revenue. From a computation perspective, it is not known how to efficiently find an -approximately optimal mechanism in this setting where the number of types is exponential in the number of items. In contrast, our guarantees apply uniformly to any mechanism from within a variety of parameterized classes, so the seller can use our guarantees to bound the expected profit of the mechanism he obtains via any optimization procedure. However, there may not be a mechanism in these classes with nearly optimal revenue.

7 Conclusion

We studied profit maximization when the mechanism designer has a set of samples from the distribution over buyers’ values. We identified structural similarities of mechanism classes including non-linear pricing mechanisms, generalized VCG mechanisms such as affine maximizer auctions, and lotteries: profit is a piecewise-linear function of the mechanism class’s parameters. These similarities led us to a general theorem that gives generalization bounds for a broad range of mechanism classes. It offers the first generalization guarantees for many important classes and also matches and improves over many existing bounds. Finally, we provided guarantees for optimizing a fundamental tradeoff in sample-based mechanism design: more complex mechanisms have higher average profit over the samples than simpler mechanisms, but require more samples to avoid overfitting.

An important direction for future research is the development of learning algorithms for multi-item profit maximization. Learning algorithms have been proposed for several of the mechanism classes we consider, including two-part tariffs [11], affine maximizer auctions [69], and item-pricing mechanisms [19, who also provide algorithms for other multi-item mechanism classes]. A line of research also provides learning algorithms for single-item profit maximization [31, 47, 43, 45].

Another direction is to use tools such as Rademacher complexity to provide generalization bounds for non-worst-case distributions beyond item-independent distributions (the focus of Section 4). For example, suppose any buyer’s values for any items are correlated, but his values are independent of any other buyer’s values. Can the bounds in this paper be improved?

Acknowledgements.

This material is based on work supported by the National Science Foundation under grants CCF-1422910, CCF-1535967, CCF-1733556, CCF-1910321, IIS-1617590, IIS-1618714, IIS-1718457, IIS-1901403, SES-1919453, and a Graduate Research Fellowship; the ARO under awards W911NF2010081 and W911NF1710082; the Defense Advanced Research Projects Agency under cooperative agreement HR00112020003; an Amazon Research Award; a Microsoft Research Faculty Fellowship; an AWS Machine Learning Research Award; a Bloomberg Data Science research grant; an IBM PhD Fellowship; and a fellowship from Carnegie Mellon University’s Center for Machine Learning and Health.

References

- Alon et al. [2017] Noga Alon, Moshe Babaioff, Yannai A Gonczarowski, Yishay Mansour, Shay Moran, and Amir Yehudayoff. Submultiplicative Glivenko-Cantelli and uniform convergence of revenues. Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), 2017.

- Anthony and Bartlett [2009] Martin Anthony and Peter Bartlett. Neural Network Learning: Theoretical Foundations. Cambridge University Press, 2009.

- Araman and Caldentey [2009] Victor F. Araman and René Caldentey. Dynamic pricing for nonperishable products with demand learning. Operations Research, 57(5):1169–1188, 2009.

- Babaioff et al. [2014] Moshe Babaioff, Nicole Immorlica, Brendan Lucier, and S. Matthew Weinberg. A simple and approximately optimal mechanism for an additive buyer. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), 2014.

- Babaioff et al. [2017] Moshe Babaioff, Yannai A Gonczarowski, and Noam Nisan. The menu-size complexity of revenue approximation. In Proceedings of the Annual Symposium on Theory of Computing (STOC), 2017.

- Balcan et al. [2005] Maria-Florina Balcan, Avrim Blum, Jason D. Hartline, and Yishay Mansour. Mechanism design via machine learning. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), pages 605–614, 2005.

- Balcan et al. [2008a] Maria-Florina Balcan, Avrim Blum, Jason Hartline, and Yishay Mansour. Reducing mechanism design to algorithm design via machine learning. Journal of Computer and System Sciences, 74:78–89, December 2008a.

- Balcan et al. [2008b] Maria-Florina Balcan, Avrim Blum, and Yishay Mansour. Item pricing for revenue maximization. In Proceedings of the ACM Conference on Economics and Computation (EC), pages 50–59, 2008b.

- Balcan et al. [2014] Maria-Florina Balcan, Amit Daniely, Ruta Mehta, Ruth Urner, and Vijay V Vazirani. Learning economic parameters from revealed preferences. In Proceedings of the Conference on Web and Internet Economics (WINE), 2014.

- Balcan et al. [2016] Maria-Florina Balcan, Tuomas Sandholm, and Ellen Vitercik. Sample complexity of automated mechanism design. In Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), 2016.

- Balcan et al. [2020] Maria-Florina Balcan, Siddharth Prasad, and Tuomas Sandholm. Efficient algorithms for learning revenue-maximizing two-part tariffs. In Proceedings of the International Joint Conference on Artificial Intelligence (IJCAI), 2020.

- Bartlett and Mendelson [2002] Peter L Bartlett and Shahar Mendelson. Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482, 2002.

- Bateni et al. [2015] MohammadHossein Bateni, Sina Dehghani, MohammadTaghi Hajiaghayi, and Saeed Seddighin. Revenue maximization for selling multiple correlated items. In Proceedings of the European Symposium on Algorithms (ESA), 2015.

- Besbes and Zeevi [2009] Omar Besbes and Assaf Zeevi. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research, 57(6):1407–1420, 2009.

- Blumer et al. [1987] Anselm Blumer, Andrzej Ehrenfeucht, David Haussler, and Manfred K Warmuth. Occam’s razor. Information processing letters, 24(6):377–380, 1987.

- Broder and Rusmevichientong [2012] Josef Broder and Paat Rusmevichientong. Dynamic pricing under a general parametric choice model. Operations Research, 60(4):965–980, 2012.

- Bubeck et al. [2017] Sébastien Bubeck, Nikhil R Devanur, Zhiyi Huang, and Rad Niazadeh. Online auctions and multi-scale online learning. Proceedings of the ACM Conference on Economics and Computation (EC), 2017.

- Buck [1943] R. C. Buck. Partition of space. Amer. Math. Monthly, 50:541–544, 1943. ISSN 0002-9890.

- Cai and Daskalakis [2017] Yang Cai and Constantinos Daskalakis. Learning multi-item auctions with (or without) samples. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), 2017.

- Cai and Zhao [2017] Yang Cai and Mingfei Zhao. Simple mechanisms for subadditive buyers via duality. In Proceedings of the Annual Symposium on Theory of Computing (STOC), 2017.

- Cai et al. [2016] Yang Cai, Nikhil R. Devanur, and S. Matthew Weinberg. A duality based unified approach to Bayesian mechanism design. In Proceedings of the Annual Symposium on Theory of Computing (STOC), 2016.

- Chawla and Miller [2016] Shuchi Chawla and J Benjamin Miller. Mechanism design for subadditive agents via an ex ante relaxation. In Proceedings of the ACM Conference on Economics and Computation (EC), 2016.

- Chawla et al. [2007] Shuchi Chawla, Jason D Hartline, and Robert Kleinberg. Algorithmic pricing via virtual valuations. In Proceedings of the ACM Conference on Economics and Computation (EC), 2007.

- Chawla et al. [2010] Shuchi Chawla, Jason D Hartline, David L Malec, and Balasubramanian Sivan. Multi-parameter mechanism design and sequential posted pricing. In Proceedings of the Annual Symposium on Theory of Computing (STOC), 2010.

- Chawla et al. [2014] Shuchi Chawla, Jason Hartline, and Denis Nekipelov. Mechanism design for data science. In Proceedings of the ACM Conference on Economics and Computation (EC), 2014.

- Cole and Roughgarden [2014] Richard Cole and Tim Roughgarden. The sample complexity of revenue maximization. In Proceedings of the Annual Symposium on Theory of Computing (STOC), 2014.

- Collins [2000] Michael Collins. Discriminative reranking for natural language parsing. Proceedings of the International Conference on Machine Learning (ICML), 2000.

- Conitzer and Sandholm [2002] Vincent Conitzer and Tuomas Sandholm. Complexity of mechanism design. In Proceedings of the Conference on Uncertainty in Artificial Intelligence (UAI), 2002.

- Conitzer and Sandholm [2003] Vincent Conitzer and Tuomas Sandholm. Applications of automated mechanism design. In UAI-03 workshop on Bayesian Modeling Applications, 2003.

- Conitzer and Sandholm [2004] Vincent Conitzer and Tuomas Sandholm. Self-interested automated mechanism design and implications for optimal combinatorial auctions. In Proceedings of the ACM Conference on Economics and Computation (EC), 2004.

- Devanur et al. [2016] Nikhil R Devanur, Zhiyi Huang, and Christos-Alexandros Psomas. The sample complexity of auctions with side information. In Proceedings of the Annual Symposium on Theory of Computing (STOC), 2016.

- Devanur et al. [2017] Nikhil R Devanur, Zhiyi Huang, and Christos-Alexandros Psomas. The sample complexity of auctions with side information. arXiv preprint arXiv:1511.02296, 2017.

- Dobzinski and Dughmi [2009] Shahar Dobzinski and Shaddin Dughmi. On the power of randomization in algorithmic mechanism design. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), 2009.

- Dobzinski and Sundararajan [2008] Shahar Dobzinski and Mukund Sundararajan. On characterizations of truthful mechanisms for combinatorial auctions and scheduling. In Proceedings of the ACM Conference on Economics and Computation (EC), 2008.

- Dudley [1987] Richard Dudley. Universal Donsker classes and metric entropy. The Annals of Probability, 15(4):1306–1326, 1987.

- Dütting et al. [2020] Paul Dütting, Thomas Kesselheim, and Brendan Lucier. An prophet inequality for subadditive combinatorial auctions. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), 2020.

- Edelman et al. [2007] Benjamin Edelman, Michael Ostrovsky, and Michael Schwarz. Internet advertising and the generalized second-price auction: Selling billions of dollars worth of keywords. The American Economic Review, 97(1):242–259, March 2007.

- Eden et al. [2021] Alon Eden, Michal Feldman, Ophir Friedler, Inbal Talgam-Cohen, and S Matthew Weinberg. A simple and approximately optimal mechanism for a buyer with complements. Operations Research, 69(1):188–206, 2021.

- Elkind [2007] Edith Elkind. Designing and learning optimal finite support auctions. In Proceedings of the ACM-SIAM Symposium on Discrete Algorithms (SODA), 2007.

- Feldman et al. [2015] Michal Feldman, Nick Gravin, and Brendan Lucier. Combinatorial auctions via posted prices. In Proceedings of the ACM-SIAM Symposium on Discrete Algorithms (SODA), 2015.

- Feldstein [1972] Martin S Feldstein. Equity and efficiency in public sector pricing: the optimal two-part tariff. The Quarterly Journal of Economics, pages 176–187, 1972.

- Goldner and Karlin [2016] Kira Goldner and Anna R Karlin. A prior-independent revenue-maximizing auction for multiple additive bidders. In Proceedings of the Conference on Web and Internet Economics (WINE), 2016.

- Gonczarowski and Nisan [2017] Yannai A Gonczarowski and Noam Nisan. Efficient empirical revenue maximization in single-parameter auction environments. In Proceedings of the Annual Symposium on Theory of Computing (STOC), pages 856–868, 2017.

- Gonczarowski and Weinberg [2018] Yannai A Gonczarowski and S Matthew Weinberg. The sample complexity of up-to- multi-dimensional revenue maximization. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), 2018.

- Guo et al. [2019] Chenghao Guo, Zhiyi Huang, and Xinzhi Zhang. Settling the sample complexity of single-parameter revenue maximization. Proceedings of the Annual Symposium on Theory of Computing (STOC), 2019.

- Hart and Nisan [2012] Sergiu Hart and Noam Nisan. Approximate revenue maximization with multiple items. In Proceedings of the ACM Conference on Economics and Computation (EC), 2012.

- Hartline and Taggart [2016] Jason Hartline and Samuel Taggart. Non-revelation mechanism design. arXiv preprint arXiv:1608.01875, 2016.

- He et al. [2014] Xinran He, Junfeng Pan, Ou Jin, Tianbing Xu, Bo Liu, Tao Xu, Yanxin Shi, Antoine Atallah, Ralf Herbrich, Stuart Bowers, and Joaquin Quinonero Candela. Practical lessons from predicting clicks on ads at Facebook. In Proceedings of the International Workshop on Data Mining for Online Advertising, 2014.

- Huang et al. [2015] Zhiyi Huang, Yishay Mansour, and Tim Roughgarden. Making the most of your samples. In Proceedings of the ACM Conference on Economics and Computation (EC), 2015.

- Jehiel et al. [2007] Philippe Jehiel, Moritz Meyer-Ter-Vehn, and Benny Moldovanu. Mixed bundling auctions. Journal of Economic Theory, 134(1):494–512, 2007.

- Koltchinskii [2001] Vladimir Koltchinskii. Rademacher penalties and structural risk minimization. IEEE Transactions on Information Theory, 47(5):1902–1914, 2001.

- Kothari et al. [2019] Pravesh Kothari, Sahil Singla, Divyarthi Mohan, Ariel Schvartzman, and S Matthew Weinberg. Approximation schemes for a unit-demand buyer with independent items via symmetries. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), 2019.

- Lavi et al. [2003] Ron Lavi, Ahuva Mu’Alem, and Noam Nisan. Towards a characterization of truthful combinatorial auctions. In Proceedings of the IEEE Symposium on Foundations of Computer Science (FOCS), 2003.

- Li and Yao [2013] Xinye Li and Andrew Chi-Chih Yao. On revenue maximization for selling multiple independently distributed items. Proceedings of the National Academy of Sciences, 110(28):11232–11237, 2013.

- Likhodedov and Sandholm [2004] Anton Likhodedov and Tuomas Sandholm. Methods for boosting revenue in combinatorial auctions. In Proceedings of the AAAI Conference on Artificial Intelligence, 2004.

- Likhodedov and Sandholm [2005] Anton Likhodedov and Tuomas Sandholm. Approximating revenue-maximizing combinatorial auctions. In Proceedings of the AAAI Conference on Artificial Intelligence, 2005.

- Matoušek and Vondrák [2001] Jiří Matoušek and Jan Vondrák. The probabilistic method. Lecture Notes, Department of Applied Mathematics, Charles University, Prague, 2001.

- Medina and Vassilvitskii [2017] Andrés Muñoz Medina and Sergei Vassilvitskii. Revenue optimization with approximate bid predictions. Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), 2017.

- Mohri and Medina [2014] Mehryar Mohri and Andrés Muñoz Medina. Learning theory and algorithms for revenue optimization in second price auctions with reserve. In Proceedings of the International Conference on Machine Learning (ICML), 2014.

- Morgenstern and Roughgarden [2015] Jamie Morgenstern and Tim Roughgarden. On the pseudo-dimension of nearly optimal auctions. In Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), 2015.

- Morgenstern and Roughgarden [2016] Jamie Morgenstern and Tim Roughgarden. Learning simple auctions. In Proceedings of the Conference on Learning Theory (COLT), 2016.

- Myerson [1981] Roger Myerson. Optimal auction design. Mathematics of Operation Research, 6:58–73, 1981.

- Oi [1971] Walter Y Oi. A Disneyland dilemma: Two-part tariffs for a Mickey Mouse monopoly. The Quarterly Journal of Economics, 85(1):77–96, 1971.

- Pollard [1984] David Pollard. Convergence of Stochastic Processes. Springer, 1984.

- Roberts [1979] Kevin Roberts. The characterization of implementable social choice rules. In J-J Laffont, editor, Aggregation and Revelation of Preferences. North-Holland Publishing Company, 1979.

- Roughgarden and Schrijvers [2016] Tim Roughgarden and Okke Schrijvers. Ironing in the dark. In Proceedings of the ACM Conference on Economics and Computation (EC), 2016.

- Rubinstein and Weinberg [2015] Aviad Rubinstein and S Matthew Weinberg. Simple mechanisms for a subadditive buyer and applications to revenue monotonicity. In Proceedings of the ACM Conference on Economics and Computation (EC), 2015.

- Sandholm [2003] Tuomas Sandholm. Automated mechanism design: A new application area for search algorithms. In Proceedings of the International Conference on Principles and Practice of Constraint Programming (CP), 2003.

- Sandholm and Likhodedov [2015] Tuomas Sandholm and Anton Likhodedov. Automated design of revenue-maximizing combinatorial auctions. Operations Research, 63(5):1000–1025, September–October 2015.

- Shalev-Shwartz and Ben-David [2014] Shai Shalev-Shwartz and Shai Ben-David. Understanding machine learning: From theory to algorithms. Cambridge University Press, 2014.

- Syrgkanis [2017] Vasilis Syrgkanis. A sample complexity measure with applications to learning optimal auctions. Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), 2017.

- Tang [2017] Pingzhong Tang. Reinforcement mechanism design. In Proceedings of the International Joint Conference on Artificial Intelligence (IJCAI), 2017.

- Tang and Sandholm [2012] Pingzhong Tang and Tuomas Sandholm. Mixed-bundling auctions with reserve prices. In Proceedings of the Conference for Autonomous Agents and Multi-Agent Systems (AAMAS), 2012.

- Vapnik and Chervonenkis [1974] Vladimir Vapnik and Alexey Chervonenkis. Theory of pattern recognition, 1974.

- Wilson [1993] Robert B Wilson. Nonlinear pricing. Oxford University Press on Demand, 1993.

- Yao [2014] Andrew Chi-Chih Yao. An n-to-1 bidder reduction for multi-item auctions and its applications. In Proceedings of the ACM-SIAM Symposium on Discrete Algorithms (SODA), 2014.

- Yee and Ifrach [2015] Hector Yee and Bar Ifrach. Aerosolve: Machine learning for humans. Open Source, 2015. URL http://nerds.airbnb.com/aerosolve/.

Appendix A Proofs from Section 3

Corollary A.1.

Let be the mechanism that maximizes expected profit over the distribution over buyers’ values. For any , with probability at least over the draw of a set of samples of size from the distribution over buyers’ values, the difference between the expected profit of and expected profit of is at most

Proof.

Let be the mechanism in that maximizes empirical profit over . With probability at least ,

| (1) | ||||

| (2) | ||||

| (3) | ||||

| (4) |

Inequality (1) follows from standard uniform convergence bounds: with probability at least ,

Inequality (2) follows from the fact that has empirical profit that is within an additive factor of from empirically optimal over the set of samples, or in other words, . Inequality (3) follows because is the empirical profit maximizer (i.e., it maximizes ). Finally, inequality (4) is a result of Hoeffding’s inequality, which guarantees that with probability at least , .

Rearranging, we get that

as claimed. ∎

Corollary A.2.

Let be a mechanism class and let be a mechanism with maximum expected profit. Given a set of samples , let be a mechanism in with empirical profit that is at least an -fraction of the empirically optimal: . With probability at least over the draw , the difference between the expected profit of and an -fraction of the expected profit of is at most :

Proof.

Let be a set of samples of buyer valuations. With probability at least ,

These inequalities follow for the same reasons as in the proof of Corollary A.1. ∎

Lemma A.3 (Shalev-Shwartz and Ben-David [70], Lemma A.2).

Let and . Then implies that .

Lemma A.4.

No matter which parameters the mechanism designer chooses in or , if all buyers simultaneously choose the tariff and the number of units that maximize their utilities, then .

Proof.

We prove this lemma for non-anonymous prices, and the lemma for anonymous prices follow since they are a special case of non-anonymous prices. For a contradiction, suppose there exists a set of buyers’ values and a non-anonymous menu of two-part tariffs with parameters in such that if is the tariff that buyer chooses and is the number of units he chooses, . Since the mechanisms are profit non-negative, we know that , where . We also know that each buyer’s value for the units he bought is greater than the price: . Therefore, . However, this contradicts Assumption 3.13, so the lemma holds. ∎

See 3.15

Proof.

A length- menu of two-part tariffs is defined by parameters. The first parameters (denoted ) define the first tariff in the menu, the second parameters (denoted ) define the second tariff in the menu, and so on. Buyer will prefer to buy units using menu entry (defined by the parameters ) so long as for any and . In total, these inequalities define hyperplanes in . In any region defined by these hyperplanes, the menu entries and quantities demanded by all buyers are fixed. In any such region, profit is linear in the fixed fees and unit prices.

In the case of non-anonymous reserve prices, the same argument holds, except that every length- menu of two-part tariffs is defined by parameters: for each buyer, we must set the fixed fee and unit price for each of the menu entries. ∎

Lemma A.5.

No matter which parameters the mechanism designer chooses in or , if all buyers simultaneously choose the bundles that maximize their utilities, then for all .

Proof.

We prove this lemma for non-anonymous prices, and the lemma for anonymous prices follow since they are a special case of non-anonymous prices. For a contradiction, suppose there exists a set of buyers’ values and a non-anonymous non-linear pricing mechanism with parameters in such that if is the bundle buyer chooses, for some . Since the mechanisms are profit non-negative, we know that , where . We also know that each buyer’s value for the units he bought is greater than the price: . Therefore, . However, this contradicts Assumption 3.13, so the lemma holds. ∎

Definition A.6 (Profit non-negative non-linear pricing mechanisms).

In the case of anonymous prices (respectively, non-anonymous), let (respectively, ) be the set of mechanism parameters such that for each buyer and each allocation , the seller’s utility is non-negative: The set of profit non-negative non-linear pricing mechanisms is defined by parameters in (respectively, ).

See 3.16

Proof.

We begin by analyzing the case where there are anonymous prices. By Lemma A.5, the mechanism designer might as well set the price of any bundle such that for some to . Therefore, every non-linear pricing mechanism is defined by parameters because that is the number of different bundles and there is a price per bundle. Buyer will prefer the bundle corresponding to the quantity vector over the bundle corresponding to the quantity vector if . Therefore, there are at most hyperplanes in determining each buyer’s preferred bundle — one hyperplane per pair of bundles. This means that there are a total of hyperplanes in such that in any one region induced by these hyperplanes, the bundles demanded by all buyers are fixed and profit is linear in the prices of these bundles.

In the case of non-anonymous prices, the same argument holds, except that every non-linear pricing mechanism is defined by parameters — one parameter per bundle-buyer pair. ∎

Definition A.7 (Additively decomposable non-linear pricing mechanisms).

Additively decomposable non-linear pricing mechanisms are a subset of non-linear pricing mechanisms where the prices are additive over the items. Specifically, if the prices are anonymous, there exist functions for all such that for every quantity vector , . If the prices are non-anonymous, there exist functions for all and such that for every quantity vector , .

Lemma A.8.

Let and be the classes of additively decomposable non-linear pricing mechanisms with anonymous and non-anonymous prices, respectively. Then is

and is -delineable.

Proof.

In the case of anonymous prices, any additively decomposable non-linear pricing mechanism is defined by parameters. As in the proof of Lemma 3.16, there are a total of hyperplanes in such that in any one region induced by these hyperplanes, the bundles demanded by all buyers are fixed and profit is linear in the prices of these bundles.

In the case of non-anonymous prices, the same argument holds, except that every non-linear pricing mechanism is defined by parameters — one parameter per item, quantity, and buyer tuple. ∎

See 3.17

Proof.

In the case of anonymous prices, every item-pricing mechanisms is defined by prices , so the parameter space is . Let be the buyer with the highest value for item . We know that item will be bought so long as . Once the items bought are fixed, profit is linear. Therefore, there are hyperplanes splitting into regions where profit is linear.

In the case of non-anonymous prices, the parameter space is since there is a price per buyer and per item. The items each buyer is willing to buy is defined by hyperplanes: . So long as these preferences are fixed, profit is a linear function of the prices. Therefore, there are hyperplanes splitting into regions where profit is linear. ∎

See 3.18

Proof.

For a given valuation vector , let be the highest bidder for item and let be the second highest bidder. Under anonymous prices, item will be bought so long as . If buyer buys item , his payment depends on whether or not . Therefore, there are hyperplanes splitting into regions where profit is linear. In the case of non-anonymous prices, the only difference is that the parameter space is . ∎

Definition A.9 (Mixed-bundling auctions with reserve prices (MBARPs)).

MBARPs are defined by a parameter and reserve prices . Let be a function such that if some buyer receives the grand bundle under allocation and 0 otherwise. For an allocation , let be the items not allocated. Given a valuation vector , the MBARP allocation is

Using the notation

buyer pays

See 3.19

Proof.

An MBARP is defined by parameters since there is one reserve per item and one allocation boost. Let be the total number of allocations. Fix some valuation vector . We claim that the allocation of any MBARP is determined by at most hyperplanes in . To see why this is, let and be any two allocations and let and be the bundles of items not allocated. Consider the hyperplanes defined as

In the intersection of these hyperplanes, the allocation of the MBARP is fixed.

By a similar argument, it is straightforward to see that hyperplanes determine the allocation of any MBARP in this restricted space without any one bidder’s participation. This leads us to a total of hyperplanes which partition the space of MBARP parameters in a way such that for any two parameter vectors in the same region, the auction allocations are the same, as are the allocations without any one bidder’s participation. Once these allocations are fixed, profit is a linear function in this parameter space. ∎

Definition A.10 (Affine maximizer auction).

An AMA is defined by a weight per buyer and a boost per allocation . The AMA allocation is the one which maximizes the weighted social welfare, i.e., Using the notation

each buyer pays

See 3.20

Proof.

Let be the total number of allocations and let be a parameter vector where the first components correspond to the bidder weights for , the next components correspond to for , the next components correspond to for all , the next components correspond to for every allocation , and the final components correspond to for all allocations and all bidders . In total, the dimension of this parameter space is at most . Let be a valuation vector. We claim that this parameter space can be partitioned using hyperplanes into regions where in any one region , there exists a vector such that for all .

To this end, an allocation will be the allocation of the AMA so long as for all allocations . Since the number of different allocations is at most , the allocation of the auction on is defined by at most hyperplanes in . Similarly, the allocations are also determined by at most hyperplanes in . Once these allocations are fixed, profit is a linear function of this parameter space.

The proof for VVCAs follows the same argument except that we redefine the parameter space to consist of vectors where the first components correspond to the bidder weights for , the next components correspond to for , the next components correspond to for all , the next components correspond to the bidder-specific bundle boosts for every quantity vector and bidder , and the final components correspond to for every quantity vector and every pair of bidders . The dimension of this parameter space is at most .

Finally, the proof for -auctions follows the same argument as the proof for AMAs except there are zero bidder weights. Therefore, the parameter space consists of vectors with components corresponding to for every allocation . ∎

Lemma A.11.

For all and all , .

Proof.

By definition of ,

From the other direction,

Therefore, . ∎

See 3.22

Proof.

We know that with probability at least over the draw of a sample

for all mechanisms ,

We also know from Lemma A.11 that

Therefore, the theorem statement holds. ∎

See 3.21

Proof.

A length- lottery menu is defined by parameters. The first parameters (denoted ) define the first lottery in the menu, the second parameters (denoted ) define the second lottery in the menu, and so on. The buyer will prefer the menu entry (defined by the parameters ) so long as for any . In total, these inequalities define hyperplanes in . In any region defined by these hyperplanes, the menu entry that the buyer prefers is fixed. Next, for each menu entry , there are hyperplanes determining the vector , and thus the cost . These vectors have the form Thus, there are a total of hyperplanes determining the costs. Let be the union of all hyperplanes. Within any connected component of , the menu entry that the buyer buys is fixed and for each menu entry, is fixed. Therefore, profit is a linear function of the prices . ∎

A.1 Additional lottery results

Lotteries for a unit-demand buyer.

Recall that if the buyer is unit-demand, then for any bundle , . We assume that under a lottery with a unit-demand buyer, the buyer will only receive one item, and the probability that item is item is . Thus, we assume that . Since is their value for item times the probability they get that item, their expected utility is , as in the case with an additive buyer. Therefore, the following theorem follows by the exact same proof as Lemma 3.21.

Theorem A.12.

Let be the class of functions defined in Section 3.4.4. Then is

Lotteries for multiple unit-demand or additive buyers.

In order to generalize to multi-buyer settings, we assume that there are units of each item for sale and that each buyer will receive at most one unit of each item. The buyers arrive simultaneously and each will buy the lottery that maximizes her expected utility. Thus, the following is a corollary of Lemma 3.21.

Theorem A.13.

Let be the class of functions defined in Section 3.4.4. Then is

A.2 Mixed bundling auctions

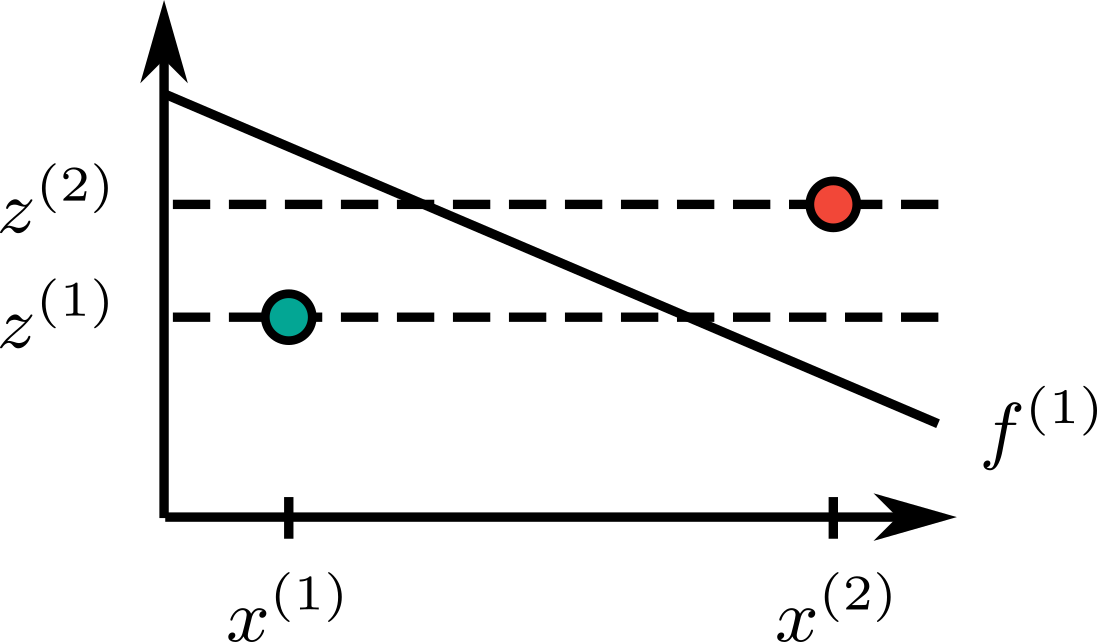

Mixed bundling auctions (MBAs) are defined by a single parameter . They correspond to a -auction where if some buyer receives the grand bundle under allocation and 0 otherwise. The class of MBAs is particularly simple, and we prove an even tighter bound on the Rademacher complexity of MBAs than that guaranteed by Theorem 3.9. Our analysis requires us to understand how the profit of a -MBA on a single bidding instance changes as a function of . We take advantage of this function’s structural properties, first uncovered by Jehiel et al. [50]: no matter the number of buyers and no matter the number of items, there exists an easily characterizable value such that the function in question is increasing as grows from 0 to , and then it is non-increasing as grows beyond . This is depicted in Figure 6.

Intuitively, represents the number at which has grown so large that the MBA has morphed into a second price auction on the grand bundle. As a result, no matter how much larger grows beyond , the value of no longer factors into the profit function. This simple structure allows us to prove the strong generalization guarantee described in Theorem A.14.

Theorem A.14.

Let be the class of MBAs. Then .

Proof.

First, we show that the pseudo-dimension of the class of -buyer, -item MBAs is at most 2. Let be a set of -buyer valuation functions that can be shattered by a set of MBAs. This means that there exist witnesses such that each MBA in induces a binary labeling of the samples of (whether the profit of the MBA on is at least or strictly less than ). Since is shatterable, we can thus label in every possible way using MBAs in .

Now, fix one sample . We denote the profit of the -MBA on as a function of as . From Lemma A.15, we know that there exists , such that is non-decreasing on the interval and non-increasing on the interval . Therefore, there exist two thresholds and such that is below its threshold for , above its threshold for , and below its threshold for . Now, merge these thresholds for all samples on the real line and consider the interval between two adjacent thresholds. The binary labeling of the samples in on this interval is fixed. In other words, for any sample , is either at least or strictly less than for all . There are at most intervals between adjacent thresholds, so at most different binary labelings of . Since we assumed is shatterable, it must be that , so

Finally, we show that the pseudo-dimension of the class of -buyer, -item MBAs is at least 2 by constructing a set that can be shattered by the set of MBAs. To construct this set of samples , let

Finally, let buyers 3 through have all-zero valuations in both and and let the cost function be 0 for all allocations.