Optimal Invariant Tests in an Instrumental Variables Regression With Heteroskedastic and Autocorrelated Errors ††thanks: Preliminary results were presented at seminars organized by BU, Brown, Caltech, Harvard-MIT, PUC-Rio, University of California (Berkeley, Davis, Irvine, Los Angeles, Santa Barbara, and Santa Cruz campuses), UCL, USC, and Yale, at the FGV Data Science workshop, and at conferences organized by CIREq (in honor of Jean-Marie Dufour), Harvard University (in honor of Gary Chamberlain), Oxford University (New Approaches to the Identification of Macroeconomic Models), the Tinbergen Institute (Inference Issues in Econometrics), and Vanderbilt (Identification in Econometrics. This study was financed in part by the Coordenação de Aperfeiçoamento de Pessoal de Nível Superior - Brazil (CAPES) - Finance Code 001. This research was also supported in part by the University of Pittsburgh Center for Research Computing through the resources provided.

Abstract

This paper uses model symmetries in the instrumental variable (IV) regression to derive an invariant test for the causal structural parameter. Contrary to popular belief, we show that there exist model symmetries when equation errors are heteroskedastic and autocorrelated (HAC). Our theory is consistent with existing results for the homoskedastic model (Andrews, Moreira, and Stock (2006) and Chamberlain (2007)). We use these symmetries to propose the conditional integrated likelihood (CIL) test for the causality parameter in the over-identified model. Theoretical and numerical findings show that the CIL test performs well compared to other tests in terms of power and implementation. We recommend that practitioners use the Anderson-Rubin (AR) test in the just-identified model, and the CIL test in the over-identified model.

1 Introduction

In a regression model, the explanatory variable can be correlated with the error due to omitted variables. To solve this endogeneity problem, practitioners often look for instrumental variables (IVs). The instruments are valid if they are correlated with the endogenous variable but uncorrelated with the error. The instruments are said to be weak when their correlation with the endogenous explanatory variable is small. Under weak identification, standard estimators may be far from the true causality parameter, and commonly-used tests do not have correct size. Searching for valid IVs can, unfortunately, narrow down the choices to only weak instruments. Furthermore, techniques proposed to mitigate these problems can themselves have limitations. Cruz and Moreira (2005) show that the second-order bias for the two-stage least squares (2SLS) estimator is unreliable under weak identification. Lee, McCrary, Moreira, and Porter (2020) point out that the standard F¿10 rule for the t-ratio leads to important size distortions in practice, even in the just-identified model. They propose a novel tF procedure if practitioners wish to use the F statistic combined with the t-ratio.

With cross-sectional data, the errors in the IV model can be heteroskedastic. With time-series or panel data, errors can also be autocorrelated. For these more complex data generating processes (DGPs) for the errors, the asymptotic variance matrix of sample IV moments can be quite different from the one obtained from serially uncorrelated and homoskedastic errors. Consistent estimators for this variance are readily available: see Newey and West (1987) and Andrews (1991).

Andrews, Moreira, and Stock (2006) (abbreviated as AMS06 hereinafter) and Chamberlain (2007) show that symmetries exist in the IV model with homoskedastic errors when the variance is fixed. Up until the emergence of this project (Moreira and Ridder (2017)), it was widely accepted that there are no symmetries in the IV model with heteroskedastic and/or autocorrelated (HAC) errors. Indeed, at first sight, invariance does not seem applicable to the HAC-IV model. We argue that this view is incorrect. The HAC-IV has model symmetries if the HAC variance matrix is assumed to be known but not fixed, an important distinction from the method used by AMS06, Chamberlain (2007), and related papers, for homoskedastic and uncorrelated errors. We find the largest affine group which preserves the null hypothesis for the causality parameter. This allows us to find weights for the novel conditional integrated likelihood (CIL) test. This test is invariant and can be interpreted as the limit of a sequence of conditional weighted-average power (WAP) tests. Andrews and Mikusheva (2020) provide a general framework for decision rules in GMM. They do not propose a two-sided test, which is our main goal in this paper. Unlike the CIL test, other (limits of) conditional WAP tests can be severely biased, as the critique by Moreira and Moreira (2019) asserts.

In the just-identified model, the AR test is optimal within the classes of either unbiased or invariant tests, assuming the reduced-form variance mentioned above is known; see Moreira (2002, 2009), AMS06, and Moreira and Moreira (2019). In the over-identified model, the AR test is not efficient under the usual asymptotic theory. Several proposed tests are asymptotically optimal under standard asymptotics. Moreira and Ridder (2020) show that the Lagrange Multiplier/score (LM) and the conditional quasi-likelihood ratio (CQLR) tests can suffer severe power deficiencies when distinguishing the null from the alternative hypothesis should be easy. The weighted-average strongly unbiased (SU) tests are not invariant for arbitrary weight choices. Furthermore, implementing the SU tests requires linear programming. Although algorithms are readily available, it requires the calculation of a density ratio. If not dealt with properly, the computation can exceed the numerical accuracy of computer packages. This leaves, as the main contender, the true conditional likelihood ratio (CLR) test; see Andrews and Mikusheva (2016) and Moreira and Moreira (2019). The CLR test does not have a closed-form expression with HAC errors, and requires numerical optimization. We show some important limitations to the implementation of the CLR test. We prove here that we can compactify the parameter space for the optimization. This is important, and avoids some natural pitfalls if the parameter space is unbounded. However, we find that the number of initial points needed for the optimization algorithm depends on the errors’ DGPs and on the instrument strength. In practice, we document the need to include several initial points when errors are HAC. Worse yet, the optimization can be even more troublesome when computing the conditional quantiles. This happens because the model is misspecified for DGPs under the alternative hypothesis when we simulate these null conditional quantiles.

We then compare power between the AR, CLR, and CIL tests. For homoskedastic errors, the CLR test simplifies to the CQLR test, which has a closed-form expression. Andrews, Moreira, and Stock (2004) use these symmetries to choose weights for a conditional WAP test. Power gains beyond the CQLR are small, as the latter performs near a two-sided power envelope for invariant tests with homoskedastic errors. It is, however, reassuring that the CIL test performs on an equal footing with the CQLR test. For HAC errors, the IV model is much more complex than the simple homoskedastic model. Even reducing the data using invariance, several parameters can affect the performance of AR, LM, CQLR, CLR, CIL, and any other invariant tests. We choose the same designs as Moreira and Moreira (2019) and Moreira and Ridder (2020), to forestall any criticism that we may be selecting parameter combinations which favor the CIL test. To bypass the aforementioned numerical problems for the CLR test, we choose to implement an infeasible version of the CLR test, in case better optimization methods are found in the future. This implementation selects the unknown value of the structural parameter as one of the initial points in the likelihood optimization. Overall, the CIL test outperforms the AR and CLR tests, with significant power gains for several of these designs.

This paper is organized as follows. Section 2 introduces the IV model, and describes the family of similar tests robust to heteroskedastic-autocorrelated errors. Section 3 shows model symmetries when the asymptotic variance can change with data transformations. We present different representations of the CIL test. One of them is important to show that this test is invariant, as discussed later. The other expression is useful to derive confidence sets based on the CIL test. Section 4 shows that the CIL test can have very good power (the supplement provides further evidence in favor of the CIL test). The more technical details behind model invariance are left to the end of the paper. Section 5 shows that the theory of AMS06 is a special case of ours when the variance has a Kronecker product form. Section 6 derives the theory of conditional invariant tests. It shows that the AR, CLR, and Lagrange Multiplier/score (LM) tests are also invariant. Section 7 discusses the next steps in this research agenda and highlights the methodological importance of distinguishing between parameters being known and being fixed. The online appendix provides the proofs for our theory.

2 The IV Model and Statistics

2.1 The HAC-IV model

Consider the following structural equation for the -th observation of the variable :

| (2.1) |

where is an endogenous random variable with corresponding coefficient , is a fixed vector of exogenous control variables with corresponding vector of coefficients , and is an error term. We also consider the following reduced-form equation for the endogenous explanatory random variable:

| (2.2) |

where is a fixed vector of instrumental variables (IVs) with corresponding coefficients , , and an error term . It may be possible that , so that is an endogenous random variable. Equations (2.1) and (2.2) can be presented in the following matrix format:

| (2.3) | |||||

where , , , , and . We assume that the matrix has full column rank .

Our focus is on testing the null hypothesis against the two-sided alternative hypothesis . It is convenient to transform the IV matrix to which is orthogonal to matrix , . For a conformable matrix , we define and . We write

| (2.4) |

where . By substituting from the reduced-form equation (2.4) to the structural equation (2.3), we have

| (2.5) |

where and . The reduced-form equations (2.4) and (2.5) can be written in the following matrix notation:

| (2.6) |

where , , .

Moreira and Moreira (2019) consider . Because the transformed IV matrix is orthogonal to , we have

| (2.7) |

where and . Commonly-used estimators and tests depend on the data through and estimators for the variance of . For example, consider the t-statistic based on the 2SLS estimator

| (2.8) |

The estimator is clearly a ratio of quadratic forms of . In our notation, the t-statistic (also known as the Wald statistic) is

| (2.9) |

where and is the second column of .

The two-sided t-test rejects the null when is larger than the quantile of a standard normal distribution. For this critical value to be reliable, the t-statistic needs to be approximately normally distributed. This happens when the number of observations increases and the IVs are strong. In applied work, however, it can be difficult to find variables that are also uncorrelated with the error terms of the structural equation (2.1). In practice, the search for valid IVs may lead to choices which are weakly correlated with the endogenous explanatory variable . As a result, the null rejection probability for the t-test can be sensitive to the quality of the instruments; see Nelson and Startz (1990), Dufour (1997), and Staiger and Stock (1997). In particular, the null rejection probability can be much larger than the usual nominal level. This problem spurs us to develop similar tests which, by construction, have null rejection probability equal to nominal level , no matter how weak the IVs are.

2.2 Similar Tests

For simplicity, we start by assuming that is normally distributed with zero mean and is known. The online appendix relaxes this assumption, at the cost of asymptotic approximations. For example, the t-statistic for known (to streamline notation, we omit the subscript from ) would be

| (2.10) |

For other test statistics, it is convenient to transform into the pair of statistics, being pivotal and independent of the statistic . Moreira and Moreira (2019) and Moreira and Ridder (2020) define

| (2.11) | ||||

for and . Their marginal distributions are given by

| (2.12) | |||||

Examples of test statistics based on and are the Anderson-Rubin (AR), the score or Lagrange multiplier (LM), and the quasi likelihood ratio (QLR) statistics. Anderson and Rubin (1949) propose a pivotal test statistic. In our model, the Anderson-Rubin statistic is given by

| (2.13) |

Moreira and Moreira (2019) derive the statistic under the same distributional assumption that we make here. The two-sided statistic is

| (2.14) |

The and statistics have chi-square distributions with and one degrees of freedom, respectively. The AR and LM tests reject the null when their respective statistics are larger than their chi-square quantiles. By construction, both tests have correct size at level .

Kleibergen (2005), among others, adapts the likelihood ratio statistic for homoskedastic errors to HAC errors. The quasi-likelihood ratio statistic is

| (2.15) |

where . Andrews (2016) proposes tests based on the following combination:

| (2.16) |

where . Unlike the and statistics, neither the nor the statistics are pivotal. We follow Moreira and Moreira (2019) and reject the null hypothesis when the test statistic is larger than , which is the null quantile conditional on . Writing a test statistic as we can compute the conditional rejection probability under the null:

| (2.17) |

This probability does not depend on because the distribution of under the null is pivotal. By construction, the conditional null quantile satisfies

| (2.18) |

Consequently, the unconditional null rejection probability is ,

| (2.19) |

For example, the conditional test based on the statistic rejects the null when this statistic is larger than its null conditional quantile. If the statistic is pivotal, like the and statistics, the conditional quantile collapses to the null unconditional quantile.

The and statistics depend on only through the and statistics. Moreira and Ridder (2020) show that the statistic has useful information beyond the Anderson-Rubin and score statistics when the covariance matrix does not have a Kronecker product structure. For that reason, we recommend the use of conditional tests based on either a likelihood ratio statistic or a WAP statistic to be introduced here. These tests take advantage of information beyond the Anderson-Rubin and score statistics.

The likelihood ratio statistic based on is

| (2.20) |

where can be written in terms of the pivotal statistic and the complete statistic ; see Moreira and Moreira (2019). In the appendix, we show that this statistic can be written as

| (2.21) |

where . Hence, is associated to the GMM objective function based on the moment and the continuously-updating weighting matrix; see Andrews and Mikusheva (2016) for the general case. The statistic does not have a closed-form solution and requires numerical searching methods. We instead use invariance to find an integrated likelihood test.

3 Invariance and the CIL Test

Contrary to popular belief, the IV model with HAC errors presents symmetries.111An econometric model is a (parametric, semi-parametric, or non-parametric) family of probability measures for the data . Consider the transformations on the data given by a group . This action yields a transformation given by for any Borel set . The model is said to be symmetric when for every and . The theory developed for the IV model thus far assumes the variance matrix is fixed. This assumption prevents us from finding symmetries with more general error DGPs. In this paper, we instead assume that the variance is known, but not fixed.

To explain the symmetries present in the IV model, first consider a simple example, in which , where is unknown. We want to test the null hypothesis against , treating as a nuisance parameter. For any scalar , the transformed data has distribution . This simple model is then symmetric (or said to be preserved) for the multiplicative group . The transformation preserves the null (and therefore, the alternative) because the mean of is zero if and only if the mean of is zero. The sufficient statistic for is the sample mean and the variance estimator . The transformation above induces a change in the space of sufficient statistics: the pair and become and , respectively. If these transformations preserve the hypothesis-testing problem and the original data are supportive of a hypothesis, the transformed data should be equally supportive of the same hypothesis. This is called the invariance principle. Therefore, the test statistic should be the same whether computed from the original or from the transformed data; in other words, the test has to be invariant. Any invariant test can be written as a function of the largest invariant statistic. In this example, the maximal invariant is then . Its distribution depends only on and has a monotone likelihood ratio property. As a result, the uniformly most powerful invariant (UMPI) test rejects the null when is sufficiently large. We refer interested readers to Eaton (1989) and Lehmann and Romano (2005) for the theory of optimal tests.

Now, consider instead the case in which is known. The multiplicative group does not preserve the model if we assume to be fixed. We would have to consider a much smaller group in which only (this restriction is in perfect analogy to the sign group defined by AMS06, as we shall see in Section 5). However, this transformation only reduces the sufficient statistic to the maximal invariant and . How, then, can we use the model symmetries to obtain a further reduction? One possibility is to distinguish the assumption of a known variance from the assumption of a fixed variance. The distinction hinges on whether we actually know and treat it as fixed, even after we transform the data. If an outsider tells us the value of , this person would give a different answer if we asked what the variance is after multiplying the data by a nonzero scalar. The person reports a known, but not fixed, variance. We can still get an optimal test if we restrict ourselves to unbiased tests. Because our simple model belongs to a one-parameter exponential family, we automatically find that the uniformly most powerful unbiased (UMPU) test rejects the null hypothesis for large values of .

Instead, we can take the variance as both part of the data and the parameter space. The sufficient statistic is now the pair and , while the parameters are and also . The same multiplicative group transforms the sufficient statistic to and , and induces a change in the mean from to and the variance from to . The maximal invariant is then . This statistic has a noncentral chi-square distribution, where the noncentrality parameter is zero if and only if the null hypothesis is true. Because this distribution also has a monotonic likelihood ratio property, we again obtain a UMPI test that rejects the null hypothesis if is large.

In this simple canonical model, the UMPU and UMPI tests are the same. This is not a coincidence: if a UMPU test is unique (up to sets of measure zero) and there exists a UMPI test with respect to some group of transformations, then both coincide (up to sets of measure zero). For the IV model, however, there are no uniformly most powerful tests. In perfect analogy to our canonical model, there are two lines of research in the IV model. Moreira and Moreira (2019) seek optimal two-sided tests within a restricted class of tests (the so-called SU tests) by fixing a long-run reduced-form variance matrix, i.e., they consider the known and fixed case. In this paper, we instead explore model symmetries by taking the reduced-form variance to be known, but not fixed. As in the canonical model above, we prefer not to take a stance on which thought experiment is more suitable. We consider both approaches to be useful, leading to new insights in the IV model.

If the error variance matrix in the instrumental variable regression is considered known –but not fixed– then the model satisfies some natural symmetries. The main contribution of this paper is that we propose a test that is invariant for the largest data transformation that leaves the model and null hypothesis unchanged. The novel test, called the conditional integrated likelihood (CIL) test, is invariant and the limit of WAP tests. The weights are derived from relatively invariant measures on the parameter space. The weights of the transformed parameters are then proportional to the weights of the original parameters. The test statistic is the ratio of the integrated likelihoods of the parameter space under the null and alternative hypotheses. As a result, the invariance of the model combined with the proportional effect of the transformation on the weights make the CIL test invariant to the transformation, as required.

3.1 Model-Preserving Transformations in the HAC-IV Model

To understand model symmetries, it is convenient to transform the random matrix into

| (3.1) |

so that the mean of the first column of is zero under the null. The distribution of is

| (3.2) |

where , , and

| (3.3) |

We partition the inverse variance as

| (3.6) | |||||

For , the variance matrix trivially has a Kronecker structure, as defined in Section 5. Hence, AMS06 is directly applicable. In particular, the Anderson-Rubin test is the UMPI test in the just-identified model (); see Comment 2 following Corollary 1 of AMS06.222AMS06’s optimality result for invariant tests when can be seen from the perspective of unbiased tests. Moreira (2002, 2009) shows that the Anderson-Rubin test is uniformly most powerful unbiased (UMPU). If there is a UMPI test, then the Anderson-Rubin test must be the one; see Theorem 6.6.1 of Lehmann and Romano (2005).

For , we recommend a novel WAP test. The weights are based on invariance arguments. To show the model symmetries, we consider the affine group of transformations of :

| (3.7) |

If we consider to be fixed, we have to impose restrictions on and/or for the transformation to preserve the model, so that

| (3.8) |

If the variance matrix is known but not fixed, it changes with the transformation. If is a known variance matrix, so is .

Partitioning into -dimensional vectors and into matrices:

| (3.9) |

we find that the expectation of the transformed becomes

| (3.10) |

To preserve the null hypothesis , the first sub-vector of the mean has to be zero for all values of . This forces and . In the original model, the mean of is proportional to the mean of . To preserve the model, the two subvectors of the transformed mean must be proportional to each other, which forces and

| (3.11) |

for all . This implies that with being constants of proportionality, and a matrix. As a result,

| (3.12) |

where is a lower triangular matrix. Therefore, transforms the data to

| (3.13) |

We use the transpose of so that the associated transformation is a left action. This transformation leaves the model unchanged: it preserves the null and the proportionality of the subvectors of the mean of . Specifically,

| (3.14) |

If the matrix is invertible, as we assume here, then and must be non-singular.333Therefore, and are non-zero elements. This means that and , respectively, the groups of invertible matrices and of invertible lower-triangular matrices (with matrix multiplication as the group operator).

If the original data are supportive of the null hypothesis, then the transformed data should be equally supportive of this hypothesis. The test should be the same whether it is computed from the original or from the transformed data, i.e. the test should be invariant to the transformation . As we show later, the AR, LM, CQLR, and CLR tests are invariant to the group of transformations presented above. Without further restrictions on the weight , the CLC test may be sensitive to this transformation. Likewise, the weighted-average-power SU test proposed by Moreira and Moreira (2019) may also change with data transformations. As a result, the CLC and SU tests may have power that changes with the data transformation. Next, we propose a conditional integrated weighted likelihood test that is invariant to . This test does not have the undesirably low power of WAP tests based on generic weights documented by Moreira and Moreira (2019).

3.2 The CIL Test

Consider an integrated likelihood () statistic which is the ratio of two terms. The numerator is the integrated likelihood over with respect to the Lebesgue measure and over with respect to . The denominator is the density of the pivotal statistic under the null hypothesis. In Appendix A, we show the statistic is

up to a multiplication by . We also prove this integral is finite in the over-identified case . The conditional (on ) integrated likelihood (CIL) test based on (3.2) is invariant to the transformation because both the statistic and its conditional quantile have the same proportionality multiplier with respect to . Furthermore, the CIL test is the limit of a sequence of WAP tests. We relegate the theory and proofs to Section 6. Here, we focus on the implementation of the CIL test.

The integral defined in (3.2) is improper, which can create computational difficulties. We circumvent this problem by changing variables, so that the integral is proper. This is convenient for the numerical integration that we use to compute the statistic. First, we standardize the vector to have norm one:

| (3.16) |

We note that and also that

| (3.17) |

Therefore,

By changing variables following

| (3.19) |

the statistic becomes

where . Because

| (3.21) |

the statistic simplifies to

which is easier to compute.

The statistic can be compared to the statistic that integrates the likelihood with respect to the Lebesgue measure without the weights :

(The derivation of is analogous to the statistic, as shown in Appendix A.) Numerically, the computation of or is equally difficult. Without the weights , the statistic does not yield an invariant test when . Hence, the test suffers the power problems documented by Moreira and Moreira (2019).

The representation of in terms of and is convenient to prove that the CIL test is invariant to the transformation (3.13). However, the approach can be unnecessarily challenging when testing for different levels of . This pitfall can be important to derive confidence regions, which consist of all values of which are not rejected by the CIL test. For numerical stability, we instead recommend representing in terms of the original data, and .

Algebraic manipulations show that

By changing variables

| (3.25) |

and following steps analogous to the derivation of (3.2), we show in Appendix A that

The factor can be ignored in the computation of the CIL test, as it is directly absorbed by the critical value function. Hence, we suggest implementing the conditional test based on the statistic.

There are also connections between the statistic and the statistic. The statistic maximizes, with respect to ,

| (3.27) |

which is the term inside the brackets of (3.2). The statistic integrates the exponential of this term after two corrections. The first correction, , arises from integration with respect to the Lebesgue measure . The second correction ensures that the test is two-sided and invariant, so that we avoid the one-sided power behavior in parts of the parameter space. In the next section, we show some advantages of the CIL test over the AR and CLR tests.

4 Numerical Simulations

Here, we provide numerical simulations for the AR, CLR, CIL, and CIL0 tests. All results reported here are for and only one level of instrument strength based on 1,000 Monte Carlo replications for power and 1,000 simulations to approximate the tests’ critical value function. In the supplement, we provide two levels of identification strength and consider . For reasons explained below, a reliable implementation for the CLR test is computationally intensive. Because of this, the supplemental power plots are limited to only 200 replications and 200 simulations for the conditional quantile.

We first illustrate numerical problems with likelihood optimization and integration. Some of these difficulties arise even in the simple case in which errors are homoskedastic. We focus on tests with significance level 5% for testing . We set the parameter for and set , where is a -dimensional vector of ones and is a measure of the IVs’ strength. The variance of structural-form errors is one and their correlation is . We present plots for the power envelope and power functions against various alternative values of . We plot power as a function of the rescaled alternative , which reflects the difficulty of making inference on for different instruments’ strength.

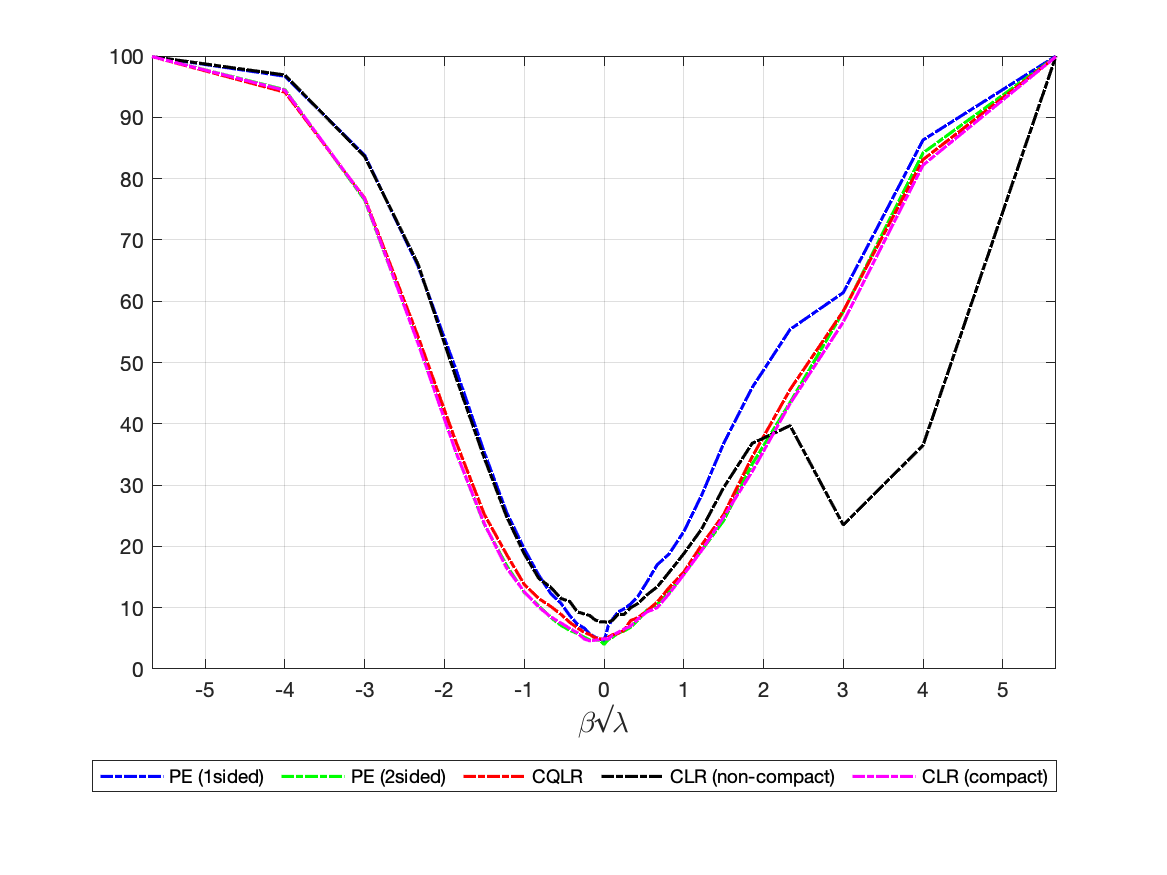

(Likelihood Optimization)

Figure 1 presents the one-sided and two-sided power envelope for invariant similar tests. These power envelopes are derived analytically by Mills, Moreira, and Vilela (2014) and Andrews, Moreira, and Stock (2006), respectively; see earlier theory by Andrews, Moreira, and Stock (2004). This early work also shows these power bounds are valid for all invariant tests which have correct size. We also plot power curves for the CQLR test as well as two numerical optimization strategies to obtain the CLR test. The first randomly draws the initial point for the search optimization algorithm in (2.20) for . Here, we consider the uniform distribution over . The second one relies on the fact that we can maximize the likelihood over a compact set, without loss of generality. We can write the likelihood ratio statistic as

| (4.1) |

where the maximization is over the compact set . The initial point is drawn from a uniform distribution over that same set. Recall that the CQLR and CLR tests are theoretically identical when errors are homoskedastic. Any power difference between the CQLR test and these numerical implementations for the CLR test arises from failures in the likelihood optimization.

The power upper bounds are useful to understand the difficulty in the likelihood optimization behind the CLR test. Both CQLR and CLR tests based on optimization over the compact set for perform alike. These two tests have power very close to the two-sided power envelope. The CLR test based on a draw-and-search for the optimal fails remarkably. In the first graph, this implementation has power above the two-sided power envelope and close to the one-sided power bound for parts of the parameter space. Furthermore, this implementation must fail to deliver a test with correct size. Indeed, the implementation for the CLR test over the whole real line has size close to 10% instead of the correct 5% level. To make matters even worse, the second plot in Figure 1 shows bad behavior associated with the sample implementation of the CLR test. The power can even be close to zero for parts of the parameter space.

Of course, one could simply use the CQLR test for the homoskedastic case. The lesson learned here is that likelihood optimization does matter for the power performance of the CLR test in general. In more complex designs (i.e., non-Kronecker error variance), drawing a unique initial point is far from sufficient. Our experience is that likelihood maximization for the implementation of the CLR test can be very slow and unreliable. This is particularly true when several initial points are required, as happens in some designs below.

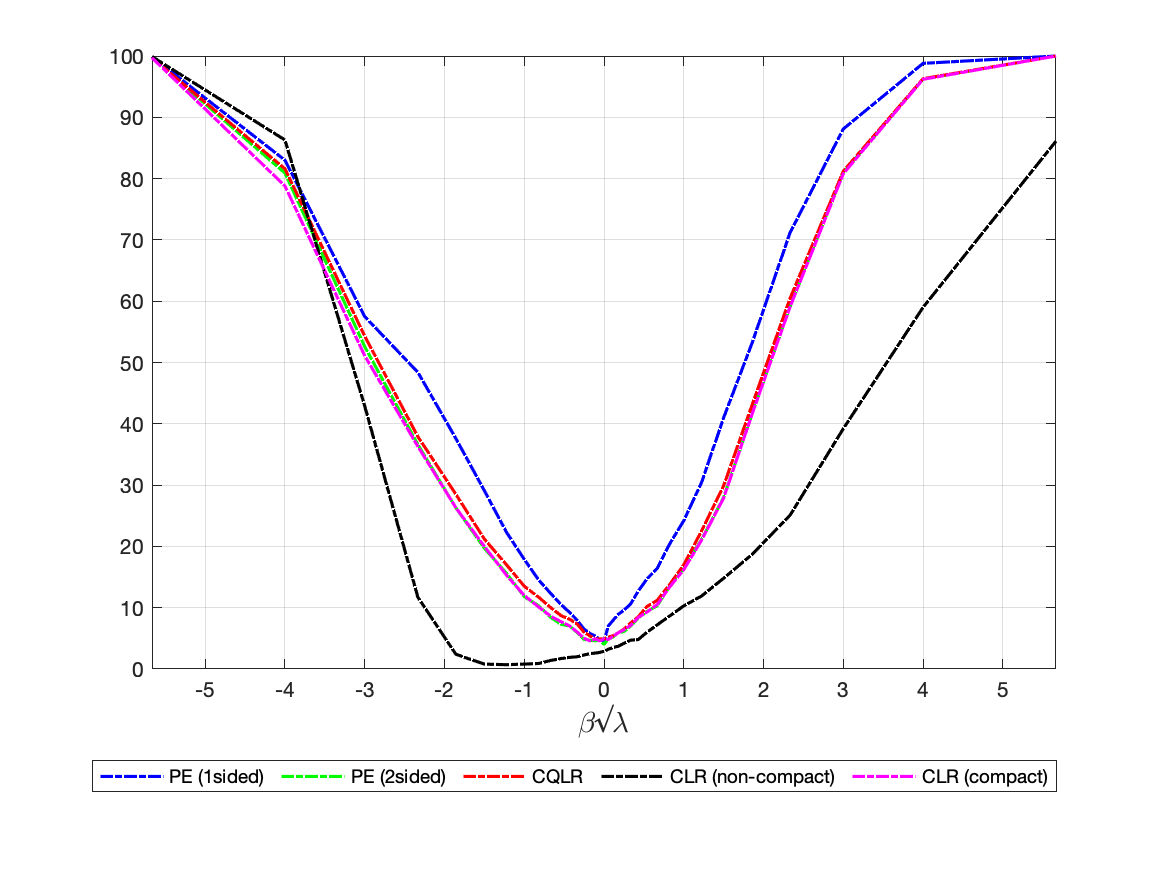

(Integrated Likelihood)

Figure 2 presents power for the AR, CQLR, CIL, and CIL0 tests. The CQLR and CIL tests have comparable power and outperform the AR test. These plots are a reassurance that the CIL test performs well in scenarios more favorable to CQLR. The CIL0 test has behavior quite different from the CIL test. The dissimilar behavior of the CIL and CIL0 tests illustrates that tests based on likelihood integration are sensitive to weight choices. While the CIL and CIL0 tests perform comparably when increases, they have distinct properties when IVs are weak. For one side of the alternative, the power of CIL0 is smaller than that of the CQLR and CIL tests. For the other side of the alternative, it actually has larger power. Therefore, the CIL0 behaves as a one-sided test. The CIL0 test being biased means the null rejection probability is smaller for some alternatives than under the null. This undesirable feature of the CIL0 test is not shared by the CQLR and CIL test. These two tests do not suffer the same power deficiencies as the CIL0 test. They behave as two-sided tests by construction, and have power close to the power upper bound.

We now move to the more complex case in which errors can be heteroskedastic, autocorrelated, and/or clustered (HAC). We replicate four designs: the near-singular (NS), a variation thereof (NS with perturbation), and growing alternative (GA) designs of Moreira and Ridder (2020), and the non-Kronecker (NK) design of Moreira and Moreira (2019). While these simulations are not exhaustive for all parameter combinations, none of these designs is chosen to favor the CIL test over the CLR test. The main goal of these designs is only to show that there exist invariant tests which depend on the statistic beyond and .

| (1,No) | (0,Yes) | (51,No) | (50, Yes) | |

|---|---|---|---|---|

| (1,No) | - | 64.7 | 86.7 | 87.7 |

| (0,Yes) | 26.0 | - | 47.1 | 47.2 |

| (51,No) | 0.1 | 3.5 | - | 4.2 |

| (50,Yes) | 0.1 | - | 0.4 | - |

To conserve space, we focus here only on simulations based on the NS design for . We set , with . For the variance matrix, we define to be the matrix with the anti-diagonal elements equal to one and the other components zero. We have . The submatrices of are

| (4.2) |

where , , and are tuning parameters. The values for the NS design are , , and . In this design, the power of both LM and CQLR tests is essentially equal to size. The full set of results for and for all four designs, as well as descriptions of the NS with perturbation, GA, and NK designs, are presented in the supplement.

| (1,No) | (0,Yes) | (51,No) | (50, Yes) | |

|---|---|---|---|---|

| (1,No) | - | 3,270.1 | 5,446.5 | 5,410.0 |

| (0,Yes) | 964.9 | - | 9,910.7 | 9,890.0 |

| (51,No) | 1,114.7 | 452.6 | - | 379.1 |

| (50,Yes) | 0.2 | - | 7.7 | - |

When the variance matrix has a Kronecker product form, the statistic has a closed-form solution, and the CLR test reduces to the CQLR test. This sidesteps the daunting task of numerically optimizing the likelihood. In the special case with homoskedastic errors, choosing only one initial point after compactifying the search set is enough for our purposes. Unfortunately, this conclusion is not valid for more complex variance matrices. Table 1 assesses improvements for the likelihood optimization under the null hypothesis. The values inside the parentheses indicate the number of random initial points for and whether is included or not, respectively. We compute the LR statistic over 1,000 simulations for each case. We then report the proportion of times in which one setup outperforms another setup (relative improvement by an error margin of at least 0.1%).

Each row in Table 1 corresponds to a choice of the number of starting values and whether is among the starting values, as specified in the row header. The entries in a row report the fraction of repetitions in which the initial values selection and the inclusion of , as specified in the column header, give a higher maximum likelihood value. For example, if we choose instead of only one random point as the initial value, we see improvements in the likelihood optimization 64.7% of the time. Conversely, the likelihood optimization performs better 26.0% of the time if we choose a random point instead of . For both of these scenarios, improvements are gained by adding about 50 random initial values. This can be seen in the upper-right block in Table 1, where the improvements range from 47.1% to 87.7%. On the other hand, the improvements are negligible from starting with 50 random points and as initial values –even when we include 51 other random points. What is perhaps interesting is the improvement of 3.5% from adding as an initial value in addition to the 50 random points. These two findings suggest that running optimization algorithms after including 50 random points and as initial values should suffice for our purposes. More worrisome, for smaller values of or other combinations of and the variance matrix, we may need to include even more initial points. This may happen, for example, if the likelihood can be flat for parts of the parameter space.

Table 2 presents the average percentage improvement (for the observations in which the error margin is at least 0.1%). Even when we include 51 random initial points, meaningful improvements can be gained by including the unknown parameter . These gains are on the order of 379.1% for 4.2% of the replications when we include another 50 random initial points and itself. On the other hand, when we include 51 other random initial points beyond and 50 points, the average improvement is on the order of 7.7% for only 0.4% of the repetitions.

All simulations are for the null hypothesis. For the alternative, it is natural to use 50 random points, the null , and the alternative as initial points. Of course, the parameter is unknown. However, we want to minimize the numerical issues associated with the CLR test, in case better optimization methods are found in the future. The table shows that the solution of using in addition to 50 random points works well to compute the LR statistic. A more complex problem happens when we find the approximation for the critical value function. Recall that this function is the conditional quantile under the null hypothesis. This quantile is found by generating from a standard multivariate normal distribution. That means the model is misspecified when is not generated under the null. One possibility is to use the pseudo-parameter which minimizes the Kullback-Leibler divergence criterion. This strategy follows from the fact that the maximum likelihood (ML) estimator converges to this pseudo-parameter under strong instruments. This route seems complicated and unnecessary for our purposes. Excluding this parameter, we get smaller values for the test statistic –not larger. Hence, the 95% quantile used for the critical value function tends to underestimate the true conditional quantile. The bottom line is that by including , the statistic is optimized properly while the conditional quantile can be smaller than it should be. This means that, if anything, we may be overestimating the power of the CLR test.

Finally, we evaluate improvements over other numbers of random initial points for . For example, unreported simulations show gains of about 5.3% obtained from adding 1 initial random point beyond 20 random initial points. The choice of 50 seems the most sensible, in terms of reliability and computational speed. Even then, the computation time for CLR is about 35 times slower than that of the CIL test, on average (with the range between 4 to 100 times slower). For the aforementioned reasons, we include and as initial points as well. At least for the designs considered here, unreported power comparisons for different choices of initial values indicate that including 50 random points, , and offers stable and reliable power curves. There is, of course, no guarantee that this searching scheme would be sufficient for other designs.

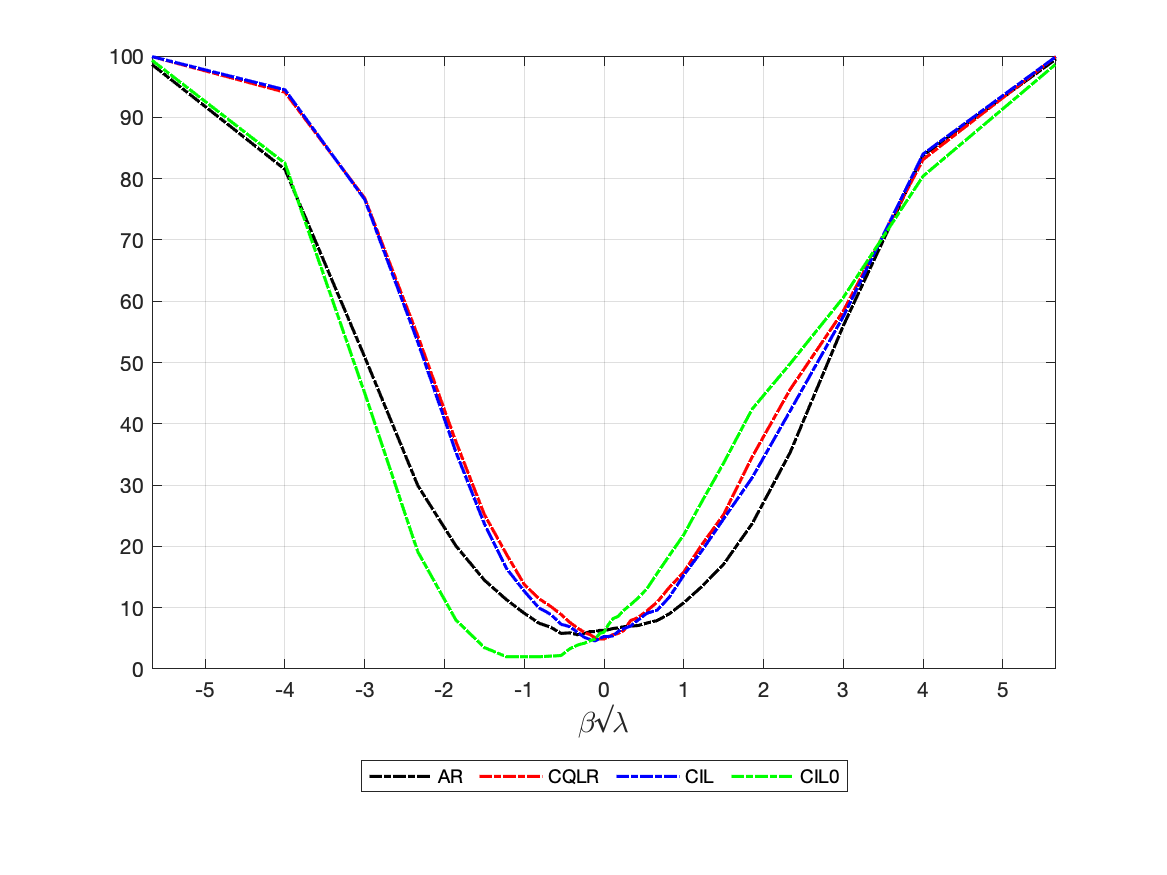

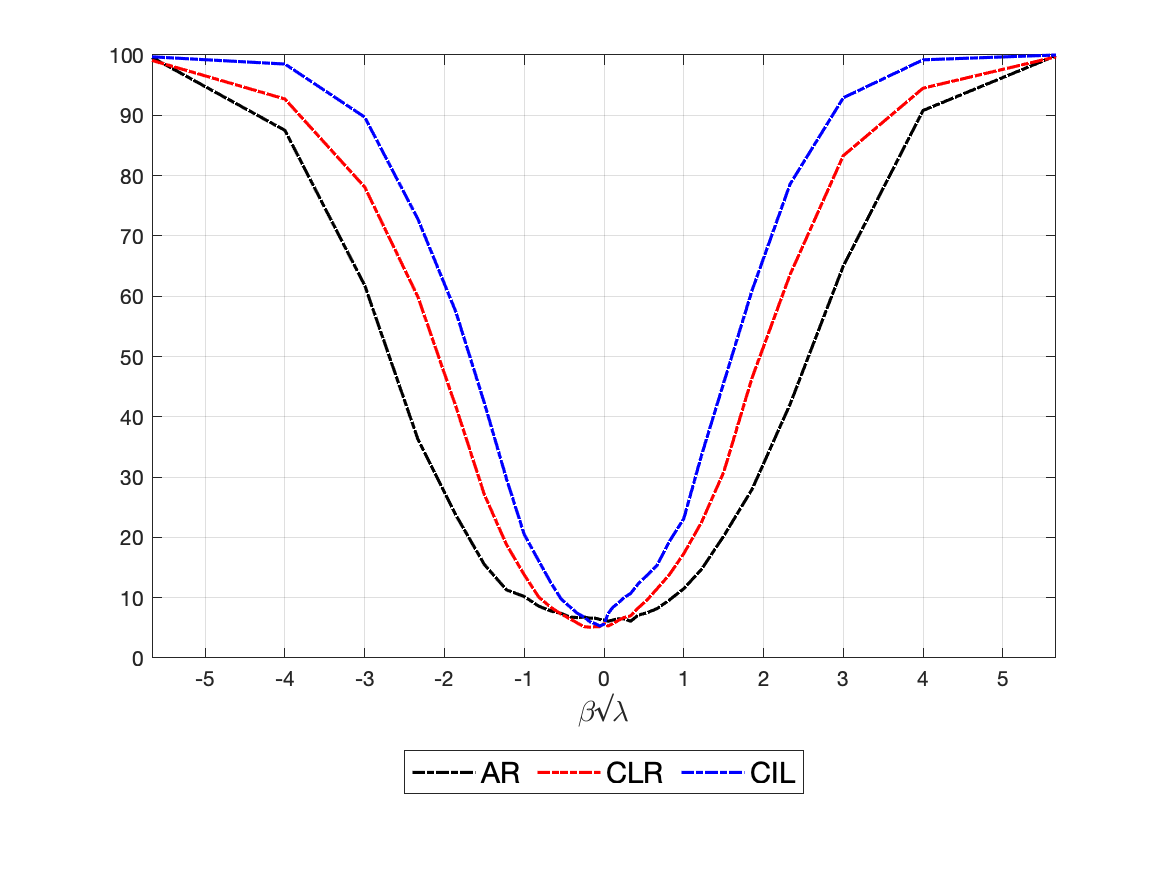

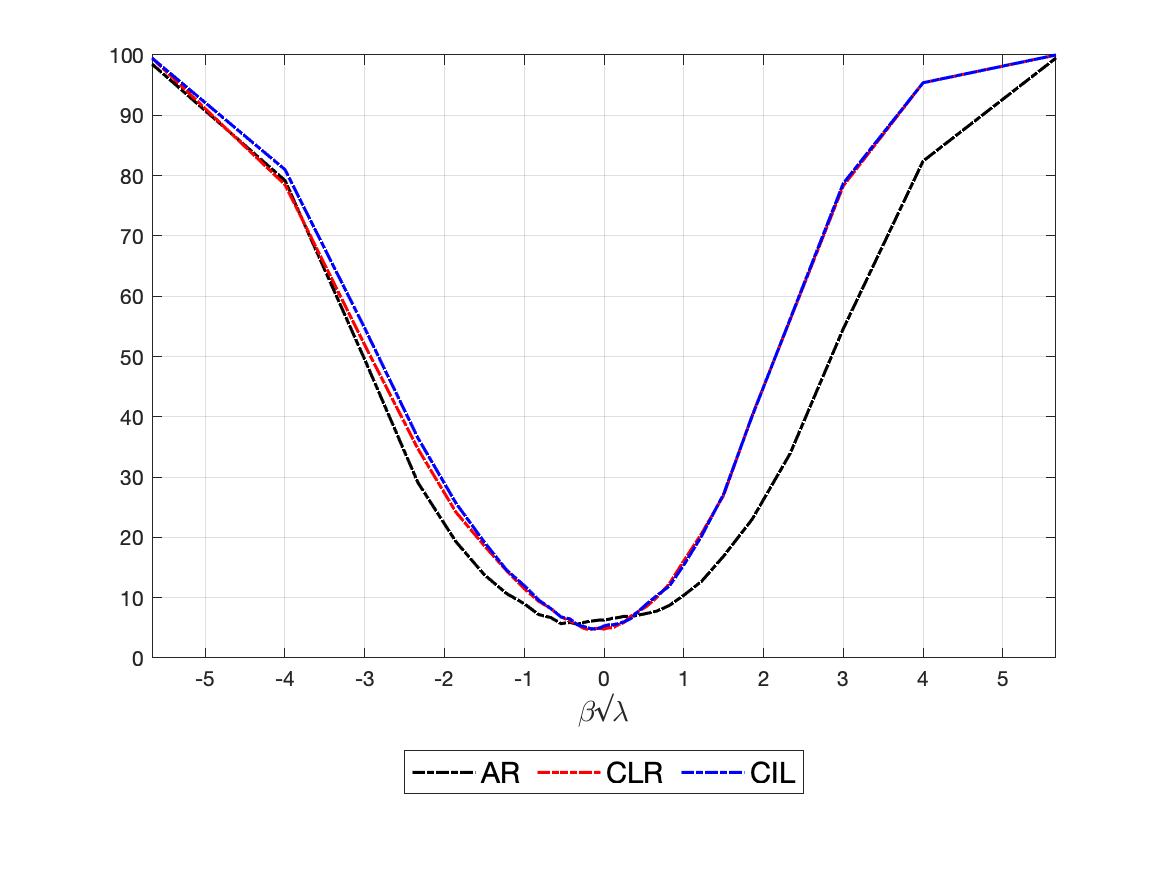

We now briefly discuss power. More extensive power comparisons are reported in the supplement (due to computational time for the CLR, these additional comparisons use only 200 Monte Carlo replications for power and 200 simulations for conditional quantiles). Figure 3 presents power for the AR, CLR, CIL, and CIL0 tests when and . We consider all four sets of simulations: NS design, NS design with a perturbation, GA design, and NK design. As before, the CIL0 test can be biased, while the CLR and CIL tests dominate the AR test. In general, the CIL test outperforms the CLR test. The power difference can be as large as 15% for these specific designs. For example, the CIL test can have power near 85% when the CLR test rejects the null about 70% of the time. This difference happens even when we implement the infeasible version of the CLR test which includes as one of the initial points.

5 Kronecker Variance Matrix

We first consider the special case where with a matrix and a matrix. The Kronecker product framework is particularly interesting for two reasons. First, we find the maximal invariant, taking into consideration a transformation of which is known but not fixed. This yields the same data reduction from and as that obtained by AMS06 under the assumption that is known and fixed. This result is striking as the AMS06 approach does not hold for general , but ours does. Second, AMS06 do not rule out the possibility that the test depends on beyond the statistics and , because AMS06 treat as being fixed. Our framework instead shows that invariant tests should not depend on at all.

The and statistics in (2.11) simplify to the original statistics of Moreira (2002, 2009) and AMS06 for the homoskedastic model. When , the statistics and become

| (5.1) | |||||

Their distribution is given by

| (5.2) |

with and . AMS06 develop the theory of invariant tests by treating as known and fixed. Even if is known, the parameter is unknown, because is unknown. Hence, AMS06’s invariance argument applies to the new parameter . Specifically, let , the group of orthogonal matrices with matrix multiplication as the group operator. The corresponding transformation in the sample space is

| (5.3) |

The associated transformation in the parameter space is

| (5.4) |

The transformation does not change , so our testing problem is preserved. As argued before, this means that the test statistic should be an invariant statistic (under the transformation ).

The maximal invariant statistic for the orthogonal transformation is

| (5.5) |

That is, any invariant test depends on the data only through . The density of at for the parameters and is given by

| (5.6) | |||

where , is the gamma function, denotes the modified Bessel function of the first kind, and

| (5.7) |

AMS06 further shows that another group, given by sign transformations, preserves against . Consider the group , which contains only two elements: . For , the data transformation is given by

| (5.8) |

(by the definition of a group, the parameter remains unaltered at ). This yields a transformation in the maximal invariant space for :

| (5.9) |

The maximal invariant for the joint transformation is the vector with components , , and . In principle, the tests can depend on with homoskedastic errors. As we will see in Theorem 2, we are able to eliminate the dependence on the variance as well, and show the triad , , and is the maximal invariant for in the case of known, but not fixed, variance.

5.1 Instrument Transformation

The orthogonal transformation argument of AMS06 is originally designed for homoskedastic errors. For the general Kronecker case, both and (which are equivalent to the original statistics of AMS06) have variance . Because their methodology assumes the variance to be fixed, their orthogonal transformation would not work, in general, because the variance would change. We could manually standardize their statistics by to obtain our statistics and , and apply the orthogonal group, as done earlier.444We could look instead at such that . This yields . This is the same as transforming the data to , applying the orthogonal transformations, and transforming the data back to . An alternative solution is to allow to be known, but for it to change as we transform the data. For example, take the special case in which is a diagonal matrix. If we were to permute the entries of and jointly, perhaps we should allow the permutation of the diagonal entries of as well. Formally, we will take the variance as part of both data and parameter spaces.

For the special case in which , the distribution of is given by

| (5.10) |

where , , and . The data are the realizations and the parameters are . The matrices are assumed to be known, but not fixed. Thus, are both parameters and part of the data, simultaneously.

We introduced the transformation in Section 3.1. Its action on the sample space is given by

| (5.11) |

We note that

| (5.12) |

so the corresponding action on the parameter space is

| (5.13) |

We now show that the matrix

| (5.14) |

together with itself, is the maximal invariant statistic. That is, any other invariant statistic can be written as a function of . The distribution of the maximal invariant depends only on the concentration parameter , the parameter of interest , and itself.

Theorem 1.

Comments: 1. The data is a one-to-one transformation from the primitive data . Hence, there is no loss of generality in using the pivotal statistic and the complete statistic instead of using (or ).

2. There is a one-to-one mapping between and . Hence, is a maximal invariant as well. We continue to use because it is useful to find a maximal invariant for the two-sided transformations to be considered next.

3. The statistic is the maximal invariant based on the compact orthogonal group on , which is a straightforward application of AMS06. We instead allow the much larger, noncompact group of nonsingular matrices with unitary determinant. The data also contain the variance components given by and . Because the group is not amenable, the Hunt-Stein theorem is not applicable, and we do not necessarily obtain a minimax result. This is in contrast to Chamberlain (2007), who builds on the fact that the orthogonal group is compact.

4. The component completely vanishes as the noncompact group acts transitively on . Hence, the matrix is not part of the maximal invariant.

5.2 Two-Sided Transformation

We now apply the transformation introduced in Section 3.1. The two-sided transformation in the Kronecker model is given by

| (5.15) |

where , the group of nonsingular lower triangular matrices. The transformation in the parameter space is

| (5.16) |

Theorem 2 finds the maximal invariant based on and .

Theorem 2.

For the data group actions defined in (5.11) and (5.15), and the parameter actions in (5.13) and (5.16), we find

(i) The induced group action of on the space is

(ii) The data maximal invariant to is

(iii) The induced group action by on the parameter functions is given by

(iv) The parameter maximal invariant to is

Comments: 1. The parameters and remain unchanged by the action (5.13). Because the parameters and depend only on and , they are preserved as well. The result now follows trivially because .

2. We note that may be different from zero. Hence, the group of transformations is larger than scale multiplication to each entry of the vector . A naive generalization for the sign group of transformations by AMS06 to our setup is a diagonal matrix . In the online appendix, we show that some invariant tests based on the associated maximal invariant can behave as one-sided tests. Hence, we illustrate the importance of finding the largest group of transformations before deriving invariant tests.

These actions are defined using the reduced-form matrix . For the homoskedastic model, we could analyze the transformations in the structural-form matrix

| (5.17) |

One may wonder if there are actually symmetries in the original model. This turns out to be true. In fact, the action in the structural-form variance matrix has a very simple structure.

Proposition 1.

The group action on the reduced-form matrix induces an action on the structural-form matrix :

Comment: Take . When and , we have . Therefore, and are preserved while changes sign. Since , the new value for the structural-form covariance scalar, , and the new value of the parameter, , comprise the only transformation that works for any value of .

6 Invariant Tests

We now use the group of transformations by to develop the CIL test. Recall that the data consist of and , where has a normal distribution and the distribution of is degenerate. So, the density of the data is the product of two parts. The first part is the normal distribution of , which is absolutely continuous with respect to the Lebesgue measure. The second part is the degenerate distribution of , which is absolutely continuous with respect to the counting measure. Understanding how the density changes with the data transformation is important for the development of the CIL test.

The density of evaluated at is given by

| (6.1) |

As in Theorem 2, we consider the groups of instrument transformations and two-sided transformations together, so that we have the joint transformation defined in Section 3.1, where and , and the associated transformation in the parameter space.

Basic algebraic manipulations show that

| (6.2) |

because

| (6.3) |

Therefore,

| (6.4) |

where for the sub-group multipliers and . Hence, the density of is relatively invariant with multiplier .

Of course, the action is not proper.555See Definition 5.1 of Eaton (1989) for a formal statement on a group acting properly on the sample space. In our case, it is trivial that the action by is not proper, since we can multiply and divide by the same constant. We can impose so that . In this case, , the group of invertible matrices with determinant equal to one. Alternatively, we can use another standardization such as . To develop the integrated likelihood invariant test, we use Haar measures to obtain invariant tests. It is harder to work with the Haar measure for than for ; see Dedić (1990). On the other hand, it is relatively simple to derive the Haar measure for lower triangular matrices with . For this reason, we prefer to impose a restriction on .

For the second part, the data have a distribution that assigns probability one to the value itself. Therefore, the density at some arbitrary matrix value is

The joint likelihood is then given by

| (6.7) |

so that

| (6.8) |

i.e. the likelihood is relatively invariant with multiplier . Because the Lebesgue measure is relatively left invariant for the group with multiplier , the (relative) invariance of the likelihood follows directly.

We use the invariance of the likelihood to propose a conditional weighted likelihood ratio test. We also show that the AR, LM, CQLR, and CLR tests are also invariant.

6.1 Optimal Tests

Our goal in this section is to find optimal tests. Specifically, a test is defined to be a measurable function that is bounded by and . For a given outcome, the test rejects the null with probability and accepts the null with probability , e.g., the Anderson-Rubin test is simply where is the indicator function. The test is said to be nonrandomized if takes only values and ; otherwise, it is called a randomized test. The rejection probability is given by

| (6.9) |

where is the counting measure. The rejection probability (6.9) simplifies to

| (6.10) | |||||

The rejection probability taken as a function of , , and gives the power curve for the test . In particular, gives the null rejection probability.

Let the parameter space for be denoted by , with -field the intersection of and sets in . Let be a measure on that -field. We average the power curve over the parameter space to obtain the weighted average power with weights that are given by the measure . By Tonelli’s theorem, the weighted average power is

| (6.11) |

If the weights are such that for ,

| (6.12) |

where and has unitary mass on , then

| (6.13) |

where is defined as

| (6.14) |

For a given weight , we seek optimal similar tests

| (6.15) |

The next proposition finds the WAP test.

Proposition 2.

The optimal test in (6.15) rejects the null when

| (6.16) |

where is the density of the statistic under the null.

Comment: Because is sufficient for under the null, we condition on . The dependence of the test statistic on is absorbed in the critical value of the test.

For arbitrary weights, the WAP similar test is not guaranteed to have overall good power in finite samples. In particular, the power can be near zero for parts of the parameter space (as happens with the CIL0 test for ). We circumvent this problem by carefully choosing weights so that the test given by (6.16) is invariant. The CIL test behaves as a two-sided test, and so, it does not suffer the criticism by Moreira and Moreira (2019).

6.2 Similar Invariant Tests

Invariance of conditional tests follows from the relative invariance of test statistics.

Definition 1.

A statistic is relatively (left) invariant to with multiplier if

for any .

Proposition 3 establishes the invariance of the conditional test if the test statistic is relatively invariant.

Proposition 3.

Suppose that is a continuous random variable under for every . Define to

be the quantile of the null distribution of . Then the following hold:

(i) The conditional test that

rejects the null when

is similar at level ;

(ii) If

is relatively invariant under with multiplier , then is itself relatively invariant with multiplier ; and

(iii) The conditional test is

invariant.

Comments: 1. Careful examination of the proof shows that invariance of the conditional quantile does not depend on the group transformation used. It is also applicable to other models as long as there is a sufficient statistic, e.g. here under the null, that is boundedly complete.

2. The comment above explains why the conditional quantile of the statistic depends only on in the homoskedastic case. The LR statistic does not depend on at all, and is the maximal invariant to orthogonal transformations . This is consistent with the results of Moreira (2003) and AMS06, but with no need to use pivotal statistics and independence.

Before showing that the CIL test is invariant and is the limit of conditional WAP tests, as given by (6.16), we establish that the , , , and statistics are invariant.

Proposition 4.

The , , , and statistics are invariant to .

Comment: Close inspection shows the proof of invariance of the statistic is very general. It works for any model in the presence of symmetries which preserve the testing problem.

6.3 An Invariant WAP Similar Test

The goal is to obtain a WAP invariant similar test in the over-identified model (). This entails finding weights so that the final test is relatively invariant.

Definition 2.

A measure is relatively (left) invariant with multiplier if

for any real-valued continuous function with bounded support.

We could apply this result for . However, the parameter is known, but changes according to the data transformation. Therefore, it is enough to allow to be the parameters only.

Lemma 1.

The product measure is relatively (left) invariant to with multiplier .

The next proposition shows that the conditional test is invariant and can be evaluated with a single (and not multiple) integral.

Theorem 3.

The conditional test based on the test statistic

is invariant and is the limit of a sequence of WAP tests defined in (6.16).

In separate work, we address admissibility of the CIL test. Showing admissibility based on invariant weights for non-amenable groups is done on a case-by-case basis. This issue is analogous to that encountered for the commonly-accepted and widely-used Hotelling statistic for testing means of different populations. Stein (1955) addresses the admissibility of the Hotelling statistic. This test relies on the same non-amenable group considered here for the HAC-IV model.

For the construction of the statistic, both priors for and are improper. In the spirit of Theorem 3, we need to consider sequences of weights for the alternative hypothesis instead. For the nuisance parameter , Moreira and Moreira (2019) and Andrews and Mikusheva (2020) allow an “identification” parameter go to infinity, so that the prior converges weakly to the Lebesgue measure. The completeness theorem shows that any admissible test is the limit of Bayes tests (sufficiency). However, is the limit of any sequence of Bayes tests admissible (necessity)? Farrell (1968a, b) considers a more concrete version of Stein’s proof of admissibility. For example, Moreira and Moreira (2013, 2019) rely on Farrell’s approach by using subsequence arguments for admissibility of WAP similar tests.

7 Conclusion and Extensions

This paper shows the importance of distinguishing between parameters being known or being fixed when showing the presence of symmetries in the HAC-IV model. However, this distinction is applicable to many other models. The existence of symmetries could be useful, as they could simplify inference (e.g., data reduction by invariance) or enable us to find better estimators and tests.

Econometricians are often interested in some parameters in the presence of others. It is well-understood that knowing the value of a nuisance parameter typically yields more efficient estimators and tests than estimating it. In some cases, however, knowing or estimating the nuisance parameter yields the same asymptotic efficiency. This feature can happen in parametric models in cross-section or time-series data, as well as in semi-parametric models, among others.

-

•

Consider a linear regression when the error variance is unknown (up to a parameter of fixed dimension). The generalized least-squares (GLS) estimator is the optimal linear unbiased estimator. It enjoys asymptotic efficiency among regular estimators. The feasible generalized least-squares (FGLS) estimator is asymptotically efficient when we consistently estimate the parametric error variance.

-

•

Take the predictive regression model where the explanatory variable can be nearly integrated of order one. The asymptotic behavior of several tests is the same whether the long-run variance matrix of the errors is known or consistently estimated.

-

•

In the GMM model, we can consistently estimate the optimal weighting matrix using a HAC estimator. Assuming the variance is known or estimated, the GMM estimators are asymptotically equivalent and efficient.

These examples illustrate the caveats of estimating or testing by assuming some parameters are known. This natural simplification ironically leads to complications when parameters are assumed to be fixed. In particular, it leads to the incorrect folk theorem that many models do not present natural symmetries. Once we distinguish between the assumptions of known versus fixed parameters, model symmetries can exist, contrary to popular belief. We hope this new methodology will lead to new inferential methods to apply to important econometric models.

References

- (1)

- Anderson and Rubin (1949) Anderson, T. W., and H. Rubin (1949): “Estimation of the Parameters of a Single Equation in a Complete System of Stochastic Equations,” Annals of Mathematical Statistics, 20, 46–63.

- Andrews (1991) Andrews, D. W. K. (1991): “Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimation,” Econometrica, 59, 817–858.

- Andrews, Moreira, and Stock (2004) Andrews, D. W. K., M. J. Moreira, and J. H. Stock (2004): “Optimal Invariant Similar Tests for Instrumental Variables Regression,” NBER Working Paper t0299.

- Andrews, Moreira, and Stock (2006) (2006): “Optimal Two-Sided Invariant Similar Tests for Instrumental Variables Regression,” Econometrica, 74, 715–752.

- Andrews (2016) Andrews, I. (2016): “Conditional Linear Combination Tests for Weakly Identified Models,” Econometrica, 84, 2155–2182.

- Andrews and Mikusheva (2016) Andrews, I., and A. Mikusheva (2016): “Conditional Inference with a Functional Nuisance Parameter,” Econometrica, 84, 1571–1612.

- Andrews and Mikusheva (2020) (2020): “Optimal Decision Rules for Weak GMM,” Unpublished manuscript, Harvard University.

- Chamberlain (2007) Chamberlain, G. (2007): “Decision Theory Applied to an Instrumental Variables Model,” Econometrica, 75, 609–652.

- Cruz and Moreira (2005) Cruz, L. M., and M. J. Moreira (2005): “On the Validity of Econometric Techniques with Weak Instruments: Inference on Returns to Education Using Compulsory School Attendance Laws,” Journal of Human Resources, 40, 393–410.

- Dedić (1990) Dedić, L. (1990): “On Haar Measure on SL(N,R),” Publications de L’Institut Mathématique, 47, 56–60.

- Dufour (1997) Dufour, J.-M. (1997): “Some Impossibility Theorems in Econometrics with Applications to Structural and Dynamic Models,” Econometrica, 65, 1365–1388.

- Eaton (1989) Eaton, M. L. (1989): Group Invariance Applications in Statistics. Regional Conference Series in Probability and Statistics, Volume 1. Hayward, CA: Institute of Mathematical Statistics.

- Farrell (1968a) Farrell, R. H. (1968a): “On Necessary and Sufficient Condition for Admissibility,” The Annals of Mathematical Statistics, 38, 23–28.

- Farrell (1968b) (1968b): “Towards a Theory of Generalized Bayes Tests,” The Annals of Mathematical Statistics, 38, 1–22.

- Kleibergen (2005) Kleibergen, F. (2005): “Testing Parameters in GMM without Assuming that they are Identified,” Econometrica, 73, 1103–1123.

- Lee, McCrary, Moreira, and Porter (2020) Lee, D. S., J. McCrary, M. J. Moreira, and J. Porter (2020): “Valid t-ratio Inference for IV,” arXiv:2010.05058v1.

- Lehmann and Romano (2005) Lehmann, E. L., and J. P. Romano (2005): Testing Statistical Hypotheses. Third edn., New York: Springer Series in Statistics.

- Mills, Moreira, and Vilela (2014) Mills, B., M. J. Moreira, and L. P. Vilela (2014): “Tests Based on t-Statistics for IV Regression with Weak Instruments,” Journal of Econometrics, 182, 351–363.

- Moreira and Moreira (2013) Moreira, H., and M. J. Moreira (2013): “Contributions to the Theory of Optimal Tests,” Ensaios Economicos, 747, FGV/EPGE.

- Moreira and Moreira (2019) (2019): “Optimal Two-Sided Tests for Instrumental Variables Regression with Heteroskedastic and Autocorrelated Errors,” Journal of Econometrics, 213, 398–433.

- Moreira (2002) Moreira, M. J. (2002): “Tests with Correct Size in the Simultaneous Equations Model,” Ph.D. thesis, UC Berkeley.

- Moreira (2003) (2003): “A Conditional Likelihood Ratio Test for Structural Models,” Econometrica, 71, 1027–1048.

- Moreira (2009) (2009): “Tests with Correct Size when Instruments Can Be Arbitrarily Weak,” Journal of Econometrics, 152, 131–140.

- Moreira and Ridder (2017) Moreira, M. J., and G. Ridder (2017): “Optimal Invariant Tests in an Instrumental Variables Regression with Heteroskedastic and Autocorrelated Errors,” arXiv:1705.00231.

- Moreira and Ridder (2020) (2020): “Efficiency Loss of Asymptotically Efficient Tests in an Instrumental Variables Regression,” arXiv:2008.13042v1.

- Nelson and Startz (1990) Nelson, C. R., and R. Startz (1990): “The Distribution of the Instrumental Variables Estimator and its t-Ratio when the Instrument is a Poor One,” Journal of Business, 63, 5125–5140.

- Newey and West (1987) Newey, W. K., and K. D. West (1987): “A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix,” Econometrica, 55, 703–708.

- Staiger and Stock (1997) Staiger, D., and J. H. Stock (1997): “Instrumental Variables Regression with Weak Instruments,” Econometrica, 65, 557–586.

- Stein (1955) Stein, C. (1955): “A Necessary and Sufficient Condition for Admissibility,” The Annals of Mathematical Statistics, 26, 518–522.