Dynamical Analysis of Stock Market Instability by Cross-correlation Matrix

Abstract

We study stock market instability by using cross-correlations constructed from the return time series of 366 stocks traded on the Tokyo Stock Exchange from January 5, 1998 to December 30, 2013. To investigate the dynamical evolution of the cross-correlations, cross-correlation matrices are calculated with a rolling window of 400 days. To quantify the volatile market stages where the potential risk is high, we apply the principal components analysis and measure the cumulative risk fraction (CRF), which is the system variance associated with the first few principal components. From the CRF, we detected three volatile market stages corresponding to the bankruptcy of Lehman Brothers, the 2011 Tohoku Region Pacific Coast Earthquake, and the FRB QE3 reduction observation in the study period. We further apply the random matrix theory for the risk analysis and find that the first eigenvector is more equally de-localized when the market is volatile.

1 Introduction

The stock market is a complex system that undergoes unstable periods that result in financial crises in some cases. Measuring systemic risk is an important task to monitor current market status and possibly to avoid a future financial crisis. In financial crises, many stocks are interconnected and move collectively. The level of interconnectedness can be measured by cross-correlations between stocks, and there are a variety of works on cross-correlations that include the random matrix theory (RMT)[1, 2, 3, 4, 5] and the principal component analysis (PCA)[6, 7, 8, 9]. In this study, we calculate cross-correlations between stocks traded on the Tokyo Stock Exchange from January 5, 1998 to December 30, 2013 and apply the PCA and the RMT to analyze the dynamical properties of cross-correlations. In particular, we focus on the market instability and investigate when the market was volatile during the study period.

2 Cross-correlation matrix

We analyze the daily closing price data of stocks traded on the Tokyo Stock Exchange from January 5, 1998 to December 30, 2013, which corresponds to 3932 working days. We choose 366 stocks listed on the Topix 500 index.

Let be a return for stock at time defined by the log-price difference as

| (1) |

where is the price for stock on day . We also define the normalized return as

| (2) |

where indicates the time series average and is the standard deviation of .

Using the normalized return , an equal-time cross-correlation matrix is calculated as , where an average, i.e. , is taken over a period of the rolling window. In this study, we consider a rolling window of 400 working days, which roughly corresponds to two years. By definition, the elements of the cross-correlation matrix are restricted to .

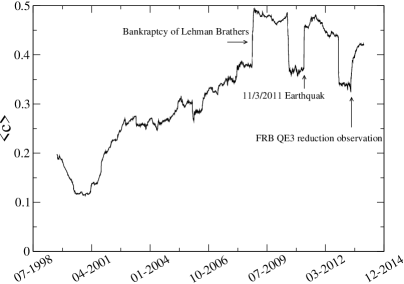

Fig.1(Left) shows the dynamical evolution of the average off-diagonal matrix element given by

| (3) |

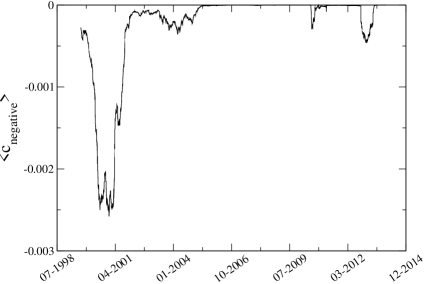

where . From the figure, we recognize that there exist three points where increases abruptly. According to the historically observed events, these points correspond to the bankruptcy of Lehman Brothers, the Tohoku region pacific coast earthquake on 11/3/2011, and the FRB QE3 reduction observation as indicated in the figure. In Fig.1(Right), we also show the average of negative off-diagonal elements,

| (4) |

Notably, in the recent years, the contribution of negative off-diagonal elements to the cross-correlation matrix becomes less than that around 2000. In particular, at volatile stages, negative off-diagonal components disappear and most stocks are positively correlated.

3 Dynamical behavior of Cumulative Risk Fraction

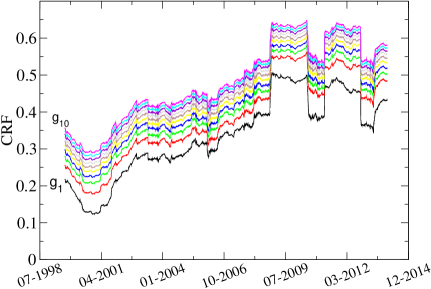

In order to further investigate the dynamical properties of cross-correlation matrices, we apply the principal component analysis (PCA). Billio et al.[6] suggested to use the PCA to quantify the systemic risk and introduced the cumulative risk fraction (CRF) as a risk measure. The PCA has also been used to measure the systemic risk[7, 8, 9]. To construct the CRF, we first compute the eigenvalues of cross-correlation matrices, denoted as , where all eigenvalues are sorted as . Then, we calculate the CRF defined by[6]:

| (5) |

where is the total variance of the system given by and is the risk associated with the first principal components given by . The CRF quantifies the portion of the total variance explained by the first principal components over the total variance[7]. Usually, the first few principal components explain most of the system variance. In the periods of financial crisis, many stocks are highly interconnected and their prices easily move together. In such periods, the CRF is expected to increase considerably because the system variance also increases.

Fig.2(Left) shows the time evolution of the CRF for . We find that the structures of time evolution of for are very similar. This indicates that the first eigenvalue dominates in the CRF. We also find that the structure of the CRF resembles that of average off-diagonal elements of the cross-correlation matrix, and the CRF increases abruptly at the same points as observed in the CRF, that is, Fig.1(Left).

4 Changes of the Cumulative Risk Fraction

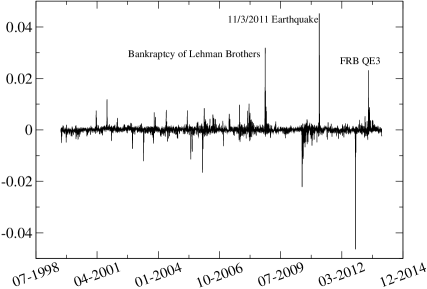

Zheng et al.[8] introduced the changes of the CRF to effectively quantify the points where the potential risk is high. The changes of the CRF is defined by

| (6) |

The time evolution of is presented in Fig.2(Right). We find that the change of the CRF shows pronounced positive spikes at the same three points where we observed the three abrupt increases in the CRF. Note that large negative spikes are artificially caused by the period of the rolling window.

5 Random Matrix Theory

Let be an independent, identically distributed random variable with at time . Then, we define the normalized variable:

| (7) |

where is the standard deviation of . The equal time cross-correlation between variables is given by . The matrix is called Wishart matrix. For and with , an eigenvalue distribution of the matrix is theoretically given by[10, 11]:

| (8) |

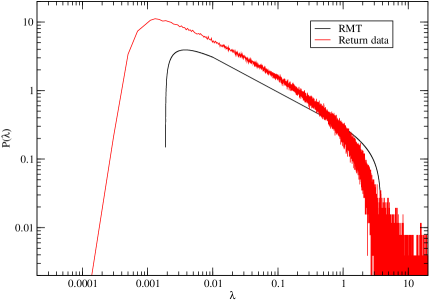

Fig.3(Left) compares an eigenvalue distribution of the matrix with that of the empirical cross-correlation matrix , where . The eigenvalue distribution of the empirical cross-correlation matrix differs considerably from the result from the RMT expectation. In particular, we find that for the empirical cross-correlation matrix, there exist many eigenvalues less than and larger than .

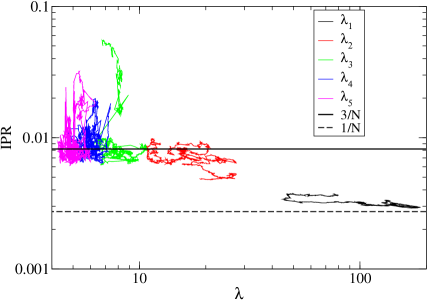

Another interesting entity, the inverse partition ratio that characterizes the eigenvectors, is defined by

| (9) |

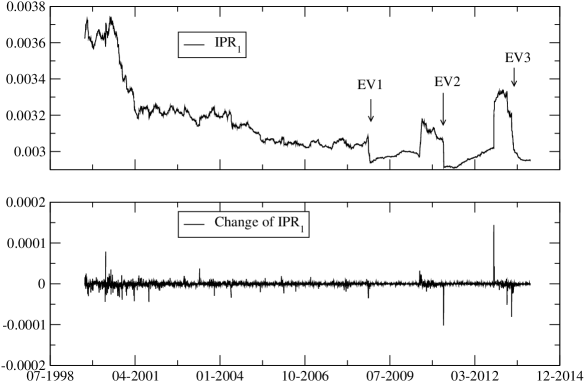

where is the j-th component of the eigenvector for the k-th eigenvalue. In the RMT, the eigenvector components are de-localized and distributed as a Gaussian distribution. In such a case, the expectation of the IPR is . On the other hand, when the eigenvector components are localized, for example, only one component has a non-zero value, the expectation of the IPR would be 1. There also exists another de-localized case in which all eigenvector components are equally de-localized, and in this case, the expectation of the IPR is . Fig.3(Right) shows the IPR versus the eigenvalue . The IPRs for approach , which is the RMT expectation. On the other hand, the IPR for , the largest eigenvalue, is near , which means that the eigenvector components are equally de-localized. Fig.4 shows the time evolution of and the change of , where the definition of the change of is the same as eq.(6). The seems to decrease and approach at the three points found in the cross-correlation and the CRF, although their signals are not very clear. This observation on the indicates that when the market is volatile, the largest eigenvalue components are more equally de-localized, which is different from the RMT expectation, and in such a case, the IPR approaches .

6 Conclusions

We have analyzed the cross-correlation matrices between 366 stocks traded on the Tokyo Stock Exchange from January 5, 1998 to December 30, 2013. We find that both the average off-diagonal elements of cross-correlation matrices and the cumulative risk fraction show abrupt increases at three points that correspond to three volatile stages of the Japanese stock market: the bankruptcy of Lehman Brothers, the Tohoku Region Pacific Coast Earthquake, and the FRB QE3 reduction observation. The change of the CRF also identifies these three points. From comparison with the random matrix theory, we find that the empirical cross-correlation matrix differs from the random matrix and, especially, the first eigenvector is more equally de-localized when the market is volatile. The cross-correlation matrices contain relevant information on the financial market status. By carefully analyzing the dynamical properties of the cross-correlations, we could monitor the risk that the financial markets confront.

Acknowledgement

Numerical calculations in this work were carried out at the Yukawa Institute Computer Facility and the facilities of the Institute of Statistical Mathematics. This work was supported by JSPS KAKENHI Grant Number 25330047.

References

References

- [1] Plerou V, Gopikrishnan P, Rosenow B, Amaral L A N and Stanley H E 1999 Phys. Rev. Lett. 83 1471-1474

- [2] Laurent Laloux L, Cizeau P, Bouchaud J-P and Potters M 1999 Phys. Rev. Lett. 83 1467

- [3] Plerou V, Gopikrishnan P, Rosenow B, Amaral L A N and Stanley H E 2000 Physica. A. 287 374-382

- [4] Plerou V, Gopikrishnan P, Rosenow B, Amaral L A N, Guhr T and Stanley H E 2002 Phys. Rev. E 65 066126

- [5] Utsugi A, Ino K and Oshikawa M 2004 Phys. Rev. E 70 026110

- [6] Billio M, Getmansky M, Lo A W and Pelizzon L 2012 J. Financ Econ. 104 535

- [7] Kritzman M, Li Y Z, Page S and Rigobon R 2011 J. Portf. Manag. 37 112

- [8] Zheng Z, Podobnik B, Feng L and Li B 2012 Sci. Rep. 2 888

- [9] Ren F and Zhou W Z 2014 PLoS ONE 9(5) e97711

- [10] Edelman A 1998 SIAMJ. Matrix Anal. Appl. 9 543

- [11] Sengupta A M and Mitra P P 1999 Phys. Rev. E 60 3389