Regular Decomposition: an information and graph theoretic approach to stochastic block models

Abstract

A method, regular decomposition (RD), for compression of large graphs and matrices to a block structure is proposed. Szemerédi’s regularity lemma is used as a generic motivation of the significance of the corresponding stochastic block models (SBMs). Another ingredient of the method is Rissanen’s minimum description length principle (MDL). We analyze consistency of RD in detecting a block structure in a large and dense graph generated from a SBM with fixed number of blocks. We show that the coding length of the graph, used as a cost function in MDL, decreases until the right number of blocks is reached, then the coding length reaches a plateau with very slow or no reduction in value. This enables a practical algorithm for finding such block structures. Simulations are used to illustrate that this scenario is visible already in modest sizes of the graph.

Keywords: Szemerédi’s Regularity Lemma, Minimum Description Length Principle, stochastic block model, big data

1 Introduction

In recent years, the analysis of large graphs, matrices and hypergraphs has become more contemporary. One reason for this is the elicitation of big data and its accumulation at an accelerating pace.

Usually, the complete information of these objects (large graphs, matrices and hypergraphs) is not available or/and it’s just too large to be practically applied. In this situation, the methods that can acquire a low-dimensional approximation of the underlying graphs are of a paramount interest. Such approximations can be seen as a compressed representation of the large-scale structure. This makes information theory a natural choice for the analysis which was pointed out by Rosvall and Bergstrom [27]. Roughly speaking, this means grouping redundant elements into a few communities. In case of graphs, examples are well-known division of nodes into communities or modules. Information theory will aid in choosing the optimal structures, in particular, the number of communities or modules.

Our aim is to develop a corresponding rigorous methodology and proofs of correctness in the limit of large structures. We also introduce concrete algorithms and numerical examples that clarify how to use our method in practice. This work completes and partly summarizes our previous work on this subject [13, 16, 21, 23, 24, 11, 22].

Another source of ideas is the fundamental mathematics of large structures which indicates the directions from which some exact results can be expected. A fundamental result in graph theory that is highly typical for problems of big data and related graphs is Szemerédi’s Regularity Lemma (SRL) [31]. SRL is a fundamental result in graph theory. Roughly speaking, SRL states that any large enough graph can be approximated arbitrarily well by nearly regular, pseudo-random bipartite graphs, induced by a partition of the node set into a bounded number of equal-sized sets. For many graph problems, it suffices to study the problem on a corresponding random structure, resulting in a much easier problem (see, e.g., [10]). SRL is fundamental also in theoretical computer science, say, in showing the existence of polynomial-time approximations for solving dense graph problems, and in characterizing the class of so-called testable graph properties [2].

Despite the impressive theoretical applications of SRL, it has had only few applications to ’real-life’ problems. The main reason might be that SRL has extremely bad worst-case scenarios in the sense that the lower bound of graph sizes, for which the partition claim holds with reasonable accuracy and without a single exception, is enormous. Thus, a real-world application of SRL in the literal sense is impossible. However, this drawback does not mean that regular partitions could not appear in much smaller scales which are relevant to applications. On the contrary, one could conjecture that regular partitions or structures be commonplace and worth revealing.

The goal of our work is on realistic, yet preferably large networks that appear in almost all imaginable application areas. The regular structure granted by SRL is then replaced by a probabilistic model, substituting the regular bipartite components with truly random bipartite graphs. This model class is well known as stochastic block models [9] (SBM), and it has recently gained much attention in research and popularity in practical applications like community detection [17, 7, 12]. However, the fundamental nature of SRL suggests the (heuristic) conjecture that stochastic block models present a very generic form of the separation of structure and randomness in large real-world systems. That is why we think that SRL and related results should be kept in mind in practical applications as a rich source of abstractions that can lead to new applications.

SBM structuring of data has good practical properties. Methods, such as maximum likelihood fitting, expectation maximization, simulated annealing and Monte Carlo Markov Chain algorithms, can be used.

There are also some examples of graph decomposition applications that have been explicitly inspired by SRL. The practical contexts are varied: brain cortex analysis [13], image processing [30], peer-to-peer network[16], analyzing the functional magnetic resonance (fMRI) data to depict functional connectivity of the brain [15] and a matrix of multiple time series [21]. In the last mentioned work, the method was generalized from graphs to arbitrary positive matrices using a Poissonian construction as an intermediary step.

Interestingly, the authors of the recent work [28] define a ’practical’ variant of SRL by relaxing algorithmic SRL in a certain way to make it more usable in machine-learning tasks, see also [19]. Bolla [3] has developed a spectral approach for finding regular structures of graphs and matrices. Our emphasis is more information theoretical by nature and continues the works of [13, 16, 21, 23, 24]. It would be very interesting to compare the methods of [28, 3] and those of this paper in depth.

The third main ingredient in this paper is Rissanen’s Minimum Description Length (MDL) principle (see [6]), according to which the quality of a model should be measured by the length of the bit string that it yields for the unique encoding of the data. In our case, the data has the form of a graph or matrix, and we present the stochastic block models as a modeling space in the sense of the MDL theory. Within this modeling space, the model corresponding to minimum code length encoding presents the optimal regular decomposition (partition) of the data. Therefore we call this Szemerédi-motivated and technically MDL-based approach Regular Decomposition.

By information theory, the optimal coding reveals as much redundancy in the data as is possible from within the given modeling framework. The regular structure has a high degree of redundancy: a regular pair is an almost structureless subgraph in which almost all the nodes have similar and uniform connectivity patterns. By definition, the MDL principle should be able to discover regular structures. Note that this principle presents a case of ’Occam’s Razor’, a general rule of reasoning that has proved fruitful in all areas of science.

In non-hierarchic clustering tasks, it has been a major challenge to select the ’right’ size of a partition (). Intuitively, the optimal choice of will strike a balance between the simplest partition of the data using a single cluster and the maximal partition assigning each data point to its own cluster, and selecting something in between. A popular device has been the Akaike information criterion (AIC), which was applied also in [13]. The AIC simply adds the ’number of model parameters’ to the maximal log-likelihood and chooses the model that minimizes the sum. Our MDL-based approach solves the corresponding model selection task in a better founded way (see also [18]).

The contributions of this paper are the following: (i) the linkage of SRL, stochastic block models and the MDL principle, (ii) the unified handling of graphs and matrices, (iii) the effective practical algorithms for revealing regular structures in data, and (iv) Theorem 4.1 that characterizes how accurately the MDL principle identifies a stochastic block model.

The paper is structured as follows: Section 2 presents the definitions of the main notions: SRL, stochastic block models and MDL. The last topic is expanded in Section 3. Section 4 presents our main technical results, in particular the algorithms and Theorem 4.1. The proof of Theorem 4.1 is given in Section 5. It is structured into several propositions and makes strong use of information-theoretic tools presented in Appendix A.

1.1 Related work

Let us enlist contributions that are most relevant to core results of our work.

Peixoto suggests to use MDL in the SBM context in [18] which continues earlier work by Rosvall and Bergstrom [27] where this idea was first suggested. It has interesting estimates which indicate that there is an upper limit of the number of communities that can be detected, as a function of number of nodes . However, Peixoto does not consider the exact detection of communities with a bounded number of communities, that is the focus of the current work. Peixoto has also made several implementations of corresponding algorithms and made them available [18].

Wang and Bickel [33] used information theory for likelihood-based model selection for the SBM. Their conclusions are similar to ours. In addition they show validity of results also in a sparse case when the average degree grows in polylog (polynomial in , is number of nodes) rate and in the case of degree-corrected block models. They use asymptotic distributions instead of the exact ones that we use. The algorithmic part also deviates from ours. They end up in a likelihood-based criterion, Bayesian information criterion (BIC), that is asymptotically consistent. Along with a term that corresponds to log likelihood there is a term proportional to with some tuning coefficient that has to be defined separately in every concrete case. In so defined BIC has a minimum at the right value of the . Instead of such a term we prefer to use MDL model complexity that is not case sensitive.

2 Basics and definitions

2.1 Szemerédi’s Regularity Lemma

Consider simple graphs , where is the set of nodes (vertices) and is the set of links (edges). The link density of a non-empty node set is defined as

and denotes the cardinality of a set. Similarly, the link density between two disjoint non-empty node sets is defined as

Definition 2.1.

Let . A pair of disjoint sets of is called -regular, if for every and , such that and we have

A partition of into sets, where all except have equal cardinalities, is called -regular, iff all except at most pairs are -regular and .

Theorem 2.1.

(Szemerédi’s Regularity Lemma, [31]) For every and for any positive integer , there are positive integers and , such that for any graph with there is an -regular partition of into classes with .

Roughly, SRL states that nodes of any large enough graph can be partitioned into a bounded number () of equal-sized sets and into one small set in such a way that links between most pairs of sets look like those in a random bipartite graphs, whose link probability equals the link density between the pair.

The claim of SRL is significant for sufficiently dense graphs, i.e., when the link density is higher than .The result can be modified to sparse graphs by multiplying at the right-hand side of the regularity definition by the link density of the entire graph [29].

It is remarkable that the regularity claim holds for all graphs starting from a lower bound for size that depends only on . However, it is also well-known that this dependence on is of extremely bad kind: the known lower bound for the graph size is extremely large, like a tower of powers of 2:

where the height of the tower is bounded above by . Such a number is too big to be considered in any applications. Thus, all real-world networks fall into a ’grey area’ with respect to SRL.

As we stated in the Introduction, there has been attempts to use algorithmic versions of SRL (ASRL), introduced by Alon et al, [1], also in practical applications. The large numbers like the upper bound of is problematic. Although ASRL has time complexity that is only polynomial , corresponding to the time for multiplying two binary matrices, it requires this enormous size () of graph to be able to find a regular partition.

A considerable improvement was found in the recent work [5], where the execution time is only linear in the graph size using a randomized algorithm. From a practical point of view, this algorithm works in a more realistic fashion than the original ASRL: for any graph, it either finds an -regular partition or concludes that such a partition does not exists. Another randomized algorithm with the same feature was suggested by Tao [32].

In principle, such algorithms could possibly be applicable for real-world graphs, although some prohibitively big upper-bounds of the constants of the algorithm are a problem that needs a solution. That is why, we conclude that our approach is also needed.

2.2 Stochastic block models

The notion of an -regular partition is purely combinatorial. The stochastic model closest to this notion is the following.

Definition 2.2.

Let be a finite set and a partition of . A stochastic block model is a random graph with the following structure:

-

•

There is a symmetric matrix of real numbers satisfying the irreducibility condition that no two rows are equal, i.e.,

(2.1) -

•

For every pair of distinct nodes of such that , , let be a Bernoulli random variable with parameter , assuming that all ’s are independent. The edges of are

Note that the case of the trivial partition yields the classical random graph with edge probability .

A graph sequence presenting copies of the same stochastic block model in different sizes can, for definiteness, be constructed as follows.

Construction 2.3.

Let be positive, distinct real numbers such that . Divide the interval into segments

and denote . For , let the vertices of be

For each , let be the partition of into the blocks

For small , we may obtain several empty copies of the empty set numbered as blocks. However, from some on, all blocks are non-empty and is a genuine partition of . We can then generate stochastic block models based on according to Definition 2.2.

Remark 2.4.

A slightly different kind of stochastic block model can be defined by drawing first the sizes of blocks as independent Poisson random variables and proceeding then with the matrix as before. The additional level of randomness, regarding the block sizes, is however of no interest in the present paper.

Next, we define the notion of a Poissonian block model in complete analogy with Definition 2.2. (This allows almost one-to-one transfer of the proofs in Section 5 to the Poissonian case.)

Definition 2.5.

Let be a finite set of vertices, , and let be a partition of . The symmetric Poissonian block model is a symmetric random matrix with the following structure:

-

•

There is a symmetric matrix of non-negative real numbers satisfying the irreducibility condition that no two rows are equal, i.e.,

(2.2) -

•

For every unordered pair of distinct nodes of such that , , let be a Poisson random variable with parameter , assuming that all ’s are independent. The matrix elements of are for , and for the diagonal elements.

Thanks to the independence assumption, the sums are Poisson distributed for any .

Remark 2.6.

The rest of the technical contents of this paper focus on the simple binary and Poissonian models of Definitions 2.2 and 2.5. However, the following extensions are straightforward:

-

•

bipartite graphs: this is just a subset of simple graphs;

-

•

matrices with independent Poissonian elements: a matrix can be seen as consisting of edge weights of a bipartite graph, where the parts are the index sets of the rows and columns of the matrix, respectively;

-

•

directed graphs: a directed graph can be presented as a bipartite graph consisting of two parts of equal size, presenting the input and output ports of each node.

3 MDL approach to stochastic block models

In this Section we describe some basic definitions and notations for applying standard MDL modeling approach to graphs and matrices.

3.1 The Minimum Description Length (MDL) principle

The Minimum Description Length (MDL) Principle was introduced by Jorma Rissanen, inspired by Kolmogorov’s complexity theory, and an extensive presentation can be found in Grünwald’s monography [6], see also [26]. The basic idea is the following: a set of data is optimally explained by a model , when the combined unique encoding of the (i) model and (ii) the data as interpreted in this model is as concise as possible. By encoding we mean here a mapping that specifies an object uniquely.

The principle is best illustrated by our actual case, simple graphs. A graph with can always be encoded as a binary string of length , where each binary variable corresponds to a node pair and a value 1 (resp. 0) indicates an edge (resp. absense of an edge). Thus, the MDL of is always at most . However, may have a structure whose disclosure would allow a much shorter description. Our heuristic postulate is that in the case of graphs and similar objects a good a priori class of models should be inferred from SRL, which points to stochastic block models.

Definition 3.1.

Denote by the set of irreducible stochastic block models with

-

•

,

-

•

, and, denoting ,

-

•

for ,

The condition in the last bullet entails that each modeling space is finite.

Remark 3.2.

Without the irreducibility condition (2.1), there would not be a bijection between stochastic block models and their parameterizations.

The models in are parameterized by . A good model for a graph is the one that gives maximal probability for and is called the maximum likelihood model. We denote the parameter of this model

| (3.1) |

where denotes the probability that the probabilistic model specified by produces .

One part of likelihood optimization is trivial: when a partition is selected for a given graph , the optimal link probabilities are the empirical link densities:

| (3.2) |

Thus, the nontrivial part is to find the optimal partition for the given graph. This is the focus of the next sections.

3.2 Two-part MDL for simple graphs

Let us denote the set of all simple graphs with nodes as

A prefix (binary) coding of a finite set is an injective mapping

| (3.3) |

such that no code is a prefix of another code. Recall the following proposition from information theory (see, e.g., [4]):

Theorem 3.1.

(Kraft’s Inequality) For an -element alphabet there exists a binary prefix coding scheme with code lengths iff the code lengths satisfy: .

An important application of Theorem 3.1 is the following: if letters are drawn from an alphabet with probabilities , then there exists a prefix coding with code lengths , and such a coding scheme is optimal in the sense that it minimizes the expected code length (in this section, the logarithms are in base 2). In particular, any probability distribution on the graph space indicates that there exists a prefix coding that assigns codes to elements of with lengths equal to .

The code length is the number of binary digits in the code of the corresponding graph. In case of a large set , most such codes are long and as a result the ceiling function can be omitted, a case we assume in sequel. A good model results in good compression, meaning that a graph can be described by much less bits than there are elements in the adjacency matrix. An incompressible case corresponds to the uniform distribution on and results in code length , equivalent to writing down all elements of the adjacency matrix.

For every graph from and model we can associate an encoding with code length distribution . However, this is not all, since in order to be able to decode we must know what particular probabilistic model is used. This means that also must be prefix encoded, with some code-length . We end up with the following description length:

| (3.4) |

Eq. (3.4) presents the so-called two-part MDL, [6]. In an asymptotic regime with , we get an analytic expression of the refined MDL. A simple way of estimating is just to map injectively every model in to an integer and then encode integers with as an upper bound of the code-length. Here

| (3.5) |

gives, as shown by Rissanen, the shortest length prefix coding for integers (see [6, 25]). The size of the graph must also be encoded with bits (it is assumed that there is a way of defining an upper bound of the models with given ). In this point, it is necessary to assume that the modeling space is finite. This results in

Proposition 3.3.

For any graph , there exists a prefix coding with code-length

where is the Stirling number of the second kind.

Proof.

The expression in (3.4) corresponds to a concatenation of two binary codes. The -part is the length of a code for describing the parameters of the model (in the case of a non-unique maximum, we take, say, the one with smallest number in the enumeration of all such models). The corresponding code is called the parametric code. The parametric code uniquely encodes the model. To create such an encoding, we just enumerate all possible models, given in Definition 3.1, and use the integer to fix the model. The length of a prefix code corresponding to an integer is the -function computed for that integer, and we add 1 to handle the ceiling function.

To obtain an upper bound for the parametric code length , we find an upper bound for the number of models in the modeling space. The number of models is upper-bounded by the product of two integers. The first is the number of partitions of an -element set into non-empty sets (blocks), which equals , and the second bounds the number of different link density configurations per partition. We can view the blocks of a partition as the nodes of a ‘reduced multi-graph’ (in a multi-graph, there can be several links between a node pair, as well as self-loops). The range of multi-links is between zero and : if we consider a pair of blocks (or one block internally), there can be at most nodes in such a pair (in one set, slightly less), since there must be at least nodes in the other blocks of the partition. Obviously, in such a subgraph of nodes there can be at most links. Thus, the number of values each multi-link can take is upper-bounded by . Since the number of node pairs in the reduced multi-graph is , we obtain the second multiplier in the argument of in the proposition.

Finally, we show that the coding of the graph is prefix. We concatenate both parts into one code that has the prescribed length and put first the prefix code of the integer that defines the parameters of the maximum likelihood model. When we start to decode from the beginning of the entire code, we first obtain a code of an integer, because we used a prefix coding for integers. At this stage we are able to define the probabilistic model that was used to create the other part of the code, corresponding to the probability distribution . Using this information we can decode the graph . It remains to show that the concatenated code itself is prefix. Assume the opposite: some prefix of such a code is prefix to some other similar code, say, the first code is a prefix to the second one. However, the parametric code was prefix, so both codes must correspond to the same model. Since the first two-part code is a prefix to the second, they both share the same parametric part, and the code for the graph of the first is a prefix of the second one. But this is impossible, since the encoding for graphs within the same model is prefix. This contradiction shows that the two-part coding is prefix. ∎

Finally, we call

| (3.6) |

the full regular decomposition modeling space of .

3.3 Two-part MDL for matrices

In this section we consider input data in the form of a matrix with non-negative entries. With such a matrix we associate a random bipartite multi-graph. The set of rows and the set of columns form a bipartition. Between row and column there is a random number of links that are distributed according to Poisson distribution with mean . Such a model was introduced in [14] and it has been used in various tasks in complex network analysis, see [8]. The aim of this model is to back up, heuristically, a corresponding practical algorithm for regular decomposition of matrices. Our approach is closely related to but slightly different from the Poissonian block model. Assume that is used to generate random matrices with independent integer-valued elements following Poisson() distributions. The target is to find a regular decomposition model that minimizes the expected description length of such random matrices. We propose the following modeling spaces:

Definition 3.4.

For integers , from ranges and , the parameters of a model in the modeling space for an integer matrix are partition of rows into non-empty sets and partition of columns into non-empty sets and block average matrix , with elements .

Thanks to the addition rule of Poisson distributions, the likelihood of in a model , corresponds to probabilistic models where the elements of are independent and Poisson distributed with parameters , where , in the model . The corresponding likelihood is denoted as , the actual probability of is denoted as . The maximum likelihood model is found from the program that maximizes the expected log-likelihood:

where is the Kullback-Leibler divergence between distributions, denotes entropy and and are the two families of Poisson distributions for the matrix elements of . Since is independent of , it does not affect the identification of the maximum likelihood model. Thus, the final program for finding the optimal model is

| (3.7) |

The description length of a model consists of the description length of the two partitions and the description length of the block average matrix . For the latter we need to know only the integers presenting the block sums of , since the denominator is known for a fixed partition . The code lengths of such integers are, for large matrices, simply the logarithms of the integers. For we use the same entropy based formula as in (4.1). As a result we end up with the following expression for the description length of the random multi-graph model using the modeling space :

where

The star superscript refers to parameters corresponding to the solution of the program (3.7). The expectation of logarithm is not explicitly computable. However, we assume large matrices and blocks, and then Jensen’s inequality provides a tight upper bound that can be used in practical computations. Thus, the final expression for the description length of is

| (3.8) |

where

The full two-part MDL would now be realized by finding the global minimum of this expression over various . We return to this case in the algorithm section 6.1. Although a heuristic one, we believe that our method for matrices is both reasonable and easy to use and implement, see [21].

3.4 Refined MDL and asymptotic model complexity

Let us next consider Rissanen’s refined MDL variant (see [6]). The idea is to generate just one distribution on , called the normalized maximum likelihood distribution . Then a graph has the description length which is at most as large as the one given by the two-part code in (3.4). The function maps graphs of size into , and it is not a probability distribution, because . However, a related true probability distribution can be defined as

| (3.9) |

The problem with this is that a computation of the normalization factor in (3.9) is far too involved: finding a maximum likelihood parametrization for a single graph is a ‘macroscopic’ computational task by itself and it is not possible to solve such a problem explicitly for all graphs. Therefore the two-part variant is a more attractive choice in a practical context. However, the refined MDL approach is useful as an idealized target object for justifying various approximate implementations of the basic idea. It appears that in an asymptotic sense the problem is solvable for large simple graphs. The logarithm of the normalization factor in (3.9) is called the parametric complexity of the model space :

| (3.10) |

In a finite modelling space case like in ours, this can be considered as a definition of model complexity. We have now the following simple bounds:

Proposition 3.5.

where we use the same notation as in Proposition 3.3.

Proof.

The lower bound follows from the fact that we can have at least this number of graphs that have likelihood 1 in . This corresponds to graphs for which the nodes can be partitioned into non-empty sets and inside each set we have a full graph and no links between the distinct sets. Thus, for every partition there is at least one graph that has likelihood one and all such graphs are different from each other since there is a bijection between those graphs and partitions.

For the upper bound, we notice that according to Proposition 3.3, there is a prefix coding with code lengths that correspond to the two-part code. As a result, Kraft’s inequality yields that , or

from which we get

Taking logarithms, we arrive at the claimed upper bound. ∎

When considering large-scale structures corresponding to moderate , the upper and lower bounds in Proposition 3.5 are asymptotically equivalent, and we have

Corollary 3.6.

Assume that is fixed. Then

Proof.

Denoting the lower and upper bound of parametric complexity in Proposition 3.5 respectively by and , we argue that asymptotically when . This follows from the fact that the dominant asymptotic component of both and is . Indeed, for fixed , the asymptotic of is linear in , and all other terms of the asymptotics of both bounds are additive and at most logarithmic in . ∎

Remark 3.7.

The speed of convergence of the upper and lower bounds in Proposition 3.5 is of type .

3.5 -regularity vs. stochastic block models

Although the structure that a MDL-based algorithm finds typically looks like an -regular structure, there is a principal difference. In particular cases, an -regular graph can have a structure that allows much better compression than that provided by the -regular partition. In this section we give an explicit example of such a case.

An important point in SRL is that for any , there is an upper bound for the size of regular partition, so that for any graph with size above some finite threshold , all such graphs have a regular partition with at most sets. Based on this, we show that the -regular structure of SRL and the structure induced by the MDL need not coincide. Let us fix an order of graph , large enough so that SRL holds for some , and that for some fixed .

Proposition 3.8.

There is a graph of order such that it has a MDL structure with code length and an regular structure that allows only code length, where denotes any strictly linear function of .

Proof.

Take large enough as prescribed above. Then construct a bipartite graph with such that is divisible by with some rational . Assume that both parts of the bipartition are further partitioned into equal size blocks: , . Define then a random graph as follows. For each pair , take , where is a Bernoulli random variable with parameter , and the variables for different pairs are independent. Assume that there are no other edges.

We show that, with high probability, is -regular with regular partition . In the -approach, such a structure has a coding length at least . This comes from the log-likelihood part, and the corresponds to very small deviations of link densities from the expected value that can be made arbitrarily small by increasing . Now we check that the -regularity of graph has a positive probability, which implies that such an -regular pair exists (actually, it appears that this happens with high probability). -regularity means that for any , , , the link density deviates from the link density of the pair, , no more than by . By definition,

and as a result the expectation is

Denote

The range of is interval of unit length. Hoeffding’s inequality yields for that

where is the range of variable . The denominator of the exponent in the right hand-side of the Hoeffding inequality can be bounded as

By taking we get for the link density:

Finally, since there are at most pairs of subsets from which to choose, the probability that none of them violates regularity is lower bounded by

if the exponent has a positive power of , and this happens when . Thus, all large subsets have densities that deviate from expectation less than with a probability tending to one. Thus, we have shown the -regularity of the partition .

On the other hand, using MDL, we could reach the level of small sets and , and the corresponding log-likelihood is zero. The model complexity is , as can be easily seen from asymptotic formulas for the upper bound for , with . ∎

4 The Regular Decomposition approach to stochastic block models

4.1 Block model codes

The previous section developed both the two-part and refined variants of the MDL theory, as presented in [6], for the model space of stochastic block models. In the following, we formulate a variant of two-part MDL that allows both practical implementations and a proof of consistency, i.e., that the MDL principle identifies a correct block model. It was shown above that the most difficult task in the description of a block model is identifying the partition. The same is true for the model complexity, which is asymptotically just the logarithm of the number of partitions. It appears that in order to prove consistency, we need quite a delicate estimate for the description length of the partition. The asymptotic model complexity given in Corollary 3.6 seems to be too crude for proof of consistency. A full resolution of this intriguing question is left for further investigations.

We call our two-part MDL construction a block model code of a graph with respect to a partition of its nodes that allows the computation of a tight upper bound of the code length. This upper bound is also consistent with a more generic information theoretic point of view with a semi-constructive coding scheme.

We denote by both Shannon’s entropy function of a partition and the entropy of a Bernoulli distribution, i.e.

Remark 4.1.

In the rest of this paper, we define also information-theoretic functions in terms of natural logarithms, and certain notions like code lengths should be divided by to obtain their values in bits.

Definition 4.2.

A block model code of a graph with respect to a

partition of is a code with the following structure:

The model part:

-

•

first, the sizes of the blocks are given as integers;

-

•

second, the edge density inside each block and the edge density between each pair of distinct blocks are given as the numerators of the rational numbers presenting the exact densities.

The aim of these two codes is to describe the parameters of two

probability distributions, one for the links and the other for the membership

of nodes in the blocks of the partition.

The data part:

-

•

third, the partition is specified by a prefix code corresponding to membership distribution , where all nodes are independent of each other;

-

•

fourth, the edges inside each block are specified by a prefix code corresponding to a stochastic block model distribution of links inside each block of ;

-

•

fifth, the edges between each pair of blocks are specified by a prefix code corresponding to a block model distribution of links between pairs of blocks in .

The description of link densities as link probabilities (the second code) is natural, since conditionally to a partition the stochastic block model is just a collection of Bernoulli models, where the best choice is to use averages as parameters. Note that a block model code can be given for any graph with respect to any partition of its nodes.

From Kraft’s inequality and the above definitions, it follows that there exists a prefix code for a graph with respect to a partition of with length at most (and, for large graphs, typically close to)

| (4.1) | ||||

where was defined by (3.5). Below we shall approximate by without further mentioning, because their difference is insignificant in our context. Similarly, we have dropped ceiling functions systematically. Also, recall Remark 4.1 on the use of natural logarithms.

Next, we shall define block model codes for the Poissonian block models of Definition 2.5. The entries of the random matrix are Poisson distributed integers. For a pair of disjoint sets , the set is a sample from a distribution that is mixture of Poisson distributions. It would be hard to encode the sample by first estimating the unknown mixture distribution. Instead, we base the code simply on the sample mean

and encode as if it came from a Poisson distribution with parameter . Thus, by Kraft’s inequality, a value can be well encoded by a codeword with approximate length

By the fundamental information inequality

this encoding is suboptimal for arbitrary disjoint subsets and , but it is optimal when and are blocks of the model partition and presents a pure Poisson distribution. Thus, the suboptimality only improves the contrast between and other partitions of .

For an arbitrary partition , the encoding of all with the above rule requires about

where -symbols refer to the empirical distribution of the s,

and

Now, we define the Poissonian block model code length of with respect to any partition as

| (4.2) | ||||

Note that the term is independent of the partition and can be neglected when minimizing over .

4.2 Accuracy of block structure identification by MDL

The general idea of the Regular Decomposition method is to be a generic tool for separating structure and randomness in large data sets of graph or matrix form. A partition of a real-world data set that minimizes the (nominal) code length given in (4.1) resp. (4.1) can often not be compared with a ‘true solution’ for the simple reason that there may not be any objective notion of a ‘true structure’ of the data. However, it is important to analyse and understand how the method performs when the data really originates from a stochastic block model. This question is called the consistency of MDL. Our results on this question are summarized in the following theorem, formulated in terms of the asymptotic behavior of a model sequence as specified by Construction 2.3. In such a framework, an event is said to happen with high probability, if its probability tends to 1 when .

Theorem 4.1.

Consider a sequence of stochastic block models based on a vector of relative block sizes and a matrix of link probabilities, as described in Definition 2.2 and Construction 2.3. With high probability, the following hold:

-

1.

Among all partitions of such that , is the single minimizer of .

-

2.

For any fixed , is the single minimizer of among partitions with minimal block size larger than .

-

3.

No refinement of with improves by more than .

The corresponding claims hold for the Poissonian block model mutatis mutandis.

Proof.

The results of Section 5 offer a richer picture than what was distilled into Theorem 4.1. For example, Proposition 5.1 shows that if and differs from only a little, then the remaining misplaced nodes can be immediately identified by computing their effect to the value of . On the other hand, we have not been able to exclude the possibility that a refinement of could yield a slight improvement of the code length.

Remark 4.3.

It is rather obvious that with large , the identification of the block structure is robust against independent noise. The simplest case is that the Poissonian block model is disturbed by additive Poissonian noise to each matrix element:

where the s are i.i.d. with , . Then is again an irreducible Poissonian block model with the same partition. More interesting cases are binary flips in the graph case and multiplicative noise with mean 1 in the case of non-negative matrices. We leave these for forthcoming work.

5 Proof of Theorem 4.1

Through this section, we consider a sequence of increasing versions of a fixed stochastic block model based on a vector of relative block sizes and a matrix of link probabilities, as specified in Construction 2.3.

Consider partitions of . Denote

Thus, if and only if is a refinement of . If and , denote by the partition obtained from by moving node to block (if , then ).

Proposition 5.1.

There is a number such that the following holds with high probability: if and , then

Proof.

Let be small numbers and a positive integer to be specified. They can be chosen so that the following holds:

-

•

is small so that and nearly overlap when :

(5.1) -

•

all the differing link probabilities are widely separated in units:

(5.2) -

•

the empirical densities are close to their mean values: for any (possibly ), we have, with high probability,

(5.3)

Let be a partition of such that . Condition (5.1) entails that for each block there is a unique block such that . Let us now assume that and , and compare the partitions and . Denote , , and , . Then

| (5.4) |

Consider first the sum over . Leaving out the common factor , each term of the sum can be written as

(note the addition and subtraction of the term ). Using Lemmas A.3 and A.7, and the assumptions on , and , the last expression can be set to be, with high probability, arbitrarily close to the number

(the function , the Kullback-Leibler divergence of Bernoulli distributions, is defined in (A.2)). Thus, the sum over is, with high probability, close to

Let us then turn to the remaining parts of (5.4) that refer to two codings of the internal links of . Similarly as above, we can add and subtract terms to transform these parts into

By the above analysis of (5.4), we have obtained

| (5.5) |

By the irreducibility assumption (2.1), there is a block such that , with the possibility that . It follows that at least one of the ’s in (5.5) is positive. Denote

Thus, with high probability,

On the other hand, it is easy to compute that

The changes of and when moving from to are negligible. This concludes the proof. ∎

The proof of Proposition 5.1 showed that when , moving any node to its correct block decreases at least by . In particular, with high probability, is the unique minimizer of among -partitions satisfying .

Proposition 5.2.

For any and positive integer , there is a constant such that the following holds with high probability:

Proof.

Fix an and let be a partition of such that . By the concavity of , we have

| (5.6) |

By assumption, there is such that for every . It is easy to see that there must be (at least) two distinct blocks, say and , such that

| (5.7) |

By the irreducibility assumption (2.1), there is a block such that , with the possibility that . Fix an arbitrary to be specified later. By -regularity (claim 2 of Lemma A.7), with high probability, every choice of a partition with results in some blocks , , with the above characteristics plus the regularity properties

| (5.8) |

where denotes a block of that maximizes (note that because , ). By the concavity of ,

In the case that and , we obtain a similar equation where is partly replaced by . Because of (5.8) and (5.7), the difference between the sides of the equality has a positive lower bound that holds with high probability. On the other hand, this difference is part of the overall concavity inequality (5.6). ∎

Proposition 5.3.

For any refinement of , we have

| (5.9) |

where refers to stochastic order, the ’s are i.i.d. Exp random variables, and

| (5.10) |

Proof.

Here we apply results presented in Appendix A. Denote by the subset of whose members are subsets of the block of . Writing the edge code lengths of the coarser and finer partition similarly as in (5.6), taking the difference and using (A.5), we obtain

| (5.11) |

Applying Proposition A.6 to each term of both outer sums now yields the claim, because

∎

Remark 5.4.

It is rather surprising that the stochastic bound (5.9) depends only on the number of blocks in — not on their relative sizes, nor on the overall model size .

Proposition 5.5.

For any positive integer , the following holds with high probability:

where the relation means that is a refinement of , and was defined in (5.10).

Proof.

Let be a refinement of . Refining the partition w.r.t. yields a gain, based on the concavity of , in the code part , but costs in the parts , and . We have to relate these to each other.

Consider first the value of . In our analysis, it is important to distinguish between ‘large’ and ‘tiny’ blocks, where the relative sizes of large blocks exceed some pre-defined number and the rest can be arbitrarily small, even singletons. Now, each block must contain at least one block such that . Define

Because no concavity gain can be obtained with an index pair such that , it does not restrict generality to assume that for all . Then, by (4.1),

On the other hand, the bound yields

Thus,

| (5.12) |

We obviously have also , but this difference is insignificant in the present context.

The refinement gain in code parts and was bounded in Proposition 5.3 stochastically by Exp random variables. The rate function (see the beginning of Appendix A) of the distribution Exp is

Denote

Proposition 5.3 yields, using (A.1) and Proposition A.1, that for

where the second factor is bounded and will be henceforth neglected.

For two refinements of , write if the block sizes of in each are identical to those of . The number of refinements of with is upperbounded by

where denotes the entropy of the partition of induced by . On the other hand, we have

Write

Denote . Recalling (5.12), the union bound yields

The number of different block size sequences is upper bounded by . Thus, a second application of the union bound yields

∎

Corollary 5.6.

is the unique minimizer of among partitions with .

Proof.

Proposition 5.7.

Let . Consider refinements of with relative minimal block size , i.e. the set

| (5.13) |

With high probability,

| (5.14) |

Proof.

The restriction implies . The difference to the conditions of Proposition 5.5 is now just the magnitude of . When ,

so that

By a corresponding computation as in the proof of Proposition 5.5, we obtain for any fixed that

Proceeding with a second union bound like in the proof of Proposition 5.5 yields

where the maximum over was obtained with the smallest value . ∎

6 Algorithms, codes and illustrations

6.1 Regular decomposition algorithms based on MDL

In this section we present algorithms that we have used in actual computations of regular decompositions of graph and matrix data. These are written for standard two-part MDL, where the code lengths and have a usual interpretation as a minus log-likelihood of a graph corresponding to a stochastic block model.

Thus, we use link coding lengths found in the upper bound of Proposition 3.3. In many cases, this is all that can be computed realistically. Moreover such overestimating is not critical since the over-fitting seems to be a common problem, because the minimum of MDL tend to be very shallow and is easily passed unnoticed. We can obviously describe a partition into nonempty sets using an binary matrix with all row sums equal to one and requiring that none of the column sums equals zero. The space of all such matrices we denote as and the members of this set as .

Definition 6.1.

For a given graph with adjacency matrix and a partition matrix , denote

where stands for matrix transpose, the column sums of are denoted as

and the number of links within each block and between block pairs as

where if and otherwise. Then define

Then the coding length of the graph corresponding to using the model is:

Definition 6.2.

where

is the code length of the model, according to our theory and notation.

The two-part MDL program of finding the optimal model, denoted as , can now be written as:

| (6.1) |

To solve this program approximately, we can use the following greedy algorithm.

Algorithm 6.3.

Greedy Two-part MDL

Input: a simple graph of size .

Output: , such that the two-part code for is shortest possible for all models in by using this pair as a model.

Start: , , ,

, where is denotes the matrix with all elements equal to .

1. Find

using subroutine ARGMAX k (Algorithm 6.5).

2. Compute

3. If then , ,

4.

5. If , Print and STOP the program.

6. GoTo 1.

Definition 6.4.

Matrices noted as and are defined as:

where we set (all values will be later multiplied by 0),

A mapping is defined as follows:

The mapping moves each node to a possibly different block in such a way that the description length would be minimized if all other nodes stay in their current blocks. A Python code with generating synthetic binary graphs is given in [20].

Algorithm 6.5.

ARGMAX k

Algorithm for finding optimal regular decomposition for fixed

Input: : the adjacency matrix of a graph (an symmetric binary matrice with zero trace); : an integer (the number of iterations in the search of a global optimum);

: a positive integer.

Start: .

1. ; generate a uniformly random element .

2. If at least one of the column sums of is zero, GoTo 1. Otherwise, set

3. If , set and GoTo 2.

4. ; ;

.

5. If , GoTo 1.

6. ; .

Output optimal solution: .

For very large graphs, the program may not be solvable in the sense that it is not possible and reasonable to go through all possible values of . One option is to limit the range of . In case that no minimum is found, then use as an optimal choice the model found for the largest within this range. Another option is to find the first minimum with smallest and stop. When the graph is extremely large, it makes sense to use only a randomly sampled sub-graph as an input — indeed, when , a large-scale structure can be estimated from a sample [24].

Our algorithm for Poissonian block models and matrices is essentially similar, with certain differences in formulae as detailed below. Algorithms for other cases like directed graphs and non-quadratic matrices are written very similarly, although two partitions are needed, one for rows and one for columns. The logic of the solution remains the same however.

A semi-heuristic two-part MDL algorithm for finding a regular decomposition for an matrix with non-negative entries works as follows. The decomposition takes a form of a bi-clustering: there are two partitions, one for rows and one for columns. Such partitions are described by binary matrices with row sums equal to one. The two-part MDL program to find an optimal regular decomposition is written as follows:

The row partition-matrices are denoted as with dimensions , , and the column partition matrices as with dimensions , .

Let us formulate the cost function for the matrix case that is derived from Eq (9). The number of matrix elements in row group and column group can be written as a matrix element:

Assuming that all blocks are non-empty, all , we can define an average matrix element of block . First compute the sum of all matrix elements of over such a block:

The corresponding block averages form a -matrix with elements

The coding length of the matrix using a two-part MDL code with partitions can be written as

Here we assume a similar handling of ’s as in the binary case. and are the sizes of row and column blocks, and denotes the integer part of ; it is assumed that such block sums are large numbers with finite decimal precision . The description length of such decimals is the last term and it is small compared with other terms for large matrices and can be safely ignored. Similarly to the binary case, the two-part MDL program is defined as:

Definition 6.6.

| (6.2) |

where

The greedy algorithm for solving this program is very similar to the case of a binary matrix. The difference is that two parametric sequences of partitions must be searched, and , and in the subroutine that finds the optimal partitions for fixed and . One may consider different strategies in the corresponding search of an optimal pair. For instance, moving first along the diagonal , and finding the value where the cost function (coding length of ) has a knee-point, and after that make an off-diagonal search near that value. Another option could be moving along the steepest descent direction of the cost function, or alternating the directions of increments in and , until a saturation is reached in one direction, and then keeping that parameter fixed and finding the optimum on the second parameter. This question is a subject to further experimenting with real and artificial data. Therefore we write only the subroutine that finds the optimal partitioning with fixed and in a greedy fashion. First we need

Definition 6.7.

Define the mappings and as follows. Let be an matrix with all elements equal to . Then, using the definition of -matrix and -matrix (related to as in binary case), define two matrices using a block-matrix notation:

and

Define

and

Then,

and

The main greedy subroutine is:

Algorithm 6.8.

ARGMAX

Algorithm for finding optimal regular decomposition for fixed .

Input: : a real matrix with non-negative entries; : a positive integer (the number of iterations in the search of a global optimum); : a pair of positive integers.

Start: .

1. ; generate uniformly random elements . and .

2. If at least one of column sums of or is zero, GoTo 1. Otherwise, set

3. If or , set and GoTo 2.

4. ; ; ;

5. If , GoTo 1.

6. ; .

OUTPUT optimal solution: .

Remark 6.9.

It is also possible to find regular decompositions in the case of partly missing matrix elements [23, 24]and also in the case of mixed positive and negative entries. In the latter case, we can use the idea of directed links already used in[13]. In the first case, we note that the main characteristic of the regular decomposition is the -matrix with elements that are averages of the data matrix over large blocks that can be estimated, in many cases, despite a portion of data is missing.

6.2 Simulations

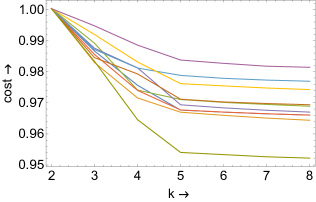

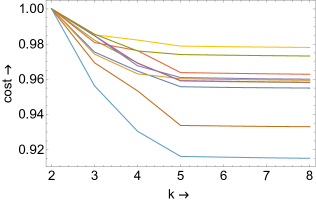

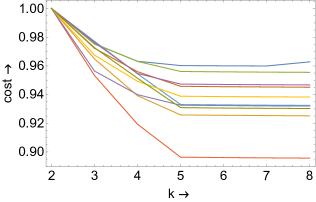

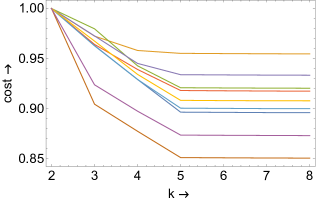

To illustrate MDL based RD, we run several computer experiments. The purpose was to verify whether the right numbers of blocks could be found.

We used a simple stochastic block model for this purpose. There were blocks and each node was placed in a block uniformly at random. The number of nodes was . Link probabilities in blocks and between them were uniformly random reals in range . After the probabilities were generated they were multiplied by a constant factor . These factors had values and experiments were run for each value. The aim of the factor was to generate graphs with different densities.

For each set of parameters, experiments were repeated times to get diversity of samples. RD algorithm was run in one node of a high power computation cluster at VTT. The whole experiment took several days to complete.

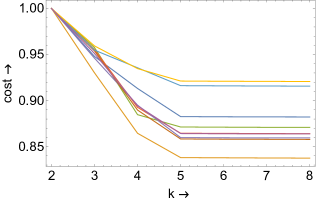

The result in most cases is that the right number of blocks can be identified. The results are presented graphically in the series of figures in Figure 1. The cost function is the smallest found - log-likelihood + the complexity term . The first corresponds to the length of a code that encodes the partition and the last one to the coding length of the number of links between and inside the block. The cost function shows a characteristic kink at value . After this value of is exceeded the cost function remains almost flat.

|

|

|

|

|

The main observation is that RD must be done carefully, meaning that the greedy algorithm must be rerun many times in order to find a good approximation of the global optimum. In our case runs seems to work.

In [24] we showed that RD can work on very large graphs generated from a SBM, provided is a known constant and the graph is dense with fixed link probabilities independent on graph size. When MDL is used in RD, it is very likely that the right structure can be found from samples of a very large graph without knowing the right .

SBM is called sparse when link probabilities tend to as . In this case we suggested [22] to use RD to analyze the graph distance matrix instead of the adjacency matrix. In cases when the graph distances can be estimated, this could be used to find block structures of very large graphs using a similar sampling approach as in the dense graph case.

Appendix A Chernoff bounds and other information-theoretic preliminaries

Consider a random variable with moment generating function

and denote . We restrict to distributions of for which is an open (finite or infinite) interval. The corresponding rate function is

is a strictly convex function with minimum 0 at and value outside the range of . For the mean of i.i.d. copies of , we have

| (A.1) |

The Chernoff bound (also known as Cramér-Lundberg bound):

Proposition A.1.

This has the following simple consequence that plays an important role below. Let the convex hull of the support of be the closure of , and denote

( if and only if the distribution of has an atom at , similarly for ). We can now write

With the assumptions made above, the functions and are, respectively, bijections from and to and .

Lemma A.2.

where denotes stochastic order and is a random variable with distribution Exp.

Proof.

In the case that has the Bernoulli distribution, we have

| (A.2) |

Lemma A.3.

The first and second derivatives of the functions and are

| (A.3) | ||||||

| (A.4) |

Since and , we also have

| (A.5) |

and

Proposition A.4.

Let and let and be independent random variables with distributions Bin and Bin, respectively. Denote and , , . Then the following identities hold:

| (A.6) | ||||

| (A.7) | ||||

| (A.8) |

The identities in Proposition (A.4) are obtained by writing the full expression of (A.6) and re-arranging the terms in two other ways. Formulae (A.7) and (A.8) are written without , expressing the fact that any two of the three random variables , and contain same information as the full triple. Note that (A.7) and (A.8) do not contain . This reflects the fact that the conditional distribution of given , known as the hypergeometric distribution, does not depend on . The identity of (A.6) and (A.8) can be interpreted so that the two positive terms of (A.6) measure exactly same amount of information about as what is subtracted by the negative term. Moreover, (A.8) has the additional interpretation of presenting the rate function of the hypergeometric distribution:

Proposition A.5.

Let have the distribution Hypergeometric, i.e. the conditional distribution of of Proposition A.4 given that . The rate function of is

| (A.9) |

Proof.

Define the bivariate moment-generating function of

Write

and note that we can assume . We can now derive the claim using in similar manner as in the well-known proof of the one-dimensional Chernoff bound. ∎

Proposition A.6.

Let and let , , be independent random variables with distributions Bin, respectively. Denote , , and . Then

| (A.10) |

where are independent Exp random variables.

Proof.

For , the left hand side of (A.10) equals

| (A.12) |

by Proposition A.4. For any , consider the conditional distribution of (A.12), given that . By Proposition A.5, this is the distribution of the Hypergeometric rate function taken at the random variable with the same distribution. The claim now follows by Lemma A.2, because the stochastic upper bound does not depend on , i.e. on the value of .

For we proceed by induction. Assume that the claim holds for and write

By the induction hypothesis, the first row of the second expression is stochastically bounded by , irrespective of the value of . Similarly, the second row is stochastically bounded by , where , irrespective of the value of . It remains to note that can be chosen to be independent of , because is independent of , and of in particular. ∎

Lemma A.7.

Consider the sequence of stochastic block models as in Theorem 4.1. Then the following holds.

-

1.

For any blocks and such that , it holds for an arbitrary with high probability that

-

2.

For any , the partition is -regular with high probability.

Proof.

Remark A.8.

Because as , the proof of claim 2 indicates that with a fixed , -regularity starts to hold when .

Preliminaries for the Poissonian block model

By the Poissonian block model, the function replaces binomial entropy in the counterparts of code lengths . We indicate below how the crucial steps of the proofs would change.

Denote by the Kullback-Leibler divergence between distributions and

| (A.13) |

For a counterpart to Lemma A.3, note that, for any ,

| (A.14) |

Lemma A.9.

For any and , denote . Then we have

| (A.15) | ||||

| (A.16) |

Proof.

The Poissonian counterpart of Proposition A.6 is the following.

Proposition A.10.

Let , , , , and . Let , , be independent random variables with distributions Poisson, respectively. Denote , and . Then

| (A.17) |

where are independent Exp random variables.

Proof.

The proof of Proposition A.6 can be imitated as follows:

-

•

Using induction, it suffices to consider the case .

- •

- •

∎

Acknowledgment. We thank Dr. Tomi Räty for proof-reading the manuscript and for making many useful suggestions. This work was partly financially supported by the Academy of Finland projects 294763 (Stomograph) and 288907.

References

- [1] N. Alon, R. Duke, H. Lefmann, V. Rödl, and R. Yuster. The algorithmic aspects of the regularity lemma. Journal of Algorithms, 16:80–109, 1994.

- [2] N. Alon, E. Fischer, I. Newman, and A. Shapira. A combinatorial characterization of the testable graph properties: It’s all about regularity. In STOC’06, Seattle, U.S., May 2006.

- [3] M. Bolla. Spectral Clustering and Biclustering. Wiley, 2013.

- [4] T. Cover and J. Thomas. Elements of Information Theory. John Wiley and Sons, U.S.A., 1991.

- [5] E. Fischer, A. Matsliah, and A. Shapira. Approximate hypergraph partitioning and applications. Foundations of Computer Science, pages 579–589, 2007.

- [6] P. Grünwald. Minimum Description Length Principle. The MIT Press, 2007.

- [7] S. Heimlicher, M. Lelarge, and L. Massoulié. Community detection in the labelled stochastic block model. In NIPS Workshop on Algorithmic and Statistical Approaches for Large Social Networks, 2012.

- [8] R. v. d. Hofstad. Random graphs and complex networks. Cambridge University Press, 2016.

- [9] P. Holland, K. Laskey, and S. Leinhardt. Stochastic blockmodels: First steps. Social Networks, 5(2):109–137, 1983.

- [10] J. Komlós and M. Simonovits. Szemerédi’s regularity lemma and its applications in graph theory. In D. Miklós, V. Sós, and T. Szonyi, editors, Combinatorics, Paul Erdös is Eighty, pages 295–352. János Bolyai Mathematical Society, Budapest, 1996.

- [11] P. Kuusela, I. Norros, H. Reittu, and K. Piira. Hierarchical multiplicative model for characterizing residential electricity consumption. Journal of Energy Engineering, 144(3), 2018.

- [12] L. Massoulié. Community detection thresholds and the weak Ramanujan property. In Proceedings of the Forty-sixth Annual ACM Symposium on Theory of Computing, STOC ’14, pages 694–703, New York, NY, USA, 2014. ACM.

- [13] T. Nepusz, L. Négyessy, G. Tusnády, and F. Bazsó. Reconstructing cortial networks: case of directed graphs with high level of reciprocity. In B. Bollobás, R. Kozma, and D. Miklós, editors, Handbook of Large-Scale Random Networks, number 18 in Bolyai Society of Mathematical Studies, pages 325–368. Springer, 2008.

- [14] I. Norros and H. Reittu. On a conditionally Poissonian graph process. Adv. Appl. Prob., 38:59–75, 2006.

- [15] I. Pappas and P.Pardalos. Identifying cognitive states using regularity partitions. PLoS ONE, 10(8): e0137012, 2015. https://doi.org/10.1371/journal.pone.0137012.

- [16] V. Pehkonen and H. Reittu. Szemerédi-type clustering of peer-to-peer streaming system. In Proc. Cnet 2011, San Francisco, U.S.A., 2011.

- [17] T. P. Peixoto. Entropy of stochastic blockmodel ensembles. Physical Review E, 85(056122), 2012.

- [18] T. P. Peixoto. Parsimonious module inference in large networks. Phys. Rev. Lett., 110:148701, Apr 2013.

- [19] M. Pelillo, I. Elezi, and M. Fiorucci. Revealing structure in large graphs: Szemerédi’s regularity lemma and its use in pattern recognition. Pattern Recognition Letters, 87:4–11, 2017.

- [20] H. Reittu. Regular decomposition python code for simple graphs. 2019. https://github.com/hannureittu/Regular-decomposition.

- [21] H. Reittu, F. Bazsó, and R. Weiss. Regular decomposition of multivariate time series and other matrices. In P. Fränti, G. Brown, M. Loog, F. Escolano, and M. Pelillo, editors, Proc. S+SSPR 2014, number 8621 in LNCS, pages 424–433. Springer-Verlag, 2014.

- [22] H. Reittu, L. Leskelä, T. Räty, and M. Fiorucci. Analysis of large sparse graphs using regular decomposition of graph distance matrices. In Proceedings - 2018 IEEE International Conference on Big Data, Big Data 2018, pages 3784–3792, December 2018. Workshop: Advances in High Dimensional Big Data, Seattle U.S.A., Chaired by S. Tasoulis, N. Pavlidis and V. Plagianakos. DOI: 10.1109/BigData.2018.8622118.

- [23] H. Reittu, I. Norros, and F. Bazsó. Regular decomposition of large graphs and other structures: scalability and robustness towards missing data. In Proceedings - 2017 IEEE International Conference on Big Data, Big Data 2017, Boston, U.S.A., Dec. 2017. Fourth International Workshop on High Performance Big Graph Data Management, Analysis, and Mining (BigGraphs 2017), Editors Mohammad Al Hasan and Kamesh Madduri and Nesreen Ahmed.

- [24] H. Reittu, I. Norros, T. Räty, M. Bolla, and F. Bazsó. Regular decomposition of large graphs: foundation of a sampling approach to stochastic block model fitting. Data Science and Engineering, pages 1–17, 2019. https://doi.org/10.1007/s41019-019-0084-x.

- [25] J. Rissanen. A universal prior for integers and estimation by minimum description length. The Annals of Statistics, 11(2):416–431, 1983.

- [26] J. Rissanen. Stochastic Complexity in Statistical Inquiry, volume 15. World scientific, 1998.

- [27] M. Rosvall and C. T. Bergstrom. An information-theoretic framework for resolving community structure in complex networks. PNAS, 104:7327–7331, May 2007.

- [28] G. Sárkozy, F. Song, E. Szemerédi, and S. Trivedi. A practical regularity partitioning algorithm and its application in clustering. 2012. arXiv:1209.6540v1 [math.CO ] 28 Sep 2012.

- [29] A. Scott. Szemerédi’s regularity lemma for matrices and sparce graphs. Combinatorics, Probability and Computing, 20(3):455–466, 2011.

- [30] A. Sperotto and M. Pelillo. Szemerédi’s regularity lemma and its applications to pairwise clustering and segmentation. In Proc. EMMCVPR 2007, Italy, 2007.

- [31] E. Szemerédi. Regular partitions of graphs. In Problemés Combinatoires et Théorie des Graphes, number 260 in Colloq. Intern. C.N.R.S., pages 399–401, Orsay, 1976.

- [32] T. Tao. Szemerédi’s regularity lemma via random partitions, 2009. Blog entry, https://terrytao.wordpress.com/2009/04/26/szemeredis-regularity-lemma-via-random-partitions/.

- [33] Y. X. R. Wang and P. J. Bickel. Likelihood-based model selection for stochastic block models. Ann. Statist., 45(2):500–528, 04 2017.