A level-1 Limit Order book with time dependent arrival rates

Abstract.

We propose a simple stochastic model for the dynamics of a limit order book, extending the recent work of Cont and de Larrard (2013), where the price dynamics are endogenous, resulting from market transactions. We also show that the conditional diffusion limit of the price process is the so-called Brownian meander.

1. Introduction

In the now classical approach of financial engineering, one assumes a given model for the price of assets, e.g., geometric Brownian motion, and then uses the model to evaluate options or optimized portfolios. In this approach, the notion of bid/ask spread is generally not considered and the value of a portfolio is a linear function of the “price” of the assets. However, in practice, the value of a portfolio is not a linear function of the prices. In addition, also in contrast to the classical approach, the selling value of a portfolio is smaller than the buying value of the same positions. These values are really determined by the so-called limit order book, giving the list of possible bid/ask prices together with the size (number of shares available) at each price.

This limit order book changes rapidly over time, many orders possibly arriving within a millisecond. Either for testing high frequency trading strategies or deciding on an optimal way to buy or sell a large number of shares, it is important to try to model the behavior of limit order books. Several authors suggested interesting models for limit order books. For example, in Smith et al., (2003), the authors assumed that the tick size (least difference between two bid or ask prices) is constant; this implies that prices are multiples of the tick size. They also assumed that the markets orders (bid/ask) arrive independently at rate in chunks of shares; since these orders reduce the number of shares at the best bid or best ask price, they are usually combined with order cancellations. In their model, the limit orders (bid/ask) also arrive independently at rate in chunks of shares; the associated price is said to be selected “uniformly” amongst the possible bid prices or ask prices, whatever it means. Basically, they examined some properties of the resulting limit order book, trying to use techniques used in physics to characterize some macro quantities of their model.

More recently, Cont and de Larrard, (2013) proposed a similar model and they found the asymptotic behavior of the price. In fact, the behaviour of the asset price is a consequence of their model for orders arrivals. Contrary to Smith et al., (2003), they only consider the level-1 order book, meaning that only the best bid and best ask prices are taken into account. In order to do so, they assumed that the bid/ask spread is constant. As before, markets orders for the best bid/ask prices arrive independently at rate , in chunks of shares, and limit orders for the best bid/ask prices arrive independently at rate , also in chunks of shares. When the size (number of shares) of the best bid price attains 0, the bid price decreases by and so does the ask price; the sizes of the best bid/ask prices are then chosen at random from a distribution . When the size of the best ask price attains 0, the ask price increases by and so does the bid price; the sizes of the best bid/ask prices are then chosen at random from a distribution . With this simple but tractable model, they were able to determine the asymptotic behavior of the price process, instead of assuming it.

According to some participants in the high frequency trading world, the hypothesis of constant arrivals of orders is not justified. Therefore, one should assumed that the arrival rates are time-dependent. This is the model proposed here. We extend the Cont and de Larrard, (2013) setting by assuming that the rates for market orders and limit orders depend on time and that they are also different if they are bid or ask orders. As in Cont and de Larrard, (2013), under some simple assumptions, we are also able to find the limiting behavior of the price process, and we show how to estimate the main parameters of the model. The main ingredients are the random times at which the price changes, the associated counting process, and the distribution of the price changes.

More precisely, in Section 2, we present the construction of the model we consider. Under some simplifying assumptions, we derive in Section 3 the distribution of the random times at which the price changes. The asymptotic distribution of the price process is examined in Section 4, while the estimation of the parameters is discussed in Section 5, together with an example of implementation. The proofs of the main results are given in Appendix B.

2. Description of the model

We discuss a level-1 Limit Order Book model using as a framework the model proposed in Cont and de Larrard, (2013). However, the point processes describing the arrivals of Limit orders have time-dependent periodic rates proportional to the rate describing the arrival of Market orders plus Cancellations.

Recalling the Cont-de Larrard model we will define the level-1 Limit Order book model as follows:

-

•

There is just one level on each side of the order book, i.e., one knows only the best bid and the best ask prices, together with their sizes (number of available shares at these prices).

-

•

The spread is constant and always equals the tick size .

-

•

Order volume is assumed to be constant (set as one unit).

-

•

Limit Orders at the bid and ask sides of the book arrive independently according to inhomogeneous Poisson processes and , with intensities and respectively.

-

•

Market Orders plus Cancellations at the bid and ask sides of the book arrive independently according to inhomogeneous Poisson processes and , with intensities and respectively.

-

•

The processes and are all independent.

-

•

Every time there is a depletion at the ask side of the book, both the bid and the ask prices increase by one tick, and the size of both queues gets redrawn from some distribution .

-

•

Every time there is a depletion at the bid side of the book, both the bid and the ask prices decrease by one tick, and the size of both queues gets redrawn from some distribution .

2.1. Construction of the processes

First, consider the following infinitesimal generators of birth and death processes:

| (1) |

| (2) |

Note that is an absorbing state for any Markov chain with generators or . When a chain reaches the absorbing point , one calls it extinction.

To describe precisely the behavior of the price process and the queues sizes process , one needs to define the following sequence of random times. Let and be the extinction times of independent Markov chains and with generators and , starting from and respectively, where and . Further set and .

Having defined , set , and let and be the extinction times of independent Markov chains and with generators and , starting respectively from and , where and , ; then set . Here the random variables are -measurable, for any . In fact, is chosen at random from distribution , while is chosen at random from distribution if and chosen at random from distribution if . Now for , and starting respectively from and at time . Finally, the price process , representing either the price or the log-price, is defined the following way: for , and if while if .

In Cont and de Larrard, (2013), the authors assumed that the arrivals were time homogeneous, meaning that and . In fact, most of their results were stated for the case , where

| (3) |

| (4) |

and

| (5) |

3. Distributional properties

Because of the independence between the ask and the bid side of the book before the first price change, to analyze the distribution of , it is enough to study one side of the orderbook, say the ask. In this case, an explicit formula for is given in the next section.

3.1. Distribution of the inter-arrival time between price changes

Let be the infinitesimal generator of a non homogeneous birth and death process given by

| (6) |

Notice that 0 is an absorbing state. Also, let be the first hitting times of 0 for this process, i.e.,

| (7) |

Then since is an absorbing state, one has .

It is hopeless to expect solving the problem for general generators so as a first approach, some assumptions and will be made.

Assumption 1.

There exists a measurable function such that for any , with and .

Remark 3.1.

Under the assumption that , a process with infinitesimal generator can be seen as a time change of a process with infinitesimal generator , viz. . In particular, if and are respectively the first hitting time of for and , then for any ,

| (8) |

This result is essential in what follows since it implies that the distribution of the time between price changes in the present model is comparable to the distribution of the inter-arrival time between price changes for the model considered by Cont and de Larrard, (2013).

The following lemma gives the distribution of the extinction time of a birth and death process with generator .

Lemma 3.2.

Let be a birth and death process with generator given by (5). If , then , where

| (9) |

and where is the modified Bessel function of the first kind.

If , then

| (10) |

In particular, .

Remark 3.3.

The case is proven in Cont and de Larrard, (2013). For the case , note that , so letting yields . It then follows that . Then . Hence the result.

It is important to analyze the tail behavior of the survival distribution for . The following lemma, whose proof is deferred to Appendix B, establishes such behavior. Recall that is the incomplete gamma function.

Lemma 3.4.

Let be a birth and death process with generator given by (5), and assume that . Set . Then, for a sufficiently large ,

Consequently, as expected, if , , whereas if , for . In particular, for every .

Remark 3.5.

Note that if , the results in Lemma 3.4 agree with the results obtained in Eq. (6) in Cont and de Larrard, (2013). However, if , Eq. (5) in Cont and de Larrard, (2013) says that , which is incorrect, since for a birth and death process with death rate larger than its birth rate , the extinction time has moments of all orders. An easy way to see this is to use the moment generating function (mgf) computed in Proposition 1 of Cont and de Larrard, (2013) and observe that if , then the mgf is defined on an open interval around 0; see, e.g., (Billingsley,, 1995, Section 21).

Lemma 3.2 allows a closed formula to be obtained for the distribution of , when the rates are proportional to each other, as in Assumption 1. Such a formula is described in the following proposition, whose proof is deferred to Appendix B.

Proposition 3.6.

Let be a birth and death process with generator satisfying . If , then the distribution of is given by

Corollary 3.7.

Under Assumption 1, for , the distribution of is given by

Proof.

The result follows from the fact that , Proposition 3.6 and the independence between and . ∎

Now, we present the asymptotic behavior of the survival distribution function of under . It follows directly from Lemma 3.4 and Corollary 3.7.

Lemma 3.8.

Let , , and set , . Assume that and . Then, as , is asymptotic to

In particular, if and , then

Remark 3.9.

It might happen that either or . If both these conditions hold, there is a positive probability that the queues will never deplete, so this case must be excluded. There are basically two cases left. The following result follows directly from the proof of Lemma 3.8.

-

(C1)

Suppose that and . Then, as , is asymptotic to

-

(C2)

Suppose that and . Then, as , is asymptotic to

In particular, if and , then

3.2. Probability of a price increase

In Cont and de Larrard, (2013, Proposition 3), the authors considered an asymmetric order flow as given here by the processes and for computing the probability of a price increase. This was not used elsewhere in their paper. They obtained the following result, which we cite without much changes. However there are some typos that are corrected here. The proof of the result is given in Van Leeuwaarden et al., (2013).

Proposition 3.10.

Suppose that and . Given , the probability that the next price change is an increase is

where , , and .

Under Assumption 1, the same result applies for our model since and .

4. Long-run dynamics of the price process

Let be the time of the -th jump in the price, as defined in Section 2.1. We are interested in analyzing the asymptotic behavior of the number of price changes up to time , that is, in describing the counting process

| (11) |

4.1. Asymptotic behavior of the counting process

The next proposition, depending on a new assumption, whose proof is deferred to Appendix B, provides an expression which relates the distribution of the partial sums for the waiting times between price changes for the models with the generators and .

Assumption 2.

. This is true for example, when (i) and , or (ii) . Properties (i) and (ii) are used for example in Cont and de Larrard, (2013).

Remark 4.2.

Under generator , are independent and are i.i.d. The starting point must be random with the correct distribution in order that has the same law as .

In order to deal with the counting process , we need another assumption.

Assumption 3.

There exists a positive constant such that as .

Remark 4.3.

Assumption 3 is true for example if is periodic. Such an assumption makes sense. One can easily imagine that repeats itself everyday. Of course, it must be validated empirically. One can also suppose that is random but independent of the other processes. In this case, would act as a random environment and if we assume that is stationary and ergodic, then Assumption 3 holds almost surely. However, in this case, all computations are conditional on the environment.

In order to obtain the asymptotic behavior of the prices, there are two cases to be taken into account: and .

4.1.1. Case

First, assume that

| (12) |

Now, from Abramowitz and Stegun, (1972, p. 376), , so for any , . In this case, it follows from Lemma 3.2 and Lemma 3.4 that

where and . Then, under Assumptions 1–2 and under model , a.s. Using Assumption 3 and Lemma 3.8, one then finds that under model , converges in probability to . Finally, using Propositions A.1–A.2, one finds that under , converges in probability to . In addition, , where is a Brownian motion. This follows from the convergence of , under , to a Brownian motian. It also holds under , using Assumption 3.

4.1.2. Case

Assume that

| (13) |

Then it follows from Lemma 3.8 and Proposition A.4 that

As a result, using Propositions A.1–A.2 with , one finds that under , converges in probability to . In particular, if , then converges in probability to . Also, , where is a stable process of index . It then follows that . Note that is the weak limit of under , and , where is the limit of , where . Next, it follows from Feller, (1971) that the characteristic function of is , where

4.2. Asymptotic behavior of the price process

Under no other additional hypothesis on and than Assumption 2, the sequence of price changes is an ergodic Markov chain with transition matrix ; the sequence is also independent from . Note that and , so the associated transition matrix is given by

with stationary distribution satisfying

If stands for the largest integer smaller of equal to , then the sequence converges in law to , where is a Brownian motion, and the variance is given by

| (14) |

with being the element of .

Remark 4.4.

If , then the variables , , are i.i.d. In fact,

and

Note also that the variables , , are independent from . However, unless and is symmetric, one cannot conclude that .

Finally, the price process can be expressed as

To state the final results, set or , according as or not. Then, using the results of Section 4.1, converges in probability to , where or according as or not. It is then easy to show that , where is a Brownian motion. In fact, for any , . Next,

| (15) |

This expression shows that there are really two sources of randomness involved in the asymptotic behavior of . As before, one must consider the cases and .

4.2.1.

In this case, setting , then , where is a Brownian motion and

| (16) |

In fact, , where and are the two independent Brownian motions appearing respectively in the asymptotic behaviour of the Markov chain and the counting process. Note that the volatility could be estimated by taking the standard deviation of the price increments every minutes, as proposed in Cont and de Larrard, (2013); see also Swishchuk et al., (2016). More generally, if is the time in seconds between successive prices and is the corresponding standard deviation of the price increments over interval of size , then .

4.2.2.

In this case, if , then using (15), one obtains that , where is the Brownian motion resulting from the convergence of the Markov chain.

However, if , then , where is the stable process defined in Section 4.1.2.

Remark 4.5.

Note that in Cont and de Larrard, (2013), , so the limiting process is a Brownian motion whether or .

4.3. Conditioned limit of the price process

If one thinks about it, what one wants to achieve in rescaling the price process is to replace a discontinuous process by a more amenable process if possible, over a given time interval. However, on this time interval, the price is known to be positive, so the limiting distribution should be also be positive.

If the unconditioned limit is a Brownian motion, then the conditioned limit, i.e., conditioning on the fact that the Brownian motion is positive, is called a Brownian meander (Durrett et al.,, 1977, Revuz and Yor,, 1999). If the unconditioned limit is a stable process, then the conditioned limit could be called a stable meander. See, e.g., Caravenna and Chaumont, (2008) for more details. Note that according to Durrett et al., (1977), a Brownian meander over has conditional density

, , where is the distribution function of a centered Gaussian variable with variance and associated density . It then follows that the infinitesimal generator of is given by

5. Estimation of parameters

In order to have identifiable parameters, one has to answer the following question about : What happens if is multiplied by a positive factor ? Then, the value in Assumption 3 is multiplied by . Thus the parameters , , , and are all divided by , since for example, . As a result, is then multiplied by and so is . It then follows that and are invariant by any scaling. So, one could normalize so that . This is what we will assume from now on. The estimation of the parameters will then be easier.

Next, one of the assumptions of the model is that the size of the orders are constant, which is not the case in practice. So in view of applications, and depending of the statistics of sizes for level-1 orders, if the chosen size is say, then an order of size would count for orders.

Assume that data are collected over a period of days. Recall that time corresponds to the opening of the market at 9:30:00 ET. Let and be the number of limit orders for bid and ask respectively up to time (measured in seconds) for day . Further let be the number of seconds considered in a day. Typically, . Finally, let and be the number of market orders and cancellations for bid and ask respectively up to time (measured in seconds) for day . For any , set , and set . Then for any , one should have approximately

Having assumed that , one can set

Finally, note that the transition matrix can be estimated directly from the data, as is from .

5.1. Example of implementation

For this example, we use the Facebook data provided in Cartea et al., (2015), from November 3rd, 2014 to November 7th, 2014. First, the results for the spread are given in Table 1, from which we can see that most of the time, the spread is .

| Day | ||||||

|---|---|---|---|---|---|---|

| Spread | 1 | 2 | 3 | 4 | 5 | Ave. |

| 91.6% | 91.8% | 89.7% | 88.4% | 93.6% | 91.0% | |

| 7.6 % | 8.0 % | 10.1% | 11.1% | 5.9% | 8.5% | |

| 0.8 % | 0.2 % | 0.2% | 0.5% | 0.5% | 0.5% | |

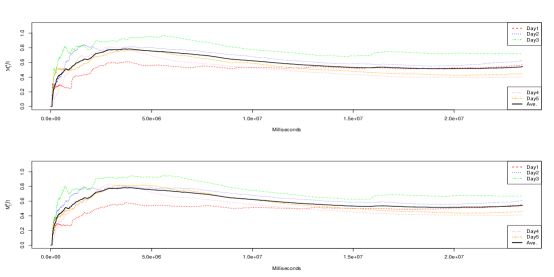

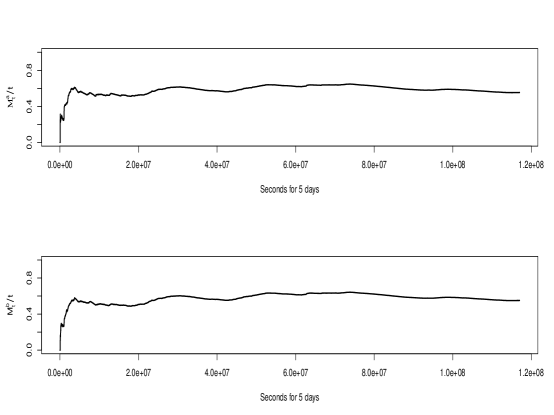

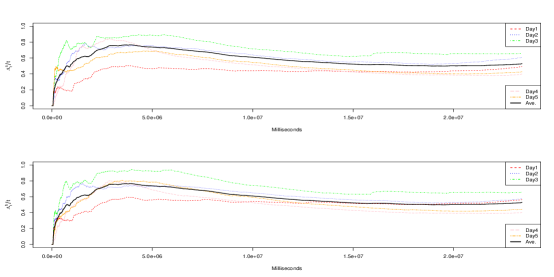

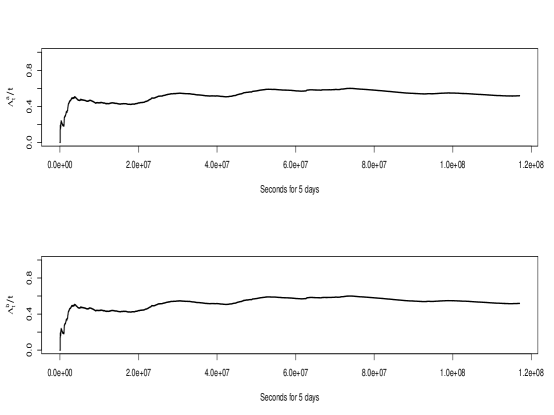

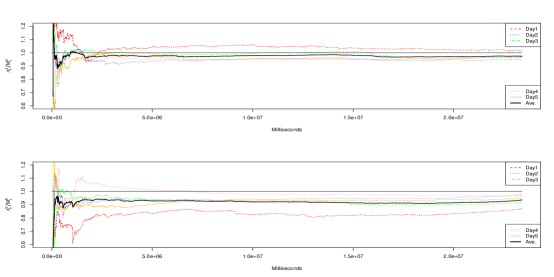

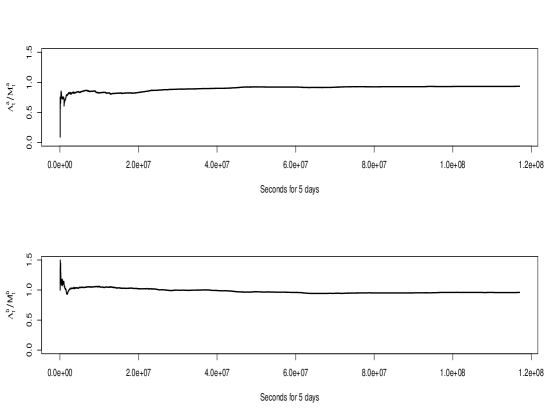

The values in Table 2 can be extracted from Figures 1–3. It follows that and , So with these data, we are in the case where , meaning that the unconditioned limiting price process is a Brownian motion with volatility satisfying (16).

Remark 5.1.

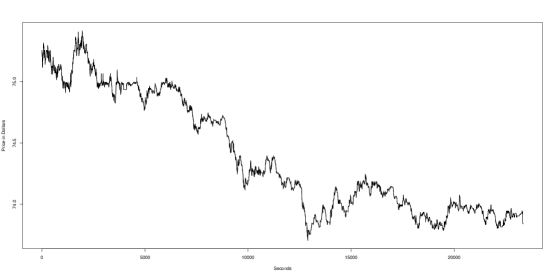

According to Figure 5, on November 3rd, the ratio is bigger than one, while the ratio is smaller than one, meaning that most of the time, the bid queue will be depleted before the ask queue, so the price has a negative trend throughout that day. This is well illustrated in Figure 7, where it is seen that the price indeed goes down on that day.

| Day | ||||

|---|---|---|---|---|

| 1 | 494.1500 | 563.2474 | 570.6227 | 553.9348 |

| 2 | 610.9476 | 578.6165 | 628.9185 | 613.8630 |

| 3 | 661.5511 | 658.3967 | 719.7569 | 672.8735 |

| 4 | 398.4293 | 401.4344 | 404.4485 | 415.3457 |

| 5 | 427.9106 | 440.4546 | 447.9598 | 458.7763 |

| ave. | 518.5977 | 528.4299 | 554.3413 | 542.9587 |

There are basically two ways of estimating . One can use the standard deviation of high-frequency data, as exemplified in Table 3, or we could use the analytic expression, as proposed in Swishchuk and Vadori, (2017), Swishchuk et al., (2016).

| Day | 10-minute | 5-minute | 1-minute |

|---|---|---|---|

| 1 | 0.0040 | 0.0052 | 0.0057 |

| 2 | 0.0079 | 0.0073 | 0.0075 |

| 3 | 0.0069 | 0.0070 | 0.0082 |

| 4 | 0.0071 | 0.0062 | 0.0059 |

| 5 | 0.0038 | 0.0040 | 0.0051 |

| pooled | 0.0062 | 0.0060 | 0.0066 |

To estimate analytically, one needs the estimation of the transition matrix . With the data set, we get . It then follows that , so , and using formula (14), one obtains . Next, , so , which is quite close to the pooled values in Table 3.

References

- Abramowitz and Stegun, (1972) Abramowitz, M. and Stegun, I. E. (1972). Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables, volume 55 of Applied Mathematics Series. National Bureau of Standards, tenth edition.

- Billingsley, (1995) Billingsley, P. (1995). Probability and Measure. Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons Inc., New York, third edition. A Wiley-Interscience Publication.

- Caravenna and Chaumont, (2008) Caravenna, F. and Chaumont, L. (2008). Invariance principles for random walks conditioned to stay positive. Ann. Inst. Henri Poincaré Probab. Stat., 44(1):170–190.

- Cartea et al., (2015) Cartea, Á., Jaimungal, S., and Penalva, J. (2015). Algorithmic and high-frequency trading. Cambridge University Press.

- Cont and de Larrard, (2013) Cont, R. and de Larrard, A. (2013). Price dynamics in a Markovian limit order market. SIAM J. Financial Math., 4(1):1–25.

- Durrett, (1996) Durrett, R. (1996). Probability: Theory and Examples. Duxbury Press, Belmont, CA, second edition.

- Durrett et al., (1977) Durrett, R. T., Iglehart, D. L., and Miller, D. R. (1977). Weak convergence to Brownian meander and Brownian excursion. The Annals of Probability, 5(1):117–129.

- Feller, (1971) Feller, W. (1971). An Introduction to Probability Theory and its Applications, volume II of Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons, second edition.

- Olver et al., (2010) Olver, F. W., Lozier, D. W., Boisvert, R. F., and Clark, C. W. (2010). NIST Handbook of Mathematical Functions. Cambridge University Press, New York, NY.

- Revuz and Yor, (1999) Revuz, D. and Yor, M. (1999). Continuous martingales and Brownian motion, volume 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, third edition.

- Smith et al., (2003) Smith, E., Farmer, J. D., Gillemot, L., and Krishnamurthy, S. (2003). Statistical theory of the continuous double auction. Quantitative Finance, 3(6):481–514.

- Swishchuk et al., (2016) Swishchuk, A., Cera, K., Schmidt, J., and Hofmeister, T. (2016). General semi-Markov model for limit order books: theory, implementation and numerics. arXiv preprint arXiv:1608.05060.

- Swishchuk and Vadori, (2017) Swishchuk, A. V. and Vadori, N. (2017). A semi-Markovian modeling of limit order markets. SIAM Journal on Financial Mathematics. (in press).

- Van Leeuwaarden et al., (2013) Van Leeuwaarden, J. S., Raschel, K., et al. (2013). Random walks reaching against all odds the other side of the quarter plane. Journal of Applied Probability, 50(1):85–102.

Appendix A Auxiliary results

Proposition A.1.

Suppose that , where the variables are i.i.d. with . Then , as .

Proof.

First, for any and ,

so as , . Next, for any non negative random variable and any ,

As a result, if , as , then, as ,

Therefore, setting , one obtains, for a fixed ,

since as . Hence, , as . ∎

Proposition A.2.

Suppose that , as , where is regularly varying of order . Define and suppose that for some function on , , as . Then .

Proof.

The proof is similar to the proof of the renewal theorem in Durrett, (1996)[Theorem 7.3]. By definition, . As a result,

By hypothesis, converges in probability to , as . Also, since is finite for any , it follows that converges in [probability to as . Next, since as , it follows that as , converges in probability to . Also, is regularly varying of order , so one may conclude that . ∎

Remark A.3.

If , then and one can take .

Proposition A.4.

Set , for any . Then there exists a constant so that for any , and any ,

Proof.

First, note that . It is well-known that

Next, set , . Then

According to Olver et al., (2010, Section 6.8.1), for any . Furthermore, and for any . As a result,

for any , where . ∎

Appendix B Proofs

Proof of Lemma 3.4.

From Olver et al., (2010)[Formula 10.30.4], for fixed , as . Also, from Abramowitz and Stegun, (1972, p. 376), , so for any , . Thus, as ,

Also, for any ,

| (17) |

Consequently, if , and

This agrees with the result proved in Cont and de Larrard, (2013). However, if , using the change of variable , one gets

To compute the expectation in the case where , note that for large enough , , whereas if , for a sufficiently large , there are finite constants and such that for any ,

∎

Proof of Proposition 4.1.

Let and denote the cdf of and , respectively, starting from , with densities and , where is the convolution of times with . The result will be proven by induction. The base case is given in Corollary 3.7. Assume the result is true for any . Then by Corollary 3.7 and the induction hypothesis,

| (18) |

Also, by the definition of and , under Assumption 2, if , then

where we used the fact that for any , given , so . Furthermore, in the last equality we used the fact that for and , non-negative independent random variables,

with and denoting the cdfs of and . Furthermore, starting from distribution , one obtains that . ∎