Records in Fractal Stochastic Processes

Abstract

The records statistics in stationary and non-stationary fractal time series is studied extensively. By calculating various concepts in record dynamics, we find some interesting results. In stationary fractional Gaussian noises, we observe a universal behavior for the whole range of Hurst exponents. However, for non-stationary fractional Brownian motions the record dynamics is crucially dependent on the memory, which plays the role of a non-stationarity index, here. Indeed, the deviation from the results of the stationary case increases by increasing the Hurst exponent in fractional Brownian motions. We demonstrate that the memory governs the dynamics of the records as long as it causes non-stationarity in fractal stochastic processes, otherwise, it has no impact on the records statistics.

I Introduction

Emergent extreme events are a key characteristic of complex dynamical systems, and the investigation of such events is a pivotal problem in understanding and predicting various complex systems Dean and Majumdar (2001); Majumdar and Krapivsky (2002); Burkhardt et al. (2007); Sabhapandit and Majumdar (2007); Györgyi et al. (2008). Recently, the extreme event studies have been developed using various approaches, such as the density of states Burkhardt et al. (2007); Sabhapandit and Majumdar (2007), first-passage and return-time statistics Majumdar and Bray (2001); Redner (2001); Leadbetter et al. (1982), persistence Majumdar (1999), interoccurrence time statistics Manshour et al. (2016); Bunde et al. (2003); Eichner et al. (2006) and record statistics Chandler (1952); Arnold et al. (1998); Nevzorov (1988). Among them, there has been considerable interest in investigating the record statistics, which has found many fruitful applications in diverse complex systems, such as spin glasses Sibani and Littlewood (1993); Sibani et al. (2006), adaptive processes Orr (2005), domain wall dynamics Alessandro et al. (1990), avalanche dynamics Doussal and Wiese (2009), stock prices Wergen et al. (2012, 2011a), global warming Wergen and Krug (2010); Newman et al. (2010), growing network Godréche and Luck (2008), high-temperature superconductors Oliveira et al. (2005), the ant movements dynamics Richardson et al. (2010), flood dynamics Vogel et al. (2001), sport statistics Gembris et al. (2002, 2007), earthquakes Davidsen et al. (2006, 2008), and evolutionary biology Franke et al. (2011); Wergen (2013).

A record is an entry in a series that is larger (or smaller) than all previous entries. From another point of view, records are extreme rare events related to an increasing (or decreasing) threshold. The investigation of the record statistics was started by the pioneering work of Chandler Chandler (1952), which was based on independent and identically distributed (i.i.d.) stochastic time series. One of the most important findings of the record statistics in such random processes is their universal characteristics in the sense that they are completely independent of the underlying distribution Arnold et al. (1998). To include more complicated systems, many research studies have been performed. For example, the record statistics of independent random variables from non-identical distributions Krug (2007), broadening distributions Krug (2007); Eliazar and Klafter (2009), and time-dependent distributions (linear drift) Wergen et al. (2011b); Franke et al. (2012) are also well understood. However, many time series in real situations are correlated. In this respect, records in symmetric random walks has been well studied, recently Majumdar and Ziff (2008), which triggers a series of new research studies, e.g., record statistics of biased random walks and Levy flights Wergen et al. (2011a, 2012), multiple independent random walks Wergen et al. (2012), and continuous-time random walks Sabhapandit (2011). The main aim of such studies is to understand and model the statistics of records in observational data by comparing with various kinds of stochastic processes. Despite the striking significance and numerous applications of fractal processes in various areas of science, much less is known about their record statistics. In this regard, it is important to improve our understanding of the record dynamics in such a broader class of stochastic processes.

In order to model turbulent flows, fractional Brownian motion (fBm), a generalization of the more well-known Brownian motion, was introduced many decades ago Kolmogorov (1940); Mandelbrot and Ness (1968), and has become one of the most studied stochastic processes widely used in a variety of fields, including physics, probability, statistics, hydrology, economy, biology, and many others Robinson (2003); Embrechts and Maejima (2002); Mandelbrot (2002); Alvarez-Lacalle et al. (2006); Varotsos and Kirk-Davidoff (2006); Karagiannis et al. (2004); Manshour (2015). A fBm is a self-similar Gaussian process with stationary increments (called fractional Gaussian noise-fGn) and possesses long-range linear correlation which depends on a parameter, called the Hurst exponent, Hurst (1951), where . The case corresponds to the ordinary Brownian motion in which successive increments are statistically independent of one another. For , the increments of the process are positively correlated (persistent), and for , consecutive increments are more likely to have opposite signs (anti-persistent).

The rest of this paper is organized as follows. In section II, we review and discuss some basic definitions and general findings in the record theory. In particular, we present important findings from two most studied time series: an i.i.d. process and a symmetric random walk. Next, by using extensive numerical analysis, we study the record statistics of non-stationary fractional Brownian motions as well as stationary fractional Gaussian noises in section III. We show that for stationary fractal series a robust universal behavior in the record dynamics is observed. We also demonstrate that the non-stationarity in fractal processes destroys such a universality observed in the stationary case. Finally, we conclude in section IV.

II General concepts in records statistics

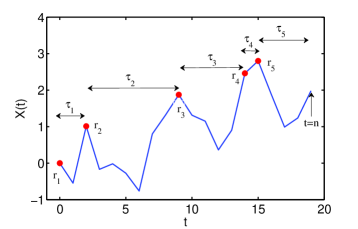

In a series of random variables , the data point is a record if . Fig. 1 represents the records evolution in a symmetric random walk, in which filled red dots show the records. One of the fundamental quantities in the records theory is the record rate, , defined as the probability that is a record. To simplify the analysis, it is helpful to introduce a quantity called the record indicator, as follows:

| (1) |

Then, in terms of the record indicator, we can write

| (2) |

Hence, the ensemble averaging of the record indicator at time step , reads,

| (3) |

In practice, represents the value that one would obtain after collecting and averaging many samples of the time series. The number of records that occur up to time is another quantity of particular interest (see Fig. 1), and defined as the sum over the record indicator

| (4) |

This means that the average record number is just the sum over the record rate ,

| (5) |

For i.i.d. random time series, due to the equal probability of the record occurrence at each time step, one finds that , which is completely independent of the underlying distribution of the series Nevzorov (1988); Arnold et al. (1998). By substituting this into Eq. 5, one obtains for the average record number , where is the Euler-Mascheroni constant Abramowitz and Stegun (1972). The mean number of records is an increasing (but extremely slow) function of time, due to the fact that the probability of the record occurrence decays with time. Also, the distribution of the record number, , over a large number of realizations of i.i.d series approaches a Gaussian function, with mean and variance of Krug (2007), as follows:

| (6) |

Similar universal properties have been found for the record statistics of symmetric random walks, by Majumdar and Ziff Majumdar and Ziff (2008). They showed that for a symmetric random walk and as . As it can be seen, the record rate of symmetric random walks decays much slower than that of i.i.d. random series. They also computed the record number distribution, and showed that it approaches a half-Gaussian form of

| (7) |

where the most probable value of is zero. We note that the standard deviation of is large () for large , in contrast to the i.i.d. case which is small () compared to the mean. This indicates that the record number distribution of a (correlated) symmetric random walk is significantly broader than that of an (uncorrelated) i.i.d. time series.

In order to search for the time characteristics of the record statistics, one may take into account the record ages. Let denote the time intervals between successive records. On the other word, is the age of the th record; i.e., it denotes the time up to which the th record survives (see Fig. 1). Note that the last record, i.e., the th record, still stays a record at the th step since there are no more record breaking events after. The typical age of a record can be estimated as , which behaves as and for i.i.d. and random walk time series, respectively Majumdar and Ziff (2008). However, there are rare records with completely different age behavior. For example, one may consider the longest age of the records. In particular, the asymptotic large behavior of the average of can be extracted explicitly as , with and for i.i.d. and symmetric random walk series, respectively Majumdar and Ziff (2008). This shows that the longest age of the records is much larger than the typical one.

Further, one may ask wether the record occurrences are correlated. To quantify such a correlation, we can take into account the joint probability of the occurrence of two records at time steps and . It was shown Arnold et al. (1998) that for i.i.d. time series, the individual record events are uncorrelated, and our knowledge about the present record tells us nothing about the future one. This means that the record events of and are completely independent if , and the joint probability becomes . In the language of probability theory, for the conditional probability we have , which defines the occurrence probability of a record at time step , given that a record has occurred in time step . Thus, in the case of i.i.d. processes, is simply equal to . For a symmetric random walk, records are not independent, and the conditional probability of two successive records is given by for large Wergen et al. (2011b). This shows that the record events in symmetric random walks effectively attract each other, i.e., there is an increased probability for the occurrence of a record if another record has occurred in the previous time step Wergen et al. (2011b).

III Records in fractals

In this section, we present an extensive numerical analysis of the record statistics for fractal time series with various Hurst exponents. We discuss the effect of correlation, as well as stationarity/non-stationarity on various aspects of the record dynamics. In order to investigate the record statistics of fractional processes, we construct such time series through a generic noise with Fourier filtering method Makse et al. (1996). Then, we search for various record features of fractional time series of size up to . Also, all calculations have been performed by averaging over different realizations.

III.1 Record rate

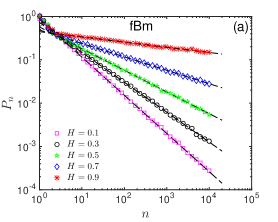

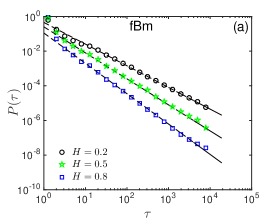

At first, we construct series of record events, corresponding to fractional Brownian motions and fractional Gaussian noises with different Hurst exponents, and search for various statistics. In Fig. 2(a), we plotted in logarithmic scale, the record rates for fBm series with different Hurst exponents of , , , , and . We fit power-law functions (dashed lines) of the form of to the record rates, and find that . Majumdar and Ziff showed Majumdar and Ziff (2008) that the probability for a record in the th event of a symmetric random walk is the same as the corresponding persistence probability , which is the probability that a random walker starting from the origin stays bellow the origin without crossing it for the next steps, and given by as . On the other hand, it was shown Krug et al. (1997) that the persistence probability for a fBm series is given by . Here, we find numerically such a power-law behavior for the record rate of fractional Brownian motions.

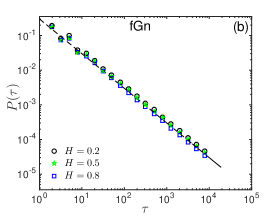

We also search for the record rates corresponding to fractional Gaussian noises. Fig. 2(b), shows log-log plots of the record rates, , for different Hurst exponents. Interestingly, all the curves collapse into a universal power-law function of the form of (dashed line) for the whole range of Hurst exponents. This result is the same as the one obtained for an i.i.d. random series. Indeed, we find that the record rate in stationary fractional Gaussian noises is independent of the underlying memory in the time series. We will discuss this finding in more details in section 7, by searching for correlations between the records.

III.2 Record number

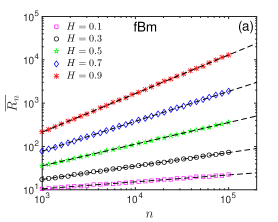

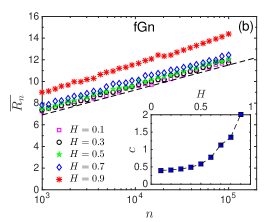

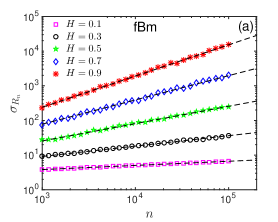

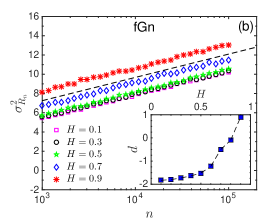

As we mentioned above, the record number is an important quantity in the record theory. Fig. 3(a) demonstrates the average record number versus time for fBm series with five different Hurst exponents. We find a power-law behavior (dashed lines) of the form of . However, a completely different behavior is observed for fGn series. Fig. 3(b) shows semi-logarithmic plots of for fGn series with various Hurst exponents. We find a logarithmic increase as , where depends on the Hurst exponent, as indicated in the inset of Fig. 3(b). Clearly, the mean record number for a non-stationary fBm series grows much faster than that for a stationary fGn series. Further, we also search for the fluctuations about these average values. In Fig. 4, we plotted the standard deviation of the record number against time for fBm and fGn series with different Hurst exponents. We find again a power-law form of for fBm, and a logarithmic form of for fGn series. Here, is also dependent on the Hurst exponent, as shown in the inset of Fig. 4(b).

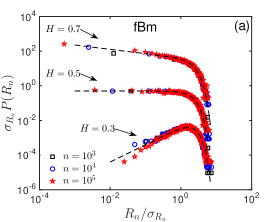

To find out more about the nature of the record number fluctuations, it is helpful to take into account the record number distributions . In Fig. 5(a), we plotted the normalized probability distributions of the record number for fBm series of sizes , , and , and with three different Hurst exponents of , , and . Due to better visibility, the curves in Fig. 5(a) are shifted vertically by a factor of and for and , respectively. The dashed lines show fitted functions of the form of

| (8) |

where , , and is positive/zero/negative for Hurst exponents smaller than/equal to/larger than . We observe that approaches an asymmetric Gaussian form, as , and tends to a power-law functional form, as . Therefore, in non-stationary fractal processes, increasing broadens the record number distribution. Note that for , we find the half-Gaussian distribution of Eq. 7, as expected.

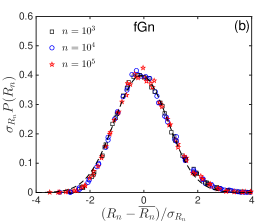

Fig. 5(b) shows the record number distributions for stationary fGn series, with different sizes and Hurst exponents. The curves are normalized to zero mean and unit standard deviation. As it can be seen, all curves collapse into a universal Gaussian function of the form of

| (9) |

where and . This indicates that the record number distribution of stationary fractal time series is the same as that of an i.i.d random series of Eq. 6, and is completely independent of the memory aspects of the original process. We note here that for non-stationary fractal series, the width of the record number distribution increases as the Hurst exponent increases, in contrast with the case of stationary fGn series. This indicates that for high values of the Hurst exponent in an fBm series, the record parameters can largely fluctuate about their mean values, and thus we should be careful when we talk about such average values.

III.3 Record ages

We are also interested in questions like “how long should one wait for the occurrence of the next record?”. In this respect, we calculate the age distribution of the records for both fGn and fBm series with various Hurst exponents. Fig. 6(a) represents such distributions for fBm series with three Hurst exponents of , , and . The dashed lines exhibit power-laws of the form of

| (10) |

with . In the case of fGn series, we find again a universal power-law behavior of the form of (dashed line in Fig. 6(b)) for different Hurst exponents. It is interesting to note here that any questions about the average of the record age does not make sense, since due to the power-law behavior of the age distribution with exponents between and , diverges as .

III.4 Correlation in records

At the end, we are interested in correlations between the individual record events. To quantify the correlation properties between two records at time steps and , we introduce a correlation index, , as follows:

| (11) |

where . Due to the binary property of the record indicator, , and one simply gets . On the other hand, the joint probability of the occurrence of two record events can be written, in terms of the record indicator , as

| (12) |

Then, by using Eq. 3, we have

| (13) |

Hence, for an independent sequence with , we obtain . From now on, we concentrate our attention only on the correlation between two successive points, i.e., . According to the power-law form of the record rate, we get . Thus, one can assume that for . By using the relationship , we have

| (14) |

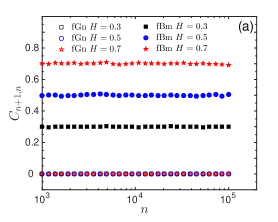

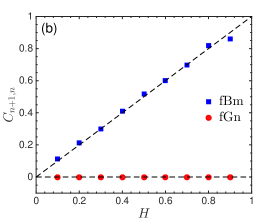

For , we can also neglect in comparison with , and then finally we get . We know that for a fBm process, the conditional probability equals to the probability of the occurrence of a positive increment, and equals to . Thus, we find which is independent of . To check this, we plotted in Fig. 7(a) the time behavior of the correlation index, , for fractal time series with different Hurst exponents. We observe that for fBm series, , and is approximately independent of time for , as expected. Also, for stationary fGn series, we find , independent of the Hurst exponent. This indicates that the record events in stationary fractal time series are uncorrelated for large . For better understanding, we also plotted in Fig. 7(b), the correlation index at a fixed time step , for various Hurst exponents. As it can be seen, we find a linear behavior of versus for fBm series, in perfect agreement with our analytical result. Interestingly, for fGn series with various Hurst exponents, the record dynamics is uncorrelated and independent of the Hurst exponent. We find an important result: the record statistics of stationary fractal time series are uncorrelated, even with the presence of long-range linear correlations in the original process. In fact, this feature influences all aspects of the record dynamics, causing the observed universal behavior in the records statistics, mentioned above.

IV conclusion

In conclusion, we investigated the record statistics of stationary and non-stationary fractal time series, i.e., fractional Gaussian noises and fractional Brownian motions, respectively. By doing extensive numerical calculations, we found a power-law functional form for many record features such as the record rates and the age distributions. We have also investigated other dynamical characteristics of the records, such as correlation between the record events, and found that the record dynamics are uncorrelated in stationary fractal time series, in spite of the existence of long-range linear correlation in the original series. Further, we have shown that for stationary fractal time series, a universal behavior is observed in all aspects of the record dynamics, independent of the memory inherited in the process. On the other hand, for non-stationary fractal processes, the record dynamics strongly depends on the Hurst exponent. This deviation from the results of the stationary case is increased by increasing the Hurst exponent, which can be considered as the degree of non-stationarity in such fractal series. Finally, we have demonstrated that the memory in fractal time series can affect the record dynamics, only if the existing correlation can produce non-stationarity in such fractal processes.

Acknowledgements.

The support from Persian Gulf University Research Council is kindly acknowledged.References

- Dean and Majumdar (2001) D. S. Dean and S. N. Majumdar, Phys. Rev. E 64, 046121 (2001).

- Majumdar and Krapivsky (2002) S. N. Majumdar and P. L. Krapivsky, Phys. Rev. E 65, 036127 (2002).

- Burkhardt et al. (2007) T. W. Burkhardt, G. Györgyi, N. R. Moloney, and Z. Racz, Phys. Rev. E 76, 041119 (2007).

- Sabhapandit and Majumdar (2007) S. Sabhapandit and S. N. Majumdar, Phys. Rev. Lett. 98, 140201 (2007).

- Györgyi et al. (2008) G. Györgyi, N. R. Moloney, K. Ozogany, and Z. Racz, Phys. Rev. Lett. 100 (2008).

- Majumdar and Bray (2001) S. N. Majumdar and A. J. Bray, Phys. Rev. Lett. 86, 3700 (2001).

- Redner (2001) S. Redner, A Guide to First-Passage Processes (Cambridge University Press, Cambridge, 2001).

- Leadbetter et al. (1982) M. R. Leadbetter, G. Lindgren, and H. Rootzen, Extremes and Related Properties of Random Sequences and Processes (Springer-Verlag, New York, 1982).

- Majumdar (1999) S. N. Majumdar, Curr. Sci. 77, 370 (1999).

- Manshour et al. (2016) P. Manshour, M. Anvari, N. Reinke, M. Sahimi, and M. R. R. Tabar, Sci. Rep. 6, 27452 (2016).

- Bunde et al. (2003) A. Bunde, J. F. Eichner, S. Havlin, and J. W. Kantelhardt, Physica A 330, 1 (2003).

- Eichner et al. (2006) J. F. Eichner, J. W. Kantelhardt, A. Bunde, and S. Havlin, Phys. Rev. E 73 (2006).

- Chandler (1952) K. N. Chandler, J. R. Statist. Soc. B 14, 220 (1952).

- Arnold et al. (1998) B. C. Arnold, N. Balakrishnan, and H. N. Nagaraja, Records, 1st ed. (Wiley-Interscience, New York, 1998).

- Nevzorov (1988) V. B. Nevzorov, Theory Probab. Appl. 32, 201 (1988).

- Sibani and Littlewood (1993) P. Sibani and P. B. Littlewood, Phys. Rev. Lett. 71, 1482 (1993).

- Sibani et al. (2006) P. Sibani, G. F. Rodriguez, and G. G. Kenning, Phys. Rev. B 74, 224407 (2006).

- Orr (2005) H. A. Orr, Nat. Rev. Genet. 6, 119 (2005).

- Alessandro et al. (1990) B. Alessandro, C. Beatrice, G. Bertotti, and A. Montorsi, J. Appl. Phys. 68, 2901 (1990).

- Doussal and Wiese (2009) P. L. Doussal and K. J. Wiese, Phys. Rev. E 79 (2009).

- Wergen et al. (2012) G. Wergen, S. N. Majumdar, and G. Schehr, Phys. Rev. E 86 (2012).

- Wergen et al. (2011a) G. Wergen, M. Bogner, and J. Krug, Phys. Rev. E 83 (2011a).

- Wergen and Krug (2010) G. Wergen and J. Krug, EPL (Europhysics Letters) 92, 30008 (2010).

- Newman et al. (2010) W. I. Newman, B. D. Malamud, and D. L. Turcotte, Phys. Rev. E 82 (2010).

- Godréche and Luck (2008) C. Godréche and J. M. Luck, J. Stat. Mech. Theor. Exp. 2008, P11006 (2008).

- Oliveira et al. (2005) L. P. Oliveira, H. J. Jensen, M. Nicodemi, and P. Sibani, Phys. Rev. B 71 (2005).

- Richardson et al. (2010) T. O. Richardson, E. J. H. Robinson, K. Christensen, H. J. Jensen, N. R. Franks, and A. B. Sendova-Franks, PLoS ONE 5, 1 (2010).

- Vogel et al. (2001) R. M. Vogel, A. Zafirakou-Koulouris, and N. C. Matalas, Water Resour. Res. 37, 1723 (2001).

- Gembris et al. (2002) D. Gembris, J. G. Taylor, and D. Suter, Nature 417, 506 (2002).

- Gembris et al. (2007) D. Gembris, J. G. Taylor, and D. Suter, J. Appl. Stat. 34, 529 (2007).

- Davidsen et al. (2006) J. Davidsen, P. Grassberger, and M. Paczuski, Geophys. Res. Lett. 33, L11304 (2006).

- Davidsen et al. (2008) J. Davidsen, P. Grassberger, and M. Paczuski, Phys. Rev. E 77 (2008).

- Franke et al. (2011) J. Franke, A. Klözer, J. A. G. M. de Visser, and J. Krug, PLoS Comput. Biol. 7, 1 (2011).

- Wergen (2013) G. Wergen, J. Phys. A 46, 223001 (2013).

- Krug (2007) J. Krug, J. Stat. Mech. Theor. Exp. 2007, P07001 (2007).

- Eliazar and Klafter (2009) I. Eliazar and J. Klafter, Phys. Rev. E 80 (2009).

- Wergen et al. (2011b) G. Wergen, J. Franke, and J. Krug, J. Stat. Phys. 144, 1206 (2011b).

- Franke et al. (2012) J. Franke, G. Wergen, and J. Krug, Phys. Rev. Lett. 108 (2012).

- Majumdar and Ziff (2008) S. N. Majumdar and R. M. Ziff, Phys. Rev. Lett. 101 (2008).

- Sabhapandit (2011) S. Sabhapandit, EPL (Europhysics Letters) 94, 20003 (2011).

- Kolmogorov (1940) A. N. Kolmogorov, Dokl. Acad. Sci. USSR 26, 115 (1940).

- Mandelbrot and Ness (1968) B. B. Mandelbrot and J. W. V. Ness, SIAM Review 10, 422 (1968).

- Robinson (2003) P. M. Robinson, ed., Time Series with Long Memory (Oxford University Press, Oxford, 2003).

- Embrechts and Maejima (2002) P. Embrechts and M. Maejima, Self-similar Processes (Princeton University Press, Princeton, 2002).

- Mandelbrot (2002) B. Mandelbrot, Gaussian Self-Affinity and Fractals (Springer-Verlag, New York, 2002).

- Alvarez-Lacalle et al. (2006) E. Alvarez-Lacalle, B. Dorow, J.-P. Eckmann, and E. Moses, Proc. Natl. Acad. Sci. USA 103, 7956 (2006).

- Varotsos and Kirk-Davidoff (2006) C. Varotsos and D. Kirk-Davidoff, Atmos. Chem. Phys. 6, 4093 (2006).

- Karagiannis et al. (2004) T. Karagiannis, M. Molle, and M. Faloutsos, IEEE Internet Comput. 8, 57 (2004).

- Manshour (2015) P. Manshour, Chaos 25, 103105 (2015).

- Hurst (1951) H. E. Hurst, Trans. Amer. Soc. Civil Eng. 116, 770 (1951).

- Abramowitz and Stegun (1972) M. Abramowitz and I. Stegun, Handbook of Mathematical Functions (Dover Publishers, New York, 1972).

- Makse et al. (1996) H. A. Makse, S. Havlin, M. Schwartz, and H. E. Stanley, Phys. Rev. E 53, 5445 (1996).

- Krug et al. (1997) J. Krug, H. Kallabis, S. N. Majumdar, S. J. Cornell, A. J. Bray, and C. Sire, Phys. Rev. E 56, 2702 (1997).