Nonparametric inference of gradual changes in the jump behaviour of time-continuous processes

Michael Hoffmann111Ruhr-Universität Bochum,

Fakultät für Mathematik, 44780 Bochum, Germany.

E-mail: holger.dette@rub.de, michael.hoffmann@rub.de , Mathias Vetter222Christian-Albrechts-Universität zu Kiel,

Mathematisches Seminar, Ludewig-Meyn-Str. 4, 24118 Kiel, Germany.

E-mail: vetter@math.uni-kiel.de and Holger Dette11footnotemark: 1 ,

Ruhr-Universität Bochum & Christian-Albrechts-Universität zu Kiel

Abstract

In applications the properties of a stochastic feature often change gradually rather than abruptly, that is: after a constant phase for some time they slowly start to vary. In this paper we discuss statistical inference for the detection and the localisation of gradual changes in the jump characteristic of a discretely observed Ito semimartingale. We propose a new measure of time variation for the jump behaviour of the process. The statistical uncertainty of a corresponding estimate is analyzed by deriving new results on the weak convergence of a sequential empirical tail integral process and a corresponding multiplier bootstrap procedure.

Stochastic processes in continuous time are widely used in the applied sciences nowadays, as they allow for a flexible modeling of the evolution of various real-life phenomena over time. Speaking of mathematical finance, of particular interest is the family of semimartingales, which is theoretically appealing as it satisfies a certain condition on the absence of arbitrage in financial markets and yet is rich enough to reproduce stylized facts from empirical finance such as volatility clustering, leverage effects or jumps. For this reason, the development of statistical tools modeled by discretely observed Itō semimartingales has been a major topic over the last years, both regarding the estimation of crucial quantities used for model calibration purposes and with a view on tests to check whether a certain model fits the data well.

For a detailed overview of the state of the art we refer to the recent monographs by Jacod and Protter, (2012) and Aït-Sahalia and Jacod, (2014).

These statistical tools typically differ highly, depending on the quantities of interest. When the focus is on the volatility, most concepts are essentially concerned with discrete observations of the continuous martingale part. In this case one is naturally close to the Gaussian framework, and so a lot of classical concepts from standard parametric statistics turn out to be powerful methods. The situation is different with a view on the jump behaviour of the process, mainly for two reasons: On one hand there is much more flexibility in the choice of the jump measure than there is regarding the diffusive part. On the other hand even if one restricts the model to certain parametric families the standard situation is the one of -stable processes, , for which the mathematical analysis is quite difficult, at least in comparison to Brownian motion. To mention recent work besides the afore-mentioned monographs, see for example Nickl et al., (2016) and Hoffmann and Vetter, (2017) on the estimation of the jump distribution function of a Lévy process or Todorov, (2015) on the estimation of the jump activity index from high-frequency observations.

In the following, we are interested in the evolution of the jump behaviour over time

in a completely non-parametric setting where we assume only stuctural conditions on the characteristic triplet of the underlying Itō semimartingale. To be precise, let be an Itō semimartingale with a decomposition

(1.1)

where is a standard Brownian motion, is a Poisson random measure on , and the predictable compensator satisfies . The main quantity of interest is the kernel which controls the number and the size of the jumps around time .

In Bücher et al., (2017) the authors are interested in the detection of abrupt changes in the jump measure of . Based on high-frequency observations , , with they construct a test for a constant against the alternative

Here the authors face a similar problem as in the classical situation of changes in the mean of a time series, namely that the “change point” can only be defined relative to the length of the covered time horizon which needs to tend to infinity. In general, this problem cannot be avoided as there are only finitely many large jumps on every compact interval, so consistent estimators for the jump measure have to be constructed over the entire positive half-line.

There are other types of changes in the jump behaviour of a process than just abrupt ones, though. In the sequel, we will deal with gradual (smooth, continuous) changes of and discuss how and how well they can be detected. A similar problem has recently been addressed in Todorov, (2016) who constructs a test for changes in the activity index. Since this index is determined by the infinitely many small jumps around zero, such a test can be constructed over a day. On the other hand, estimation of an index is obviously a simpler problem than estimation of an entire measure.

While the problem of detecting abrupt changes has been discussed intensively in a time series context

(see Aue and Horváth, (2013) and Jandhyala et al., (2013) for a review of the literature),

detecting gradual changes is a much harder problem and the methodology

is not so well developed. Most authors consider nonparametric location or parametric models with independently distributed observations,

and we refer to Bissell, (1984), Gan, (1991), Siegmund and Zhang, (1994), Hus̆ková, (1999), Hus̆ková and Steinebach, (2002) and Mallik et al., (2013) among others.

See also Aue and Steinebach, (2002) for some results in a time series model and Vogt and Dette, (2015) who developed a

nonparametric method for the analysis of smooth changes in locally stationary time series.

The present paper is devoted to the development of nonparametric inference for gradual changes in the jump properties

of a discretely observed Itō semimartingale. In Section 2 we introduce the formal setup as well as a measure of time variation which is used to identify changes in the jump characteristic later on.

Section 3 is concerned with weak convergence of an estimator for this measure, and as a consequence we also obtain weak convergence of related statistics which can be used for testing for a gradual change and for localizing the first change point. As the limiting distribution depends in a complicated way on the unknown jump characteristic, a bootstrap procedure is discussed which can be used for a data driven choice of a regularization parameter of the change point estimator and for approximating quantiles of the test statistics. Section 4 contains the formal derivation of an

estimator of the change point and a test for gradual changes. Finally, a brief simulation study can be found in Section 5, while

all proofs are relegated to Section 6.

2 Preliminaries and a measure of gradual changes

In the sequel let be an Itō semimartingale of the form (1.1) with characteristic triplet for each . We are interested in investigating gradual changes in the evolution of the jump behaviour and we

assume throughout this paper that there is a driving law behind this evolution which is common for all . Formally, we introduce a transition kernel from into such that

(2.1)

for . This transition kernel shall be an element of the set to be defined below. Throughout the paper denotes the trace -algebra of a set with respect to the Borel -algebra.

Assumption 2.1.

Let denote the set of all transition kernels from into such that

(1)

For each the measure does not charge .

(2)

The function is bounded on the interval .

(3)

If

denotes one-sided intervals and

then for every there exists a finite set , such that the function is continuous on .

(4)

For each the measure is absolutely continuous with respect to the Lebesgue measure with density ,

where the measurable function

is continuously differentiable with respect to for fixed . The function and its derivative will be denoted by

and , respectively. Furthermore, we assume for each that

where .

These assumptions are all rather mild. For Lebesgue almost every , the integral needs to be finite by properties of the jump compensator, so part (2) just serves as a condition on uniform boundedness over time. Part (3) essentially says that for each only finitely many discontinuous changes of the jump measure are allowed.

Finally, note that the existence of a density as in (4) is a standard condition when estimating a measure in a non-parametric framework.

In order to investigate gradual changes in the jump behaviour of the underlying process we

follow Vogt and Dette, (2015) and

consider a measure of time variation for the jump behaviour which is defined by

(2.2)

where and

(2.3)

Here and throughout this paper we use the convention .

The time varying measure (2.2) will be the main theoretical tool for our inference of gradual changes in the jump behaviour

of the process (1.1). Our analysis will be based on the following observation: Due to the jump behaviour corresponding to the first observations for some does not vary if and only if the kernel is Lebesgue almost everywhere constant on the interval . In this case we have for all and , since is constant on for each . If on the other hand for all and , then

for each and fixed . Therefore by the fundamental theorem of calculus and Assumption 2.1(3) for each fixed we have for every . As a consequence

(2.4)

holds for every and each outside the Lebesgue null set . Due to Assumption 2.1(2) and dominated convergence is left-continuous for positive and right-continuous for negative . The same holds for for each fixed . Consequently (2.4) holds for every and each outside the Lebesgue null set . Thus by the uniqueness theorem for measures the kernel is on Lebesgue almost everywhere equal to the Lévy measure defined by .

In practice we restrict ourselves to which are bounded away from zero, as typically as , at least if we deviate from the (simple) case of finite activity jumps. Below we discuss two standard applications of we have in mind.

(1)

(test for a gradual change) If one defines

(2.5)

for some pre-specified constant , one can characterize the existence of a change point as follows: There exists a gradual change in the behaviour of the jumps larger than of the process (1.1) if and only if

Moreover for the analysis of gradual changes it is equivalent to consider

(2.6)

because the first time points where and deviate from zero, if existent, coincide and this point is characteristic for a gradual change as we have seen previously. In this paper we consider only, since due to its monotonicity it simplifies several steps in the proofs and our notation.

In Section 4.1 we construct a consistent estimator, say , of .

The test for gradual changes in the behaviour of

the jumps larger than of the process (1.1) rejects the null hypothesis for large values of .

Quantiles for this test will be derived by a multiplier bootstrap (see Section 4.2 for details).

(2)

(estimating the gradual change point) In Section 4.1 we construct an estimator for the first point where the jump behaviour changes (gradually). For this purpose we also use the time varying measure (2.2) and define

(2.7)

where we set . We call

the change point of the jumps larger than of the underlying process (1.1).

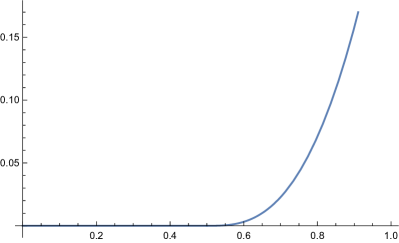

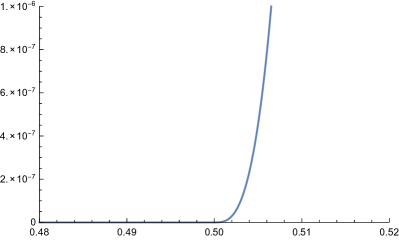

Figure 1: The function for the transition kernel (2.8), where . The “true” change point is located at .

A typical example is displayed in Figure 1. Here we show the function defined in (2.6) for , where the transition kernel is given by

(2.8)

From the right panel it is clearly visible that the function is positive for all , which identifies as the change point. Additionally we illustrate the previously introduced quantities in two further examples.

Example 2.2.

(abrupt changes)

The classical change point problem, where the jump behaviour of the underlying process is constant on two intervals, is contained in our analysis.

To be precise, assume that and that and are Lévy measures

such that the transition kernel satisfies

(2.9)

If each is absolutely continuous with respect to the Lebesgue measure and has a density which is continuously differentiable

at any point , satisfying

for every , then the kernel satisfies Assumption 2.1.

For a Lévy measure on and let . If is of the form (2.9) and is

chosen sufficiently small such that there exists a with and

then we have for all with

and consequently for each . On the other hand, if and we have

and obtain

where . For a similar calculation yields

which gives

It follows that

the quantity defined (2.7) is given by

, because for we have

(2.10)

Example 2.3.

(Locally symmetric -stable jump behaviour) A Lévy process is symmetric -stable for some if and only if its Brownian part vanishes and its Lévy measure has a Lebesgue density of the

form with [see, for instance, Chapter 3 in Sato, (1999)].

In this sense we say that an Itō semimartingale with decomposition (1.1) satisfying

(2.1) has locally symmetric

-stable jump behaviour, if the corresponding transition kernel is given by

(2.11)

for and . Here the functions and

are continuous outside a finite set, is bounded and is bounded away from . In Section 6 we show that a kernel of the form (2.11) satisfies Assumption 2.1.

Now, let with

(2.12)

for all with , . To model the continuous change after we assume that is contained in an open interval and that there exists a real analytic function

and an affine linear function

such that at least one of the functions , is non-constant as well as

(2.13)

for all . Then we also show in Section 6 that the quantity defined in (2.7) is given by for every

(see Section 6.10).

We conclude this section with the main assumption for the characteristics of an Itō semimartingale

which will be used throughout this paper.

Assumption 2.4.

For each let denote an Itō semimartingale of the form (1.1) with characteristics defined on the probability space that satisfies

(a)

There exists a such that

holds for all and all .

(b)

The drift and the volatility are predictable processes and

satisfy

for some , with .

(c)

The observation scheme satisfies

(2.14)

for .

Remark 2.5.

Assumption 2.4(a) corresponds to the typical finding in classical change point analysis that a change point can only be defined relative to the length of the data set which in our case is the covered time horizon . However, this assumption is no restriction in applications since a statistical method is always applied to a data set with a fixed length. Assumption 2.4(b) is very mild as it requires only a bound on the moments of drift and volatility (note that as ). Typical for high frequency statistics is condition (2.14), which is used to control the bias arising from the presence of the continuous part of the underlying process. Moreover, if and are deterministic and bounded functions in and , the process has independent increments and assumption (2.14) can be weakened to

3 Weak convergence

In order to estimate the measure of time variation introduced in (2.2) we use

the sequential empirical tail integral process defined by

where , , and .

The process counts the number of increments that fall into , as these are likely to be caused by a jump with the corresponding size, and will be the basic tool for estimating the measure of time variation defined in (2.2).

An estimate is given by

(3.1)

where the set is defined in (2.3). The statistic has been considered by

Figueroa-López, (2008) for observations of a Lévy process , so without a time-varying jump behaviour. In this case the author

shows that is in fact an -consistent estimator for the tail integral .

The following theorem provides a generalization of this statement. In particular, it provides the weak convergence of the sequential empirical tail integral

(3.2)

Throughout this paper we use the notation

and denotes the symmetric difference of two sets .

Theorem 3.1.

If Assumption 2.4 holds, then the process defined in (3.2) satisfies in for any , where

is a tight mean zero Gaussian process with covariance function

The sample paths of are almost surely uniformly continuous with respect to the semimetric

defined for without loss of generality. Moreover, the space is totally bounded.

Recall the definition of the measure of time variation for the jump behaviour defined in (2.2) and the definition of the set in (2.3). For

consider the functional defined by

(3.3)

As the mapping is Lipschitz continuous.

Consequently, is a tight mean zero

Gaussian process in with covariance structure

(3.4)

From the continuous mapping theorem we obtain weak convergence of the process

(3.5)

Theorem 3.2.

If Assumption 2.4 is satisfied, then the process defined in (3.5) satisfies in for any , where is a tight mean zero Gaussian process with covariance function (3).

For the statistical change-point inference proposed in the following section we require the quantiles of

functionals of the limiting distribution in Theorem 3.2. This distribution depends in a complicated way on the unknown underlying kernel

and, as a consequence, corresponding quantiles are difficult to estimate.

A typical approach to problems of this type are resampling methods.

One option is to use suitable estimates for drift, volatility and the unknown kernel to draw independent samples of an Itō semimartingale.

However, such a method is computationally expensive since one has to generate independent Itō

semimartingales for each stage within the bootstrap algorithm. Therefore

we propose an alternative bootstrap method based on multipliers.

For this resampling method one only needs to generate i.i.d. random variables with mean zero and variance one.

To be precise let and denote random variables defined on probability spaces

and

, respectively, and consider a random element

on the product space

which maps into a metric space, say . Moreover, let be a tight, Borel measurable -valued random variable.

Following Kosorok, (2008) we call weakly convergent to conditional on in probability if the following

two conditions are satisfied

(a)

(b)

for all

Here, denotes the conditional expectation with respect to given ,

whereas is the space of all real-valued Lipschitz continuous functions on with sup-norm and Lipschitz constant . Moreover, and denote a minimal measurable majorant and a maximal measurable minorant with respect to , , respectively. Throughout this paper we denote this type of convergence by .

In the following we will work with a multiplier bootstrap version of the process , that is

(3.6)

where are independent and identically distributed random variables with mean and variance and

.

The following theorem establishes conditional weak convergence of this bootstrap approximation for the sequential empirical tail integral process .

Theorem 3.3.

If Assumption 2.4 is satisfied and is a sequence of independent and identically distributed random variables with mean and variance , defined on a distinct probability space as described above,

then the process defined in (3.6) satisfies

in for any , where denotes the limiting process of Theorem 3.1.

Theorem 3.3 suggests to consider the following counterparts of the process defined in (3.5)

(3.7)

The following result establishes consistency of . Its proof

is a consequence of Proposition 10.7 in Kosorok, (2008), because we have and

with the Lipschitz continuous map defined in (3.3).

Theorem 3.4.

If Assumption 2.4 holds and is a sequence of independent and identically distributed random variables with mean and variance defined on a distinct probability space, then the process defined in (3) satisfies

in for any , where the

process is defined in Theorem 3.2.

4 Statistical inference for gradual changes

As we have seen in Section 2 the quantity defined in (2.6) is an indicator for a change

in the behaviour of the jumps larger than on . Therefore we use the estimate of the measure of time variation

defined in (3.1)

to construct both a test for the existence and an estimator for the location of a gradual change. We begin with the problem of estimating the

point of such a gradual change in the jump behaviour. The discussion of corresponding tests

will be referred to Section 4.2.

4.1 Localizing change points

Recall the definition

and the definition

of the change point in (2.7). By Theorem 3.2 the process from (3.1)

is a consistent estimator of . Therefore we set

and an application of the continuous mapping theorem and Theorem 3.2 yields the following result.

Corollary 4.1.

If Assumption 2.4 is satisfied, then in , where is

the tight process in defined by

(4.1)

with the centered Gaussian process defined in Theorem 3.2.

Intuitively, the estimation of

becomes more difficult the flatter the curve is at .

Following Vogt and Dette, (2015), we describe the curvature of by a local polynomial behaviour of the function

for values . More precisely, we assume throughout this section

that and that there exist constants such that admits an expansion of the form

(4.2)

for all , where the remainder term satisfies

for some .

The construction of an estimator for utilizes the fact

that, by Theorem 3.2, in probability for any .

We now consider the statistic

for a deterministic sequence . From the previous discussion we expect

in probability if the threshold level is chosen appropriately. Consequently, we define the estimator for the change point by

(4.3)

Note that the estimate depends on the threshold and we make this dependence visible in our notation whenever it is necessary. Our first result establishes consistency of the estimator under rather mild assumptions on the sequence .

Theorem 4.2.

If Assumption 2.4 is satisfied, , and (4.2) holds

for some , then

for any sequence with .

Theorem 4.2 makes the heuristic argument of the previous paragraph more precise. A lower

degree of smoothness in yields a better rate of convergence of the estimator.

Moreover, the slower the threshold level converges to infinity the better the rate of convergence.

We will explain below how to choose this sequence to control the probability of over- and underestimation

by using bootstrap methods.

Before that we investigate the mean squared error

of the estimator . Recall the definition of in (3.5) and define

(4.4)

which measures the absolute distance between the estimator and the true value . For a sequence with we decompose the MSE into

which can be considered as the MSE due to small and large estimation error. With these notations the following theorem gives upper and lower bounds for the mean squared error.

Theorem 4.3.

Suppose that , Assumption 2.4 and (4.2) are satisfied. Then for any

sequence with we have

(4.5)

for sufficiently large, where the constants and can be chosen as

(4.6)

for an arbitrary .

In the remaining part of this section we discuss the choice of the regularizing sequence for the estimator . Our main goal here is to control the probability of over- and underestimation of the change point .

For this purpose let be a preliminary consistent estimator of . For example, if (4.2) holds for some , one can take for a sequence satisfying the assumptions of Theorem 4.2.

In the sequel, let be some large number and let denote independent vectors of i.i.d. random variables, , with mean zero and variance one, which are defined on a probability space distinct to the one generating the data . We denote by or the particular bootstrap statistics calculated with respect to the data and the bootstrap multipliers from the -th iteration, where

(4.7)

for . With these notations and for , and we define the following empirical distribution function

and denote by

its pseudoinverse.

Given a confidence level we consider the threshold

(4.8)

This choice is optimal in the sense of the following two theorems.

Theorem 4.4.

Let , and assume that Assumption 2.4 is satisfied for some with . Suppose further that there exists some with

(4.9)

Then the probability for underestimation of the change point can be controlled by

(4.10)

Theorem 4.5.

Let , . Assume that Assumption 2.4 is satisfied for some with and that (4.2) holds for some . Furthermore suppose that there exist a constant with and a satisfying (4.9).

Additionally let the bootstrap multipliers be either bounded in absolute value or standard normal distributed. Then for each and all sequences with and with such that

1.

2.

we have

(4.11)

where , while .

Obviously, Theorem 4.5 only gives a meaningful result since can be guaranteed. Its proof shows that

a sufficient condition for this property is given by

(4.12)

for arbitrary . Moreover, (4.12) follows from without any further conditions. This explains why the threshold needs to be introduced, and it seems that the statement of (4.12) can only be guaranteed under very restrictive assumptions in the case .

Finally we illustrate that the polynomial behaviour introduced in (4.2) is satisfied in the situations of Example 2.2 and Example 2.3.

Example 4.6.

(1)

Recall the situation of an abrupt change in the jump characteristic

considered in Example 2.2. In this case it follows from (2.10) that

whenever . Therefore assumption (4.2) is satisfied with

. Moreover, the transition kernel given by

(2.9) satisfies

assumption (4.9) if and is chosen small enough.

(2)

In the situation discussed in Example 2.3 let for and . Then we have for any

where for and

denotes the -th partial derivative of with respect to at , which is a bounded function on any . Furthermore, for every there is a such that

(4.13)

on with for some , so (4.2) is satisfied. A proof of this result can be found in Section 6 as well. Again, (4.9) holds also.

4.2 Testing for a gradual change

In this section we want to derive test procedures for the existence of a gradual change in the data. In order to formulate suitable hypotheses for a gradual change point recall

the definition of the measure of time variation for the jump behaviour in

(2.2) and define for , and the quantities

We also assume that Assumption 2.4 is satisfied and we are interested in the following

hypotheses

(4.14)

which refer to the global behaviour of the tail integral. If one is interested

in the gradual change in the tail integral for a fixed one could consider

the hypotheses

(4.15)

Remark 4.7.

Note that the function in (2.2) is uniformly continuous in , uniformly in , that is for any there exists a such that

holds for each and all pairs with maximum distance .

Therefore the function is uniformly continuous on as well, and as a consequence is continuous on . Thus the alternative holds if and only if the point defined in (2.7) satisfies .

The null hypothesis in (4.14) and (4.15) will be rejected for large values of the corresponding estimators

for

and , respectively. The critical values

are obtained by the multiplier bootstrap introduced in Section 3.

For this purpose we denote by , , i.i.d. random variables

with mean zero and variance one. As before, we assume that these random variables are defined on a probability space distinct to the one generating the data .

We denote by and the statistics in (3.6) and (3) calculated from and the -th bootstrap multipliers .

For given , and a given level , we

propose to reject in favor of , if

(4.16)

where denotes the -quantile of the sample with defined in (4.7).

Note that under the null hypothesis it follows from the definition of the process in (3.5) that , which by Theorem 3.2 and the continuous mapping theorem converges weakly to , defined in (4.1). The bootstrap procedure mimics this behaviour.

Similarly, the hypothesis

is rejected in favor of if

(4.17)

where denotes the -quantile of the sample , and

Remark 4.8.

Since has to be chosen for an application of the test (4.16), one can only detect changes in the jumps larger than .

From a practical point of view this is not a severe restriction as in most applications only the larger jumps are of interest. If one is interested in the entire jump measure, however, its estimation is rather difficult, at least in the presence of a diffusion component, as provides a natural bound to disentangle jumps from volatility. We refer to Nickl et al., (2016) and Hoffmann and Vetter, (2017) for details in the case of Lévy processes.

The following two results show that the tests (4.16) and (4.17) are consistent asymptotic level tests.

Proposition 4.9.

Under and , respectively, the tests (4.16) and (4.17) have

asymptotic level . More precisely,

if there exist , with , and

if there exists a with .

Proposition 4.10.

The tests (4.16) and (4.17) are consistent in the following sense.

Under we have for all

(4.18)

Under , we have for all

5 Finite-sample properties

In this section we present the results of a simulation study, investigating the finite-sample properties of the new methodology for inference of gradual changes in the jump behaviour. The design of this study is as follows.

•

Each procedure is run times for any depicted combination of the involved constants. Furthermore in each run the number of bootstrap replications is .

•

The estimators are calculated for data points with the combination of frequencies , , resulting in the choices , , for the number of trading days. For computational reasons, if not declared otherwise, we choose for each run of the tests (4.16) and (4.17) with frequencies , , corresponding to the number of trading days , , .

•

We consider the following model for the transition kernel similar to Example 2.3:

(5.1)

with

(5.2)

for some , and . In order to simulate pure jump Itō semimartingale data according to such a gradual change we sample times more frequently and use a straight-forward modification of Algorithm 6.13 in Cont and Tankov, (2004) to generate the increments for of a -stable pure jump Lévy subordinator with characteristic exponent

where . The resulting data vector is then given by

for .

•

In order to investigate the influence of a continuous component within the underlying Itō semimartingale on the performance of our procedure we either use the plain data vector or , where .

•

For computational reasons the supremum of the tail parameter over in each statistic is approximated by taking the maximum over a finite grid. In the pure jump case we use , , , , , resulting in . In the case including a continuous component we consider , , , , , resulting in . In the latter case, we choose depending on since jumps of smaller size may be dominated by the Brownian component leading to a loss of efficiency of the statistical procedures.

5.1 Finite-sample properties of the estimator

We implement our estimation method as follows:

Step 1.

Choose a preliminary estimate , a probability level and a parameter .

Step 2.

Initial choice of the tuning parameter :

Evaluate (4.8) for and (with and as described above) and obtain .

Step 3.

Intermediate estimate of the change point.

Evaluate (4.3) for and obtain .

Step 4.

Final choice of the tuning parameter :

Evaluate (4.8) for and obtain .

Step 5.

Estimate .

Evaluate (4.3) for and obtain the final estimate of the change point.

Furthermore in order to measure the quality of the resulting estimates we subsequently use the mean absolute deviation to the true value , that is

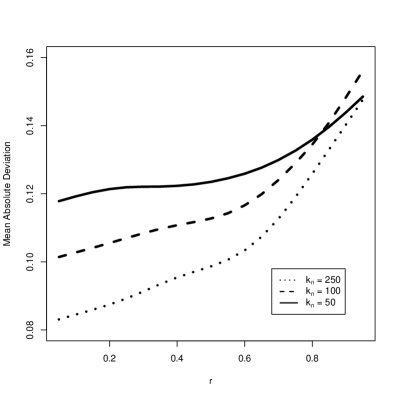

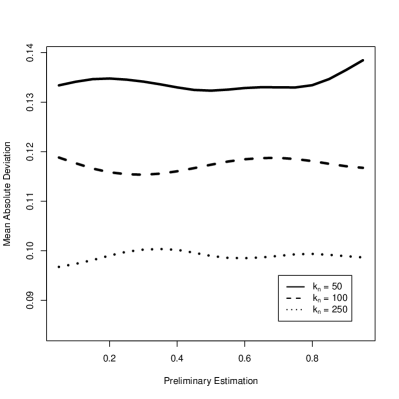

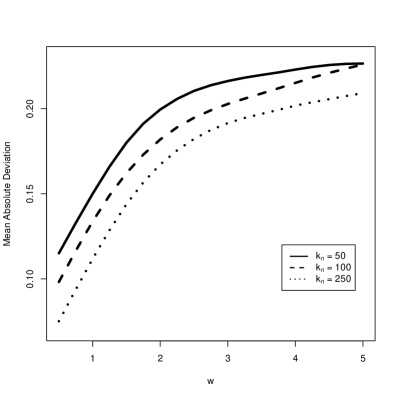

Figure 2: Mean absolute deviation for different choices of the parameter for pure jump data (left-hand side) and with an additional continuous component (right-hand side).

The results presented in Figure 2 show the mean absolute deviation for varying parameter .

Here and below we use the probability level . As a preliminary estimate we choose , whereas the true change point is located at . Moreover we simulate a linear change, that is we have in model (5.1) while the constant in

(5.2) is chosen such that the characteristic quantity for a gradual change satisfies . From the left panel it becomes apparent that in the pure jump case the mean absolute deviation is increasing in . Consequently we choose for pure jump Itō semimartingale data in all following considerations. The behaviour for data including a continuous component (right panel) is different. For the choices and it is decreasing while results in a curve which is nearly constant. Thus we choose in the following investigations whenever a continuous component is involved.

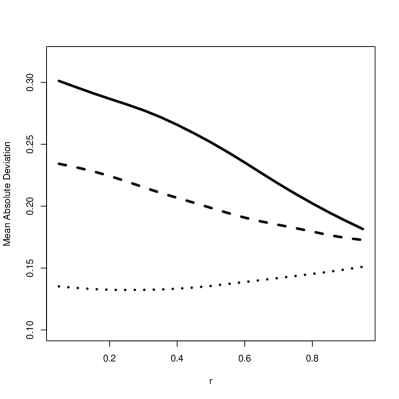

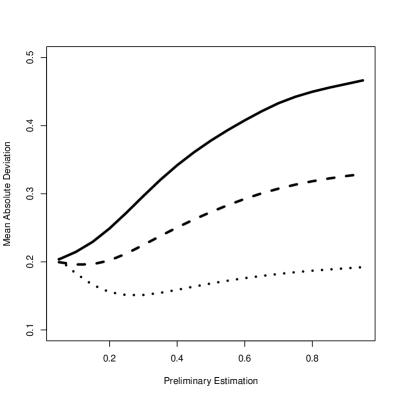

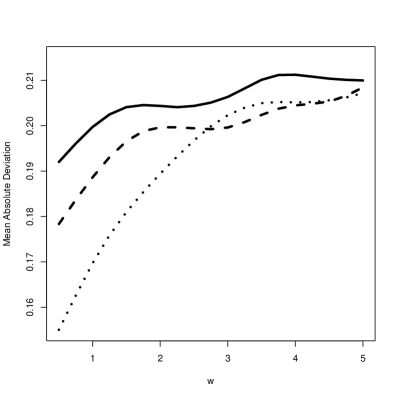

Figure 3: Mean absolute deviation of the estimator for different choices of the preliminary estimate for pure jump Itō semimartingales (left panel) and with a continuous component (right panel).

Figure 3 shows the mean absolute deviation of the estimator for different choices of the preliminary estimate . Here the change is again linear and it is located at , while the choice of the constant in (5.2) corresponds to . In the pure jump case (left-hand side) the performance of the estimator is nearly independent of the preliminary estimate. However, it can be seen from the right panel that the mean absolute deviation becomes minimal for small choices of . These findings are confirmed by a further simulation study, which is not depicted here for the sake of brevity. Our results show that large choices of the preliminary estimate yield an over-estimation, which can be explained by the fact that larger values of induce larger tuning parameters in the estimates in Steps 2–5 as well.

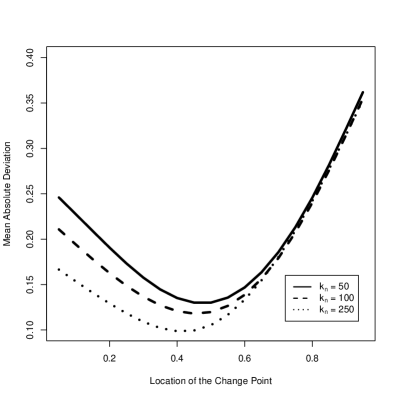

Figure 4: Mean absolute deviation for different locations of the change point for pure jump data (left-hand side) and with an additional continuous component (right-hand side).

In Figure 4 we display the performance of the estimation procedure for different locations of the change point. The change is linear

and the constant in (5.2) is chosen appropriately such that holds in each scenario. Furthermore the preliminary estimate is chosen as . The left panel suggests that a change point can be estimated best, if it is located around . This result corresponds to the findings in Figure 2 in Bücher et al., (2017), who demonstrated that under the alternative of an abrupt change the power of the classical CUSUM test is maximal for a change point around . However, from the right panel in Figure 4 it is clearly visible that, if an additional continuous component is present, large values of the change point lead to a large estimation error. This is a consequence of the shape of the model (5.1): For close to the behaviour of the underlying process is similar to the null hypothesis.

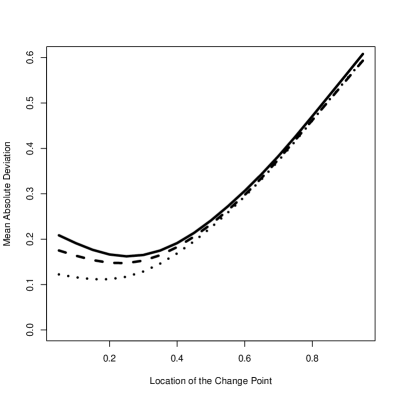

Figure 5: Mean absolute deviation of the estimator for different degrees of smoothness of the change for pure jump Itō semimartingales (left panel) and with an additional continuous component (right panel).

In Figure 5 we depict the results for different degrees of smoothness in (5.2). The true location of the change point is , while we choose for the preliminary estimate and in order to keep the results comparable the constant in (5.2) is chosen such that .

Notice that the graphic on the right-hand side has a different scale of the -axis, such that we obtain a slightly higher estimation error as well if a Brownian component and an effective drift are present. The results in Figure 5 are as expected: The higher the degree of smoothness, the more difficult a break point can be detected resulting in a larger estimation error.

5.2 Finite-sample properties of the test procedures

In order to investigate the finite-sample properties of the test procedures (4.16) and (4.17) we choose a level of significance in each of the following simulations. Table 1 and 2 contain the relative frequencies of rejections of both tests where the sample size is under and , respectively, that is for in (5.2). For the test (4.16) the supremum of the tail index is again approximated by the maximum over the finite grid , , , , in the pure jump case and over the finite grid , , , , , if a continuous component is involved. We observe a reasonable approximation of the nominal level in all cases under consideration.

Table 1: Simulated rejection probabilities of the test (4.16) and the test (4.17), using pure jump Itō semimartingale data vectors under the null hypotheses and , respectively.

Table 2: Simulated rejection probabilities of the test (4.16) and the test (4.17), using pure jump Itō semimartingale data vectors plus an effective drift and a Brownian motion under the null hypotheses and , respectively.

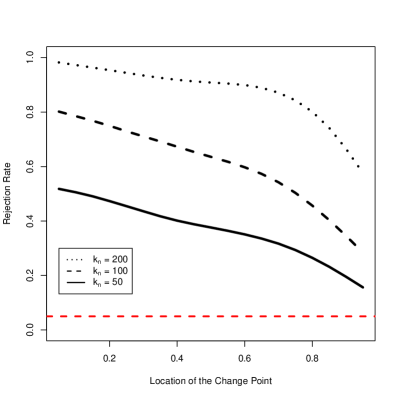

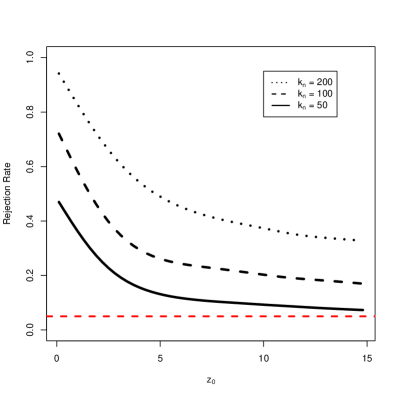

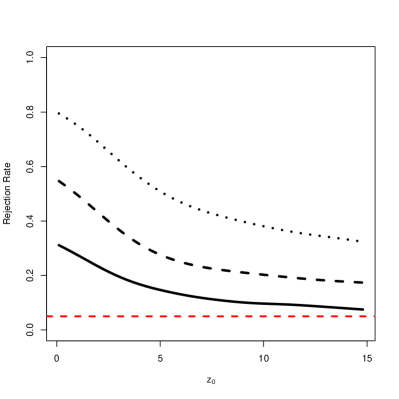

Figure 6: Simulated rejection probabilities of the test (4.16) for different locations of the change point for pure jump Itō semimartingale data (left-hand side) and with an additional continuous component (right-hand side). The dashed red line indicates the nominal level .

Figure 6 shows the simulated rejection probabilities of the test (4.16) for a linear change at different locations of the change point . The constant in (5.2) is chosen such that . In this special case the presence of a continuous component leads to a relatively strong loss of power of the test. This can be explained by the small value of , for which the rather small change in the jump behaviour is predominated stronger by the Brownian component. Furthermore the power of the test is decreasing in , which is a consequence of the fact that for large the data is ”closer” to the null hypothesis (recall the right-hand side of Figure 4).

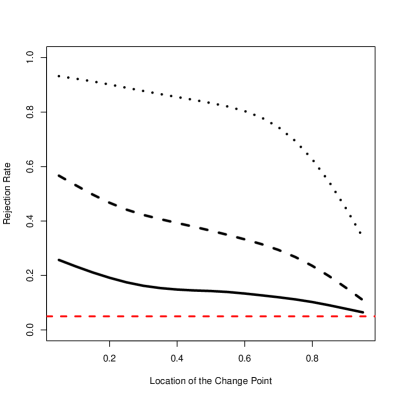

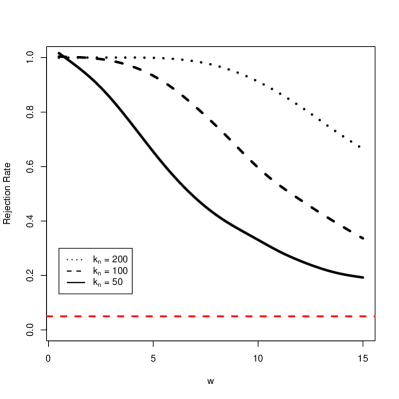

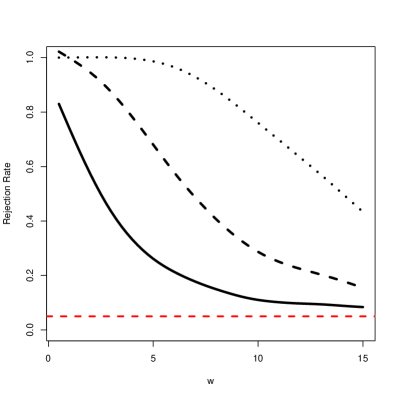

Figure 7: Simulated rejection probabilities of the test (4.17) for different choices of for pure jump data (left panel) and plus an effective drift and a Brownian motion (right panel). The dashed red line indicates the nominal level .

Figure 7 reveals the behaviour of the test (4.17) for different choices of the tail parameter . The data exhibits a linear change at with . The curves are obviously decreasing in , which is a consequence of very few large jumps even for this rather large choice of .

Figure 8: Simulated rejection probabilities of the test (4.16) for different degrees of smoothness for pure jump data (left-hand side) and with an additional continuous part (right-hand side). The dashed red line indicates the nominal level .

Finally, Figure 8 shows the dependence of the test (4.16) on the degree of smoothness . The change is located at , and in order to keep the results comparable the constant in (5.2) is chosen such that in each scenario. Overall, the power of the test in this experiment is relatively high, which is a consequence of the intermediate choice (recall Figure 4 and Figure 6). From the graphic on the right-hand side we also observe that the presence of a continuous component leads to a loss of power in this case as well. Moreover, the fact that the curves in Figure 8 are decreasing in coincides with the heuristic idea that smoother changes are more difficult to detect.

Acknowledgements

This work has been supported in part by the

Collaborative Research Center ”‘Statistical modeling of nonlinear

dynamic processes”’ (SFB 823, Projects A1 and C1) of the German Research Foundation (DFG).

We would like to thank Martina Stein who typed parts of this manuscript with considerable

technical expertise and Michael Vogt for some helpful discussions.

References

Aït-Sahalia and Jacod, (2014)

Aït-Sahalia, Y. and Jacod, J. (2014).

High-Frequency Financial Econometrics.

Princeton University Press.

Aue and Horváth, (2013)

Aue, A. and Horváth, L. (2013).

Structural breaks in time series.

Journal of Time Series Analysis, 34(1):1–16.

Aue and Steinebach, (2002)

Aue, A. and Steinebach, J. (2002).

A note on estimating the change-point of a gradually changing

stochastic process.

Statistics & Probability Letters, 56:177–191.

Bissell, (1984)

Bissell, A. F. (1984).

The performance of control charts and cusums under linear trend.

Applied Statistics, 33:145–151.

Bücher, (2011)

Bücher, A. (2011).

Statistical Inference for Copulas and Extremes.

PhD thesis, Ruhr-Universität Bochum.

Bücher et al., (2017)

Bücher, A., Hoffmann, M., Vetter, M., and Dette, H. (2017).

Nonparametric tests for detecting breaks in the jump behaviour of a

time-continuous process.

Bernoulli, 23(2):1335–1364.

Bücher and Kojadinovic, (2016)

Bücher, A. and Kojadinovic, I. (2016).

A dependent multiplier bootstrap for the sequential empirical copula

process under strong mixing.

Bernoulli, 22(2):927–968.

Chen and Shao, (2001)

Chen, L. and Shao, Q.-M. (2001).

A non-uniform Berry-Esseen bound via Stein’s method.

Probability Theory and Related Fields, 120:236–254.

Cont and Tankov, (2004)

Cont, R. and Tankov, P. (2004).

Financial Modelling with Jump Processes.

Chapman and Hall/CRC.

Figueroa-López, (2008)

Figueroa-López, J. (2008).

Small-time moment asymptotics for Lévy processes.

Statistics and Probability Letters, 78:3355–3365.

Gaenssler et al., (2007)

Gaenssler, P., Molnár, P., and Rost, D. (2007).

On continuity and strict increase of the CDF for the sup-functional

of a Gaussian process with applications to statistics.

Results in Mathematics, 51:51–60.

Gan, (1991)

Gan, F. F. (1991).

Ewma control chart under linear drift.

Journal of Statistical Computation and Simulation, 38:181–200.

Hoffmann, (2016)

Hoffmann, M. (2016).

Stochastische Integration. Eine Einführung in die

Finanzmathematik.

Springer.

Hoffmann and Vetter, (2017)

Hoffmann, M. and Vetter, M. (2017+).

Weak convergence of the empirical truncated distribution function of

the Lévy measure of an Itō semimartingale.

Stochastic Processes and their Applications, to appear.

Hus̆ková, (1999)

Hus̆ková, M. (1999).

Gradual changes versus abrupt changes.

Journal of Statistical Planning and Inference, 76:109–125.

Hus̆ková and Steinebach, (2002)

Hus̆ková, M. and Steinebach, J. (2002).

Asymptotic tests for gradual changes.

Statistics & Decisions, 20:137–151.

Jacod and Protter, (2012)

Jacod, J. and Protter, P. (2012).

Discretization of Processes.

Springer.

Jacod and Shiryaev, (2002)

Jacod, J. and Shiryaev, A. (2002).

Limit Theorems for Stochastic Processes.

Springer.

Jandhyala et al., (2013)

Jandhyala, V., Fotopoulos, S., MacNeill, I., and Liu, P. (2013).

Inference for single and multiple change-points in time series.

Journal of Time Series Analysis, forthcoming, doi:

10.1111/jtsa12035.

Kosorok, (2003)

Kosorok, M. (2003).

Bootstraps of sums of independent but not identically distributed

stochastic processes.

Journal of Multivariate Analysis, 84:299–318.

Kosorok, (2008)

Kosorok, M. (2008).

Introduction to Empirical Processes and Semiparametric

Inference.

Springer Series in Statistics. Springer.

Mallik et al., (2013)

Mallik, A., Banerjee, M., and Sen, B. (2013).

Asymptotics for -value based threshold estimation in regression

settings.

Preprint.

Nickl et al., (2016)

Nickl, R., Reiß, M., Söhl, J., and Trabs, M. (2016).

High-frequency Donsker theorems for Lévy measures.

Probability Theory and Related Fields, 164(1-2):61–108.

Rüschendorf and Woerner, (2002)

Rüschendorf, L. and Woerner, J. H. C. (2002).

Expansion of transition distributions of Lévy processes in small

time.

Bernoulli, 8(1):81–96.

Sato, (1999)

Sato, K.-I. (1999).

Lévy Processes and Infinitely Divisible Distributions.

Cambridge University Press.

Siegmund and Zhang, (1994)

Siegmund, D. O. and Zhang, H. (1994).

Confidence regions in broken line regression.

In Carlstein, E., Müller, H.-G., and Siegmund, D., editors, Change-point problems, volume 23 of Lecture Notes–Monograph Series,

pages 292–316. Institute of Mathematical Statistics.

Todorov, (2015)

Todorov, V. (2015).

Jump activity estimation for pure-jump semimartingales via

self-normalized statistics.

The Annals of Statistics, 43(4):1831–1864.

Todorov, (2016)

Todorov, V. (2016).

Testing for time-varying jump activity for pure jump semimartingales.

The Annals of Statistics, to appear.

Van der Vaart and Wellner, (1996)

Van der Vaart, A. and Wellner, J. (1996).

Weak Convergence and Empirical Processes.

Springer.

Vogt and Dette, (2015)

Vogt, M. and Dette, H. (2015).

Detecting gradual changes in locally stationary processes.

The Annals of Statistics, 43(2):713–740.

6 Proofs and technical details

The following assumptions will be used frequently in the sequel.

Assumption 6.1.

For each let be an Itō semimartingale of the form (1.1) with characteristics and the following properties:

(a)

There exists a such that

holds for all and all as measures on .

(b)

The drift and the volatility are deterministic and Borel measurable functions on . Moreover, these

functions are uniformly bounded in and .

(c)

The observation scheme satisfies

and

We begin with an auxiliary result which is a generalization of Lemma 2 in Rüschendorf and Woerner, (2002). Throughout this section denotes a generic constant which typically changes from line to line and may depend on certain bounds and parameters, but not on .

Lemma 6.2.

Let and let be an Itō semimartingale with having a representation as in (1.1) with characteristics , where and are uniformly bounded in and and is deterministic. Suppose that there are constants such that the support of the measure is contained in the set . Furthermore assume that there is a with for all . Then for each and there are and , which depend only on , the bound on in Assumption 2.1(2) and the bounds on and , such that the transition probability is bounded by

for all .

Proof.

We will only show the inequality for fixed, because otherwise we can consider the process which has the same properties.

The Hölder inequality and the upper Burkholder-Davis-Gundy inequality yield for any and any :

and

Therefore Markov inequality ensures that the claim follows if we can show the lemma for each Itō semimartingale with .

Let be such an Itō semimartingale and let . Then by Theorem II.4.15 in Jacod and Shiryaev, (2002) is a process with independent increments with characteristic function

(6.1)

since and with

exists for all such and all by a Taylor expansion of the integrand and the assumption on the support of as well as item (2) in Assumption 2.1. Furthermore the first two derivatives of are given by

where we have exchanged differentiation and integration by the differentiation lemma of measure theory and the assumption on the support of .

Without loss of generality we may assume that the measure is not zero, because otherwise

a.s. and the assertion of the lemma is obvious. Therefore for all and is a strictly increasing function with and . Thus it has a strictly increasing, differentiable inverse function with . Moreover, it is sufficient to show the claim for all , because for and we can find some and with

and . By Corollary 1.50 in Hoffmann, (2016) and by the bounded support of the measure the right-hand side of (6.1) can be extended to an entire function on . Consequently, by Lemma 25.7 in Sato, (1999) for every and with another application of Corollary 1.50 in Hoffmann, (2016) the mapping is an entire function on . Therefore according to the identity theorem of complex analysis (6.1) holds for all . Thus by Markov inequality we have for arbitrary :

(6.2)

First suppose that . Then we obtain

and the claim obviously follows. Therefore for the rest of the proof we may assume . In this case (6.2) yields (recall that is the inverse function of )

for arbitrary and , where the constant depends only on the bound on in Assumption 2.1(2). By a series expansion of the exponential function we have

(6.6)

if and this is the case if

(6.7)

where we used (6.4) again. Combining (6), (6.6) and (6) gives

(6.8)

for . Let be small enough such that for each . Then (6.8) together with (6) yield the estimate

for each with a small enough such that

and

for every .

The preceding result is helpful to deduce the following claim which is the main tool to establish consistency of as an estimator for , when it is applied to the Itō semimartingale .

Lemma 6.3.

Suppose that Assumption 6.1 is satisfied and let . If for all , then there exist

constants and such that

holds for all , and with .

Proof of Lemma 6.3.

Let and pick a smooth cut-off function satisfying

We also define the function via . For and let be the measure defined by

for which has total mass

(6.9)

where depends only on the bound on in Assumption 2.1(2) and on and therefore on . Furthermore, let

By Theorem II.4.15 in Jacod and Shiryaev, (2002) for each and with we can decompose in law by

(6.10)

where and are independent Itō semimartingales starting in zero, with characteristics , , and , respectively.

can be seen as a generalized compound Poisson process. To be precise, let be a Poisson random measure independent of with predictable compensator and consider the process

By Theorem II.4.8 in Jacod and Shiryaev, (2002) is a process with independent increments and distribution

(here we use the convention that is the Dirac measure with mass in zero). Moreover, for each let be a sequence of independent processes, which is also independent of the Poisson random measure and of the process , such that for each and its distribution is given by

Then we have for any and

(6.11)

because by using independence of the involved quantities we calculate the characteristic function for and as follows:

(6.12)

In the above display denotes the characteristic function of a finite Borel measure . The last equality in (6) follows from Theorem II.4.15 in Jacod and Shiryaev, (2002). Furthermore note that in the case

the distributions in (6.11) are obviously equal.

Let with , define and recall the decomposition in (6.10) and the representation (6.11)

for . As the processes and are independent, we can calculate

(6.13)

For the first summand on the right-hand side of the last display we use Lemma 6.2 with and and obtain

(6.14)

for , where and depend only on , the bound

for the transition kernel in Assumption 2.1(2) and the bounds on and . Note that is bounded for by a bound which depends on , thus on , and on the previously mentioned bound on . Also, for the third term on the right-hand side of (6), we have

(6.15)

by (6.9) since is bounded by . Now, if the second term in (6) and vanish. Hence the lemma follows from (6.14) and (6.15). Thus in the following we assume and consider the term . For the distribution of has the Lebesgue density

As a consequence (for ), the function

is twice continuously differentiable and it follows

(6.16)

where the constant depends only on the bound in Assumption 2.1(4) for some with but not on or . Using the independence of and it is sufficient to discuss . Itô formula (Theorem I.4.57 in Jacod and Shiryaev, (2002)) gives

(6.17)

where denotes the predictable quadratic variation of the continuous local martingale part of , and

is the jump size at time . We now discuss each of the four summands in (6) separately for : first, implies by definition of . Thus, with

By the canonical representation of semimartingales (Theorem II.2.34 in Jacod and Shiryaev, (2002)) we get the decomposition

where is a local martingale with characteristics which starts at zero and has bounded jumps. Consequently is a locally square integrable martingale and by Proposition I.4.50 b), Theorem I.4.52 and Theorem II.1.8 in Jacod and Shiryaev, (2002) its predictable quadratic variation is given by

Thus for and because of the boundedness of and the construction of the stochastic integral the integral process stopped at time is in fact a square integrable martingale because

Therefore we obtain

and according to (6.16) we get a bound for the second term in (6):

(6.18)

where depends only on , the bounds on the characteristics and the bounds of Assumption 2.1(2) and (4) for an appropriate . For the third term in (6) it is immediate to get an estimate as in (6.18). Finally, let denote the random measure associated with the jumps of which has the predictable compensator . Therefore Theorem II.1.8 in Jacod and Shiryaev, (2002) yields for the expectation of the last term in (6)

(6.19)

Note that the integrand in the second line in (6) is a concatenation of a Borel measurable function on and the obviously predictable function from into . Consequently, this integrand is in fact a predictable function and Theorem II.1.8 in Jacod and Shiryaev, (2002) can in fact be applied. The first inequality in (6) follows with (6.16) and a Taylor expansion of the integrand. Accordingly the constant after the last inequality in (6) depends only on the quantities as claimed in the assertion of this lemma. Thus we have

which together with for small as well as (6), (6.14) and (6.15) yields the lemma.

Let denote a semimartingale of the form (1.1) and consider the decomposition , where

and is a pure jump Itō semimartingale with characteristics . Furthermore we consider the process

in . The proof can be divided into two steps:

(6.20)

(6.21)

The assertion of Theorem 3.1 then follows from Lemma 1.10.2(i) in Van der Vaart and Wellner, (1996).

(6.20) can be obtained with similar steps as in the first part of the proof of Theorem 2.3 in Bücher et al., (2017) using Theorem 11.16 in Kosorok, (2008) which is a central limit theorem for triangular arrays of row-wise i.i.d. data. The main difference regards the use of Lemma 6.3 which is needed as we work in general with a time-varying kernel .

where denotes the statistic based on the scheme . For the first term in (6.22) we obtain

uniformly on , with the same arguments as in the second part of the proof of Theorem 2.3 in Bücher et al., (2017). Furthermore, along the lines of the proof of Corollary 2.5 in Bücher et al., (2017), but using Lemma 6.3 instead, one can show that the second term in (6.22) is a uniform on .

Recall the decomposition in the proof of Theorem 3.1. The idea of the proof is to show the claim of Theorem 3.3 for , the process being defined exactly as in (3.6) but based on the increments . This can be done with Theorem 3 in Kosorok, (2003), because we have i.i.d. increments of the processes . Furthermore, by Lemma A.1 in Bücher, (2011) it is then enough to prove in order to show Theorem 3.3. For a detailed proof we refer the reader to the proof of Theorem 3.3 in Bücher et al., (2017), which follows similar lines.

As the process is tight, is also tight

and Theorem 3.2 together with the continuous mapping theorem yield in . The assertion now follows observing the definition of in (3.5) and the fact that

vanishes whenever .

The claim follows if we can prove the existence of a constant such that

(6.23)

(6.24)

where .

In order to verify (6.23) we calculate as follows

(6.25)

where is defined in (4.4). The third estimate is a consequence of the fact that whenever and the final convergence follows because a weakly converging sequence in is asymptotically tight.

Recall from (4.1).

It holds that

with from (4.9), and by (3) we have

(6.36)

Thus is a supremum of a non-vanishing Gaussian process with mean zero. Due to Corollary 1.3 and Remark 4.1 in Gaenssler et al., (2007) then has a continuous distribution function.

As a consequence (4.10) follows from (6.35) and Proposition F.1 in the supplement to Bücher and Kojadinovic, (2016) as soon as we can show

(6.37)

for any fixed , where are independent copies of .

In order to establish (6.37) we first show that the sample paths of are uniformly continuous on with respect to the Euclidean distance. By Theorem 3.1 and Assumption 2.1 the sample paths of the process in satisfy for all and they are uniformly continuous with respect to the Euclidean distance on . Thus the uniform continuity of the sample paths of holds if we can show that for a bounded and uniformly continuous function with for all the function defined via

is uniformly continuous on . But since a continuous function on a compact metric space is uniformly continuous it suffices to show continuity of the function

in every . The continuity of in is obvious, because is uniformly continuous and satisfies for all . Therefore only the case remains. Let be a neighbourhood of in which is bounded away from . Then it is immediate to see that the function defined by

is uniformly continuous on .

Let be arbitrary and choose such that

for all with maximum distance and additionally such that implies .

Then, if , there exists with

and we can choose a such that which gives

In an analogous manner we see that also for each with , and therefore is continuous in .

Next we show

(6.38)

for arbitrary . By Proposition 10.7 in Kosorok, (2008) and Theorem 3.4 we have in for all , which yields for all with the same reasoning as in the proof of Theorem 2.9.6 in Van der Vaart and Wellner, (1996). Theorem 1.5.7 and its addendum therein show that is asymptotically uniformly -equicontinuous in probability for each , where denotes the Euclidean metric on because the sample paths of are uniformly continuous with respect to and is totally bounded.

Therefore, for any we can choose a such that

which yields

for large enough, using consistency of the preliminary estimator.

Thus, now that we have established (6.38), by Lemma 1.10.2(i) in Van der Vaart and Wellner, (1996) we obtain (6.37) if we can show

But this is an immediate consequence of the continuous mapping theorem and

(6.39)

in for all , where are independent copies of , since , and are the images of the same continuous functional applied to , and , respectively. (6.39) follows as in Proposition 6.2 in Bücher et al., (2017).

We start with a proof of

which is equivalent to . Therefore we have to show

(6.40)

for arbitrary , by the definition of in (4.8). Since the

are pairwise uncorrelated with mean zero and bounded by , we have

(6.41)

Therefore, in order to prove (6.40), it suffices to verify

(6.42)

where the first inequality in the above display follows with the Markov inequality and the last inequality in (6.7) is a consequence of the fact that

Furthermore, by the definition of in (3.6) we have

(6.43)

because of for every . Recall the decomposition in the proof of Theorem 3.1 and let with from Assumption 2.4. Then we have for and large enough

(6.44)

where the last inequality follows using Lemma 6.3. By Hölder inequality, the Burkholder-Davis-Gundy inequalities (see for instance page 39 in Jacod and Protter, , 2012) and the Fubini theorem we have with , from Assumption 2.4, for each ,

(6.45)

and

(6.46)

Together with (6.44) and the Markov inequality these estimates yield

(6.47)

Therefore due to (6.7), (6.43), (6.47) and the Markov inequality we obtain

by the assumptions on the involved sequences. Thus we conclude .

Next we show , which is equivalent to

for each . With the same considerations as for (6.41) it is sufficient to show

By continuity of the function for from (4.9) we can find with

(6.48)

and because of

on the set and the consistency of the preliminary estimate it further suffices to prove

(6.49)

In order to show (6.49) we want to use a Berry-Esseen type result. Recall

with

and where denotes the standard normal distribution function. Before we proceed further in the proof of (6.49), we first show

(6.51)

which is

Let . Then a straightforward calculation gives

(6.52)

with . Now consider again the decomposition of the underlying Itō semimartingale as in the proof of Theorem 3.1 and the sequence with from Assumption 2.4.

With (6.45), (6.7) and Lemma 6.3 it is immediate to see that for

Setting

it is easy to deduce

using Lemma 6.3 again as well as independence of the increments of . Combining this result with (6.7) we have

for . Thus with (6.48) we obtain (6.51), because

by Theorem 3.1 we have

Recall that our main objective is to show (6.49) and thus we consider the Berry-Esseen bound on the right-hand side of (6.50). For the first summand we distinguish two cases according to the assumptions on the multiplier sequence.

Let us discuss the case of bounded multipliers first. For we have

for all on the set , since is bounded by . As a consequence

(6.53)

for large on the set .

In the situation of normal multipliers, recall that there exist constants such that for and large enough we have

(6.54)

Thus we can calculate for large enough on the set

where and depend on . The first inequality in the above display uses again and the last one follows with (6.54). Now let with and define . Then, for on the set , using , we conclude

(6.55)

We now consider the second term on the right-hand side of (6.50), for which

follows. Thus from (6.53), (6.55) and (6.7) we see that with from (6.50) for each there exists a such that

(6.57)

Now we can show (6.49). Let and according to (6.51) choose an with

for all . For this choose a such that the probability in (6.57) is smaller than for large . Then for large enough we have

using (6.50) and the fact, that if there exists a with .

Thus we have shown and we are only left with proving (4.11). Let

for all . Distinguishing the cases and we get due to

with

where . Due to the choice and the definition of it is clear that , because .

Concerning let be the distribution function of and let be the distribution function of . Then as we have seen in (6.36) in the proof of Theorem 4.4 the function is continuous and by Theorem 3.2 and the continuous mapping theorem converges pointwise to . Thus for choose an with and conclude

Therefore, as in the proof of Theorem 4.4, has a continuous cdf and

holds in for every , where are independent copies of . As a consequence the assertion follows with Proposition F.1 in the supplement to Bücher and Kojadinovic, (2016). The result for the test (4.17) follows in the same way.

If holds, then (4.18) is a simple consequence of

for all and which follow from Theorem 3.2 and Theorem 3.4 by similar arguments as in the previous proofs. The second claim can be shown in the same way.

∎

6.10 Proof of the results in Example 2.3 and Example 4.6(2).

(1)

First we show that a kernel as in (2.11) belongs to the set . Using the uniqueness theorem for measures we see that is the measure with Lebesgue density for each and . This function is continuously differentiable with derivative , and we obtain

for any so that Assumption 2.1(4) is satisfied. Assumption 2.1(3) is obvious,

and by definition it is also clear that does not charge for any , Finally, a simple calculation using symmetry of the integrand yields

by the assumptions on and . Thus also Assumption 2.1(2) is valid.

(2)

Now we show that if additionally (2.12) and (2.13) are satisfied, both holds for every and is a bounded function on as stated in Example 4.6(2). By shrinking the interval if necessary we may assume without loss of generality that the functions are bounded away from on . But then it is well known from complex analysis that there exist a domain and holomorphic functions such that are the restrictions of and to . Therefore for any the function is holomorphic in as a concatenation of holomorphic functions and thus its restriction to is real analytic. Consequently, by shrinking again if necessary, we have the power series expansion

(6.58)

for every and . If for some , then for any and we have . Thus we obtain

for every and . Taking the derivative with respect to for a fixed yields

for each and . But since it is assumed that at least one of the functions and is non-constant, there is a such that one derivative (and therefore both) are different from zero. Varying for this yields a contradiction.

In order to show that for each the function is bounded in , we use

for , where . Furthermore let the series expansion of the real analytic function be given by

(6.59)

Then, using the generalization of the product formula for higher derivatives

(6.60)

follows. The inequality in the display above holds because for the continuously differentiable function on satisfies and the only possible roots of its derivative are and . Therefore we obtain

for some suitable which does not depend on . is real analytic, thus the power series in (6.59) has a positive radius of convergence and by the Cauchy-Hadamard formula this fact is equivalent to the existence of a such that for each . As a consequence (2) yields

(6.61)

(3)

Finally, we show the expansion (4.13), and

we prove first that it suffices to verify it for from (2.5). If satisfies (4.13) with a function , we have for

where

A power series can be integrated term by term within its radius of convergence. Therefore, (6.58) gives for

which yields

(6.62)

For any set and bounded functions we have

Together with (6.62) this yields for

for , because the latter power series has a positive radius of convergence around .

For the same reason, in order to prove (6.66) we use

as .

Now, because of

(6.63) and (6.64) yield the desired expansion (4.13) for , if we can show for

The first assertion is obvious, since

by .

In order to prove the latter claim, consider for and the function with

Its derivative is given by

and it has a unique root at with

Thus because of , , for and for we obtain the result, since for