Time-dynamic inference for non-Markov transition probabilities under independent right-censoring

Abstract

††∗Department of Mathematics, Faculty of Science, Vrije Universiteit Amsterdam, 1081 HV Amsterdam, Netherlands, e-mail: d.dobler@vu.nl†††Department of Mathematics & Statistics, Lancaster University, Bailrigg, Lancaster, LA1 4YW, United Kingdom, e-mail: a.titman@lancaster.ac.ukIn this article, weak convergence of the general non-Markov state transition probability estimator by Titman (2015) is established which, up to now, has not been verified yet for other general non-Markov estimators. A similar theorem is shown for the bootstrap, yielding resampling-based inference methods for statistical functionals. Formulas of the involved covariance functions are presented in detail. Particular applications include the conditional expected length of stay in a specific state, given occupation of another state in the past, as well as the construction of time-simultaneous confidence bands for the transition probabilities. The expected lengths of stay in the two-sample liver cirrhosis data-set by Andersen et al. (1993) are compared and confidence intervals for their difference are constructed. With borderline significance and in comparison to the placebo group, the treatment group has an elevated expected length of stay in the healthy state given an earlier disease state occupation. In contrast, the Aalen–Johansen estimator-based confidence interval, which relies on a Markov assumption, leads to a drastically different conclusion. Also, graphical illustrations of confidence bands for the transition probabilities demonstrate the biasedness of the Aalen-Johansen estimator in this data example. The reliability of these results is assessed in a simulation study.

Keywords: Aalen–Johansen estimator; conditional expected length of stay; confidence bands; Markov assumption; multi-state model; right-censoring; weak convergence.

1 Introduction

Transition probabilities are essential quantities in survival analytic examinations of multi-state models. Under independent right-censoring, for instance, the Aalen–Johansen estimator assesses these probabilities optimally in nonparametric Markovian multi-state models; cf. Aalen (1978) and Section IV.4 in Andersen et al. (1993) for more details. The Markov assumption is crucial for the validity of the Aalen–Johansen estimator. However, in real world applications, it may be unrealistic to postulate such a structure: given the present patient’s state, future developments are often not independent of a severe past illness history. There have been several attempts to circumvent the Markov assumption: State occupation probabilities in general models have been estimated by Datta and Satten (2001), Datta and Satten (2002), and Glidden (2002) using the Aalen–Johansen estimator. Pepe et al. (1991) and Pepe (1991) used a combination of two Kaplan–Meier estimators to assess the relevant transition probability in an illness-death model with recovery. In illness-death models without recovery, Meira-Machado et al. (2006) used Kaplan–Meier-based techniques and consecutive latent transition times to estimate transition probabilities. More efficient variants of these estimators have been developed in de Uña-Álvarez and Meira-Machado (2015). A Kendall’s -based test of the Markov assumption in this progressive illness-death model was derived in Rodríguez-Girondo and Uña-Álvarez (2012). A competing risks-based estimator was proposed by Allignol et al. (2014) which relies on strict censoring assumptions. Eventually, Titman (2015) and Putter and Spitoni (2018) developed transition probability estimators in general non-Markov models by using different transition probability decompositions and utilizations of the Aalen–Johansen estimator. However, weak convergence properties of these estimators as elements of càdlàg function spaces have not been analyzed yet.

In the present paper, we focus on the non-Markov state transition probability estimator by Titman (2015) and its weak convergence for the following reasons: the estimator has a simple, but intuitive structure and it allows estimation of general transition probabilities between sets of states rather than single states. Finally, the bootstrap is shown to correctly reproduce the weak limit distribution. Throughout the article, let be the underlying probability space. To introduce the Titman (2015) estimator, we consider an independently right-censored multi-state model with different states. That is, the data consists of independent copies of a multi-state process which are indexed by time and which occupy the states . The right-censoring is modeled by independent random variables after which further observation of the corresponding multi-state processes is not possible any more. Let and be subsets of for which the transition probabilities

shall be estimated. Here and below, irrelevant subscripts are removed for notational convenience. Introduce the set of states , that implies sure occupancy of at all later points in time, and the set of states which prevents occupancy of at all later points of time. Individual competing risks processes, , are used in an intermediate estimation step. indicates whether the multi-state process is at time in none of the absorbing subsets or . On the other hand, holds if the transition to has been observed until time and similarly for the transition to . Let denote the at-risk indicators of the competing risks processes and let be the corresponding censoring indicators, i.e., if the transition of is eventually observed and if a censoring comes first. The final data-set is whereof, in case of , the processes and are observable only until censoring occurs. Hence, incorporating random right-censoring, the transition probability is decomposed into

The first two components in this decomposition are estimated by the standard Kaplan–Meier estimator for the survival function and the Aalen–Johansen estimator for the cumulative incidence function of the sub-group of those individuals which were observed to occupy state at time . The remaining conditional probability is estimated using the empirical proportion

where denotes the indicator function. Therefore, the overall transition probability estimator by Titman (2015) is given as

This article shall establish the weak convergence of and of a bootstrap variant thereof as . Finally, implications to confidence interval construction for the conditional expected length of stay and to time-simultaneous confidence bands for the transition probabilities are demonstrated. The proofs of all Theorems and Lemmata as well as detailed derivations of all asymptotic covariance functions are given in the appendix.

2 Main Results

We focus on the Titman (2015) estimator during where is a terminal time satisfying and . The large sample properties of are derived from central limit theorems of its individual components. To obtain such for the fraction process , we throughout assume the existence of bounded one- and two-step hazard functions for transitions into and , respectively, which are approached uniformly:

| (1) | ||||

| (2) | ||||

| (3) | ||||

| (4) |

Here, . In contrast to the standard choice in the literature, we let the at-risk indicators , that are involved in the estimator , be right-continuous. The typical reason for using the left-continuous version is the applicability of martingale methods which do not matter in our analysis of the estimators. On top of that, this choice does not matter in the present article as all transition times are continuously distributed. The definitions of the Kaplan–Meier and the Aalen–Johansen estimators remain unchanged. We equip the càdlàg function space with the supremum norm and products thereof with the maximum-supremum norm; see Chapter 3.9 in van der Vaart and Wellner (1996) for applications in survival analysis with this choice. In order to state our main theorem, it is convenient to provide an auxiliary lemma:

Lemma 1

Detailed formulas for these covariance functions are presented in the appendix. From the presentation therein it is apparent that the covariances can be estimated straightforwardly.

Define and . An application of the functional delta-method immediately yields our main theorem:

Theorem 1

To be able to use this result for time-simultaneous inference on or simply for improving the accurateness of -based inference methods with a pivotal limit distribution, the classical bootstrap seems to be a useful choice of a resampling method. To this end, a bootstrap sample is obtained by randomly drawing quadruples times with replacement from the original sample . This bootstrap sample is used to recalculate the transition probability estimator, resulting in

For this bootstrap counterpart, a central limit theorem similar to the main Theorem 1 holds:

Theorem 2

That is, the bootstrap succeeds in correctly recovering the limit distribution of the transition probability estimate , enabling an approximation of its finite sample distribution.

3 Inference Procedures

3.1 Conditional Expected Length of Stay

A practical application of both main theorems is a two-sample comparison of expected lengths of stay in the state set of interest, , given occupation of a fixed state set at time . Considering temporarily the above one-sample set-up, the conditional expected length of stay is

see e.g. Grand and Putter (2016) for a pseudo-observation regression treatment. An R package for deriving the change in lengths of stay, that relies on the Aalen–Johansen estimator, is described in Wangler et al. (2006). For further literature on lengths of stay within multi-state models, see the articles cited therein. In the special case of a simple survival model, the only expected length of stay of interest is the mean residual lifetime; see e.g. Meilijson (1972). Here, however, the Markov assumption shall not be imposed such that estimation of the length of stay is based on the Titman (2015) estimator.

Sample-specific quantities are furnished with a superscript . For instance, is the first sample’s transition probability estimate to switch into some state of at time given that a state of is occupied at time . The sample sizes and may be different. We would like to test the null hypothesis

If is a favourable set of states, then the rejection of is an indication of the superiority of the second treatment over the first. A reasonable estimator of is . Note that, even under the boundary , the underlying transition probabilities and are allowed to differ. Hence, we do not rely on the restrictive null hypothesis but rather on the hypothesis of actual interest.

Theorem 3

Replacing all estimators in the previous theorem by their bootstrap counterparts, where both underlying bootstrap samples and are obtained by and times independently and separately drawing with replacement from and , respectively, a similar convergence in conditional distribution given holds in probability. This result may be used for bootstrap-based and asymptotically exact confidence intervals for the difference in the conditional expected lengths of stay, ; see Sections 4 and 5 below.

3.2 Simultaneous Confidence Bands

Even though the bootstrap procedure is useful but not strictly necessary for inference on the expected length of stay, it plays an essential role in time-simultaneous inference on the transition probabilities . This is due to the unknown stochastic behaviour of the limit process which, again in the context of creating confidence bands, is also the reason for the inevitableness of resampling procedures for Aalen-Johansen estimators even if the Markov assumption is fulfilled; see Bluhmki et al. (2018) for theoretical justifications and their practical performance.

For the derivation of reasonable time-simultaneous confidence bands for on a time interval based on in combination with the bootstrap, we focus on the process

where a transformation will ensure bands within the probability bounds and , and a suitable multiplicative weight function will stabilize the bands for small samples. In particular, we use one of the log-log transformations or (Lin, 1997), depending on whether we expect to be closer to 1 or 0. As weight function, for transformation , we choose ,

With these choices, the resulting confidence bands will correspond to the classical equal precision (EP) bands for or the Hall-Wellner (H-W) bands for if is an absorbing subset of states; cf. p. 265ff. in Andersen et al. (1993) for the survival case and or Lin (1997) in the presence of competing risks and .

The confidence bands are found by solving for in the probability . Here, the value of is approximated by the -quantile of the conditional distribution of the supremum of the bootstrap version of given the data, where in the definition of all estimators and are replaced with their bootstrap counterparts and .

Finally, the resulting confidence bands for are as follows:

The performance of these confidence bands as well as the confidence band obtained from not transforming or weighting the transition probability estimator are assessed in a simulation study in the subsequent sections.

4 Simulation Study

4.1 Conditional Expected Length of Stay

To assess the performance of the conditional length of stay estimators for finite sample sizes a small simulation study is conducted. Data are simulated from a pathological non-Markov model in which the subsequent dynamics of the process depend on the state occupied at . A three-state illness-death model with recovery is used where the state means “healthy”, “ill”, and “dead”. The transition intensities are , while

| (7) |

In the last part of the appendix we prove that the conditions (1)–(4) are satisfied in the present set-up. Subjects are independently right-censored via an exponential distribution with rate 0.04. We focus on the expected length of stay in the health state conditional on an earlier illness at time , i.e. and . For each simulated dataset, is estimated and 95% confidence intervals are constructed via three methods; a Wald interval using the plug-in variance estimator of , in which the canonical estimators of , , , , and are chosen, a classical bootstrap and a bootstrap-t procedure using the bootstrap-version of to studentize the bootstrap samples. For each bootstrap, samples are generated.

In the present three-state model, the Titman (2015) transition probability estimator reduces to because the healthy state is non-absorbing. Thus, the asymptotic variance of each sample-specific conditional expected length of stay estimator is

As a competing method, Aalen–Johansen estimator-based Wald-type confidence intervals are constructed for the same expected length of stay. Standard arguments yield that the asymptotic covariance function of the normalized Aalen–Johansen estimator for the transition is

cf. Section IV.4.2 in Andersen et al. (1993) for the corresponding particular variance formula. The expected length of stay asymptotic variance again results from a double integral of this covariance function with integration range .

We consider several different scenarios for the total sample size, and . Note that the non-Markov estimator only uses the subgroup of subjects satisfying which corresponds to only subjects, on average. For each of the scenarios, 10000 datasets are generated. As a result the empirical coverage percentages have approximate Monte-Carlo standard error of around 0.2.

| Bias | Coverage % | |||||

| AJ | NM | Wald (AJ) | Wald (NM) | Naive bootstrap | Bootstrap-t | |

| 50 | -0.231 | 0.181 | 92.09 | 91.01 | 94.23 | 90.85 |

| 100 | -0.268 | 0.085 | 89.95 | 94.54 | 94.08 | 94.43 |

| 150 | -0.279 | 0.063 | 88.14 | 95.24 | 94.21 | 95.00 |

| 200 | -0.297 | 0.033 | 86.34 | 95.56 | 94.54 | 95.43 |

The simulation results are shown in Table 1. Both the Aalen-Johansen and non-Markov estimator have substantial bias when leading to under coverage of all the nominal 95% confidence intervals. For larger , both of the bootstrap confidence intervals and the Wald-based interval for the non-Markov estimator give close to nominal coverage. The coverage of the Aalen-Johansen based Wald confidence interval deteriorates with increasing due to the estimator being inherently biased.

4.2 Simultaneous Confidence Bands

To investigate the coverage probabilities of simultaneous confidence bands introduced in Section 3.2, datasets are simulated under the same non-Markov model as above, again considering total sample sizes of and patients. 95% simultaneous confidence bands are constructed for for For the non-Markov estimator, in addition to the Hall-Wellner and equal precision bands using the transformation , a naive confidence band based on a constant weight function, , and an identity transformation, , is also constructed. In addition, for the Aalen-Johansen estimates, EP bands based on , are constructed via the wild bootstrap using the R code which has been made available in the supplement to Bluhmki et al. (2018). In all cases, for each bootstrap samples are generated.

Table 2 gives the empirical coverage probabilities of the simultaneous confidence bands based on 5000 simulated datasets. For the bands based on the Non-Markov estimator, the H-W and EP bands tend to over-cover quite markedly for small sample sizes, while the naive bands under-cover. Adequate coverage is achieved for the H-W and EP bands by . Since the Aalen-Johansen estimator is biased for this scenario we would expect the coverage of the EP Aalen-Johansen bands to deteriorate with increasing sample size. However, it appears this is counteracted by the estimated quantiles, increasing with . As a consequence, the coverage initially grows with increasing before beginning to decrease.

| Non-Markov | Aalen-Johansen | |||

| H-W | EP | Naive | EP | |

| 50 | 0.9996 | 0.9972 | 0.9226 | 0.9154 |

| 100 | 0.9896 | 0.9846 | 0.9238 | 0.9188 |

| 150 | 0.9604 | 0.9542 | 0.9298 | 0.9230 |

| 200 | 0.9496 | 0.9496 | 0.9420 | 0.9124 |

5 Application to the Liver Cirrhosis Data-Set

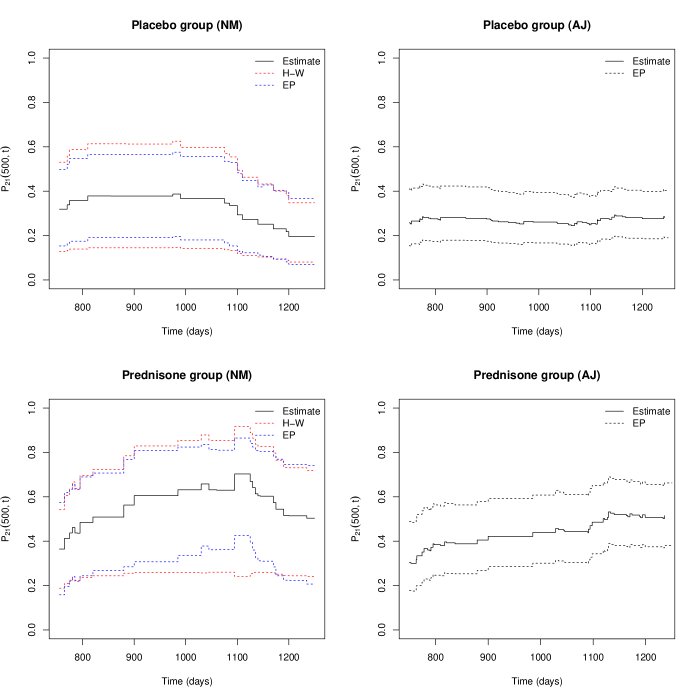

As an illustrative example we consider the liver cirrhosis data set introduced by Andersen et al. (1993) and also analyzed by Titman (2015). Patients were randomized to either a treatment of prednisone (251 patients) or a placebo (237 patients). A three-state illness-death model with recovery is assumed where the healthy and illness states correspond to normal and elevated levels of prothrombin, respectively. A potential measure of the effectiveness of prednisone as a treatment is the expected length-of-stay in the normal prothrombin level state, from a defined starting point. Specifically we consider , the difference in conditional expected length-of-stay in normal prothrombin levels, given the patient is alive and with abnormal prothrombin at time , for the prednisone and placebo groups, corresponding to and , respectively. Titman (2015) observed an apparent treatment difference with respect to the transition probabilities with respect to days post-randomization. We consider the expected length-of-stay in state 0 up to time days.

In this case, patients in the prednisone group and patients in the placebo group meet the condition that and . Bootstrap based confidence intervals are constructed using bootstrap samples within each group.

| Method | 95% CI | |

|---|---|---|

| Wald | 375.3 | (-2.1, 752.8) |

| Naive bootstrap | 375.3 | (14.7, 740.0) |

| Bootstrap-t | 375.3 | (-5.1, 747.3) |

| AJ (Wald) | 11.9 | (-217.3, 241.1) |

Table 3 shows the three constructed 95% confidence intervals, which are broadly similar, although the naive bootstrap interval excludes 0, whereas the Wald and bootstrap-t intervals do not. The Aalen-Johansen based estimate and a Wald confidence interval is also given. It is seen that there is a dramatic difference between the non-Markov and Aalen-Johansen estimates, with the latter indicating no treatment difference. Potentially, the apparent non-Markov behaviour in the data may be due to patient heterogeneity within the treatment groups.

To illustrate the construction of simultaneous confidence bands we construct 95% confidence bands for , in the interval . Since it was seen in Section 4 that reasonable sample size is required for good coverage an earlier start time is used here than for the estimate of the expected length of stay to ensure sufficient numbers of patients are under observation. Since we expect , we chose the confidence bands using the transformation

Figure 1 shows the confidence bands for the placebo and prednisone groups using Hall-Wellner and equal precision intervals using the non-Markov estimator and using the equal precision intervals for the Aalen-Johansen estimator.

6 Discussion

To the best of our knowledge, our paper is the first to prove weak convergence properties of a general transition probability estimator in independently right-censored non-Markov multi-state models while also providing explicit formulas of the asymptotic covariance functions. Similar proofs have been given for the classical bootstrap, which finally allows the utilization of the Titman (2015) estimator in time-simultaneous inference procedures. Unfortunately, when focusing on inference on the expected length of stay for single time points, both bootstrap methods applied in Section 4 yielded a greater deviance of the nominal coverage level than the simple studentization method based on the asymptotic quantiles of the standard normal distribution. Even though the simulated small sample coverage probabilities were more satisfying, other resampling procedures might improve the performance in both, small and large samples. For example, the martingale residual multiplier methods of Lin (1997), Beyersmann et al. (2013), or Dobler et al. (2017) are the method of choice in incomplete competing risks data and they may be adapted for the present context in a future paper.

On the other hand, the time-simultaneous confidence bands derived in this paper cannot rely on a purely asymptotic quantile finding approach. Instead, they truly require a resampling method such as the bootstrap method developed here. Furthermore, the simulation results in Section 4.2 and the application to the liver cirrhosis data set in Section 5 demonstrate their practical usefulness: not only did they reveal reliable coverage probabilities for relatively small sample sizes already. They were also only slightly wider than the confidence bands based on the Aalen-Johansen estimator for which there is no guarentee of applicability.

Another field of possible future interest is the extension of the present methodology to quality-adjusted sums of expected lengths of stay in a specific sub-set of states; cf. Williams (1985) who proposed such quality-adjusted life years for operation considerations. For instance, the expected length of stay in a healthy state could be weighted with a factor whereas the length of stay in the illness state obtains the weight . The specific choice of may be obtained from additional information on, e.g., the pain scores of patients in the illness state and may be chosen individually by the patients themselves. This way, a comparison of treatments could be achieved that more realistically accounts for the circumstances of a specific disease. However, one should bear in mind the controversial debate on quality-adjusted life years as articulated by e.g. Harris (1987); see also the discussion of the paper by Cox et al. (1992). Therein, G. W. Torrance appreciates the usefulness of quality-adjusted life years for resource allocation if combined with other measures and advices: He states that quality-adjusted life years “were never intended for clinical decision-making - they were developed for use in resource allocation.” They should also be reported together with other important measures for reaching a decision. Finally, one should add “a thorough sensitivity analysis and thoughtful discussion, including caveats” to obtain an informative quality-adjusted life years analysis.

Finally, reconsider the data analysis in Section 5 where the Aalen–Johansen estimator yielded a difference of expected lengths of stay which drastically deviates from the same quantity based on the Titman (2015) estimator. This might be considered as a strong evidence against the Markov assumption. If, on the other hand, a formal test of Markovianity does not find such evidence, the resulting estimated lengths of stay might be comparable as well. Even more can be gained by means of such tests: as apparent from the mentioned liver cirrhosis data example, the confidence intervals and simultaneous confidence bands based on the Aalen–Johansen estimator are much narrower, resulting from the efficiency of this estimator in comparison to non-Markov transition probability estimates. Equivalently, test procedures based on the classical estimator are more powerful in detecting deviances from null hypotheses. Therefore, formal tests for the applicability of the classical Aalen–Johansen estimator shall be developed in future articles.

Acknowledgements

The authors would like to thank Markus Pauly for helpful discussions. Dennis Dobler was supported by a DFG (German Research Foundation) grant.

References

- Aalen (1978) O. O. Aalen. Nonparametric Inference for a Family of Counting Processes. The Annals of Statistics, 6(4):701–726, 1978.

- Akritas (1986) M. G. Akritas. Bootstrapping the Kaplan–Meier Estimator. Journal of the American Statistical Association, 81(396):1032–1038, 1986.

- Allignol et al. (2014) A. Allignol, J. Beyersmann, T. Gerds, and A. Latouche. A competing risks approach for nonparametric estimation of transition probabilities in a non-Markov illness-death model. Lifetime Data Analysis, 20(4):495–513, 2014.

- Andersen et al. (1993) P. K. Andersen, Ø. Borgan, R. D. Gill, and N. Keiding. Statistical Models Based on Counting Processes. Springer, New York, 1993.

- Beyersmann et al. (2013) J. Beyersmann, M. Pauly, and S. Di Termini. Weak Convergence of the Wild Bootstrap for the Aalen–Johansen Estimator of the Cumulative Incidence Function of a Competing Risk. Scandinavian Journal of Statistics, 40(3):387–402, 2013.

- Billingsley (1999) P. Billingsley. Convergence of Probability Measures. John Wiley & Sons, New York, second edition, 1999.

- Bluhmki et al. (2018) T. Bluhmki, C. Schmoor, D. Dobler, M. Pauly, J. Finke, M. Schumacher, and J. Beyersmann. A wild bootstrap approach for the Aalen–Johansen estimator. Biometrics, early view, 74(3):977–985, 2018.

- Cox et al. (1992) D. R. Cox, R. Fitzpatrick, A. E. Fletcher, S. M. Gore, D. J. Spiegelhalter, and D. R. Jones. Quality-of-life Assessment: Can We Keep It Simple? Journal of the Royal Statistical Society. Series A (Statistics in Society), 155(3):353–393, 1992.

- Datta and Satten (2001) S. Datta and G. A. Satten. Validity of the Aalen–Johansen estimators of stage occupation probabilities and Nelson–Aalen estimators of integrated transition hazards for non-Markov models. Statistics & Probability Letters, 55(4):403–411, 2001.

- Datta and Satten (2002) S. Datta and G. A. Satten. Estimation of Integrated Transition Hazards and Stage Occupation Probabilities for Non-Markov Systems Under Dependent Censoring. Biometrics, 58(4):792–802, 2002.

- de Uña-Álvarez and Meira-Machado (2015) J. de Uña-Álvarez and L. Meira-Machado. Nonparametric Estimation of Transition Probabilities in the Non-Markov Illness-Death Model: A Comparative Study. Biometrics, 71(2):364–375, 2015.

- Dobler (2016) D. Dobler. Nonparametric inference procedures for multi-state Markovian models with applications to incomplete life science data. PhD thesis, Universität Ulm, Deutschland, 2016.

- Dobler and Pauly (2014) D. Dobler and M. Pauly. Bootstrapping Aalen-Johansen processes for competing risks: Handicaps, solutions, and limitations. Electronic Journal of Statistics, 8(2):2779–2803, 2014.

- Dobler et al. (2017) D. Dobler, J. Beyersmann, and M. Pauly. Non-strange weird resampling for complex survival data. Biometrika, 104(3):699–711, 2017.

- Gill (1989) R. D. Gill. Non- and Semi-Parametric Maximum Likelihood Estimators and the von Mises Method (Part 1). Scandinavian Journal of Statistics, 16(2):97–128, 1989.

- Glidden (2002) D. V. Glidden. Robust Inference for Event Probabilities with Non-Markov Event Data. Biometrics, 58(2):361–368, 2002.

- Grand and Putter (2016) M. Klinten Grand and H. Putter. Regression models for expected length of stay. Statistics in Medicine, 35(7):1178–1192, 2016.

- Harris (1987) J. Harris. QALYfying the value of life. Journal of medical ethics, 13(3):117–123, 1987.

- Jacod and Shiryaev (2003) J. Jacod and A. N Shiryaev. Limit Theorems for Stochastic Processes. Springer, Berlin, second edition, 2003.

- Lin (1997) D. Y. Lin. Non-parametric inference for cumulative incidence functions in competing risks studies. Statistics in Medicine, 16(8):901–910, 1997.

- Meilijson (1972) I. Meilijson. Limiting Properties of the Mean Residual Lifetime Function. The Annals of Mathematical Statistics, 43(1):354–357, 1972.

- Meira-Machado et al. (2006) L. Meira-Machado, J. de Uña-Álvarez, and C. Cadarso-Suárez. Nonparametric estimation of transition probabilities in a non-Markov illness–death model. Lifetime Data Analysis, 12(3):325–344, 2006.

- Pepe (1991) M. S. Pepe. Inference for Events with Dependent Risks in Multiple Endpoint Studies. Journal of the American Statistical Association, 86(415):770–778, 1991.

- Pepe et al. (1991) M. S. Pepe, G. Longton, and M. Thornquist. A qualifier Q for the survival function to describe the prevalence of a transient condition. Statistics in Medicine, 10(3):413–421, 1991.

- Pollard (1984) D. Pollard. Convergence of Stochastic Processes. Springer, New York, 1984.

- Putter and Spitoni (2018) H. Putter and C. Spitoni. Non-parametric estimation of transition probabilities in non-Markov multi-state models: The landmark Aalen–Johansen estimator. Statistical Methods in Medical Research, 27(7):2081–2092, 2018.

- Rodríguez-Girondo and Uña-Álvarez (2012) M. Rodríguez-Girondo and J. Uña-Álvarez. A nonparametric test for Markovianity in the illness-death model. Statistics in Medicine, 31(30):4416–4427, 2012.

- Titman (2015) A. C. Titman. Transition Probability Estimates for Non-Markov Multi-State Models. Biometrics, 71(4):1034–1041, 2015.

- van der Vaart and Wellner (1996) A. W. van der Vaart and J. A. Wellner. Weak Convergence and Empirical Processes. Springer, New York, 1996.

- Wangler et al. (2006) M. Wangler, J. Beyersmann, and M. Schumacher. changeLOS: An R-package for change in length of hospital stay based on the Aalen–Johansen estimator. R News, 6(2):31–35, 2006.

- Williams (1985) A. Williams. Economics of coronary artery bypass grafting. British Medical Journal (Clinical Research Edition), 291(6491):326–329, 1985.

This appendix includes the proofs of Lemma 1 and the main Theorems 1 to 3 as well as a detailed derivation of the limit covariance functions. Furthermore, it is proven that the model in the simulation Section 4 satisfies the main conditions (1)–(4).

Appendix A Asymptotic covariance functions and comments on their estimation

We begin by stating all covariance functions which are involved in the limit theorems. In particular, introducing the following covariance functions will prove to be useful:

With these abbreviations, we conveniently introduce the asymptotic covariance functions which appear in Lemma 1 of the manuscript. Their derivation in detail will be done in the next section.

The asymptotic variance-covariance functions of the Kaplan–Meier and the Aalen–Johansen estimator for different time points are well-known and therefore not listed. The derivation of and will be made explicit in Section F below. In the display above, we used . Note that these functions may be decomposed into

of which the first probability is again estimable by Kaplan–Meier or Aalen–Johansen-type estimators based on those individuals that are observed to satisfy and . Hence, consistent plug-in estimates of the above covariance function are found easily. However, the number of individuals satisfying that and that is observed might be quite small in practical applications. This could lead to a large variance of the estimators of .

Appendix B Proof of Lemma 1

The large sample properties concerning the conditional Kaplan–Meier estimator and the conditional Aalen–Johansen estimator follow from standard theory. Their variance-covariance functions are obtained in the same way. The asymptotic covariance functions between and as well as are derived in Appendix F below. For technical reasons, we consider weak convergence on the càdlàg space equipped with the supremum norm instead of the usual Skorohod metric. In case of continuous limit sample paths, weak convergence on the Skorohod and the supremum-normed càdlàg space are equivalent; cf. Gill (1989), p. 110 in Andersen et al. (1993), or p. 137 in Pollard (1984). The advantage is that the functional delta-method is available on the supremum-normed space. Additionally, the general Aalen–Johansen estimator is known to have continuous limit distribution sample paths; cf. Theorem IV.4.2 in Andersen et al. (1993). However, this may not be true for the weak limit of as because the censoring distribution may have discrete components. This problem is solved by an application of a technique as used by Akritas (1986): Each discrete censoring components is distributed uniformly on adjacent, inserted small time intervals during which no state transition can occur. Instead, all future state transitions are shifted by the preceding interval lengths. Write and , where and . The resulting weak limit sample paths of the time transformed and will be continuous and the functional delta-method is applicable to obtain the corresponding result for . Note that the values of none of these processes were modified outside the just inserted small time intervals. Finally, the projection functional, which projects a time-transformed process to the original time line, is continuous. Hence, the continuous mapping theorem eventually yields the desired central limit theorem for the process as .

It remains to give a weak convergence proof of the finite-dimensional margins of the process and to verify its tightness under the temporary assumption of continuously distributed censoring times. Combining both properties, weak convergence on follows, as indicated above.

Finite-Dimensional Marginal Distributions

Weak convergence of the finite-dimensional margins is shown by applying the functional delta-method after utilizations of the central limit theorem. The weak convergences of all finite-dimensional marginal distributions are easily obtained by the multivariate central limit theorem: For points of time, , consider in distribution, as , with th covariance entry

Similarly, in distribution, as , with th covariance entry

The convergence of both vectors even holds jointly, implying that the th entry of the covariance matrix of both limit vectors is given by

Denote by the subset of càdlàg functions with are positive and bounded away from zero, which is equipped with the supremum norm. Note that defines a Hadamard-differentiable map with Hadamard-derivative , with . This of course also implies Fréchet-differentiability on all finite-dimensional projections. Therefore, the multivariate delta-method yields the convergence in distribution

as . The asymptotic covariance matrix has th entry

Tightness

We will show tightness on the Skorohod space of càdlàg functions by showing that a modulus of continuity becomes small in probability; see Theorem 13.5 in Billingsley (1999). Remember that this property will imply weak convergence on the Skorohod space which, due to the temporary continuity of the limit processes, is equivalent to weak convergence on the supremum-normed space.

Now, for the modulus of continuity, we consider for any small the expectation

| (8) |

We start by rewriting as

Note that, in the product appearing in (8), the products of the above indicator functions with identical indices vanish for unequal time pairs and . Additionally, due to the independence of all individuals, all terms with a single separate index vanish too. Hence, by an application of the Cauchy-Schwarz inequality, the expectation in (8) is bounded above by

for all . Let denote the survival function of the censoring times and let denote the (unconditional) probability to be still under risk at time . By the temporarily continuous censoring distribution, is a continuous and non-decreasing function and thus it is suitable for an application of Theorem 13.5 in Billingsley (1999). Then the terms in the above display are not greater than

Hence, tightness in the Skorohod space of the process affiliated with the denominator of follows.

It remains to prove tightness of the numerator process. At first, we rewrite for

For later calculations, we derive products of the -indicators for different points of time:

Therefore, the expectation to be bounded for verifying tightness has the following structure:

where the inequality follows from an application of the Cauchy-Schwarz inequality. The terms in the previous display are not greater than

It remains to calculate and bound the single expectations.

holds by the same reasons as above and a similar representation holds for the other second moments. By conditions (1) to (4) in the manuscript, there is a global constant , that is independent of , such that . Similarly, as well as .

The first expectation (involving fourth moments) contains the following terms:

For the expectation, first we obtain

Similarly, we have . It remains to consider , and .

Similarly, and due to independent right-censoring.

Assume that . Otherwise, nothing needs to be shown. Thus,

Due to condition (4), there is a constant , which is independent of , such that

for a global constant . Similarly . Therefore, we conclude that

for the non-decreasing and continuous function .

All in all, we conclude that

where defines a continuous and non-decreasing function, independently of . Hence, tightness of the process follows which in turn implies convergence in distribution on the Skorohod space . Finally, proceed as indicated in the beginning of this Appendix section.

Appendix C Proof of Theorem 1

The proof of Theorem consists of an application of the functional delta-method applied to the functional which is Hadamard-differentiable at with derivative

For the asymptotic covariance function, note that both terms and vanish for .

Appendix D Proof of Theorem 2

First, the finite-dimensional, conditional marginal distributions of the estimator given are shown to be consistent, as for the corresponding marginal distributions of the limit process . This is verified via empirical process theory: Let be finitely many time points. The finite-dimensional marginals of the estimator are Hadamard-differentiable functionals of the empirical process based on

where . The empirical process is indexed by the family of functions

where the particular functions are defined as

Certainly, defines a Donsker class. The derivation of the Kaplan–Meier estimator based on parts of this empirical process has been verified in Section 3.9 of van der Vaart and Wellner (1996). This similarly holds for the Aalen–Johansen estimator under competing risks by another, final application of the Wilcoxon functional and the use of the cause-specific Nelson–Aalen estimator; see Section F below for a more detailed derivation. The proportion-type estimator is given by a simple Hadamard-differentiable functional of the empirical process indexed by the functions . Therefore, combining again all separate estimators, the functional delta-method is applicable to the bootstrap empirical process and the same Hadamard-differentiable functional as well (in outer probability); see Chapter 3.6 in van der Vaart and Wellner (1996) for details. It follows that the conditional finite-dimensional marginal distributions of converge weakly to the limit distributions of the original normalized estimator.

Second, conditional tightness in probability needs to be verified. To this end, we utilize a variant of the tightness criterion in Theorem 13.5 in Billingsley (1999), in which the involved continuous, non-decreasing function may depend on the sample size and it need not be continuous, but only point-wise convergent and asymptotically continuous. See the Appendix A.1 in the PhD thesis by Dobler (2016) or the comment on p. 356 in Jacod and Shiryaev (2003) for details. As in the first part of this appendix, we assume without loss of generality that the censoring distribution is continuous. To verify tightness, we consider the conditional version of expectation that we bounded accordingly for verifying tightness of the original, normalized estimator in the first part of this appendix. All quantities with a superscript star are the obvious bootstrap counterparts of the quantities introduced earlier. We again focus on proving tightness for the bootstrap counterparts and of and , respectively. Furthermore, the normalized, bootstrapped Kaplan–Meier estimator is well-known to be tight and the same property is easily seen for the normalized, bootstrapped Aalen–Johansen estimator under competing risks. Finally, we will apply the continuous mapping theorem in order to conclude asymptotic tightness of .

Let us abbreviate and , where is independent of . Let . Denote by a constant which may become larger along the subsequent inequalities, but which is independent of . Then, by the Cauchy-Schwarz inequality,

As shown in e.g. Dobler and Pauly (2014), we have and . Furthermore, it is easy to show that . Therefore, the expectation in the previous display is bounded above by

We apply the Cauchy-Schwarz inequality to (and similarly for the ’s) which is bounded above by . Therefore, the terms in the previous display are bounded above by

| (9) |

which we abbreviate by . Now, verifying the unconditional Billingsley criterion implies conditional tightness in probability: Suppose is a random element of for which tightness in probability given some random element shall be shown and for which it hold that: For all we have for the modulus of continuity , using the notation of Billingsley (1999), that

Then, by the Markov inequality,

Therefore, we need to find a suitable upper bound for the expectation of (9). By the Cauchy-Schwarz inequality we have the upper bound

Here, we begin by looking for a bound of

We note that each and are differences of indicator functions. In particular, we have that

Therefore, we can bound

A similar bound holds for . Thus, we have for the product

Similarly to the proof in Appendix B, we obtain the upper bound

due to conditions (1) to (4) in the main article, where the function was defined in Appendix B.

Next, we find an upper bound for

which holds for the same reasons as before. Similarly, we obtain the same upper bound for . We finally conclude that

As argued above, Theorem 13.5 in Billingsley (1999) now implies conditional tightness in probability given .

The same holds true for which, as was the case for the original estimator, is more easily shown than for and it is thus left to the reader. All in all, conditional convergence in distribution of on given in probability follows by the functional delta-method. The Gaussian limit process is the same as for the original estimator.

Appendix E Proof of Theorem 3

Consider subsequences of increasing sample sizes for which . Due to the independence of the eventual limit distribution on the specific value of , the convergence in distribution still holds under the bounded --condition. The proof follows from a two-fold application of the continuous mapping theorem to the integration and the subtraction functional as well as from the independence of both samples. If is a zero-mean Gaussian process with covariance function , then has a zero-mean normal distribution with variance

Appendix F Detailed Derivation of the Covariance Function

As stated in Theorem 1, the covariance function consists of several simpler covariance functions of which and still need to be determined. Note that, if denotes the limit Gaussian process of the normalized Aalen–Johansen estimator for the cumulative incidence function of the second risk, then

due to on . It is therefore enough to focus on the covariance function which involves the Aalen–Johansen limit. This may be derived based on the asymptotic linear representation of all three separate estimators as Hadamard-derivatives , , and , which are continuous and linear functionals, applied to an empirical process and to , respectively. More precisely, we have

Here is the empirical process based on the censoring or event times , the censoring or competing risk indicator , and as well as , where and . Finally, is the distribution of each single observed quadruple. The empirical process is indexed by , , and , . This certainly is a Donsker class; see Example 3.9.19 in van der Vaart and Wellner (1996) for a similar indexing leading to the (all-cause) Nelson–Aalen estimator. In the following part, we calculate the exact structure of the above linear expansions for the case . This suffices to determine the asymptotic covariance structure of the estimators as the covariances of the above linear functionals are the same for all .

As argued in the main article, it does not matter whether the left- or right-continuous versions of the at-risk indicators are considered. This is also true for the at risk functions involved in the Kaplan–Meier and Aalen–Johansen estimators. For technical convenience, we choose the right-continuous at-risk functions. Let , , and . The above Hadamard-derivatives are given by

Thereof, is the Hadamard-derivative of the product-integral leading to the Kaplan–Meier estimator, i.e.

cf. e.g. Lemma 3.9.30 in van der Vaart and Wellner (1996), but take notice of the additional minus sign. Here, is the continuous cumulative (all-cause) hazard function for all individuals for which . The functional is the Hadamard-derivative of the Wilcoxon functional, i.e.

cf. e.g. Example 3.9.19 in van der Vaart and Wellner (1996). Finally, is the Hadamard-derivative of , after indexing the distribution with , i.e.

From the above derivations, we have that

We proceed similarly for the Aalen–Johansen estimator

of , where now denotes the first cause-specific cumulative hazard of those individuals for which . Define . Thus, as the estimator consists of the Wilcoxon functional applied to the left-continuous version of a product integral and another Wilcoxon functional (the Nelson–Aalen estimator), we have

The tilde on top of the first Hadamard-derivative shall express the slight variation of the original functional, as we now use the left-continuous version of the integrand. Furthermore, . Hence, the previous display can be expanded to

Finally, we calculate the remaining linear functional applied to a pair of centered indicator functions that appear in the estimator :

For later calculations we note that

that , and that

where .

After this preparation, we are now able to determine the asymptotic covariance. Because of the independencies and the identical distribution structure in the asymptotic, linear representation,

We begin by considering the case for which the covariance reduces to

The round bracket in the last line equals . Hence, asymptotic independence follows in case of .

We hence continue with the case . Let and be any suitable functions. The following side calculation due to a decomposition will prove beneficial:

For a better presentation of the calculations, we split the covariance terms into two parts. First,

Thereof, the sum of the last four terms can be summarized similarly as in the case , i.e. it equals

The sum of the remaining four terms equals, after integration by parts,

Comparing these terms with those four which we derived first, we see that all integrals from to are cancelled out. Therefore, the following terms remain:

Due to , this equals

We continue by deriving the second half of the asymptotic covariance function also in case of , i.e.

We apply integration by parts to the first integral. Note that, if is the variable of integration,

Therefore, the first integral of equals

All in all, the sum of both parts and equals

which, due to , further simplifies to

Appendix G Conditions (1)–(4) in the Simulation Study

In this section we prove that the conditions (1)–(4) of the main manuscript are satisfied in the situation of Section 4 therein. Recall that the stochastic development of the process depends on the state occupied at time . Hence, conditional on and after time , is a Markov process with cumulative hazard matrix

Otherwise, if , the process subsequently is a Markov process with cumulative hazard matrix

Write and . In this conditionally homogeneous Markov set-up it follows that the matrix of transition probabilities at time is given by

where is the matrix exponential of a square matrix . Now, it is obvious that is infinitely often continuously differentiable, hence (1) and (2) are satisfied. In the same way, (3) and (4) are satisfied as well because is a Markov process conditionally on , so its state at an earlier intermediate time is irrelevant.