On a pricing problem for a multi-asset option

with general transaction costs

Abstract

We consider a Black-Scholes type equation arising on a pricing model for a multi-asset option with general transaction costs.

The pioneering work of Leland is thus extended in two different ways: on the one hand, the problem is multi-dimensional since it involves different underlying assets; on the other hand, the transaction costs are not assumed to be constant (i.e. a fixed proportion of the traded quantity). In this work, we generalize Leland’s condition and prove the existence of a viscosity solution for the corresponding fully nonlinear initial value problem using Perron method. Moreover, we develop a numerical ADI scheme to find an approximated solution. We apply this method on a specific multi-asset derivative and we obtain the option price under different pricing scenarios.

Keywords: Nonlinear parabolic differential equations, Option pricing models, Leland model, Transaction costs, Perron method, ADI splitting scheme

2010 MSC: 35K20, 35K55, 91G20, 91G60

1 Departamento de Matemática,

Facultad de Ciencias Exactas y Naturales

Universidad de Buenos Aires and

2 IMAS - CONICET

Ciudad Universitaria, Pabellón I, 1428 Buenos Aires, Argentina

E-mails: pamster@dm.uba.ar — amogni@dm.uba.ar

1 Introduction

The Black-Scholes model [3] relies on different assumptions such as constant values of volatility and interest rates, the non-existence of dividend yields, the efficiency of the markets and the non-existence of transaction costs, among others. Following Leland’s approach [15], transaction costs can be included in the pricing methodology by applying a discrete-time replicating strategy. A nonlinear partial differential equation is obtained for the option price, which is denoted by ; namely,

| (1.1) |

where is defined based upon the transaction costs function. For example, if transaction costs are defined by a constant rate , then is given by

where is the Leland number.

The original approach was extended by different authors. A discrete approximation is studied in [4] by developing a binomial option pricing model with constant transaction costs. The generalization of Leland’s methodology for a portfolio of options is presented in [9] and the existence of solution is studied in [10]. In [7], a method of upper and lower solutions is used to study the original stationary problem. Also, an analysis of the original hedging strategy is found in [6] and a modification of the strategy is considered in [16] to guarantee that the approximation error vanishes in the limit.

Different choices of transaction costs functions lead to variations on the nonlinear term of the partial differential equation. In [1], the authors propose a non-increasing linear function and find solutions for the stationary problem. In [19], the concept of transaction costs function is generalized and the so-called mean value modification of the transaction costs function is developed. This transformation allows the authors to formulate a general one-dimensional Black-Scholes equation by solving the equivalent quasilinear Gamma equation. Moreover, viscosity solutions have been studied in the nonlinear problems that arises from including transaction costs in the option pricing framework . The seminal work of [5] finds the option price by comparing the maximum utilities available to the writer leading to solve two stochastic optimal control problems. Unique viscosity solutions are found as the value functions of these problems. Moreover, the work of [2] uses a utility function with an asymptotic analysis of partial differential equations to quantify the dependence on preferences in European call option problem.

The main distinctive aspect in the above-cited works is that they all consider only one asset within the partial differential equation. In [20] and [21], the author generalizes the Leland approach in order to cover different types of multi-asset options, developing the nonlinear partial differential equation and solving numerically a list of examples.

In this work, we prove the existence of a viscosity solution for the problem of pricing a multi-asset option with a general transaction costs function. We derive the following nonlinear problem

| (1.2) |

where , is the option price, is an elliptic operator, is a nonlinear term and is the initial condition. This problem can be rewritten in terms of a nonlinear elliptic operator as

| (1.3) |

This presentation helps us to introduce the Perron method to find a viscosity solution. Indeed, in our work we show that a generalization of Leland’s condition is required such that the nonlinear operator becomes degenerate elliptic and a solution can be found. By defining properly the sub and supersolutions of problem (1.3) and recalling a comparison principle, we use Perron method to derive the existence of solution.

In the second part of the work, we develop a numerical approach in order to find a solution using an iterative method. For this purpose, the Alternating Difference Implicit (ADI) scheme is selected within the family of splitting operators. Different works [12, 13, 18, 17] study the applicability of this approach to deal with the mixed derivatives terms of the discretization. On multidimensional problems, the ADI method allows to solve efficiently the PDE problem by applying a tridiagonal matrix algorithm in comparison to the classical Crank-Nicholson scheme. In this section we provide results regarding the convergence of the numerical scheme, the sensitivity of the final output to the choice of timing parameters and the impact of the transaction costs in the option price.

The structure of the paper is as follows. In Section 2 we derive the nonlinear PDE that explains the dynamics of the option price for a multi-asset derivative considering a general transaction costs function. In Section 3 we apply all the necessary steps to prove the existence of a viscosity solution using Perron method. Finally, in Section 4 we develop the ADI framework in order to find a strong solution and price a specific multi-asset derivative.

2 PDE derivation for multiple assets and general transaction costs function

Let be the portfolio that contains of asset and an option over those assets at time . This portfolio can be represented by

| (2.1) |

If we define as the one-step variation of a process (i.e ), by applying the Itô’s formula over , we get

| (2.2) |

Transaction costs appear when calculating , which expresses the variation of the portfolio at each time . Specifically, the variation of the portfolio is represented by

| (2.3) |

where is the amount of transaction costs when buying or selling assets of . By taking , we obtain

| (2.4) |

Following the approach in [19], it is seen that

| (2.5) |

where is the transaction costs function. By defining to be the expected value of the change of the transaction costs per unit time interval and price , we see that

Thus, we approximate the transaction costs by the expected value of the transaction costs function applied to the amount of assets bought or sold and multiplied by these amount again. This value is then multiplied by the price of asset in order to get a transaction cost in money terms.

| (2.6) |

From the assumption and (2.6), we obtain

| (2.7) |

where .

Equation (2.7) is the nonlinear PDE that represents the behaviour of the option price for a multi-asset option when defining a general transaction costs function. In order to get the complete expression of the PDE, we have to calculate . From previous steps we know that

taking only the terms with order . Noting that

with being a standard normal variable, we find that

Setting , we obtain that with

| (2.8) |

where is the correlation parameter between and . Therefore,

| (2.9) |

Using (2.9) in (2.7), we find the following nonlinear PDE which models the dynamic of a multi-asset option.

| (2.10) |

3 Existence of solution for the resulting PDE

3.1 Defining the nonlinear problem

Let be a measurable bounded transaction costs function such that , and let be such that for every . Moreover, we denote and . Let us define to be the nonlinear operator

| (3.1) | ||||

| (3.2) |

where is given by

| (3.3) |

where is the correlation parameter between and , both standard normal variables. Moreover, let us denote to be the following parabolic operator

| (3.4) |

Then, we define the nonlinear PDE for the problem of pricing a multi-asset option with general transaction costs as of

| (3.5) |

Our objective is to find a viscosity solution of problem (3.1). For this purpose, we will rewrite problem (3.1) to match with the notation of [11]. Hence, we redefine our nonlinear parabolic equation as

| (3.6) |

where

| (3.7) |

Remark 3.1.

Equation (3.6) can be rewritten following a matricial form. If we denote the matrix as

| (3.8) |

then the function can be set as

| (3.9) |

For the nonlinear term that correspond to the function we first note that the value of is equivalent to the i-th term of the diagonal of the product , i.e.

| (3.10) |

Then, the function noted in a matricial form as of

| (3.11) |

3.2 Degenerate Ellipticity and Leland’s condition

3.2.1 Deriving the conditions

We are going to prove the existence of a viscosity solution of problem (3.6) using Perron method. The main idea of the method is to construct a subsolution and a supersolution of the nonlinear parabolic equation such that . Moreover, it is possible to construct a subsolution lying between and and see that the lower semi-continuous envelope of the subsolution is a supersolution. Before applying Perron method, we need to set different conditions on the nonlinear operator . Let us start by presenting the definition of degenerate ellipticity. For this purpose, we will denote as the space of N-dimensional square symmetric matrices.

Definition 3.1.

A nonlinear function is degenerate elliptic if

| (3.12) |

Given the definition of degenerate ellipticity we have to set the correspondent conditions such that the nonlinear function follows Condition (3.12). Let us start by denoting the differential of function with respect to the second derivative component as

| (3.13) |

By Definition 3.1, given a positive definite matrix , we want to see that

If this condition is fulfilled, we can use the mean value theorem to prove that operator is degenerate elliptic so

| (3.14) | ||||

where and is a positive definite matrix.

Let us recall the Leland condition which is present in the unidimensional problem with a constant transaction costs function. The aim of the this condition is in fact to define a degenerate elliptic operator such that the matrix of coefficients that correspond to the second derivatives is definite positive. In our work, the generalized Leland condition will act as the same and will be deduced from the following two Lemmas.

The first Lemma shows that, if the differential matrix is symmetric, evaluating the differential on any definite positive matrix is equivalent to calculating the trace of the product between the differential matrix and the correspondent definite positive matrix.

Lemma 3.2.

Let be a positive definite matrix and the differential matrix with respect to component Y. Then,

Proof.

Let us see that the result follows by using the definition of the Frobenius inner product. From the definition of the the trace of the product between and the positive definite matrix and the symmetry of matrix we have that

Now, we can arrange terms so that

∎

The second Lemma states that we can characterize the sign of the eigenvalues of the differential matrix in terms of the sign of the trace of the product between and a definite positive matrix .

Lemma 3.3.

Let be a positive definite matrix. Then is negative definite if and only if for all .

Proof.

Let us start observing that as is a symmetric matrix, there exists a diagonal matrix and a change of basis matrix such that . Then, we have that

| (3.15) |

If we denote , the previous equation can be rewritten as

| (3.16) |

where is a positive definite matrix. Using the last equality we can prove our statement. If for all , let us choose a sparse matrix such that column corresponds to the standard vector . Then, and . Using the fact that , we deduce that each .

Let us now suppose that is negative definite. Then,

| (3.17) |

as each are negative and each are positive.

∎

Both Lemmas 3.2 and 3.3 can be resumed in the following line: If the differential matrix is symmetric, for all matrix the following equivalences are valid

Recalling (3.14), the matrix is definite positive so by discarding the dependencies, the inequality becomes

| (3.18) |

Hence, the nonlinear operator is degenerate elliptic if the differential matrix is symmetric definite negative. In the following section we will see that the condition of being symmetric definite negative is the generalization of the Leland condition defined for the unidimensional problem with constant transaction costs.

3.2.2 Differential Matrix calculation

In this section we perform the calculations of the differential matrix with respect to the second derivatives of the nonlinear term . Let us recall Equation (3.9) such that

| (3.19) |

Then, by applying standard calculations and discarding function dependencies, we have that

| (3.20) |

The first derivative follows recalling the linearity of the trace function and the symmetry of matrix . Then,

| (3.21) |

The second derivative involves applying the product rule on the transaction costs term. Then,

| (3.22) |

The above calculation can be solved by analysing two derivatives. The first one correspond to the function defined in (3.3). The calculation of the derivative of this term is done in A and is given by

| (3.23) |

The second derivative corresponds to the derivative of the transaction costs function with respect to matrix . Again, the complete calculation is presented in A. Then, the derivative with respect to matrix is equal to

| (3.24) |

Now, we can write Equation (3.20) as

| (3.25) |

Equation (3.25) defines the final state of the differential matrix of the nonlinear parabolic operator with respect to the component of the second derivatives. The generalized Leland’s condition found in Lemmas 3.2 and 3.3 requires that the differential matrix is definite negative. In fact, we can check that this condition reduces to the original Leland’s condition when fixing and the function of transaction costs as constant.

Remark 3.4.

Let us show that effectively our condition reduces to Leland’s condition in the unidimensional case with constant transaction costs. For this purpose, we assign , and as in the unidimensional case. Then,

| (3.26) |

If we apply this definitions on Equation (3.25), we get that

| (3.27) |

Then, is negative if and only if

| (3.28) |

3.3 Perron method for existence of solution

Let us start this section by setting the framework to apply the well-known Perron method to derive the existence of a viscosity solution. We will first apply a change of variables so that the nonlinear operator is defined with constant coefficients. Then, we apply the change of variables

so that the nonlinear operator becomes

| (3.29) |

and the nonlinear function becomes

| (3.30) |

with

| (3.31) |

| (3.32) |

where is the initial condition. Hence, the main theorem of this work is defined as follows

Theorem 3.5.

Assume that the differential matrix with respect to the Hessian matrix of the nonlinear operator is negative definite. Then, the problem (3.3) has at least one viscosity solution.

Before passing to the proof of the theorem, we are going to state some important definitions that will be used afterwards. Given an open set , we recall that is lower semi-continuous (LSC) or upper semi-continuous (USC) at if for all sequences ,

| (LSC) | ||||

Moreover, we define the lower semi-continuous envelope of V as the largest lower semi-continuous function lying below and the correspondent upper semi-continuous envelope of V as the smallest upper semi-continuous function lying above .

Let us continue by presenting the definition of viscosity solutions, which are the type of solutions that we will look for. Let us recall and a function . Then, we have the following definitions.

Definition 3.6.

is a subsolution of (3.3) if is upper semi-continuous and if, for all and all the test functions such that in a neighbourhood of and , we have that

| (3.33) |

is a supersolution of (3.3) if is lower semi-continuous and if, for all and all the test functions such that in a neighbourhood of and , we have that

| (3.34) |

Finally, is a solution of (3.3) if it is both a sub and supersolution.

Now we can present Perron method to find a solution of problem (3.3). First of all, we require that the nonlinear operator is degenerate elliptic. Then, Perron method is defined as follows.

Theorem 3.7.

Assume is a subsolution of problem (3.3) and is a supersolution of problem (3.3) such that . Suppose also that there is a subsolution and a supersolution of problem (3.3) that satisfy the boundary condition . Then,

| (3.35) |

In order to apply the Perron method we first have to set a subsolution and supersolution of problem (3.3). Then, we have to construct a maximal subsolution such that it lies between both sub and supersolutions. Finally, we have to define the proper comparison principle such that the boundary condition defined in Theorem 3.7 holds.

Hence, let us start by recalling the equivalent ”Black-Scholes” linear problem. If we denote the linear elliptic operator as

| (3.36) |

then there exists a unique solution of the problem

| (3.37) |

Based on the existence of this unique solution , we will construct our sub and supersolutions. Then, the following Lemma presents both sub and supersolutions of problem (3.3).

Lemma 3.8.

Let be the nonlinear elliptic operator defined in Equation (3.29). Then the following functions are sub and supersolutions of problem (3.3).

where is the unique solution of problem (3.37) and is a positive constant such

| (3.38) |

Proof.

Let us see that the is a subsolution of (3.3). Firstly, the upper semi-continuity of follows from the continuity of the solution . Let us see that for all test functions such that in a neighbourhood of and , it follows that is negative.

Let be a test function such that . Then, we have

Now we use the condition of degenerate ellipticity of the operator . This condition implies that

where the last inequality holds using Condition 3.38.

Let us now prove that is in fact a supersolution. In this case, the lower semi-continuity follows from the continuity of the solution . Let us see that for all test functions such that in a neighbourhood of and , it follows that is positive.

Let be a test function such that . Then, we have that

Now we use the condition of degenerate ellipticity of the operator and Condition 3.38. Both conditions imply that

Then, is a supersolution of problem (3.3). ∎

Remark 3.9.

By definition, it remains valid that .

Remark 3.10.

Given the ”Black-Scholes” solution , the nonlinear term is bounded for every in . Based on the construction of the replicant portfolio, it is observed that the transaction costs are proportional to the second derivatives of the option. Moreover, from the solution of the linear problem, we know that the second derivatives tend to zero when the prices are too small or too large. Then, in those scenarios, the replicant potfolio is almost not rebalanced so that a little amount of stocks are traded resulting on a small contribution of the transaction costs function.

Following Lemma 2.3.15 from [11], there exists a function such that and is a subsolution of (3.3) and is a supersolution of (3.3). Then, to finally prove Theorem 3.5, we need to confirm that . For this purpose, we will consider the comparison principle stated in [11].

Proposition 3.1 (Comparison Principle).

Hence, our last Lemma is stated below:

Lemma 3.11.

Proof.

Let us first observe that the inequality holds by definition of the semi-continuous envelopes. For the other inequality let us recall and defined in Lemma 3.8 and, using the continuity of the linear solution , we have that

In particular, in the parabolic boundary, we find that both sub and supersolutions are equal to . Then, it is valid that

| (3.39) |

Moreover, for Lemma 2.3.15 from [11], . Using this result and the previous inequality, it follows that

| (3.40) |

Finally, the expected inequality is obtained by the comparison’s principle result. ∎

4 Numerical Implementation

4.1 Numerical Framework

In this section we derive a numerical framework that is used to find an approximate solution of problem (1.2). This solution will help us to understand how the presence of transaction costs affects the pricing of a specific financial option. With this aim, we develop an iterative scheme such that on every step, an approximate solution is found. Each step is then repeated until the convergence of the scheme. By recalling the nonlinear problem, we propose the following iterative process

| (4.1) |

with , and as defined in Equation (3.3). For numerical convenience, we approximate the original smooth domain by a discrete one , setting and in order to cover a set of feasible stock prices. The step of the spatial variables is uniformly set as , being the number of grid points in the x- direction. The step of the temporal variable is also uniformly set as being the number of grid points in the - direction. We define as the step of the iterative problem and, given , as each of the temporal steps. Hence, we define the solution to the -step iterative problem as where and .

At each step , we have to solve a linear problem involving both second and mixed derivatives of . If we apply directly a finite difference scheme, the invertible matrix would not be tridiagonal as mixed spatial derivatives have to be considered. Hence, we apply an Alternating Direction Implicit (ADI) method with a Finite Difference approach (FD).

We follow the steps presented in the work of [14] to determine the two stages of the procedure. The main idea of the ADI method is to generate an intermediate step between steps and . The first half step is taken implicitly in the x-direction and explicitly in the y-direction. The other half step is taken implicitly in the y-direction and explicitly in the x-direction.

In the first place, we split the temporal derivative as shown on (4.2)

| (4.2) |

Then, we discretize the lineal operator

setting

As in section 2.1 of [14], we split the discretization of the operator between

and

obtaining a two-stage full scheme

As the problem (4.1) contains the linear function , we add this term on the second stage of the procedure by redefining .

The proposed framework is used to calculate first and then . The most important gain with the ADI method is that it only requires the solution of two tridiagonal sets of equations at each time step.

4.2 Numerical Results

In order to implement the framework proposed in section 3, we select a type of multi-asset option and a transaction costs function. First, we price a best cash-or-nothing option call on two assets. This option pays out a predefined cash amount if assets or are above or equal to the strike price . The closed-form formula is presented on [8] as

| (4.3) | ||||

where and are the stock prices, and are the volatilities, is the correlation between both assets, is the maturity and is

Second, given the nonlinear function defined on (3.30), we choose an exponential decreasing transaction costs function defined as

for each asset . Hence, by recalling (2.9), we can see that

Then,

| (4.4) |

Table 1 presents the parameters chosen for the numerical implementation. Three different tests were then applied by varying the values of the stocks price, volatility, interest rate and strike among others.

| Parameters | Testing 1 | Testing 2 | Testing 3 | |||

|---|---|---|---|---|---|---|

| Asset 1 | Asset 2 | Asset 1 | Asset 2 | Asset 1 | Asset 2 | |

| year | year | year | ||||

We analyze different aspects of the ADI algorithm implemented and the dynamics of the general transaction cost model proposed. We focus on the following three points:

-

1.

Measure the impact of transaction costs in the option price.

-

2.

Given an optimal number of iterations such that convergence is achieved, analyze the sensitivity of the final output to the choice of .

-

3.

Given the iteration procedure proposed in (4.1), determine the optimal number of such that the convergence is achieved and how the error diminishes as more steps are added.

4.2.1 Transaction Costs impact

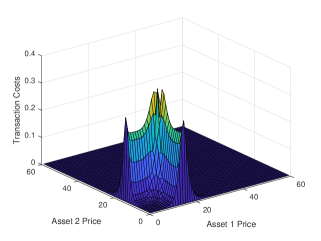

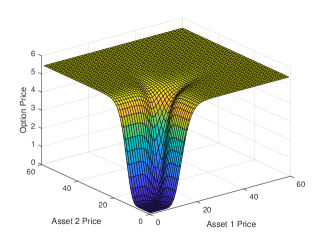

Figure (1) to Figure (3) present the results for both transaction costs function and option price with transaction costs at . By recalling the transaction costs function in (4.2) it can be noted that the costs are proportional to the assets spot price, the size of the second derivatives (i.e. Gamma) of the option price and the volatilities of each asset.

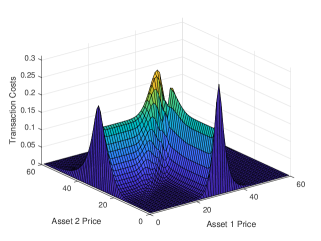

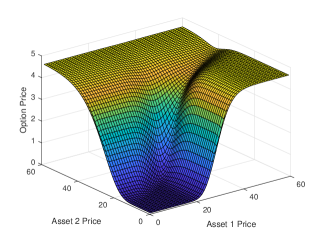

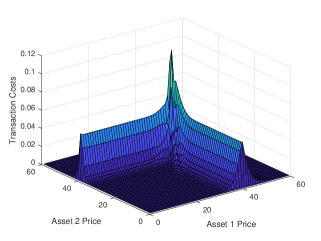

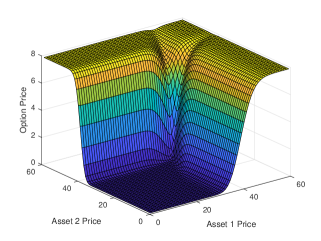

Testing 1 is defined based on a strike at with a premium paid at . Figure (1) shows an exponential transaction costs function where the maximum is reached around the strike value. This behavior is expected as the maximum of Gamma is found near the at-the-money price. As these derivatives converge to zero when deep out-of-the-money or in-the-money, the transactions costs function vanishes. Figure (1) describes the dynamics of the option price when considering the transaction costs function.

The results for Testing 2 framework are presented in Figure (2). It is defined a strike value at , a premium paid at and with two low volatile assets. The transaction costs function presented in Figure (2) shows a similar increasing pattern on its value up to the at-the-money region. Moreover, the higher volatilty of Asset 2 is observed by noting that transaction costs are higher when fixing a price for Asset 2 in comparison with Asset 1. As the option gets out-of-the-money, the shape of the transaction costs function becomes more symmetric and smoother.

Testing framework 3 is presented on Figure (3). Both assets are defined to have the same volatility but almost uncorrelated. The strike price is fixed at and the premium paid is equal to . The symmetry observed in both Figures (3) and (3) are expected due to the design of the testing. Again, the maximum of the transaction costs function is reached when the prices are near the strike value and the converge to zero is seen when the option is deeper out-of-the-money or in-the-money. The option prices reflect the complementary pattern by showing a decrease in its value when the option is near the strike price.

4.2.2 Sensitivity of the option to changes in

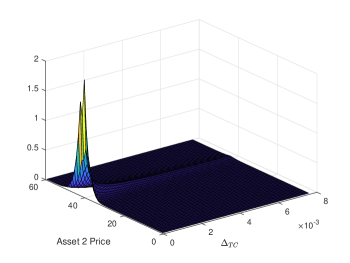

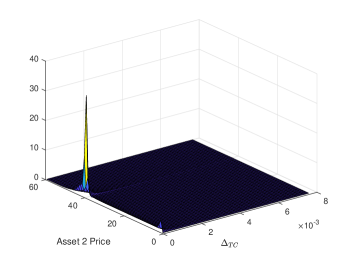

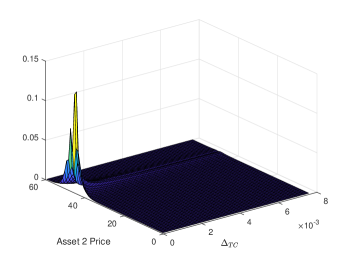

In this section we study the sensitivity of the option price to changes in the size of the time-step for rebalancing the replicant portfolio. By observing Equation (4.2), it can be seen that the transaction costs function tends to infinity if tends to zero. Hence, we expect to see this results in the numerical testing. For this purpose, we ran Testing 2 framework under possible values of ranging from (approximately rebalancing every minutes) to (approximately rebalancing every years). The results can be observed in Figures 4 and 5.

Figure 4 presents two different plots which show two states of the option price. In the panel on the left side it can be observed how the transaction costs behave when the price of Asset 1 is equal to and the parameter . It can be noted that the maximum value is reached at-the-money with a transaction cost of almost . This maximum is also reached when is minimum. When the option becomes deeper in-the-money and out-of-the-money and increases, transaction costs tend to zero. A similar pattern is observed in the figure on the right side. The main difference resides on how the transaction costs highly increase as the Asset 1 price is set as of . As Gamma is maximum near the at-the-money moneyness of the option, transaction costs explode near this pricing area. As it can be seen, the costs are of when both prices are set as . This will be the case in which rebalancing is done too often so that the option price becomes negative due to the high amount of transaction costs payed.

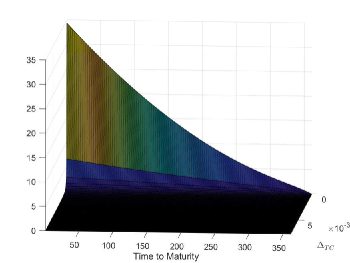

The plot of the left side of Figure 5 shows the same dynamics for the case when Asset 1 price is equal to . These dynamics are similar to the one observed in the plot of the left side of Figure 4. As Gamma decreases when prices are to low or to high, transaction costs present the usual spike near the strike value. Moreover, this costs tend to zero as becomes larger and rebalancing is done less periodically. The plot on the right helps us to understand how far can the transaction costs increase. For this purpose, we fixed the prices of both assets as of and . Then, we plotted the value of the transaction costs with respect to its time to maturity and the size of . It can be observed that when , transaction costs are near to zero as the option price is the predefined payoff. As time passes and the payoff is discounted, transaction costs increases as Gamma increases. When we reach , transaction costs grow up to . This result helps us to confirm the following expected conclusion: As the frequency of rebalancing of the replicant portfolio increases, transaction costs increase such that after a certain point of time, the option price turns into negative and the model becomes ill-posed.

4.2.3 Convergence Analysis

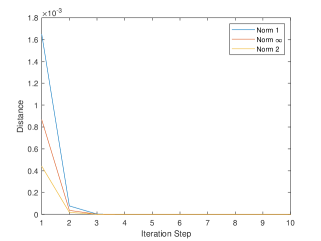

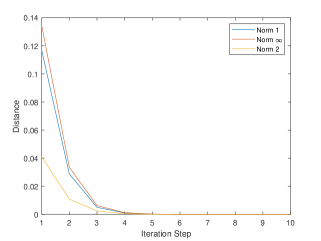

The third item of the previous list involves measuring the convergence of the iterative framework in terms of the differences between consecutive solutions. Our approach will follow from the observation that the result of each iteration correspond to a square matrix. Hence, fixing the last time step , we calculate the distance between two consecutive final results. For this purpose, we use three different p-norms matrix which are: the norm, the norm and the norm. In summary, for each step and solution , we calculate

| (4.5) |

Our objective is to see that this distance tends to zero as increases. Figure (6) to (8) present the plots of the results for the three scenarios. The figures plot the distance between two consecutive solutions against the iteration step . In the right side, we provide a table with all the numerical results up to iteration . In the first case, it can be seen that the three norms exponentially decrease to zero and, between iteration and , convergence is achieved. In the second case, convergence is achieved even faster as by step , the distance between both consecutive results is of order . The third case is similar as the first scenario by noting that convergence is achieved at iteration with a distance between consecutive solutions of order .

‘

| Iteration | Norm 1 | Norm 2 | Norm |

|---|---|---|---|

| 1 | 0.2727 | 0.1120 | 0.5187 |

| 2 | 0.1162 | 0.0738 | 0.3024 |

| 3 | 0.0442 | 0.0403 | 0.1460 |

| 4 | 0.0196 | 0.0189 | 0.0676 |

| 5 | 0.0076 | 0.0076 | 0.0267 |

| 6 | 0.0028 | 0.0027 | 0.0090 |

| 7 | 8.8E-4 | 8.6E-4 | 0.0027 |

| 8 | 2.5E-4 | 2.5E-4 | 7.5E-4 |

| 9 | 8.1E-5 | 6.7E-5 | 1.9E-4 |

| 10 | 2.3E-5 | 1.6E-5 | 4.5E-5 |

| Iteration | Norm 1 | Norm 2 | Norm |

|---|---|---|---|

| 1 | 0.0017 | 4.4E-4 | 8.6E-4 |

| 2 | 7.7E-5 | 1.8E-5 | 3.6E-5 |

| 3 | 2.6E-5 | 6.9E-7 | 1.2E-6 |

| 4 | 8.3E-8 | 2.1E-8 | 3.6E-8 |

| 5 | 2.4E-9 | 6E-10 | 9E-10 |

| 6 | 6E-11 | 1E-11 | 2E-11 |

| 7 | 1E-12 | 3E-13 | 5E-13 |

| 8 | 2E-14 | 8E-15 | 1E-14 |

| 9 | 7E-16 | 2E-16 | 2E-16 |

| 10 | 3E-16 | 1E-16 | 1E-16 |

| Iteration | Norm 1 | Norm 2 | Norm |

|---|---|---|---|

| 1 | 0.1169 | 0.0410 | 0.1344 |

| 2 | 0.0287 | 0.0108 | 0.0335 |

| 3 | 0.0050 | 0.0024 | 0.0062 |

| 4 | 0.0010 | 4.8E-4 | 0.0012 |

| 5 | 1.7E-4 | 8.6E-5 | 2.0E-4 |

| 6 | 2.6E-5 | 1.4E-5 | 3.0E-5 |

| 7 | 3.7E-6 | 2.1E-6 | 4.2E-6 |

| 8 | 5.0E-7 | 3.0E-7 | 5.5E-7 |

| 9 | 6.7E-8 | 4.0E-8 | 6.9E-8 |

| 10 | 8.5E-9 | 5.0E-9 | 8.3E-9 |

5 Conclusion

In this paper we studied the nonlinear partial differential equation that explains the dynamic of a financial option under a Black-Scholes’ model with transaction costs. We extended the general literature on this subject by generalizing the dimension of the option (i.e multi-asset option) and allowing different transaction costs function. Following Perron methodology, we proved the existence of a viscosity solution by finding a proper set of sub and supersolutions of the original problem. Furthermore, we developed a numerical procedure to find an approximate strong solution by following an iterative method. For this purpose, an ADI scheme was developed in order to deal with mixed derivatives and to work under a finite difference approach. Nonetheless, we provided numerical examples by setting different possible asset prices, volatilities and interest rates among others to study how the ADI framework performs and how sensitive the output is to changes in the delta hedging time step. Different expected results are observed after running the simulations. Firstly, as transaction costs are proportional to the second derivatives of the option price, the transaction costs function reaches its maximum near the at-the-money region. Secondly, it is seen that the transaction costs function explodes when the frequency of rebalancing the replicant portfolio tends to infinity (and goes to zero). Finally, we observe that given the three proposed testing frameworks, the iterative method converges after less than seven iterations.

6 Acknowledgement

This work was partially supported by project CONICET PIP 11220130100006CO and project UBACYT 20020160100002BA.

Appendix A Differential matrix calculation steps

Result (3.21) follows from these steps:

| (A.1) |

Result (3.23) follows from these steps:

| (A.2) |

If we denote

| (A.3) |

then, result (3.24) follows from these steps:

| (A.4) |

References

- [1] P Amster, CG Averbuj, MC Mariani, and D Rial. A Black–Scholes option pricing model with transaction costs. Journal of Mathematical Analysis and Applications, 303(2):688–695, 2005.

- [2] Guy Barles and Halil Mete Soner. Option pricing with transaction costs and a nonlinear black-scholes equation. Finance and Stochastics, 2(4):369–397, 1998.

- [3] Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. The Journal of Political Economy, pages 637–654, 1973.

- [4] Phelim P Boyle and Ton Vorst. Option replication in discrete time with transaction costs. The Journal of Finance, 47(1):271–293, 1992.

- [5] Mark HA Davis, Vassilios G Panas, and Thaleia Zariphopoulou. European option pricing with transaction costs. SIAM Journal on Control and Optimization, 31(2):470–493, 1993.

- [6] Peter Grandits and Werner Schachinger. Leland’s approach to option pricing: The evolution of a discontinuity. Mathematical Finance, 11(3):347–355, 2001.

- [7] MR Grossinho and E Morais. A note on a stationary problem for a Black-Scholes equation with transaction costs. Int. J. Pure Appl. Math, 51:579–587, 2009.

- [8] Espen Gaarder Haug. The complete guide to option pricing formulas. McGraw-Hill Companies, 2007.

- [9] T Hoggard, AE Whalley, and P Wilmott. Hedging option portfolios in the presence of transaction costs. Advances in Futures and Options Research, 7(1):21–35, 1994.

- [10] Hitoshi Imai, Naoyuki Ishimura, Ikumi Mottate, and Masaaki Nakamura. On the Hoggard-Whalley-Wilmott equation for the pricing of options with transaction costs. Asia-Pacific Financial Markets, 13(4):315–326, 2006.

- [11] Cyril Imbert and Luis Silvestre. An introduction to fully nonlinear parabolic equations. In An introduction to the Kähler-Ricci flow, pages 7–88. Springer, 2013.

- [12] KJ In’t Hout and S Foulon. Adi finite difference schemes for option pricing in the Heston model with correlation. International journal of numerical analysis and modeling, 7(2):303–320, 2010.

- [13] KJ In’t Hout and BD Welfert. Stability of ADI schemes applied to convection–diffusion equations with mixed derivative terms. Applied numerical mathematics, 57(1):19–35, 2007.

- [14] Darae Jeong and Junseok Kim. A comparison study of ADI and operator splitting methods on option pricing models. Journal of Computational and Applied Mathematics, 247:162–171, 2013.

- [15] Hayne E Leland. Option pricing and replication with transactions costs. The Journal of Finance, 40(5):1283–1301, 1985.

- [16] Emmanuel Lepinette. Modified Leland’s Strategy for a Constant Transaction Costs Rate. Mathematical Finance, 22(4):741–752, 2012.

- [17] S McKee and AR Mitchell. Alternating direction methods for parabolic equations in two space dimensions with a mixed derivative. The Computer Journal, 13(1):81–86, 1970.

- [18] S McKee, DP Wall, and SK Wilson. An alternating direction implicit scheme for parabolic equations with mixed derivative and convective terms. Journal of Computational Physics, 126(1):64–76, 1996.

- [19] Daniel Ševčovič and Magdaléna Žitňanská. Analysis of the nonlinear option pricing model under variable transaction costs. Asia-Pacific Financial Markets, pages 1–22, 2016.

- [20] Valeri Zakamouline. Hedging of option portfolios and options on several assets with transaction costs and nonlinear partial differential equations. International Journal of Contemporary Mathematical Sciences, 3(4):159–180, 2008.

- [21] Valeriy Zakamulin. Option pricing and hedging in the presence of transaction costs and nonlinear partial differential equations. Available at SSRN 938933, 2008.