Tests for qualitative features in the random coefficients model

Abstract

The random coefficients model is an extension of the linear regression model that allows for unobserved heterogeneity in the population by modeling the regression coefficients as random variables. Given data from this model, the statistical challenge is to recover information about the joint density of the random coefficients which is a multivariate and ill-posed problem. Because of the curse of dimensionality and the ill-posedness, pointwise nonparametric estimation of the joint density is difficult and suffers from slow convergence rates. Larger features, such as an increase of the density along some direction or a well-accentuated mode can, however, be much easier detected from data by means of statistical tests. In this article, we follow this strategy and construct tests and confidence statements for qualitative features of the joint density, such as increases, decreases and modes. We propose a multiple testing approach based on aggregating single tests which are designed to extract shape information on fixed scales and directions. Using recent tools for Gaussian approximations of multivariate empirical processes, we derive expressions for the critical value. We apply our method to simulated and real data.

Keywords:

Gaussian approximation; mode detection; monotonicity; multiscale statistics; shape constraints; Radon transform; ill-posed problems.

1 Introduction

In the random coefficients model, i.i.d. random vectors are observed, with a -dimensional vector of design variables and

| (1.1) |

The unobserved random coefficients are i.i.d. realizations of an unknown -dimensional distribution with Lebesgue density Design variables and random coefficients are assumed to be independent. The statistical task is to recover properties of the joint density which is assumed to belong to some nonparametric class. In this work, we derive tests for increases and modes of

For the random coefficients model simplifies to nonparametric density estimation. For recovery of is an inverse problem with ill-posedness depending on the distribution of the design vectors If the design is sufficiently regular, the inverse problem is mildly ill-posed. Otherwise, the model can be severely ill-posed or even be non-identifiable. In this work, we study the mildly ill-posed regime and consider in particular the random coefficients model with random intercept

| (1.2) |

which can be obtained from (1.1) setting almost surely.

Random coefficients models appear in econometrics and epidemiology and are used to model unobserved heterogeneity in the population. While the standard linear regression model accounts for unobserved heterogeneity only by an intercept that varies across the population, the random coefficients model allows in addition that different individuals have different slopes. Applications in epidemiology are considered by Greenland, (2000); Gustafson and Greenland, (2006). In economics, random coefficients models are frequently used to evaluate panel data, cf. Hsiao, (2014) or Hsiao and Pesaran, (2004), Chapter 6, for an overview. Modeling and estimating consumer demand in industrial organization and marketing often makes use of random coefficients Berry et al., (1995); Petrin, (2002); Nevo, (2001); Berry and Pakes, (2007); Dubé et al., (2012). In all these works, parametric assumptions on are imposed. Recently, nonparametric approaches for random coefficients became popular in microeconometrics Hoderlein et al., (2010); Masten, (2017); Hoderlein et al., (2015); Dunker et al., (2017), frequently combined with binary choice Ichimura and Thompson, (1998); Gautier and Hoderlein, (2012); Gautier and Kitamura, (2013); Masten and Torgovitsky, (2014); Dunker et al., (2013); Fox and Gandhi, (2016); Dunker et al., (2018), among others.

The random coefficients model also includes quantum homodyne tomography. In this case, we observe an angle and

| (1.3) |

with i.i.d. random variables which are unobserved and independent of The angles can be chosen by the experimenter and are typically uniform on The interest is in reconstruction of the Wigner function which takes the role of the joint density of Because and are not jointly observable, the Wigner function can take negative values. For more on quantum homodyne tomography and the Wigner function, see Butucea et al., (2007).

We propose a nonparametric test for shape information of the joint density in the random coefficients model. The focus will be on a test for directional derivatives and modes. The nonparametric estimation theory for has been developed in Beran and Hall, (1992); Beran et al., (1996); Feuerverger and Vardi, (2000); Hoderlein et al., (2010). Due to the ill-posedness of the problem and the curse of dimensionality induced by pointwise estimation rates are slow. The reason is that small perturbations in the signal are indistinguishable given the data. Nevertheless, we can get good detection rates for larger features, such as an accentuated mode or a strong increase in the joint density along some direction. From a practical point of view, the relevant information regarding an unknown density is typically its shape rater than its precise, full reconstruction. It is therefore essential to recover increases/decreases and the modes of a density. If, say, two modes in the joint density of two random quantities are detected, this indicates that two different groups can be identified. Hence, shape information allows to interpret a given dataset.

Larger features of the density will also be discovered by a nonparametric estimator even if it suffers from slow pointwise convergence. There are, however, two important reasons why a testing approach might be more appropriate. Firstly, with a significance test of level we can conclude that with probability a detected feature is not an artifact. Secondly, for an estimator we need to pick one bandwidth or smoothing parameter while detection of different features might require different bandwidth choices depending on the size of the hidden features themselves. Indeed, a short and steep increase will be best detected on a small scale whereas for finding a longer and less strong increase the choice of a larger bandwidth is beneficial. Using multiple testing methods, it is possible to combine a whole range of smoothness parameters into one test and to adapt to different shapes of features.

We construct a so called multiscale test, aggregating single tests on different scales and directions. Multiscale tests can be viewed as a multiple testing procedure specifically designed for nonparametric models. Given a model, the theoretical challenge is to prove that a multiscale statistic can be approximated by a distribution free statistic which is independent of the observations. This allows us then to compute quantiles and to find approximations for the critical values of the multiscale statistic. So far, qualitative feature detection based on multiscale statistics has been studied for various nonparametric models, including the Gaussian white noise model Dümbgen and Spokoiny, (2001), density estimation Dümbgen and Walther, (2008) and deconvolution Schmidt-Hieber et al., (2013). In multivariate settings the classical KMT approximation suffers from the curse of dimensionality which then leads to very restrictive conditions on the usable scales. Instead, very recent results on Gaussian approximations of suprema of multivariate empirical processes developed by Chernozhukov et al., (2017) can be used (Eckle et al., 2017a, ; Proksch et al.,, 2016, in the context of multivariate deconvolution and multivariate linear inverse problems with additive noise, respectively). In this work, we extend these techniques. The main difficulties are twofold. First, we need to derive specific properties of the inverse Radon transform for general dimension . Second, in contrast to the other works on multiscale inference, no distribution free approximation can be obtained and we therefore need to study the approximating process if several unobserved functions are replaced by estimators.

In order to study the power of the multiscale test, a theoretical detection bound and numerical simulations are provided. The theoretical result gives conditions under which a mode can be detected. In a numerical simulation study, we investigate the power of the test for increases/decreases along some direction and mode detection in dependence on the sample size and the design variables. We also analyze real consumer demand data from the British Family Expenditure Survey.

Let us briefly summarize related literature on testing in the random coefficients model. Under a parametric assumption on the density Beran, (1993) considers goodness-of-fit testing and Swamy, (1970); Andrews, (2001) test whether some of the random coefficients are deterministic. The only test based on a nonparametric assumption was proposed recently by Breunig and Hoderlein, (2018). It allows to assess whether a given set of data follows the random coefficients model.

This paper is organized as follows. In Section 2, we describe the connection between the random coefficients model and the Radon transform. Rewriting the model as an inverse problem in terms of the Radon transform reveals the ill-posed nature of the model. This allows us to construct and to analyze the multiscale test in Section 3. In this part we also derive the asymptotic theory of the estimator and obtain theoretical detection bounds. In Section 4 the test is studied for simulated data. As a real data example, consumer demand is analyzed in Section 5. Proofs and technicalities are deferred to a supplement. An R package and Python code is available as a supplement as well, https://arxiv.org/abs/1704.01066.

Notation: Throughout the paper, vectors are displayed by bold letters, e.g. Inequalities between vectors are understood componentwise. The Euclidean norm on is denoted by and the corresponding standard inner product by We further denote by the standard ON-basis of the -dimensional Euclidean space, denotes the unit sphere in and we write for the cylinder . Furthermore, we write for any direction . For two positive sequences or mean that for some positive constant for all As usual, we write if and

2 The random coefficients model as an inverse problem

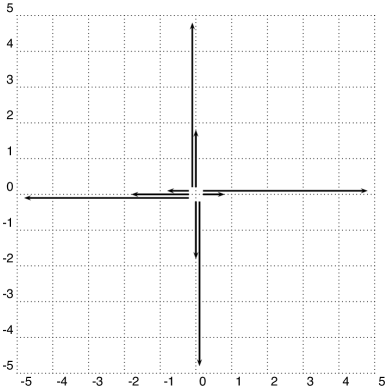

The random coefficients model can be written in terms of the Radon transform (cf. Beran et al.,, 1996). This allows us then to interpret the model as an inverse problem. In this section, we summarize the main steps and review relevant results on the inversion of the Radon transform. Let denote the -Sobolev space. The Radon transform is the operator with

![[Uncaptioned image]](/html/1704.01066/assets/x1.png)

and the surface measure on the -dimensional hyperplane . The Radon transform maps therefore a function to all its integrals over hyperplanes parametrized by The figure above shows the parametrization in two dimensions.

For the connection between the Radon transform and the random coefficients model (1.1) consider the normalized observations

The random vectors take values in the -dimensional sphere . In the random coefficients model with intercept (1.2), is always in the upper hemisphere, i.e. the first component of is positive. In this case, we extend the distribution of to the whole sphere by randomizing the signs of the design variables. For this purpose, we generate independent random variables , , with which are independent of the data , and define and Independent of the symmetrization, we have . The conditional distribution of is therefore

and the conditional density becomes

| (2.1) |

Recall that we have access to an i.i.d. sample of the joint density . This allows for nonparametric estimation of via . Applying the inverse Radon transform to this estimate gives an estimator for the joint density This inversion scheme suffers from two sources of ill-posedness. Firstly, dividing by might result in very unstable reconstructions if is small. This happens if the normalized design variables systematically miss observations from some directions. In this case the problem becomes unevenly harder and only logarithmic convergence rates can be obtained (see Davison,, 1983; Frikel,, 2013; Hohmann and Holzmann,, 2016). When the support of does not contain an open ball, might be non-identifiable. Secondly, even with regularity on the distribution of the design, the Radon inversion is known to be an ill-posed problem with degree of ill-posedness . Hence, regularization of the inversion scheme is necessary.

In this work, we study the mildly ill-posed case where the random directions are sufficiently regularly distributed over the sphere and the ill-posedness is only due to the inversion of the Radon transform. The precise assumptions on the design are stated in Section 3.2.

Our approach makes use of the following explicit inversion formula of the Radon transform. Define the operator via

| (2.2) |

where denotes the identity for odd and the Hilbert transform

for even. Let for odd and for even. If is a Schwartz function on , then we have the inversion formula

| (2.3) |

cf. Theorem 3.8 in Helgason, (2011). The so called back projection operator is the adjoint of the Radon transform with respect to the scalar product. Notice that our constant differs from the constant in Helgason, (2011) as we use the standard definition of the Hilbert transform and define as the adjoint of the Radon transform (as opposed to the dual transform).

3 Multiscale tests for qualitative features

3.1 Multiscale inference

The goal of this work is to derive confidence statements for qualitative features of the joint density of the random coefficients. In particular, we are interested in the detection of modes (local maxima) of the density. Following the approach of Schmidt-Hieber et al., (2013), we express the features in terms of differential operators. To be precise, for a collection of compactly supported, non-negative and sufficiently smooth test functions consider the integral

| (3.1) |

for some directional vector and . Since there should not be any favored direction, we consider in the following radially symmetric test functions,

| (3.2) |

with a non-negative and sufficiently smooth kernel with and support on . Moreover, denotes the volume of the sphere and . Notice that is supported on the ball with center and radius The normalization for turns out to be convenient but does not entail that integrates to one.

If the integral (3.1) is positive, there exists a subset of with positive Lebesgue measure on which is positive. On this subset, is thus strictly increasing in direction Similarly, we can recover a decrease if the integral (3.1) is negative. To construct a statistical test for increases and decreases it is therefore natural to use an empirical counterpart of the functional defined in (3.1).

Let for , where the inequalities for the vectors are understood componentwise. For statistical inference regarding the sign of the directional derivatives of , we fix a subset and test for all simultaneously the corresponding hypotheses of the form

| (3.3) |

and

| (3.4) |

For constructing global tests, we can now argue as in Eckle et al., 2017a . Our main interest are the following three global testing problems (i)-(iii).

(i) Testing for the presence of a mode at a fixed location. Tests for the hypotheses (3.3) and (3.4) can be used for the detection of specific shape constraints such as a mode at a given point . For this purpose, we consider several bandwidths/scales and for each consider pairs , where , are directional vectors and the test locations are points on the line in a neighborhood of . Inference for the presence of a mode at the point can now be conducted by studying the testing problem

| (3.5) |

with ranging over all chosen scales and Level and power of the mode test (3.5) for different designs are reported in Section 4.2. In Section 4.3, we also show that it is essential to include several bandwidths/scales in order to separate modes which are close.

(ii) A global testing procedure for all modes. Simultaneous tests for the hypotheses (3.3) and (3.4) can be used for a global testing procedure to detect all modes of the density on a domain. Compared to the previous case, we search for evidence over a range of different which then inflates the number of local tests.

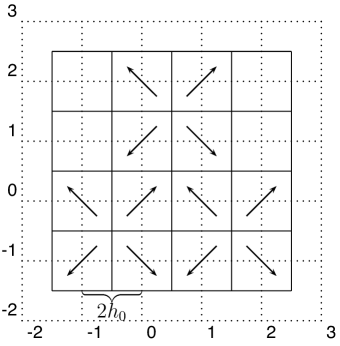

(iii) A graphical representation of the local monotonicity behavior for bivariate densities. Let and define a subset for a fixed scale of the form , where contains the vertices of an equidistant grid of width and contains the directions. We restrict the testing procedure to one fixed scale for an easy to read graphical representation. We consider four equidistant directions on given by Since , we have symmetry in the hypotheses, i.e. . Therefore, we test only for all triples Figure 1 displays an example for the test outcome with the hypotheses in (3.3) and as above. An arrow in a direction at a location represents a rejection of the corresponding hypothesis and provides an indication of a negative directional derivative of in direction at the location . Thus, Figure 1 provides strong evidence that the density is trimodal with modes close to the locations , , and . A detailed description of the settings used to generate Figure 1 and an analysis of the results is given in Section 4.1.

We now derive an empirical counterpart of the functional (3.1) in terms of the Radon transform . We make the following assumptions for the inversion of the Radon transform.

Assumption 1.

Suppose that the function in (3.2) is -times continuously differentiable with .

Assumption 2.

Suppose that the density is compactly supported, continuously differentiable and bounded from below in the test region by a constant

Assumption 2 is too restrictive for quantum homodyne tomography (model (1.3)), where the density is given by the Wigner function. The Wigner function can take negative values and is not compactly supported. In this case, we replace Assumption 2 by the following conditions.

Assumption 2′.

Suppose that is continuously differentiable and, for some ,

-

(i)

is bounded;

-

(ii)

for all ;

-

(iii)

There exist constants such that for every hyperplane with ,

Under the assumptions above the inversion formula (2.3) holds for partial derivatives of the test functions . This is a direct consequence of Theorem 3.8 in Helgason, (2011). The following lemma analyzes the structure of a partial derivative of the test function transformed by the operator introduced in (2.2) and how this transform depends on .

Lemma 3.1.

Work under Assumption 1 and let

| (3.6) |

Then

where and are defined in (2.2) and (3.1), respectively. Moreover,

| (i) | ; |

| (ii) | for . |

For a given triple we study the statistic

By Lemma 3.1, the expectation of this statistic can be written as

with being the surface measure on , i.e. for any measurable By an application of the inversion formula introduced in (2.3) and Lemma 5.1 in Helgason, (2011), we obtain

| (3.7) |

Up to rescaling, is thus an empirical counterpart of the functional defined in (3.1).

The statistic depends on the density In quantum homodyne tomography this density is known. For many other applications, however, needs to be estimated from the data. In this case, we use a standard cut-off kernel density estimator for based on an additional sample which is independent of . See also Appendix A for the definition of the estimator. We replace by its estimator and consider the test statistic

| (3.8) |

3.2 Assumptions on the design

As mentioned in Section 2, the inverse problem might become severely ill-posed or non-identifiable if the density approaches zero for some directions. This section provides conditions on the design which ensure that has positive Hölder smoothness and is bounded from below and above. These results are of independent interest.

In the random coefficients model (1.1), the density can be expressed in terms of the density via . To enforce that is bounded from below we restrict ourselves to designs where is bounded away from . The formula also allows to relate the smoothness of to the smoothness of

Although, the random coefficients model with intercept (1.2) could be viewed as a special case of the more general model (1.1) it requires a different set of assumptions. For model (1.2), we write as a function of and obtain

| (3.9) |

see Appendix B for a proof. A necessary condition to ensure that is given by as . This corresponds to Cauchy-type tails of the design variables. Thinner tails will increase the ill-posedness of the problem. In order to avoid very technical proofs, we consider in the random coefficients model with intercept only the case where follows a multivariate Cauchy distribution, i. e.,

| (3.10) |

with and a symmetric and positive definite matrix. We can compute explicitly using (3.9)

| (3.11) |

where denotes the signum function. In this case, is bounded from above and below and is continuously differentiable on the hemispheres and . In particular, if is standard Cauchy, then the density is constant. This leads to the following assumptions on the design.

In quantum homodyne tomography we set a global equal to the minimum of from Assumption 2’ and from Assumption 3.

It is important to notice that statistical testing in the random coefficients model relies on two unrelated sets of assumptions. Firstly, there are assumptions on the density of the random coefficients as introduced in Section 3.1. Restrictions of this kind are common in statistical inference for an unknown density. On the other hand, there are assumptions (see Assumption 3 above) on the design. These assumptions control the ill-posedness of the problem.

3.3 Asymptotic properties

This section presents the main theoretical result of the paper stating that the standardized and properly calibrated test statistic (3.8) can be uniformly approximated by a maximum of a Gaussian process. For that we need the definition of a Gaussian process on the cylinder . To this end, let be the Borel -algebra on . Define the -finite measure

Let denote the collection of all sets of finite -measure and let denote Gaussian -noise on . For disjoint sets this implies

(Adler and Taylor,, 2007, Chapter 1.4.3). is a random, finitely additive, signed measure. Integration w.r.t. can be defined similarly to Lebesgue-integration, starting with a definition for simple functions and an extension to general via approximation by simple functions in the -limit. Integration with respect to yields

and for where denotes the collection of all random variables whose first absolute moments exist. For more details, cf. Adler and Taylor, (2007), Chapter 5.2.

Let us provide some heuristic for the Gaussian approximation of . The process has in the important case the same mean and covariance structure as the Gaussian process

| (3.12) |

In the proof of Theorem 3.2 below we show that the expectation is asymptotically negligible in the limit process. The test statistic and the Gaussian process depend, however, on the unknown densities and which have to be estimated from the second part of the sample. To this end, we use the standard cut-off kernel density estimates and defined in Appendix A. For Gaussian -noise that is independent of the data let

and

| (3.13) |

The Gaussian approximation result for the family of test statistics holds for a finite subset . Its cardinality may, however, grow polynomially of arbitrary degree with the sample size. Moreover, the range of bandwidths must be bounded from above and below by and , both converging to zero as goes to infinity. The precise conditions are summarized in the following assumption.

Assumption 4.

Let be the set of half-open hyperrectangles in , i.e. every has the representation for some . For finite sets and two stochastic processes and which are defined on the same probability space, we write

if

3.4 Construction of the multiscale test

With the previous theorem, we can now construct simultaneous statistical tests for the hypotheses (3.3) and (3.4). If the constant is positive then the method consists of rejecting the hypotheses in (3.3) for small values of and rejecting in (3.4) for large values of , and vice versa if is negative. Theorem 3.2 is used to control the multiple level of the tests. Let and denote by the smallest number such that

By Theorem 3.2, is bounded uniformly with respect to . Define for the quantiles

| (3.14) |

and reject the hypothesis (3.3), if

| (3.15) |

Similarly, the hypothesis (3.4) is rejected, whenever

| (3.16) |

Theorem 3.3.

Based on the previous result, we now propose a method for the detection and localization of modes on a subdomain. For convenience, we only consider the case of a hyperrectangle . We study the case that there is a mode in the interior For the multiscale test to have power we need that the set of local tests is rich enough. This can be expressed in terms of conditions on Let be the set of all scales/bandwidths such that for every scale in this set all triples are in where ranges over all grid points of an equidistant grid with component wise mesh size in the hyperrectangle , and ranges over all grid points of a grid of and grid width converging to zero with increasing sample size.

The testing procedure is as follows. For any in let be the set of all sequences of triples such that for some sufficiently large and as , where denotes the angle between two vectors. The previous conditions ensure that several such sequences can be found. If for all triples in all local tests (3.16) reject the hypotheses (3.5), we have evidence for the existence of a mode at the point . By choosing the test locations as the vertices of an equidistant grid no prior knowledge about the location of has to be assumed. Theorem 3.4 below states that the procedure detects all modes of the density with probability converging to one as .

Theorem 3.4.

Assume the conditions of Theorem 3.2 and suppose that for any mode in there are functions , such that the density has a representation of the form

| (3.17) |

in an open neighborhood of . Furthermore, let be differentiable in an open neighborhood of with and when for all with . In addition, let be differentiable in an open neighborhood of zero with for .

If is nonempty for some sufficiently large constant then the procedure described in the previous paragraph detects the mode with probability converging to one as

The rate for the localization of the modes is (up to some logarithmic factor). Since this rate matches the optimal rate for mode detection in an inverse problem with ill-posedness of degree over a 2-Hölder class. Assumption 4 requires, however, To be able to include scales of the order we need The right hand side is smaller than one for

4 Finite sample properties

In this section we illustrate the finite sample properties of the proposed test in a bivariate and a trivariate setting. In the bivariate setting we illustrate how simultaneous tests for the hypotheses (3.3) and (3.4) can be used to obtain a graphical representation of the local monotonicity properties of the density. In the trivariate setting we investigate the performance of the test for modality at a given point (see the hypotheses in (3.5)) and the dependence of its power on the distribution of .

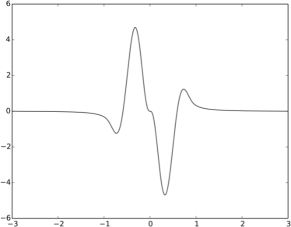

As test function we consider the simplest polynomial which satisfies the conditions of Assumption 1 for , that is,

with such that Figure 2 displays the function for Throughout this section the nominal level is fixed as , and all level and power statements are in percent. Except for Table 2, none of the simulations in this section assumes knowledge of the design density or uses a parametric specification of it.

4.1 Inference about local monotonicity of a bivariate density

We follow the multiscale approach in Section 3.1 to obtain a graphical representation of the monotonicity behavior for a bivariate density of random coefficients. To test the hypotheses (3.4) we use (3.16) with Here, is fixed and the set of test locations is defined as the set of vertices on an equidistant grid in the square with width one. Finally, the set of test directions is

The data are simulated with the density of the normal mixture The design is chosen such that is uniformly distributed on the sphere . Figure 1 in Section 3.1 displays the monotonicity behavior of the density based on sample size . Each arrow at a location in direction displays a rejection of a hypothesis (3.4). The map indicates the existence of modes around the points , , and and thus detects the true modes fairly well.

4.2 Influence of the design on the power

Given the random coefficients model with , we study the power of the test for the existence of a mode at a given location considering only few local tests. The postulated mode is given by the point and we take with the -th standard unit vector in We conclude that has a local maximum at the point , whenever all hypotheses are rejected, i.e.

| (4.1) |

where is defined by (3.14). Recall that the quantiles are constructed in such a way that the probability of at least one false rejection within the six tests (4.1) is bounded by . However, the mode test detects the presence of a mode whenever all six tests (4.1) are rejected at the same time. The multiscale method is therefore rather conservative for the specific task of mode detection. In this simulation, we also study a calibrated version of the test where the quantiles are chosen such that the test keeps its nominal level and detects the presence of a non existing mode in about 5 percent of the simulation runs. For the calibration of the test we work under the null hypothesis assuming that is uniform. Therefore, knowledge about the true unknown density is not required.

Numerical simulations for random coefficients model without intercept: At first, we consider model (1.1) with uniform design To study the level of the test, we used For the power we took as the density of a trivariate standard normal distribution. All results are based on the local tests (4.1) and 1000 repetitions. Level simulations with the theoretical quantiles confirm that the multiscale test keeps its nominal level as the percentage of false rejections of at least one of the six hypotheses in (4.1) for sample size is nearly percent. The results of mode test are reported in Table 1.

Next, we investigate an asymmetric distribution of the directions by sampling , with the identity matrix. We only consider the calibrated mode test. Results are reported in columns five and six in Table 1. Compared to the case of uniform design, we observe a decrease in the power of the mode test (4.1). The explanation is that the uniform design on the induces a more uniform distribution of on the sphere which makes it simpler to recover information about the joint density as discussed in Section 2.

| power | level (cal.) | power (cal.) | level (cal.) | power (cal.) | |

|---|---|---|---|---|---|

| 250 | 9 | 4.5 | 91.0 | 4.7 | 66.1 |

| 500 | 15.7 | 4.6 | 99.1 | 4.5 | 78.8 |

| 1000 | 79.1 | 5.0 | 100 | 4.5 | 90.6 |

Numerical simulations for random coefficients model with intercept: We study model (1.2) with In a first simulation, we sample the random vectors from a standard bivariate Cauchy distribution, such that the density is constant. Except for the different design, we consider otherwise the same test settings as above. The simulated level and power of the calibrated version of the test (4.1) are reported in Table 2. To investigate the influence of the estimation of the design density on the power of the test we also perform simulations in which we assume that the density is known to be constant. These are shown in Table 2, fourth and fifth column.

| unknown | known | |||

| level (cal.) | power (cal.) | level (cal.) | power (cal.) | |

| 250 | 4.8 | 91.3 | 5.0 | 93.3 |

| 500 | 5.2 | 99.0 | 5.2 | 99.7 |

| 1000 | 5.3 | 100 | 5.3 | 100 |

Compared to the power approximations for unknown , we observe only a slight increase in power of the test for known .

Finally, we consider two designs which do not satisfy Assumption 3. Table 3 reports the level and power for the same setting as above except that now is drawn from a standard normal distribution or We observe only a slight decrease in the power of the test for normally distributed design compared to the setting where Assumption 3 holds. Even under uniform design, the test performs fairly well.

| level (cal.) | power (cal.) | level (cal.) | power (cal.) | |

| 250 | 5.1 | 88.3 | 5.1 | 64.8 |

| 500 | 5.5 | 98.3 | 5.1 | 78.1 |

| 1000 | 5.1 | 100 | 5.5 | 89.4 |

4.3 Multiscale mode testing

For multimodal densities which have a second mode close to the test location testing different bandwidths simultaneously can be advantageous to separate the modes. This is illustrated by the following example, where we consider the random coefficients model without intercept with The data are simulated with being the density of the normal mixture

We consider a design such that is uniformly distributed on the circle . The level is fixed to five percent. We conducted simultaneously twelve tests with three different scales for the hypotheses (3.5) with . The tests are given by We analyze the outcome of the twelve tests in two ways. Firstly, we investigate the performance of each of the three tests for modality for the bandwidths , and separately. Secondly, we consider the performance of a combined test for modality using two scales and . The power approximations for sample sizes based on 1000 repetitions are displayed in Table 4.

| 2000 | 100 | 0 | 0 | 25 |

| 5000 | 100 | 0 | 1 | 86.3 |

| 15000 | 100 | 0 | 68.7 | 100 |

Figure 3 illustrates the results of the twelve tests for the hypotheses (3.5) conducted simultaneously. Each arrow at a location in direction displays a rejection of a hypothesis (3.5) and the length of the arrows corresponds to the respective bandwidths.

The results in Table 4 show that the mode test for detects in all cases a mode in a neighborhood of . However, the bandwidth is too large to distinguish between the underlying modes of at and . The test for the bandwidth fails to detect the mode as is still too large to separate the two modes of On the contrary, is too small to detect the decrease with small slope corresponding to the eigenvalue of the covariance matrix in the first mixture component of Note that this effect vanishes for increasing sample size. By conducting the tests for the bandwidths and simultaneously, we are able to detect the mode at in most of the simulations.

4.4 Comparison with the parametric random coefficient model

It is common in the literature to use a parametric specification of the random coefficients. Usually, is assumed to have a multivariate normal distribution. In this section, we compare our nonparametric approach with mode estimation under a parametric specification of the random coefficient distribution. Our findings are similar to what is usually observed when parametric and nonparametric methods are compared. If the parametric specification of the model is consistent with the data generating process, the parametric approach outperforms the nonparametric one in terms of estimation errors, power of tests, and computation time. However, when the parametric specification and the data generating process differ, a model misspecification bias is present in the parametric estimation. This will not vanish, even if the sample size is large. The nonparametric model does not suffer from this problem and can in these cases perform better than the parametric model. We illustrate this effect in the following simulations.

We consider the parametric random coefficients model where the density of belongs to some parametric family with parameter . Note that we can rewrite the equation as a mixed model . Here are fixed effects and are random effects with expectation . If is unimodal with a mode at , we just need to derive confidence statements for . This is in particular true if is a normal density, which is the most common choice. A simple and efficient way to estimate is heteroscedasticity robust linear regression. Obviously, the computational complexity of this method is much smaller than the complexity of our algorithm.

Our test example is the random coefficients model with intercept (1.2) with and sampled from a standard bivariate Cauchy distribution. The distribution of the random coefficients in the data generating process is given by (i) a standard Gaussian, (ii) the normal mixture and (iii) an exponential-2 distribution for and independent of the first component. Table 5 reports estimates for obtained by transforming and to and and running a heteroscedasticity robust regression.

| (i) () | (ii) () | (iii) () | ||||

|---|---|---|---|---|---|---|

| 0.00 | (0.02) | 1.00 | (0.02) | 2.03 | (0.03) | |

| 0.02 | (0.02) | 0.00 | (0.01) | -0.02 | (0.02) | |

| 0.00 | (0.02) | 0.01 | (0.01) | 0.02 | (0.02) | |

In column (i) of Table 5 the parametric assumption holds and the procedure detects the true mode of the density with high precision compared to the bandwidth choice in the simulations presented in Table 2 in Section 4.2. In contrast, for the bimodal density in column (ii) the coefficient vector does not describe a representative member of the population because the misspecification bias is too large. For the skewed distribution of column (iii) the estimator also fails to detect the mode of the density for the same reason.

By applying our testing procedure in the setting of columns (ii) and (iii) we can show that the OLS results do not represent modes of the density. To this end, we set in (ii)

and in (iii)

Both tests reject (in (ii) in and in (iii) in percent of 1000 repetitions). Therefore, our procedure shows that neither in (ii) nor in (iii) are modes of the underlying density. Of course, the parametric model would be able to detect the modes in cases (ii) and (iii) with a different parametric specification. However, this would require considerable a priori knowledge about the data. If we did not interpret the results as estimators for the mode but as estimators for , the parametric method would perform well.

5 Application to consumer demand data

Heterogeneity of consumers is a major challenge in modeling and estimating consumer demand. In several different demand models random coefficients were proposed to account for the heterogeneity in the population of consumers.

5.1 Model and data

In this section we are interested in the almost ideal demand system (AIDS) which was initially proposed by Deaton and Muellbauer, (1980) with fixed coefficients. This model does not explain demand for a product itself but explains the budget share spent on a product by a linear equation. The explanatory variables are log prices and the log of total expenditure divided by a price index. A detailed discussion of the model is contained in Lewbel, (1997).

Fixed coefficients in this model mean that all consumers are assumed to react in the same way when the price of a product changes. It is well known that some consumers are very price sensitive and change their behavior significantly with small variations in prices while other consumers are less price sensitive. This type of heterogeneity can be modeled by a random coefficient on log prices which is assumed to vary across the population of consumers. A similar argument suggests a random coefficient on log total expenditure. Recently, applications of the AIDS using a nonparametric random coefficient specification instead of fixed coefficients were presented in Hoderlein et al., (2015) and Breunig and Hoderlein, (2018).

We apply our multiscale test to detect modes in the random coefficients for budget shares for food at home (BSF)

| (4.1) |

Food expenditure is a large fraction of total expenditure and is roughly about 20%.

We analyze the data of the British Family Expenditure Survey which ran from 1961 to 2001. It reported yearly cross sections for household income, expenditure and other characteristics of roughly 7000 households. We use data of the years 1997–2001 only which gives a sample size of about 33000. Budget shares of food are generated by dividing the expenditure for all food by total expenditure. Food prices are reported as relative prices in comparison to a general prize index. The variable is normalized to January 2000 real prizes.

Assumption 3 and the numerical simulations in Section 4 suggest that our test has more power when the normalized regressors are approximately uniform on the sphere. We can achieve this by symmetrizing the design in model (4.1) as follows:

| (4.2) |

The relation of the modified model to the random coefficients in (4.1) is , , . Observations of the new variable lie between and . The observations of range from to .

5.2 Results

For a first evaluation of the data we assumed fixed coefficients in model (4.2) and estimated the model with ordinary least squares (OLS).

In order to find modes of the density we conducted simultaneously tests on the level of the form (3.5) on the two scales and . Recall from Section 4.2 that our testing procedure also performs well when the are not Cauchy distributed. Therefore, to obtain a testing procedure which is more flexible with respect to the design, we use the nonparametric density estimator instead of a parametric estimation procedure. We were testing for modes on the equidistant grid covering with grid width . Hence, the grid had 27 nodes. For every grid point tests of the hypotheses (3.5) were conducted for the directions and locations

where denote the standard unit vectors of . We detected a single mode in the neighborhood of the grid point for the tests with bandwidth . The test for the bandwidth did not detect a mode.

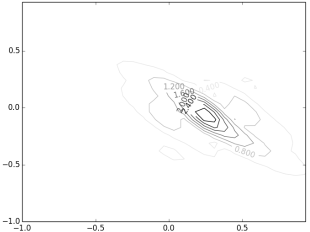

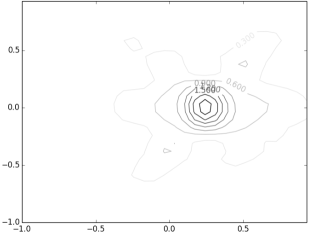

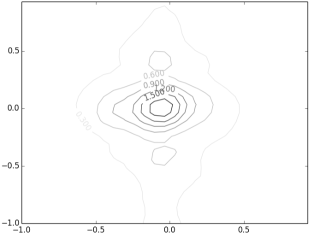

In the following we use nonparametric density estimation to motivate hypotheses for the testing procedure. It is important that this estimate and the test are independent, otherwise the testing procedure would be biased and could not guarantee a bound on the error rate. We meet the requirement by splitting the sample in two independent equally sized sub-samples. The first sub-sample is used for nonparametric estimation of the random coefficient density in model (4.2) with the estimator in Hoderlein et al., (2010). Figure 4 gives contour plots for the joint densities of , , and based on about 16500 observations. We chose the smoothing parameters and in the estimator in Hoderlein et al., (2010) equal to 0.05 and 0.1, respectively. Note that these bandwidth choices do not affect the level of the test performed below as the test does not depend on this estimator. The nonparametric estimate suggests that the random coefficient density of has one (well-pronounced) mode close to

| (4.3) |

This is consistent with the results of the test above which found a mode close to . Since the marginal densities of are nearly symmetric it is also consistent that the mode is close to the OLS estimates given in Table 6. With a significantly skewed or with a multimodal random coefficient density location of modes would differ from OLS.

With the second sub-sample we studied whether a mode can be found for the location given by (4.3) on a smaller scale than in the test above. This would then indicate that the location of the mode is not . Our primary interest is in the coefficients on and on total expenditure and food prices. In order to see if the mode is indeed in a location where and , we conduct two mode tests (4.3) simultaneously for the bandwidths and , that is, we test twelve hypotheses (3.5) for the following locations and directions On scale , we tested

and on scale

The test rejected all local hypotheses on scale but not on scale This gives evidence that the mode is in a location where is negative but we cannot decide whether is positive at the mode.

Let us return to the initial model (4.1). The results of our test give evidence that a mode exists close to

with strong evidence that is indeed negative. This vector of coefficients describes a representative member of the majority of consumers. It suggests that in the majority group food budget shares decrease with increasing log total expenditure. The nonparametric estimate in Figure 4 shows that there is considerable variance among consumers around this representative member.

Acknowledgments

J. Schmidt-Hieber was partially funded by a TOP II grant from the Dutch science foundation. F. Dunker acknowledges support by the Ministry of Education and Cultural Affairs of Lower Saxony in the project Reducing Poverty Risk. K. Proksch acknowledges financial support by the German Research Foundation DFG through subproject A07 of CRC 755. K. Eckle has been supported by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823, Project C4) of the German Research Foundation (DFG). We are very grateful to two referees and an associate editor for their constructive comments, which led to substantial improvement of an earlier version of this manuscript.

References

- Adler and Taylor, (2007) Adler, R. J. and Taylor, J. E. (2007). Random fields and geometry. Springer Monographs in Mathematics. Springer, New York.

- Andrews, (2001) Andrews, D. (2001). Testing when a parameter is on the boundary of the maintained hypothesis. Econometrica, 69(3):683–734.

- Bai et al., (1988) Bai, Z. D., Rao, C. R., and Zhao, L. C. (1988). Kernel estimators of density function of directional data. J. Multivariate Anal., 27(1):24–39.

- Bates et al., (2015) Bates, D., Mächler, M., Bolker, B., and Walker, S. (2015). Fitting linear mixed-effects models using lme4. Journal of Statistical Software, 67(1):1–48.

- Beran, (1993) Beran, R. (1993). Semiparametric random coefficient regression models. Ann. Inst. Statist. Math., 45(4):639–654.

- Beran et al., (1996) Beran, R., Feuerverger, A., and Hall, P. (1996). On nonparametric estimation of intercept and slope distributions in random coefficient regression. Ann. Statist., 24(6):2569–2592.

- Beran and Hall, (1992) Beran, R. and Hall, P. (1992). Estimating coefficient distributions in random coefficient regressions. Ann. Statist., 20(4):1970–1984.

- Berry et al., (1995) Berry, S., Levinsohn, J., and Pakes, A. (1995). Automobile prices in market equilibrium. Econometrica, 63(4):841–890.

- Berry and Pakes, (2007) Berry, S. and Pakes, A. (2007). The pure characteristics demand model. Internat. Econom. Rev., 48(4):1193–1225.

- Breunig and Hoderlein, (2018) Breunig, C. and Hoderlein, S. (2018). Specification Testing in Random Coefficient Models. Quantitative Economics, forthcoming.

- Butucea et al., (2007) Butucea, C., Guţă, M., and Artiles, L. (2007). Minimax and adaptive estimation of the wigner function in quantum homodyne tomography with noisy data. Ann. Statist., 35(2):465–494.

- Chernozhukov et al., (2017) Chernozhukov, V., Chetverikov, D., and Kato, K. (2017). Central limit theorems and bootstrap in high dimensions. Ann. Probab., 45(4):2309–2352.

- Davison, (1983) Davison, M. E. (1983). The ill-conditioned nature of the limited angle tomography problem. SIAM J. Appl. Math., 43(2):428–448.

- Deaton and Muellbauer, (1980) Deaton, A. and Muellbauer, J. (1980). An almost ideal demand system. American Economic Review, 70:312–326.

- Dubé et al., (2012) Dubé, J.-P., Fox, J. T., and Su, C.-L. (2012). Improving the numerical performance of static and dynamic aggregate discrete choice random coefficients demand estimation. Econometrica, 80(5):2231–2267.

- Dümbgen and Spokoiny, (2001) Dümbgen, L. and Spokoiny, V. G. (2001). Multiscale testing of qualitative hypotheses. Ann. Statist., 29(1):124–152.

- Dümbgen and Walther, (2008) Dümbgen, L. and Walther, G. (2008). Multiscale inference about a density. Ann. Statist., 36(4):1758–1785.

- Dunker et al., (2013) Dunker, F., Hoderlein, S., and Kaido, H. (2013). Random coefficients in static games of complete information. cemmap Working Papers, CWP12/13.

- Dunker et al., (2017) Dunker, F., Hoderlein, S., and Kaido, H. (2017). Nonparametric identification of random coefficients in endogenous and heterogeneous aggregate demand models. cemmap Working Papers, CWP11/17.

- Dunker et al., (2018) Dunker, F., Hoderlein, S., Kaido, H., and Sherman, R. (2018). Nonparametric identification of the distribution of random coefficients in binary response static games of complete information. Journal of Econometrics, forthcoming.

- (21) Eckle, K., Bissantz, N., and Dette, H. (2017a). Multiscale inference for multivariate deconvolution. Electron. J. Stat., 11(2):4179–4219.

- (22) Eckle, K., Bissantz, N., Dette, H., Proksch, K., and Einecke, S. (2017b). Multiscale inference for a multivariate density with applications to x-ray astronomy. Annals of the Institute of Statistical Mathematics, https://doi.org/10.1007/s10463-017-0605-1.

- Feuerverger and Vardi, (2000) Feuerverger, A. and Vardi, Y. (2000). Positron emission tomography and random coefficients regression. Ann. Inst. Statist. Math., 52(1):123–138.

- Fox and Gandhi, (2016) Fox, J. T. and Gandhi, A. (2016). Nonparametric identification and estimation of random coefficients in multinomial choice models. The RAND Journal of Economics, 47(1):118–139.

- Frikel, (2013) Frikel, J. (2013). Sparse regularization in limited angle tomography. Appl. Comput. Harmon. Anal., 34(1):117–141.

- Gautier and Hoderlein, (2012) Gautier, E. and Hoderlein, S. (2012). A triangular treatment effect model with random coefficients in the selection equation. cemmap Working Papers, CWP39/12.

- Gautier and Kitamura, (2013) Gautier, E. and Kitamura, Y. (2013). Nonparametric estimation in random coefficients binary choice models. Econometrica, 81(2):581–607.

- Giné and Guillou, (2001) Giné, E. and Guillou, A. (2001). On consistency of kernel density estimators for randomly censored data: rates holding uniformly over adaptive intervals. Ann. Inst. H. Poincaré Probab. Statist., 37(4):503–522.

- Greenland, (2000) Greenland, S. (2000). When should epidemiologic regressions use random coefficients? Biometrics, 56(3):915–921.

- Gustafson and Greenland, (2006) Gustafson, P. and Greenland, S. (2006). The performance of random coefficient regression in accounting for residual confounding. Biometrics, 62(3):760–768.

- Helgason, (2011) Helgason, S. (2011). Integral geometry and Radon transforms. Springer, New York.

- Hoderlein et al., (2015) Hoderlein, S., Holzmann, H., and Meister, A. (2015). The triangular model with random coefficients. cemmap Working Papers, CWP33/15.

- Hoderlein et al., (2010) Hoderlein, S., Klemelä, J., and Mammen, E. (2010). Analyzing the random coefficient model nonparametrically. Econometric Theory, 26(3):804–837.

- Hohmann and Holzmann, (2016) Hohmann, D. and Holzmann, H. (2016). Weighted angle radon transform: Convergence rates and efficient estimation. Statistica Sinica., 26:157–175.

- Hsiao, (2014) Hsiao, C. (2014). Analysis of Panel Data. Cambridge University Press. Cambridge Books Online.

- Hsiao and Pesaran, (2004) Hsiao, C. and Pesaran, M. H. (2004). Random Coefficient Panel Data Models. CESifo Working Paper Series 1233, CESifo Group Munich.

- Ichimura and Thompson, (1998) Ichimura, H. and Thompson, T. (1998). Maximum likelihood estimation of a binary choice model with random coefficients of unknown distribution. Journal of Econometrics, 86(2):269 – 295.

- Lewbel, (1997) Lewbel, A. (1997). Consumer demand systems and household equivalence scales. In Pesaran, M. H. and Schmidt, P., editors, Handbook of applied econometrics, volume 2, chapter 4, pages 167–201. Blackwell, Oxford.

- Masten and Torgovitsky, (2014) Masten, M. and Torgovitsky, A. (2014). Instrumental variables estimation of a generalized correlated random coefficients model. cemmap Working Papers, CWP02/14.

- Masten, (2017) Masten, M. A. (2017). Random coefficients on endogenous variables in simultaneous equations models. The Review of Economic Studies, page rdx047.

- Nevo, (2001) Nevo, A. (2001). Measuring market power in the ready-to-eat cereal industry. Econometrica, 69(2):307–342.

- Petrin, (2002) Petrin, A. (2002). Quantifying the benefits of new products: The case of the minivan. Journal of Political Economy, 110(4):705–729.

- Proksch et al., (2016) Proksch, K., Werner, F., and Munk, A. (2016). Multiscale scanning in inverse problems. ArXiv Preprint, arXiv:1611.04537.

- Schmidt-Hieber et al., (2013) Schmidt-Hieber, J., Munk, A., and Dümbgen, L. (2013). Multiscale methods for shape constraints in deconvolution: confidence statements for qualitative features. Ann. Statist., 41(3):1299–1328.

- Swamy, (1970) Swamy, P. (1970). Efficient inference in a random coefficient regression model. Econometrica, 38(2):311–323.

Supplementary material to “Tests for qualitative features in the random coefficients model”

Appendix A Nonparametric estimators for the densities and

In this section we discuss the estimation of the densities and and related quantities. We use kernel density estimators based on the second half of the observations . The density of the random vector is denoted by . In the random coefficients model without intercept is a -variate density and a -variate density in the random coefficients model with intercept. Throughout the following, is assumed to be Lipschitz continuous, non-negative and

In the random coefficients model without intercept, we introduce the kernel density estimator

| (4.1) |

with normalization constant

As shown in Bai et al., (1988), the integral does not depend on and converges to some positive constant as . For the joint density of we propose the kernel density estimator

| (4.2) |

In the random coefficients model with intercept the symmetrizations and with Rademacher variables correspond to point reflections of the densities at the origin. Thus, the density is in general not continuous on the boundary of the hemisphere (see also (3.11)). Smoothness is, however, necessary to control the bias. Therefore, we use a two step procedure for the estimation of and in the random coefficients model with intercept. First, we estimate the density of the non-symmetrized samples and , on the hemisphere and on , respectively. The estimators for and are then the same as (4.1) and (4.2) except that now and the normalization constant is replaced by a function , defined by

In a second step, we symmetrize the estimators and divide by two to get estimators of the densities and on the whole domain.

In the next lemma we establish convergence of these estimators. If in Lemma A.1 follows a multivariate Cauchy distribution, then . Otherwise, comes from Assumption 3 (iii).

Lemma A.1.

Suppose Assumption 3 is satisfied for some and set in the case of the random coefficients model with intercept. In both models, the estimator with bandwidth and satisfies

| (i) | |

|---|---|

| (ii) | |

| (iii) |

The proof is delayed to the end of this section. Let us now discuss properties of the density By (2.1), Under Assumption 2, is compactly supported and consequently, and for are uniformly bounded. Moreover, is Hölder continuous with Hölder constant . This is a straightforward consequence of the Hölder -continuity of shown in the proof of Lemma A.1 and the identity

where denote an orthonormal basis of the orthogonal complement of , together with the compact support and the Lipschitz-continuity of (following from Assumption 2). Moreover, the properties of discussed above also hold in quantum homodyne tomography under Assumption 2’. We point out that the marginal densities of the Wigner function, which are given by the Radon transform, are nonnegative. This will be used later to bound the standard deviation away from zero.

If in Lemma A.2 follows a multivariate Cauchy distribution, then . Otherwise, comes from Assumption 3 (iii).

Lemma A.2.

For the estimation of the test statistic and the limiting process the quantities and need to be estimated. The functions and are not smooth in zero and we therefore introduce the cut-off estimators

| (4.3) |

By the boundedness from below of and Lemma A.1 it holds almost surely for sufficiently large.

Proof of Lemma A.1.

We only consider the case without intercept, that is, (i)-(iii) in Assumption 3 hold. In the case with intercept, we use and the fact that is Lipschitz-continuous with respect to to arrive at the same conclusion.

To prove (i) observe that

Here, we used the compact support of and the identity . Since , we have by Assumption 3 (iii) for . By definition of the constant , we obtain and this proves (i).

Next, we bound the stochastic error term (ii) using an entropy argument and Bernstein’s inequality. Observe that by the Lipschitz-continuity of is Lipschitz-continuous with Lipschitz constant of order For let be defined as the set of smallest cardinality such that for some constant If is chosen small enough, then

| (4.4) |

In order to bound the probability, we apply Bernstein’s inequality to with

We find for some constant and for some constant

using the boundedness of and as well as the definition of . Hence, an application of Bernstein’s inequality yields with (4.4),

Since is a polynomial power of the claim follows by choosing the constant large enough.

For (iii) one proceeds similarly with the choice using the summability of the probabilities. ∎

To prove Lemma A.2, we make use of a slightly modified version of Proposition 2.2 in Giné and Guillou, (2001) which we state below as Proposition A.1. If is a uniformly bounded class of measurable functions on a measurable space with a measurable and bounded envelope , then is said to be a measurable uniformly bounded VC class of functions if there are constants such that

for all , where denotes the -covering number of the metric space and the supremum is taken over all probability measures on .

Proposition A.1.

Let be any probability measure on and let be independent with common law . Let further be a measurable uniformly bounded VC class of functions and let and be any numbers such that and . Then there exist universal constants such that the exponential inequality

| (4.5) | ||||

is valid for all

In contrast to Proposition 2.2 in Giné and Guillou, (2001), Proposition A.1 contains the explicit dependence of the right hand side of (LABEL:1.1) on the constants and .

Proof of Lemma A.2.

Similarly as in the proof of Lemma A.1, it is enough to consider the random coefficients model without intercept only and to work under Assumption 3, (i)-(iii). If the design density is multivariate Cauchy, we can derive the properties in a similar way for . An upper bound of the bias can be derived similarly to Lemma A.1 (i). For the stochastic error

we apply Proposition A.1 to the function class

which depends on via . By the boundedness of we find . To show that is a VC class of functions, we introduce a discretization of as follows: Let be a sufficiently small constant only depending on the kernel . We chose a grid of with grid width at most . Obviously, this is possible with . Moreover, introduce the set of intervals , . For each probability measure there are at most sets such that . Let be an equidistant grid of

with grid width and let denote an arbitrary point in Basic calculations show Moreover, the subset of indexed by

is an -covering set of . To see this, fix . Then

by the Lipschitz continuity of . Hence, by construction of the set there exists such that

For we obtain

since the support of is compact and does not intersect with any of the sets for sufficiently small. A similar argument applies to . Hence,

and is a VC class of functions with and . An application of Proposition A.1 yields

for sufficiently large. We have used that for . The last line of the equation converges to zero at a summable rate since by assumption which concludes the proof of the uniform almost sure convergence of . ∎

Let us turn to the standard deviation

| (4.6) |

and its estimator defined in (3.13). The following lemma shows that it is uniformly bounded from above and below. The proof is deferred to Appendix B.

The proof is given in Appendix B. The consistency of the estimates and shows that is a consistent estimator of the standard deviation .

Proof.

Proof.

We discussed in Section 3 that the test statistic relies on the unknown density and therefore we introduced the statistic , where the density is replaced by the estimate . An important part of the proof of Theorem 3.2 consists of showing that this replacement is asymptotically negligible. To this end, the bias of the estimate has to be controlled.

Lemma A.6.

Under Assumption 3,

Appendix B Proofs related to properties of the Radon transform

Proof of (3.9): Recall that in the random coefficients model with intercept

where is a Rademacher variable. Hence, we obtain

∎

Proof of Lemma 3.1.

By assumption, is radially symmetric and satisfies (3.2). We fix a direction and consider the directional derivative

where is the usual derivative of . The Radon transform of this directional derivative is

Set For using the definition of in (3.6),

For let with and write for . Then

as is an even function. Now we can proceed similarly as in the case .

If is odd, the proof of the representation of is completed by taking the -th derivative with respect to the variable . If is even, for any function , for any fixed , and for

by substitution. That exists is shown below for the choice . Hence, we obtain for even.

Next we prove for The case is obvious. We use the chain rule for higher order derivatives given by Faà di Bruno’s formula

| (4.1) |

where is the set of all -tuples of non-negative integers satisfying . Since is a.e. -times continuously differentiable, we can interchange the integral with the -fold differentiation for the variable provided that

exists for all . Applying (4.1) with and gives

for suitable constants and Applying the chain rule to yields

for non-negative integers and suitable constants . As is compactly supported, it remains to show that each of the functions

| (4.2) |

for is uniformly bounded, where are arbitrary elements of the set . Notice that

A uniform bound for the integral on the right hand side of (4.2) can be found easily when is bounded away from zero. We can thus assume that . Splitting the integral and using that by Taylor expansion and Assumption 1,

as well as , we obtain an upper bound (up to some constant) for the integral on the right hand side of (4.2) by

By the use of , and , we find that this is bounded by which proves the result.

Next, we prove that exists. Recall that and consequently, is Lipschitz continuous. For any Lipschitz continuous function with compact support,

where denotes the Lebesgue measure of the support of . Moreover,

By the Lipschitz-continuity of , such that the r.h.s. can be bounded by a constant that does not depend on . The result follows with . This proves assertion (i) in the Lemma.

Finally, we prove (ii). As shown above, is bounded. For odd dimension the claim therefore follows from substitution and the compact support of . For even, substitution and the fact that the Hilbert transform defines a bounded operator for all yield the required result.

∎

Proof of Lemma A.3.

The existence of a uniform upper bound of follows directly from the boundedness of . The uniform lower bound of follows from Assumption 3. The integrability of is shown in the proof of Lemma 3.1 (ii). For the lower bound of recall that

By Assumption 2, for all and is uniformly continuous. Hence, there exists , which does not depend on , such that is uniformly bounded from below in the ball of radius around any , say, for all . Define for

where form an orthonormal basis of the orthogonal complement of . Clearly, , and all satisfy

In particular, Thus,

Hence, is uniformly bounded from below for all , and . Therefore,

| (4.3) |

where the inequality holds uniformly over .

In quantum homodyne tomography, Assumption 2’ (iii) yields

for if is sufficiently small. Hence, (4.3) holds in this case as well. Furthermore, since we obtain

If there exists such that

for all . The equality on the r.h.s. is trivial for odd dimensions and follows for even dimensions from the anti self-adjointness of the Hilbert transform and . ∎

Appendix C Proof of Theorem 3.2

If , Theorem 3.2 obviously holds. In the following we assume and define

where the equality follows from Lemma 3.1 (i).

C.1 Controlling the effect of density estimation in the test statistic

Theorem C.1.

Under the assumptions of Theorem 3.2,

Proof.

By the triangle inequality

with and We first bound using

and

| (4.1) |

The last inequality follows for odd dimension by the boundedness of and the integrability of For even dimension, recall that is bounded as shown in the proof of Lemma 3.1. Notice that

by (which holds for any function with compact support and bounded Hilbert transform) and the integrability of for . For the remainder, we find

by the boundedness of for all and

as for A similar argument can be used to bound the integral Applying Lemma A.6 with bandwidth gives

| (4.2) |

Next, we prove as where . If for some positive constant

then by Lemma A.1

for sufficiently large Now we apply Bernstein’s inequality to

By Lemma 3.1 (i), can be bounded by a constant uniformly over Moreover,

The inequality , the uniform lower bound of , almost surely for sufficiently large, Lemma A.1, and the definition of imply that each summand in is bounded on by

for some constants . By a change of variables in the integral for the variable , the uniform boundedness of , and the integrability of as shown in Lemma 3.1 (i), we find for the conditional variance with a similar argument as above

with some constants . Bernstein’s inequality yields

as . Finally, the claim follows from and the boundedness from below of shown in Lemma A.3. ∎

C.2 Approximation of the limit statistic

Define the process

Note that corresponds to the process where the density estimators have been replaced by the true densities. The proof of Theorem 3.2 relies on a recently obtained Gaussian approximation result which is reproduced here for convenience.

Theorem C.2 (Chernozhukov et al., (2017), Proposition 2.1).

Let be independent random vectors in with and for . Moreover, let be independent random vectors in with . Let be some constants and let be a sequence of constants, possibly growing to infinity as . Denote further by the set of all hyperrectangles in of the form for . Assume that

| (i) | for all ; |

|---|---|

| (ii) | for all and ; |

| (iii) | for all |

and define

Then there exists a constant only depending on and such that

Theorem C.3.

Under the assumptions of Theorem 3.2,

Proof.

To take absolute values into account, we introduce the set

| (4.3) |

Moreover, for let with

Notice that . In a first step, we show that for

| (4.4) |

Observe that by (4.1) and the uniform lower bound of established in Lemma A.3,

| (4.5) | ||||

Because of this bound, the expectation in the definition of will only provide terms of negligible order if we check the conditions of Theorem C.2. In particular, condition (i) is a direct consequence of the definition of in (4.6). By Lemma 3.1 (ii), the uniform lower bound of in Lemma A.3, the lower bound of , and the boundedness of , we find for . This implies condition (ii) of Theorem C.2 with .

Lemma 3.1 (i) implies which proves assertion (iii) in the theorem for any and , provided that the constant is chosen sufficiently large. Consequently, Theorem C.2 applies and for

choosing large enough and using Assumption 4.

In a second step, we show that there exists a version of the Gaussian noise such that

To this end, we define the Gaussian process indexed by as the centered Gaussian process with covariance function

Thus, there exists a version of such that Recall that defines a Gaussian process whose mean and covariance functions are and , respectively. Basic calculations show that there exists a version of such that

Hence,

By (4.5), Furthermore, which implies that An application of Markov’s inequality finally proves

The insertion of the bandwidth normalization terms has no influence on the convergence as translation and multiplication preserve the interval structure. ∎

C.3 Boundedness of the limit statistic

Recall from Lemma A.3 that is uniformly bounded from below whenever is sufficiently small, where the upper bound for only depends on , and We therefore introduce the set

Theorem C.4.

Under the assumptions of Theorem 3.2, is almost surely bounded.

Proof.

We apply Theorem 6.1 in Dümbgen and Spokoiny, (2001) to the non-normalized process

Denote by the canonical pseudo-metric on , induced by

In the next step, we prove

| (4.6) |

By the uniform lower and upper bound for

| (4.7) | ||||

In order to bound the expectation of the first term on the right hand side of (4.7), we use the boundedness properties of and

We show that the three terms can be bounded by the squared r.h.s. in (4.6). From Lemma 3.1 (ii) we obtain For we distinguish between the cases and . In the first case, the triangle inequality and Lemma 3.1 (ii) give In the second case, the integral w.r.t. the variable in is equal to

Recall that the Hilbert transform and the differentiation operator commute. Therefore, using the differentiability of which has been shown in the proof of Lemma 3.1, we find that

for some between and . Hence,

Here, we used the boundedness of shown in Lemma 3.1 (i), for all in the case , and . The latter is obvious for odd. For even we find that is an odd function and therefore is an odd function. Moreover, for any odd function such that exists, we have, up to some constant,

Here all integrals are understood in the principal value sense. Finally, a similarly argument as in the proof of Lemma 3.1 shows that exists and that by the compact support of .

We finally turn to . Without loss of generality, we may assume . We study the cases and , separately. In the first case, the triangle inequality and Lemma 3.1 (ii) give If we argue as for the upper bound of and find

for some between and . Recall that and . Thus,

where we used that . Finally, implies

For the second term on the right hand side of (4.7) we use that . Using again the uniform boundedness from above and below of and the fact that for all gives

For the second term in the last line, the bounds above apply which completes the proof for (4.6).

Set and such that

For fixed , the random variable follows a normal distribution with mean zero and variance bounded by a constant multiple of . Thus, there exists a constant such that for any ,

Furthermore, as corresponds to a standard normal distributed random variable. Thus, conditions (i) and (ii) of Theorem 6.1 in Dümbgen and Spokoiny, (2001) are satisfied. As in Eckle et al., 2017a one shows that condition (iii) of Theorem 6.1 in Dümbgen and Spokoiny, (2001) holds with and that the process is almost surely continuous on with respect to . The boundedness of follows by an application of Theorem 6.1 and Remark 1 in Dümbgen and Spokoiny, (2001). ∎

C.4 Replacing the true densities in the limit process by estimators

Theorem C.5.

Under the assumptions of Theorem 3.2,

Proof.

Recall the definition of the symmetrized set in (4.3) and let

Lemma A.5 and an argument as in the proof of Lemma A.4 show that for almost surely. Define

and We write and for the probability and expectation conditionally on , . Under , the vectors and are centered and normally distributed with

almost surely. Hence, an application of Theorem 2.2.5 in Adler and Taylor, (2007) gives

Moreover, by the almost sure asymptotic boundedness of proved in Theorem C.4, we have almost surely. Finally, for some constant ,

for almost surely, by Markov’s inequality. The constants introduced above do not depend on the second sample , and therefore the claim follows by an application of the law of iterated expectations. ∎

C.5 Replacement of the standard deviation by an estimator

Proof.

We only prove (i) as (ii) follows by a similar argument. By Lemma A.3 and Lemma A.4, and are almost surely uniformly bounded from below for all sufficiently large . Thus,

almost surely. The claim follows from Lemma A.4, Theorems C.1 and C.3 and the almost sure boundedness of established in Theorem C.4. ∎

Appendix D Proofs of Theorems 3.3 and 3.4

Proof of Theorem 3.3.

Proof of Theorem 3.4.

We assume in the following that . The case can be treated similarly. The following statement can be derived similarly as in the proof of Theorem 3.3 in Eckle et al., 2017a . For a null sequence converging sufficiently slowly and for the set of all triples for which the inequality

| (4.1) |

is satisfied it holds that

Hence, the hypotheses (3.5) are rejected simultaneously on the set of scales with asymptotic probability one. Moreover, for a mode in of and any triple , one can prove that for all by following the arguments in the proof of Theorem 10 in Eckle et al., 2017b . Consequently,