Incorporating Signals into Optimal Trading

Incorporating Signals into Optimal Trading

Abstract

Optimal trading is a recent field of research which was initiated by Almgren, Chriss, Bertsimas and Lo in the late 90’s. Its main application is slicing large trading orders, in the interest of minimizing trading costs and potential perturbations of price dynamics due to liquidity shocks. The initial optimization frameworks were based on mean-variance minimization for the trading costs. In the past 15 years, finer modelling of price dynamics, more realistic control variables and different cost functionals were developed. The inclusion of signals (i.e. short term predictors of price dynamics) in optimal trading is a recent development and it is also the subject of this work.

We incorporate a Markovian signal in the optimal trading framework which was initially proposed by Gatheral, Schied, and Slynko [21] and provide results on the existence and uniqueness of an optimal trading strategy. Moreover, we derive an explicit singular optimal strategy for the special case of an Ornstein-Uhlenbeck signal and an exponentially decaying transient market impact. The combination of a mean-reverting signal along with a market impact decay is of special interest, since they affect the short term price variations in opposite directions.

Later, we show that in the asymptotic limit were the transient market impact becomes instantaneous, the optimal strategy becomes continuous. This result is compatible with the optimal trading framework which was proposed by Cartea and Jaimungal [10].

In order to support our models, we analyse nine months of tick by tick data on 13 European stocks from the NASDAQ OMX exchange. We show that orderbook imbalance is a predictor of the future price move and it has some mean-reverting properties. From this data we show that market participants, especially high frequency traders, use this signal in their trading strategies.

1 Introduction

The financial crisis of 2008-2009 raised concerns about the inventories kept by intermediaries. Regulators and policy makers took advantage of two main regulatory changes (Reg NMS in the US and MiFID in Europe) which were followed by the creation of worldwide trade repositories. They also enforced more transparency on the transactions and hence on market participants positions, which pushed the trading processes toward electronic platforms [27]. Simultaneously, consumers and producers of financial products asked for less complexity and more transparency.

This tremendous pressure on the business habits of the financial system, shifted it from a customized and high margins industry, in which intermediaries could keep large (and potentially risky) inventories, to a mass market industry where logistics have a central role. As a result, investment banks nowadays unwind their risks as fast as possible. In the context of small margins and high velocity of position changes, trading costs are of paramount importance. A major factor of the trading costs is the market impact: the faster the trading rate, the more the buying or selling pressure will move the price in a detrimental way.

Academic efforts to reduce the transaction costs of large trades started with the seminal papers of Almgren and Chriss [5] and Bertsimas and Lo [8]. Both models deal with the trading process of one large market participant (for instance an asset manager or a bank) who would like to buy or sell a large amount of shares or contracts during a specified duration. The cost minimization problem turned out to be quite involved, due to multiple constraints on the trading strategies. On one hand, the market impact (see [7] and references therein) demands to trade slowly, or at least at a pace which takes into account the available liquidity. On the other hand, traders have an incentive to trade rapidly, because they do not want to carry the risk of an adverse price move far away from their decision price.

The importance of optimal trading in the industry generated a lot of variations for the initial mean-variance minimization of the trading costs (see [27, 15, 22] for details). In this paper, we consider the mean-variance minimization problem in the context of stochastic control (see e.g. [26], [9]). In this approach some more realistic control variables which are related to order book dynamics and specific stochastic processes for the underlying price can be used (see [23] and [30] for related work).

In this paper we address the question of how to incorporate signals, which are predicting short term price moves, into optimal trading problems. Usually optimal execution problems focus on the tradeoff between market impact and market risk. However, in practice many traders and trading algorithms use short term price predictors. Most of such documented predictors relate to orderbook dynamics [29]. They can be divided into two categories: signals which are based on liquidity consuming flows [11], and signals that measure the imbalance of the current liquidity. In [28], an example of how to use liquidity imbalance signals within a very short trading tactic was studied. These two types of signals are closely related, since within short terms, price moves are driven by matching of liquidity supply and demand (i.e. current offers and consuming flows).

As mentioned earlier, one of the major influencers on transaction costs is the market impact. Empirical studies have shown that the influence of the market impact is transient, that is, it decays within a short time period after each trade (see [7] and references therein). In this paper we will focus on two frameworks which take into account different types of market impact:

-

•

Gatheral, Schied and Slynko (GSS) framework [21], in which the market impact is transient and strategies have a fuel constraint, i.e., orders are finished before a given date ;

-

•

Cartea and Jaimungal (CJ) framework [10], where the market impact is instantaneous and the fuel constraint on the strategies is replaced by a smooth terminal penalization.

Note that [21] is not the only framework with market impact decay. This kind of dynamics was originally introduced in [31] and reused in [2] as in some other papers. We decided to focus on these two frameworks since they are extensively used in the financial literature. The model and analysis which are developed in this paper, could be applied also to other optimal trading frameworks.

The main theoretical result of this work deals with the addition of a Markovian signal into the optimal trading problem which was studied in [21].

We will argue in Section 2.1, that this is modelled mathematically by adding a Markovian drift to the martingale price process. We formulate a cost functional which consists of the trading costs and the risk of holding inventory at each given time.

Then we prove that there exists at most one optimal strategy that minimizes this cost functional. The optimal strategy is formulated as a solution to an integral equation. We then derive explicitly the optimal strategy, for the special case where the signal is an Ornstein-Uhlenbeck process. From the mathematical point of view this is the first time that a non martingale price process is incorporated to a optimal liquidation problem with a decaying market impact. Therefore the results of Theorems 2.3 and 2.4

extend Proposition 2.9 and Theorem 2.11 of [21], respectively.

Later we show that in the asymptotic regime were the transient market impact becomes instantaneous, the singular optimal strategies which were derived in the (GSS) framework, becomes continuous. Moreover we show, that asymptotics of the optimal strategy in the (GSS) framework coincide with the optimal strategy which is obtained in the (CJ) framework (see Remark 2.8 and Section 3).

This benchmark between different trading frameworks provides researchers and practitioners a wider overview, when they are facing realistic trading problems.

The use of predictive signals optimal trading, in the context which was described above, is relatively new (see [11]). To the best of our knowledge, this is the first time that a Markovian signal and a transient market impact are confronted.

The (GSS) framework already includes a transient market impact, without using signals. The (CJ) framework includes only a bounded Markovian signal and not a decaying market impact. Moreover, our results on optimal trading in the (GSS) framework incorporate a risk eversion term to the cost functional, which was not taken into account in the results of [21].

The main contribution of this work is in providing a new framework for optimal trading, which is an extension of the classical frameworks of [10] and [21] among others. The motivation to use this framework arises from market needs as our data analysis in Section 4 suggests. From a theoretical point of view, these models of trading with signals provide some new mathematical challenges. We will describe in short two of these challenges.

The optimal strategies that we derive in Theorem 2.4 and Corollary 2.7 (i.e. in the GSS framework) are deterministic and they use only information on the signal at time . One of the challenging questions which remain open, is how to optimise the trading costs over strategies which are adapted to the signal’s filtration (see Remark 2.9).

An interesting phenomenon which arises from our results, is that the optimal strategies may not be monotone once we take into account trading signals (see figure 1). It implies that price manipulations, triggered by trading strategies, are possible. Another challenge is to establish conditions on the market impact kernel function and on the signal, that will prevent price manipulations (see Remark 2.10).

Another contribution of this paper, is the statistical analysis of the imbalance signal and its use in actual trading, which we present in Section 4. In order to validate our assumptions and theoretical results, we use nine months of real data from nordic European equity markets (the NASDAQ OMX exchange) to demonstrate the existence of a liquidity driven signal. We focus the analysis on 13 stocks, accounting for more than 9 billions of transactions. We also show that practitioners are at least partly conditioning their trading rate on this signal. Up to 2014, this exchange provided with each transaction the identity of the buyer and the seller. This database was already used for some academic studies, hence the reader can refer to [36] for more details. We added to these labelled trades, a database of Capital Fund Management (CFM) that contains information on the state of the order book just before each transaction. Thanks to this hybrid database, we were able to compute the imbalance of the liquidity just before decisions are taken by participants (i.e. sending a market orders which consume liquidity).

We divide most members of the NASDAQ OMX into four classes: global investment banks, institutional brokers, high frequency market makers and high frequency proprietary traders (the classification is detailed in the Appendix). Then, we compute the average value of the imbalance just before each type of participant takes a decision (see Figure 4). The conclusion is that some participants condition their trading rate on the liquidity imbalance. Moreover, we provide a few graphs that demonstrate a positive correlation between the state of the imbalance and the future price move. These graphs also provide evidences for the mean-reverting nature of the imbalance signal (see Figure 5–7). In Figure 9 we preset the estimated trading speed of market participants as a function of the average value of the imbalance, within a medium time scale of 10 minutes. The exhibited relation between the trading rate and the signal in this graph is compatible with our theoretical findings.

This paper is structured as follows. In Section 2 we introduce a model with a market impact decay, a Markovian signal and strategies with a fuel constraint (i.e in the (GSS) framework). We provide general existence and uniqueness theorems, and then give an explicit solution for the case of an Ornstein-Uhlenbeck signal. The addition of a signal to market impact decay is the central ingredient of this Section. In Section 3 we compare our results from Section 2 to the corresponding results in the (CJ) framework. We show that the optimal strategy in the (GSS) framework coincides with the optimal strategy in the (CJ) framework, in the asymptotic limit where the transient market impact become instantaneous and the signal is an Ornstein-Uhlenbeck process. In Section 4 we provide an empirical evidence for the predictability of the imbalance signal and its use by different types of market participants. We also preform a statistical analysis which supports our focus on an Ornstein-Uhlenbeck signal in the example which is given in Section 2. The last section is dedicated to proofs of the main results.

2 Model Setup and Main Results

2.1 Model setup and definition of the cost functional

In this section we define a model which incorporates a Markovian signal into the (GSS) optimal trading framework. Definitions and results from [21] are used throughout this section.

We consider a probability space satisfying the usual conditions, where is trivial. Let be a right-continuous martingale and a homogeneous càdlàg Markov process satisfying,

| (2.1) |

Here represents expectation conditioned on . In our model represents a signal that is observed by the trader.

We assume that the asset price process , which is unaffected by trading transactions, is given by

hence the signal interacts with the price through the drift term. This setting allows us to consider a large class of signals. The visible asset price, which is described later, also depends on the market impact that is created by trader’s transactions.

Let be a finite time horizon and be the initial inventory of the trader. Let be the amount of inventory held by the trader at time . We say that is an admissible strategy if it satisfies:

-

(i)

is left–continuous and adapted.

-

(ii)

has finite and -a.s. bounded total variation.

-

(iii)

and , -a.s. for all .

As in [21, 17, 16], we assume that the visible price is affected by a transient market impact, and it is given by

| (2.2) |

where the decay kernel is a measurable function such that the following limit exists

| (2.3) |

Next we derive the transaction costs which are associated with the execution of a strategy .

Note that if is continuous in , then the trading costs that arise by an infinitesimal order are . When has a jump of size at , the price moves from to and the resulted costs by the trade are given by (see Section 2 of [21])

It follows that the trading costs which arise from the strategy are given by

From Lemma 2.3 in [21], we get a more convenient expression for the expected trading costs,

We are interested in adding a risk aversion term to our cost functional. A natural candidate is , which is considered as a measure for the risk associated with holding a position at time ; see [4, 19, 35] and the discussion in Section 1.2 of [33]. Hence our cost functional which is the sum of the expected trading costs and the risk aversion term has the form

| (2.4) |

where is a constant.

The main goal of this work is to minimize this cost functional (2.4) over the class of admissible strategies. Before we discuss our main results in this framework, we introduce the following class of kernels.

We say that a continuous and bounded is strictly positive definite if for every measurable strategy we have

| (2.5) |

We define to be the class of continuous, bounded and strictly positive definite functions .

Remark 2.1.

Remark 2.2.

An important subclass of is the class of bounded, non increasing convex functions (see Proposition 2 in [3]).

2.2 Results for a Markovian Signal

In this section we introduce our results on the existence and uniqueness of an optimal strategy, when the signal is a càdlàg Markov process. As in Section 2 of [21] we restrict our discussion to deterministic strategies. The minimization of the cost functional over signal-adaptive random strategies, will be discussed in Remark 2.9.

We consider the following class of strategies,

Note that for any in , the cost functional (2.4) has the form,

| (2.6) |

In our first main result we prove that there exists at most one strategy which minimizes the cost functional (2.6).

Theorem 2.3.

Assume that . Then, there exists at most one minimizer to the cost functional (2.6) in the class of admissible strategies .

In our next result we give a necessary and sufficient condition for the minimizer of the cost functional (2.6).

Theorem 2.4.

minimizes the cost functional (2.6) over , if and only if there exists a constant such that solves

| (2.7) |

A few remarks are in order.

Remark 2.5.

Remark 2.6.

Dang studied the case where the risk aversion term in (2.4) is nonzero, but again . In Section 4.2 of [17], a necessary condition for the existence of an optimal strategy is given, when the admissible strategies are deterministic and absolutely continuous. Our condition in (2.7) coincides with Dang’s result when and the admissible strategies are absolutely continuous. Note however that the question if the condition in [17] is also sufficient and the uniqueness of the optimal strategy, remained open even in the special case where .

2.3 Result for an Ornstein-Uhlenbeck Signal

As mentioned in the introduction, a special attention is given to the case where the signal is an Ornstein–Uhlenbeck process,

| (2.8) | ||||

where is a standard Brownian motion and are constants. In the following corollary we derive an explicit formula for the optimal strategy in the case of zero risk aversion and when has an exponential decay. The following corollary generalizes the result of Obizhaeva and Wang [31], who solved this control problem when there is no signal.

Corollary 2.7.

Note that and for , moreover, the optimal strategy is linear both in and .

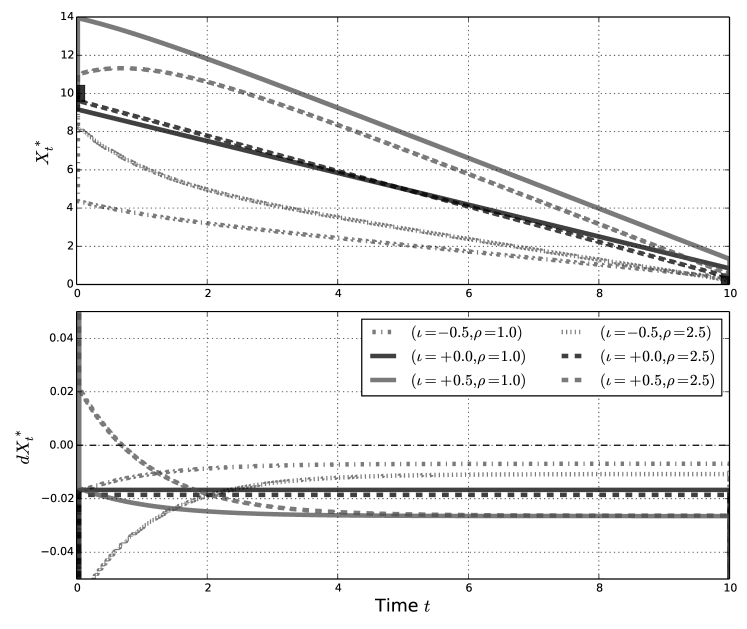

In Figure 1 we present some examples of optimal strategy with the following parameters: . These particular values are compatible with the empirical parameters which are estimated at the end of Section 4.2. Arbitrary initial values (-0.5, 0 and +0.5) are taken for the signal . The special case where gives similar result to Obizhaeva and Wang [31]. The parameter , which controls the market impact decay, cannot be estimated from the data that we have, hence we take two arbitrary but realistic values (1.0 and 2.5). We observe that for large values of , the initial jump in the optimal trading strategy is larger than the corresponding jump in the small strategies, but the trading speed tends to have a less variations. We particularly notice that when the initial signal is at an opposite direction to the trading ( for a sell order) the trading starts with purchases as expected, and afterwords the trading speed eventually becomes negative. On the other hand, when the initial signal is at the same direction to the trading, it is optimal to start selling immediately and most of the inventory is sold before .

In the following remarks we discuss the result of Corollary 2.7.

Remark 2.8.

Note that in the limit where , the market impact term in (2.6), formally corresponds to the costs arising from instantaneous market impact, that is . We briefly discuss the asymptotics of the optimal strategy in (2.9) when . It is easy to verify that in the limit, the jumps of vanish (see and in (5.12) for the explicit expression of the jumps), and the limiting optimal strategy is a smooth function which is given by

Motivated by these asymptotic results, in the next section we further explore absolutely continuous strategies which minimize the trading costs – risk aversion functional. We will assume there that the market impact is instantaneous, that is and drop the fuel constraint ( for ) from the admissible strategies. Then, explicit formulas for the optimal strategy are derived when the risk aversion term is non-zero.

Remark 2.9 (An adaptive version of (2.9)).

Equation (2.9) gives an optimal solution for a trader with inventory at , who is observing the initial value of the signal and wishes to minimize (2.6) for exponentially decaying kernel and . The cost functional is there given by,

where is the natural filtration of . In this setting, once the trading started, it is no longer possible to update the strategy while taking into account new information, i.e. new values of the signal. This can be compared to simpler frameworks like the one of Section 3, in which the optimal strategy is updated for any . We therefore add a short discussion on an adaptive framework for (2.9).

A natural way to update the optimal strategy at any time , is to define as the optimal strategy of the cost functional

Note however that

where

and

This implies if is used in place of for some , the trader will have an -adapted control , but it will not be necessarily consistent with which minimizes . Therefore, in practice one can choose between the following options:

-

•

the optimal strategy , limited to the information on the signal at ;

-

•

an approximate strategy updated at each time , which takes into account the whole trajectory of ;

-

•

the optimal strategy which corresponds to a market impact without a decay (as shown in Section 3).

The question which of these strategies gives the best results remains open.

Remark 2.10 (Price manipulation).

Market impact models admit transaction-triggered price manipulation if the expected costs of a sell (buy) strategy can be reduced by intermediate buy (sell) trades (see Definition 1 in [3]). Theorem 2.20 in [21] implies that transaction-triggered price manipulation are impossible for the cost functional in 2.7, over the class of admissible strategies, in the case where and . However, Figure 1, shows that adding signals to the same market impact model can create optimal strategies which are not monotone decreasing, and therefore implies a possible price manipulation. It would be very interesting to investigate the conditions on the market impact kernel and the trading signals which ensure no price manipulations. Study of the possible implications of these price manipulations on other market participants is also of major importance.

3 Optimal strategy for temporary market impact

In this section we study an optimal trading problem which has some common features to the problem which was introduced in Section 2.1. We consider again a price process which incorporates a Markovian signal. The main change in this section, is that the market impact in (2.2) is temporary, i.e. the kernel is given by , where is Dirac’s delta measure and is a constant. Note that this type of kernel is not included in the class of kernels which was introduced in (2.2). The main goal of this section is to show of how to incorporate trading signals in the (CJ) framework [10]. The results that we obtain could be compared to the results of Section 2 (see Remark 2.8). Recall that we heuristically obtained the optimal strategy when the kernel “converges” to Dirac’s delta measure as .

We continue to assume that is a càdlàg Markov process as in the beginning of Section 2 but we add the assumption that

| (3.1) |

for some constant .

For the sake of simplicity we will assume that so that

where is a Brownian motion and is a positive constant.

In the following example the fuel constraint on the admissible strategies will be replaced with a terminal penalty function. This allows us to consider absolutely continuous strategies as in the framework of Cartea and Jaimungal (see e.g. [12, 13, 14]). We introduce some additional definitions and notation which are relevant to this setting.

Let denote the class of progressively measurable control processes for which , -a.s.

For any we define

| (3.2) |

Here is the amount of inventory held by the trader at time . We will often suppress the dependence of in , to ease the notation.

The price process, which is affected by the linear instantaneous market impact, is given by

where . Note that here corresponds to (2.2) when .

The investor’s cash satisfies

with .

For the sake of consistency with earlier work of Cartea and Jaimungal in [12, 13, 14], we will define the liquidation problem as a maximization of the difference between the cash and the risk aversion. As mentioned earlier, the fuel constraint on the admissible strategies will be replaced by the penalty function, which is given by where is a positive constant.

The resulted cost functional is given by

| (3.3) |

where is a constant and represents expectation conditioned on .

The value function is

Note that this control problem could be easily transformed to a minimization of the trading costs and risk aversion as in Section 2.

Let be the generator of the process . Then, the corresponding HJB equation is

| (3.4) |

with the terminal condition

Let represent expectation conditioned on . In the following proposition we derive a solution to (3.4). The proof of Proposition 3.1 follows the same lines as the proof of Proposition 1 in [14].

Proposition 3.1.

Assume that . Then, there exists a solution to (3.4) which is given by

| (3.5) |

where

and the constants and are given by

In the following proposition we prove that the solution to (3.4) is indeed a an optimal control to (3.3).

Proposition 3.2.

The proofs of Propositions 3.1 and 3.2 are given in Section 5.2.

The following corollary follows directly from Propositions 3.1 and 3.2. Note that an Ornstein-Uhlenbeck process satisfies (3.1).

Corollary 3.3.

Remark 3.4.

Remark 3.5.

One can heuristically impose a “fuel constraint” on the optimal strategy in Corollary 3.3, by using the asymptotics of when . In this case and the limiting optimal speed which we denote by is

where

Remark 3.6.

It is important to notice that (2.9) gives the optimal strategy on the time horizon in the (GSS) framework, by using only information on the O.U. signal at . On the other hand (3.6), which is the optimal trading speed in the (CJ) framework is using the information on the signal at time . A crucial point here is, that if one tries to solve repeatedly the control problem in the (GSS) framework on time intervals for any , by using and as an input, the optimal strategy will not necessarily minimize the cost functional (2.4) on . The reason for that is that the control problem in (2.4) may be is inconsistent. The market impact (and therefore the transaction costs) which are created on affect the cost functional at (see Remark 2.9 for more details). This effect disappears when we set in (3.3).

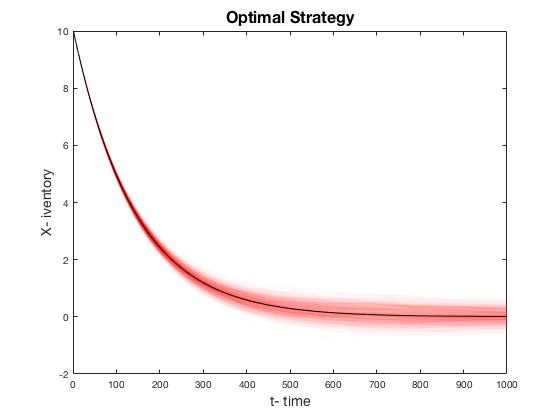

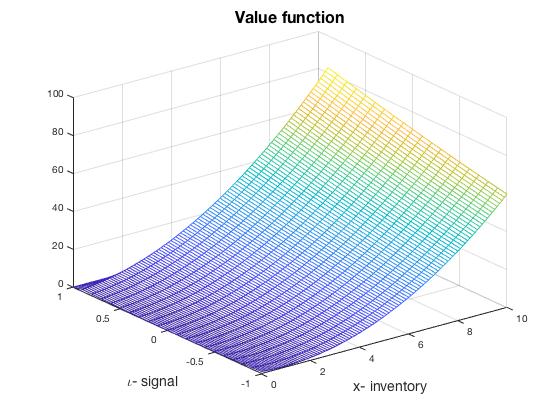

In Figure 2 we simulate the optimal inventory which is resulted by the optimal trading speed from Corollary 3.3. In the black solid line we present the optimal inventory in the case where there is no signal, therefore in this case the optimal strategy is deterministic. The red region in Figure 2 is a “heat map” of realizations of the optimal inventory . The pamperers of the model are , and for I as in (2.8), and , , , and , for the cost functional (3.3). We observe that the random strategies are a perturbation of the classical deterministic optimal strategy. In Figure 3 we present the value function (3.5) at , under the same assumptions as in Figure 2, that is, assuming that is an OU process and that the model parameters are similar. More precisely, we plot , hence we omit constants which do not contribute to the behaviour of the model. We observe that the revenue resulted by the optimal sell strategy is affected by the direction and value of the signal . The revenue of a sell strategy when the signal positive, which indicates on a potential price increase, is higher than negative signal scenarios.

4 Evidence for the use of signals in trading

In this section we analyse financial data which is related to the limit order book imbalance. The data analysis in this section is directed to support the models which were introduced in Sections 2 and 3. In Section 4.1 we describe our data base and provide an empirical evidence for the use of the imbalance signal, which is a liquidity driven signal. In Section 4.2 we study the statistical properties of the signal and motivate our model from Section 2.3, of an Ornstein-Uhlenbeck Signal. Finally in Section 4.3 we study the use of this signal during liquidation by different market participants. Note that in Sections 2 and 3 we also discussed more general signals which are not necessarily liquidity driven.

4.1 The database: NASDAQ OMX trades

The database which is used in this section is made of transactions on NASDAQ OMX exchange. This exchange used to publish the identity of the buyer and seller of each transaction until 2014. To obtain order book data, we use recordings made by Capital Fund Management (CFM) on the same exchange, which were matched with NASDAQ OMX trades thanks to the timestamp, quantity and price of each trade. On a typical month, the accuracy of such matching is more than 99.95%.

The NASDAQ OMX trades were already used for academic studies (see [36] and [28] for details). We study 13 stocks traded on NASDAQ OMX Stockholm from January 2013 to September 2013. The purpose of this section is not to conduct an extensive econometric study on this database; such work deserves a paper of its own. Our goal here is to show qualitative evidences for the existence of the order book imbalance signal and to study how market participants decisions depend on its value.

The 13 stocks which are used in this section have been selected for this research, since High Frequency Proprietary Traders took part in at least 100,000 trades on each of them during the studied period. More details on the classification of the traders to different classes are given later in this section.

| Company | Daily | Avg. | Avg. | Volatility | Min. |

|---|---|---|---|---|---|

| Name (code) | Traded | Price | BA-spread | (GK) | tick |

| Value () | |||||

| Volvo AB (VOLVb.ST) | 431.20 | 94.87 | 0.057 | 15.08% | 0.05 |

| Nordea Bank AB (NDA.ST) | 384.48 | 76.09 | 0.053 | 15.02% | 0.05 |

| Telefonaktiebolaget LM Ericsson (ERICb.ST) | 373.20 | 78.41 | 0.054 | 15.20% | 0.05 |

| Hennes & Mauritz AB (HMb.ST) | 361.66 | 232.89 | 0.112 | 11.37% | 0.10 |

| Atlas Copco AB (ATCOa.ST) | 329.94 | 175.19 | 0.110 | 16.13% | 0.10 |

| Swedbank AB (SWEDa.ST) | 313.18 | 151.97 | 0.108 | 15.29% | 0.10 |

| Sandvik AB (SAND.ST) | 296.09 | 90.88 | 0.067 | 17.01% | 0.05 |

| SKF AB (SKFb.ST) | 255.99 | 161.11 | 0.112 | 16.47% | 0.10 |

| Skandinaviska Enskilda Banken AB (SEBa.ST) | 221.23 | 66.85 | 0.053 | 15.56% | 0.05 |

| Nokia OYJ (NOKI.ST) | 209.77 | 28.84 | 0.019 | 36.89% | 0.01 |

| Telia Co AB (TLSN.ST) | 207.09 | 45.14 | 0.014 | 10.13% | 0.01 |

| ABB Ltd (ABB.ST) | 179.51 | 144.35 | 0.108 | 11.89% | 0.10 |

| AstraZeneca PLC (AZN.ST) | 168.06 | 318.57 | 0.127 | 12.09% | 0.10 |

Table 1 discloses descriptive statistics on the considered stocks in the database. Stocks are ranked by the average daily traded value (in unites of of the local currency, the Swedish krona), which can be considered as an indicator of liquidity. We also included in Table 1 the average price during the study period, since European exchanges apply dynamic tick size schedules. The lower the average stock price, the lower is the tick size (see Chapter 1, Section 3 of [27]). The Minimum tick size is the smallest tick size which was applied to the stock price during our study period. If the price changes are large enough, different tick sizes could have been applied during the study period, therefore we also added the yearly estimated Garman and Klass volatility to the table (see [20]). Last but not least the average bid-ask spread has to be compared with the tick size: for all these stocks the bid-ask spread lays between one and two ticks. All this stocks are therefore liquid and large tick stocks.

| Code | Global | HF MM | Instit. | HF Prop. | Trades | Pct. | Pct. LOB |

|---|---|---|---|---|---|---|---|

| Banks | Brokers | Count | Ident. | matched | |||

| VOLVb.ST | 56.9% | 17.1% | 10.6% | 15.3% | 927,467 | 76.7% | 97.4% |

| NDA.ST | 60.7% | 10.6% | 9.9% | 18.7% | 694,509 | 76.8% | 97.4% |

| ERICb.ST | 57.8% | 17.6% | 7.7% | 16.9% | 811,931 | 81.0% | 97.2% |

| HMb.ST | 58.5% | 16.0% | 8.9% | 16.6% | 716,644 | 76.8% | 97.8% |

| ATCOa.ST | 58.2% | 13.7% | 10.5% | 17.6% | 677,981 | 79.1% | 98.0% |

| SWEDa.ST | 61.2% | 12.2% | 9.5% | 17.2% | 600,655 | 74.6% | 97.7% |

| SAND.ST | 61.0% | 15.2% | 10.4% | 13.4% | 701,961 | 77.4% | 96.9% |

| SKFb.ST | 60.9% | 13.8% | 10.4% | 14.9% | 587,088 | 77.1% | 97.0% |

| SEBa.ST | 61.5% | 12.1% | 8.8% | 17.7% | 515,743 | 75.8% | 97.8% |

| NOKI.ST | 54.5% | 8.1% | 8.9% | 28.5% | 710,173 | 79.6% | 99.2% |

| TLSN.ST | 61.2% | 10.0% | 10.6% | 18.2% | 548,602 | 68.9% | 97.8% |

| ABB.ST | 50.1% | 15.6% | 5.2% | 29.2% | 359,067 | 86.2% | 98.1% |

| AZN.ST | 51.4% | 12.8% | 9.0% | 26.8% | 411,118 | 89.6% | 98.8% |

| Average | 58.3% | 13.6% | 9.4% | 18.7% | — | 77.7% | — |

The NASDAQ OMX database contains the identity of the buyer and the seller from the viewpoint of the exchange, that is, the members of the exchange who made the transactions. Asset managers for example, are not direct members of the exchange. On the other hand, brokers, banks and some other specific market participants are members. We classify the market members into four types (for more details see Appendix A.1):

-

•

Global investment banks (GIB);

-

•

Institutional brokers (IB);

-

•

High frequency market makers (HFMM);

-

•

High frequency proprietary traders (HFPT).

Table 2 gives some plain statistics about the number of trades on each stock of our database involving these types of participants. Keep in mind that the database covers 180 trading days. It can be read on the last line that, on average, Global investment banks are involved in 58% of the trades while High Frequency Traders are involved into 32% of them, the remaining 10% involve institutional brokers. The percentage of identified participant is on average 78%, that is, 22% of the trades took place between two participants which we are not associated with any of our four classes (GIB, IB, HFMM, HFPT). Moreover, we had to filter around 2% of the trades (see last column) because of some cases where we could not match limit orderbook records with the observed transactions.

We expect institutional brokers to execute orders for clients without taking additional risks (i.e. act as “pure agency brokers”). Such brokers often have medium size clients and local asset managers. They do not spend of lot of resources such as technology or quantitative analysts to study the microstructure and react fast to microscopic events.

Global Investment Banks can take risks at least on a fraction of their order flow. Most of them already had proprietary trading desks and high frequency trading activities in 2013 (i.e. during the recording of the data). They usually have large international clients and have the capability to react to changes in the state of the order-book.

High frequency market makers are providing liquidity on both sides of the order book. They have a very good knowledge on market microstructure. As market makers, we expect them to focus on adverse selection, and not to keep large inventories. On the other hand, high frequency proprietary traders take their own risks in order to earn money, while taking profit of their knowledge of the order book dynamics.

| Participant Class | Trade | Average | Average | Pct. |

|---|---|---|---|---|

| Type | imbalance | Number | ||

| Global Banks | Limit | -0.41 | 103,418 | 48.2% |

| Market | 0.56 | 111,082 | 51.8% | |

| HF MM | Limit | -0.31 | 30,747 | 73.0% |

| Market | 0.62 | 11,818 | 27.0% | |

| HF Prop. Traders | Limit | -0.37 | 28,763 | 47.2% |

| Market | 0.63 | 31,858 | 52.8% | |

| Instit. Brokers | Limit | -0.56 | 9,984 | 33.6% |

| Market | 0.33 | 19,505 | 66.4% |

The data in Table 3 is compatible with our prior knowledge on the different classes of traders:

-

•

HFMM trade far more with limit orders (73%), than with market orders;

-

•

IB use more market orders than limit orders;

-

•

on average, HFPT and GIB have balanced order flows.

Moreover, high frequency participants (HFMM and HFPT) both use market orders to consume liquidity on the weak size of the book (i.e. buying when the imbalance is on average 0.60 and selling when it is on average -0.60), and provide liquidity when the imbalance is less intense than -0.5. The latter observation can be compatible with HF participant contributing to stabilize the price with their limit orders.

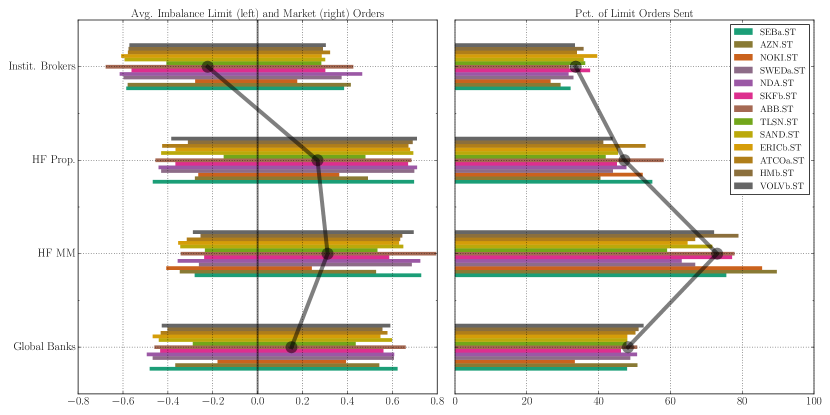

These numbers are only averages, in Figure 4 we give their dispersion across our 13 stocks. It can be seen in Figure 4 that the asymmetry between HFPT and IB is observed for all stocks (see left panel). Moreover, the left panel suggests that high frequency participants use market orders and limit orders when the imbalance is in their favour.

4.2 The Imbalance Signal

The order book imbalance has been identified as one of the main drivers of liquidity dynamics. It plays an important role in order-book models and more specifically it drives the rate of insertions and cancellations of limit orders near the mid price (see [1, 25]). As an illustration of the theoretical results of this paper, we document here the imbalance signal and its use by different types of participants. This signal is computed by using the quantity of the best bid and the best ask of the order book,

just before the occurrence of a transaction at time . Note that our 13 stocks are considered as “large tick stocks” except from Sandvik AB (SAND.ST) and Telia Co AB (TLSN.ST) for which the average bid-ask spread is greater than 1.4 times the tick size. This means that the liquidity at the best bid and ask gives a substantial information on the price pressure (see [24] for details about the role of the tick size in liquidity formation). For smaller tick stocks, several price levels need to be aggregated in order to obtain the same level of prediction for future price moves.

| d Price | Imb. 3t | Imb. 5t | Imb. 7t | Imb. 10t | Imb. 100t | ||

|---|---|---|---|---|---|---|---|

| VOLVb.ST | 0.58 | 0.16 | 0.91 | 0.72 | 0.49 | 0.26 | 0.03 |

| NDA.ST | 0.58 | 0.16 | 0.90 | 0.71 | 0.51 | 0.30 | 0.04 |

| ERICb.ST | 0.62 | 0.15 | 0.93 | 0.74 | 0.53 | 0.30 | 0.03 |

| HMb.ST | 0.59 | 0.08 | 0.84 | 0.62 | 0.41 | 0.21 | 0.02 |

| ATCOa.ST | 0.60 | 0.13 | 0.85 | 0.58 | 0.34 | 0.13 | 0.02 |

| SWEDa.ST | 0.62 | 0.14 | 0.87 | 0.67 | 0.45 | 0.23 | 0.02 |

| SAND.ST | 0.56 | 0.15 | 0.81 | 0.57 | 0.37 | 0.20 | 0.03 |

| SKFb.ST | 0.59 | 0.13 | 0.76 | 0.49 | 0.28 | 0.13 | 0.01 |

| SEBa.ST | 0.61 | 0.15 | 0.91 | 0.73 | 0.51 | 0.28 | 0.03 |

| NOKI.ST | 0.41 | 0.01 | 0.18 | 0.08 | 0.05 | 0.03 | 0.00 |

| TLSN.ST | 0.54 | 0.04 | 0.43 | 0.22 | 0.13 | 0.08 | 0.02 |

| ABB.ST | 0.59 | 0.11 | 0.86 | 0.61 | 0.33 | 0.11 | 0.03 |

| AZN.ST | 0.64 | 0.04 | 0.47 | 0.20 | 0.09 | 0.05 | 0.02 |

In order to demonstrate the predictive power of the imbalance, we consider the average mid price move after 10 trades as a function of the current imbalance (see Figure 5). Table 4 gives data which is associated to these curves. The column “d Price” shows the price change re-normalized by the average bid-ask spread on each stock after 10 trades. This price move is on average close to 0.6 times the imbalance just before the first of these trades;

Mean-reversion of the imbalance.

Figure 7 on the right shows the average value of the imbalance after and trades as a function of its current value. The colors of the curves represent the same stocks as in Figure 5. The decreasing slopes around are underlined by the last columns of Table 4. It demonstrates the mean reverting property of the imbalance. We will not comment too much on the decreasing slopes for large imbalance values. We will just mention that strong imbalance may imply on a future price change, which in turn, can create a depletion of the “weak side of the order-book” (in the sense of [18]). This phenomenon may cause an inversion of the imbalance, since the queue in second best price level of the order book, which is now “promoted” to be the first level, could be large. See [25] for details about queues dynamics in order-books.

To approximately fit Ornstein-Uhlenbeck (OU) dynamics to the imbalance data, we will use “trade time” instead of “calendar time” (i.e. seconds), in order to compensate on different frequencies of trading for each of our 13 stocks (see columns on Table 9 in the Appendix). This implies a discrete version of an OU,

where is the number of trades ahead you look at, is the speed of mean-reversion parameter and is the standard deviation of the innovation . The linear regressions on the last columns of Table 4 are following the model

Some numerical values of the model parameters.

At a time scale of 35 seconds or 7 trades, should be taken close to 0.92 and close to 0.22. We also provide an estimator for the instantaneous market impact using the empirical average of the mid-price move111The mid-price is the middle of the best bid and best ask prices. after a trade times the sign of the trade. Table 9 in the Appendix shows that the average value of divided by the average bid-ask spread is close to 0.1.

We summarise the main findings of this section:

-

(i)

the imbalance can be considered as a liquidity-driven short term signal,

-

(ii)

this signal has mean-reverting properties,

- (ii)

4.3 Use of signals by market participants

As previously mentioned, we expect HF Proprietary Traders, HF Market Makers and Global Investment Banks to pay more attention to order-book dynamics than Institutional Brokers. However, as market makers, HFMM are expected to earn money by buying and selling when the mid price does not change much (relying on the bid-ask bounce). On the other hand, HFPT are typically alternating between intensive buy and sell phases which are based on price moves.

Our expectations are met in Table 3, where the average imbalance just before a trade is shown for each type of market participant. All the trades in this table are normalized as if all orders were buy orders. The imbalance is positive when its sign is in the direction of the trade, and negative if it is in an apposite direction.

We notice the following behaviour:

-

•

when the transaction is obtained via a market order, the market participant had the opportunity to observe the imbalance before consuming liquidity.

-

•

when the transaction is obtained via a limit order, fast participants have the opportunity to cancel their orders to prevent an execution and potential adverse selection.

Table 3 underlines that HF participants and GBI make “better choices” on trading according to the market imbalance. Institutional Brokers seems to be the less “imbalance aware” when they decide to trade. This could be explained either by the fact that they invest less in microstructure research, quantitative modelling and automated trading; or either because they have less freedom to be opportunistic. Since they act as pure agency brokers, they do not have the choice to retain clients orders, and it could prevent them from waiting for the best imbalance to trade.

Strategic behaviour.

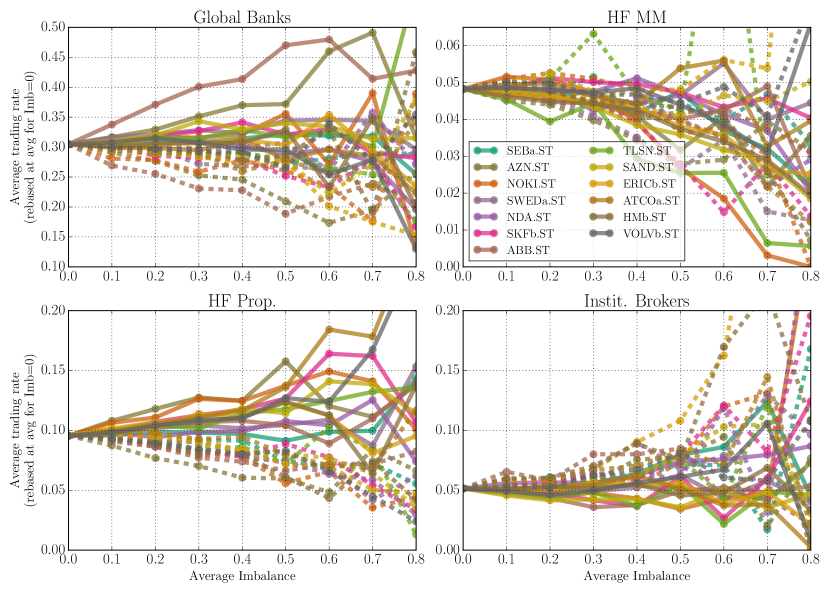

Once we suspect that some participants take into account the imbalance in their trading decisions; we can look for a relation between the trading rate and the corresponding imbalance for each type of participant. This is motivated by the optimal trading frameworks of previous sections, where we used the trading rate as a control.

In order to learn more about the relation between the imbalance signal and the trading speed, we compute the imbalance-conditioned trading rate and for each type of market participant, during all consecutive intervals of 10 minutes from January 2013 to September 2013 (within the trading hours, i.e. 9h00 to 17h30). Note that in the following analysis the signal, time and trading quantities are discrete.

Definition 4.1 (Imbalance conditioned trading quantities).

The Imbalance conditioned trading rate of market participants of type during the time interval are given by

where

-

•

is the sign of the trade at time .

-

•

is , if at time the imbalance sign times the sign of the trade is equal to , and otherwise.

-

•

is the traded amount of the trade at time .

-

•

is if the trade at time involved a participant of type , and otherwise.

-

•

is if the absolute value of the imbalance at time equals to , and otherwise.

-

•

is the of number of trades involving participant in when the imbalance is equals to .

Qualitatively, have the following interception,

-

•

is an estimate of the amount traded in the direction of the imbalance, when the absolute value of the imbalance is , by participants of type during the time interval interval ,

-

•

is an estimate of the amount traded in the opposite direction of the imbalance, when the absolute value of the imbalance is , by participants of type during interval .

In order to get the trading imbalance conditioned rates we renormalize by the traded amount during the interval given the imbalance is :

Then divided by is an estimate of the probability that a stock is traded by a participant of type during interval in the direction of the imbalance, given that the imbalance is . divided by is an estimate to the probability that a stock is traded by a participant of type during interval , in an opposite direction of the imbalance, given the imbalance is .

Let be the number of ten minutes intervals in our data base. We define

which are unbiased estimators for the probability that a participant of type trades in the direction (respectively, opposite direction) of the imbalance, given that the absolute value of the imbalance is .

To be able to put all the stocks on the same graph, we draw

in Figure 9. Here is the average of over all stocks .

Figure 9 shows the variations of (the relative speed of trading in the direction to the imbalance, in solid lines) and (the relative speed of trading in the opposite direction to the imbalance, in dashed lines) with respect to the imbalance before the trade, for each type of market participant and for each stock. From this graph we observe the following:

-

•

High Frequency Market Makers: we observe that the higher the imbalance in the orderbook, the less they trade. This effect does not seem to be related to the direction of their trades. It corresponds to an expected behaviour from market makers.

-

•

High Frequency Proprietary Traders: the higher the imbalance, the more they trade in the similar direction, and the less they trade in the opposite direction.

-

•

Institutional Brokers do not seem to be influenced by the imbalance. Additional data analysis shows that they they trade more with limit orders when the imbalance is intense, this may derive the price to move in the opposite direction.

-

•

The behaviour of Global Banks seems to be influenced by the imbalance for part of the stocks in our sample.

Towards a theory for the strategic use of signals.

The analysis in this section suggests that some market participants are using liquidity-driven signals in their trading strategies. The liquidity imbalance, computed from the best bid and ask prices of the order-book for medium and large tick stocks, appears to be a good candidate. Moreover, its dynamics exhibit mean-reverting properties.

The theory developed in Sections 2 and 3 can be regarded as a tentative framework to model the behaviour the following participants. Global investment banks who execute large orders, seem to be a typical example for participants who adopt the type of strategies that we model. HFPT who are combining slow signals (which may be considered as execution of large orders) along with fast signals, could also use our framework. We could moreover hope that thanks to the availability of such frameworks, Institutional Brokers could optimize their trading, and to increase the profits for more final investors.

5 Proofs

5.1 Proofs of Theorems 2.3, 2.4 and Corollary 2.7

The proofs of Theorems 2.3 and 2.4 use ideas from the proofs of Proposition 2.9 and Theorem 2.11 in [21].

Proof of Theorem 2.3

Since is strictly positive definite we have for any ,

| (5.2) |

is quadratic in and therefore we have

| (5.3) |

Let . We define the following cross functionals,

Note that

and

| (5.4) |

From (5.2) it follows that and together with (5.4) we get

Repeating the same steps, using (5.3) instead of (5.2) we get

Since is linear in we have

From (5.1) it follows that

Let . The claim that

follows from the continuity of , by a standard extension argument. Since is strictly convex, we get that there exists at most one minimizer to in .

∎

Proof of Theorem 2.4

First we prove that (2.7) is necessary for optimality. Let and consider the round trip

For all we have

| (5.5) |

and

| (5.6) |

Let , and recall that . Using (5.5) and (5.6) we can differentiate with respect to and get

From optimality we have and therefore we expect that

| (5.7) |

Note that

and

We get that (5.7) is equivalent to

Since and were chosen arbitrarily this implies (2.7).

Assume now that there exists satisfying (2.7), we will show that minimizes . Let be any other strategy in . Define . Then from (2.7) we have

| (5.8) | ||||

where we have used the fact that in the last equality.

Proof of Corollary 2.7

5.2 Proofs of Propositions 3.1 and 3.2

Proof of Proposition 3.1.

The proof follows the same lines as the proof of Proposition 1 in [14].

Pluggin in the ansatz we get

Optimizing over it follows that

| (5.13) |

and we get the following PDE

| (5.14) |

where .

As in equation (A.2) in [14], we have a linear and quadratic -terms in (5.14) along with a quadratic terminal condition, hence we make the following ansatz on the solution:

By comparing terms with similar powers of , we get the following system of PDEs,

| (5.15) | |||||

| (5.16) | |||||

| (5.17) |

with the terminal conditions

We first find a solution to (5.17). Note that since the terminal condition is independent of we might be able to find a independent solution, that is which satisfies

This is a Riccati equation which has the following solution (see the proof of Proposition 1 in [14]),

where

Let represent expectation conditioned on .

Proof of Proposition 3.2

Note that is a classical solution to 3.4. By standard arguments (see e.g. Theorem 3.5.2 in [32]), in order to prove that in (3.5) is the value function of (3.3), it is enough to show that is admissible and that

| (5.18) |

Clearly . From our conditions on we have

then we will have

and (5.18) follows. To prove that is admissible it is enough to show that . Since is bounded we notice that

where we used (3.2) in the last inequality. From Gronwall inequality we have

hence is admissible. ∎

Acknowledgements

We are very grateful to anonymous referees and to the editors for careful reading of the manuscript, and for a number of useful comments and suggestions that significantly improved this paper.

Index

References

- [1] F. Abergel, M. Anane, A. Chakraborti, A. Jedidi, and I. M. Toke. Limit Order Books (Physics of Society: Econophysics and Sociophysics). Cambridge University Press, 1 edition, 2016.

- [2] A Alfonsi, A. Fruth, and A. Schied. Optimal execution strategies in limit order books with general shape functions. Quant. Finance, 10:143–157, 2010.

- [3] A Alfonsi, A Schied, and A. Slynko. Order book resilience, price manipulation, and the positive portfolio problem. SIAM J. Financial Math., 3(1):511–533, 2012.

- [4] A. Almgren. Optimal trading with stochastic liquidity and volatility. SIAM J. Financial Math., 3:163–181, 2012.

- [5] R. Almgren and N. Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3(2):5–39, 2000.

- [6] R. Almgren and J. Lorenz. Adaptive arrival price. Institutional Investor Journals: Algorithmic Trading III, 2007.

- [7] E. Bacry, A. Luga, M. Lasnier, and C. A. Lehalle. Market Impacts and the Life Cycle of Investors Orders. Market Microstructure and Liquidity, 1(2), 2015.

- [8] D. Bertsimas and A. W. Lo. Optimal control of execution costs. Journal of Financial Markets, 1(1):1–50, 1998.

- [9] B. Bouchard, N. M. Dang, and C. A. Lehalle. Optimal control of trading algorithms: a general impulse control approach. SIAM J. Financial Mathematics, 2(1):404–438, 2011.

- [10] Á. Cartea and S. Jaimungal. Modelling asset prices for algorithmic and high-frequency trading. Applied Mathematical Finance, 20(6):512–547, 2013.

- [11] Á. Cartea and S. Jaimungal. Incorporating Order-Flow into Optimal Execution. S. Math Finan Econ, 10: 339, 2016.

- [12] Á. Cartea and S. Jaimungal. Optimal execution with limit and market orders. Quantitative Finance, 15(8):1279–1291, 2015.

- [13] Á. Cartea and S. Jaimungal. Risk metrics and fine tuning of high-frequency trading strategies. Mathematical Finance, 25(3):576–611, 2015.

- [14] Á. Cartea and S. Jaimungal. Incorporating order-flow into optimal execution. Mathematics and Financial Economics, 10(3):339–364, 2016.

- [15] Á. Cartea, S. Jaimungal, and J. Penalva. Algorithmic and High-Frequency Trading (Mathematics, Finance and Risk). Cambridge University Press, 1 edition, October 2015.

- [16] G. Curato, J. Gatheral, and F. Lillo. Optimal execution with non-linear transient market impact. Quantitative Finance, 17(1):41–54, 2017.

- [17] N. M. Dang. Optimal execution with transient impact. ssrn-id2183685, 2014.

- [18] Pietro Fodra and Huyên Pham. Semi Markov model for market microstructure. Applied Mathematical Finance, 22(3):261-295, 2015.

- [19] P. Forsyth, J. Kennedy, T. S. Tse, and H. Windclif. Optimal trade execution: a mean-quadratic-variation approach. Journal of Economic Dynamics and Control, 36:1971–1991, 2012.

- [20] M. B. Garman and M. J. Klass. On the estimation of security price volatility from historical data. Journal of Business, 53(1):67-78, 1980.

- [21] J. Gatheral, A. Schied, and A. Slynko. Transient linear price impact and Fredholm integral equations. Math. Finance, 22:445–474, 2012.

- [22] O. Guéant. The Financial Mathematics of Market Liquidity: From Optimal Execution to Market Making. Chapman and Hall/CRC, 2016.

- [23] O. Guéant, C. A. Lehalle, and J. Fernandez-Tapia. Optimal Portfolio Liquidation with Limit Orders. SIAM Journal on Financial Mathematics, 13(1):740–764, 2012.

- [24] W. Huang, C. A. Lehalle, and M. Rosenbaum. How to predict the consequences of a tick value change? Evidence from the Tokyo Stock Exchange pilot program, arXiv:1507.07052, 2015.

- [25] W. Huang, Charles-Albert Lehalle, and Mathieu Rosenbaum. Simulating and analyzing order book data: The queue-reactive model. Journal of the American Statistical Association, 10(509), December 2015.

- [26] I. Kharroubi and H. Pham. Optimal portfolio liquidation with execution cost and risk. SIAM Journal on Financial Mathematics, 1(1):897–931, 2010.

- [27] C. A. Lehalle, S. Laruelle, R. Burgot, S. Pelin, and M. Lasnier. Market Microstructure in Practice. World Scientific publishing, 2013.

- [28] C. A. Lehalle and O. Mounjid. Limit Order Strategic Placement with Adverse Selection Risk and the Role of Latency. Market Microstructure and Liquidity, 3(1), 2017.

- [29] A. Lipton, U. Pesavento, and M. G. Sotiropoulos. Trade arrival dynamics and quote imbalance in a limit order book, arXiv:1312.0514, 2013.

- [30] E. Neuman and A. Schied. Optimal portfolio liquidation in target zone models and catalytic superprocesses, Finance Stoch., 20: 495, 2016.

- [31] A. A. Obizhaeva and J. Wang. Optimal trading strategy and supply/demand dynamics. Journal of Financial Markets, 16(1):1 – 32, 2013.

- [32] H. Pham. Continuous-time stochastic control and optimization with financial applications, volume 61 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2009.

- [33] A. Schied. A control problem with fuel constraint and Dawson–Watanabe superprocesses. Ann. Appl. Probab., 23(6):2472–2499, 2013.

- [34] T. Sch neborn. Optimal Trade Execution for Time-Inconsistent Mean-Variance Criteria and Risk Functions. SIAM Journal on Financial Mathematics, 6(1):1044-1067, 2015.

- [35] S. T. Tse, P. A. Forsyth, J. S. Kennedy, and H. Windcliff. Comparison between the mean-variance optimal and the mean-quadratic-variation optimal trading strategies. Appl. Math. Finance, 20(5):415–449, 2013.

- [36] V. van Kervel and A. Menkveld. Do High-Frequency Traders Engage in Predatory Trading? Technical report, VU University Amsterdam., 2014.

Appendix A Tables and complementary statistics

A.1 Composition of market participants groups

High Fequency Traders

Name

NASADQ-OMX

Market

Prop.

member code(s)

Maker

Trader

All Options International B.V.

AOI

Hardcastle Trading AG

HCT

IMC Trading B.V

IMC, IMA

Yes

KCG Europe Limited

KEM, GEL

Yes

MMX Trading B.V

MMX

Nyenburgh Holding B.V.

NYE

Optiver VOF

OPV

Yes

Spire Europe Limited

SRE, SREA, SREB

Yes

SSW-Trading GmbH

IAT

WEBB Traders B.V

WEB

Wolverine Trading UK Ltd

WLV

Global Investment Banks

Name

NASADQ-OMX

member code(s)

Barclays Capital Securities Limited Plc

BRC

Citigroup Global Markets Limited

SAB

Commerzbank AG

CBK

Deutsche Bank AG

DBL

HSBC Bank plc

HBC

Merrill Lynch International

MLI

Nomura International plc

NIP

Institutional Brokers

Name

NASADQ-OMX

member code(s)

ABG Sundal Collier ASA

ABC

Citadel Securities (Europe) Limited

CDG

Erik Penser Bankaktiebolag

EPB

Jefferies International Limited

JEF

Neonet Securities AB

NEO

Remium Nordic AB

REM

Timber Hill Europe AG

TMB

A.2 Complementary Statistics

| estimates | 3 trades | 5 trades | 7 trades | 10 trades | 100 trades |

|---|---|---|---|---|---|

| VOLVb.ST | 0.97 | 0.94 | 0.93 | 0.93 | 0.99 |

| NDA.ST | 0.97 | 0.94 | 0.93 | 0.93 | 0.99 |

| ERICb.ST | 0.98 | 0.95 | 0.93 | 0.93 | 0.99 |

| HMb.ST | 0.95 | 0.92 | 0.92 | 0.92 | 0.99 |

| ATCOa.ST | 0.95 | 0.92 | 0.91 | 0.91 | 0.99 |

| SWEDa.ST | 0.96 | 0.93 | 0.92 | 0.92 | 0.99 |

| SAND.ST | 0.94 | 0.91 | 0.91 | 0.92 | 0.99 |

| SKFb.ST | 0.92 | 0.90 | 0.90 | 0.91 | 0.99 |

| SEBa.ST | 0.97 | 0.95 | 0.93 | 0.93 | 0.99 |

| NOKI.ST | 0.73 | 0.82 | 0.86 | 0.90 | 0.99 |

| TLSN.ST | 0.81 | 0.84 | 0.88 | 0.91 | 0.99 |

| ABB.ST | 0.95 | 0.92 | 0.90 | 0.91 | 0.99 |

| AZN.ST | 0.82 | 0.84 | 0.87 | 0.90 | 0.99 |

| over | (sec) | ||||||

|---|---|---|---|---|---|---|---|

| spread | 3 trades | 5 trades | 7 trades | 10 trades | 100 trades | ||

| VOLVb.ST | 0.088 | 5.30 | 0.25 | 0.23 | 0.22 | 0.19 | 0.06 |

| NDA.ST | 0.098 | 7.20 | 0.26 | 0.24 | 0.22 | 0.20 | 0.07 |

| ERICb.ST | 0.092 | 6.60 | 0.25 | 0.23 | 0.22 | 0.19 | 0.06 |

| HMb.ST | 0.095 | 6.68 | 0.27 | 0.25 | 0.22 | 0.19 | 0.06 |

| ATCOa.ST | 0.109 | 7.77 | 0.27 | 0.25 | 0.23 | 0.20 | 0.06 |

| SWEDa.ST | 0.105 | 7.73 | 0.27 | 0.25 | 0.23 | 0.20 | 0.06 |

| SAND.ST | 0.101 | 7.24 | 0.28 | 0.25 | 0.22 | 0.19 | 0.06 |

| SKFb.ST | 0.108 | 8.53 | 0.28 | 0.25 | 0.23 | 0.20 | 0.06 |

| SEBa.ST | 0.099 | 9.13 | 0.26 | 0.24 | 0.22 | 0.19 | 0.06 |

| NOKI.ST | 0.172 | 10.24 | 0.33 | 0.26 | 0.22 | 0.19 | 0.06 |

| TLSN.ST | 0.134 | 7.74 | 0.31 | 0.26 | 0.22 | 0.19 | 0.06 |

| ABB.ST | 0.113 | 15.13 | 0.28 | 0.26 | 0.24 | 0.20 | 0.07 |

| AZN.ST | 0.163 | 15.51 | 0.32 | 0.26 | 0.23 | 0.19 | 0.06 |