A comparative study of counterfactual estimators

Abstract

We provide a comparative study of several widely used off-policy estimators (Empirical Average, Basic Importance Sampling and Normalized Importance Sampling), detailing the different regimes where they are individually suboptimal. We then exhibit properties optimal estimators should possess. In the case where examples have been gathered using multiple policies, we show that fused estimators dominate basic ones but can still be improved.

1 Introduction

The Reinforcement Learning (RL) theory gathers approaches that enable autonomous agents to learn how to evolve in an unknown environment through trial-and-error feedbacks. These algorithms optimize the behavior of an agent according to rewards received through past interactions with the world ([2, 14]). Recently, RL has had success with implementing agents which learned to control a remote helicopter or play several Atari games without any prior knowledge on the environment. Very recently, it was a key block in AlphaGo, the first algorithm able to beat a human world master at Go.

To interact with its environment, an autonomous agent follows a policy dictating the action to take, accordingly to some prescribed distribution. The expected reward of a policy is then defined as

where is the set of all actions , is the expected reward associated with and is the distribution prescribed by the policy. A possible way to estimate is to sample from and collect, for each rollout , the chosen action , and the reward whose conditional expectation is . Then, noting the sequence of actions and collected rewards, we may use the classical Monte-Carlo estimator: .

However, in many settings such as robotics or industrial applications, it can be crucial to estimate the expected reward of a policy without sampling from it, as it may be too expensive (in time or money). Thus, the estimation of a new policy has to be based on data gathered with a previous policy , usually called the behavior policy in the RL community.

Offline methods were developed to use data from the behavior policy to evaluate the expected reward of a test policy (also called the target policy). This setting is known as off-policy evaluation (OPE) or counterfactual reasoning [3]. Over the years, many estimators of the performances of a test policy have been developed, amongst which Basic Importance Sampling (BIS, [5]), Normalized Importance Sampling (NIS, [10]), Empirical Average (EA, [6]) and Capped Importance Sampling (CIS, [3]).

All these estimators achieve a different tradeoff between bias and variance and the standard way to compare them is through the use of the Mean Square Error (MSE), as mentioned by [15]. However, when faced with a particular setup, there are no guidelines to choose a good estimator and one is often left with the task of trying them all. [8] provided a first comparative study of basic importance sampling with the empirical average estimator but this was not extended to other popular estimators.

We study in section 2 the differences between BIS, NIS and EA with a single policy. In particular, we show that NIS may be seen as an interpolation between BIS, which we prove to be optimal when the rewards have high variance, and EA, which we prove to be optimal when the rewards are deterministic. We also make explicit desirable properties an estimator should have to achieve low MSE.

Even though these estimators were designed assuming all the examples were collected using a single policy , they can be extended to the case where each sample has been collected using a different policy as shown in [1]. Further, in section 3, we prove that, when examples have been collected using multiple policies, FIS dominates BIS. The proof is slightly different from the one provided in [1]. We then show that FIS is the optimal unbiased estimator when the variance of the rewards is very large but that, in the low variance regime, better performing unbiased estimators exist.

Let us now introduce some notations. First of all, for simplicity we will assume that the set of actions is finite, even though our results (apart from those concerning (EA)) extend to the infinite case. Every time we select action , we observe a random reward with (unknown) expectation and variance . The objective is to estimate the expected reward of the target policy :

| (1) |

We consider we have collected where the sequence of actions , that we call the sampled path, was generated by following the behavior policy .

2 Examples collected with a single policy

In this section, we assume that all the examples were collected using the same behavior policy . Further, we will assume most of the time that all actions have been selected at least once, so that EA is well defined.

We recall the formula for the estimators we consider:

where, for EA, is the empirical average111In most implementations, when action has never been sampled, is set to 0. of the rewards of action . To exhibit the difference between these estimators, we rewrite them under the form

| (2) |

and where is the empirical average of action and is the number of times action has been sampled in . We shall compare these weights to the theoretical weights the estimator minimizing the MSE would have, which will now be computed.

2.1 Theoretical optimal weights

Since the samples are exchangeable, the dependency of the optimal weights on is only limited to , the list of all counts for a given path . We also denote the set of all possible such . Thus, we can rewrite the MSE as

As optimal weights only depend on , we can optimize independently each . Moreover, for every , is constant for all paths such that . The problem therefore becomes

These optimal weights can be computed analytically (the calculation is provided in the appendix) and are equal to

where we used the notation to simplify notations. We emphasize that these weights are only theoretical since and are unknown.

In the case of a single action, this simplifies to

| (3) |

Moreover, in that case, an unbiased estimator requires . We see that, when the variance is large, the optimal weight trades off variance for bias.

When we recover that the weights should be constant equal to one. Indeed in this case, the term appearing in the MSE is the bias term and the weights that are setting the bias to zero are constant and equal to one. These weights correspond to the empirical average weights.

When is high, we find that the optimal weight should depend on and . Intuitively, the bias should be higher when the variance of is very high. This variance depends both on the intrinsic variance of the reward and the number of times the action was taken. That is why the optimal weights depend on and .

2.2 Suboptimality of traditional counterfactual estimators

We now explore in which settings BIS, EA, NIS are suboptimal. To that extent, it is beneficial to realise where the variance of these estimators comes from. There are two sources of variance in a counterfactual estimator. The first one comes from the variance of the rewards and the second one comes from the variance of the path induced by the behavior policy. These two components can be made explicit by computing the variance of any estimator using the law of total variance (detailed in the appendix):

| (4) |

is equal to when the weights are independent of the path , as is the case with EA. is small when weights are small for the actions whose empirical average reward has high variance. However, since the latter depends on the number of times the action has been drawn, and thus on , each estimator achieves a different tradeoff between and .

2.2.1 Basic Importance Sampling

We recall that and these weights are linear in . This linear relationship is the one found in the optimal weights of Eq. 3 when the variance is much larger than . So, in the case of high variance , we expect BIS to be close to optimal. In particular, BIS has the desirable property that action sampled many times, and whose average reward is well estimated, have a higher weight in the final estimator than actions with poorly estimated average reward. In the low variance regime, dominates . Since this estimator does not take the sampled path into account to reduce , BIS is suboptimal in that low variance regime. We exhibit experiments in Figure 1 where we can observe the suboptimality of BIS when is small.

2.2.2 Empirical Average

We recall that the weights of the EA estimator are . They are equal to the optimal weights of Eq. 3 when . Indeed, if rewards are deterministic, dominates . Since the constant weights of EA induce , the EA estimator is optimal in that regime, provided each action was sampled at least once. If, however, the variance of the rewards is large, then dominates . Since it focuses on setting to 0 at the expense of a larger , EA is suboptimal in that high variance regime. Instead, we would like to downweight the actions which have been rarely sampled and upweight those which have been sampled often. Figure 1, we show experiments that prove this suboptimal behavior of EA when is large

2.2.3 Normalized Importance Sampling

We now focus our attention on NIS and show that this estimator may be seen as an interpolation between BIS and EA. First, we recall that the weights of the NIS estimator are

which can be rewritten

To simplify the analysis, we make the assumption that which is true in expectation if the behavior policy does not depend on the quality of the arms. Under this assumption,

| (5) |

is a weighted harmonic average between and . Interestingly, while we would ideally like to interpolate between BIS and EA based on the variance of the rewards, the weight of NIS depends on instead.

In Table 1, we compute the value of for different value of based on this approximation.

| 1 |

We show in Figure 1 this interpolation by plotting the MSE of the three estimators as a function of the variance of the rewards. It makes it clear that

-

i)

the empirical average estimator is optimal and normalized important sampling is better than basic importance sampling when is low,

-

ii)

basic importance sampling is better than empirical average when is high

-

iii)

NIS achieves a tradeoff between empirical average and normalized importance sampling.

We now present one experiment to show these different properties.

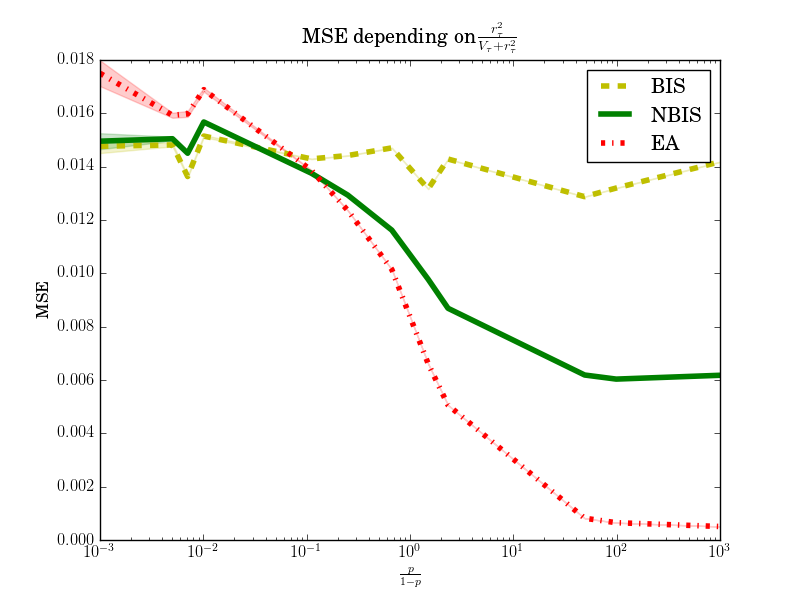

2.3 Experiment with one behavior policy

We consider an environment with actions where each action yields rewards following a scaled Bernoulli distribution, i.e., with probability and 0 otherwise, with . Indexing the actions from to , we consider a symmetric reward defined as for and for . Since and , varying from to changes the ratio .

For the sampling policy, we consider . Thus, symmetric actions have the same but the action whose index is superior to is sampled more times than the action whose index is inferior to . is a peaked distribution, choosing two actions with equal probability ( and ) and the remaining actions with equal probability .

Fig. 1 shows the MSE of the estimators as a function of . When rewards are almost deterministic (right part of each plot), we see the optimality of EA and the strong dependance of BIS on . The gap between the MSE of EA and the MSE of BIS is in the right part of the plots corresponds to . When is high, BIS and NIS achieve a lower MSE than EA since the weights of empirical average do not depend on and suffer from a high .

[\capbeside\thisfloatsetupcapbesideposition=left,center,capbesidewidth=.5]figure[\FBwidth]

3 Examples collected with multiple policies

We extend our analysis to the case where different policies have been used to collect examples. Formally, we consider a family of behavior policies such that action was sampled according to . In the same spirit of [1], we show that, in this context, BIS is dominated by another estimator called Fused Importance Sampling (FIS, [9]). We then study how both of these estimators are suboptimal. Additionally, we provide a new unbiased estimator which theoretically outperforms the FIS. Finally, we detail why, in some cases with several policies implemented, one must be careful when using the EA estimator.

3.1 BIS and FIS in the context of multiple policies

With multiple policies, importance sampling techniques can be used by considering the importance weights corresponding to the policy used to collect data. Corresponding estimators may be written

where . To distinguish from Eq. 2, we denote weights by instead of .

FIS uses another formulation for the weights, namely . FIS is usually preferred to BIS but, until now, there was no theoretical justification for this choice (the result is briefly mentioned in [13]). Lemma 1, whose proof is delayed to appendix, proves that FIS dominates BIS.

Lemma 1 (FIS dominates BIS).

Assume policies sampled each an action and received a random reward . To assess the average reward obtained using a test policy , define the two estimators, Basic Importance Sampling and Fused Importance Sampling by:

Then we have . Further, since both estimators are unbiased, dominates .

The intuition is the following. Consider a fixed action and assume that this action has been sampled several times, at stage . The overall weight put by BIS is of the order of

while the weight put by FIS would be of the order of . If one of the is really small (but not the other), then the weight put on BIS can be huge while the one of FIS would remain reasonably small. Looking at the details of the proof, the key argument when comparing the variances is how different means (Cesaro vs harmonic means) compare with each other.

3.2 The optimal unbiased estimator

Even though FIS dominates BIS, it is not optimal and we provide a new estimator with a lower MSE.

Lemma 2 (Optimal unbiased estimator).

Consider the family of estimators of the form:

where for all , it holds that . Amongst this family, the weights of the estimator that minimizes the MSE can be written as:

with and as defined in the introduction.

Proof.

As estimators must be unbiased, we only need to minimize the variance of with respect to . Since we are free to choose the weights for each action independently, we focus on minimizing the MSE computed on one action . For a given action , the estimator is the sum of N independent random variables. Focusing on the variance for one sample, we have

We can use the law of total variance and compute:

Since the unbiasedness requires , we compute the Lagrangian:

that we optimize to find . ∎

In the sequel, we call this estimator the Optimal Unbiased importance sampling estimator (OUIS). We first remark that there exists a trade-off between and . When is small, the optimal weights depend on which differ from the weights corresponding to the fused distribution, linear in . This is striking when collecting policies are peaked. However, when is high, weights matchs those of the fused distribution. We proved that the weights of the latter are the unbiased weights with no dependence on the sampled path that are minimizing . We also remark that when the rewards are deterministic, the optimal weights are equal to:

| (6) |

Here, we do not need to compute estimates of and to be able to use the weights.

3.3 Dependence of sampling policies on previous observed rewards

There exists a strong difference between EA and importance sampling based estimators when the sampling policies were dependent from rewards previously observed by the system. It is the case for instance if is dependent from the rewards gathered by sampling . This dependence can appear when the sampling policies are the intermediate steps of some policy learning algorithms.

We claim that in this case importance sampling based methods still lead to unbiased counterfactual estimators whereas the empirical average estimator can be biased. Indeed, consider a simple setting with one action whose reward is a Bernoulli of parameter 1/2. The policy stops sampling this action as soon as it experiences a 0. By doing the calculation, we can show that the expected value of EA is and its bias equals (we provide the details in the appendix).

On the other hand, important sampling based methods are unbiased even when collecting policies are dependent: this is a standard result in the adversarial bandit literature (e.g. [4]).

3.4 Experiments with multiple policies

3.4.1 Cartpole environment

To compare the performances with multiple policies, we first test them on the Cartpole222https://gym.openai.com/ environment. We consider stochastic linear policies where at each time step the cart moves right with probability where is the state of the environment and the parameter of the model. To optimize the reward of the agent, we use the PoWER algorithm [7] and consider policies that were used to collect data in the optimisation process. To test our estimators, we estimated the expected reward of the final policy reached by the optimisation algorithm with the data collected by the 10 previous implemented policies. In each experiment, we use 300 rollouts (30 rollout per policy) to compute the estimators.

We use the per-decision version of each estimatoy [11] and we we compute its RMSE by running this process 400 times. We compute confidence intervals by bootstrapping and give the value of the 5th, 50th, and 95th percentiles. For the capped estimators, we use 10 as capping parameter. We also tested the Normalized fused importance sampling estimator as defined by [12].

| RMSE (5th) | RMSE (mean) | RMSE(95th) | |

|---|---|---|---|

| BIS | 122.32 | 236.73 | 321.40 |

| BCIS | 84.65 | 87.30 | 90.24 |

| NBIS | 39.34 | 43.22 | 47.52 |

| NBCIS | 31.02 | 32.77 | 34.63 |

| FIS | 23.10 | 25.38 | 27.91 |

| OUIS | 23.13 | 25.82 | 28.77 |

| NFIS | 7.06 | 7.91 | 8.66 |

Our optimal unbiased estimator has similar performance to the Fused Importance Sampling estimator as the probability of most of the rollouts (except path of size one and 2) is tiny and . Thus, the fused weights are very close to the optimal unbiased weights .

3.4.2 Blackjack environment

We ran similar experiments in a blackjack environment. We used a policy iteration algorithm to maximize the reward of the agent. The algorithm is a Monte-Carlo policy iteration algorithm that plays epsilon-greedy according to the current Q function. As in the Cartpole example, we select several policies that were considered in the optimisation process. We run the policy iteration algorithm 5000 times and consider 10 policies corresponding respectively to the time steps multiple of 500. The task is to compute the expected reward of the final policy based on 1000 rollouts (100 per policy).

If the policies considered are similar, i.e, if for all and all , , then all the considered estimators are similar. To avoid this case, we play on the exploration rate in the policy iteration algorithm. An exploration rate that is decreasing slowly will lead to non-similar policies. We tested two different schemes to decrease the exploration rate, namely and , where is the number of iterations of the policy iteration algorithm. The policies used in the estimator must be more different in both cases and we should observe a higher difference between the fused importance sampling estimator and the optimal unbiased estimator. We have not implemented the capped estimators since the weights are not very high. The confidence intervals are computed by bootstrapping based on 2000 runs of the experiment. The results are gathered below.

| MSE with (2000 runs) | MSE with (2000 runs) | ||||||

| 5th | mean | 95th | 5th | mean | 95th | ||

| BIS | 0.1251 | 0.1255 | 0.1261 | 0.0905 | 0.0910 | 0.0915 | |

| FIS | 0.1249 | 0.1254 | 0.1258 | 0.0870 | 0.0875 | 0.0880 | |

| OUIS | 0.1250 | 0.1253 | 0.1258 | 0.0855 | 0.0860 | 0.0865 | |

| NBIS | 0.0427 | 0.0438 | 0.0450 | 0.0523 | 0.0535 | 0.0546 | |

| NFIS | 0.0347 | 0.0354 | 0.0363 | 0.0429 | 0.0441 | 0.0453 | |

| NOUIS | 0.0363 | 0.0374 | 0.0383 | 0.0458 | 0.0468 | 0.0479 | |

For the first exploration parameter, policies used to compute the estimator are similar and differenced between OUIS and FIS cannot be observed. With sufficiently different policies, significant differences between the two estimators can bd observed and OUIS has a lower MSE as expected. We also tested a normalized estimator based on the weights of OUIS but this estimator has higher MSE than NFIS. Having better weights in the unbiased case is not a guarantee to build a better normalized estimator.

4 Conclusion

Our work provides some key elements for understanding in which cases the different usual counterfactual estimators are suboptimal and why we can see normalized importance sampling as an interpolation between empirical average and basic importance sampling.

We also focused on estimators that are using data gathered by multiple policies. We proved that fused importance sampling dominates basic importance sampling and then exhibited a new estimator that dominates FIS. This estimator is the optimal unbiased estimator. However, finding a better estimator that trades off bias for variance is still an open question in the case of multiple policies.

These estimators represent a way to build data efficient off policy learning algorithms since they can reuse all data gathered in the learning process. One of our further direction of research would be to see how they reduce the number of examples that need to be sampled and if they can be improved to speed up the convergence of the different learning algorithms.

References

- [1] Aman Agarwal, Soumya Basu, Tobias Schnabel, and Thorsten Joachims. Effective evaluation using logged bandit feedback from multiple loggers. arXiv preprint arXiv:1703.06180, 2017.

- [2] Dimitri P Bertsekas and John N Tsitsiklis. Neuro-dynamic programming: an overview. In Decision and Control, 1995., Proceedings of the 34th IEEE Conference on, volume 1, pages 560–564. IEEE, 1995.

- [3] Léon Bottou, Jonas Peters, Joaquin Quinonero Candela, Denis Xavier Charles, Max Chickering, Elon Portugaly, Dipankar Ray, Patrice Y Simard, and Ed Snelson. Counterfactual reasoning and learning systems: the example of computational advertising. Journal of Machine Learning Research, 14(1):3207–3260, 2013.

- [4] Sébastien Bubeck and Nicolo Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Machine Learning, 5(1):1–122, 2012.

- [5] JM Hammersley and DC Handscomb. Monte Carlo Methods. Chapter, 1964.

- [6] Keisuke Hirano, Guido W Imbens, and Geert Ridder. Efficient estimation of average treatment effects using the estimated propensity score. Econometrica, 71(4):1161–1189, 2003.

- [7] Jens Kober and Jan R Peters. Policy search for motor primitives in robotics. In Advances in neural information processing systems, pages 849–856, 2009.

- [8] Lihong Li, Remi Munos, and Csaba Szepesvári. On minimax optimal offline policy evaluation. arXiv preprint arXiv:1409.3653, 2014.

- [9] Leonid Peshkin and Christian R Shelton. Learning from scarce experience. arXiv preprint cs/0204043, 2002.

- [10] MJD Powell and J Swann. Weighted uniform sampling?a monte carlo technique for reducing variance. IMA Journal of Applied Mathematics, 2(3):228–236, 1966.

- [11] Doina Precup. Eligibility traces for off-policy policy evaluation. Computer Science Department Faculty Publication Series, page 80, 2000.

- [12] Christian R Shelton. Policy improvement for pomdps using normalized importance sampling. In Proceedings of the Seventeenth conference on Uncertainty in artificial intelligence, pages 496–503. Morgan Kaufmann Publishers Inc., 2001.

- [13] Christian Robert Shelton. Importance sampling for reinforcement learning with multiple objectives. 2001.

- [14] Richard S Sutton and Andrew G Barto. Introduction to reinforcement learning, volume 135. MIT Press Cambridge, 1998.

- [15] Philip S Thomas and Emma Brunskill. Data-efficient off-policy policy evaluation for reinforcement learning. arXiv preprint arXiv:1604.00923, 2016.

Appendix A Proof: Law of total variance for deriving the estimators variance

We prove that when:

the variance can be written as:

with the sampled path.

Proof.

Following the law of total variance,

with:

and

∎

Appendix B Proof: Optimal weights with one collecting policy

We show how to compute the weights which minimizes:

They are equal to:

Proof.

The MSE is quadratic in :

and

We note . We have:

By summing these expressions over , we reach:

and

Then,

Thus:

∎

Appendix C Proof: FIS dominates BIS

The basic importance sampling (BIS) estimator can be written

| (7) |

where is drawn from a distribution with mean and variance . Similarly, the fused importance sampling (FIS) estimator can be written

| (8) |

We know that both estimators are unbiased so we focus on their variance. Using the law of total variance, we have that

Let us start with the second term. Given the rewards, the expectation of the estimator is to be taken over the draws. We get:

and the variance of this estimator is

| (9) |

Doing the same for FIS, we get

and the variance of this estimator is

| (10) |

We now focus on the first term of the total variance. Since both BIS and FIS are averages over , we compute the variance for each then average them.

Thus, the variance of the global estimator is

Taking the expectation over yields

Summing both terms for BIS, we get

Let us know compute the conditional variance of FIS for one sample.

Taking the expectation over yields

Summing over yields

Summing both terms for FIS, we get

We may now compute the difference of the two variances:

We prove the positivity of the first term through a lemma:

Lemma 3.

Let strictly positive numbers. Then

| (11) |

Proof.

Since both sides of the equation are strictly positive, we instead prove that the ratio of the two quantities is greater than 1.

This concludes the proof. ∎

Using and the positivity of , this proves the positivity of the first term.

To prove the negativity of the second term, we define a new random variable

where is taken uniformly at random in . The variance of is:

Since is positive, the second term of Eq. C is negative. Thus, is positive and FIS dominates BIS.

Appendix D Proof: Biasedness of EA when sampling policies depend on previous observed data

We provide a small example why EA can be biased when the sampling policies depend on previous observed data.

We consider a setting with one action whose reward is a Bernoulli of parameter 1/2. The policy stops sampling this action as soon as it experiences a 0.

We can compute analytically the expectation of the empirical average estimator.

Thus, we underestimate the true reward of the action by ln(2) - 1/2.