Cash-settled options for wholesale electricity markets

Abstract

: Wholesale electricity market designs in practice do not provide the market participants with adequate mechanisms to hedge their financial risks. Demanders and suppliers will likely face even greater risks with the deepening penetration of variable renewable resources like wind and solar. This paper explores the design of a centralized cash-settled call option market to mitigate such risks. A cash-settled call option is a financial instrument that allows its holder the right to claim a monetary reward equal to the positive difference between the real-time price of an underlying commodity and a pre-negotiated strike price for an upfront fee. Through an example, we illustrate that a bilateral call option can reduce the payment volatility of market participants. Then, we design a centralized clearing mechanism for call options that generalizes the bilateral trade. We illustrate through an example how the centralized clearing mechanism generalizes the bilateral trade. Finally, the effect of risk preference of the market participants, as well as some generalizations are discussed.

keywords:

Electricity Markets, Call Options, Mechanism Design, Stackelberg Equilibrium.1 Introduction

Various states in the U.S. and countries around the world have adopted aggressive targets for the integration of renewable energy resources. Wind and solar energy are two of the most prominent resources. The inherent variability of these resources makes it difficult to maintain the balance of demand and supply of power at all times. By variable, we mean they are uncertain (errors in day-ahead forecasts are significantly higher than those in bulk power demand), intermittent (shows large ramps over short time horizons), and non-dispatchable (output cannot be varied on command). See Bird et al. (2013) for a comprehensive discussion on the challenges of renewable integration.

Energy is typically procured in advance to meet the demand requirements. Forward planning is necessary since many generators – such as the ones based on nuclear technology or coal – cannot alter their outputs arbitrarily fast to track demand requirements; some lead time is necessary. In its simplest abstraction, one can model the system operation to proceed in two stages: a forward stage, conducted a day or a few hours in advance, and the real-time stage. Roughly, the forward stage optimizes the dispatch against a forecast of the demand and supply conditions at real-time. The impending deviation from such forecasts are then balanced in real-time. While demand forecasts even a day in advance are within 1-3% accuracy, the same forecasts in the availability of variable renewable resources can be significantly higher; they can be as high as 12%111Some promising forecasting techniques have been known to reduce the forecast error further to 6-8% over large geographical regions. For more details on the statistics, see Bird et al. (2013). Variability in supply from resources like wind and solar exposes market participants to increased financial risks. The forward market design in practice does not allow participants in the wholesale market to adequately hedge their financial risks. This paper proposes a financial instrument for the same. The deepening penetration of variable renewable supply will increase the volatility in payments to market participants and hence, increase the financial risks borne by market participants (see Wang et al. (2011); Cochran et al. (2013)). One needs to better design the financial instruments to mitigate such risks.

Electricity market participants engage in trading financial derivatives, i.e., instruments that derive their values based on the prices in the wholesale market. Traded financial derivatives in practice include electricity forwards, futures, swaps, and options. See Deng and Oren (2006); Kovacevic and Pflug (2014); Kluge (2006) and the references therein. Some are traded on an exchange and many are traded bilaterally.

In this paper, we consider how an intermediary (called the ‘market maker’) can convene a financial market for trading in cash-settled call options, and how such a financial market can reduce payment volatilities of wholesale electricity market participants. Upon buying one unit of a cash-settled call option at a negotiated option price, the buyer is entitled to receive a cash payment equal to the real-time price of a commodity (that is electricity in our case) less the negotiated strike price. In order to apply the market design to electricity markets, we adopt an economic dispatch and pricing model in Section 2 to provide us with a real-time (spot) price of electricity. Then, we use that model on a stylized example in Section 3 and illustrate that a bilateral trade in cash settled call-options between a renewable power producer and a dispatchable peaker power plant can lower their respective payment volatilities. We recognize that engaging in multiple bilateral option trades on a daily basis will likely be difficult in a practical electricity market setting, and will adversely affect the liquidity of such trades.222As such, markets for financial derivatives associated with electricity markets have been known to suffer from low liquidity. For example, see de Maere d’Aertrycke and Smeers (2013). The remedy we offer is a centralized market clearing mechanism for call options in Section 4 for its use among electricity market participants. Such a mechanism will make option trading more viable in practice and attractive to market participants. We delineate the salient features and discuss possible generalizations of our design in Section 5, and and we conclude in Section 6.

Our proposed mechanism is compatible with alternate wholesale electricity market designs, as given in Wong and Fuller (2007); Pritchard et al. (2010); Bouffard et al. (2005a, b); Bose (2015). Even with different designs, market participants can have incentives to strategize their actions in the electricity market and the option trade together.333We refer to Ledgerwood and Pfeifenberger (2013); Prete and Hogan (2014) for discussions on how market participants can strategize their actions across the electricity markets and their associated financial instruments.Such interactions can adversely affect the market outcomes. However, we relegate such considerations for future work.

1.0.1 Notation:

We let denote the set of real numbers, and (resp. ) denote the set of nonnegative (resp. positive) numbers. For , we let . We let denote the expectation of a random variable . For any set , we denote its cardinality by . For an event , we denote its probability by for a suitably defined probability measure . The indicator function for an event is given by

In any optimization problem, a decision variable at optimality is denoted by .

2 Describing the marketplace

The wholesale electricity market is comprised of consumers and producers of electricity. The consumers in this market are the load-serving entities that represent the retail customers they serve within their geographical footprint. Examples of such load-serving entities are the utility companies and retail aggregators. Bulk power generators are the producers in this market. We distinguish between two sets of generators. The first type is a dispatchable generator that can alter its output within its capabilities on command. Such generators are fuel based; e.g., they run on nuclear technology, or fossil fuels like coal or natural gas, or dispatchable renewable resources such as biomass or hydro power. The second type is a variable renewable power producer. Its available capacity of production depends on an intermittent resource like wind or solar irradiance. The system operator, denoted by , implements a centralized market mechanism that determines the production and consumption of each market participant and their compensations. It does so in a way that balances demand with supply, and the power injections across the grid induce feasible power flows over the transmission lines. Most electricity markets in the United States have a locational marginal pricing based compensation scheme. In this paper, we ignore the transmission constraints of the grid and hence, describe an electricity market with a marginal pricing scheme. Generalizing this work to the case with a network is left for future work.

2.0.1 Modeling uncertainty in supply:

To model uncertainty in supply conditions, we consider a two-period market model as follows. Let denote the ex-ante stage, prior to the uncertainty being realized. At this stage, one only has forecasts of the uncertain parameters. The uncertainty is realized at , the ex-post stage. One can identify as the day-ahead stage and as the real-time stage in electricity market operations. Let denote the probability space, describing the uncertainty. Here, is the collection of possible scenarios at (which could be uncountably infinite) 444In this paper, we use “distribution” and “measure” interchangeably, as appropriate., is a suitable -algebra over , and is a probability distribution over . We assume that all market participants know .

2.0.2 Modeling the market participants:

Let denote the aggregate inflexible demand that is accurately known a day in advance555Day-ahead demand forecasts in practice are typically quite accurate. Notwithstanding the availability of such forecasts, our work can be extended to account for demand uncertainties.. Let and denote the collection of dispatchable generators and variable renewable power producers, respectively. We model their individual capabilities as follows.

-

•

Let each dispatchable generator produce in scenario . We model its ramping capability by letting where is a generator set point that is decided ex-ante, and is the ramping limit. Let the installed capacity of generator be , and hence . Its cost of production is given by the smooth convex increasing map .

-

•

Each variable renewable power producer produces in scenario . It has no ramping limitations, but its available production capacity is random, and we have That is, denotes the random available capacity of production, and denotes the installed capacity for . Similar to a dispatchable generator, the cost of production for is given by the smooth convex increasing map .

We call a vector comprised of for each and for each a dispatch.

2.0.3 Conventional dispatch and pricing model:

The balances demand and supply of power in each scenario. It determines the dispatch and the compensations of all market participants. In the remainder of this section, we describe the so-called conventional dispatch and pricing scheme. This market mechanism serves as a useful benchmark for electricity market designs under uncertainty, e.g., in Morales et al. (2014, 2012).

We assume that the SO knows for each and for each . In practice, the cost functions are derived from supply offers from the generators. The market participants, in general, may have incentives to misrepresent their cost functions. Analyzing the effects of such strategic behavior is beyond the scope of this paper.

2.0.4 The day-ahead stage:

The SO computes a forward dispatch against a point forecast of all uncertain parameters. In particular, the SO replaces the random available capacity by a certainty surrogate for each , and computes the forward dispatch by solving

| minimize | |||||

| subject to | |||||

over , and . A popular surrogate666See Morales et al. (2012) for an alternate certainty surrogate. is given by .

The forward price is given by the optimal Lagrange multiplier of the energy balance constraint. Denoting this price by , generator is paid , while producer is paid . Aggregate consumer pays .

2.0.5 At real-time:

Scenario is realized, and the SO solves

| minimize | |||||

| subject to | |||||

over and . The real-time (or spot) price is again defined by the optimal Lagrange multiplier of the energy balance constraint, and is denoted by . Note that the optimal computed at defines the generator set-points for each generator . Generator is paid , while producer is paid . The aggregate consumer does not have any real-time payments, since there is no deviation in the demand.

The total payments to each participant is the sum of her forward and the real-time payments. Call these payments as for each and for each in scenario .

We remark that the conventional dispatch model generally defines a suboptimal forward dispatch in the sense that the generator set-points are not optimized to minimize the expected aggregate costs of production. Several authors have advocated a so-called stochastic economic dispatch model, wherein the forward set-points are optimized against the expected real-time cost of balancing. See Wong and Fuller (2007); Pritchard et al. (2010); Bouffard et al. (2005a, b); Bose (2015). Our financial market is designed to work in parallel to any electricity market. Different designs of the latter can be accommodated. We adopt the conventional model to make our discussion and examples concrete.

3 An example with bilateral cash-settled call option

In this section, we study a simple power system example and illustrate that a bilateral cash-settled call option can reduce the variance of the payments and even mitigate the risks of negative payments or financial losses to market participants. This example will motivate our study of a centralized call option market in the next section.

Consider an example power system (adopted from Bose (2015)) with two dispatchable generators and a single variable renewable power producer: , where is a base-load generator, is a peaker power plant, and is a wind power producer.

Let Therefore, and have infinite generation capacities. cannot alter its output in real-time from its forward set-point, and has no ramping limitations. Suppose and both have linear costs of production. has a unit marginal cost, while has a marginal cost of . Let , i.e., is more expensive than .

To model the uncertainty in available wind, we let

and take to be the uniform distribution over . One can verify that and define the mean and the variance of the distribution, respectively. Then, the available wind capacity in scenario is encoded as . Further, assume that produces power at zero cost, and that .

This stylized example is a caricature of electricity markets with deepening penetration of variable renewable supply. Base-load generators, specifically those based on nuclear technology, have limited ramping capabilities. Peaker power plants based on internal combustion engines can quickly ramp up their power outputs. Utilizing them to balance variability, however, is costly. Finally, demand is largely inflexible and can be predicted with high accuracy.

In what follows, we analyze the effect of a bilateral call option on this market example. Insights from this example will prove useful in the balance of the paper.

3.0.1 Conventional dispatch and pricing for the example power system:

The conventional dispatch model yields the following forward dispatch and forward price.

In scenario , the real-time dispatch is given by

and the real-time price is given by

| (1) |

where denotes the indicator function. The dispatch and the prices yield the following payments in scenario :

Next, we consider a bilateral cash-settled option between and . We will show that such an option can reduce the volatility of the payments to and . Also of interest is ’s payment, when and the realized available wind is in , where

| (2) |

For such a scenario , we have . That is, incurs a loss for each . As we will illustrate, can avoid incurring such a loss in a subset of the scenarios by trading in an option with .

3.1 Bilateral cash-settled call option between and

Suppose buys cash-settled call options from . One unit of such an option entitles to a claim of a cash payment of the difference between the real-time price and a pre-negotiated strike price from . We will discuss how such an option reduces their volatility of payments.

We model the bilateral option trade between and as a robust Stackelberg game (see Başar and Olsder (1999)) as follows. Right after the day ahead market is settled at , announces an option price and a strike price for the call option it sells. Then, responds by purchasing options.777For simplicity, we allow the possibility of a fractional number of options being bought. This option entitles to a cash payment of from in scenario . The option costs a fee of . Assume that there is an exogenously defined cap of on the amount of option can buy from . The cap equals the maximum loss that can incur from the electricity market in real-time.

Then, the total payments to and in scenario are given by

| (3) | ||||

| (4) |

respectively, when they agree on the triple . Assume that is risk-neutral and has the correct conjectures on the real-time prices. Then, the perceived payoff for in the day-ahead stage is given by . If believes in a different price distribution, the perceived payoff for can be modified accordingly. Moreover, if is risk-averse, one can replace with a suitable risk-functional. Similar considerations extend to the perceived payoff for .

The possible outcomes of the option trade are identified as the set of Stackelberg equilibria (SE) of . Precisely, we say constitutes a Stackelberg equilibrium of , if

where is the best response of to the prices announced by . For a given , the best response satisfies

for all . In the following result, we characterize all Stackelberg equilibria of . In presenting the result, we make use of the notation to denote the variance of a real valued map .

Proposition 1

The Stackelberg equilibria of are given by , where

Moreover, for any , the variances of the payments satisfy

for each .

Proof of this Proposition can be found in Appendix A.

We remark that it can be verified that volatility in payments -measured in terms of the respective variance- will decrease for any nontrivial SE. However, our choice of reveals the main insights without loss of generality. describes the degenerate case, where and essentially do not participate in the option market.

Proposition 1 implies that whenever a trade occurs. Thus, for a given option price, the reduction in variance increases as decreases. Said differently, both participants gain more in terms of reduction in volatility as the peaker plant becomes more costly, leading to the possibility of price spikes in the real-time electricity market. Further, the mentioned reduction in variance increases with . Again, the participants stand to gain more (in terms of volatility in payments) from the option trade as the available wind becomes more uncertain.

Finally, consider the collection of scenarios where suffers a financial loss in the energy market, i.e., . Recall that this happens when and as defined in (2). When and participate in the bilateral option trade, then suffers a loss only when , where

| (5) |

Note that is a strict subset of . Thus, is less exposed to negative payments with the option trade.

3.1.1 Limitations of bilateral trading:

Our stylized example reveals the benefits of a bilateral trade in call options. In a wholesale market with and describing the set of dispatchable and variable generators, respectively, one can conceive of bilateral trade agreements. It is difficult to convene and settle such a large number of trades on a regular basis. To circumvent this difficulty, we propose a central clearing mechanism for cash-settled call options among the market participants.

4 Centralized market clearing for cash-settled call options

Consider an intermediary who acts as an aggregate buyer of such options for a collection of option sellers, and acts as a seller of such options for a collection of option buyers. Call this intermediary a market maker, denoted by . An established financial institution or even the can fulfill the role of such a market maker. Let be the set of buyers and be the set of sellers of the call options. The option market proceeds as follows.

4.0.1 Day-ahead stage:

-

•

broadcasts a set of allowable trades , given by

to all the market participants .

-

•

Each submits an acceptable set of option trades, denoted by .888One can fix a parametric description, where market participants communicate their choices of parameters.

-

•

correctly conjectures the real-time prices in each scenario , and solves the following stochastic optimization problem to clear the option market.

(6) over , -measurable maps for each , and for each . The function is a real-valued -measurable map over all the optimization variables.

-

•

Buyer pays to .

-

•

pays to seller .

-

•

is left with a day-ahead merchandising surplus of

4.0.2 Real-time stage:

-

•

Scenario is realized, and the real-time price of electricity is computed by .

-

•

pays to buyer .

-

•

Seller pays to .

-

•

is left with a real-time merchandising surplus of

4.0.3 Explaining the market clearing procedure:

The volume of call options bought by the renewable power producers are deemed to equal the volume sold by the dispatchable generators at the forward stage. The option prices and the volumes are decided in a way that each triple lies in the set of acceptable trades for each participant . In real-time, if the price exceeds the strike price for a renewable power producer, it will exercise its right to receive the cash amount . The total volume of encashed call options equals the sum of over the set of buyers for whom the spot price exceeds their strike price. allocates this volume among the option sellers. That is, it decides for each seller in a way that the volume of call options encashed equals the total volume allocated to the sellers.

4.0.4 How market participant decides :

Consider a seller who expects a revenue in scenario . By participating in the energy market and the option trade with the triple , she receives a payoff of

if allocates in scenario . Having no control over , assume that seller regards as adversary. That is, she conjectures that chooses in a way that minimizes ’s payoff in scenario :

Then, a risk-neutral market participant will accept the trade defined by , if

That is, is comprised of the trades that satisfy the above inequality. Similarly, for a risk-neutral buyer is comprised of the trades defined by that satisfy where

If a market participant is risk-averse, one can replace the expectation with an appropriate risk-functional; see Section 5 for more details.

4.0.5 The objective function :

The function appearing in (6) depends on the nature of the market maker. As an example, consider to be a risk-neutral profit-maximizer. Then, is the merchandising surplus for in scenario , given by

4.1 Example power system with centralized option market

Recall that we presented a bilateral trade of a call option between the wind power producer and a peaker power plant in the example in Section 3. We now reconsider the same example and demonstrate how the centralized clearing mechanism generalizes the bilateral trade.

Let be the only option buyer and be the only option seller. decides , the set of acceptable option prices, strike prices, and trade volumes. For illustrative purposes and to avoid trivial trades in our discussion, consider

We assume that caps the trade volume to equal the maximum energy shortfall in available wind from its forward contract . Assuming the players to be risk-neutral, the set of acceptable trades for and are given by

| (7) | |||

| (8) |

Assuming to be risk-neutral, she solves (at day-ahead)

| (9) |

We characterize the optimal solutions of (9) in the following result, whose proof can be found in Appendix A.

Proposition 4

The triple given by

for each , constitutes the optimal solution of (9). Moreover, at , the variances of the total payments satisfy

We note that volatility in payments for and always decrease, for any other optimal and . However, we restrict our attention to for illustrative purposes. Proposition 2 reveals that the centralized option market allows both and to reduce their payment volatilities. This reduction closely resembles the one in Proposition 1. The exact value of reduction, however, depends on the strike prices that chooses. The merchandising surplus of in scenario is given by

The above expression implies that the expected merchandising surplus of the market maker remains zero, irrespective of the choice of and . A risk-neutral market maker is agnostic to that choice, which however affects the volatilities of the market participants differently. The choice yields the outcome for the bilateral trade, in which case the market maker only facilitates passing the payments from one player to another in each scenario . We note that such a choice will be appropriate, if is motivated by a social goal, e.g., when is the .999By setting to zero for all scenarios, the optimization problem (9) can be reformulated into a system of nonlinear equations, which can be solved by the widely used Newton-Raphson’s method, and it can be verified that it converges to . Our discussion serves to illustrate that the bilateral trade is a special case of the centralized clearing mechanism.

Consider the case where another generator joins the market, a peaker plant that has a linear cost of production with a marginal cost higher than that of . Again, suppose has an infinite capacity of production. It can be verified that will never be dispatched, and hence, does not get paid from the electricity market. can still participate in the options trade, wherein she fulfills the role of a seller. then allocates the option demand from between and . One can show that the profits and losses from the options trade in various scenarios will then be shared between and . While the option trade will still reduce the volatility of the payments for , the absolute reduction in volatility will be lower. The payments to , however, remain unaffected by the presence of .

5 Generalizations

Recall that we described the set of acceptable trades for each by assuming each market participant to be risk-neutral in Section 4. A trade, identified by the triple , is deemed acceptable, if the expected payment from participation in the option trade together with the electricity market improves upon the expected payment from the electricity market alone. Market participants in electricity markets are known to be risk-averse in practice; e.g., see Bjorgan et al. (1999); Deng and Oren (2006). Here, we model such risk-aversion and demonstrate its effect on the sets of acceptable trades.

Assume that a risk-averse market participant finds a trade triple acceptable, if

| (10) |

where

is a real-valued -measurable map, and is a parameter that quantifies the extent of risk-aversion. is the popular conditional value at risk functional that describes a coherent risk measure; see FÖllmer and Schied (2010) for a survey. If is the monetary loss in scenario , equals the expected loss over the scenarios that result in the highest losses.

Consider the set of acceptable trades described by (10) for market participant , when her parameter for risk-aversion is . To make its dependence on explicit, call this set . The risk-neutral case is modeled as . The closer is to , the more risk-averse is. Notice that the set depends on the payments from the option trade alone. When , the set also depends on the payments from the electricity market.

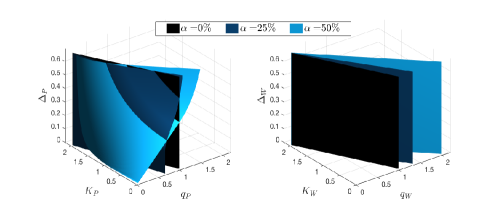

Recall that we characterized in (8) when is risk-neutral. To study the effect of risk-aversion, we plot the boundary of for various values of . In these plots, we let the cap on be to better illustrate the sets in Figure 2 (acceptable trades are on the left of the boundary). The larger the is, the larger is the set of acceptable trades. Intuitively, a more risk-averse will accept higher option/strike prices to mitigate the real-time financial risks. In a sense, puts more weight on monetary losses as grows. For this example, we have

The boundary of is portrayed in Figure 2, and the acceptable set is on the right of the boundary. The changes in the sets and with are qualitatively different. The difference stems from the fact that is exposed to negative payments while is not. In a sense, more risk aversion makes more prone to purchase the options, while becomes less likely to sell more options.

5.0.1 Effect of incorrect price/payment conjectures:

If a market participant, say , has an incorrect price conjecture, denoted by , then her set of acceptable trades can be different from . While we assumed in our examples that participants have correct price conjectures, our model can be generalized to the case where a seller or a buyer bids an incorrect set. Furthermore, even if has the correct conjecture, she might have an incentive to misrepresent her acceptability set. Such considerations are beyond the scope of this paper and can be investigated in future work.

6 Conclusions

This paper has explored the design of a centralized cash-settled options market that can be implemented in parallel with an existing electricity market. Through stylized examples, we have demonstrated that our design leads to reduction in the volatility in payments. Additionally, we have shown that a renewable supplier is less exposed to negative payments under uncertainty, compared to a conventional approach. The paper serves as a stepping stone for a more comprehensive market with deep integration of renewable supply. An attractive feature of the proposed design is that it can be applied to any existing electricity market, making its implementation less complex. Generalizations include: effect of risk-aversion, effect of price conjectures, computational aspects, and multi-period considerations.

Appendix A Proofs of Propositions

A.1 Proof of Proposition 1

With a slight abuse of notation, we sometimes use for . Suppose chooses the pair . Then, the payoff of from the option trade alone is given by

Utilizing the relation in (3), we have

| (11) |

We characterize the best response of to the choice of by . Call it the set-valued map . If , then . Otherwise,

-

•

If , then .

-

•

If , then is agnostic to the choice of , and hence, .

-

•

If , then .

Similarly, define as the payoff of from the option trade. Then, (3) and (4) imply that

| (12) |

Given the best response of , we have the following cases.

-

•

If , then , and hence no trades will occur and must choose such that .

-

•

If , then , and with , this is the only case at which nontrivial trades occur.

-

•

If , and with , trivial trades occur.

Thus, the Stackelberg equilibria of are given by , where

For any Stackelberg equilibrium , we have , if . Otherwise, . The differences in variances are given by

where . Using the fact that , it can be verified upon substitutions that

For , we have and the statement of the Proposition can be easily verified.

A.2 Proof of Proposition 2

References

- Başar and Olsder (1999) Başar, T. and Olsder, G.J. (1999). Dynamic Noncooperative Game Theory. SIAM.

- Bird et al. (2013) Bird, L., Milligan, M., and Lew, D. (2013). Integrating variable renewable energy: Challenges and solutions. Technical report, National Renewable Energy Laboratory.

- Bjorgan et al. (1999) Bjorgan, R., Liu, C.C., and Lawarree, J. (1999). Financial risk management in a competitive electricity market. IEEE Trans. Power Systems, 14(4), 1285–1291.

- Bose (2015) Bose, S. (2015). On the design of wholesale electricity markets under uncertainty. Proc. Fifty-third Annual Allerton Conference Allerton House, UIUC, Illinois, USA.

- Bouffard et al. (2005a) Bouffard, F., Galiana, F.D., and Conejo, A.J. (2005a). Market-clearing with stochastic security-part I: formulation. IEEE Trans. Power Systems, 20(4), 1818–1826.

- Bouffard et al. (2005b) Bouffard, F., Galiana, F.D., and Conejo, A.J. (2005b). Market-clearing with stochastic security-part II: case studies. IEEE Trans. Power Systems, 20(4), 1827–1835.

- Cochran et al. (2013) Cochran, J., Miller, M., Milligan, M., Ela, E., et al. (2013). Market evolution: Wholesale electricity market design for 21st century power systems. Technical report, National Renewable Energy Laboratory.

- de Maere d’Aertrycke and Smeers (2013) de Maere d’Aertrycke, G. and Smeers, Y. (2013). Liquidity risks on power exchanges: a generalized Nash equilibrium model. Mathematical Program, Series B.

- Deng and Oren (2006) Deng, S. and Oren, S.S. (2006). Electricity derivatives and risk management. Energy, 31.

- FÖllmer and Schied (2010) FÖllmer, H. and Schied, A. (2010). Convex and coherent risk measures. Encyclopedia of Quantitative Finance, 1200–1204.

- Hong and Liu (2011) Hong, L.J. and Liu, G. (2011). Monte Carlo estimation of value-at-risk, conditional value-at-risk and their sensitivities. Proc. of the 2011 Winter Simulation Conference.

- Kluge (2006) Kluge, T. (2006). Pricing swing options and other electricity derivatives. Ph.D. thesis, University of Oxford.

- Kovacevic and Pflug (2014) Kovacevic, R.M. and Pflug, G.C. (2014). Electricity swing option pricing by stochastic bilevel optimization: a survey and new approaches. European J. of Operational Research.

- Ledgerwood and Pfeifenberger (2013) Ledgerwood, S.D. and Pfeifenberger, J.P. (2013). Using virtual bids to manipulate the value of financial transmission rights. The Electricity J., 26(9).

- Morales et al. (2012) Morales, J.M., Conejo, A.J., Liu, K., and Zhong, J. (2012). Pricing electricity in pools with wind producers. IEEE Trans. Power Systems, 27(3), 1366–1376.

- Morales et al. (2014) Morales, J.M., Zugno, M., Pineda, S., and Pinson, P. (2014). Electricity market clearing with improved scheduling of stochastic production,. European J. of Operational Research, 235(3), 765–774.

- Prete and Hogan (2014) Prete, C.L. and Hogan, W.W. (2014). Manipulation of day-ahead electricity prices through virtual bidding in the U.S. International Association for Energy Economics 37th International Conference.

- Pritchard et al. (2010) Pritchard, G., Zakeri, G., and Philpott, A. (2010). A single-settlement, energy-only electric power market for unpredictable and intermittent participants. Operations Research, 58.

- Wang et al. (2011) Wang, G., Kowli, A., Negrete-Pincetic, M., Shafieepoorfard, E., and Meyn, S. (2011). A control theorist’s perspective on dynamic competitive equilibria in electricity markets. Proc. 18th World Congress of the International Federation of Automatic Control (IFAC).

- Wong and Fuller (2007) Wong, S. and Fuller, J.D. (2007). Pricing energy and reserves using stochastic optimization in an alternative electricity market. IEEE Trans. Power Systems, 22(2), 631–638.